Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The North America People Screening Market Report is Segmented by Technology (X-Ray Systems, Millimeter-Wave Scanners, and More), Deployment Mode (Fixed Checkpoint, Mobile Systems), Detection Method (Metallic, Non-Metallic, Identity Verification), End-User (Transportation, Government, Commercial, and More), and by Country. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

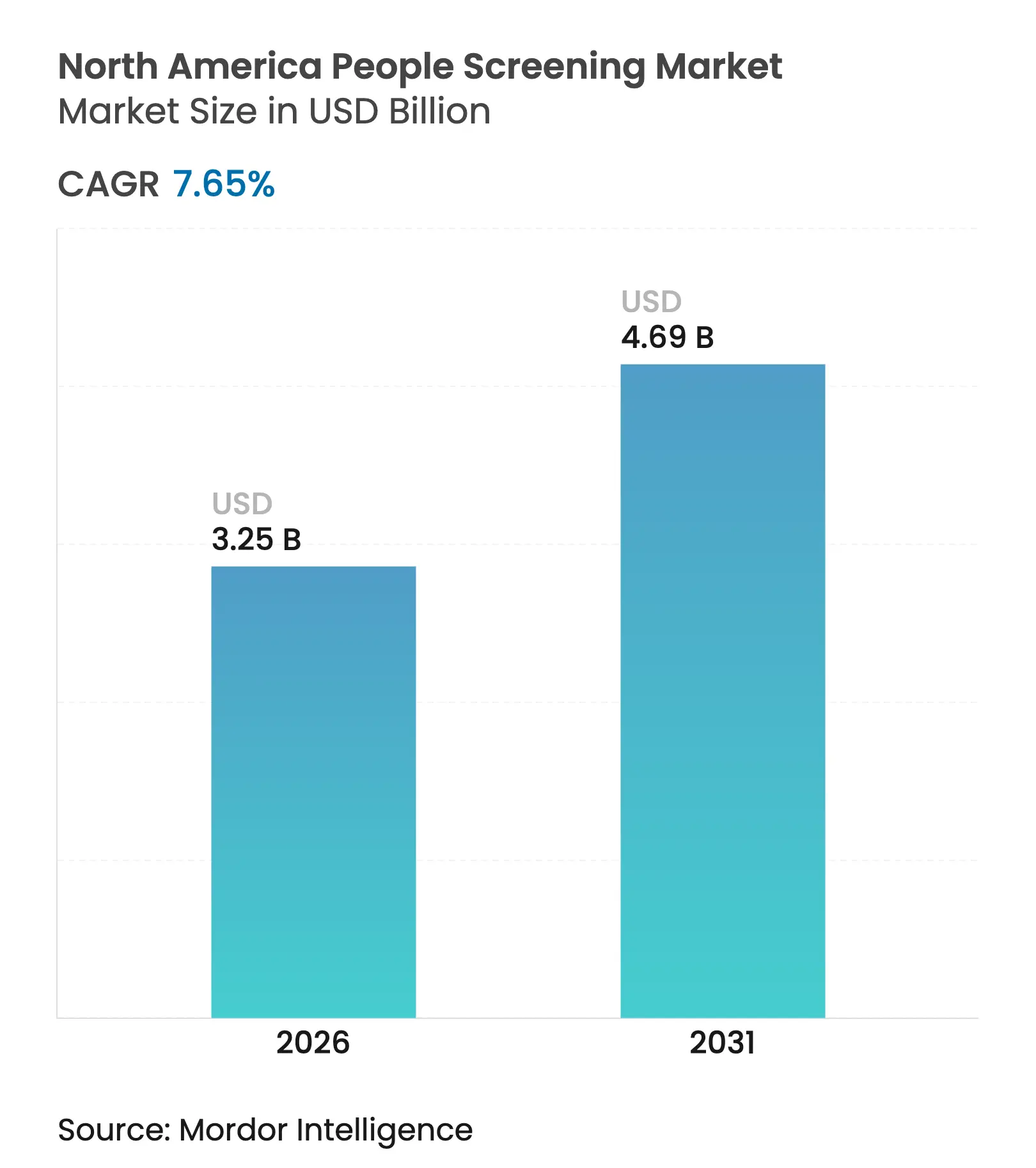

| Market Size (2026) | USD 3.25 Billion |

| Market Size (2031) | USD 4.69 Billion |

| Growth Rate (2026 - 2031) | 7.65 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The North America people screening market size was valued at USD 3.02 billion in 2025 and estimated to grow from USD 3.25 billion in 2026 to reach USD 4.69 billion by 2031, at a CAGR of 7.65% during the forecast period (2026-2031). Strong federal funding cycles, a pivot toward contactless biometrics, and security retrofits across stadiums and schools are expanding the total addressable opportunity for vendors. [1]Transportation Security Administration, “Fiscal Year 2025 President’s Budget Request,” tsa.gov Airport authorities are shifting capital budgets toward high-definition CT scanners that let passengers keep electronics and liquids in bags, thereby improving throughput while meeting rigorous detection thresholds. Cannabis retail legalization is standardizing employee vetting rules across states and provinces, creating recurring hardware and software demand at dispensaries. Rising e-commerce returns along U.S.–Mexico corridors are pushing logistics operators to adopt mobile screening pods that can be repositioned as volumes fluctuate. Procurement timelines remain sensitive to semiconductor supply constraints, yet the strategic intent of regulators is clear—modernize infrastructure, close detection gaps, and reduce screening friction without compromising privacy.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

TSA-mandated Checkpoint Modernization Accelerating U.S. Airport People Screening Investments TSA-mandated Checkpoint Modernization Accelerating U.S. Airport People Screening Investments | +1.8% | United States, spillover to Canada | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.8% | Geographic Relevance:United States, spillover to Canada | Impact Timeline:Medium term (2-4 years) |

Rapid Adoption of Contactless Biometrics in North American Stadiums & Arenas Rapid Adoption of Contactless Biometrics in North American Stadiums & Arenas | +1.2% | United States & Canada, concentrated in major metropolitan areas | Short term (≤ 2 years) | |||

Expanding Cannabis Retail & Logistics Network Necessitating Employee Screening Expanding Cannabis Retail & Logistics Network Necessitating Employee Screening | +0.9% | United States & Canada, state/provincial regulatory variations | Medium term (2-4 years) | |||

U.S. Infrastructure Investment & Jobs Act Funding Subway & Rail Security Upgrades U.S. Infrastructure Investment & Jobs Act Funding Subway & Rail Security Upgrades | +0.7% | United States, focus on Northeast Corridor and major transit systems | Long term (≥ 4 years) | |||

Growth of Cross-Border E-commerce Returns Centers Requiring High-Throughput Screening Growth of Cross-Border E-commerce Returns Centers Requiring High-Throughput Screening | +0.6% | US-Mexico border regions, expanding to US-Canada corridors | Medium term (2-4 years) | |||

Rising Active-Shooter Incidents Driving Security Retrofits in K-12 Schools & Universities Rising Active-Shooter Incidents Driving Security Retrofits in K-12 Schools & Universities | +0.5% | United States & Canada, accelerated adoption in urban districts | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

TSA-mandated checkpoint modernization accelerating U.S. airport people screening investments

Federal appropriations totaling USD 11.8 billion for the Transportation Security Administration in 2025 assign USD 99 million specifically for credential authentication and CT scanner procurement, triggering multiyear refresh cycles across Category X airports. The self-service screening prototype in Las Vegas allows passengers to control the process, reducing staff hours by up to 30% while preserving lane throughput. The Department of Homeland Security’s Screening at Speed program adds high-definition imaging that operates at millimeter-wave emissions of −50 dBm/cm², well below safety thresholds.[2]U.S. Department of Homeland Security, “Reimagining Imaging at the Airport,” dhs.govDenver International Airport’s USD 1.3 billion checkpoint expansion exemplifies how airports bundle new lanes, automated bin return, and CAT-2 authentication into integrated projects. Together, these deployments set performance benchmarks that other U.S. hubs and Canadian gateways rapidly emulate.

Rapid adoption of contactless biometrics in North American stadiums & arenas

Venue operators face intense pressure to shorten gate queues and boost secondary spend on concessions. Major League Baseball and CLEAR introduced biometric ticketing that matches fingerprints or faces to credentials, cutting check-in times to under 15 seconds. Seattle stadiums layer the same biometric token into payments and age verification, linking security with revenue generation. Resistance from law-enforcement unions, as seen in Las Vegas, underlines the importance of consent frameworks and transparent data governance. Despite friction, the tangible uplift in fan satisfaction and sponsorship inventory is compelling ownership groups to budget for next-generation access control.

Expanding cannabis retail & logistics network necessitating employee screening

Canada’s national clearance program records a 95% approval rate, yet still demands criminal background verification and law-enforcement database queries, anchoring predictable demand for vetting tools.[3]Health Canada, "About the process: Cannabis security clearances," canada.ca Washington State imposes rolling disclosure of offenses within 30 days, reinforcing continuous monitoring use cases. British Columbia seeks to scrap worker-level checks, but federal air-cargo rules still compel 100% screening for cannabis consignments, ensuring technology pull-through at logistics hub. These overlapping mandates standardize risk-based screening across cultivation, transport, and storefronts.

U.S. Infrastructure Investment & Jobs Act funding subway & rail security upgrades

The Bipartisan Infrastructure Law earmarks USD 108 billion for public transit, with a portion prioritized for cybersecurity resilience and passenger inspection. The Northeast Corridor will receive USD 16.4 billion to modernize tunnels and stations, embedding intelligent screening gates into architectural redesigns.[4]U.S. Department of Transportation, "President Biden Advances Vision for World Class Passenger Rail with USD16 Billion Investment in America's Busiest Corridor," railroads.dot.govThe Metropolitan Transportation Authority’s USD 254 million grant packages accessibility upgrades with security kiosks that align with universal design. These commitments guarantee a baseline of install demand for at least a decade, offering suppliers annuity streams from maintenance contracts and software updates.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Increasing Privacy Litigation Over Body Scanners in the United States Increasing Privacy Litigation Over Body Scanners in the United States | -0.4% | United States, potential spillover to Canada | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-0.4% | Geographic Relevance:United States, potential spillover to Canada | Impact Timeline:Medium term (2-4 years) |

Canada's Radio-frequency Exposure Rules Limiting Millimeter-Wave Deployment Canada's Radio-frequency Exposure Rules Limiting Millimeter-Wave Deployment | -0.3% | Canada, potential influence on U.S. border facilities | Long term (≥ 4 years) | |||

Semiconductor Supply Constraints Raising Lead Times for Advanced Imaging Systems Semiconductor Supply Constraints Raising Lead Times for Advanced Imaging Systems | -0.2% | North America, global supply chain impacts | Short term (≤ 2 years) | |||

Shortage of Qualified Technicians for Calibration & Maintenance in Rural Airports Shortage of Qualified Technicians for Calibration & Maintenance in Rural Airports | -0.1% | United States & Canada, rural and remote regions | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Increasing privacy litigation over body scanners in the United States

The Electronic Privacy Information Center’s lawsuits forced the withdrawal of backscatter X-ray units and continue to scrutinize millimeter-wave algorithms that might store raw images. Ongoing claims argue that intrusive scans could divert travelers to less safe road transport, raising public-health concerns. Discovery motions reveal gaps in radiation testing documentation, prompting airports to defer procurement until clarity emerges. Vendors must now invest in privacy-by-design firmware features such as software-only silhouettes and dynamic mask algorithms. The litigation climate therefore slows the replacement cycle for legacy equipment and marginally tempers the growth slope of the North America people screening market.

Canada’s radio-frequency exposure rules limiting millimeter-wave deployment

Innovation, Science and Economic Development Canada mandates extensive compliance dossiers before listing devices on the Radio Equipment List. Health Canada applies conservative MRI-derived reference levels that can restrict scanner power output. Certification timelines therefore stretch beyond U.S. FCC benchmarks, often adding six to nine months. The Canadian Air Transport Security Authority’s decision to prioritize CT over millimeter-wave platforms underscores how regulatory friction shapes procurement roadmaps. Manufacturers are responding with dual-SKU strategies—high-power units for U.S. settings and lower-power variants for Canadian gateways—raising production complexity and cost.

By Technology: AI-enhanced systems challenge millimeter-wave dominance

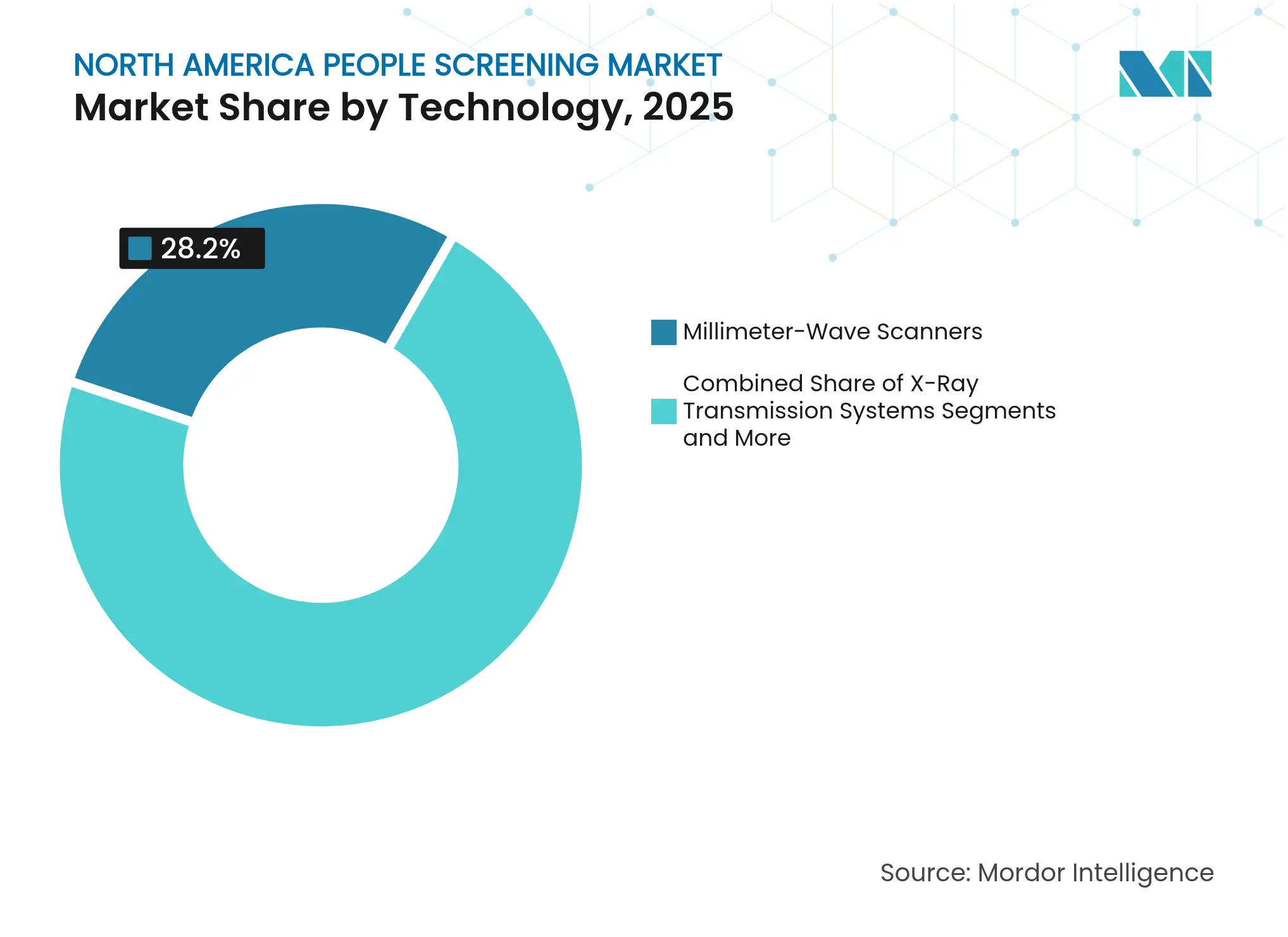

Millimeter-wave scanners still represented 28.20% of the North America people screening market share in 2025, anchored by almost universal deployment at U.S. Transportation Security Administration checkpoints. Yet hybrid AI-enhanced screening pods are on track for an 8.35% CAGR, injecting machine-learning analytics that reduce false alarms and speed adjudication. The Department of Homeland Security’s high-definition imaging prototypes confirm that algorithmic inspection will supersede manual resolution, setting a trajectory where dual-energy CT, object classification, and facial recognition operate in one enclosure.

Early mover airports are already replacing single-modality portals with jumbo pods that handle people and bags simultaneously, foreshadowing convergence cycles across transit hubs, stadiums, and border crossings. X-ray transmission systems will retain relevance where cost sensitivity overrides space constraints, while passive terahertz imaging serves niche concealed weapon detection missions. In parallel, biometric identification modules are displacing boarding pass scanners as identity anchors. These overlapping trends keep the North America people screening market in a state of continuous technology leapfrog, rewarding vendors able to launch modular upgrades rather than forklift replacements.

Note: Segment shares of all individual segments available upon report purchase

By Deployment Mode: Mobile systems gain traction

Fixed checkpoint lanes account for 71.60% of the North America people screening market size, reflecting legacy capital layouts in aviation and government facilities. Automation investments, such as integrated belts that return bins, preserve this mode’s productivity edge under peak loads. However, mobile and portable systems are forecast to log a 8.95% CAGR because operators in school districts, convention centers, and border pop-up sites need flexible capacity.

Baltimore County and Alexandria City schools demonstrate how wheeled sensor towers can be rolled into entryways at start-of-day and stored off-site during class hours, avoiding costly renovation. Transportation Security Administration field teams also deploy trailer-mounted CT units at seasonal airports. Such examples highlight a strategic pivot whereby hardware form factors match fluctuating risk profiles, thereby broadening addressable demand within the North America people screening market.

By Detection Method: Identity verification emerges as growth leader

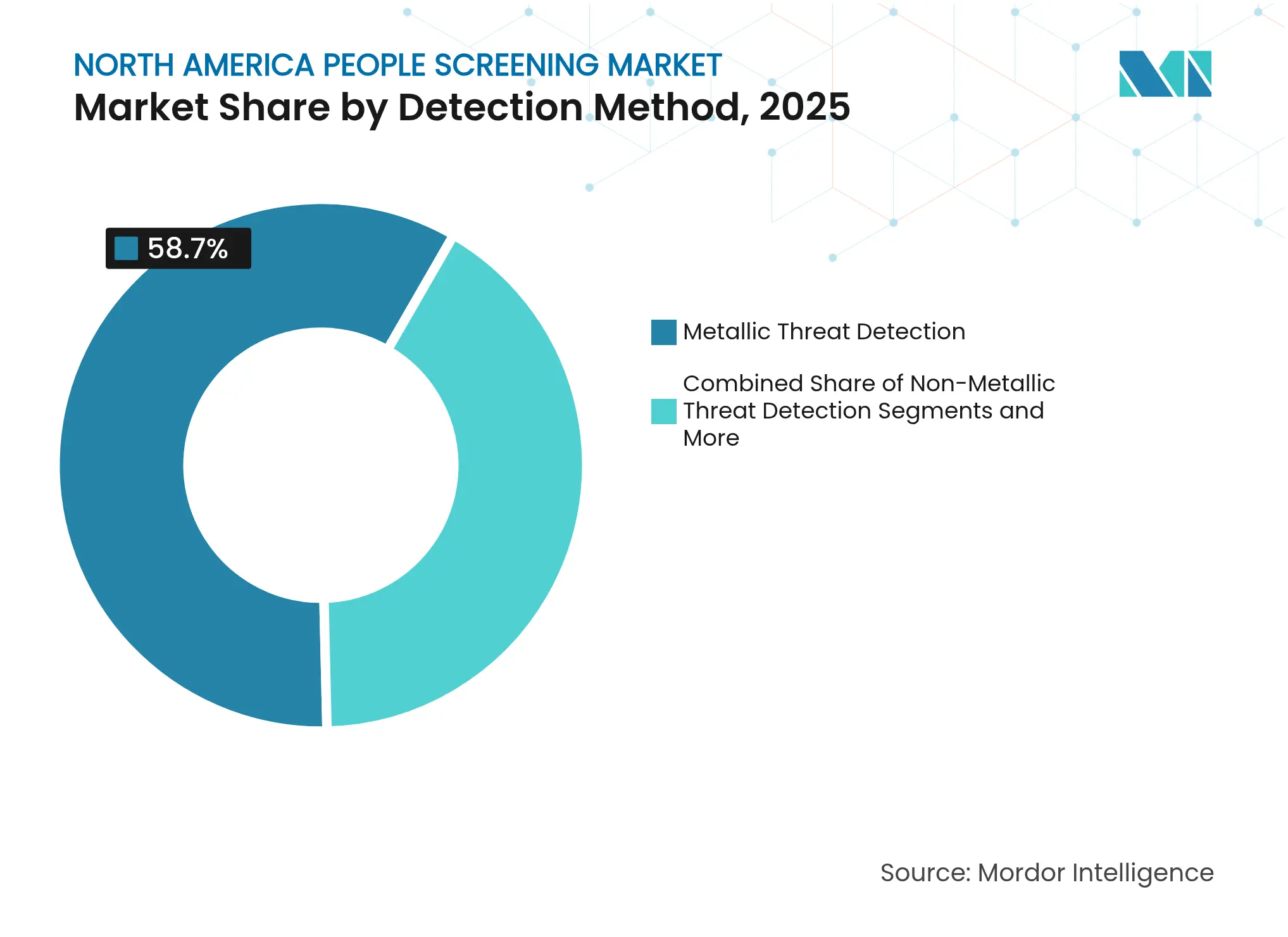

Metallic threat detection secured 58.70% of the North America people screening market size in 2025, yet identity and credential verification solutions are projected to grow fastest at 9.15% CAGR. Enforcement of REAL ID from May 2025 drives airport demand for readers that parse state and provincial barcodes while executing facial matches. The U.S. Customs and Border Protection’s passenger processing program cuts transaction time by 90%, proving that biometric tokenization is not just secure but operationally superior.

Non-metallic detection is improving due to advances in 3D object libraries that now flag polymer and ceramic weapons. The marriage of threat detection with credential validation inside one decision engine creates a flywheel where each scan enriches the library, lifting accuracy in real time. Suppliers that expose open APIs for airline, stadium, and property-management apps are positioned to capture incremental software revenue, reinforcing the resilience of the North America people screening market.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Sports venues drive growth beyond airports

Airports retained a commanding 44.90% share of the North America people screening market size in 2025 because federal mandates tie passenger throughput to specific detection standards. Nevertheless, sports and entertainment venues will clock a 8.85% CAGR as they re-tool fan journeys from ticket purchase to concession checkout. Major League Baseball’s rollout with CLEAR exemplifies how layered biometric flows monetize security investments through higher per-capita spend.

Warehouse and logistics hubs, particularly along the U.S.–Mexico border, add volume as 70% cargo-scan targets approach. Educational institutions are moving from pilot projects to district-wide installs, encouraged by grant pools that combine school safety and mental health allocations. Collectively, these adjacencies insulate the North America people screening market from aviation traffic cycles, paving multi-segment revenue pathways for system integrators and component suppliers.

The United States generated 81.90% of North America people screening market revenue in 2025, supported by USD 11.8 billion in TSA appropriations, Infrastructure Investment and Jobs Act disbursements, and an ambitious plan to scan 70% of border cargo. Federal contracting frameworks such as the Capital Investment Plan guarantee multiyear order visibility for CT, CAT-2, and biometric devices. State and municipal entities enhance top-down mandates with local initiatives that retrofit schools and courthouses, translating national security posture into granular equipment demand.

Canada follows with a sophisticated yet smaller install base, anchored by the Canadian Air Transport Security Authority’s CT expansion program across major hubs including Vancouver and Calgary. Ottawa’s commitment to replace aging large-scale imaging at land borders further diversifies opportunities. Stringent radio-frequency exposure rules, however, tilt airports toward X-ray over millimeter-wave solutions, influencing vendor product roadmaps and manufacturing allocations. Provincial variability in cannabis legislation also shapes screening specifications at retail stores and warehouses, adding complexity and niche customization in the North America people screening market.

Mexico is the fastest-expanding geography with an 7.75% CAGR outlook as bilateral trade edges toward USD 1 trillion by 2028. Customs authorities are scaling inspection yards and secondary examination zones like the Roma logistics park, rolling out high-throughput, trailer-sized imaging portals. Rising tourism and cruise traffic in Caribbean nations prompt airport and seaport operators to adopt modular people screening pods, yet volumes remain sub-scale relative to mainland corridors. Collectively, these geographic dynamics sustain balanced demand curves across the North America people screening market, preventing over-reliance on any single national budget.

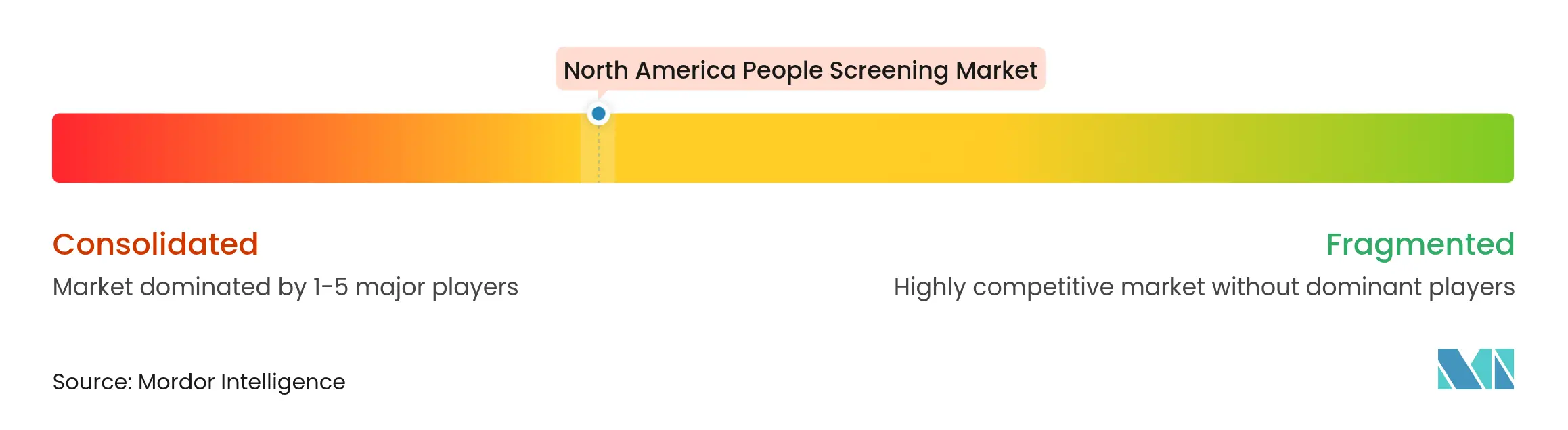

Market Concentration

The North America people screening market is moderately concentrated, with a handful of multinational suppliers capturing the bulk of federal and Tier-1 airport contracts through proprietary imaging algorithms and compliance credentials. Patent portfolios that cover automatic target recognition and AI-assisted resolution underpin competitive moats. Established players sustain margins by cross-selling maintenance and analytics subscriptions under five-to-ten-year master service agreements.

Entrants leverage differentiated capabilities—such as passive terahertz antennas, cloud-native screening orchestration, or privacy-preserving facial encoding—to penetrate verticals like sports venues and cannabis dispensaries where incumbents lack tailored offerings. Technology convergence is accelerating; vendors increasingly bundle credential authentication with multi-energy threat detection to deliver turnkey pods that fit within existing architectural footprints. The TSA’s public-private innovation consortia amplify this race, offering pilot lanes where experimental hardware gains real-world data sets that shorten commercialization cycles.

Strategic moves include vertical integration through mergers, such as First Advantage’s USD 2.2 billion acquisition of Sterling Check that augments background screening breadth. OEMs also forge channel alliances with stadium consultants and school-security contractors to minimize sales-cycle friction. Looking forward, platform openness, cybersecurity certifications, and AI auditability emerge as decisive buying factors, compelling suppliers to invest in SOC 2 compliance, explainable AI workflows, and continual firmware patching to defend share in the North America people screening market.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

People screening refers to inspecting individuals entering secure areas such as airports, government buildings, sporting events, or other sensitive locations. The main purpose of people screening is to identify potential threats, such as weapons or explosives, and individuals with malicious intent, such as terrorists or criminals. The study focuses on the market analysis of people screening products sold across the globe, and market sizing encompasses the revenue generated through these products sold by various market players. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which are expected to support the market estimations and growth rates during the forecast period. The study further analyzes the overall impact of macroeconomic factors on the ecosystem.

The North American people screening market is segmented by technology (X-ray systems, metal detectors, body scanners, biometric systems, millimeter wave whole body scanners, and other technologies), end-user industry (corporate buildings, warehouse and logistics, commercial spaces, transportation infrastructure [airports, railway stations, etc.], government buildings, law enforcement, and other end-user industries), and country (United States and Canada). The market sizes and forecasts are provided in terms of value (USD) for all the segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.