Pet Diabetes Care Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.38 Billion |

| Market Size (2031) | USD 3.17 Billion |

| Growth Rate (2026 - 2031) | 5.85% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

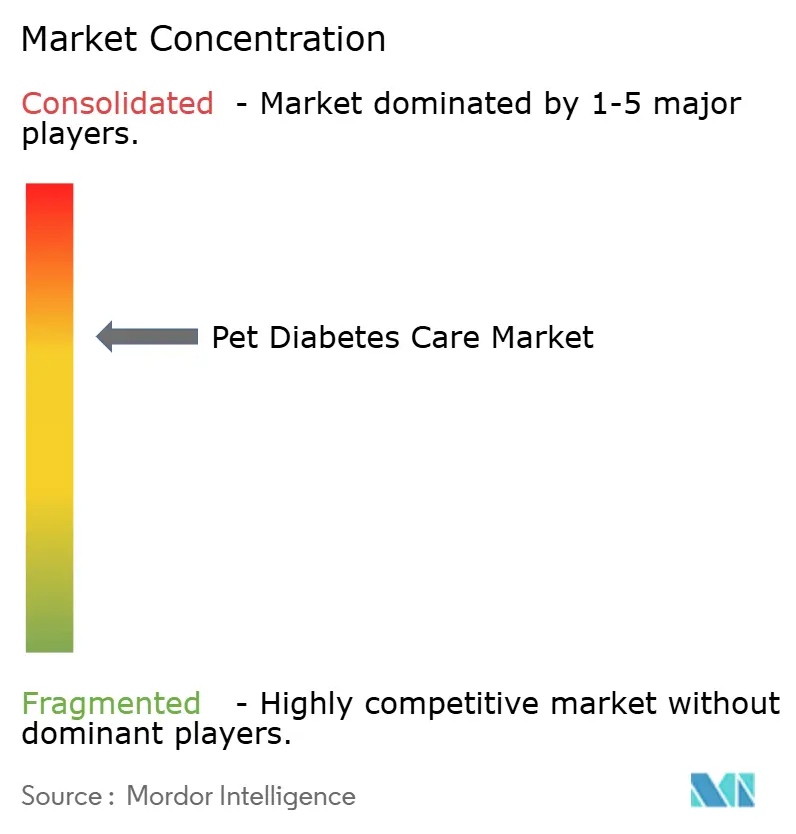

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pet Diabetes Care Market Analysis by Mordor Intelligence

Pet Diabetes Care Market size in 2026 is estimated at USD 2.38 billion, growing from 2025 value of USD 2.25 billion with 2031 projections showing USD 3.17 billion, growing at 5.85% CAGR over 2026-2031. Continued growth in the pet diabetes care market stems from the convergence of rising disease prevalence, the first-in-class oral SGLT-2 inhibitors for cats, and steady uptake of continuous glucose monitoring (CGM) devices. Increasing pet obesity, estimated at 22-40% in dogs and 19-52% in cats, enlarges the addressable base for the pet diabetes care market. At the same time, humanization of companion animals is lifting veterinary expenditure; U.S. households alone spend more than USD 136 billion per year on overall pet care, placing diabetes management firmly within discretionary budgets. Competitive intensity is moderate: three multinational leaders—Boehringer Ingelheim, Merck Animal Health, and Zoetis—dominate product innovation while smaller device specialists enter through CGM and tele-health niches.

Key Report Takeaways

- By care type, insulin therapy led with 58.12% of the pet diabetes care market share in 2025, whereas oral medications are projected to expand at a 6.65% CAGR through 2031.

- By animal type, canine treatments accounted for 64.30% of the pet diabetes care market size in 2025, while the feline segment is advancing at a 7.35% CAGR to 2031.

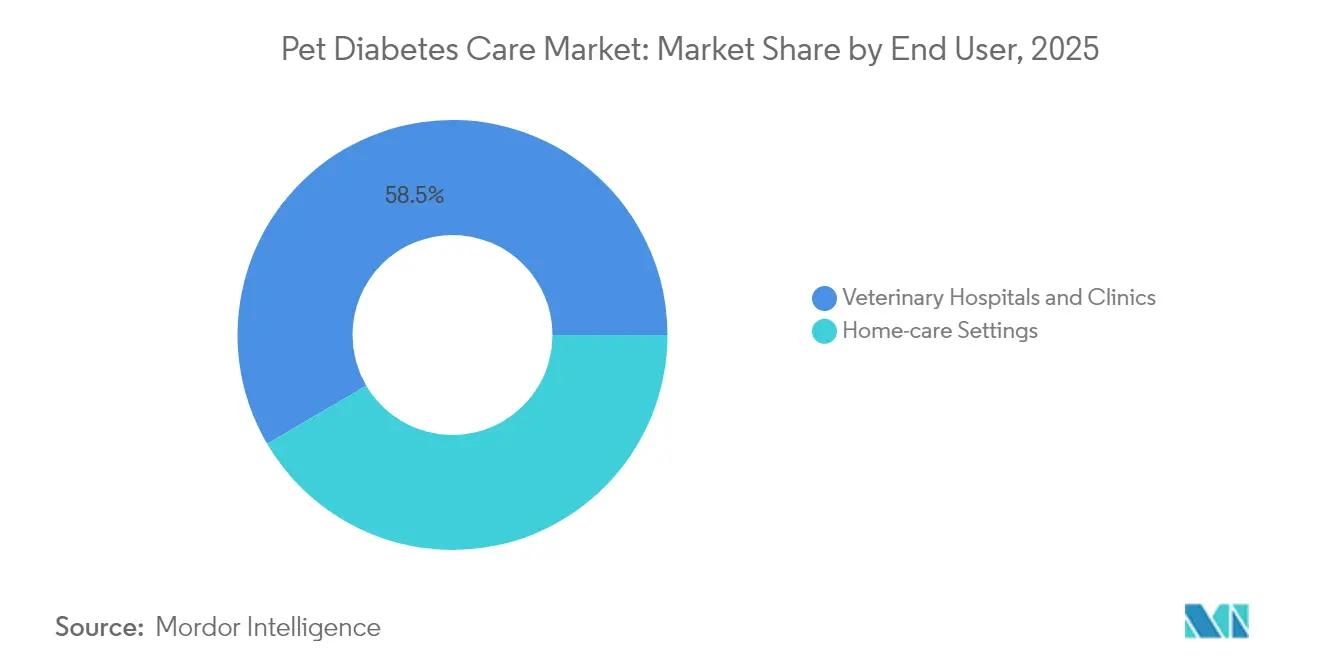

- By end user, veterinary hospitals and clinics captured 58.45% of demand in 2025; home-care settings represent the fastest-growing channel with a 7.42% CAGR through 2031.

- By distribution channel, veterinary pharmacies maintained 66.41% share in 2025, yet online retailers are forecast to post the strongest growth at a 7.55% CAGR to 2031.

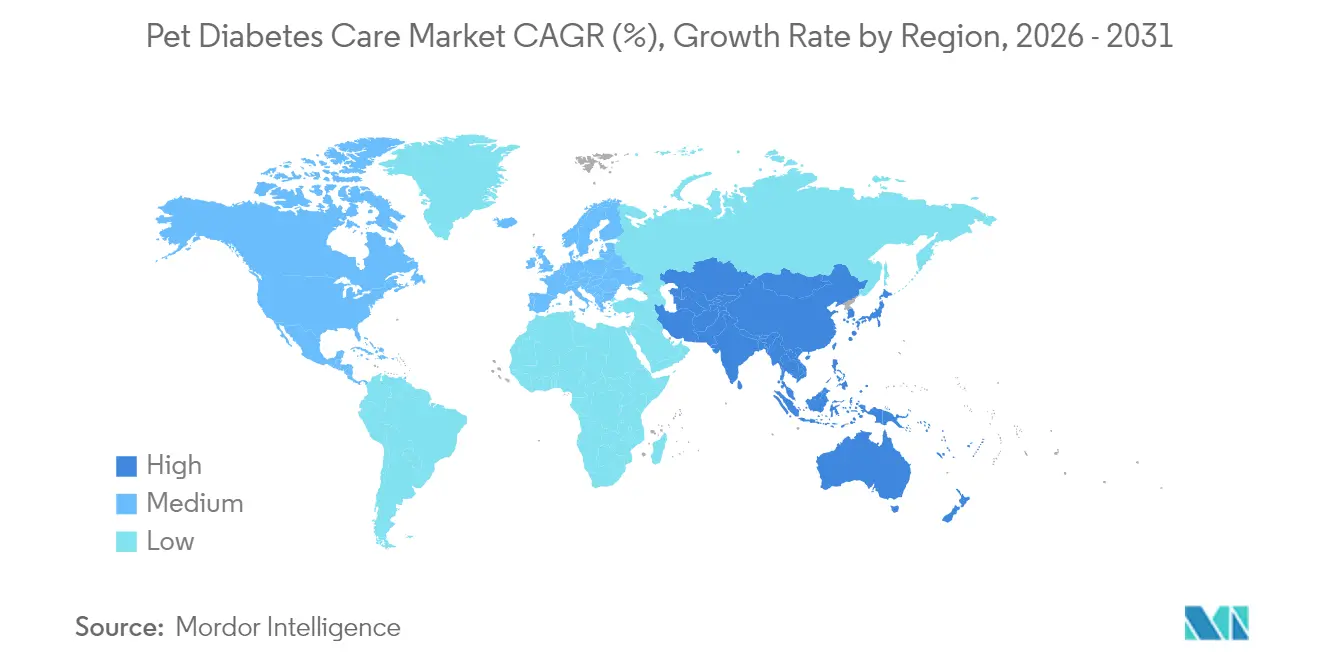

- By region, North America held 38.71% of 2025 revenue, whereas Asia-Pacific is poised to register the highest 7.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pet Diabetes Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Diabetes & Pet Obesity | +1.8% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Increase in Pet Adoption & "Pet-Parent" Spending | +1.2% | Global, led by North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Advances in Veterinary Diagnostics & CGM Technology | +1.0% | North America & Europe core, spill-over to Asia-Pacific | Medium term (2-4 years) |

| AI-Powered Tele-Vet Glucose Analytics Platforms | +0.8% | North America & Europe, early adoption in urban Asia-Pacific | Long term (≥ 4 years) |

| FDA Approvals of Novel Oral SGLT-2 Inhibitors For Cats | +0.7% | North America, expanding to Europe and Asia-Pacific | Short term (≤ 2 years) |

| Growing Insurer & VC Focus on Chronic Pet Disease Mgmt. | +0.5% | North America & Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Diabetes & Pet Obesity

Obesity-driven metabolic dysfunction now affects as many as 52% of domestic cats, creating fertile ground for the pet diabetes care market. Recorded canine diabetes incidence has climbed 79.7% since 2006, translating to roughly 165,000 dogs under active treatment in the United States.[1]Source: Frontiers in Immunology, “Canine Diabetes Mellitus Demonstrates Multiple Markers of Chronic Inflammation,” frontiersin.org Excess adiposity induces insulin resistance in both species, and the pathophysiology mirrors type 2 human diabetes, further validating pharmacologic crossover strategies. In affluent economies, lower activity levels and calorie-dense “human-grade” diets exacerbate the condition. An ageing pet population adds momentum because metabolic flexibility diminishes with age, thereby prolonging treatment duration and lifting the lifetime value of each diabetic pet to the pet diabetes care market.

Increase in Pet Adoption & “Pet-Parent” Spending

Post-pandemic social dynamics have redefined companion care budgets, with Millennials and Gen Z now representing more than 60% of new pet owners in the United States. A similar shift is visible in Asia-Pacific, where ownership rates reach 70-80% in India, Thailand, Indonesia, and China. Younger owners favour technology-enabled services and direct-to-consumer delivery, accelerating CGM and tele-vet adoption. The pet diabetes care market benefits because these demographics are more willing to finance chronic care, including wearable monitors, subscription insulin shipments, and personalized nutrition plans.

Advances in Veterinary Diagnostics & CGM Technology

CGM platforms such as FreeStyle Libre report 93-99% accuracy across glycaemic states in dogs and cats, making them clinically viable replacements for point-in-time glucometer readings. Purpose-built solutions, notably GluCurve Pet CGM, now integrate automated insulin-dosing suggestions and cloud dashboards. Zoetis’ AlphaTrak 3 further enhances at-home monitoring with streamlined app connectivity. These tools lower clinic visit frequency and improve time-in-range metrics, directly boosting therapeutic outcomes and reinforcing owner adherence—key success factors for the pet diabetes care market.

FDA Approvals of Novel Oral SGLT-2 Inhibitors for Cats

Bexacat and the follow-on Senvelgo offer the first needle-free solutions for newly diagnosed feline diabetes, achieving 88.4% clinical success within 30 days. By targeting renal glucose reabsorption, both agents avert hypoglycaemia risk while simplifying administration. Reduced injection anxiety improves owner compliance, historically a weak link for feline treatment, and thereby expands the treated population available to the pet diabetes care market. Ongoing post-marketing surveillance in Europe and Japan indicates early safety parity with standard insulin regimens.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Insulin & Monitoring Supplies | -1.5% | Global, most pronounced in emerging markets | Long term (≥ 4 years) |

| Adverse Reactions to Insulin/Oral Agents | -0.8% | Global, regulatory scrutiny highest in North America & Europe | Medium term (2-4 years) |

| Supply-Chain Risks for Animal-Sourced Insulin | -0.6% | Global, critical impact in North America & Europe | Short term (≤ 2 years) |

| Data-Privacy Barriers to CGM Cloud Integration | -0.4% | Europe & North America, emerging in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Insulin & Monitoring Supplies

Diabetes management runs USD 120 – 386 per month, escalating annual outlays beyond USD 6,600 for complex cases.[2]Source: Spot Pet Insurance, “Quarterly Report 2024 Q1,” spotpet.com Insurance rarely covers pre-existing conditions, so most owners self-fund medication, syringes, CGM sensors, and lab checks. In lower-income economies, these costs suppress diagnosis rates and lengthen untreated disease duration. Even in mature markets, price sensitivity motivates the shift toward online pharmacies and subscription discounts, reshaping channel dynamics within the pet diabetes care market.

Supply-Chain Risks for Animal-Sourced Insulin

Historical supply chain disruptions have demonstrated the vulnerability of animal-sourced insulin availability. Health Canada’s decision to end Hypurin Pork production with remaining inventory expiring by 2026 magnifies exposure in the Canadian segment. FDA watchlists continue to flag potential insulin and device shortages, and any disruption can trigger glycaemic instability in thousands of animals. Diversification into recombinant or synthetic formulations therefore remains a strategic necessity for the pet diabetes care market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: Oral Medications Disrupt Insulin Dominance

Insulin therapy held 58.12% of the pet diabetes care market share in 2025, reflecting its entrenched status as first-line therapy. Oral drugs—chiefly the SGLT-2 class—are forecast to outpace at a 6.65% CAGR as newly diagnosed felines migrate away from injections. This shift, coupled with real-time glucose metrics, raises owner satisfaction and broadens uptake.

The pet diabetes care market size for oral medications is projected to grow in the coming years, buoyed by 88.4% response rates recorded in pivotal trials. Insulin delivery innovation continues through devices such as VetPen, yet CGM systems like GluCurve now anchor data-driven dose optimization. Collectively, these innovations introduce pluralistic treatment pathways that reduce reliance on a single modality and stabilize growth in the broader pet diabetes care market.

By Animal Type: Feline Segment Accelerates Growth

Canines constituted 64.30% of total therapy revenue in 2025 as higher disease prevalence and larger body mass translate to greater insulin volume use. The pet diabetes care market size for feline therapy nonetheless is climbing more quickly, reflecting a forecast 7.35% CAGR through 2031 on the back of oral therapy convenience.

Commercial availability of Bexacat and Senvelgo positions cats for meaningful share gains, and remission prospects in diet-controlled cases further elevate owner motivation. Parallel increases in CGM acceptance—for example, FreeStyle Libre 3 correlations of r = 0.86 under stable glycaemia—make at-home monitoring feasible even for smaller animals. These dynamics collectively expand the treated feline cohort within the pet diabetes care market.

By End User: Home-Care Settings Gain Momentum

Veterinary hospitals and clinics accounted for 58.45% of 2025 demand, owing to diagnostic equipment concentration and professional oversight. Yet growth favours home-care environments, supported by CGM, mobile apps, and tele-consults, propelling a 7.42% CAGR to 2031. The COVID-19 pandemic accelerated the adoption of telemedicine and remote monitoring solutions, creating new care delivery models that persist beyond the pandemic period.

The pet diabetes care market size that flows through home settings benefits from reduced stress, real-time alerts, and lower per-visit costs. Veterinary practices are responding by offering subscription coaching and virtual check-ins, transforming service models into hybrid ecosystems. Telemedicine platforms are integrating with monitoring devices to provide real-time veterinary support for home-based diabetes care, creating hybrid care models that combine clinical expertise with convenient home monitoring.

By Distribution Channel: Online Retailers Challenge Traditional Channels

Veterinary pharmacies retained 66.41% share in 2025 due to prescription control and veterinarian trust. However, online retailers are expanding rapidly at 7.55% CAGR through 2031, driven by convenience, competitive pricing, and the growing comfort of pet owners with e-commerce platforms for healthcare products. Major acquisitions like Tractor Supply Company's purchase of Allivet, a leading online pet pharmacy, demonstrate the strategic importance of digital distribution channels

Pet specialty stores represent a smaller but stable segment, focusing on premium products and specialized nutrition for diabetic pets. The rise of subscription-based services, exemplified by Chewy's Autoship program accounting for 73% of net sales, indicates strong consumer preference for automated delivery of chronic care products. Veterinary pharmacies maintain advantages in prescription management, clinical support, and relationships with veterinary practices, but face pressure to enhance their digital capabilities and competitive pricing to retain market share.

Geography Analysis

North America contributed 38.71% of 2025 revenue, supported by high insurance penetration and early access to SGLT-2 therapies. Forward growth remains steady as tele-medicine regulation relaxes and CGM reimbursement expands. Canada’s pending exit from animal-sourced insulin, however, introduces near-term sourcing risk that could elevate costs and drive therapeutic substitutions.

Europe combines stringent regulatory oversight with receptive consumers. GDPR compliance shapes cloud data flows for CGM, yet harmonized VICH rules ease product registration, fostering cross-border launches for devices such as AlphaTrak 3. Northern markets are adopting AI-powered analyzers rapidly, while Southern states see incremental gains through rising pet humanization. Collectively, these dynamics reinforce Europe as a profitable yet compliance-heavy portion of the pet diabetes care market.

Asia-Pacific is the fastest-growing region with an 7.85% CAGR to 2031. Rising disposable income, smartphone penetration, and cultural acceptance of e-commerce fortify momentum. Japan and China anchor premium demand, whereas India and Indonesia supply volume growth through expanding pet bases. Government initiatives to support tele-veterinary services, notably in Thailand and Singapore, further accelerate digital treatment adoption in the pet diabetes care market.

Regulatory Landscape

In the United States, pet diabetes therapeutics (insulins and oral agents) are regulated as animal drugs by the FDA Center for Veterinary Medicine (CVM), typically moving through an Investigational New Animal Drug (INAD) file toward a New Animal Drug Application (NADA) under the Federal Food, Drug, and Cosmetic Act (including pathways described in 21 CFR Part 511). This framework governs evidence requirements for chronic-use products, including chemistry, manufacturing, and controls (CMC) and post-approval safety monitoring, which is particularly relevant for newer feline oral SGLT-2 therapies that shift treatment away from injections.

In the European Union, veterinary medicinal products fall under Regulation (EU) 2019/6, which harmonizes authorization, manufacturing, distribution, and pharmacovigilance requirements across member states. EMA and its Committee for Veterinary Medicinal Products (CVMP) also issue targeted risk communications when new safety signals emerge; for example, CVMP issued a Direct Animal Healthcare Professional Communication in July 2024 regarding Senvelgo (velagliflozin) and diabetic ketoacidosis risk management in cats. Separately, the USDA APHIS Center for Veterinary Biologics (CVB) oversees veterinary biologics (distinct from diabetes drugs and devices) under the Virus-Serum-Toxin Act, setting licensing and inspection expectations that affect adjacent diagnostic and preventive inputs used in veterinary practices.

Value Chain Analysis

The value chain starts with R&D and regulatory submissions for veterinary drugs (e.g., insulin therapies and feline oral SGLT-2 inhibitors), alongside device engineering for glucose monitoring, then moves into specialized manufacturing and quality systems. For drugs, supply depends on validated active pharmaceutical ingredient sourcing, sterile fill-finish, stability programs, and pharmacovigilance, while CGM supply relies on high-value, low-volume sensor and electronics manufacturing and calibration, including veterinary-calibrated systems such as Zoetis AlphaTrak 3 and veterinary-focused offerings such as ALR Technologies GluCurve Pet CGM. Labeling, product information, and safety communication requirements are built in throughout, with EU alignment under Regulation (EU) 2019/6 influencing documentation and packaging workflows.

Commercialization is anchored in veterinary hospitals and clinics as the point of diagnosis, prescribing, and onboarding, then extends into refills and consumables distribution through veterinary pharmacies and increasingly online retailers and subscription models. Logistics and channel execution matter for diabetes care because repeat purchasing is routine: insulin refills, syringes/pen needles, CGM sensors, and test strips drive ongoing demand. Tele-vet integrations and cloud dashboards add a service layer, but bottlenecks remain around continuity of supply for insulin and device consumables, and around data-sharing and privacy constraints that can slow scaling of remote monitoring programs across regions and providers.

Competitive Landscape

The pet diabetes care industry revolves around three diversified leaders that collectively control much of the prescription channel. Boehringer Ingelheim delivered EUR 4.7 billion in 2023 animal-health sales after launching Senvelgo, and it is scaling U.S. capacity with a USD 66.1 million plant expansion in Georgia. Merck Animal Health maintains a robust insulin franchise and leverages the Safe-Net distribution alliance to guarantee supply continuity. Zoetis differentiates through diagnostics, debuting the cartridge-based AI hematology analyzer and broadening reference labs to integrate CGM data streams.

Emergent technology platforms intensify competition. ALR Technologies’ GluCurve Pet CGM secures early veterinary interest for its species-specific algorithms, whereas tele-medicine providers such as Vetster partner with sensor manufacturers to deliver closed-loop remote monitoring. Start-ups like Endo Health attract venture funding to pursue algorithmic dosing aids, hinting at future ecosystem consolidation. Distribution is fragmenting: Tractor Supply’s Allivet acquisition opens an USD 15 billion incremental addressable pool, and Chewy’s private-label nutrition portfolio positions it as a one-stop channel for diabetic pets.

Supply resilience remains a watchpoint. The Vetsulin incident sharpened regulatory focus on sterility and batch consistency, prompting risk-mitigation alliances among manufacturers. Strategic stockpiling and multi-supplier frameworks are now embedded in procurement policies across major veterinary chains. Overall, although barriers to molecule development remain high, device entrants and digital players are lowering service barriers, preserving moderate concentration in the pet diabetes care market.

Pet Diabetes Care Industry Leaders

Merck & Co., Inc.

Allison Medical

UltiMed Inc.

Boehringer Ingelheim

Zoetis

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Guideline-driven standardization is creating whitespace for companies bundling drugs, CGM, and care pathways into repeatable protocols for clinics and home care. The update to the 2025 Diabetes Management Guidelines for Cats from AAHA recognizes SGLT-2 inhibitors as a treatment option and emphasizes continuous glucose monitoring, supporting CGM onboarding, data review, and dose-adjustment workflows in veterinary settings. This supports opportunities for device makers, tele-vet platforms, and veterinary chains to package diabetes management as subscription programs that combine sensors, virtual coaching, and prescription refills.

Regulatory modernization and market-entry actions broaden the innovation funnel. The June 2026 FDA MUMS Blueprint for Success (2026-2028) expands development options for minor uses and minor species, supporting differentiated companion-animal indications and formulations. From a commercialization angle, ALR Technologies moved from readiness to in-market availability in Canada, relaunching GluCurve Pet CGM in January 2026 after internal manufacturing testing, and then launching the product in May 2026. This sequence illustrates how CGM-enabled home monitoring partnerships can expand beyond initial launch geographies.

Recent Industry Developments

- June 2026: The FDA released its MUMS Blueprint for Success (2026-2028), outlining actions to modernize and expand drug development for minor uses and minor species. The program supports development pathways relevant to companion-animal chronic diseases, improving the commercial viability of differentiated formulations and novel mechanisms. For pet diabetes care, it strengthens the regulatory backdrop for companies pursuing niche indications, new delivery formats, and label expansions.

- April 2025: AAHA released 2025 Diabetes Management Guidelines for Cats recognizing SGLT-2 inhibitors and emphasizing continuous glucose monitoring to support clinic workflows and home-care programs. The update broadens adoption of CGM-enabled care and clarifies data-sharing expectations in practice, which may accelerate integration of CGM in routine management.

- July 2024: EMA and CVMP issued a Direct Animal Healthcare Professional Communication for Senvelgo (velagliflozin) highlighting risk management for diabetic ketoacidosis in cats and emphasizing close monitoring in the initial treatment period. The communication tightened clinical protocols around feline oral SGLT-2 use and reinforced post-marketing vigilance for newer diabetes drug classes. This step influences product education, veterinarian onboarding, and real-world evidence generation for oral therapies.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market tracks the value of products and care used to manage diabetes in companion animals, covering treatment, monitoring, and supporting supplies purchased through veterinary and retail channels across major geographies.

Scope exclusions: We exclude non-diabetes routine wellness products and general pet foods that are not positioned or used for diabetes management.

Segmentation Overview

- By Care Type

- By Drug Type

- Insulin Therapy

- Oral Medication

- By Device Type

- Glucose Monitoring Devices

- Insulin Delivery Devices

- By Drug Type

- By Animal Type

- Canine

- Feline

- By End User

- Veterinary Hospitals & Clinics

- Home-care Settings

- By Distribution Channel

- Veterinary Pharmacies

- Online Retailers

- Pet Specialty Stores

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping how diabetic pets are diagnosed, treated, and monitored, then aligning that with what gets sold through the main channels. We rely on public, non-paywalled sources such as USDA pet health materials, FDA animal drug and device information, CDC-aligned publications where diabetes education content overlaps, and peer-reviewed veterinary journals that report prevalence and treatment patterns.

To shape the commercial picture, we also review company annual reports and investor presentations, association and veterinary hospital group websites, and reputed press coverage for product launches and pricing signals. Where needed, paid subscriptions for company financials and intelligence are used to cross-check revenue exposure and geographic mix, and a patent database is used to confirm the pace of new monitoring and delivery concepts. The sources named above are illustrative, and additional public references were used to fill gaps, validate assumptions, and clarify definitions.

Primary Interviews and Surveys

Primary inputs are collected through expert interviews and structured surveys with veterinarians, clinic procurement teams, distributors, and product specialists to confirm treatment splits and typical purchasing behavior. For a global market like this, feedback is balanced across the Americas, EMEA, and APAC, then sources are re-contacted when a key assumption (for example, insulin usage duration or monitoring adoption) appears inconsistent with the broader set of signals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 13% | APAC: 47% |

| Mid tier: 54% | Functional/Unit leaders: 31% | EMEA: 35% |

| Smaller Players: 14% | Managers: 56% | Americas: 18% |

Market-Sizing & Forecasting

Sizing is built using a top-down demand pool approach where prevalence and diagnosis rates are used to reconstruct the treated pet base, which is then translated into annual spend using care intensity assumptions. After forming the headline number, we run selective bottom-up checks, including sampled ASP times volume for insulin and test strips, channel checks with clinics and distributors, and a light roll-up of relevant revenue lines where disclosures allow.

Key inputs that typically move the model include the estimated diabetic pet population by major regions, the share of pets receiving insulin therapy versus diet and adjunct care, average refill frequency for insulin and consumables, monitoring method mix (spot testing versus continuous monitoring where applicable), and average price progression by channel. When a datapoint cannot be observed directly, we use bounded ranges from interviews and public evidence, and the midpoint is adjusted only if it also matches the implied spend per treated pet.

Forecasting uses scenario analysis supported by short series trend smoothing, since adoption of monitoring tools and owner compliance can change quickly after new launches or guideline changes. The scenarios are tied to a small set of trackable drivers, such as veterinary visit rates, the direction of pet insurance penetration, and the pace of device adoption reported by practitioners, then reconciled back to spending capacity visible in the broader companion animal health budget.

Data Validation & Update Cycle

Outputs are validated through cross-checks against independent signals such as estimated treated-pet counts, typical monthly therapy costs, and channel feedback on order volumes, and then the variance is reviewed before sign-off. If an outlier is found, the assumption is traced back to its source, recalculated, and in many cases clarified through a fresh follow-up with an interviewee.

We run a multi-step internal review so the same math can be repeated by another analyst and the model reaches the same totals. The report is refreshed annually, with interim updates when material events occur, such as product withdrawals, major regulatory actions, or step changes in pricing, and a final pre-delivery check is completed so clients receive the latest view.

Mordor Intelligence's Pet Diabetes Care Market Sizing Compared With Other Published Estimates

Published market sizes for pet diabetes care often differ because each publisher makes different choices on what is counted, which year is treated as the start point, and how device adoption is projected. Some publishers also mix adjacent pet health spending into the total, which can increase the number without being obvious to a reader.

The main gap comes from whether veterinary diets and broader endocrine care are included, and how quickly pricing and monitoring uptake are allowed to rise. Mordor Intelligence counts only diabetes-specific drugs, monitoring, and related supplies, then stress-tests per-pet annual spend against clinic-level usage patterns.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.38 B (2026) | |

| Global Consultancy A | USD 2.27 B (2025) | Uses an earlier base year and appears to rely more heavily on device-led growth assumptions, which can pull forward monitoring adoption and lift near-term totals versus a treated-pet demand build. |

| Industry Publisher B | USD 2.31 B (2025) | Anchors the market on a different starting year and applies a faster multi-year expansion rate, which can reflect a more aggressive scenario for therapy compliance and price progression across channels. |

Across the three figures, the spread is mainly explained by scope and by how quickly monitoring and ongoing therapy spend is assumed to scale in the first few years. By keeping the build-up tied to treated pets and repeatable spend drivers, the resulting size stays easier to audit and update when new clinical or pricing signals emerge.

Key Questions Answered in the Report

How large is the pet diabetes care market in 2026?

The pet diabetes care market size is valued at USD 2.38 billion in 2026.

What is the expected growth rate of the pet diabetes care market through 2031?

The market is projected to post a 5.85% CAGR, reaching USD 3.17 billion by 2031.

Which therapy type is growing fastest?

Oral medications, led by feline-specific SGLT-2 inhibitors, are forecast to expand at 6.65% CAGR.

Which region shows the highest growth potential?

Asia-Pacific is the fastest-growing geography with an 7.85% CAGR to 2031, driven by high pet adoption and rising disposable income.

Why are CGM devices important for diabetic pets?

CGM devices enhance glycaemic control by providing real-time data, reducing clinic visits, and supporting remote dose adjustments, thereby improving outcomes and owner compliance.

Page last updated on: