Polyhydroxyalkanoate (PHA) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

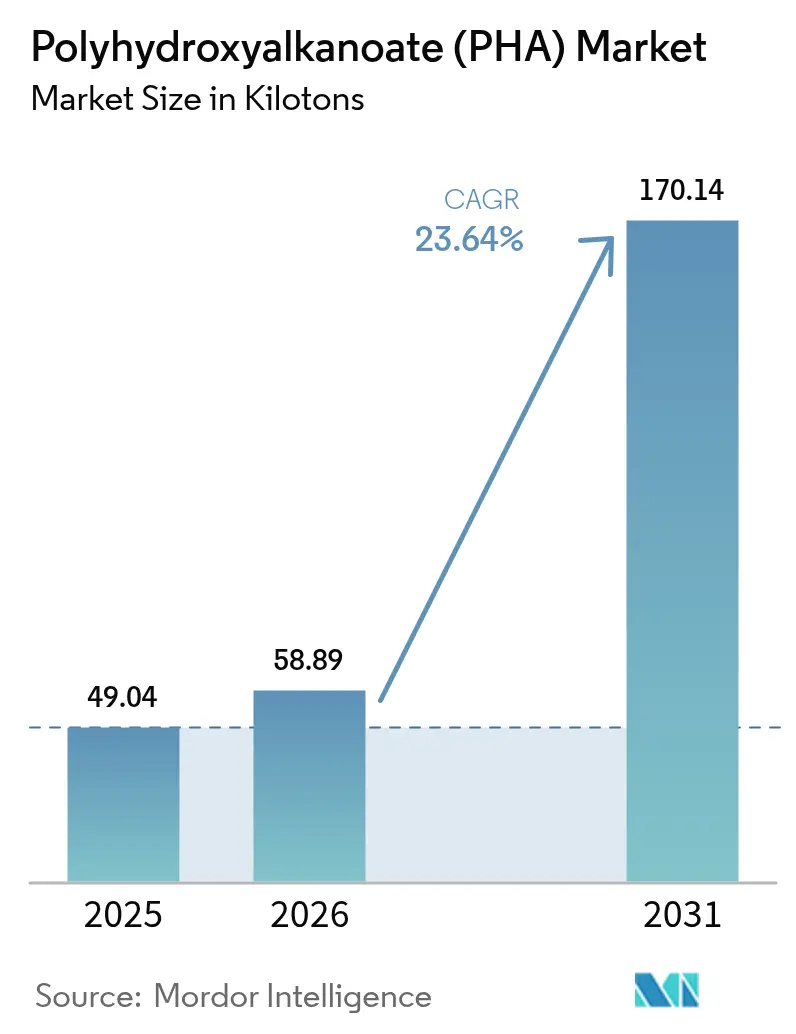

| Market Volume (2026) | 58.89 kilotons |

| Market Volume (2031) | 170.14 kilotons |

| Growth Rate (2026 - 2031) | 23.64% CAGR |

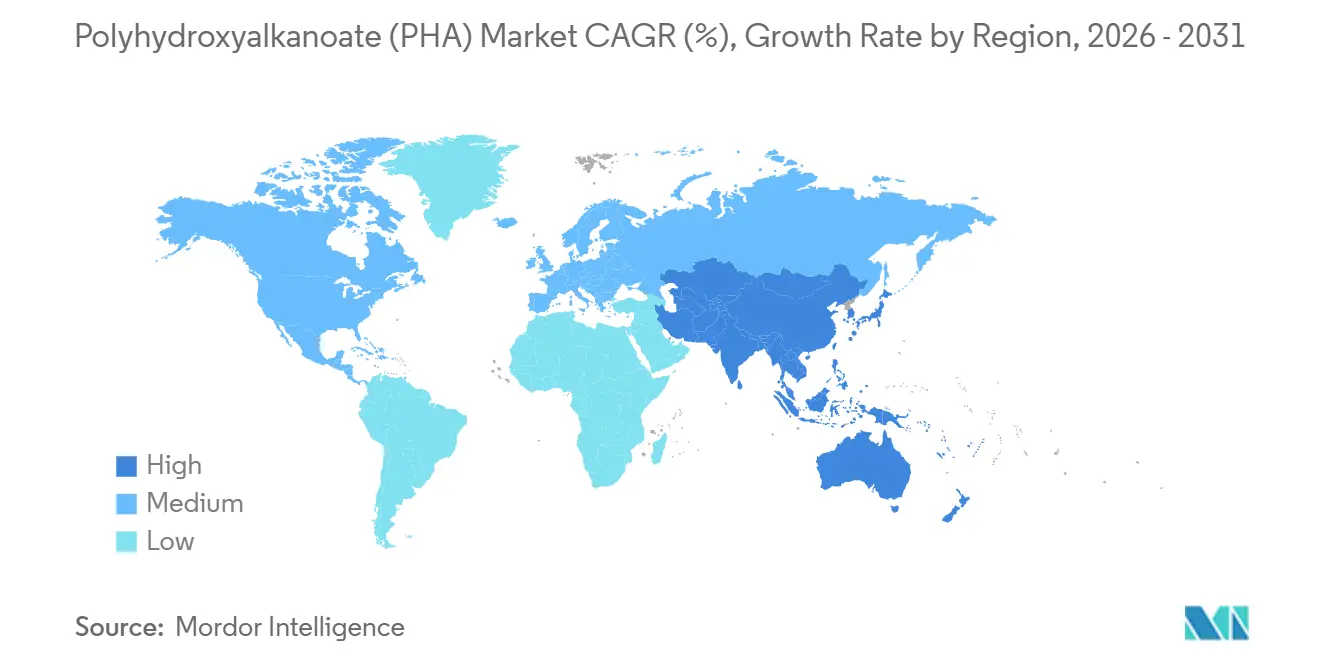

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyhydroxyalkanoate (PHA) Market Analysis by Mordor Intelligence

The Polyhydroxyalkanoate Market size is expected to increase from 49.04 kilotons in 2025 to 58.89 kilotons in 2026 and reach 170.14 kilotons by 2031, growing at a CAGR of 23.64% over 2026-2031. Rapid substitution of petroleum plastics, escalating single-use-plastic bans across Europe and Asia-Pacific, and accelerating demand for bio-resorbable medical devices are moving the Polyhydroxyalkanoates market onto a structurally steeper growth path. Brand-owner procurement commitments, especially in fast-moving consumer goods, are locking in multi-year offtake contracts that underpin capacity expansion plans, while halophilic-microbe and mixed-culture fermentation are lowering production costs and broadening feedstock flexibility. Simultaneously, a shift from sugar feedstocks toward waste oils and agricultural residues is mitigating ESG controversy over palm oil and smoothing raw-material price volatility. Competitive rivalry remains moderate: four incumbent producers jointly control nearly two-thirds of installed volume, yet face pressure from venture-backed entrants promising sub-USD 2 per kilogram costs by 2028. Scale bottlenecks outside North America and East Asia, combined with stringent medical-grade approvals, will likely keep supply tight through the medium term, supporting premium price realization.

Key Report Takeaways

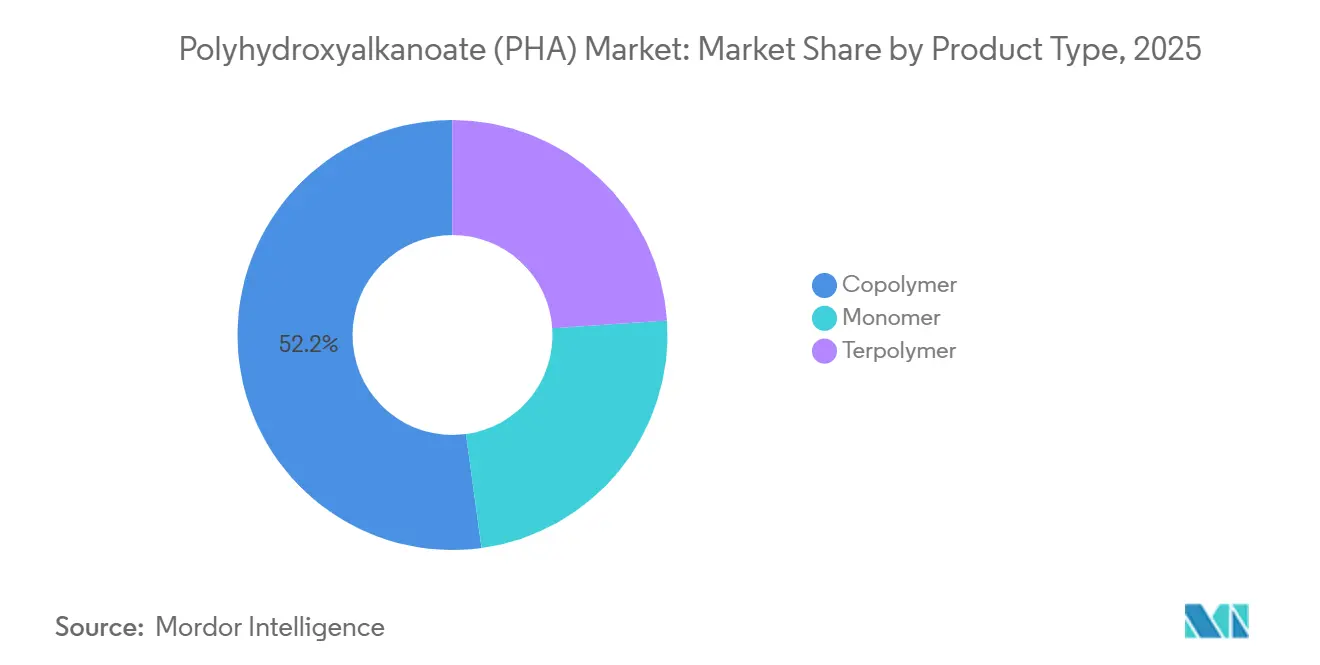

- By product type, co-polymers led with 52.15% of polyhydroxyalkanoate market share in 2025; terpolymers are forecast to advance at a 24.24% CAGR to 2031.

- By feedstock, sugar/molasses held a 57.24% share of the polyhydroxyalkanoate market size in 2025, while waste oils are estimated to record the highest projected CAGR at 24.38% through 2031.

- By production method, bacterial fermentation accounted for 77.28% of the polyhydroxyalkanoate market size in 2025; mixed microbial culture is set to expand at a 25.11% CAGR between 2026-2031.

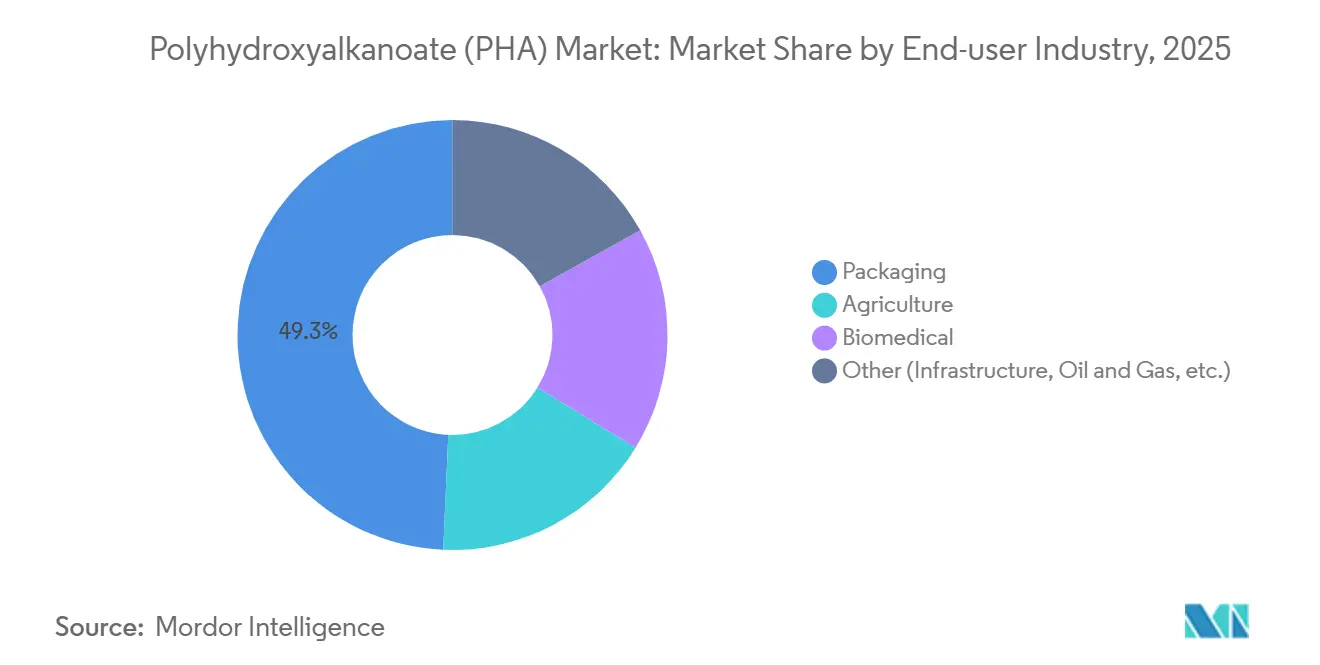

- By end-user industry, packaging captured 49.31% of the polyhydroxyalkanoate market share in 2025; biomedical uses are growing fastest at 25.22% CAGR to 2031.

- By geography, Europe commanded 44.28% of the polyhydroxyalkanoate market size in 2025, and Asia-Pacific is forecast to climb at a 24.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Polyhydroxyalkanoate (PHA) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory bans on single-use plastics | +6.2% | Europe, India, China; spill-over to North America | Medium term (2-4 years) |

| Growing demand for sustainable polymers | +5.8% | Global, strongest in Europe and North America | Long term (≥ 4 years) |

| Growing awareness over sustainability in FMCG | +4.1% | Global, led by European and North American brand owners | Medium term (2-4 years) |

| Rising demand for bio-resorbable implants | +3.9% | North America, Europe, Japan, South Korea | Long term (≥ 4 years) |

| Growing usage in agriculture | +3.2% | India, China, Mediterranean Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Bans on Single-Use Plastics Accelerating PHA Demand

The global cohort aged 65+ surpassed 761 million in 2021 and will exceed 1.5 billion by 2050, expanding orthopedic and cardiovascular device volumes. FDA clearances in 2024-2025 for PHBV sutures and bone screws validate PHA’s biocompatibility advantages, and Japan’s fast-track approvals are further boosting regional demand. Terpolymer formulations with 20-30 mol% 3-hydroxyhexanoate match cortical-bone stiffness while resorbing in 18-24 months, eliminating removal surgeries and lowering lifetime procedure costs by 15-20% for typical knee-replacement patients. Cardiovascular device makers are testing PHA scaffolds for fully bio-degradable stents, where degradation avoids late-stage thrombosis associated with metal implants, further supporting growth in the polyhydroxyalkanoates market.

Growing Demand for Sustainable Polymers

Unilever, Nestlé, and PepsiCo have pledged to eliminate virgin fossil-based plastics from packaging by 2030, catalyzing multi-year supply contracts for bio-based resins, including RWDC’s 160,000-ton offtake to Cove bottled water, the largest single PHA agreement to date. Life-cycle analyses show PHA produced from renewable oils cuts greenhouse emissions by 70-80% relative to polyethylene, allowing consumer-goods makers to report lower Scope 3 footprints under the Greenhouse Gas Protocol. Institutional investors are embedding plastic-waste metrics into ESG screens, raising the cost of capital for laggard firms and indirectly advantaging PHA suppliers. The global biodegradable-plastics segment doubled from 1.1 million tons in 2023 to an expected 2.8 million tons by 2028, and the Polyhydroxyalkanoates market is capturing a rising fraction of this pool.

Growing Awareness Over Sustainability in FMCG Sector

Ocean-plastic pollution, estimated by the United Nations at 11 million tons annually, has heightened brand-reputation risk, prompting Mars Wrigley to shift Skittles packs to Danimer’s PHA film in 2024 and Bacardi to debut PHA bottles in limited editions[2]United Nations Environment Programme, “From Pollution to Solution: A Global Assessment of Marine Litter,” unep.org. ASTM D6691 marine-degradability certification gives PHA a credible claim that resonates with eco-conscious consumers and differentiates premium snack and beverage offerings. Kimberly-Clark’s partnership with RWDC on diaper back-sheets signals early moves into hygiene products, a 40 million-ton plastic pool historically resistant to change because of performance demands. As FMCG plastic consumption exceeds 50 million tons annually, the Polyhydroxyalkanoates market has scope to capture high-margin niches even before broader cost parity is reached.

Rising Demand for Bio-Resorbable Implants Amid Aging Populations

Current PHA costs range between USD 4,000 and USD 15,000 per ton versus polyethylene at roughly USD 1,240, limiting penetration into high-volume disposable goods. Substrate expenses drive up to half the total: refined glucose and vegetable oils cost USD 500-800 per ton, compared with naphtha at under USD 400. Solvent extraction adds a further 30-50%, and traditional chloroform is now under regulatory withdrawal in Europe, requiring greener yet capital-intensive alternatives such as dimethyl carbonate. CRISPR-optimized halophilic strains, which operate without sterilization, have demonstrated pilot yields that would lower costs to USD 1.98 per kilogram, but no commercial plant has yet crossed the 10,000-ton threshold, constraining the polyhydroxyalkanoates market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price premium versus conventional polymers | -4.70% | Global, acute in price-sensitive segments (commodity packaging, agriculture) | Short term (≤ 2 years) |

| Limited large-scale production capacity and scalability issues | -3.80% | Global, concentrated in regions lacking fermentation infrastructure (South America, MEA, Southeast Asia) | Medium term (2-4 years) |

| Feed-oil ESG controversies creating feedstock-supply volatility | -3.10% | Global, with acute impact in Southeast Asia (Indonesia, Malaysia palm oil), South America (Brazilian soy), spill-over to North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Price Premium Versus Conventional Polymers

Current PHA costs range between USD 4,000 and USD 15,000 per ton versus polyethylene at roughly USD 1,240, limiting penetration into high-volume disposable goods. Substrate expenses drive up to half the total: refined glucose and vegetable oils cost USD 500-800 per ton, compared with naphtha at under USD 400. Solvent extraction adds a further 30-50%, and traditional chloroform is now under regulatory withdrawal in Europe, requiring greener yet capital-intensive alternatives such as dimethyl carbonate. CRISPR-optimized halophilic strains, which operate without sterilization, have demonstrated pilot yields that would lower costs to USD 1.98 per kilogram, but no commercial plant has yet crossed the 10,000-ton threshold, constraining the polyhydroxyalkanoates market.

Limited Large-Scale Production Capacity and Scalability Issues

Global installed capacity was under 200,000 tons in 2025, versus a 230 million-ton addressable plastics-replacement pool, suggesting a structural supply deficit for at least the next five years. Fermentation bioreactors demand CAPEX of USD 50 million for a 10,000-ton line, deterring entrants. Pure culture yields an average of 40-50% of cell dry weight, though 60-80% is needed to justify extraction. Mixed-culture pilots have hit 71.4% yield yet still show inconsistent polymer molecular weights that complicate extrusion stability. Regulatory sign-offs for food-contact and implanted-medical grades add 3-5 years to commercialization timelines, delaying supply response in the polyhydroxyalkanoates market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Co-Polymers Hold Lead While Terpolymers Accelerate

The Polyhydroxyalkanoates market recorded co-polymers at 52.15% of 2025 volume, supported by PHBV’s balance of stiffness and toughness for thermoformed cups and injection-molded cutlery. Terpolymers, though lower in absolute volume, are on a 24.24% CAGR, gaining traction in biomedical screws and flexible pouches where 3-hydroxyhexanoate incorporation raises elongation at break. Co-polymer dominance should persist through 2028, but terpolymers may eclipse monomers by 2031 on the back of device-maker demand for tailored degradation windows.

Genetic engineering is reshaping the competitive equation: CRISPR-edited Haloferax mediterranei generated 48.6 mol% 3-hydroxyvalerate in fermentation, permitting single-substrate copolymer production that trims raw-material steps. Yield10’s Camelina seed platform could shift co-polymer economics entirely; a successful 10% PHB seed line would bypass fermentation and halve energy input, a breakthrough that could push the Polyhydroxyalkanoates market toward sweeter cost parity after 2029.

By Feedstock: Sugar Remains Primary, Waste Oils Surge

Sugar and molasses sustained 57.24% of 2025 output, reflecting reliable carbohydrate supply chains and mature fermentation know-how. Waste oils are rising at a 24.38% CAGR as producers decouple from volatile edible-oil pricing and ESG palm-oil criticism. Methane capture and agricultural residue pathways remain experimental yet attract capital grants in California and the EU’s Horizon program, supporting innovation within the polyhydroxyalkanoates market.

Argentina’s vinasse-to-PHA pilot illustrates regional synergies between bioethanol and biopolymer value chains. In Europe, municipal organic-waste hubs are testing volatile-fatty-acid streams as direct inputs, potentially allowing near-zero feedstock cost scenarios that would transform unit economics.

By Production Method: Bacterial Fermentation Dominant, MMC Ascending

Bacterial fermentation generated 77.28% of the 2025 volume, thanks to decades-old process control and regulatory familiarity. Mixed microbial culture posted the fastest 25.11% CAGR by exploiting non-sterile operations that cut OPEX 20-30%. Despite this momentum, MMC shows polymer-quality variability that limits use in medical or thin-film packaging, influencing dynamics in the polyhydroxyalkanoate market.

Municipal wastewater plants in Belgium and Spain are co-locating MMC reactors to turn sludge into PHA pellets, creating a circular waste valorization loop and diverting organic solids from landfills. Bacterial fermentation maintains an edge in regulatory approvals; FDA cleared three new PHBV medical devices in 2025, all sourced from pure-culture lines at Danimer and Kaneka facilities, reinforcing growth in the polyhydroxyalkanoate market.

By End-User Industry: Packaging Leads, Biomedical Spikes

Packaging absorbed 49.31% of 2025 demand, with single-use foodservice ware and snack pouches moving first. Branded converters lock in premium SKUs to differentiate on sustainability, keeping the Polyhydroxyalkanoates market profitable even under low oil prices. Biomedical end use is climbing 25.22% CAGR and could top 15% share by 2031, buoyed by high ASPs of USD 20-50 per kilogram. Agriculture claims mid-teens share but depends on subsidy budgets in India and the EU.

Marine-degradable properties win PHA footholds in beverage closures, while orthopedic screws adopt terpolymer blends that match bone stiffness and bio-absorb within two years. Oil-and-gas pilots for drilling muds and plug abandonment are emerging niche outlets that may scale as offshore environmental rules tighten after 2027.

Geography Analysis

Europe accounted for 44.28% of the 2025 Polyhydroxyalkanoates market, propelled by the EU Packaging and Packaging Waste Regulation that forces universal recyclability or compostability by 2030. Germany, France, and Italy subsidize bioplastic procurement, while a GBP 200-per-ton U.K. tax on low-recycled-content plastic indirectly favors virgin PHA. Robust industrial-composting networks allow fast converter switchovers, giving Europe a structural lead in adoption.

Asia-Pacific, while smaller today, is forecast at the fastest 24.72% CAGR and could approach Europe’s volume by 2031. China’s GB 9685 marine-degradability rule positions domestic producers like Bluepha for rapid growth, and India’s nationwide single-use-plastic ban creates an immediate 1 million-ton demand swing. Japan and South Korea are channeling R&D funds toward medical-grade terpolymer development, indicating a higher-margin trajectory versus commodity packaging.

North America hosts the world’s largest single plant, Danimer’s 110,000-ton Bainbridge facility, making the region a net exporter even as state-level bans tighten local demand. Canada’s Clean Growth Program funds agriculture-film demos, and Mexico’s proximity to US value chains may spur cross-border PHA compounding under USMCA rules. South America and the Middle East & Africa trail, but Brazil’s sugarcane by-products and Saudi Arabia’s diversification fund hint at latent accelerants if policy frameworks mature, shaping future dynamics of the polyhydroxyalkanoate market.

Competitive Landscape

The Polyhydroxyalkanoate (PHA) market is moderately fragmented. Incumbents exploit vertically integrated fermentation-to-compounding lines and long-term offtake agreements with Mars, Bacardi, and PepsiCo. Scale economies imply looming consolidation: producers under 20,000-ton capacity may lack balance-sheet strength to weather price compressions once supply catches demand after 2029. However, niche medical and specialty-packaging suppliers can survive by focusing on terpolymer grades requiring bespoke fermentation and compounding expertise within the polyhydroxyalkanoate market.

Polyhydroxyalkanoate (PHA) Industry Leaders

Danimer Scientific

Kaneka Corporation

RWDC Industries

CJ Biomaterials, Inc.

TerraVerdae Bioworks Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: The Thuringian Institute for Textile and Plastics Research (TITK) and Polytives have completed a research project aimed at enhancing biopolymers, particularly polyhydroxyalkanoates (PHA), by using innovative additives to improve processing and material properties.

- March 2025: In a world-first breakthrough, Ecopha Biotech converted pongamia oil into polyhydroxyalkanoate (PHA). This innovation strengthened Australia’s position as a global player in sustainable PHA bioplastics and opened up new possibilities for eco-friendly packaging and industrial applications.

Global Polyhydroxyalkanoate (PHA) Market Report Scope

Polyhydroxyalkanoates (PHAs) are a family of bio-based, biodegradable, and biocompatible thermoplastic polyesters naturally produced by microorganisms (bacteria) as intracellular energy reserves, typically under nutrient-limiting conditions. They are sustainable alternatives to petroleum-based plastics, with properties ranging from brittle to elastic, suitable for packaging, agricultural, and biomedical applications.

The Polyhydroxyalkanoate (PHA) market is segmented by type, feedstock, production method, end-user industry, and geography. By type, the market is segmented into monomer, copolymer, and terpolymer. By feedstock, the market is segmented into sugar/molasses, plant oils and fatty acids, waste oils and glycerol, methane/CO2, and agricultural and food waste. By production method, the market is segmented into bacterial fermentation, mixed microbial culture, and engineered plants/algae. By end-user industry, the market is segmented into packaging, agriculture, biomedical, and other (infrastructure, oil and gas, and more). The report also covers the size and forecasts for the Polyhydroxyalkanoate (PHA) market in 15 countries across major regions. Each segment's market sizing and forecasts are based on volume (tons).

| Monomer |

| Copolymer |

| Terpolymer |

| Sugar / Molasses |

| Plant Oils & Fatty Acids |

| Waste Oils & Glycerol |

| Methane / CO₂ |

| Agricultural & Food Waste |

| Bacterial Fermentation |

| Mixed Microbial Culture |

| Engineered Plants / Algae |

| Packaging |

| Agriculture |

| Biomedical |

| Other (Infrastructure, Oil and Gas, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Monomer | |

| Copolymer | ||

| Terpolymer | ||

| By Feedstock | Sugar / Molasses | |

| Plant Oils & Fatty Acids | ||

| Waste Oils & Glycerol | ||

| Methane / CO₂ | ||

| Agricultural & Food Waste | ||

| By Production Method | Bacterial Fermentation | |

| Mixed Microbial Culture | ||

| Engineered Plants / Algae | ||

| By End-user Industry | Packaging | |

| Agriculture | ||

| Biomedical | ||

| Other (Infrastructure, Oil and Gas, etc.) | ||

| Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How fast is the Polyhydroxyalkanoates market expected to grow between 2026 and 2031?

Global demand is projected to increase at a 23.64% CAGR, scaling from 58.89 kilotons in 2026 to 170.14 kilotons by 2031.

Which application currently consumes the largest share of PHA volume?

Packaging leads with 49.31% of 2025 volume, spanning rigid containers, flexible films, and foam cushioning.

What factors are bringing down the cost of PHA resins?

Shifting to waste-oil feedstocks and deploying halophilic or mixed-culture fermentation cuts substrate and sterilization costs, with pilot lines demonstrating sub-USD 2 per kilogram potential.

Which region is forecast to register the fastest demand growth through 2031?

Asia-Pacific is set to post a 24.72% CAGR, propelled by China’s marine-degradability standard and India’s nationwide single-use-plastic ban.

How concentrated is current global PHA production capacity?

About 65% of installed volume sits with Danimer Scientific, Kaneka, CJ CheilJedang, and RWDC Industries, giving the segment a moderate concentration score of 6.

Page last updated on: