People Counting System Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

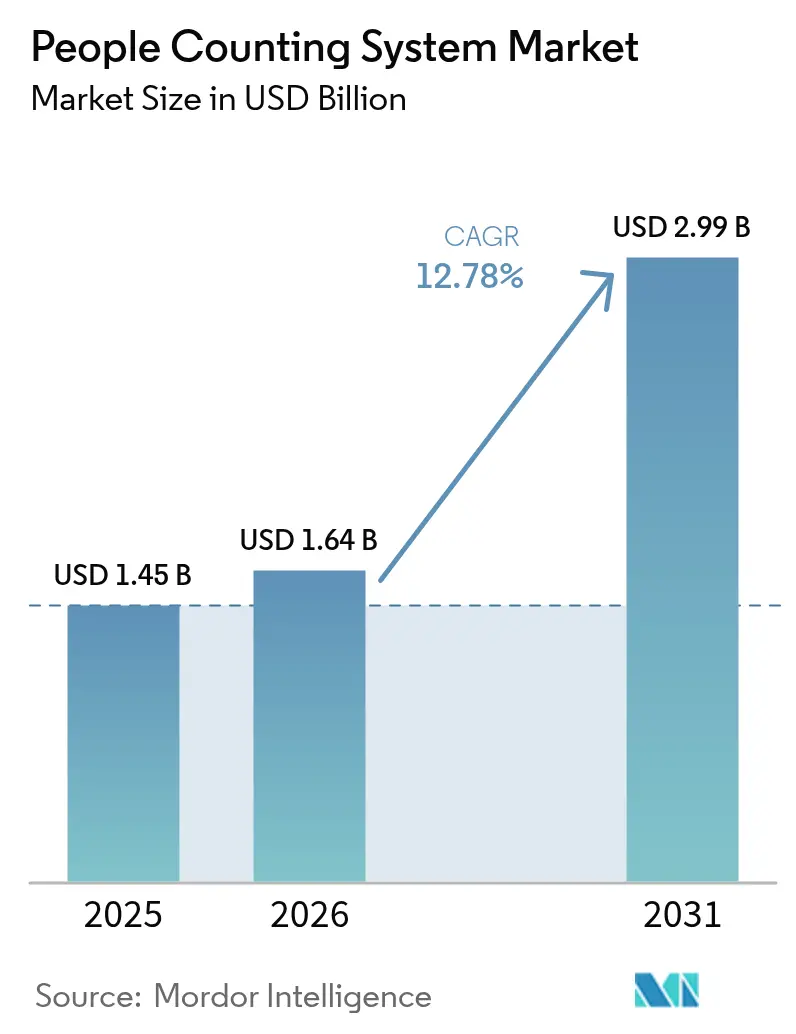

| Market Size (2026) | USD 1.64 Billion |

| Market Size (2031) | USD 2.99 Billion |

| Growth Rate (2026 - 2031) | 12.78% CAGR |

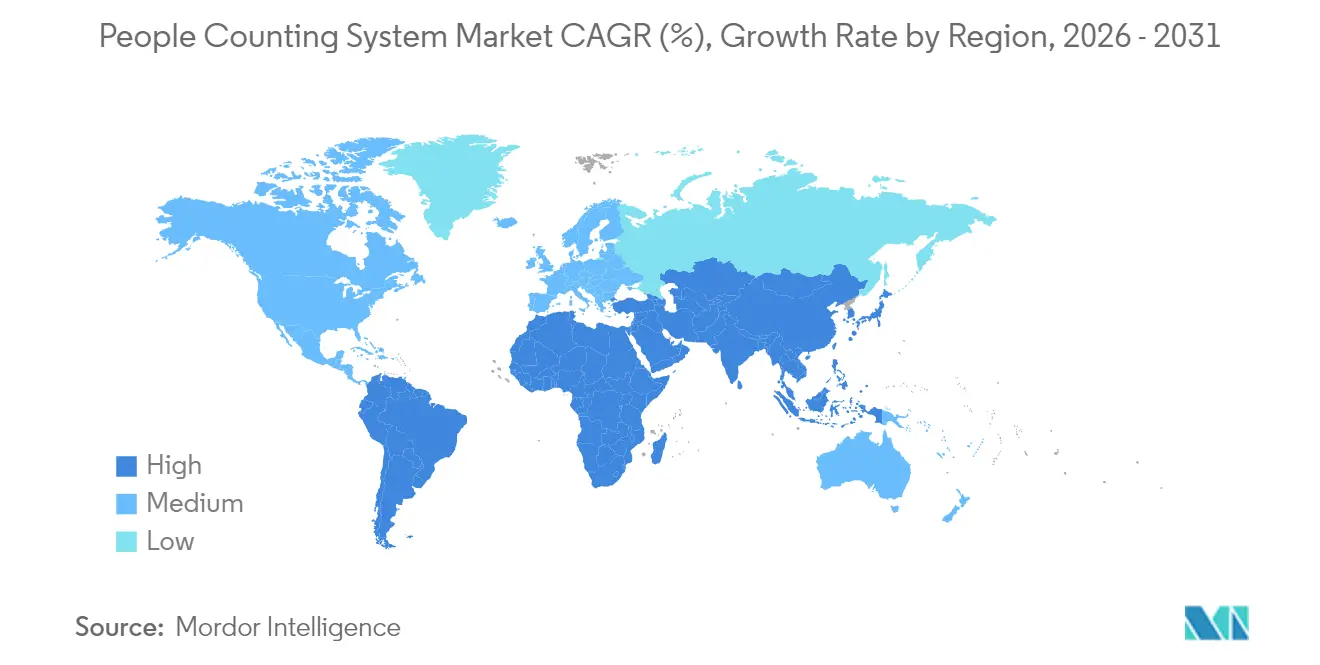

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

People Counting System Market Analysis by Mordor Intelligence

The People Counting System Market size is projected to expand from USD 1.45 billion in 2025 and USD 1.64 billion in 2026 to USD 2.99 billion by 2031, registering a CAGR of 12.78% between 2026 to 2031.

Steady demand comes from smart-city spending, post-pandemic occupancy requirements, and the continuing shift toward AI-enabled sensor fusion that raises accuracy while lowering operating costs.[1]Milesight, “milesight-vs133-ai-tof-people-counting-sensor-whitepaper,” tyrrellproducts.com Adoption accelerates as Time-of-Flight (ToF) sensors deliver 99.8% accuracy and integrate privacy-by-design features that help owners meet GDPR and CCPA mandates. Energy-saving tie-ins with HVAC systems underline a move from point analytics to portfolio-wide optimization, with documented commercial-building pilots posting 12.5% energy reductions. Smart-transport projects across Asia Pacific, metro expansion in the Middle East, and mall traffic rebounds in the United States sustain multi-vertical momentum. At the same time, semiconductor supply disruption and heightened compliance costs create price tension that smaller retailers must navigate.

Key Report Takeaways

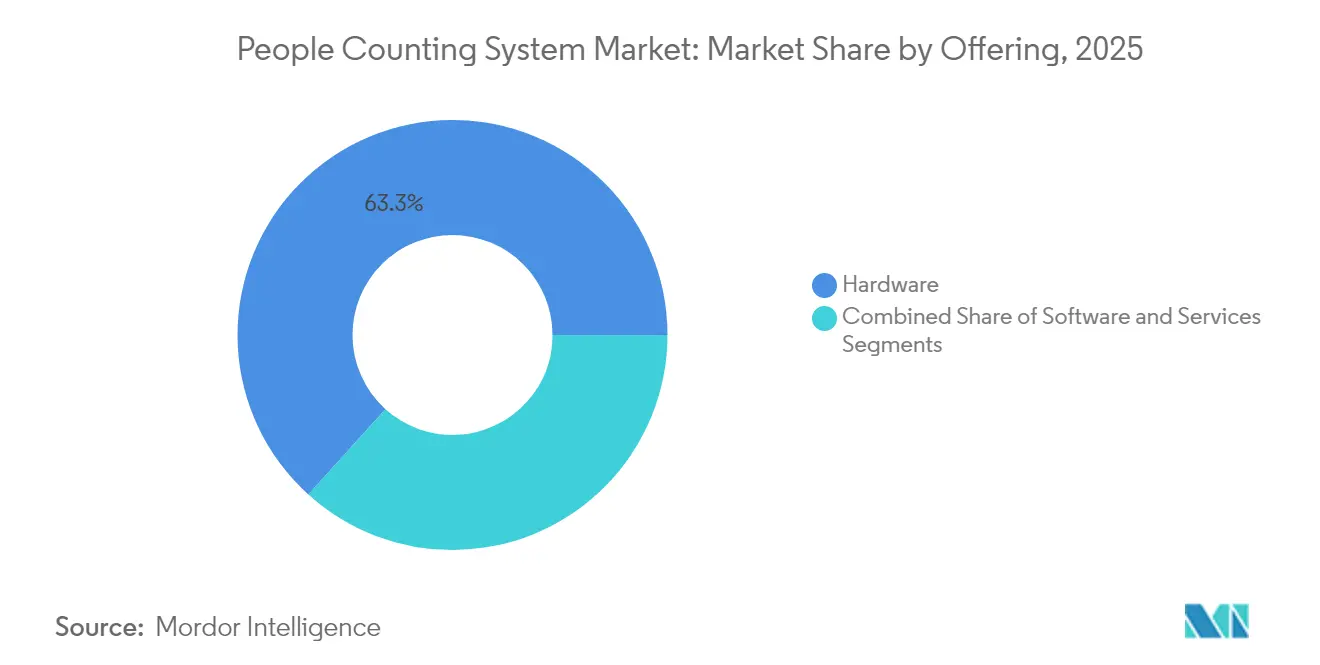

- By offering, hardware led with 63.30% revenue share in 2025, while services are forecast to expand at a 13.45% CAGR through 2031.

- By sensor technology, infrared beam sensors accounted for 36.10% of People Counting System market share in 2025; Time-of-Flight sensors are set to advance at a 14.05% CAGR to 2031.

- By deployment mode, on-premise solutions held 70.60% of People Counting System market size in 2025, whereas cloud deployment records the highest projected CAGR at 14.2% through 2031.

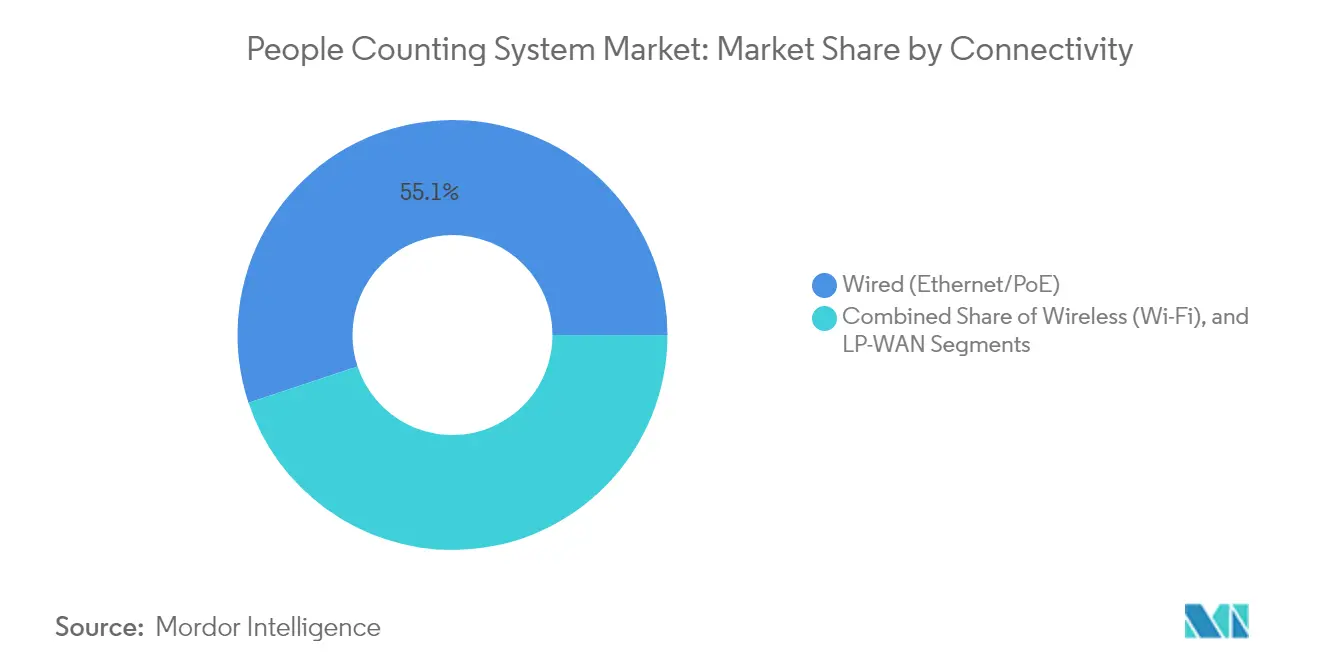

- By connectivity, wired Ethernet/PoE installations captured 55.10% share in 2025; LP-WAN links are projected to rise at a 13.5% CAGR over the forecast period.

- By end-user vertical, retail stores led with 28.40% revenue share in 2025, while transportation hubs represent the fastest-growing segment at 14.35% CAGR.

- By geography, Asia Pacific commanded 31.10% of People Counting System market size in 2025; the Middle East is poised for a 13.85% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global People Counting System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart-Retail Demand for Real-Time Footfall Analytics in North America and Europe | +2.1% | North America & Europe | Medium term (2-4 years) |

| Post-COVID Occupancy Compliance Mandates Fueling Installations (EU, US) | +1.8% | EU & US | Short term (≤ 2 years) |

| Smart-City Transportation Hubs Deploying Crowd-Flow Sensors Across Asia | +2.3% | Asia Pacific | Long term (≥ 4 years) |

| AI-Enabled Video Analytics Cutting TCO and Boosting Accuracy | +2.0% | Global | Medium term (2-4 years) |

| HVAC Energy-Optimization via Occupancy Integration in Commercial Buildings | +1.6% | Global | Long term (≥ 4 years) |

| Venture-Capital Surge into MENA Footfall-as-a-Service Platforms | +1.4% | Middle East & North Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Smart-retail demand for real-time footfall analytics in North America and Europe

Retailers rely on anonymized footfall data to raise conversion and calibrate staffing; evidence from U.S. malls shows 5-15% revenue uplift after analytics rollouts.[2]Mapzot, “US Shopping Malls Make a Comeback Foot Traffic Soars in 2025,” mapzot.ai Link Retail’s LinkVision camera software leverages existing CCTV to surpass 95% accuracy, lowering retrofit costs for European chains. Telstra’s 2024 deployment across Australian stores underscores global reach, pairing >95% accuracy with on-device processing that addresses privacy risk. By enriching traffic counts with demographic metadata, retailers adjust layouts and execute targeted promotions without data-sharing exposure. These traction points reinforce the People Counting System market as a core pillar of omnichannel strategy.

Post-COVID occupancy compliance mandates fueling installations (EU, US)

Revised building codes now require live head-counting to support emergency egress and indoor-air-quality monitoring, spurring adoption in health facilities and public offices.[3]Buildings, “The Hospital of the Future,” buildings.com The GSA Oklahoma City Federal Building linked occupancy sensors to its BMS and cut energy use 41%, proving ROI to government buyers. GDPR-aligned designs from FootfallCam anonymize data at chip level, preventing storage of personal imagery while sustaining counting fidelity. Homeland Security’s 2024 survey that endorsed 15 crowd-analysis tools confirms the technology’s relevance to public-safety readiness. Heightened compliance requirements therefore work as both catalyst and filter, rewarding vendors with defensible privacy credentials.

Smart-city transportation hubs deploying crowd-flow sensors across Asia

Metro operators in Singapore, Hong Kong, and Japan integrate ToF, LiDAR, and ticketing data to modulate passenger loads and shorten dwell times.[4]Thales and SBS Transit, “Collaboration to Deliver Better Travel Experience,” sbstransit.com.sg NEXCOM’s intelligent railway infrastructure suite fuses edge AI with LiDAR to improve safety and throughput in Hong Kong. JR East’s analytics platform draws from ~600 stations to guide retail node placement and timetable planning. Airport rollouts such as bCounted continue to deliver real-time density maps for gate management. The strong alignment between mobility modernization and counting accuracy supports the long-run expansion of the People Counting System market.

AI-enabled video analytics cutting TCO and boosting accuracy

Second-generation ToF sensors reach 99.8% accuracy while replacing server-heavy architectures with edge inference. University of Virginia research on transformer networks improves human-action recognition, enabling behavior tagging alongside raw counts. Milesight’s VS133 ToF unit discriminates between group types and filters trolleys, keeping GDPR compliance intact without external video. These innovations lower lifetime cost and open mid-market revenue pools that were previously price-locked, elevating the People Counting System market as a horizontal analytics platform.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GDPR/CCPA privacy compliance hindering camera-based adoption | -1.2% | EU & California | Medium term (2-4 years) |

| Accuracy gaps in open-area counting reducing buyer confidence | -0.8% | Global | Short term (≤ 2 years) |

| Legacy BMS integration complexity in emerging markets | -0.9% | Emerging Markets | Long term (≥ 4 years) |

| Price sensitivity of SMB retailers in South America | -0.6% | South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

GDPR/CCPA privacy compliance hindering camera-based adoption in EU and CA

Stringent consent rules compel vendors to embed anonymization and local processing, raising bill-of-materials and legal consultancy costs. Aura Vision’s on-device analytics avoid image storage, satisfying regulators yet still capturing directional counts. ToF sensors emerge as a substitute, providing >95% accuracy without identifiable frames, easing certification hurdles. Vendors that can verify end-to-end compliance are increasingly favored in public tenders, which shapes competitive dynamics within the People Counting System market.

Accuracy gaps in open-area counting reducing buyer confidence (stadiums)

Wide-entrance venues challenge legacy solutions; VizioSense finds that 2D cameras top out near 95% accuracy, while LiDAR improves precision but demands EUR 50,000 (USD 52,800) per sensor. Beonic’s LiDAR upgrade counters low-light error yet comes at a premium. Research into sensor-fusion models shows up to 98% accuracy with speed classification error below 9%, indicating progress but not parity with enclosed-doorway results. Until costs moderate, some venue owners defer procurement.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Integration services outpace hardware growth

Hardware continues to dominate People Counting System market revenue, holding 63.30% share in 2025. Capital outlays concentrate on ToF and LiDAR sensors installed across retail thresholds, airport terminals, and public facilities. Managed services, however, are climbing at a 13.45% CAGR as operators seek outsourced analytics, compliance auditing, and continuous calibration. The migration from one-off installs to subscription models transforms revenue visibility and underpins sustainable growth. People Counting System industry participants leverage cross-selling—pairing sensor upgrades with dashboard training—to lock in multi-year contracts. Software platforms move toward micro-services that ingest third-party data, supporting predictive staffing and energy-optimization use cases.

Integration depth raises complexity, positioning services firms as orchestrators that align IT security, facilities management, and marketing. Projects that join occupancy data with HVAC schedules demonstrate tangible opex gains, encouraging building owners to shift spending from fixed assets to outcome-based agreements. As a result, the services category helps diversify the People Counting System market beyond hardware refresh cycles.

By Sensor Technology: ToF accelerates amid regulatory tailwinds

Infrared beam sensors captured 36.10% of People Counting System market share in 2025 on the back of reliability in narrow-door installations. Yet ToF 3D sensors are set to expand at a 14.05% CAGR, catalyzed by privacy laws that favor non-imaging depth measurement. By converting light-flight time into depth maps, ToF differentiates people from carts and pets, sustaining accuracy under changing lighting. The shift bodes well for vendors with proprietary ToF ASICs that can embed GDPR-inclusive logic. Video-based approaches survive by pivoting to on-edge inference that strips personal imagery, but some buyers remain cautious. Thermal imaging occupies a niche in hospitals where temperature screening merges with head counts. The People Counting System market size tied to ToF sensors is projected to eclipse infrared revenues before 2030 as component cost curves decline.

Hybrid deployments that blend ToF at entry points with Wi-Fi probes in open zones demonstrate rising interest in multimodal precision. Qualcomm’s patent work on scalable depth estimation underscores wider tech-stack investment that will keep ToF on a steep performance trajectory. As adoption broadens, economies of scale further compress price points, reinforcing switch-over momentum.

By Deployment Mode: Cloud adoption broadens user base

On-premise installations accounted for 70.60% of People Counting System market size in 2025, anchored by public-sector and healthcare data-sovereignty rules. Cloud deployments are advancing fastest at 14.2% CAGR as multi-site retailers prioritize central dashboards and elastic compute. Hybrid schemes combine edge devices for millisecond latency with cloud analytics for fleet benchmarking. 5G rollouts ease high-bandwidth uploads, while LP-WAN back-channels supply redundancy. Software-only entrants such as Yellow Sub AI demonstrate a light-footprint approach that eliminates site hardware by analyzing publicly available data streams, opening fresh ground for service-led differentiation.

Cost-flexible, pay-as-you-go pricing stimulates adoption among mid-market chains. At the same time, cloud providers must prove encryption robustness and regional data residency to satisfy regulators. Progressive contracts include phased migration paths that start with on-site appliances and shift analytic workloads to the cloud once compliance gates clear, smoothing buyer journeys within the People Counting System market.

By Connectivity: LP-WAN unlocks hard-to-wire locations

Wired Ethernet or PoE still powers 55.10% of counted devices, favored for reliability and security in retail and corporate campuses. LP-WAN formats LoRa, Zigbee, BLE are growing at a 13.5% CAGR because they offer multi-year battery life and sub-GHz penetration that suits heritage buildings and temporary pop-ups. Wi-Fi remains the default in medium-scale spaces, while early-stage 6G research hints at high-bandwidth, low-power benefits for edge AI. Milesight’s LoRaWAN VS133 line proves that wire-free devices can support both uni-directional and bidirectional counting without compromising battery headroom.

Hybrid connectivity blends wired power at main entrances with LP-WAN repeaters inside large floors, tightening coverage without trenching. Vendors bundle SIM-based cellular as fallback for mission-critical sites. This flexible network layer strengthens the People Counting System market’s reach into greenfield and retrofit projects alike.

By End-User Vertical: Transportation hubs outpace retail’s mature base

Transportation hubs are forecast to post a 14.35% CAGR, buoyed by airport, metro, and bus-terminal modernization. Smart-gate systems calibrate staffing and security lanes in real time, improving traveler throughput while satisfying health-capacity guidelines. Retail retains the largest revenue pool at 28.40%, yet year-over-year growth slows as penetration rises toward saturation in tier-one chains. Malls re-engage after foot-traffic rebounds, deploying zone analytics to drive tenant leasing value. Healthcare and public buildings increasingly leverage occupancy data for infection-control and energy objectives, widening addressable demand. Sports venues, although challenged by open-area counting, represent high ticket value once accuracy hurdles resolve. The People Counting System industry thus maintains diversified exposure that lessens dependence on any single sector.

Geography Analysis

Asia Pacific holds a 31.10% revenue stake in 2025, propelled by government-funded smart-city frameworks and locally manufactured sensor hardware that compresses unit costs. Singapore’s MRT applies camera upgrades and ticket data to push crowdedness alerts, while Hong Kong integrates LiDAR-backed edge AI for railway safety. Japan’s JR East processes Suica transaction logs across ~600 stations to model commuter flow, feeding both transport planning and retail placement. China’s tier-two city urbanization fuels bulk orders for crowd-management kits, and Southeast Asian airports deploy ToF counters to speed security lines. These coordinated infrastructure goals cement the region’s long-term dominance within the People Counting System market.

The Middle East emerges as the fastest-growing geography at a 13.85% CAGR. Vision 2030 programs back large-scale sensor rollouts in Saudi Arabia, the UAE, and Qatar. Bold Technologies allocates USD 2.5 billion to the Aion Sentia cognitive-city platform that fuses mobility, healthcare, and energy data on one AI layer. Dubai targets a city-wide digital twin via street-level sensors, expanding opportunities for crowd analytics providers. Venture-capital flows into MENA analytics startups indicate rising local supply capacity.

North America sustains adoption through retail refresh cycles and federal facility mandates. The return of U.S. mall shoppers in 2025 renews appetite for staff-versus-shopper differentiation features. Europe’s GDPR regime fosters privacy-centric ToF and on-edge video solutions, stimulating upgrades rather than greenfield sales. South America grapples with SMB affordability, while Africa’s nascent smart-city schemes provide longer-dated upside.

Regulatory Landscape

In Europe, the regulatory perimeter for AI-enabled people counting tightened with the EU AI Act (Regulation (EU) 2024/1689), which entered into force on 1 August 2024. Early obligations such as prohibited practices and AI literacy applied from 2 February 2025, while obligations associated with high-risk AI systems and associated enforcement timelines start from 2 August 2026. For people counting vendors, product classification depends on whether the system performs biometric categorization (for example, age or gender inference) or identification, which triggers high-risk requirements such as conformity assessment, logging, human oversight, and registration in the EU database.

The EU AI Act sits alongside existing privacy rules rather than replacing them, so camera-based deployments that capture identifiable footage continue to be governed by GDPR, including expectations around lawful basis, DPIAs, and security controls as framed by European Data Protection Board guidance on video devices. In parallel, industry standards referenced in procurement and security programs, such as ITU-T F.743.23 for premises unit security and ISO/IEC 30137 for biometrics use in video surveillance, shape technical and assurance requirements. Taken together, these frameworks push buyers toward privacy-by-design implementations, including on-device processing and non-imaging sensors such as ToF or LiDAR, to reduce compliance burden without sacrificing accuracy.

Competitive Landscape

The People Counting System market is moderately fragmented. Axis Communications, Teledyne FLIR, and Xovis leverage camera and sensor portfolios to cross-sell analytics modules, while focused players such as FootfallCam and V-Count emphasize purpose-built accuracy and privacy. Battery Ventures’ majority stake in RetailNext supplies expansion capital for AI roadmap acceleration. Milesight aligns with Vemco Group to merge ToF edge devices and cloud dashboards, signaling a convergence toward integrated IoT stacks. Patent velocity in depth-estimation algorithms, including Qualcomm’s scalability work, highlights future differentiation on low-power edge intelligence.

Strategically, incumbents seek vertical-specific feature sets such as queue management for airports or space-planning for corporate campuses. Emerging disruptors explore software-only or subscription pricing to undercut hardware-heavy offerings. Competitive advantage increasingly pivots on compliance certification, energy tie-ins, and total-cost-of-ownership reductions. Overall, the top five players control roughly 35-40% of revenue, leaving space for regional specialists and OEM white-label suppliers.

People Counting System Industry Leaders

RetailNext Inc.

Axis Communications AB

Teledyne FLIR Systems Inc.

FootfallCam Ltd.

Xovis AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace sits in deployments that separate occupancy and flow measurement from biometric processing, since the EU AI Act raises the compliance bar for systems performing biometric categorization, while non-biometric counting can fall outside the high-risk perimeter. That dynamic is shifting product and procurement toward privacy-first architectures, including ToF and LiDAR counters and edge inference designs that avoid streaming or storing identifiable video. Vendors that can document technical boundaries between counting and categorization, and provide auditable logging and security controls aligned with EDPB video guidance, gain leverage in public tenders and multi-site enterprise rollouts.

Beyond retail, demand signals are emerging in public-sector and municipal building programs that explicitly fund occupancy monitoring and capacity control. Murcia City Council announced deployment of 33 AI-enabled optical sensors for municipal occupancy monitoring and capacity control (EUR 252,066), which points to a repeatable path for government buildings where safety, energy management, and compliance are evaluated together. There are also platform-level opportunities as people counting converges with broader visitor intelligence, including Vemco Group launching Re-ID capabilities for its VemTrack platform to support anonymous journey tracking across zones, and vendors positioning people and flow intelligence as part of unified security and surveillance stacks rather than standalone counters.

Recent Industry Developments

- April 2026: FootfallCam partnered with TSP to secure TELEC certification, supporting deployment of wireless-enabled people counting solutions in Japan. This removes a key regulatory gate for radio-connected installations and improves FootfallCam's ability to compete for Japan-based projects that require certified connectivity. It also indicates a broader reliance on local partnerships to navigate market-entry compliance for counting hardware.

- July 2025: FootfallCam launched its 3D Pro2 2025 sensor, positioning it for broader coverage by enabling connections to multiple IP cameras for full-store visibility. This expands the addressable footprint beyond single-entrance counting toward whole-floor analytics with fewer dedicated counters. The release also increases competitive pressure on legacy camera-only approaches where buyers weigh coverage, accuracy, and privacy constraints.

- January 2025: RetailNext released Traffic 3.0, updating its retail analytics platform for shopper behavior and traffic intelligence use cases. The platform refresh supports retailers seeking to centralize footfall data across multi-site networks and link traffic insights to staffing and conversion workflows. It also highlights the shift from point solutions toward software-led operating models that monetize analytics and services alongside hardware.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the revenue generated from solutions that count and track people moving through physical spaces, usually at entry and exit points, and then convert those counts into usable occupancy and footfall insights for operators.

Scope exclusions: We exclude general CCTV security setups and video management systems when they are not sold or deployed with a dedicated people counting function.

Segmentation Overview

- By Offering

- Hardware

- Software

- Services

- By Sensor Technology

- Infrared Beam

- Thermal Imaging (IR)

- Video-Based (Mono / Stereo / AI)

- Time-of-Flight (3-D)

- Pressure and Magnetic

- Wi-Fi / BLE Probe

- By Deployment Mode

- On-Premise

- Cloud

- By Connectivity

- Wired (Ethernet / PoE)

- Wireless (Wi-Fi)

- LP-WAN (LoRa, Zigbee, BLE)

- By End-User Vertical

- Retail Stores

- Shopping Malls and Hypermarkets

- Transportation Hubs (Airports / Metro / Bus)

- Hospitality and Leisure (Hotels, Casinos, Theme Parks)

- Sports and Entertainment Venues

- Banks and Financial Institutions

- Corporate and Government Buildings

- Healthcare Facilities

- Smart Cities and Public Spaces

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Nordics (Sweden, Norway, Denmark, Finland)

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Australia

- New Zealand

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to map the demand pool and the technology direction before we lock model assumptions. We typically review public sources such as US Census Bureau retail sales series, Eurostat retail trade and mobility indicators, International Air Transport Association passenger traffic releases, and UN Comtrade trade flows for relevant sensors and imaging components.

We also rely on standards and guidance from NIST, procurement and tender portals from public agencies, and peer reviewed journals that cover computer vision and sensor accuracy, along with company annual reports, investor presentations, and credible press. A paid subscription for company financials and intelligence, plus a patent database, is used selectively to cross check revenue exposure and product activity. These examples are illustrative, and other public sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focuses on confirming what is actually deployed, what gets replaced, and how pricing shifts by site type. We spoke with solution providers, installers, channel partners, and end users across retail, transportation, hospitality, and public venues. We then used follow ups to test assumptions by region and by use case maturity.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 17% | APAC: 41% |

| Mid tier: 48% | Functional/Unit leaders: 37% | EMEA: 34% |

| Smaller Players: 18% | Managers: 46% | Americas: 25% |

Market-Sizing & Forecasting

Market sizing starts with a top down build that reconstructs the addressable installation base from facility activity indicators, and then converts it into annual spending using adoption and replacement patterns. In practice, we anchor demand to metrics such as organized retail floor area trends, mall and venue footfall recovery, airport and transit passenger volumes, the mix of new openings versus refurbishments, and the typical number of counting points per site based on layout.

Those totals are then checked using selective bottom-up approximations, such as sampling average selling prices for common sensor and camera configurations, applying expected attach rates for analytics software, and validating services share through channel checks. When data is thin for smaller countries, gaps are handled by using proxy indicators like retail density, mobility trends, and import intensity, and the figures are reviewed again with expert feedback.

For forecasting, we mainly use scenario analysis supported by a light multivariate regression on key demand drivers, so growth is not driven by one single assumption. After the checks are completed, the final forecast is produced only after price progression and adoption timing are re-tested with interview inputs.

Data Validation & Update Cycle

Validation is done through triangulation across the model output, independent demand signals, and interview feedback, then followed by variance checks at region and end-use levels. If a country shows a sudden jump that is not supported by mobility, construction, or procurement signals, the assumptions are reopened and respondents may be re-contacted to understand what changed.

Before sign-off, the sizing file goes through multiple analyst review steps, including logic checks on adoption curves, pricing ranges, and regional splits. Reports are refreshed annually, and interim updates are made when material events occur, such as regulatory shifts around occupancy limits or a sharp change in retail expansion. Right before delivery, a fresh pass is done so clients receive the most current view supported by the available inputs.

Mordor Intelligence's People Counting System Market Size Compared Against Other Published Estimates

Published market values for people counting systems can look far apart, even when the topic name sounds identical. In most cases, the gap comes from how each study defines the solution set, how hardware versus software is treated, and how base-year currency timing and price changes are applied.

Some estimates fold adjacent smart building tools into the same bucket or lean heavily on a single end-use such as retail, which can lift the number quickly. In Mordor Intelligence, revenue is counted only when the offer is a dedicated people counting system across hardware, software, and related services, and generic video surveillance spending is kept out even if cameras are present.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.64 B (2026) | |

| Industry Research Publisher A | USD 1.26 B (2024) | Uses an earlier base year and appears to show mixed headline figures across years, which can shift the reported level when pricing and adoption are moving quickly. Coverage also emphasizes broader type and end-use cuts, so part of the spread can come from how bundled analytics and mounting platforms are valued. |

| Industry Research Publisher B | USD 1.46 B (2025) | Uses a different base year and a longer horizon, which changes the implied adoption curve and the way ASP progression is carried forward. Limited scope notes on what is excluded can also lead to partial inclusion of neighboring occupancy and smart venue solutions. |

The table shows that a one to two year shift in the base period and a small change in what is treated as in-scope can move the market value by a meaningful amount. With clear counting rules, practical demand drivers, and repeatable checks against deployment and traffic signals, our estimate stays traceable to how people counting systems are actually purchased and used.

Key Questions Answered in the Report

What is the current size of the People Counting System market?

The market is valued at USD 1.64 billion in 2026 and is forecast to reach USD 2.99 billion by 2031.

Which segment is growing fastest within the People Counting System market?

Services, driven by managed analytics and integration support, is projected to grow at a 13.45% CAGR through 2031.

Why are Time-of-Flight sensors gaining traction?

ToF sensors combine 99.8% accuracy with privacy-friendly depth mapping, ensuring GDPR compliance and reducing total cost of ownership.

Which geography will expand most rapidly?

The Middle East is expected to post a 13.85% CAGR through 2031 on the back of Vision 2030 smart-city investments.

How do occupancy sensors improve energy efficiency?

Integrating people counts with HVAC systems has yielded documented energy savings of up to 12.5% in commercial buildings.

What connectivity options are preferred for hard-to-wire sites?

LP-WAN technologies such as LoRa and Zigbee provide multi-year battery life and strong penetration, enabling cost-effective deployments in older or temporary structures.

Page last updated on: