Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

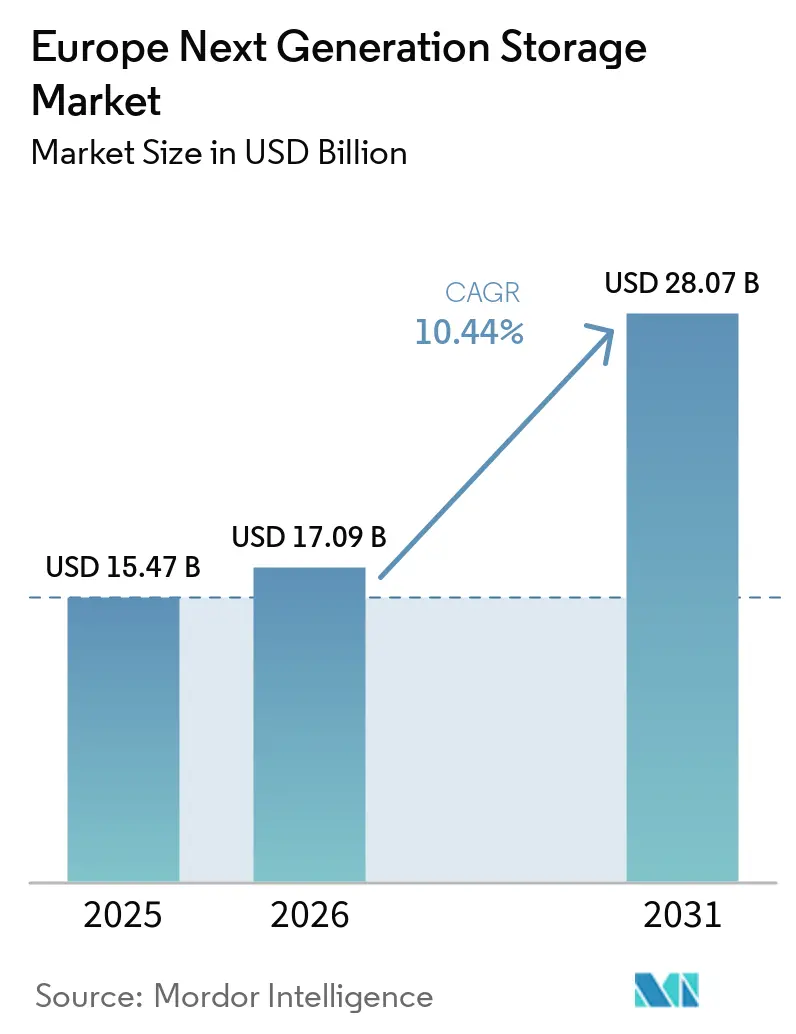

| Base Year Market Size (2025) | USD 15.47 Billion |

| Market Size (2026) | USD 17.09 Billion |

| Market Size (2031) | USD 28.07 Billion |

| Growth Rate (2026 - 2031) | 10.44% CAGR |

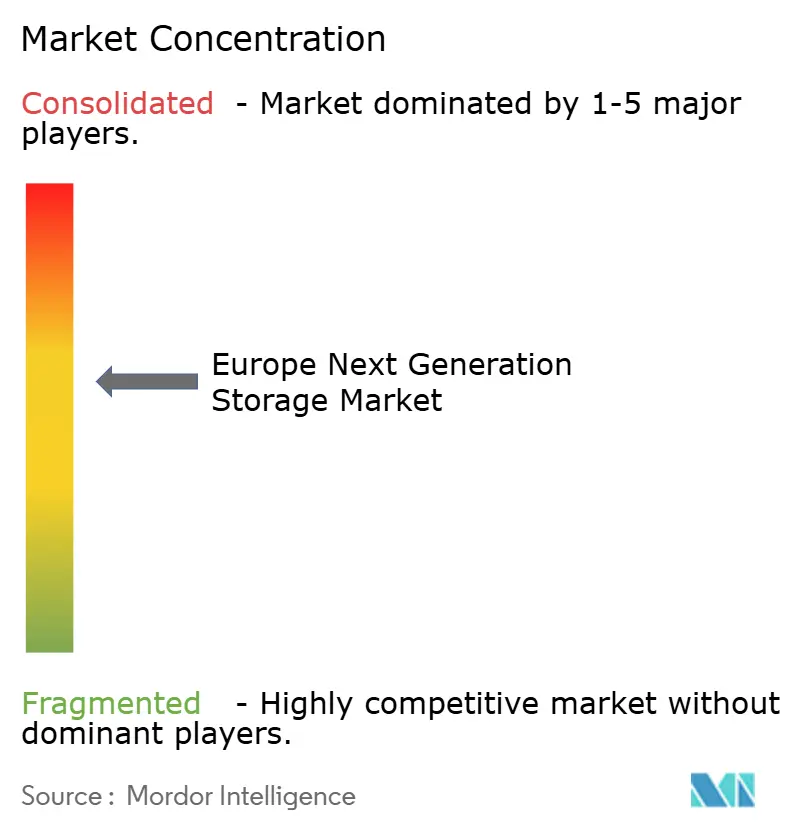

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Next Generation Storage Market Analysis by Mordor Intelligence

The Europe next generation storage market size was valued at USD 15.47 billion in 2025 and estimated to grow from USD 17.09 billion in 2026 to reach USD 28.07 billion by 2031, at a CAGR of 10.44% during the forecast period (2026-2031). Sustained growth is anchored in the EU Data Act, which comes into force in September 2025 and compels providers to enable effortless cloud switching; enterprises are therefore prioritizing portable, software-defined storage that safeguards data sovereignty. At the same time, AI training and inference workloads are multiplying storage traffic while energy-efficiency rules tighten, giving an edge to flash-based architectures that deliver low latency per watt. Capacity constraints in Frankfurt, London, Amsterdam, Paris and Dublin are pushing operators toward edge deployments, and continued investment in sovereign-cloud projects such as Gaia-X and virt8ra is stimulating demand for interoperable, vendor-agnostic platforms able to span core, cloud and edge footprints. Competitive pressure is intensifying as traditional array vendors recalibrate their portfolios to confront hyperscale cloud innovation, flash-only specialists, and European sovereign-cloud providers.

Key Report Takeaways

- By storage system, Direct-Attached Storage led with 45.02% of Europe next generation storage market share in 2025, whereas Hyper-Converged Infrastructure is projected to climb at an 11.18% CAGR through 2031.

- By storage architecture, File and Object-Based Storage held 65.05% revenue share in 2025, while Software-Defined Storage is expanding at a 11.74% CAGR to 2031.

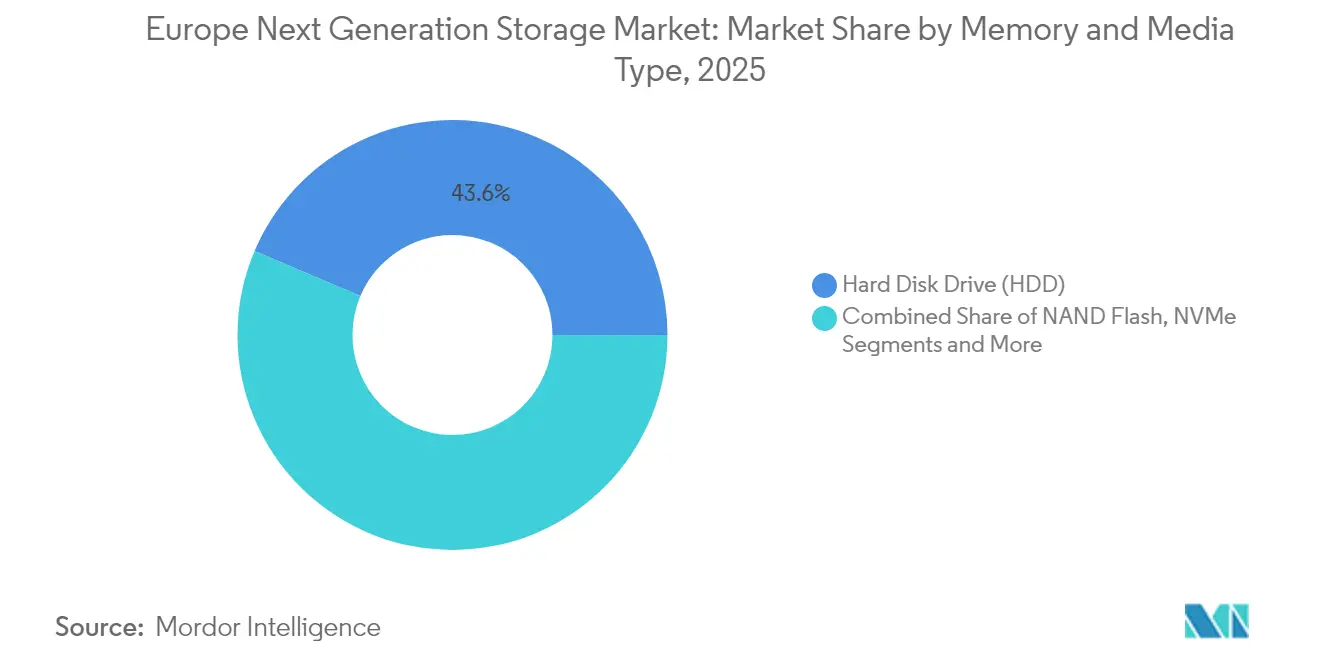

- By memory and media, Hard Disk Drives accounted for 43.62% of Europe next generation storage market size in 2025; NAND Flash is moving ahead at an 11.12% CAGR.

- By end-user industry, the IT and Telecom sector captured 25.18% revenue share in 2025; Banking, Financial Services and Insurance is accelerating at a 10.55% CAGR through 2031.

- By country, Germany contributed 39.45% revenue share in 2025, whereas the United Kingdom is outpacing peers with an 10.73% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Next Generation Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exploding volume of digital data | +2.8% | Global, with GDPR-driven concentration in EU | Long term (≥ 4 years) |

| Rapid shift to SSD and NVMe architectures | +2.1% | Germany, UK, France leading adoption | Medium term (2-4 years) |

| AI / ML workloads demanding ultra-low latency | +1.9% | Major EU data center hubs, expanding to Tier 2 cities | Short term (≤ 2 years) |

| Hybrid multi-cloud adoption across EU enterprises | +1.6% | Pan-European, strongest in financial services | Medium term (2-4 years) |

| Edge-computing and 5G micro-data-centre proliferation | +1.4% | Germany, UK, Spain leading 5G SA deployment | Long term (≥ 4 years) |

| EU Gaia-X and Data Act enabling sovereign-cloud storage | +0.8% | EU-wide, with national implementation variations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Exploding Volume of Digital Data

Global data creation is set to triple between 2023 and 2028, and local retention obligations under GDPR mean most of that growth must be stored inside EU borders. Enterprises planning for petabyte-scale capacity are therefore deploying hybrid topologies that couple on-premises arrays with sovereign-cloud extensions, ensuring compliance while keeping latency in check. Spending patterns show a marked tilt toward scalable, software-defined platforms that can ingest diverse file and object workloads without vendor lock-in. The result is a Europe next generation storage market whose expansion rate outpaces global averages as organizations attempt to blend compliance and performance within a single architecture.

Rapid Shift to SSD and NVMe Architectures

Enterprise adoption of PCIe Gen5 NVMe is eliminating the performance gap that once separated on-premises arrays from public-cloud tiers. German manufacturing plants embracing Industry 4.0 have pushed latency budgets below 100 µs, a threshold unattainable for spinning disks[1]Micron Technology, “Powering Next-Gen AI With PCIe Gen5,” micron.com. Energy efficiency is now a board-level metric; SSDs consume markedly fewer kilowatt-hours per terabyte than HDDs, helping operators meet the German Energy Efficiency Act’s 50% renewable-energy threshold for data centres set for 2027. These dynamics position flash media as a strategic rather than tactical investment across the Europe next generation storage industry.

AI / ML Workloads Demanding Ultra-Low Latency

AI training clusters in Frankfurt and Amsterdam already require more than 30 PB of high-throughput capacity, and each new generative model iteration raises I/O ratios further. Operators are therefore standardising on all-flash configurations coupled with NVMe-over-Fabric to minimise data-loading times, because up to 60% of training duration is still spent shuttling datasets instead of iterating algorithms. Government-backed AI programmes, including Germany’s EUR 1 billion commitment announced in 2025, reinforce the outlook for specialised, performance-optimised arrays that satisfy both computational and sovereignty prerequisites.

Hybrid Multi-Cloud Adoption Across EU Enterprises

Mandatory cloud portability under the EU Data Act is accelerating enterprise pivot to hybrid architectures by capping exit fees and enforcing 30-day switching windows from September 2025. Financial-services incumbents are re-architecting core banking platforms around storage-as-a-service subscriptions that can be redeployed across zones without re-ingesting data. Analysts estimate that opex services will replace more than 35% of traditional capex storage budgets by 2028 Hitachi Vantara. This policy-driven realignment places interoperable software layers at the heart of the Europe next generation storage market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of all-flash and NVMe arrays | -1.8% | Pan-European, acute in SME segment | Medium term (2-4 years) |

| Data-sovereignty compliance fragmentation across EU | -1.2% | EU-wide, varying by member state implementation | Long term (≥ 4 years) |

| Legacy workload migration and vendor lock-in risks | -0.9% | Established enterprises in Germany, UK, France | Medium term (2-4 years) |

| Rare-earth and critical-metal supply constraints for NAND/SSD | -0.7% | Global supply chain, EU manufacturing dependency | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of All-Flash and NVMe Arrays

Enterprise SSDs still carry a unit-cost premium as high as 9.9× over HDD capacity. For small and midsize firms, this delta complicates ROI calculations even when flash energy savings are factored in. Hyperscaler uptake is driving near-term price easing, but many European SMEs will continue staging workloads on hybrid tiers that mix QLC flash with high-capacity disk until flash crosses the cost-per-bit threshold.

Data-Sovereignty Compliance Fragmentation Across EU

While the Data Act aims at harmonisation, member-state transpositions introduce divergent enforcement deadlines and penalty bands. Cross-border businesses must, therefore, maintain multi-regime compliance playbooks, inflating operational overheads for storage providers that want pan-EU coverage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Storage System: Hyperconvergence Reshapes Infrastructure Deployment

Direct-Attached Storage contributed 45.02% share to Europe next generation storage market size in 2025, underscoring enterprises’ preference for predictable latency in mission-critical workloads. Hyper-Converged Infrastructure, however, is forecast to log an 11.18% CAGR, reflecting appetite for scale-out nodes that blend compute, storage and networking into a single policy domain.

Momentum toward hyperconvergence is reinforced by national digitalisation grants in Germany, where manufacturers need on-site processing to analyse sensor data without violating sovereignty rules. Dell Technologies and CoreWeave’s rack-level AI platform demonstrates how converged resources can supply 1.4 exaFLOPS alongside petabyte-scale flash, making them an attractive middle ground between monolithic arrays and purely public-cloud tiers.

By Storage Architecture: Software-Defined Solutions Drive Vendor Independence

File and Object-Based Storage captured 65.05% of Europe next generation storage market share in 2025 by delivering RESTful, scale-out repositories for unstructured datasets, from analytics logs to 8K media files. Software-Defined Storage is scaling faster at 11.74% CAGR because it uncouples services from hardware, thereby fulfilling the Data Act’s portability ethos.

European banks and insurers are piloting data-mobility orchestrators capable of live-migrating petabyte datasets between sovereign-cloud partners without disrupting transaction latency. Partnerships such as Hitachi Vantara and Hammerspace provide automated classification and movement that preserve metadata integrity, minimizing refactoring pain for legacy apps.

By Memory and Media Type: NAND Flash Acceleration Amid HDD Resilience

Hard Disk Drives still represent 43.62% of Europe next generation storage market size thanks to unmatched economics for cold data. Nonetheless, NAND Flash shipments into European data centres will grow at 11.12% CAGR, driven by AI workloads that value throughput over capacity economics.

HAMR innovations signal an HDD roadmap that remains relevant for hyperscale archives; simultaneous QLC NAND density gains are shrinking flash TCO. Pure Storage and Micron’s work on G9 QLC NAND illustrates how flash vendors tackle both density and endurance to undercut hybrid arrays on cost while surpassing them on watts per IOPS.

By End-User Industry: Financial Services Accelerate Digital Infrastructure

IT and Telecom operators held 25.18% share in 2025, retaining primacy due to constant network-function virtualisation cycles. Banking, Financial Services and Insurance is set to outpace every peer at a 10.55% CAGR, propelled by PSD3 compliance timelines and real-time fraud analytics that necessitate millisecond-level datasets.

Healthcare systems are also raising storage spend to archive high-resolution imaging and genomics workloads inside sovereign boundaries. All sectors converge on AI adoption, making low-latency, high-throughput arrays the common denominator.

Geography Analysis

Germany’s nucleus role flows from Frankfurt’s carrier-dense fabric, where cross-connect demand is pushing colocation rates to record highs. Power-allocation caps are driving operators to secondary metros such as Berlin and Munich, further expanding the geographic footprint of the Europe next generation storage market. Regulations requiring 100% renewable energy sourcing by 2027 are encouraging migration to high-density flash arrays that curtail total energy draw.

The United Kingdom’s Critical National Infrastructure designation for data centres speeds approvals for megawatt-scale builds, while the forthcoming Cyber Security and Resilience Act requires operators to meet rigorous data governance metrics. These two policies jointly spur adoption of sovereign-ready, software-defined arrays capable of rapid workload porting across domestic and EU nodes.

France blends industrial investment incentives with renewable energy goals: BSO’s DataOne campus, scaling to 400 MW by 2028, has reserved half its floor space for AI tenancy, raising immediate demand fr ultra-dense NVMe systems. Italy and Spain ride similar trajectories, aided by national cloud-first directives and solar-rich grids that allow competitive pricing of colocation footprints. Nordic territories benefit from sub-10 °C average temperatures and abundant hydropower, positioning them as cold-data repositories that can back up latency-sensitive primary stores elsewhere in the bloc.

Competitive Landscape

The Europe next generation storage market shows moderate concentration. Dell’s 29.7% global share gives it scale advantages, yet regional revenue is increasingly contested by flash-only challengers and sovereign-cloud operators. HPE’s pending acquisition of Juniper Networks (USD 14 billion) seeks to fuse edge networking and storage orchestration into a single cloud-managed fabric, a direct response to hyperscaler integrated stacks.

Pure Storage’s 22% share-price jump upon winning a top-four hyperscaler contract validates flash technology’s cost trajectory and creates a template for challengers to disrupt entrenched incumbents. NetApp’s alliances with NVIDIA and Cisco illustrate the ecosystem approach: integrating high-bandwidth interconnects, GPUs and all-flash nodes to serve AI training clusters.

European sovereign-cloud specialists differentiate on compliance tooling and transparent audit controls. Deutsche Telekom’s 8ra network is one flagship, promising sub-15 ms access across 10,000 edge nodes. Collective trends reveal three strategic vectors: incumbents layering software subscriptions atop hardware lines, flash specialists chasing AI and energy-efficiency deals, and sovereign-cloud operators leveraging policy momentum to win regulated workloads.

Europe Next Generation Storage Industry Leaders

Toshiba Corporation

Hewlett Packard Enterprise

Dell Inc.

IBM

Hitachi, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Brookfield Asset Management announced a SEK 95 billion (USD 10 billion) plan to expand Swedish AI infrastructure, lifting Strängnäs capacity to 750 MW Brookfield Asset Management.

- May 2025: BSO unveiled DataOne, set to reach 400 MW by 2028 with PUE as low as 1.06 BSO.

- January 2025: The virt8ra sovereign edge-cloud project launched with EUR 3 billion funding across six EU nations OpenNebula Systems.

- January 2025: Pure Storage and Micron deepened collaboration on G9 QLC NAND for hyperscale deployments Pure Storage.

Europe Next Generation Storage Market Report Scope

The need for greater capacity HDDs is being driven by the fact that data generation is increasing at double-digit rates annually and that cloud organizations are requesting storage space for this burgeoning data. Software-Defined Storage (SDS) feeds on the data stream. The availability of enormous amounts of data is pushing the IT industry to develop Software-Defined Storage solutions to grow in capacity and performance with ease. These solutions were created specifically for environments that use modern workloads and cloud-native applications.

Europe Next Generation Storage Market is segmented by Storage System (Direct Attached Storage (DAS), Network Attached Storage (NAS), Storage Area Network (SAN)), By Storage Architecture (File and Object-based Storage (FOBS), Block Storage), and End-user Industry (BFSI, Retail, IT and Telecom, Healthcare, Media & Entertainment, and Other) and Country.

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Storage System

| Direct-Attached Storage (DAS) |

| Network-Attached Storage (NAS) |

| Storage Area Network (SAN) |

| Hyper-Converged Infrastructure (HCI) |

| Others |

By Storage Architecture

| File and Object-Based Storage |

| Block Storage |

| Software-Defined Storage (SDS) |

By Memory and Media Type

| Hard Disk Drive (HDD) |

| NAND Flash |

| NVMe |

| 3D XPoint / Optane |

| Emerging NVM |

By End-User Industry

| BFSI |

| Retail and e-Commerce |

| IT and Telecom |

| Healthcare and Life Sciences |

| Media and Entertainment |

| Government and Defence |

| Other End-User Industries |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Storage System | Direct-Attached Storage (DAS) |

| Network-Attached Storage (NAS) | |

| Storage Area Network (SAN) | |

| Hyper-Converged Infrastructure (HCI) | |

| Others | |

| By Storage Architecture | File and Object-Based Storage |

| Block Storage | |

| Software-Defined Storage (SDS) | |

| By Memory and Media Type | Hard Disk Drive (HDD) |

| NAND Flash | |

| NVMe | |

| 3D XPoint / Optane | |

| Emerging NVM | |

| By End-User Industry | BFSI |

| Retail and e-Commerce | |

| IT and Telecom | |

| Healthcare and Life Sciences | |

| Media and Entertainment | |

| Government and Defence | |

| Other End-User Industries | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe next generation storage market in 2026?

The market is valued at USD 17.09 billion in 2026 and is projected to grow to USD 28.07 billion by 2031.

Which storage system segment is growing the fastest in Europe?

Hyper-Converged Infrastructure is expanding at an 11.18% CAGR, outpacing all other system categories through 2031.

Why is Germany the largest market within Europe?

Germany hosts more than 500 data centres, benefits from a EUR 500 billion infrastructure programme, and enforces strict data-localisation rules, giving it 39.45% market share.

What regulatory change is driving cloud portability demands?

The EU Data Act, effective September 2025, imposes cloud switching rights and fee caps, prompting enterprises to adopt portable, software-defined storage.

How are AI workloads influencing storage purchases?

AI training requires ultra-low-latency flash and NVMe media; as a result, flash adoption is accelerating at an 11.12% CAGR across European data centres.

What is the main obstacle to all-flash array deployment for SMEs?

Despite energy savings, SSDs still cost up to 9.9× more than HDDs, making initial capital outlays challenging for small and midsize enterprises.

Page last updated on: