Pediatric Telehealth Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

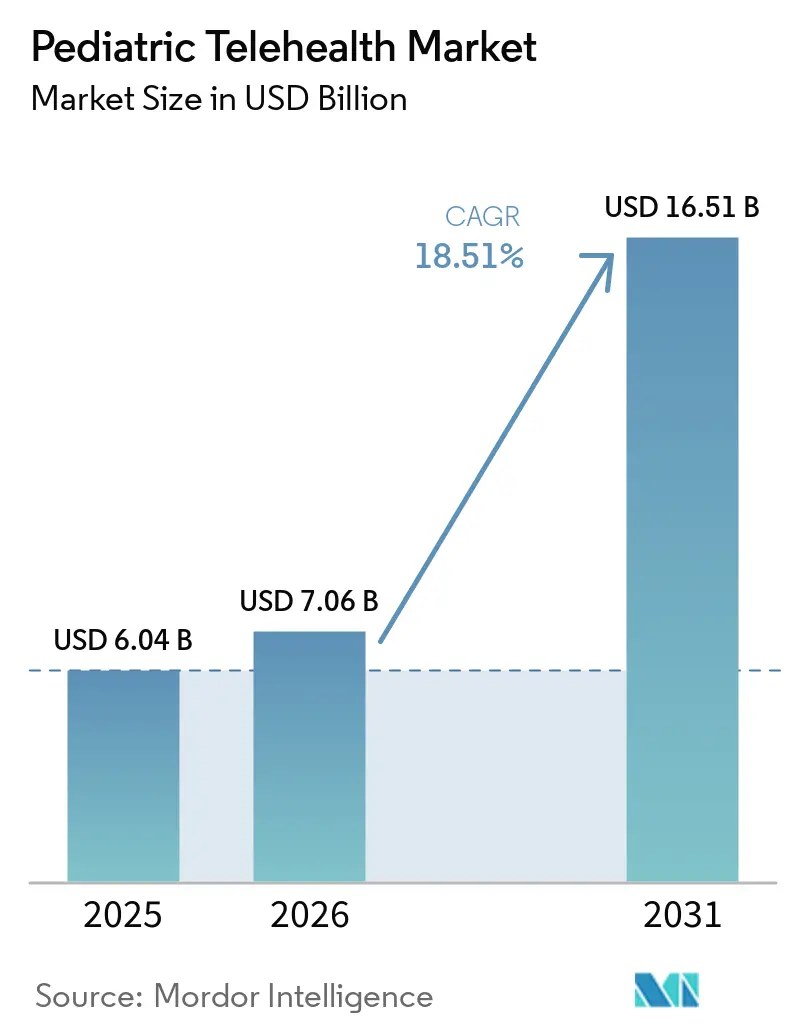

| Market Size (2026) | USD 7.06 Billion |

| Market Size (2031) | USD 16.51 Billion |

| Growth Rate (2026 - 2031) | 18.51% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pediatric Telehealth Market Analysis by Mordor Intelligence

The Pediatric Telehealth Market size is expected to increase from USD 6.04 billion in 2025 to USD 7.06 billion in 2026 and reach USD 16.51 billion by 2031, growing at a CAGR of 18.51% over 2026-2031.

The pediatric telehealth market is moving from a convenience channel to a core access model because specialist shortages are leaving large parts of rural care networks without local pediatric coverage. Demand is rising fastest where mental and behavioral care needs are outpacing specialist capacity, which is making virtual access more central to routine pediatric care pathways. Public funding, school-based delivery, and clearer Medicaid and CHIP guidance are helping the pediatric telehealth market scale through formal care pathways rather than one-off virtual visits. Opportunity is also widening across Europe and Asia Pacific as telemedicine networks shorten travel times and extend scarce pediatric expertise into secondary hospitals and underserved communities. Competition is getting sharper as large telehealth platforms, pediatric specialists, and device-enabled care models pursue growth while privacy rules and broadband gaps continue to limit full access.

