Polyolefin (PO) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

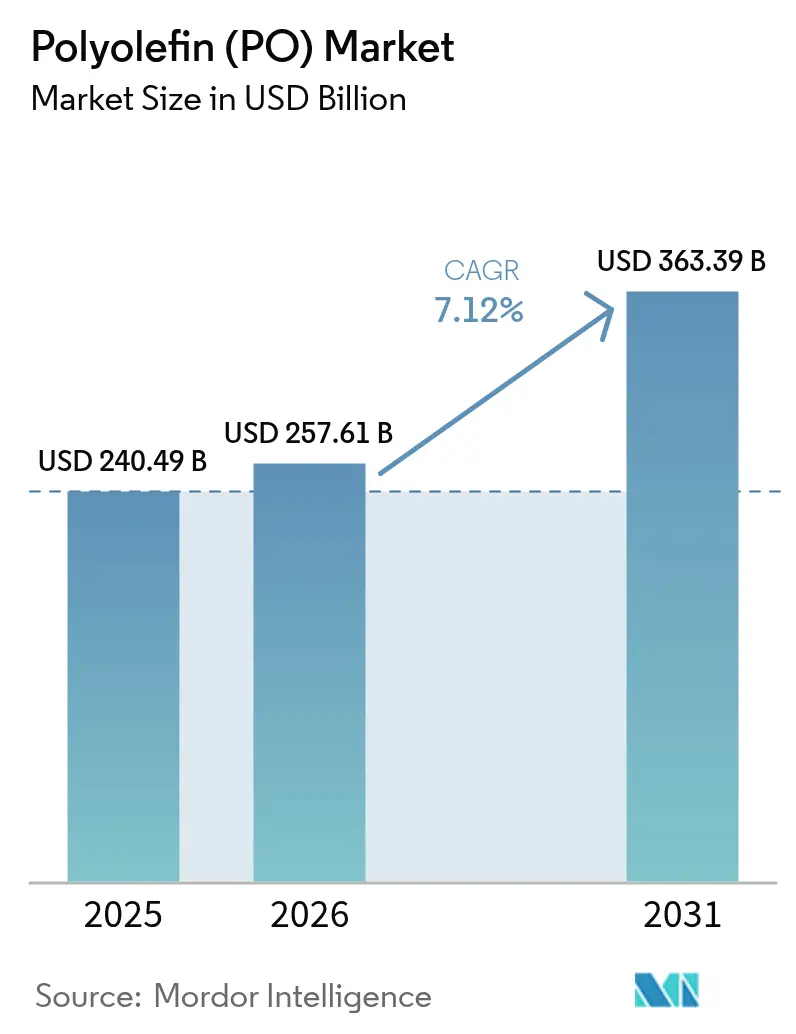

| Market Size (2026) | USD 257.61 Billion |

| Market Size (2031) | USD 363.39 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

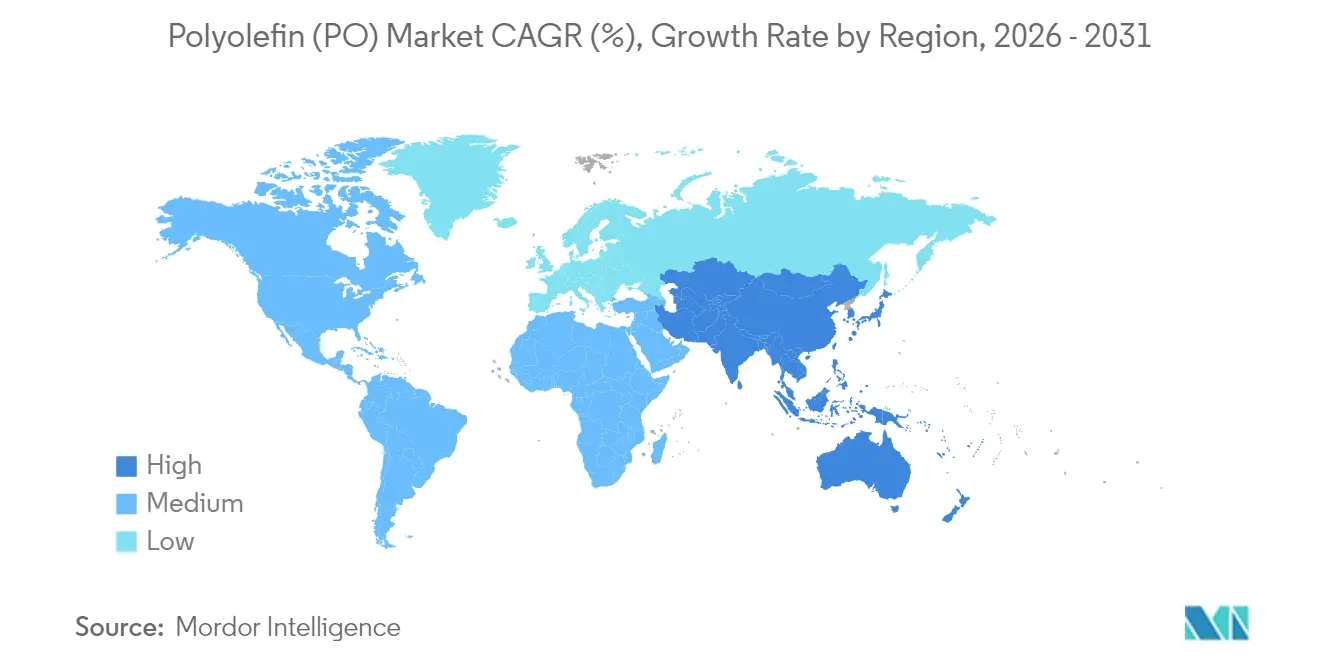

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyolefin (PO) Market Analysis by Mordor Intelligence

The Polyolefin market size is expected to grow from USD 240.49 billion in 2025 to USD 257.61 billion in 2026 and is forecast to reach USD 363.39 billion by 2031 at 7.12% CAGR over 2026-2031. Strong offtake from packaging, expanding automotive lightweighting programs, and specialty‐grade innovation underpin the trajectory despite margin pressure and regulatory disruption. Asia-Pacific anchors demand, commanding more than half of global consumption in 2024 and maintaining the quickest regional advance through 2030. Within materials, polyethylene keeps a numerical lead, yet polypropylene’s faster growth signals a portfolio pivot toward higher-performance compounds specified by car makers and appliance OEMs. Commercializing metallocene catalysts, rising chemical-recycling capacity, and escalating circular-economy mandates further shape competitive priorities across the polyolefin market.

Key Report Takeaways

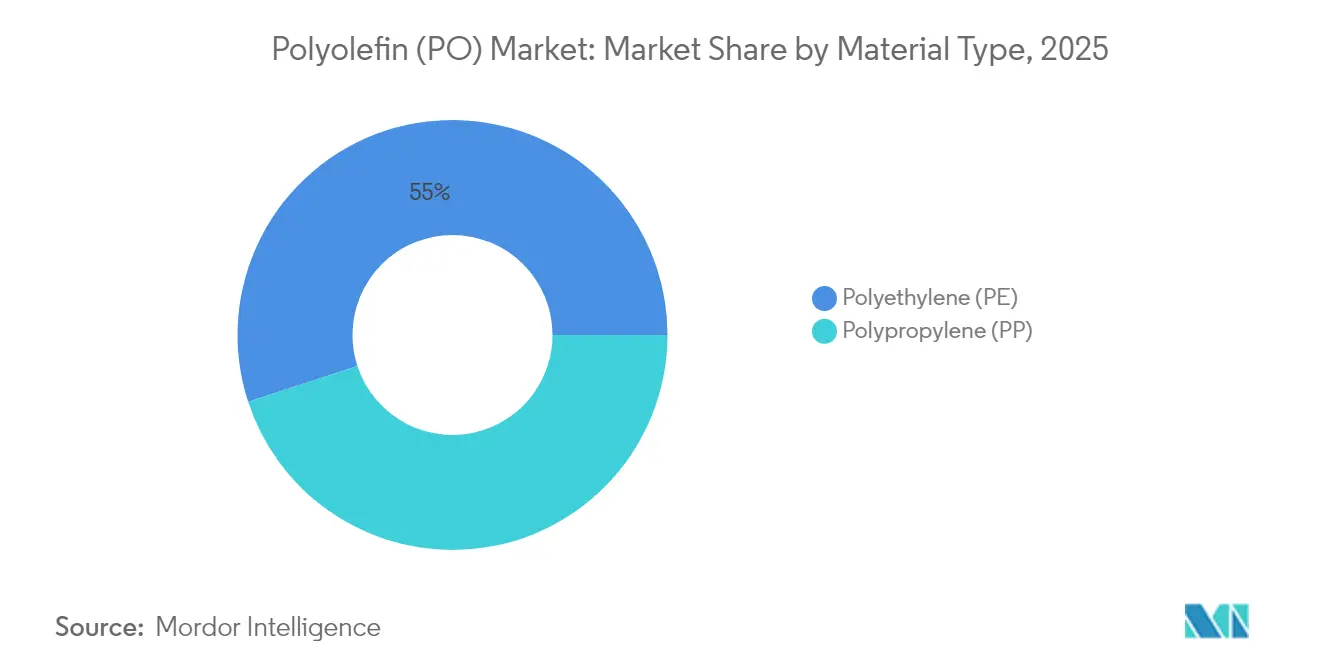

- By material type, polyethylene led with 55.02% Polyolefin market share in 2025, whereas polypropylene is projected to book the fastest 8.02% CAGR through 2031.

- By application, films and sheets held 36.05% of the Polyolefin market size in 2025, while fibers and raffia are forecast to expand at an 7.86% CAGR during 2026-2031.

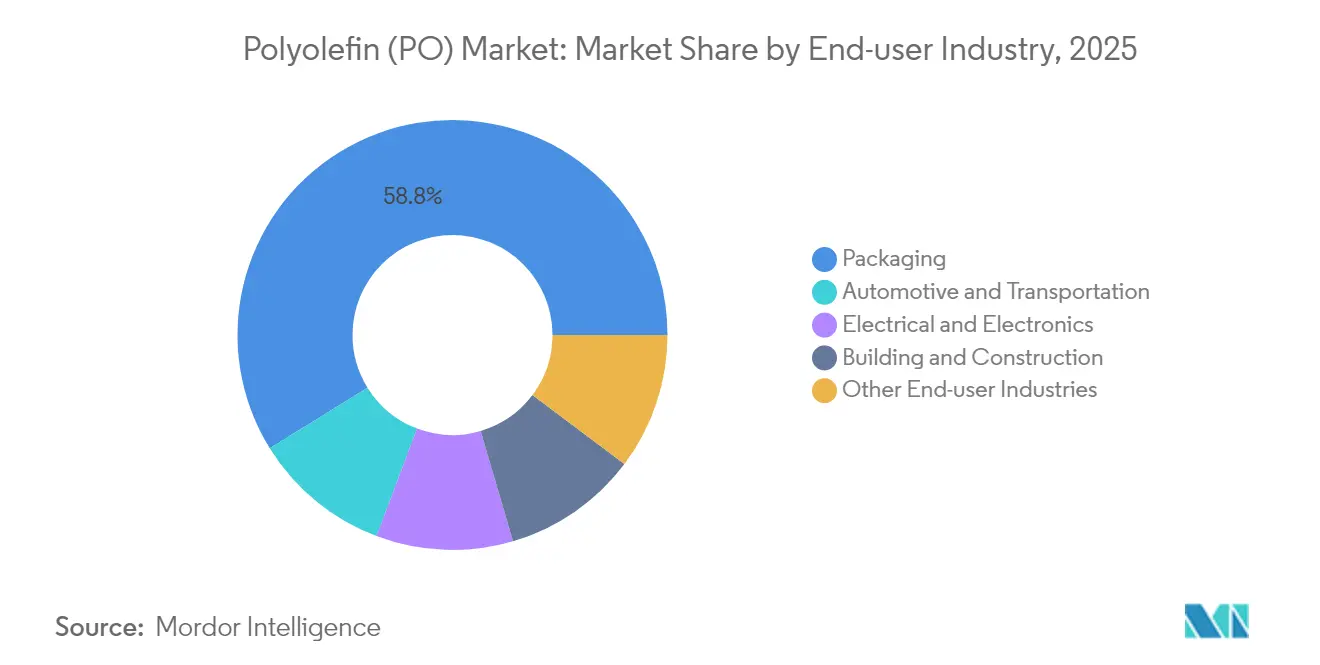

- By end user, packaging captured 58.83% of the Polyolefin market in 2025 and is tracking an 7.95% CAGR to 2031.

- By geography, Asia-Pacific accounted for 51.22 % of the Polyolefin market share in 2025 and posts the quickest 8.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Polyolefin (PO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift from Rigid to Flexible Packaging | +1.8% | Global with APAC & North America leadership | Medium term (2-4 years) |

| Demand for Cost-efficient Interior and Consumer Goods | +1.2% | APAC core, spill-over Latin America & MEA | Short term (≤ 2 years) |

| Circular-economy Mandates Driving Chemical-recycling Grades | +1.5% | Europe & North America, expanding to APAC | Long term (≥ 4 years) |

| Surging EV Lightweighting Needs for PP/POE Compounds | +1.9% | China, United States, Germany hubs | Medium term (2-4 years) |

| Metallocene-catalyst Boom Enabling Specialty PE/PP Grades | +1.1% | United States, Europe, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift from Rigid to Flexible Packaging

Brand owners migrate to lighter, flexible solutions that meet barrier targets while cutting logistics costs, a shift translating into larger film resin requirements across the polyolefin market. Flexible formats use up to 70% less material than legacy rigid containers, trimming freight emissions and warehouse space. Supply-chain disruptions in 2024 showed that mono-polyethylene pouches travel more efficiently than glass or metal options, ensuring on-shelf availability even during port congestion. Film converters now layer nano-barrier coatings on linear-low-density grades, matching shelf life once available only from multilayer laminates. EU-level design-for-recycling criteria due by 2028 favor these mono-material structures and will accelerate the replacement cycle[1]European Commission, “Packaging and Packaging Waste Regulation: Final Legislative Text,” Europa.eu.

Demand for Cost-efficient Interior and Consumer Goods

Middle-income households in India, Indonesia, and Vietnam increasingly opt for polypropylene furniture and appliance casings that deliver acceptable durability at one-third the cost of engineering plastics. OEMs reduce molding cycle time thanks to the polymer’s broad processing window, cutting electricity consumption in factories strained by high power tariffs. Automotive suppliers are also swapping glass-fiber reinforced ABS parts with impact-modified polyolefin blends for door panels, shaving vehicle mass without expensive carbon composites. The development pipeline further includes talc-filled random-copolymer grades that withstand UV exposure, making them suitable for outdoor consumer goods.

Circular-economy Mandates Driving Chemical-recycling Grades

Europe’s Packaging and Packaging Waste Regulation requires 30% post-consumer recycled content in plastic formats by 2030, compelling brands to secure chemically recycled feedstock to pass food-contact protocols. LyondellBasell’s MoReTec facility entering construction in Germany aims for virgin-equivalent output, positioning the company to monetize premium recycled PE and PP that command 20-30% higher prices. US supermarkets have trialed chemically recycled polyethylene trays for ready meals, proving scalability beyond niche pilot projects. Resin producers expect recycled-content premiums to offset higher depreciation tied to pyrolysis units and solvent cleaning trains.

Surging EV Lightweighting Needs for PP/POE Compounds

Battery enclosures, under-hood ducts, and front-end modules now specify mineral-filled polypropylene compounds that cut weight 25% relative to aluminum. Chinese new-energy vehicle makers adopted polypropylene-based rocker panels in 2024 to meet road-spray abrasion standards while simplifying recycling at end-of-life. European OEMs (original equipment manufacturers) collaborated with compounders on polyolefin elastomer blends that remain dimensionally stable from −40 °C to 90 °C, important for pack cooling plates. As unit battery costs drop, manufacturers refocus on trimming body mass, placing the polyolefin market in pole position for volume growth.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter Single-use-plastic and Carbon-tax Regulations | −0.9% | Europe, selective U.S. states | Short term (≤ 2 years) |

| Global Oversupply and Margin Pressure from Mega-crackers | −1.3% | Worldwide, acute in Europe & North America | Medium term (2-4 years) |

| Volatility in Naphtha/propane Feedstock Prices | −0.8% | Asia naphtha, North America propane pools | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter Single-use-plastic and Carbon-tax Regulations

The EU bans lightweight produce bags under 1.5 kg beginning in 2030, eliminating a 0.8 million-tonne demand stream for polyethylene film. Simultaneously, carbon levies lift cash costs at European crackers by USD 75 per tonne ethylene equivalent, compressing netbacks relative to exporters from tax-lighter regions. Producers pivot to closed-loop packaging with 35% recycled content to retain retail shelves, yet volumes lost in banned skews take time to replace. Some film converters relocate slit-roll finishing to Turkey and Egypt to avoid levy exposure, altering trade flows within the Polyolefin market.

Global Oversupply and Margin Pressure from Mega-crackers

Capacity additions in the United Arab Emirates, Qatar, and China raised the global ethylene nameplate 14 million tonnes between 2023 and 2025, outpacing polymer demand. Utilization at Europe’s smallest furnaces dipped below 65%, prompting LyondellBasell to review six assets across five countries. Feedstock-rich producers leverage discount ethane and propane to push exports, forcing high-cost naphtha players to rationalize or convert to specialty output. Analysts project that at least 10 million tonnes of further capacity must exit to restore a balanced polyolefin market by 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Polyethylene Dominance Faces Polypropylene Upswing

Polyethylene accounted for 55.02 of % Polyolefin market share in 2025, thanks to its entrenched role in packaging, construction, and agriculture. Yet polypropylene is forecast to post an 8.02% CAGR, meaning its slice of the polyolefin market size will expand meaningfully by 2031. Linear-low-density variants prosper as converters of down-gauge film, while high-density grades serve detergent bottles and corrosion-resistant pipes demanded by the water infrastructure boom across India. Low-density polyethylene faces design-for-recycling pressure, but maintains a foothold in extrusion-coating for liquid cartons.

Metallocene innovations enable ultra-thin cast films and high-stiffness polypropylene random copolymers that approach polycarbonate clarity. These grades unlock stretching and thermoforming latitude, helping brand owners migrate from polystyrene and PVC. Automakers specify long-glass polypropylene for front-end carriers, broadening revenue for compounders beyond traditional bumper fascia as chemical-recycling feedstock supply scales, polyethylene and polypropylene producers aim to certify grades with 50% circular content, reinforcing customer loyalty and protecting share in the polyolefin market.

By Application: Films Rule Volume, Fibers Accelerate Gains

Films and sheets comprised 36.05% of 2025 sales, cementing the application’s pole position within the polyolefin market. High-clarity snack pouches, bread bags, and collation shrink dominate consumption in mature regions, while agricultural mulch and greenhouse films propel volume in India and Mexico. Blow-molded HDPE (High-Density Polyethylene) jerry-cans serve industrial lubricants, and extrusion-coated paper cups rely on LDPE (Low-Density Polyethylene) moisture barriers.

Fibers and raffia log the fastest 7.86% CAGR through 2031, stimulated by woven polypropylene sacks for grain logistics and FIBC (Flexible Intermediate Bulk Container) bulk bags leveraged in e-commerce warehousing. Non-woven polypropylene shows rising penetration in hygiene applications as demographics boost adult incontinence product uptake. Injection-molded bins, crates, and thin-wall containers tap impact-copolymer polypropylene that marries toughness with flow, keeping cycle times low even on legacy presses. The end-use diversification insulates the polyolefin market from cyclical shocks, strengthening its aggregate resilience.

By End-user Industry: Packaging Leads Both Scale and Growth

Packaging captured 58.83% revenue in 2025 and will continue to dominate, not merely for food pouches but across healthcare blister packs and closure liners. Circular-economy policies amplify that dominance because mono-material solutions featuring polyethylene or polypropylene are easier to recycle than foil-laminate or Polyethylene Terephthalate (PET)-laminated bottles. The EU’s 2030 target for 30% recycled content in polyolefin formats reinforces high-volume takeaway in the polyolefin market.

Automotive retains a mid-single-digit share yet posts outsized growth from EV platform launches that embrace lightweight polypropylene compounds. Electrical and electronics buyers adopt halogen-free flame-retardant polypropylene for appliance housings, while construction contractors specify HDPE conduit and geomembranes for potable-water projects. Collectively, these segments diversify revenue and buffer the industry from packaging-centric regulation shocks.

Geography Analysis

Asia-Pacific commanded 51.22% polyolefin market share in 2025 and is tracking an 8.21% CAGR through 2031. China’s modernization of logistics packaging, India’s infrastructure push, and ASEAN’s consumer boom all funnel incremental demand. Integrated refining-to-chemicals sites grant low conversion cost, but sustainability measures—such as China’s 2026 cap on virgin-plastic consumption—will influence future capacity choices.

North America is the second-largest slice because of abundant shale-based ethane that yields cost-advantaged polyethylene. Regional demand rose 7% for polyethylene and 4% for polypropylene in 2024 due to e-commerce fulfillment and recovering durable goods orders. Resin exports from the Gulf Coast cushion producers during domestic slowdowns, though Panama Canal congestion reroutes cargo via U.S. East Coast ports, stretching transit times.

Europe wrestles with energy costs triple those in the U.S. following gas market upheaval. Nonetheless, early adoption of chemical-recycling technology positions the bloc at the forefront of circular polymer commerce. Producers pivot toward higher-margin specialty grades and service contracts with brand owners seeking traceable recycled content. The Middle East leverages a 15% rise in gas output since 2020 to supply competitively priced resin into Asia and Africa, while South America’s import reliance keeps local prices high, incentivizing Brazilian investments in new steam crackers.

Mordor Intelligence provides coverage of the polyolefin (po) market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns.

Regulatory Landscape

Circular economy and product stewardship rules are tightening around polyolefin packaging and logistics losses, with the European Union providing the most concrete near-term compliance anchors. The EU Packaging and Packaging Waste Regulation (PPWR, Regulation (EU) 2025/40) entered into force on 11 February 2025 and applies from 12 August 2026, introducing recyclability performance expectations and recycled-content obligations that affect PE and PP used in films, rigid packaging, and closures. Alongside packaging rules, Regulation (EU) 2025/2365 on preventing plastic pellet losses adds operational controls for large pellet-handling enterprises (>= 1,500 tonnes/year) with staged compliance deadlines (17 December 2027 for large enterprises; 17 December 2028 for medium-sized enterprises), pushing producers and converters to formalize containment, monitoring, and training programs.

Food-contact compliance is also being updated, shaping additive choices and qualification pathways for recycled and mass-balance materials in sensitive packaging applications. Commission Regulation (EU) 2025/351 restricts placing non-compliant plastic food contact materials on the market after 16 December 2025, with sell-through for existing stocks until 16 September 2026, narrowing the transition window for resin and masterbatch suppliers. In 2026, additional EU actions include Regulations (EU) 2026/245 and (EU) 2026/250 revising and clarifying food contact requirements, and Commission Implementing Decision (EU) 2026/1425 (30 June 2026) establishing rules for calculating, verifying, and reporting recycled plastic content, including mass balance accounting in defined cases, which raises documentation and chain-of-custody demands for polyolefin supply chains serving consumer packaging.

Value Chain Analysis

The polyolefin value chain begins with hydrocarbon feedstocks (naphtha, ethane, propane) converted into olefins (ethylene, propylene) via steam cracking or on-purpose propylene routes, then polymerized into polyethylene (HDPE, LDPE, LLDPE) and polypropylene, followed by compounding, conversion, and distribution. New integrated capacity continues to be built around advantaged feedstock and large downstream demand pools, for example ExxonMobil commencing operations at its Huizhou complex in China (including a 1.6 million tpy ethylene cracker and 1.2 million tpy LLDPE) and Formosa Plastics commissioning a 550 million pound-per-year polypropylene reactor at Point Comfort, Texas. BASF also reached mechanical completion of a 500,000 t/y polyethylene plant at its Zhanjiang integrated base in China, reinforcing how large integrated sites support supply reliability and broaden product slate coverage.

Downstream converters (films and sheets, injection molders, blow molders, fibers and raffia producers) increasingly require specialty grades and certified circular inputs, pulling recycling and certification deeper into the core chain rather than keeping it as an adjunct. Corporate collaborations reflect this shift, including Borealis and Borouge working with partners on an integrated circular waste management and polyolefin recycling ecosystem in Indonesia, and LyondellBasell partnering with Mondelez International and Amcor to supply CirculenRevive polymers into branded flexible packaging. On technology, scaling recycling routes beyond mechanical processing is emerging as a value-chain lever, with KBR and ReVentas partnering to scale polymer dissolution technology to recycle polyethylene and polypropylene, and PureCycle and Mitsui partnering with RM TOHCELLO to introduce recycled polypropylene into BOPP film applications in Japan, linking advanced recycling output to high-volume flexible packaging end uses.

Competitive Landscape

The Polyolefin Market is fragmented. Petrochemical majors with integrated feedstock chains—ExxonMobil, SABIC, and Sinopec—defend margins better than standalone polymerizers vulnerable to naphtha swings. Technology capabilities increasingly separate leaders from laggards. Companies with metallocene licenses, advanced recycling platforms, and application-development centers for EV and medical packaging win specification slots that deliver price premiums. Producers willing to co-invest in sorting lines or operate take-back schemes secure off-take commitments in exchange for locked pricing formulas. Consequently, relationship-driven business models complement scale advantages, creating a multifaceted rivalry matrix within the polyolefin market.

Polyolefin (PO) Industry Leaders

SABIC

China Petrochemical Corporation

LyondellBasell Industries Holdings B.V.

Dow

ExxonMobil Corportation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear white-space area is premium, regulation-aligned polyolefin packaging that combines design-for-recycling with auditable recycled-content accounting. The EU PPWR (Regulation (EU) 2025/40) applies from 12 August 2026, and Commission Implementing Decision (EU) 2026/1425 (30 June 2026) sets calculation and reporting rules for recycled plastic content, including defined mass balance approaches. This raises demand for traceable circular PE and PP, and for suppliers that can provide documentation-ready grades. Commercial activity already targets branded flexible packaging conversions, including LyondellBasell, Mondelez International, and Amcor collaborating on CirculenRevive polymers for Marabou chocolate bar packaging, and PureCycle and Mitsui partnering with RM TOHCELLO to bring recycled polypropylene into BOPP film applications in Japan.

Another opportunity cluster involves higher-performance and infrastructure-linked polyolefins, where producers are expanding capacity and upgrading product slates for power, construction, and industrial markets. Borouge announced delivery of the first batch of cross-linkable polyethylene (XLPE) from a 100,000 tpy expansion, aligning with demand for durable cable and energy-related applications. Capacity additions and new complexes also reshape regional sourcing options and trade flows, including Tasnee completing a USD 500 million expansion at the Saudi Ethylene and Polyethylene Company cracker (raising olefins output by 18%) and large projects progressing in Central Asia, such as equipment arrivals for the 1.25 million tpy polyethylene project in Atyrau operated by Silleno. These moves create room for compounders and converters to qualify new local supply, diversify feedstock exposure, and secure specialty grades needed for films, automotive lightweighting compounds, and infrastructure applications.

Recent Industry Developments

- July 2026: PureCycle and Mitsui announced a strategic partnership with RM TOHCELLO to introduce recycled polypropylene into biaxially oriented polypropylene (BOPP) film applications in Japan. The collaboration connects advanced recycling supply to high-volume flexible packaging, helping converters qualify recycled-content structures while maintaining performance needs.

- June 2025: LyondellBasell signed an agreement with SHCCIG Yulin Chemical Co., Ltd. to license four polyolefin technologies for a new petrochemical complex in Yulin City, China, covering two polypropylene plants and a high-density polyethylene plant. The technology package strengthens the competitive role of licensed process routes in enabling differentiated PE and PP grades at scale in Asia.

- October 2024: LyondellBasell started up a second polypropylene compounding production line with 20,000 tonnes of annual capacity at its Dalian site in China. Adding local compounding capacity improves responsiveness to OEM qualification cycles and supports growth in higher-value PP compounds used in packaging and durable goods.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of polyolefin resins sold into downstream processing, mainly polyethylene and polypropylene, across major end-use manufacturing and packaging demand. We size the market in USD terms, using consistent conversion and timing assumptions across regions.

Scope exclusions: It excludes finished plastic products and parts, as well as non-polyolefin polymers that may be used as substitutes in similar applications.

Segmentation Overview

- By Material Type

- Polyethylene (PE)

- High-Density PE (HDPE)

- Low-Density PE (LDPE)

- Linear Low-Density PE (LLDPE)

- Polypropylene (PP)

- Polyethylene (PE)

- By Application

- Films and Sheets

- Injection Molding

- Blow Molding

- Extrusion Coating

- Fibers and Raffia

- End-user Industry

- Packaging

- Automotive and Transportation

- Electrical and Electronics

- Building and Construction

- Other End-user Industries

- Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to build the backbone of the market model, especially for resin supply, trade flows, and demand indicators that can be checked across geographies. We rely on public and official sources such as national statistics offices, customs and tariff databases, energy and petrochemicals agencies, and trade bodies that publish plastics and packaging indicators. Peer reviewed journal articles and patent databases are also screened to track technology shifts that can change product mix and pricing behavior.

Along with that, we review company annual reports, investor presentations, and plant level announcements to map capacity additions, shutdowns, and feedstock constraints that affect resin availability. In a few places, paid subscriptions for company financials and intelligence, shipment level import-export records, and patent analytics are used to speed up cross checks and to close gaps where public disclosures are thin. The specific sources listed above are illustrative only, and many other references were also used for data collection, clarification, and validation.

Primary Interviews and Surveys

Primary work is used to pressure test the desk assumptions and to convert broad indicators into sizing inputs that reflect real buying and selling behavior. We spoke with a mix of resin producers, compounders, distributors, converters, and large end users, and then used follow ups to confirm regional pricing ranges, contract versus spot split, and near term demand sentiment across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 17% | APAC: 46% |

| Mid tier: 46% | Functional/Unit leaders: 27% | EMEA: 36% |

| Smaller Players: 20% | Managers: 56% | Americas: 18% |

Market-Sizing & Forecasting

The core sizing starts with a top-down build where production, capacity utilization, and trade data are used to reconstruct the available resin pool by region, which is then aligned to end-use conversion demand. This is checked through selective bottom-up approximations such as sampled price per ton ranges multiplied by estimated resin volumes in packaging, building and construction, automotive plastics, and consumer goods, and then adjusted when the two views do not line up.

Key inputs used in the model include polyolefin capacity additions and shutdowns, operating rates, net import and export balance, feedstock and energy cost direction (which influences resin pricing), packaging demand signals, and substitution intensity between polyethylene and polypropylene in major applications. Where bottom-up data is incomplete, gaps are handled using conservative penetration assumptions validated in interviews, followed by sensitivity checks on price and volume bands.

For forecasting, we primarily use scenario analysis tied to macro and industry drivers, and then refine the curve with exponential smoothing on historical demand indicators to avoid sharp jumps. Final growth paths are reviewed against expert views on the timing of new capacity, expected run rates, and the outlook for high-volume end uses like flexible packaging and rigid containers.

Data Validation & Update Cycle

Outputs are validated through triangulation across supply side signals, trade balances, and demand side indicators, and then reviewed for year-on-year breaks that do not match known industry events. When a variance shows up, we recheck unit conversions, currency timing, and pricing assumptions, and then return to interview notes or re-contact sources if the gap is still not explainable.

Before sign-off, a second analyst reviews the model logic, the input ranges, and the way assumptions were applied across regions, and then flags any outliers for correction. Reports are refreshed annually, and interim updates are made when material events occur such as major plant outages, large new capacity starts, or policy changes affecting plastics demand. Right before delivery, a final pass is done so clients receive the latest updated view.

Mordor Intelligence's Polyolefin Market Size Versus Other Published Estimates

It is normal to see different polyolefin market sizes across publications, even when the topic name looks the same. The gaps usually come from what is counted as polyolefin, what year is treated as the current value, and whether pricing is modeled as contract-led, spot-led, or a blended view.

By tracking capacity utilization, net trade balance, and resin pricing bands by region, Mordor Intelligence keeps the 2026 total tied to the resin demand pool rather than mixing in finished plastic product revenues, which some sources implicitly do. Differences also show up when one estimate anchors on a 2024 or 2025 base year and then applies a single global growth rate, while another uses region-level supply additions and feedstock driven price movement that changes the value trajectory.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 257.61 B (2026) | |

| Global Consultancy A | USD 262.71 B (2024) | Uses an earlier base year and a shorter horizon, and the value can shift if resin price progression is treated as a smoother global curve rather than region-specific bands tied to feedstock and operating rates. |

| Industry Publisher B | USD 284.40 B (2025) | Anchors the market on a later base year, and the step-up is sensitive to how contract versus spot pricing is blended and whether certain polyolefin-like materials are grouped alongside core PE and PP. |

Seen together, the spread is mainly explained by base-year selection and what is included around the core resin scope, followed by the way pricing is carried forward. Our approach stays traceable because each region is linked back to measurable supply and trade signals, and the final value is cross-checked with interview-led price and demand ranges before forecasting is applied.

Key Questions Answered in the Report

What is the current global value of the Polyolefin market and how fast is it expanding?

Global revenue reached USD 257.61 billion in 2026 and is projected to climb to USD 363.39 billion by 2031, reflecting a 7.12% CAGR.

Which region contributes the largest share of polyolefin demand today?

Asia-Pacific commands 51.22% of global consumption, led by China’s packaging and infrastructure requirements.

Why is packaging expected to remain the top-consuming end use for polyolefins?

Packaging already accounts for 58.83% of 2025 sales and continues to grow because flexible mono-material formats align with circular-economy mandates and deliver logistics savings.

Which application segment is recording the quickest volume growth?

Fibers and raffia show the fastest advance at an 7.86% CAGR through 2031, supported by woven sacks, non-woven hygiene products, and bulk-bag logistics.

How are electric vehicles influencing polyolefin demand?

Automakers specify advanced polypropylene and polyolefin elastomer compounds for battery enclosures and body panels, achieving weight cuts of up to 25% versus metal alternatives.

Page last updated on: