Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Object-Based Storage Market Report is Segmented by Deployment Model (Cloud-Based, and On-Premise), Component (Software-Defined Platforms, and More), Storage Media (All-Flash, HDD-Optimized, and More), Enterprise Size (Large Enterprises, and SMEs), Application (Backup and Archive, and More), Industry Vertical (BFSI, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

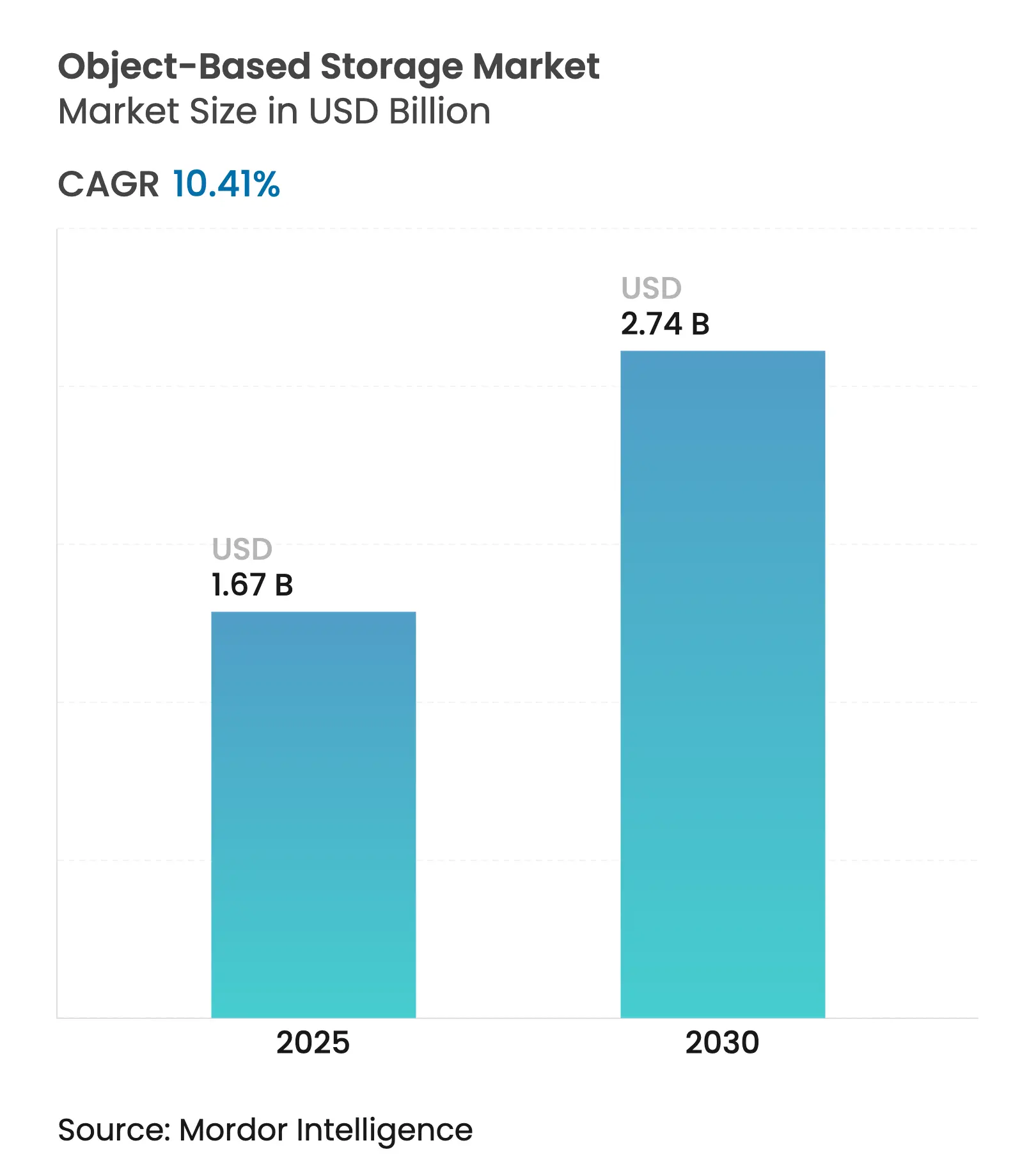

| Market Size (2025) | USD 1.67 Billion |

| Market Size (2030) | USD 2.74 Billion |

| Growth Rate (2025 - 2030) | 10.41 % CAGR |

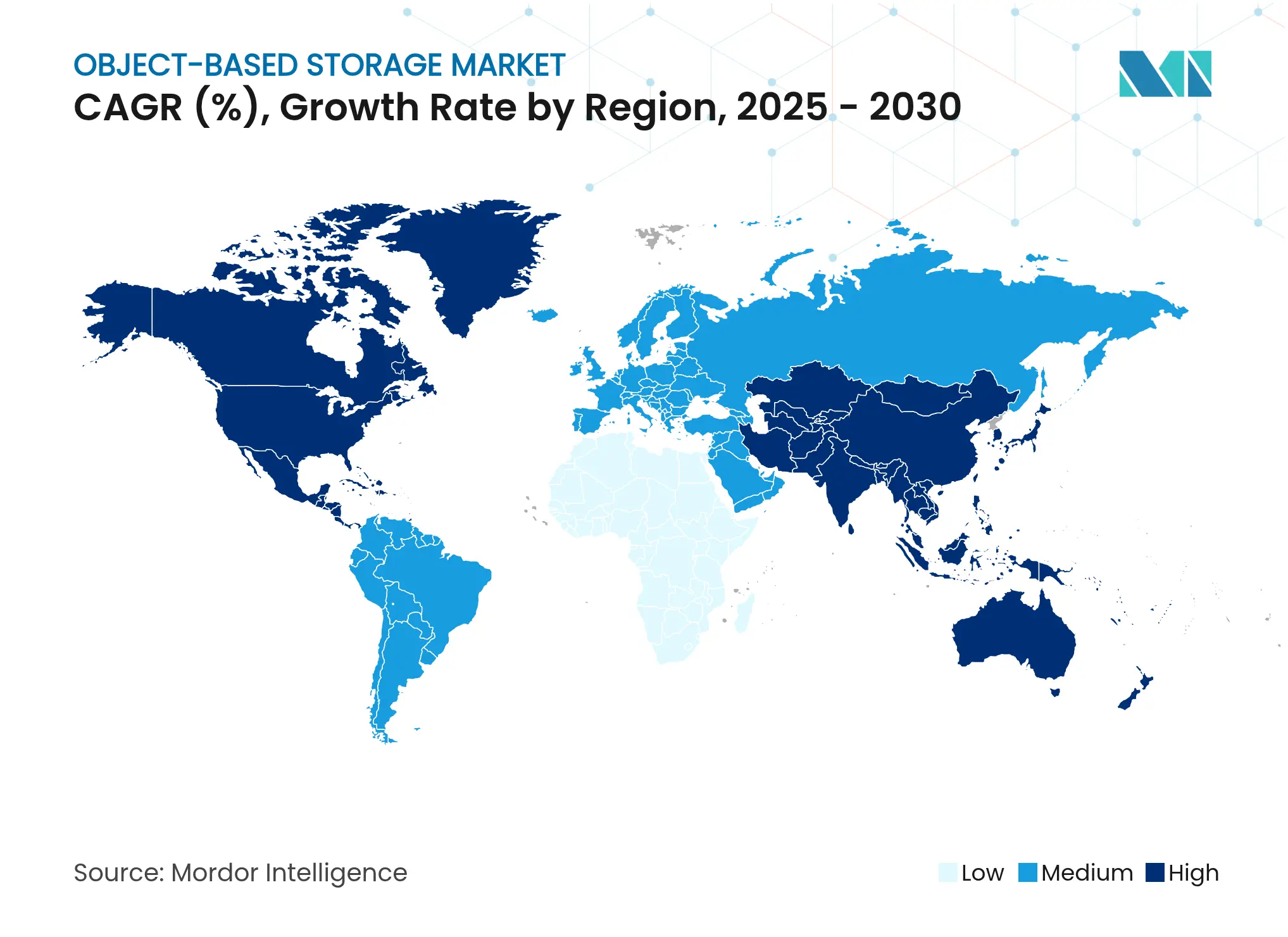

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

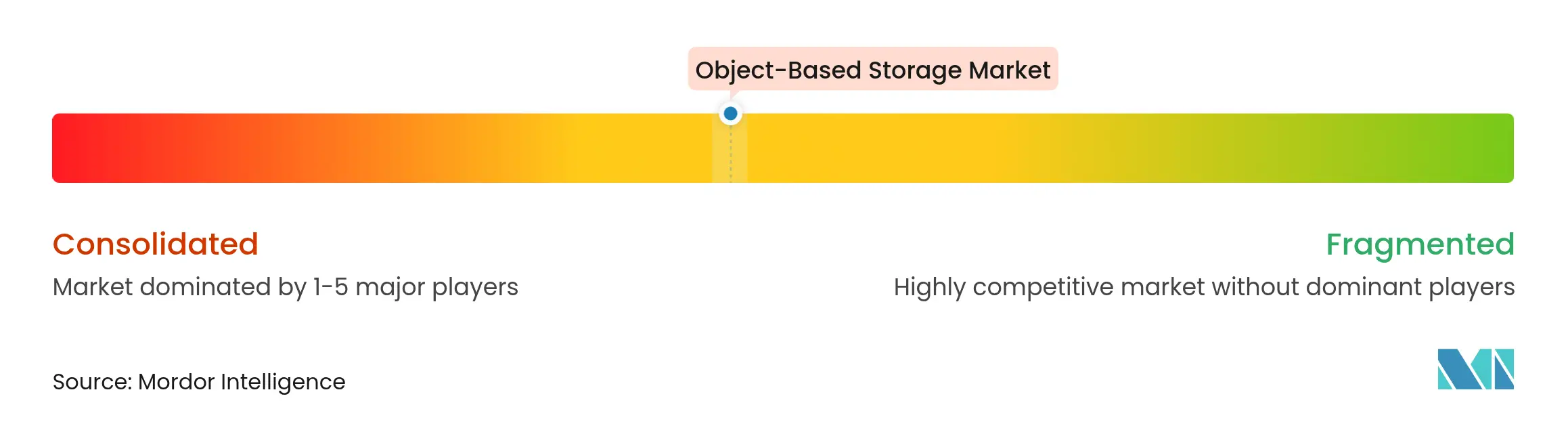

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The object-based storage market size stands at USD 1.67 billion in 2025 and is forecast to expand to USD 2.74 billion by 2030, registering a 10.41% CAGR through the period. Strong growth reflects mounting enterprise demand for cloud-native, exabyte-scale repositories that feed artificial intelligence and machine learning models. Organizations are migrating from file and block arrays toward object architectures to cope with unstructured data growth, to harden cyber-resilience through immutability features, and to simplify multi-cloud data mobility. Performance breakthroughs in all-flash object arrays, falling NAND prices, and the adoption of S3-compatible APIs across public and private clouds have improved both speed and economics, accelerating deployments. Heightened regulatory scrutiny of cross-border data flows and ransomware threats further reinforce the shift, pushing decision makers to pursue hybrid strategies that combine on-premises control with cloud scalability.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Exabyte-Scale Data Growth from AI and Generative Models Exabyte-Scale Data Growth from AI and Generative Models | +2.8% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+2.8% | Geographic Relevance:Global, led by North America and Asia-Pacific | Impact Timeline:Medium term (2-4 years) |

Rapid Enterprise Adoption of Hybrid and Multi-Cloud Object Storage Rapid Enterprise Adoption of Hybrid and Multi-Cloud Object Storage | +2.1% | Global, especially Europe and North America | Short term (≤ 2 years) | |||

Low Acquisition Cost per TB for Capacity-Optimized HDD Tiers Low Acquisition Cost per TB for Capacity-Optimized HDD Tiers | +1.4% | Cost-sensitive emerging markets | Long term (≥ 4 years) | |||

Emergence of All-Flash High-Performance Object Arrays for GPU Workloads Emergence of All-Flash High-Performance Object Arrays for GPU Workloads | +1.9% | North America and Asia-Pacific | Medium term (2-4 years) | |||

Ransomware-Driven Demand for Immutable Object Storage Targets Ransomware-Driven Demand for Immutable Object Storage Targets | +1.7% | North America and Europe | Short term (≤ 2 years) | |||

Decentralized Web3 Object Storage for Data Provenance Decentralized Web3 Object Storage for Data Provenance | +0.5% | North America and Europe | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Exabyte-Scale Data Growth from AI and Generative Models

Artificial intelligence projects now train models on datasets surpassing 100 terabytes, sending annual enterprise data creation rates surging between 40% and 60%. Object storage is preferred for these AI data lakes because it scales linearly across clusters, supports parallel access, and lowers cost per terabyte compared with block arrays. GPU-optimized object systems reduce latency by serving data directly to compute nodes, preventing idle GPU cycles that waste capital. As multimodal models incorporate text, images, video, and sensor feeds, the performance and capacity imperatives rise further, cementing object repositories as a core pillar of AI infrastructure. Edge-AI rollouts magnify the trend by requiring federated data pools spanning many sites while still delivering cloud-like management.

Rapid Enterprise Adoption of Hybrid and Multi-Cloud Object Storage

By 2024, 78% of organizations will operate multi-cloud environments, utilizing object storage as the common denominator for data mobility. S3-compatible APIs enable workloads to seamlessly transition between public clouds and on-premises clusters without requiring rewrites, thereby easing data sovereignty and disaster-recovery mandates. Firms move datasets back on-premises to meet General Data Protection Regulation rules, yet retain burst capacity in the cloud.[1]Data Repatriation Trend Analysis, NTT Data, nttdata.com Automated tiering policies further optimize total cost of ownership by shifting cold objects to low-cost cloud tiers while keeping hot data local. As data gravity intensifies, applications follow data rather than the other way around, reinforcing hybrid architectures.

Emergence of All-Flash High-Performance Object Arrays for GPU Workloads

High-performance computing teams now expect object systems to match block-storage latencies. Vendors have answered with all-flash arrays such as HPE Alletra MP X10000, which surpass 1 million IOPS for object workloads.[2]Alletra MP Storage Solutions, Hewlett Packard Enterprise, hpe.com NVMe media and GPU-direct protocols remove CPU bottlenecks, enabling linear performance scaling as GPU counts rise.[3]GPUDirect Storage Developer Documentation, NVIDIA, nvidia.com Deduplication and compression close the cost gap with HDD systems, making all-flash feasible for primary data rather than a niche option. Enterprises pursuing AI, genomic analysis, or real-time analytics increasingly require these sub-millisecond response times to keep expensive compute resources fully utilized.

Ransomware-Driven Demand for Immutable Object Storage Targets

Attackers frequently delete or encrypt backups, prompting a pivot toward immutable, write-once object buckets. Such vaults deny modification for a defined retention window, guaranteeing clean recovery points even when credentials are compromised.[4]Ransomware Protection Through Immutable Backups, Arcserve, arcserve.com Regulatory frameworks in finance and healthcare now emphasize tamper-proof archives, aligning cyber-resilience with compliance obligations. Vendors embed multifactor authentication, zero-trust networking, and in-flight plus at-rest encryption, elevating object platforms from passive repositories to security control points. As insurance underwriters tighten policy terms, immutable storage adoption accelerates.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Legacy Application Integration Challenges (POSIX vs S3) Legacy Application Integration Challenges (POSIX vs S3) | -1.8% | Mature enterprise markets worldwide | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-1.8% | Geographic Relevance:Mature enterprise markets worldwide | Impact Timeline:Medium term (2-4 years) |

High Public-Cloud Egress and API Costs High Public-Cloud Egress and API Costs | -1.2% | Data-intensive industries globally | Short term (≤ 2 years) | |||

Talent Gap in Object Storage Architecture and Operations Talent Gap in Object Storage Architecture and Operations | -0.9% | Emerging markets | Long term (≥ 4 years) | |||

Regulatory Uncertainties Around Cross-Border Data Movement Regulatory Uncertainties Around Cross-Border Data Movement | -0.7% | Europe and Asia-Pacific | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Legacy Application Integration Challenges (POSIX vs S3)

Many mission-critical workloads require hierarchical file semantics, such as random byte writes and locking, which native object protocols lack. Gateways can translate POSIX calls to S3, but add latency and operational overhead, and retrofitting decades-old code carries cost and risk. Databases and HPC jobs that rely on shared filesystems face the steepest hurdles, slowing full-scale migrations. Over time, containerization and microservice refactoring may ease dependence on POSIX, but in the medium term, integration friction will temper uptake in certain verticals.

High Public-Cloud Egress and API Costs

Egress fees hover near USD 0.09-0.12 per gigabyte, and high-transaction workloads rack up millions of API calls, pushing monthly bills beyond initial expectations. Budget unpredictability hampers planning for analytics pipelines or disaster-recovery drills that trigger large data transfers. Consequently, some enterprises cap cloud use at secondary copies while keeping primary datasets on-premises, or they adopt providers with flat-rate models. While competition may moderate fees, near-term economics remain a deterrent.

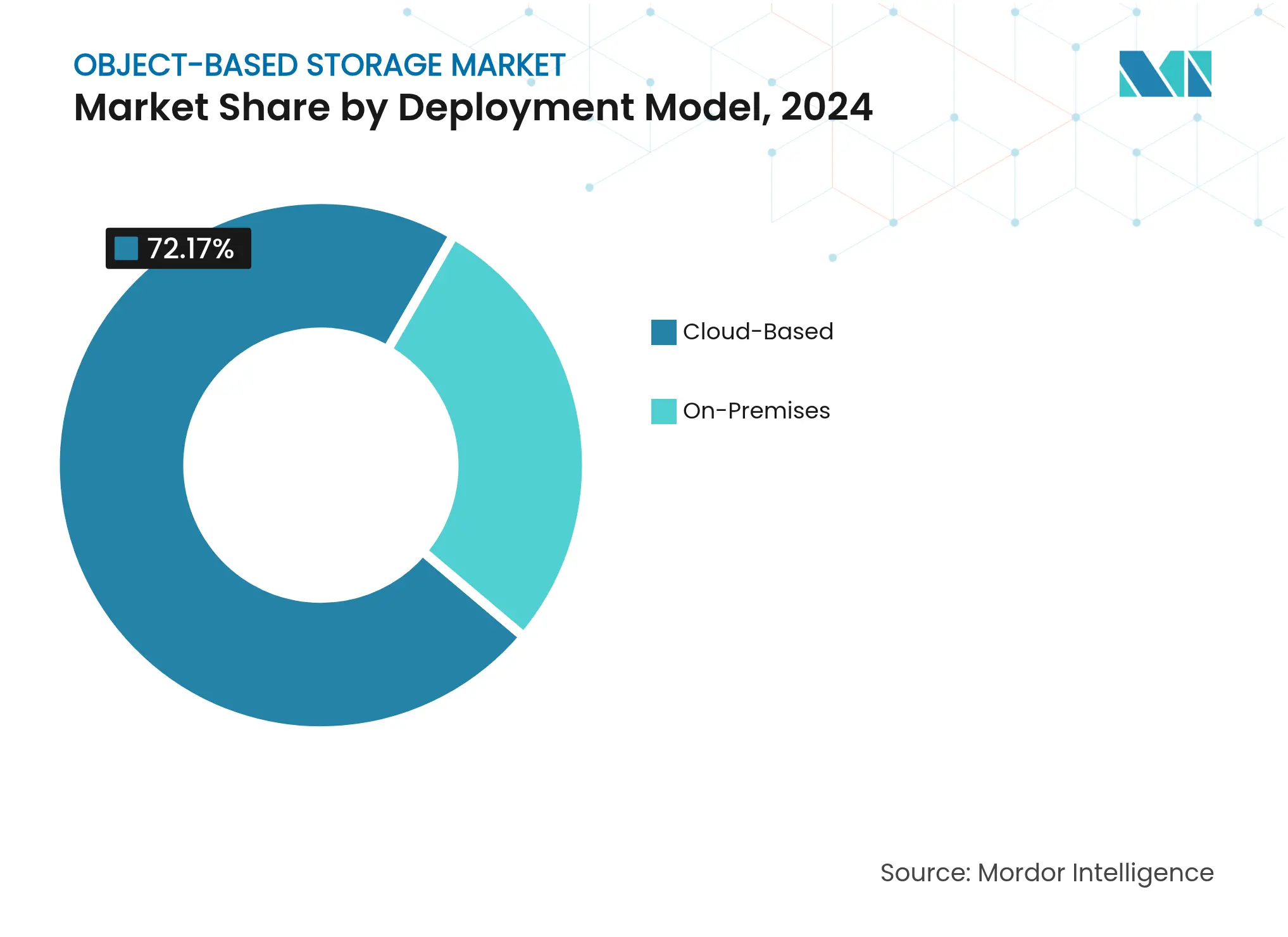

By Deployment Model: Hybrid Strategies Drive Market Evolution

Cloud architectures held 72.17% of spending in 2024, underscoring enterprise intent to blend on-premises control and public-cloud elasticity. The arrangement satisfies sovereignty mandates while enabling burst analytics during demand spikes. Data repatriation in Europe and Asia Pacific reinforces this stance as organizations respond to new privacy statutes. Cloud revenue is forecast to rise at a 10.82% CAGR, keeping the object-based storage market size on a steady upward course.

Growing edge workloads spur additional hybrid momentum. Factories, hospitals, and retail outlets collect data locally for low-latency processing then route compressed copies to core repositories for training or compliance archiving. Modern orchestration tools make these data flows policy-driven and automated, reducing administrative burden. The hybrid pattern therefore remains central to long-term infrastructure planning.

By Component: Software-Defined Platforms Lead Infrastructure Evolution

Software-defined offerings secured 61.46% share in 2024 as buyers sought hardware independence and agile feature rollouts. Separation of software from commodity servers lowers capital cost and quickens upgrades, which aligns with DevOps mind-sets spreading across IT teams. With all-flash options gaining ground, software layers now optimize data placement dynamically across media types, squeezing cost without manual tuning. The segment’s 11.01% CAGR signals confidence that code, not proprietary boxes, will drive innovation in the object-based storage industry.

Hardware appliances still appeal to risk-averse sectors that favor turnkey warranties and single-vendor support. Some suppliers now bundle software-defined stacks inside reference designs, offering a middle path that preserves flexibility while shortening deployment cycles. The resulting ecosystem fosters competition that benefits users through faster roadmap execution and price pressure.

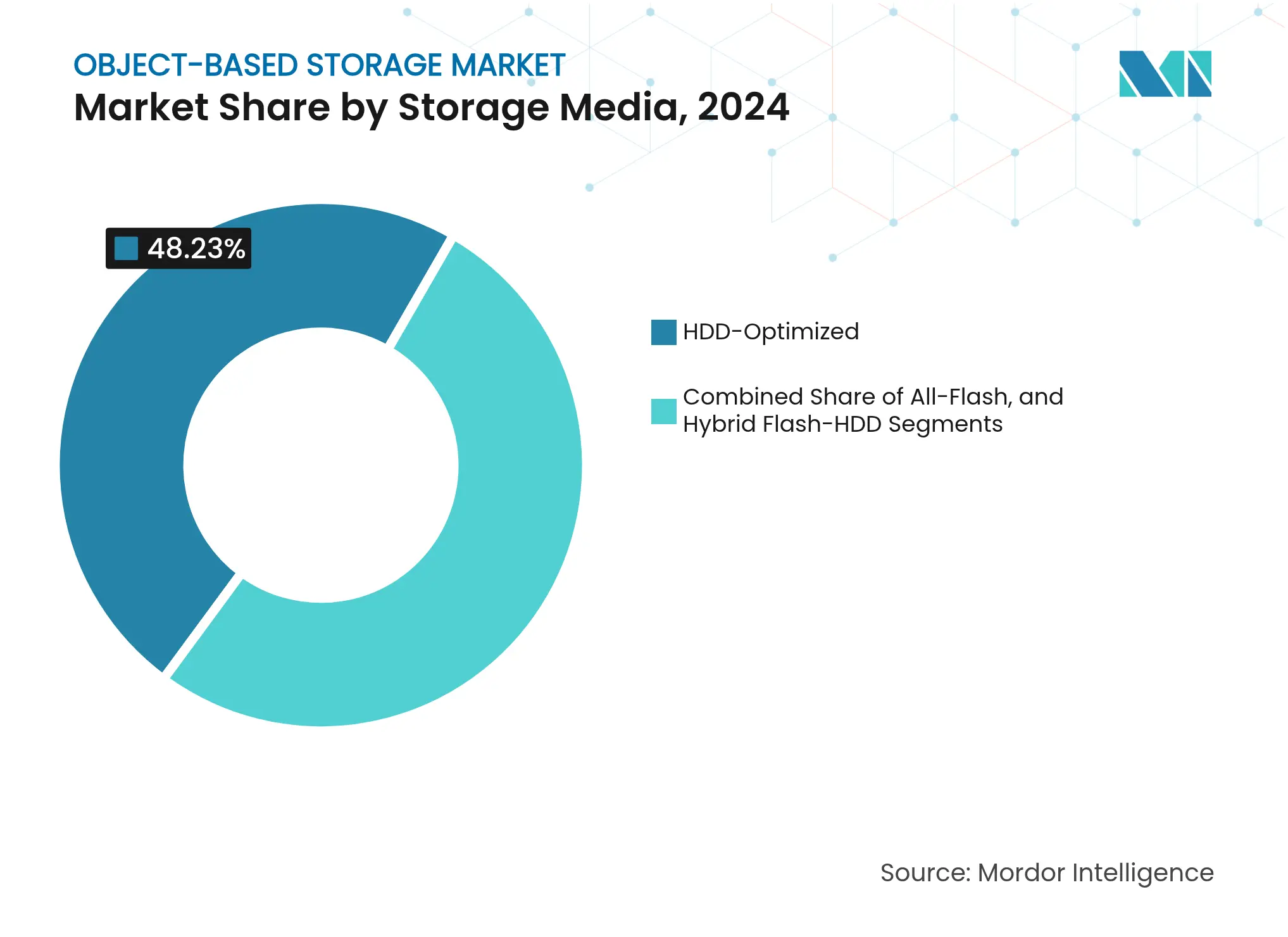

By Storage Media: All-Flash Arrays Transform Performance Paradigms

HDD-optimized arrays held 48.23% share in 2024, reflecting ongoing need for economical capacity tiers. Yet all-flash systems are advancing at 10.73% CAGR, proof that workloads such as AI and real-time analytics justify higher media prices with productivity gains. All-flash clusters exceeding 1 million IOPS attract enterprises keen to avoid GPU starvation during model training. Such performance positions flash as a mainstream choice, not merely a caching layer within the object-based storage market.

Hybrid flash-HDD architectures mediate the mix. Policy engines swap hot and cold objects between tiers without operator input, delivering SSD speed to time-sensitive jobs while capitalizing on HDD density for archives. Falling NAND pricing trends and higher drive capacities further narrow the cost delta, suggesting flash will claim a larger slice of new deployments each year.

Note: Segment shares of all individual segments available upon report purchase

By Enterprise Size: Large Enterprises Maintain Dominance While SMEs Accelerate Adoption

Large organizations captured 65.04% of revenue in 2024, leveraging global footprints and vast datasets from autonomous vehicles, satellite imagery, and genomics research. Their requirements for multi-region replication and tight compliance auditing skew purchasing toward advanced feature sets. Ongoing AI investments propel a 10.52% CAGR, ensuring that big-business budgets remain pivotal to object-based storage market growth.

Small and medium enterprises increasingly consume cloud-based services that package object storage behind usage-based billing, removing capital barriers. Managed service providers add value through data governance layers and integration with analytics stacks, allowing SMEs to pursue data-driven strategies. As digital transformation spreads deeper into supply chains, SME demand should broaden the customer base and diversify use cases.

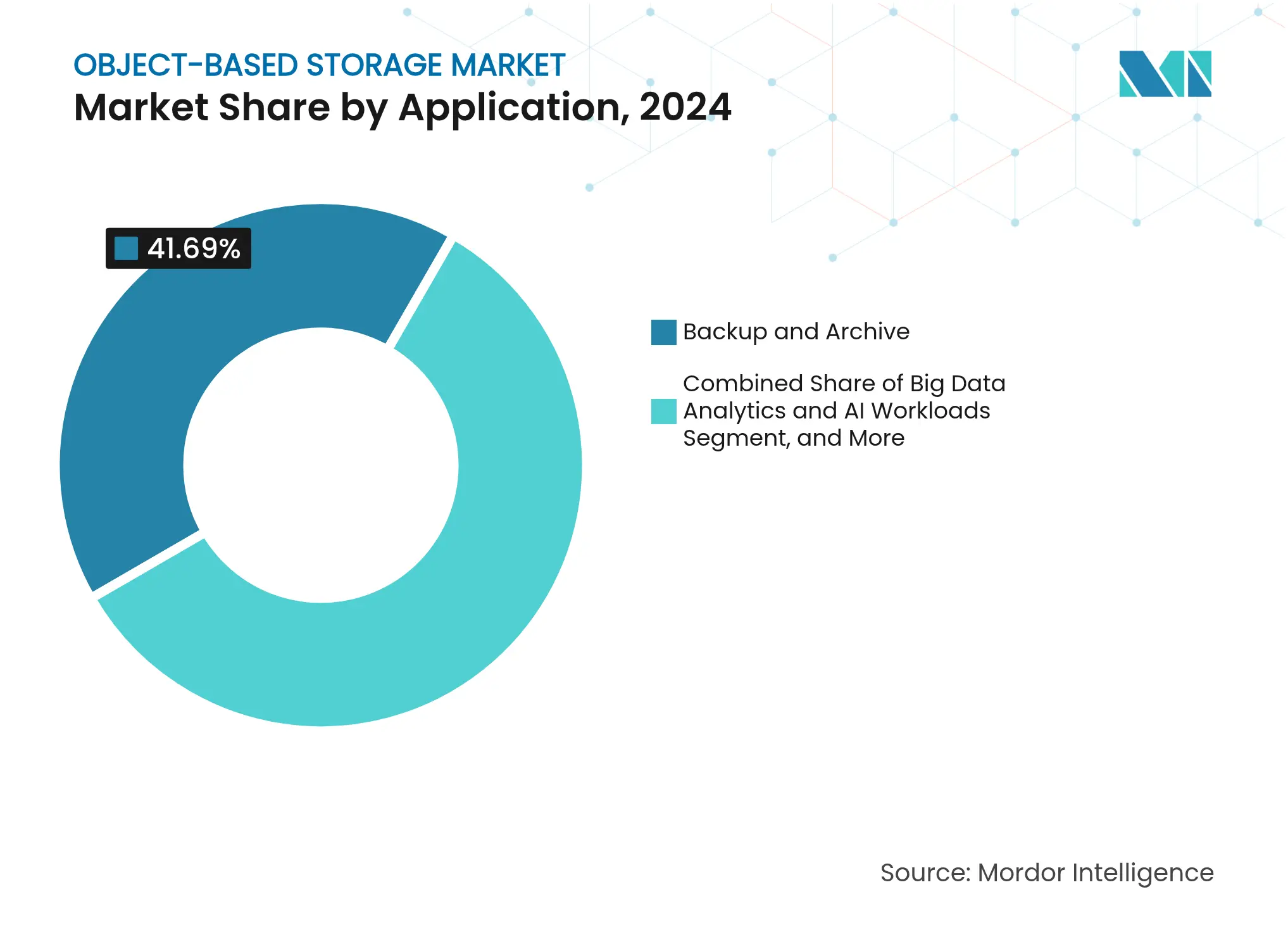

By Application: AI Workloads Reshape Storage Requirements

Backup and archive remained the largest application with 41.69% share in 2024, owing to object storage’s inherent durability and cost profile. Nonetheless, big data analytics and AI workloads top the growth chart at 11.04% CAGR, demonstrating how active data exploitation overtakes passive retention. GPU clusters ingest streaming objects for feature extraction, model training, and iterative tuning, redefining performance baselines for storage vendors within the object-based storage market size landscape.

Media streaming, IoT telemetry, and disaster-recovery scenarios also accelerate thanks to global namespace capabilities that serve content consistently from dispersed regions. Immutability features extend utility beyond compliance into cyber-resilience, making object buckets a cornerstone of zero-trust defenses. The broadening workload mix keeps vendors innovating on both throughput and manageability fronts.

Note: Segment shares of all individual segments available upon report purchase

By Industry Vertical: BFSI Leadership Faces Healthcare Challenge

Financial institutions accounted for 23.32% of 2024 revenue, driven by mandates for immutable archives, audit trails, and stringent recovery point objectives. Use cases span trade surveillance, fraud analytics, and regulatory reporting, all of which demand petabyte-scale footprints and fine-grained access controls. The sector’s data growth trajectory ensures continued investment, yet competitive intensity rises as healthcare and life sciences outpace overall expansion with a 10.97% CAGR.

Genomic sequencing, digital pathology, and clinical trial platforms generate terabytes per run, necessitating elastic and secure storage pools. Object systems meet these requirements by offering metadata-rich indexing for complex searches and by supporting multipart uploads, which are essential for large imaging files. Adoption scales across research consortia and hospital networks alike, underpinning precision medicine initiatives and remote diagnostics services.

Asia-Pacific led the object-based storage market with 37.73% share in 2024, fueled by national AI programs, 5G rollouts, and e-commerce ecosystems in China, Japan, and India. Government incentives for local data center construction and cloud adoption underpin spending, while the digitization of manufacturing drives machine data volumes. Aggressive capital deployment keeps the region at the center of vendor roadmaps.

The Middle East is expected to record the highest regional CAGR of 11.79% through 2030. Saudi Arabia’s Vision 2030 and the United Arab Emirates’ National AI Strategy bankroll hyperscale facilities and smart-city projects that demand exabyte-scale repositories. Landmark undertakings like NEOM generate continuous sensor and video streams that naturally gravitate toward object storage for durability and geo-redundancy.

North America and Europe maintain substantial positions thanks to mature cloud ecosystems and strict regulatory environments that mandate compliant storage. Data sovereignty concerns prompt European enterprises to adopt hybrid topologies, while U.S. organizations lead the way in AI-optimized all-flash arrays. South America and Africa remain nascent yet show rising interest as broadband penetration and fintech ecosystems grow, hinting at longer-term upside.

Market Concentration

The field remains moderately fragmented, spanning legacy infrastructure vendors, cloud-native specialists, and hyperscale cloud providers. Incumbents like Dell Technologies, NetApp, and IBM leverage installed bases to cross-sell object software atop existing arrays, while newer entrants such as MinIO and VAST Data emphasize Kubernetes integration and disaggregated architectures. Public clouds, notably Amazon Web Services and Microsoft Azure, continue to siphon workloads through integrated services, complicating the share calculus.

Performance differentiation now centers on GPU-direct transfers, NVMe fabrics, and software intelligence that automates data placement for cost or compliance imperatives. Vendors bundle security features such as multifactor authentication, object lock, and client-side encryption to address ransomware risks and meet audit requirements. Simplified, flat-rate pricing models from challengers like Wasabi pressure competitors to rethink egress fee structures, illustrating how business model innovation shapes the object-based storage industry.

Mergers and acquisitions accelerate capability expansion. Lenovo’s USD 200 million purchase of Infinidat in January 2025 adds high-performance tiering. Salesforce’s USD 1.9 billion acquisition of Own Company in September 2024 signals convergence between data protection services and primary storage platforms, reflecting buyer preference for integrated data-management stacks.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Object-based storage technology organizes data in a flat structure that can be retrieved in the same manner as the original data stored rather than in a hierarchical form. This report segments the market by its type (cloud-based, on-premise) and geography.

The object-based storage market is segmented by its type (cloud-based, on-premise) and geography (North America, Europe, Asia Pacific, and the Rest of the World).

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.