Key Report Takeaways

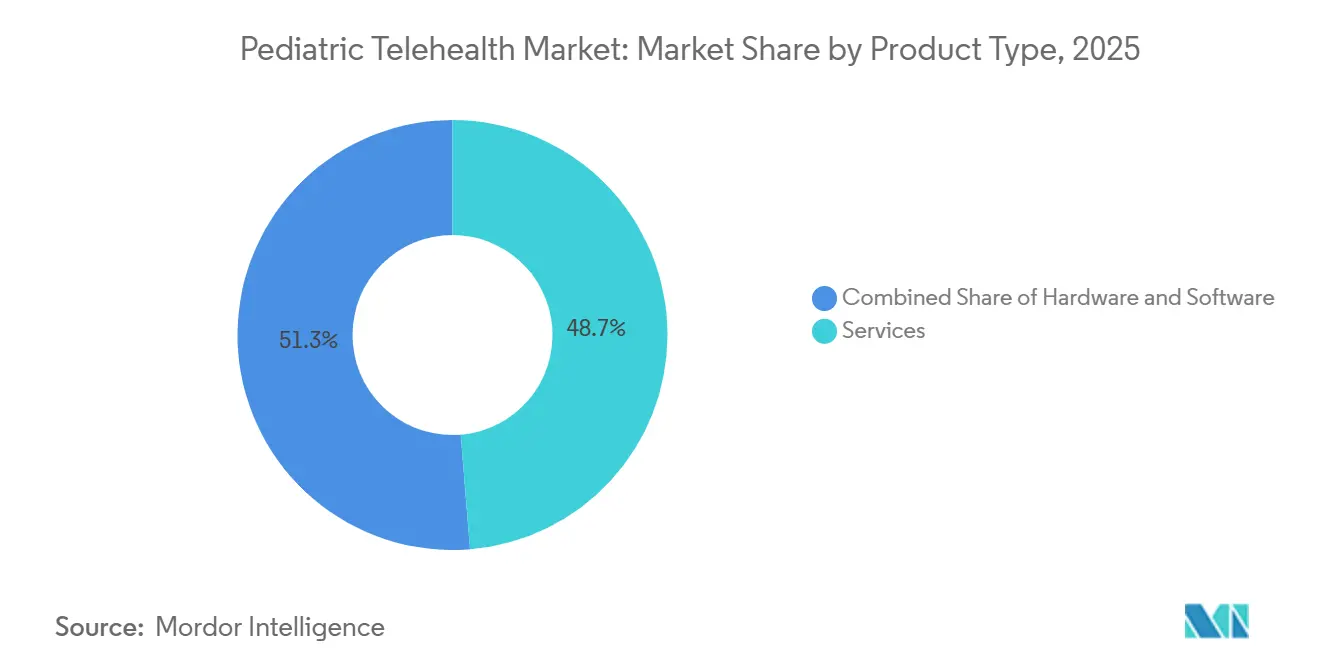

- By product type, services held 48.66% share in 2025, while software is forecast to expand at 19.68% CAGR through 2031.

- By delivery mode, web-based accounted for 44.87% share of the pediatric telehealth market size in 2025, while cloud-based delivery is projected to grow at 20.03% CAGR through 2031.

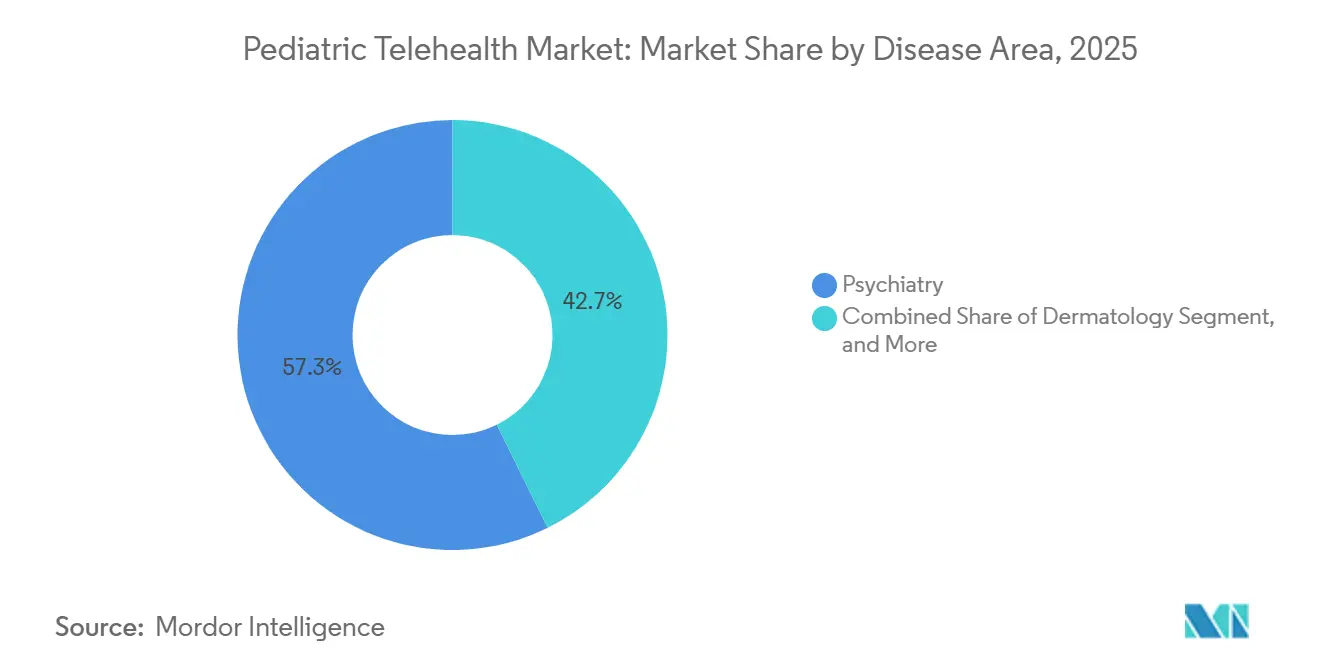

- By disease area, psychiatry held 57.27% of the pediatric telehealth market share in 2025, while neurological medicine is forecast to advance at 19.13% CAGR through 2031.

- By end user, providers held 50.23% share in 2025, while payers are projected to grow at 20.85% CAGR through 2031.

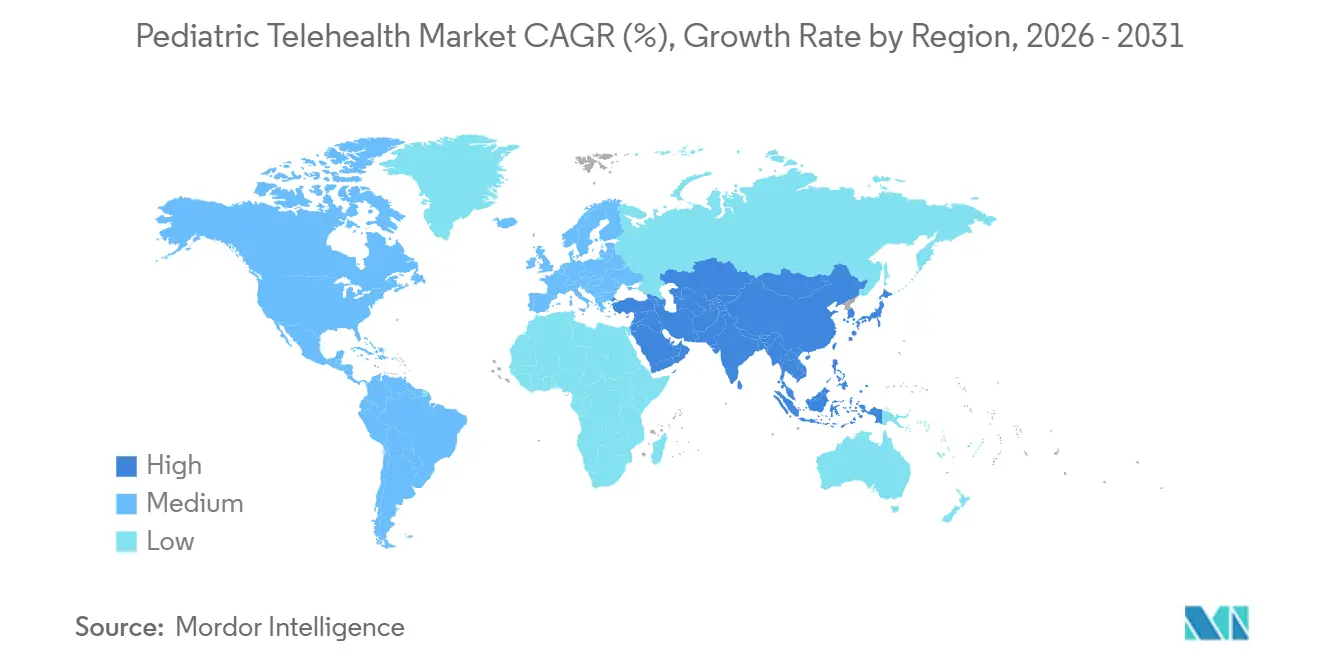

- By geography, North America led with 44.39% share in 2025, while Asia Pacific is projected to grow at 21.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pediatric Telehealth Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pediatric Specialist Shortages And Rural Access Gaps | +3.5% | Global, acute in North America, rural Europe, and South and Southeast Asia | Long term (≥ 4 years) |

| Rising Pediatric Mental And Behavioral Care Demand | +4.2% | Global, highest in North America, followed by Western Europe and East Asia | Medium term (2-4 years) |

| Remote Monitoring For Chronic Pediatric Conditions | +2.8% | North America and Europe, early stage in Asia Pacific and Middle East and Africa | Medium term (2-4 years) |

| Medicaid, CHIP, And Pediatric Telehealth Funding Support | +2.1% | United States centric, with spillover to comparable public payer models in Canada, Germany, and France | Short term (≤ 2 years) |

| School-Based Reimbursement And Campus-Access Mandates | +1.8% | North America primarily, emerging in Europe and Latin America | Short term (≤ 2 years) |

| Connected Peripherals That Improve Virtual Exam Closure | +1.5% | Global, led by North America, accelerating in Asia Pacific core markets, with spillover to Middle East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Pediatric Specialist Shortages and Rural Access Gaps

The pediatric telehealth market is being pushed forward by a care access gap that keeps widening in rural and low-density areas. Baylor College of Medicine reported in 2025 that 58.7% of rural counties and 90.4% of fully rural counties in the United States had no general pediatrician.[1]Baylor College of Medicine, “How the Pediatric Workforce Shortage Places Rural Kids at Risk in a Changing Healthcare Landscape,” Baylor College of Medicine Blog Network, blogs.bcm.edu The pressure is even harder to absorb, as local hospitals no longer have strong pediatric coverage across outpatient and acute settings. UC Davis Health found in September 2024 that hybrid school-based telehealth visits for pediatric physiatry saved USD 100 per visit in specialist travel costs and showed no statistically significant difference in parent satisfaction compared with in-person care. In Northeast Germany, the RTP-Net tele-pediatric network found that teleconsultation changed or refined the clinical diagnosis in 57.7% of cases, which shows that virtual pediatric assessment is already influencing real treatment decisions rather than only screening or triage.

Rising Pediatric Mental and Behavioral Care Demand

The pediatric telehealth market is seeing its strongest demand pull from mental and behavioral care. Diagnosed mental health conditions among US children increased 35% between 2016 and 2023, which has raised pressure on a system that already struggles with specialist availability.[2]Ryan K. McBain et al., “US Child Mental Health Care Need, Unmet Needs, and Difficulty Accessing Services,” JAMA Pediatrics, jamanetwork.com RAND reported in 2025 that 45.3% of adolescents receiving mental health treatment used telehealth, with office-based specialty care showing the highest concentration of virtual delivery.[3]Joshua Breslau et al., “Telehealth Use for Mental Health Treatment Among US Adolescents,” Journal of Adolescent Health, rand.org A 2025 retrospective cohort study in JMIR Mental Health found that virtual pediatric mental health episodes involved 18% fewer visits than in-person episodes, which matters for both care efficiency and payer economics. CMS guidance issued in September 2024 supports interprofessional teleconsultation through EPSDT, which is helping primary care settings extend behavioral care capacity without relying only on specialist referral growth.

School-Based Reimbursement and Campus-Access Mandates

The pediatric telehealth market is also gaining momentum because school-based care is moving into formal reimbursement and procurement channels. CMS announced USD 50 million in grants in 2024 for 18 states to implement or expand school-based Medicaid and CHIP services, with each state eligible for up to USD 2.5 million over 3 years. The US Department of Education reported that students are 6 times more likely to access mental health care when services are available in school settings, and Medicaid already pays USD 4 billion to USD 6 billion each year to school districts for school-based health services. This is shifting contracting power toward school districts and state agencies, which changes how telehealth vendors and providers enter the pediatric telehealth market. In North Carolina, NCDHHS partnered with Hazel Health in March 2025 to deliver virtual mental health services to nearly 400,000 K-12 students with support from UnitedHealthcare.

Connected Peripherals that Improve Virtual Exam Closure

The pediatric telehealth market is improving exam completion by using connected peripherals and clinically validated remote diagnostics. One of the core limits of pediatric virtual care has been the physical exam, especially for respiratory, ear, and throat assessment performed outside the clinic. A 2025 validation study from Singapore's National University Hospital found that the AeviceMD wearable achieved 85.3% sensitivity and 80.8% specificity for pediatric wheeze detection in emergency settings, with performance above 92% in home settings. As these tools improve, more follow-up and triage decisions can remain in the home or school environment instead of moving automatically to in-person care. That expands the software and device opportunity inside the pediatric telehealth market because platforms that can capture and interpret remote exam data become more clinically useful.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Child-Data Privacy and Cybersecurity Exposure | -1.2% | Global, highest compliance burden in North America (COPPA) and Europe (GDPR) | Short-term (≤ 2 years) |

| Broadband, Device, and Digital Literacy Gaps | -1.8% | Rural North America, Southeast US, South Asia, Sub-Saharan Africa; highest in MEA | Long-term (≥ 4 years) |

| Adolescent Confidentiality and Proxy-Portal Leakage | -0.7% | North America and Western Europe, where patient portal adoption among families is highest | Medium-term (2–4 years) |

| Interpreter, Multi-Caregiver, and Pediatric Exam Workflow Friction | -0.8% | Global, acute in multilingual and multi-caregiver households; prevalent in APAC, MEA, and Hispanic communities in North America | Medium-term (2–4 years) |

| Source: Mordor Intelligence | |||

Child-Data Privacy and Cybersecurity Exposure

The pediatric telehealth market operates in one of healthcare's most sensitive data environments because platforms handle medical, behavioral, and biometric information from minors. The FTC's 2025 COPPA update expanded the scope of personal information to include biometric identifiers and required separate verifiable parental consent for third-party data disclosures that are not integral to the service. That directly limits how pediatric platforms can use child data for model training, analytics, and external sharing. School-issued accounts can support educational purposes, but the rule does not allow those accounts to be used for broader commercial data use, which narrows monetization options for school-centered platforms. Full compliance was required by April 22, 2026, and operators now have to maintain written information security programs, annual risk assessments, and tighter handling of parental access issues under HIPAA guidance.

Broadband, Device, and Digital Literacy Gaps

The pediatric telehealth market still faces a basic access problem that cannot be solved by software alone. A 2025 national survey published in JMIR found that 19% of US households with children reported unreliable internet connectivity, and 13% to 15% of households with multiple plans still described their connection as unreliable. In rural high-needs counties in the Southeast United States, broadband subscription rates were only 43%, and the end of the Affordable Connectivity Program removed a subsidy that had supported 21 million households. A 2025 study in the American Journal of Psychiatry found that urban youth used telehealth mental health services at a rate of 32.7% versus 12.2% for rural youth, while video visit use was 41.6% for families above 400% of the federal poverty level versus 17% for families below 100% of the federal poverty level. Because these constraints sit outside provider control, infrastructure policy and affordability timelines will continue to shape the pediatric telehealth market more than product upgrades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Services Anchor Revenue, Software Commands Growth

Services held 48.66% of the pediatric telehealth market size in 2025, which kept care delivery at the center of current spending. Real-time consultations and remote patient monitoring continue to support behavioral health, chronic condition management, and post-discharge follow-ups across the pediatric telehealth market. The service layer remains especially entrenched in psychiatry and therapy, where ongoing clinician and family contact is central to treatment continuity. A 2025 Dutch study found that non-invasive home monitoring detected nocturnal heart rate elevation as the strongest passive marker of worsening asthma control in children, with an odds ratio of 2.1 for worse outcomes.

Software is the fastest-growing product type in the pediatric telehealth market, with a forecast CAGR of 19.68% through 2031. Integrated platforms are gaining ground in the pediatric telehealth industry because providers want EHR links, remote monitoring data, and care coordination in one workflow. Germany's Techped project is testing a multilingual mobile health platform for children with chronic conditions and received EUR 1.7 million, or USD 1.9 million, in federal research funding. Hardware demand is rising, but growth is less linear because clinical validation is moving faster than reimbursement coverage for the devices themselves.

By Delivery Mode: Web-Based Holds Its Ground, Cloud-Based Accelerates

Web-based delivery held 44.87% share in 2025 and remains the default option for many large school and provider networks. Browser access fits school-district IT settings where managed devices often restrict app installation. On-premises deployment still matters in large children's hospitals that want tighter control over protected health information. The updated COPPA framework is making vendor-managed security and documented controls more important across the pediatric telehealth market.

Cloud-based delivery is the fastest-growing mode in the pediatric telehealth market, with 20.03% CAGR projected through 2031. Growth is being driven by AI-supported diagnostics, multi-modal data ingestion, and the need for real-time escalation workflows. TytoCare's Smart Clinic Companion, introduced in October 2025 and now in commercial rollout in 2026, was built on a dataset of more than 7,000,000 exams that is growing 33% annually. Cloud platforms also give payers and health systems the analytics backbone needed to manage telehealth quality measures in the 2025 Child Core Set.

By Disease Area: Psychiatry Leads, Neurology Closes Fast

Psychiatry held 57.27% of pediatric telehealth market share in 2025 and remained the most established disease area for virtual pediatric care. CMS guidance, school-based grant programs, and Medicaid benefit design have all pushed reimbursement toward mental and behavioral health services. The Collaborative Care Model is active through PMHCA programs in 46 states and 8 entities, which reinforces telehealth as a routine consultation route for pediatric behavioral care. Diagnosed mental health conditions among US children increased 35% between 2016 and 2023, which helps explain why psychiatry remains the anchor use case.

Neurological medicine is the fastest-growing disease area in the pediatric telehealth market and is forecast to grow at 19.13% CAGR through 2031. Demand is rising as families seek faster follow-up for epilepsy, ADHD, autism spectrum disorder, and neuromuscular conditions. In Northeast Germany, pediatric neurology represented 50% of telemedical contacts in RTP-Net, and teleconsultation changed or refined the diagnosis in 57.7% of cases. In Chile, Red Salud UC-Christus integrated telemedicine into its autism spectrum disorder diagnostic pathway in 2025. Dermatology is increasingly suitable for virtual review, while radiology and dental remain less penetrated because imaging capture and hands-on examination still matter.

By End User: Providers Dominant, Payers Lead the Next Growth Wave

Providers held 50.23% of the pediatric telehealth market share in 2025, reflecting their early lead in telehealth infrastructure and reimbursement capture. Children's hospitals, provider groups, and federally qualified health centers remain the main operational hubs for service deployment across the pediatric telehealth market. School-linked programs have reinforced provider leadership because they extend existing clinical teams into classrooms and community sites. Direct family demand is also increasing, especially in mental health, where continuity and convenience affect retention.

Payers are the fastest-growing end-user group in the pediatric telehealth market, with forecast CAGR of 20.85% through 2031. This shift shows that payers are funding and contracting programs more directly as a way to reduce higher-cost downstream care in the pediatric telehealth industry. In North Carolina, NCDHHS and Hazel Health launched a virtual mental health program for nearly 400,000 K-12 students with support from UnitedHealthcare. Access oversight and quality reporting are also pushing payers to treat telehealth as a network adequacy tool rather than a side benefit.

Geography Analysis

North America held 44.39% of the pediatric telehealth market size in 2025 and remained the largest regional block. The United States drives most of that scale through Medicaid and CHIP reimbursement, school-based care pathways, and a large base of startup and provider activity. As of May 2024, 38 million children were enrolled in Medicaid and CHIP in the United States, giving the pediatric telehealth market the largest publicly financed pediatric demand pool in the world. Regional value is still constrained by uneven payment policy because 48 states and DC reimburse telemedicine, 39 states reimburse telemental health, and only 23 require payment parity.

Europe held the second-largest share in the pediatric telehealth market and shows how usage can rebound once telemedicine is tied to long-term care redesign. France recorded 13.9 million teleconsultations in 2024, up 20% from the prior year, and specialty teleconsultation represented 7% of psychiatrists' activity. Germany's TelEmergency Kids, launched in January 2025, shows how pediatric emergency triage is being extended from specialist centers into surrounding hospital networks. Europe also carries a high compliance burden under GDPR and the UK's Children's Code, which favors vendors that already built pediatric data governance into their platforms.

Asia Pacific is the fastest-growing region in the pediatric telehealth market and is projected to expand at 21.82% CAGR through 2031. Growth is supported by specialist shortages, expanding digital infrastructure, and national health system investment across China, India, Japan, and South Korea. In Singapore, National University Hospital validated the AeviceMD wearable in 2025 with 85.3% sensitivity and 80.8% specificity in emergency settings, with performance above 92% in home use. South America is smaller, but its operational case is becoming clearer, with Colombia's SPLA model resolving 70% of pediatric teleconsultations without in-person care and Paraguay reporting more than 500 specialized pediatric teleconsultations by April 2026 that avoided more than 66,000 kilometers of travel. The Middle East and Africa remain earlier in adoption, but public system digitalization in GCC markets is steadily widening the use of virtual pediatric triage and follow-up.

Competitive Landscape

The pediatric telehealth market has a dual competitive structure with specialized pediatric platforms on one side and large general telehealth platforms on the other. The pediatric telehealth market remains fragmented at the specialist level, where behavioral health providers, school-based platforms, and condition-focused players target narrow service lines. Teladoc Health and Amwell use broad employer and health-plan relationships to package pediatric care into larger virtual offerings. In July 2024, Teladoc Health added Brightline's pediatric mental health services to its virtual front door, which widened its age coverage from infancy through adolescence. This move shows how scale players are using partnerships instead of building every pediatric capability from scratch.

Specialist platforms are also widening scope as the pediatric telehealth market moves toward more complete care models. Hazel Health and Little Otter merged in October 2025 to combine school-centered and home-centered pediatric care and target 20 million children and families in the United States. Northwell Health and Brightline formed a strategic alliance in September 2025 to expand referrals across New York through in-person and virtual channels. These moves suggest that continuity across school, home, and specialty referral settings is becoming a stronger differentiator than single-service depth alone.

Technology and compliance are becoming the main filters for competitive advantage in the pediatric telehealth market. TytoCare integrated its Home Smart Clinic with Teladoc Health in November 2025, giving clinicians remote exam capability across lung, ear, throat, and skin assessments. The amended COPPA Rule and HIPAA guidance on parental access to minor records are raising operating standards for every platform that handles child data. White space remains most visible in pediatric dental telehealth, interpreter-enabled virtual exams, and several Latin American and Southeast Asian markets where demand is strong but investment is still thin.

Pediatric Telehealth Industry Leaders

CarePredict

Siemens Healthineers

Oracle Health

Medtronic

Teladoc Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: TytoCare integrated its FDA-cleared Home Smart Clinic with Teladoc Health's 24/7 Care and Primary360 programs. The rollout to select customers was planned for 2026, enabling Teladoc clinicians to conduct clinical-grade physical exams including lung, ear, throat, and skin assessments remotely.

- October 2025: TytoCare unveiled the Smart Clinic Companion, an AI-powered remote exam platform powered by a multi-modal health dataset of over 7 million exams. Beta rollout began in Q4 2025 with commercial availability in February 2026, targeting the primary care capacity crisis.

- October 2025: Hazel Health and Little Otter formally merged to create a combined pediatric care entity targeting 20 million children and families across the US. The combination integrates Hazel's school-based platform with Little Otter's home-based psychiatry, ADHD, and autism programs.

- September 2025: Northwell Health and Brightline announced a strategic alliance to expand pediatric and adolescent mental health services across New York, providing streamlined referrals from Northwell's network to Brightline's licensed clinicians via both in-person clinics in Brooklyn and Lake Success and virtual care.

Global Pediatric Telehealth Market Report Scope

The pediatric telehealth market refers to the industry segment providing remote healthcare services, digital platforms, and medical consultations for children and adolescents. It bridges geographical gaps, allowing pediatricians and specialists to virtually diagnose, treat, and monitor young patients without requiring in-person hospital visits.

The Pediatric Telehealth Market Report is structured to provide a comprehensive view of industry dynamics across multiple segments. By product type, the market is divided into hardware, software, and services. In terms of delivery mode, solutions are offered as on-premises, web-based, and cloud-based platforms. The disease area coverage includes psychiatry, dermatology, neurology, radiology, dental, and other pediatric specialties. The end-user base encompasses providers, payers, and patients and families. Geographically, the market spans North America, Europe, Asia-Pacific, Middle East and Africa, and South America. Market forecasts are presented in terms of value (USD), offering insights into growth opportunities and investment potential across all these segments.

| Hardware | Monitors |

| Medical Peripheral Devices | |

| Software | Standalone Software |

| Integrated Software | |

| Services | Real-Time Interactions |

| Remote Patient Monitoring | |

| Store-and-Forward | |

| Other Services |

| On-Premises |

| Web-Based |

| Cloud-Based |

| Psychiatry |

| Dermatology |

| Neurological Medicine |

| Radiology |

| Dental |

| Other Pediatric Indications |

| Providers |

| Payers |

| Patients and Families |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Hardware | Monitors |

| Medical Peripheral Devices | ||

| Software | Standalone Software | |

| Integrated Software | ||

| Services | Real-Time Interactions | |

| Remote Patient Monitoring | ||

| Store-and-Forward | ||

| Other Services | ||

| By Delivery Mode | On-Premises | |

| Web-Based | ||

| Cloud-Based | ||

| By Disease Area | Psychiatry | |

| Dermatology | ||

| Neurological Medicine | ||

| Radiology | ||

| Dental | ||

| Other Pediatric Indications | ||

| By End User | Providers | |

| Payers | ||

| Patients and Families | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected value of pediatric telehealth by 2031?

The pediatric telehealth market is forecast to reach USD 16.51 billion by 2031 from USD 7.06 billion in 2026, growing at an 18.51% CAGR.

Why is behavioral health leading virtual pediatric care adoption?

Psychiatry held 57.27% share in 2025, supported by rising mental health need, school-based care expansion, and stronger Medicaid reimbursement pathways.

Which product category is growing fastest in virtual pediatric care?

Software is the fastest-growing product type, with a projected 19.68% CAGR through 2031, as providers look for integrated workflows and remote monitoring support.

Why are payers becoming more active buyers of pediatric telehealth solutions?

Payers are the fastest-growing end-user group at 20.85% CAGR because they are using virtual care to improve access and reduce higher-cost downstream utilization.

Which region is expanding fastest for pediatric telehealth services?

Asia Pacific is projected to grow the fastest at 21.82% CAGR through 2031, supported by specialist shortages, digital health investment, and stronger caregiver connectivity.

Page last updated on: