Infrastructure Monitoring Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

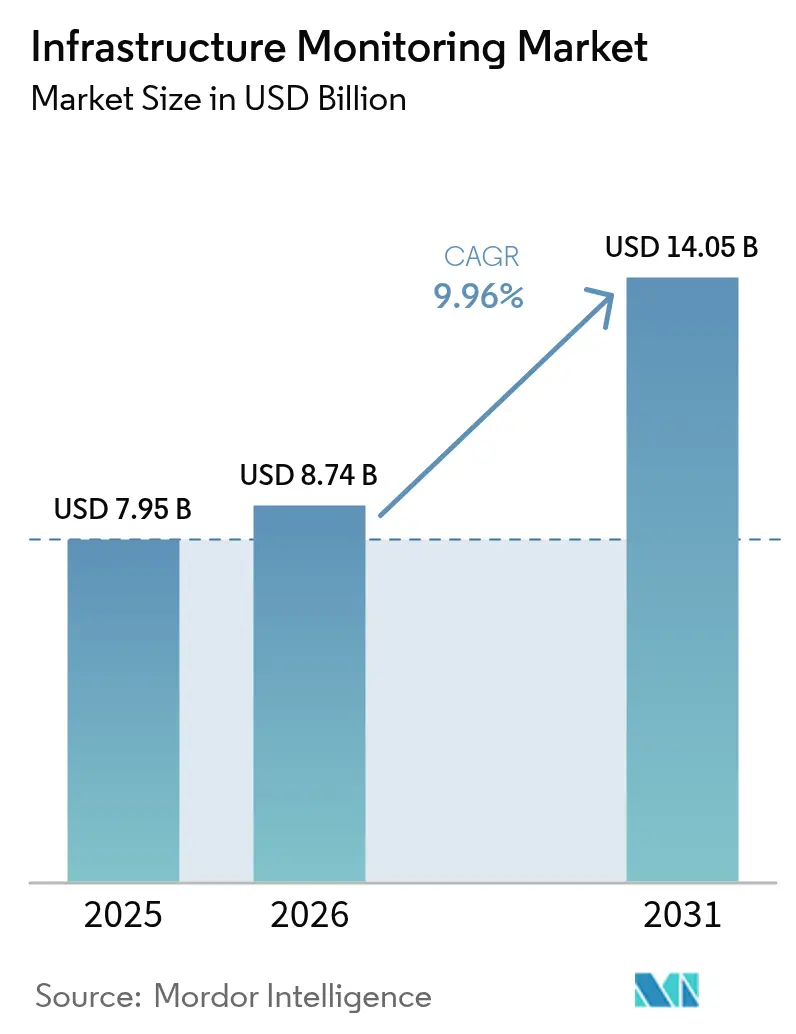

| Market Size (2026) | USD 8.74 Billion |

| Market Size (2031) | USD 14.05 Billion |

| Growth Rate (2026 - 2031) | 9.96% CAGR |

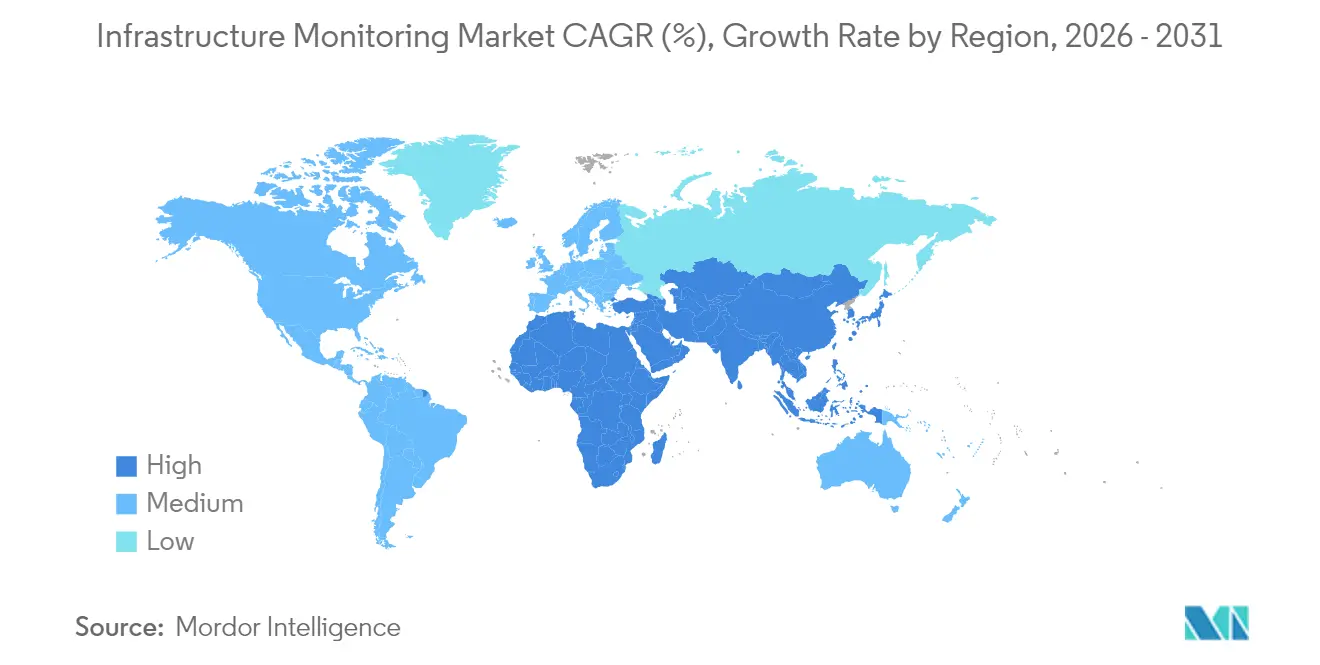

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Infrastructure Monitoring Market Analysis by Mordor Intelligence

Infrastructure monitoring market size in 2026 is estimated at USD 8.74 billion, growing from 2025 value of USD 7.95 billion with 2031 projections showing USD 14.05 billion, growing at 9.96% CAGR over 2026-2031. Robust momentum reflects escalating deployments of wireless sensor networks, falling micro-electromechanical (MEMS) sensor prices, and rising demand for predictive maintenance across aging civil assets. Integration of IoT, AI, and cloud platforms continues to reduce lifecycle costs, allowing asset owners to shift from schedule-based to condition-based maintenance. Public-sector stimulus in North America, Japan, and the EU is accelerating digital-twin roll-outs, while smart-city programs in APAC are driving real-time structural health monitoring (SHM). Competitive intensity is heightening as incumbents pivot toward end-to-end platforms and niche specialists pursue modular offerings that resolve interoperability gaps between wired and wireless systems. Market opportunities are strongest where environmental and seismic hazards intersect with aging infrastructure, creating urgent demand for multi-hazard monitoring solutions that combine structural, geotechnical, and climate data streams.

Key Report Takeaways

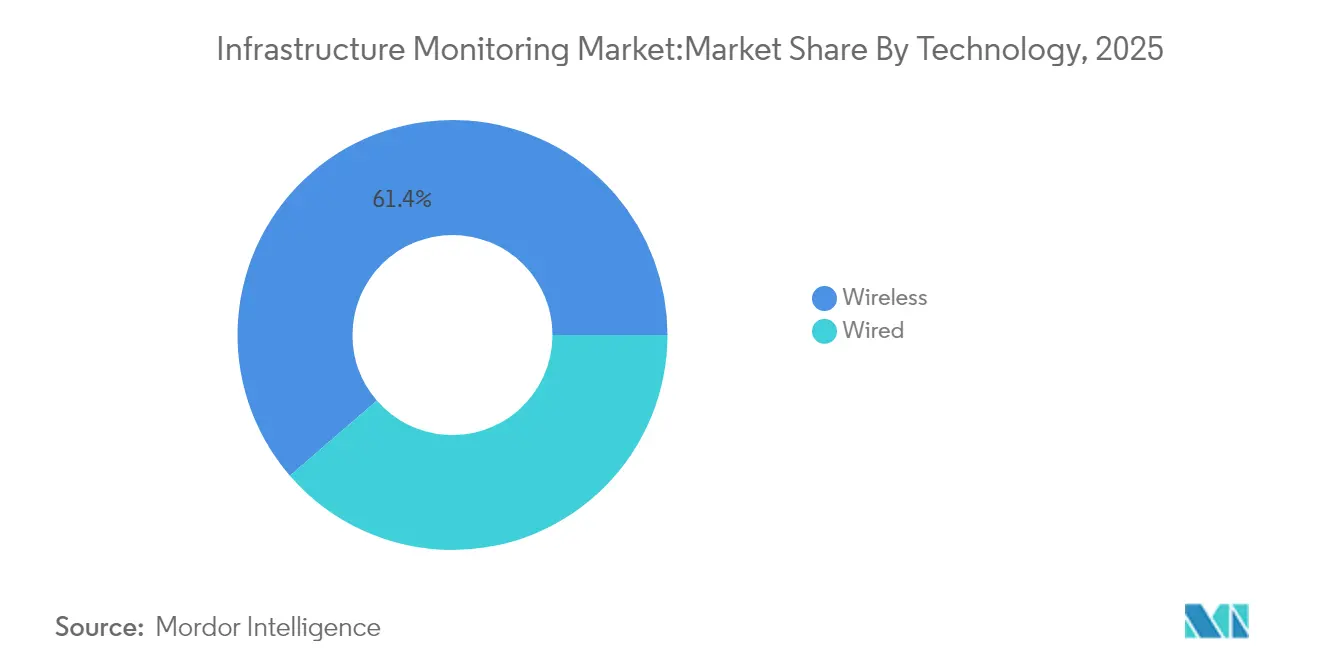

- By technology, wireless systems commanded 61.35% of the infrastructure monitoring market share in 2025; they are advancing at an 11.45% CAGR through 2031.

- By application, environmental and seismic monitoring is forecast to expand at a 12.18% CAGR, the fastest among all use cases.

- By end-user industry, civil infrastructure held 46.55% revenue share in 2025, while energy & utilities is projected to register a 11.88% CAGR to 2031.

- By deployment model, cloud/edge solutions represent the fastest trajectory with a 13.05% CAGR, even though on-premise retains a 67.10% share.

- By geography, North America led with 29.40% of the infrastructure monitoring market in 2025; Asia-Pacific shows the strongest growth outlook at 11.86% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Infrastructure Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating deployment of wireless sensor networks in aging bridges | +2.4% | North America & Europe | Medium term (2-4 years) |

| Smart-city megaprojects fuel real-time SHM demand | +2.1% | Asia-Pacific | Long term (≥ 4 years) |

| EU & Japan predictive-maintenance mandates for dams/tunnels | +1.8% | European Union & Japan | Medium term (2-4 years) |

| US IIJA-funded digital-twin roll-outs | +1.5% | United States | Short term (≤ 2 years) |

| Cloud-first monitoring adoption by GCC EPC majors | +1.2% | Middle East (GCC) | Medium term (2-4 years) |

| Falling MEMS sensor cost enabling secondary-road instrumentation | +1.7% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Deployment of Wireless Sensor Networks in Aging Bridges (NA & EU)

Aging bridges—45% are more than 50 years old—are prompting asset owners to install wireless nodes that stream strain and vibration data continuously. Linear wireless sensor network designs have cut power consumption and eased installation on long-span structures, evidenced by the 64-node Golden Gate Bridge deployment collecting 1 kHz data without traffic disruption. Project timelines are shortening because cloud-based dashboards allow engineers to validate sensor performance remotely, minimizing field revisits and scaffolding costs.[1]Lynch, J. P., and others, "Health Monitoring of Civil Infrastructures Using Wireless Sensor Networks." ACM Digital Library, dl.acm.org

Smart-City Megaprojects Fuel Real-Time SHM Demand

UN-Habitat forecasts APAC’s urban population to reach 3.5 billion by 2050, pushing municipal authorities to embed SHM into transit corridors, tunnels, and public buildings.[2]UN-Habitat, "World Smart Cities Outlook 2024", unhabitat.org ASEAN’s 108 active smart-city programs are standardizing data exchanges for structural sensors, while 5G federated edge platforms in Macau and Hong Kong stream gigabyte-scale dynamic-load data in under 50 milliseconds. Procurement frameworks now require open APIs, encouraging start-ups to license micro-services for crack detection, corrosion mapping, and anomaly triage.

EU & Japan Predictive-Maintenance Mandates for Dams/Tunnels

Society 5.0 policies in Japan and new EU dam-safety directives compel operators to shift from interval inspections to predictive analytics.[3]Kuczyńska, Agnieszka, "Analysis of Opportunities for EU SMEs in Japan's Data Economy and Artificial Intelligence in Connection with Robotics" EU-Japan Centre, eu-japan.euLive hydrological, vibration, and seepage metrics feed digital twins that simulate breach scenarios, letting owners prioritize reinforcement budgets. Joint research with universities is further de-risking procurement, as reference architectures for data integration become publicly available.

US IIJA-Funded Digital-Twin Roll-outs

IIJA appropriations earmark USD 60 billion for digital technologies. State departments of transportation are bundling lidar, BIM, and sensor data into unified twins that forecast load paths and fatigue life in real time. Early adopters report double-digit reductions in maintenance work orders and extend inspection intervals, freeing capex for resilience upgrades.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex for remote-area wireless links | −1.3% | Africa, South America, rural Asia | Medium term (2-4 years) |

| Data-governance & cybersecurity barriers in EU public assets | −0.9% | European Union | Short term (≤ 2 years) |

| Shortage of structural-data scientists in emerging markets | −0.8% | Africa, South America, Southeast Asia | Long term (≥ 4 years) |

| Interoperability gaps between legacy wired & IoT sensors | −1.1% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capex for Remote-Area Wireless Links

Sparse backhaul in remote regions raises deployment costs by up to 45%, deterring adoption despite proven ROI in urban settings. While low-earth-orbit satellite constellations promise relief, terminals remain price-prohibitive for many municipalities, postponing sensor roll-outs on rural bridges and pipelines.

Data-Governance & Cyber-Security Barriers in EU Public Assets

The EU’s stringent General Data Protection Regulation and upcoming Cyber Resilience Act impose encryption, audit, and data-sovereignty obligations that lengthen procurement cycles. Small municipalities struggle to field specialists who can manage tokenization and zero-trust architectures, delaying sensor integrations into cloud supervisory control systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Wireless Systems Redefine Infrastructure Insights

Wireless platforms underpin USD 4.88 billion of 2025 revenue, equivalent to 61.35% of the infrastructure monitoring market. Supported by improvements in mesh routing, sub-GHz radios, and energy harvesting, wireless networks now achieve five-year battery life, matching wired uptime benchmarks while avoiding conduit and trenching expenses. The infrastructure monitoring market size for wireless systems is forecast to expand at 11.45% CAGR, driven by public bridge retrofits in North America and Europe. In contrast, the wired cohort retains relevance for nuclear plants and long-span tunnels where deterministic latency is non-negotiable.

As cloud vendors introduce digital-signal-processing services, asset managers can deploy vibration and acoustic algorithms without maintaining on-premise servers. Edge-optimized AI chips embedded in wireless gateways now execute modal analysis locally, transmitting compressed features rather than raw waveforms—cutting bandwidth costs by 70%. This shift unlocks green-field opportunities in emerging economies where 3G/4G coverage is patchy yet growing.

By Offering: Services Surpass Hardware in Growth Velocity

Hardware still represents 54.30% of 2025 revenue, but services are set to outpace all other categories with a 12.44% CAGR. The infrastructure monitoring market size for services will rise as owners outsource data engineering, AI model training, and dashboard customization to firms that blend civil-engineering know-how with cloud-native skills. Demand is especially acute in Latin America and Southeast Asia, where engineer shortages hamper in-house program development.

Software platforms account for the remaining 18.35% of spending, yet face persistent integration challenges. Open-source middleware initiatives seek to standardize message brokers and semantic models, but vendor lock-in remains common. Cyber-security hardening features—zero-trust access, secure boot, over-the-air patching—are now baseline requirements for enterprise procurement.

By Deployment Model: Cloud/Edge Catalyzes Real-Time Decision-Making

On-premise systems captured 67.10% revenue in 2025, reflecting entrenched policies on data sovereignty across defense, nuclear, and water utilities. Nevertheless, cloud/edge deployments are advancing fastest at 13.05% CAGR, and their infrastructure monitoring market share is projected to exceed 42.15% by 2031. Edge nodes equipped with FPGA and GPU accelerators perform spectral clustering and anomaly detection against gigahertz data streams, forwarding only exception reports to central repositories.

Hybrid adoption patterns dominate: asset owners retain mission-critical logic on-site but push historical data and machine-learning training to the cloud. Regulatory clarity in Europe around data processing agreements is gradually reducing resistance, while zero-copy encryption technologies strengthen trust in multitenant environments. EPC majors in the GCC are institutionalizing “cloud-first” design guides, setting procurement precedents that ripple across Africa and South Asia.

By Application: Environmental & Seismic Monitoring Accelerates

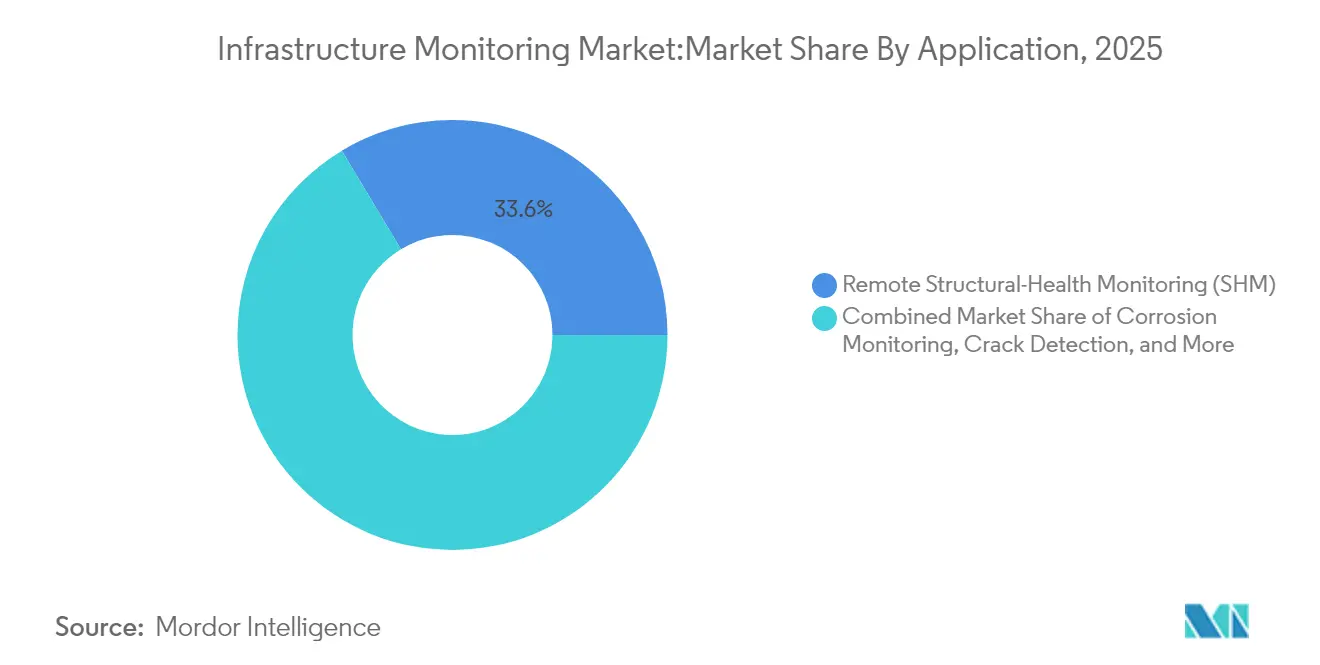

Remote structural health monitoring (SHM) remains the anchor at 33.60% revenue, yet environmental and seismic monitoring are scaling fastest at 12.18% CAGR as climate volatility escalates. The infrastructure monitoring market size for environmental applications will benefit from mandated flood-early-warning networks and landslide detection in mountainous regions. Operators now link rainfall, groundwater, and vibration sensors into integrated dashboards, providing a cohesive risk picture.

Corrosion monitoring is tracking metal-loss rates on offshore platforms with distributed fiber-optic sensors, while crack-width measurement via near-infrared fluorescence imaging reaches 0.08 mm resolution. Meanwhile, vibration and dynamic-load monitoring algorithms are extending bridge fatigue life by predicting traffic-induced stresses more accurately than previous empirical models.

By End-User Industry: Energy & Utilities Surge Ahead

Civil infrastructure held a dominant 46.55% slice in 2025, anchored by bridge and road retrofits in OECD economies. The infrastructure monitoring market size for this segment will continue to grow steadily as federal programs earmark resilience funds. Energy & utilities emerges as the growth pacesetter at 11.88% CAGR, propelled by distributed renewable assets and stricter reliability standards. Utilities layering drone imagery, line-sensor data, and weather feeds are reducing wildfire risks and shaving condition-based maintenance spend by double digits.

Transportation hubs—ports, rail corridors, airports—are expanding roll-outs of fiber-optic vibration arrays to manage increased freight volumes. Aerospace & defense engineers embed high-g accelerometers within runway slabs, monitoring FOD-induced stresses during fighter take-offs. Mining & metals firms deploy atmospheric-corrosion sensors on haul-truck frames, scheduling proactive sand-blasting and extending chassis life.

Geography Analysis

North America anchors 29.40% of 2025 revenue, supported by IIJA-funded digital-twin pilots and a policy push to rehabilitate bridges older than 50 years. Smart-sensor retrofits demonstrate 20% maintenance cost savings, prompting state agencies to incorporate sensing budgets into resurfacing contracts. Canadian provinces leverage federal green-infrastructure grants to trial edge-AI crack detection on remote timber bridges, while Mexico accelerates toll-road concessions that stipulate condition-based monitoring from day one.

Asia-Pacific delivers the steepest trajectory with a 11.86% CAGR through 2031. China’s 14th Five-Year Plan prioritizes SHM on high-speed rail viaducts, and Japan’s Society 5.0 target embeds robotics in tunnel maintenance. India’s Smart Cities Mission funds integrated command centers that ingest flood gauges and traffic sensors, offering a blueprint for mid-tier cities across ASEAN. Australia’s asset-management councils adopt fiber-optic strain lines on coastal seawalls to anticipate storm-surge damage, a practice now spreading to New Zealand and Pacific Island states.

Europe’s regulatory rigor fosters early adoption of predictive-maintenance mandates. Nordic countries pioneer infrastructure-as-a-service concessions where contractors guarantee uptime using continuous monitoring. The Netherlands applies real-time deflection sensing on dykes to counter sea-level rise, while Germany pilots quantum gravimetry to detect subsidence beneath Autobahn foundations. Southern Europe channels pandemic-recovery funds into seismic retrofits, bundling accelerometers with energy-efficiency upgrades.

Regulatory Landscape

Regulation increasingly ties infrastructure monitoring programs to continuous security monitoring and auditable logging, especially where assets are designated as critical infrastructure. In the United States, the Federal Energy Regulatory Commission (FERC) approved NERC Reliability Standard CIP-015-1 in July 2025. This formalized internal network security monitoring expectations for Bulk Electric System environments and raised baseline requirements for monitoring, logging, and integration with cyber controls used alongside operational monitoring stacks.

In Europe, the security and resilience agenda tightens monitoring obligations with an emphasis on automated detection and recordkeeping. EU Implementing Regulation (EU) 2024/2690 requires relevant entities to establish procedures and use tools to monitor and log network activities for incident detection, with a stated preference for automated and continuous monitoring where feasible. NIST Cybersecurity Framework 2.0 also reinforces continuous monitoring and technology infrastructure resilience as core functions referenced by operators and procurement teams when specifying monitoring system security, access controls, and evidence retention.

Value Chain Analysis

The value chain covers sensing and connectivity inputs (MEMS and specialty sensors, fiber-optic components, communications modules, and edge compute hardware), system design and manufacturing (instrumentation vendors and industrial OEMs), software and analytics (cloud/edge platforms, digital-twin and anomaly detection applications), and downstream implementation and lifecycle services (installation, calibration, integration, monitoring operations, and maintenance). Delivery is typically handled through system integrators, EPC partners, and value-added resellers that bundle sensor kits, gateways, and analytics subscriptions into asset-specific projects across civil infrastructure and utilities.

Partnerships are increasingly connecting physical-layer infrastructure with predictive analytics to reduce integration friction and shorten deployments. For example, in July 2025 AFL and VIE Technologies announced a strategic partnership combining fiber connectivity with AI-driven predictive monitoring for power transformers and data center mechanical equipment, showing how hardware connectivity providers and analytics specialists align to deliver end-to-end monitoring outcomes. At the same time, supply chain and third-party risk concerns raise the importance of managed security monitoring and ICT supply chain security practices (such as those promoted by CISA) as operators scrutinize vendor access, firmware provenance, and patching workflows for deployed monitoring endpoints.

Competitive Landscape

The market comprises diversified industrials, vertical-focused specialists, and venture-backed disruptors. The top five vendors collectively capture 35-40% of revenue, signalling moderate concentration. Siemens AG and Schneider Electric pursue platform consolidation, adding analytics layers and field-service capabilities via targeted M&A. Siemens’ new USD 190 million Texas facility exemplifies a capacity build-out to localize production for North American AI-enabled infrastructure programs. Schneider Electric’s motion-control launches extend its edge-compute portfolio, offering deterministic control for high-speed data acquisition.

Specialists such as Worldsensing and Sixense Group command loyalty in geotechnical and tunnel monitoring niches, leveraging proprietary long-range telemetry and high-precision fiber-optic sensors. Civionics positions as a pure-play wireless sensor vendor for bridge health, winning DOT pilots where retrofit downtime must be negligible. Start-ups exploit white spaces in secondary-road monitoring by packaging sub-USD 2 MEMS sensors with AI-in-a-box gateways, appealing to county engineers with limited IT staff.

Strategic partnerships focus on de-risking full-stack deployments: cloud hyperscalers sign MOUs with civil-engineering firms to simplify data ingestion; telecom carriers bundle 5G private networks with edge gateways; and drone operators integrate orthophoto analytics into SHM dashboards. Quantum sensing research at CU Boulder hints at longer-term disruption by enabling single-sensor multi-parameter measurements, potentially trimming instrument counts on future projects.

Infrastructure Monitoring Industry Leaders

-

National Instruments Corporation

-

Pure Technologies Ltd. Company (Xylem Inc.)

-

Structural Monitoring Systems plc

-

Acellent Technologies, Inc.

-

Campbell Scientific, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Interoperability and standards alignment are creating a clear whitespace as asset owners connect heterogeneous sensors, video, access control, and OT data into unified monitoring and response workflows. The July 2026 release of ONVIF Profile V for cloud video surveillance points to broader vendor-neutral interfaces that reduce integration effort for multi-site operators, including transportation hubs and utilities using cloud/edge monitoring. IEC 62676-6:2026 also adds performance testing and grading rules for real-time intelligent video analysis devices, giving procurement teams a concrete benchmark for specifying analytics performance across scenarios relevant to critical sites.

Regulatory and national standards activity also supports opportunities for compliant monitoring upgrades and retrofit programs that combine cyber and physical assurance. In May 2026, China implemented GB/T 46364-2025 defining technical requirements for boundary security interaction systems in video surveillance, reinforcing demand for solutions that coordinate sensors, analytics, and access control at site perimeters. In the United States, FERC actions in March 2026 approving updates to CIP standards, including strengthened cybersecurity management controls, increase the focus on monitoring, logging, and governance for critical infrastructure operators. This supports service-led offerings such as secure onboarding, continuous monitoring configurations, and audit-ready data pipelines across on-premise and hybrid deployments.

Recent Industry Developments

- May 2026: Emerson expanded NI Nigel AI across the LabVIEW+ Suite portfolio, including LabVIEW, InstrumentStudio, TestStand, and SystemLink. The update embeds AI assistance deeper into test and monitoring workflows used to validate sensors and data-acquisition systems. It also strengthens Emerson's positioning around faster configuration and maintenance of monitoring stacks across distributed infrastructure environments.

- July 2025: AFL and VIE Technologies announced a strategic partnership combining fiber connectivity with AI-driven predictive monitoring for power transformers and data center mechanical equipment. The collaboration aligns hardware connectivity with analytics to streamline deployment and operations across multi-site assets. It signals growing emphasis on end-to-end monitoring solutions in critical infrastructure networks.

- April 2024: Xylem secured a contract to inspect 24-inch water mains in Rockville, Maryland, using its inspection technology for condition assessment. The project underscores municipal investment in monitoring and inspection to reduce non-revenue water and unplanned failures. It supports adoption of specialized sensing and analytics services where utilities lack in-house diagnostic capabilities.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the infrastructure monitoring market is defined as the revenues earned from solutions and services used to track the condition and performance of physical infrastructure assets by capturing measurements, transmitting them, and converting them into actionable alerts and insights.

Scope exclusions: We exclude general IT log monitoring, standalone cybersecurity tools, and routine SCADA-only monitoring that does not provide asset-condition monitoring outcomes.

Segmentation Overview

-

By Technology

- Wired

- Wireless

-

By Offering

- Hardware

- Software

- Services

-

By Deployment Model

- On-premise

- Cloud / Edge

-

By Application

- Corrosion Monitoring

- Crack / Strain Detection

- Vibration and Dynamic Load Monitoring

- Remote Structural-Health Monitoring (SHM)

- Environmental and Seismic Monitoring

-

By End-user Industry

- Civil Infrastructure (Bridges, Roads, Tunnels, Dams)

- Energy and Utilities

- Aerospace and Defense

- Mining and Metals

- Oil and Gas / Petro-chemicals

- Transportation (Harbors, Rail, Airports)

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Argentina

- Rest of South America

-

APAC

- China

- Japan

- India

- South Korea

- ASEAN

- Rest of APAC

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Nordics

- Rest of Europe

-

Middle East and Africa

- GCC

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the basic structure of the market and to sanity-check the direction of demand across regions and end users. We reviewed public references such as transportation and infrastructure statistics from agencies like the US Department of Transportation and the Federal Highway Administration, energy and grid reliability publications such as those from the US Energy Information Administration, and standards and guidance documents from bodies such as ISO and NIST.

To understand adoption patterns and deployment constraints, we also referred to association and program websites that track bridges, tunnels, rail, and utility assets, along with peer-reviewed journal articles on structural health monitoring and sensing. Company annual reports, investor presentations, and reputable press were used to map offering types and typical go-to-market routes, and paid subscriptions for company financials and patents helped fill gaps on product positioning and innovation focus. These sources are illustrative only, and many other public references were also used for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary work centered on interviews and surveys with solution providers, system integrators, asset owners, and technical consultants who influence monitoring budgets and specifications. Coverage was balanced across major regions so assumptions on pricing, replacement cycles, and rollout pace could be tested, then refined where desk research left gaps.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 12% | APAC: 41% |

| Mid tier: 58% | Functional/Unit leaders: 41% | EMEA: 33% |

| Smaller Players: 17% | Managers: 47% | Americas: 26% |

Market-Sizing & Forecasting

Sizing started with a top-down build where infrastructure spending signals and asset base indicators were used to reconstruct the addressable monitoring demand pool, which was then filtered by adoption rates for wired and wireless monitoring and typical project intensities. The totals were corroborated with selective bottom-up approximations, such as sampled project volumes by asset class multiplied by typical system pricing, and then adjusted where they did not align.

Key inputs included the installed base of aging bridges and transport corridors, capital and maintenance spending patterns for civil and utility assets, sensor and data-acquisition unit pricing trends, the shift toward cloud and edge analytics, and observed refresh or calibration cycles for monitoring systems. Forecasts were built using scenario analysis, where adoption and pricing paths were flexed based on expert expectations for project pipelines, regulation-driven inspections, and the pace of multi-hazard monitoring rollouts. When direct data was thin for smaller geographies, we used proxy indicators like infrastructure renewal budgets and construction activity, then verified the implied uptake during primary discussions.

Data Validation & Update Cycle

Outputs were checked against independent signals such as infrastructure maintenance allocations, reported deployment activity, and the pace of wireless sensor network adoption, which helped confirm whether the modeled demand looked realistic. Variance checks were run across regions and end-user types, and any outliers were reviewed through a second analyst pass before sign-off.

The model assumptions and calculations go through a multi-step internal review, and follow-up calls are triggered when interview feedback conflicts with observed market signals or when pricing shifts sharply. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery review is completed so clients receive the most current view available.

Mordor Intelligence's Infrastructure Monitoring Market Size Measured Against Other Published Estimates

Published market sizes for infrastructure monitoring can look far apart because firms do not always count the same product boundaries, and they often anchor the model to different base years. Differences also come from how services are treated, how pricing is stepped down over time, and how quickly assumptions get refreshed after major project or policy changes.

In our checks, the biggest gap usually comes from mixing physical-asset monitoring revenues with broader IT infrastructure monitoring, and then applying a single average price across very different asset classes. Another common driver is using an older year as the base and carrying forward adoption assumptions without re-testing them with asset owners, which is why the spread is most visible when the model includes sensors, data acquisition, analytics, and related services together, and that narrower counting approach is kept consistent by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.74 B (2026) | |

| Regional Consultancy A | USD 6.20 B (2025) | Uses a different base year and appears to reflect a tighter near-term view, with limited clarity on whether analytics and ongoing monitoring services are fully included across asset types. |

| Industry Publisher B | USD 6.32 B (2025) | Starts from a 2025 base and may apply broad average pricing across wired and wireless deployments, which can understate higher-complexity projects like bridges, tunnels, and utilities. |

Overall, the table shows that year selection and scope boundaries explain most of the differences, rather than a disagreement on the direction of growth. By tying the total to observable asset needs, adoption rates, and realistic price bands, the estimate remains transparent and easier to reproduce with clear inputs.

Key Questions Answered in the Report

How big is the Infrastructure Monitoring Market?

The Infrastructure Monitoring Market size is expected to reach USD 8.74 billion in 2026 and grow at a CAGR of 9.96% to reach USD 14.05 billion by 2031.

What is the current size of the infrastructure monitoring market?

The market is valued at USD 8.74 billion in 2026.

How fast is the infrastructure monitoring market expected to grow?

It is projected to advance at a 9.96% CAGR and reach USD 14.05 billion by 2031.

Which technology segment holds the largest infrastructure monitoring market share?

Wireless systems dominate with 61.35% share in 2025 and continue to outpace other technologies.

Which application area is expanding most rapidly?

Environmental and seismic monitoring leads with a 12.18% CAGR through 2031.

Which region offers the strongest growth outlook?

Asia-Pacific shows the fastest expansion, with a 11.86% CAGR forecast for 2026-2031.

Why are digital twins important for infrastructure monitoring?

Digital twins integrate real-time sensor data with virtual models, enabling predictive maintenance and reducing lifecycle costs across bridges, tunnels, and utility networks.

Page last updated on: