Teledentistry Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

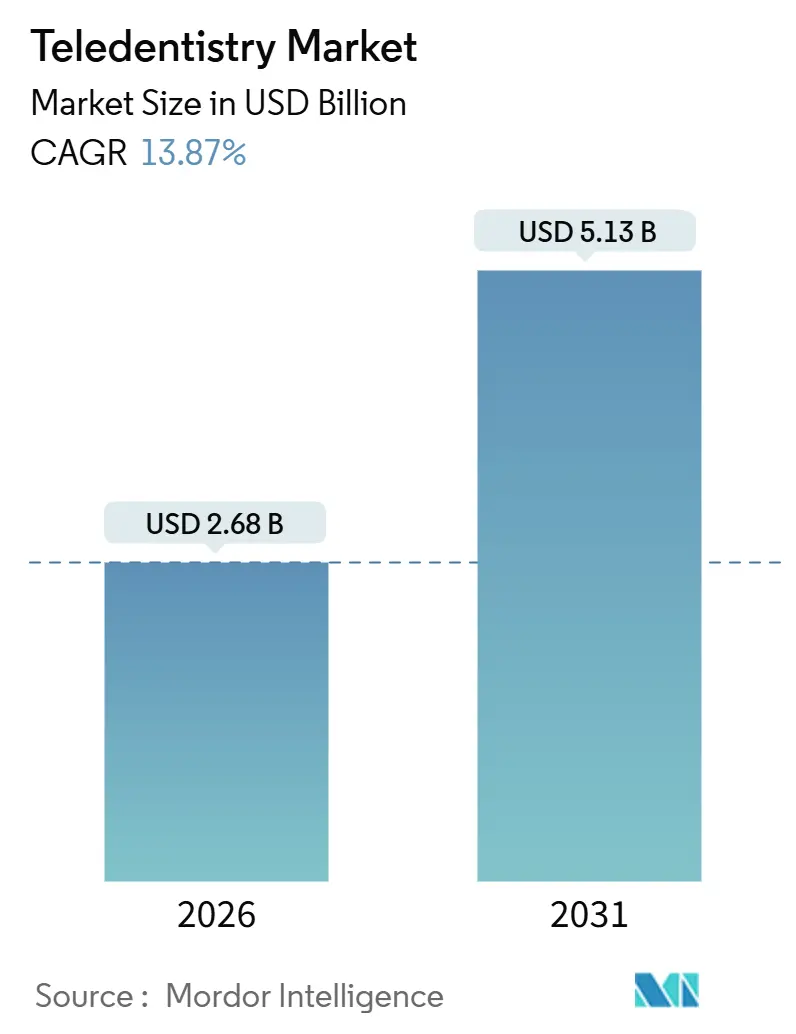

| Market Size (2026) | USD 2.68 Billion |

| Market Size (2031) | USD 5.13 Billion |

| Growth Rate (2026 - 2031) | 13.87% CAGR |

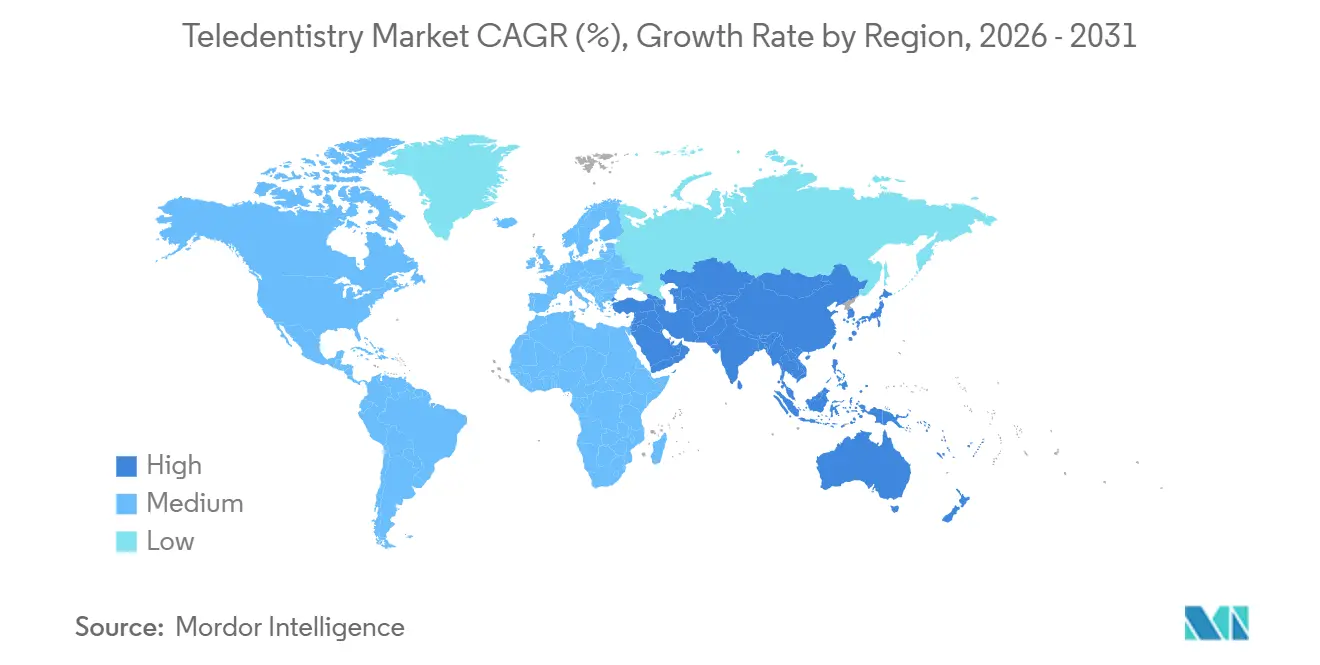

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

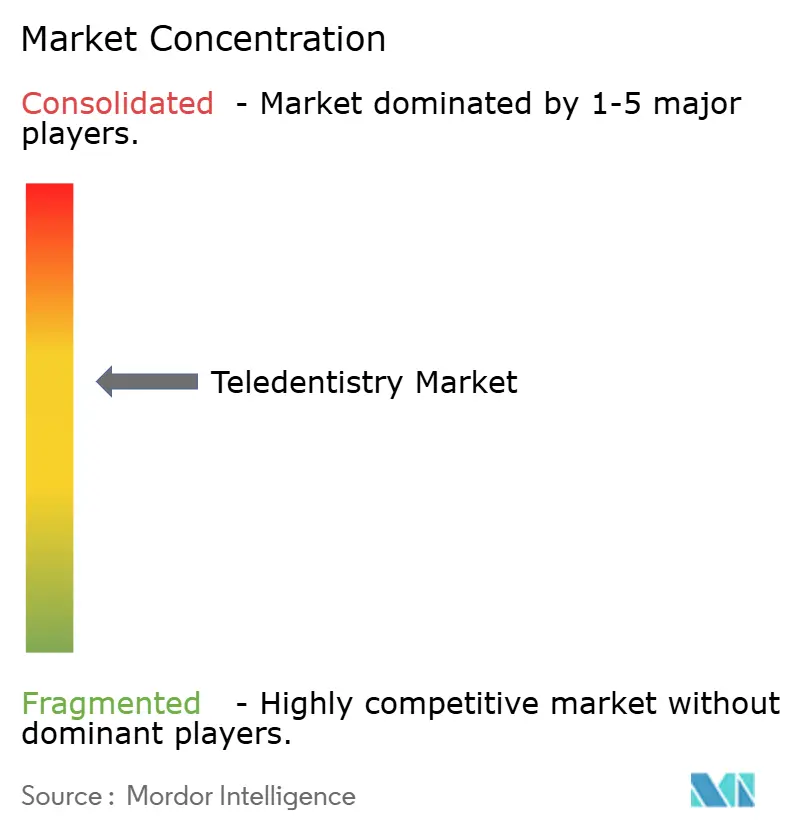

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Teledentistry Market Analysis by Mordor Intelligence

The Teledentistry Market size is estimated at USD 2.68 billion in 2026, and is expected to reach USD 5.13 billion by 2031, at a CAGR of 13.87% during the forecast period (2026-2031).

Remote oral care platforms gained momentum when pandemic-era waivers removed geographic limits on virtual visits, and many of those gains have persisted even as temporary flexibilities have sunset. Rising smartphone penetration, validated AI imaging tools, and government funding for rural connectivity continue to draw patients online. Yet, reimbursement uncertainty after January 2026 and state-by-state licensure rules temper near-term growth. Leading vendors increasingly bundle intraoral cameras, cloud analytics, and payer connectivity to reduce practice overhead. At the same time, direct-to-consumer orthodontic brands refine hybrid models that insert an in-office diagnostic checkpoint to secure regulatory approval. Scale benefits now accrue to platforms that span hardware, software, and insurer relationships, positioning them to capture a disproportionate slice of the expanding teledentistry market.

Key Report Takeaways

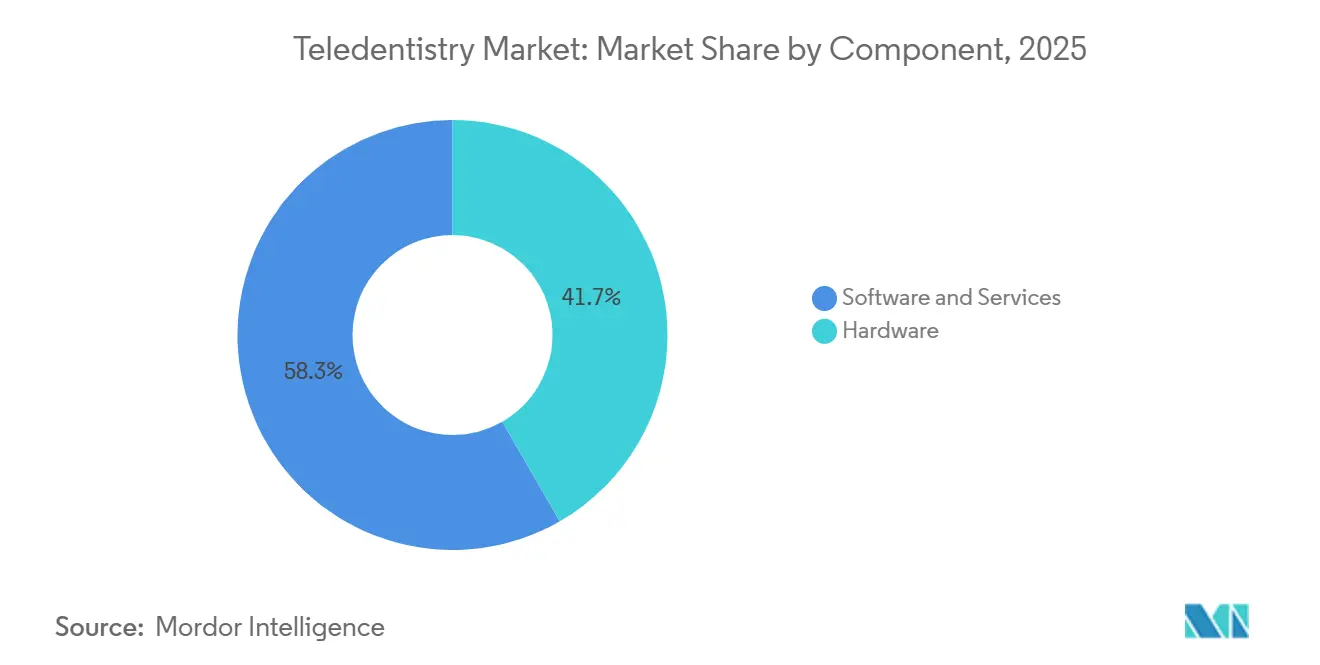

- By component, software & services led with 58.31% of 2025 revenue, whereas hardware is projected to expand at a 13.88% CAGR through 2031.

- By delivery mode, cloud-based platforms accounted for 60.73% of 2025 revenue, while Web/On-premise deployments are forecast to rise at a 14.79% CAGR to 2031.

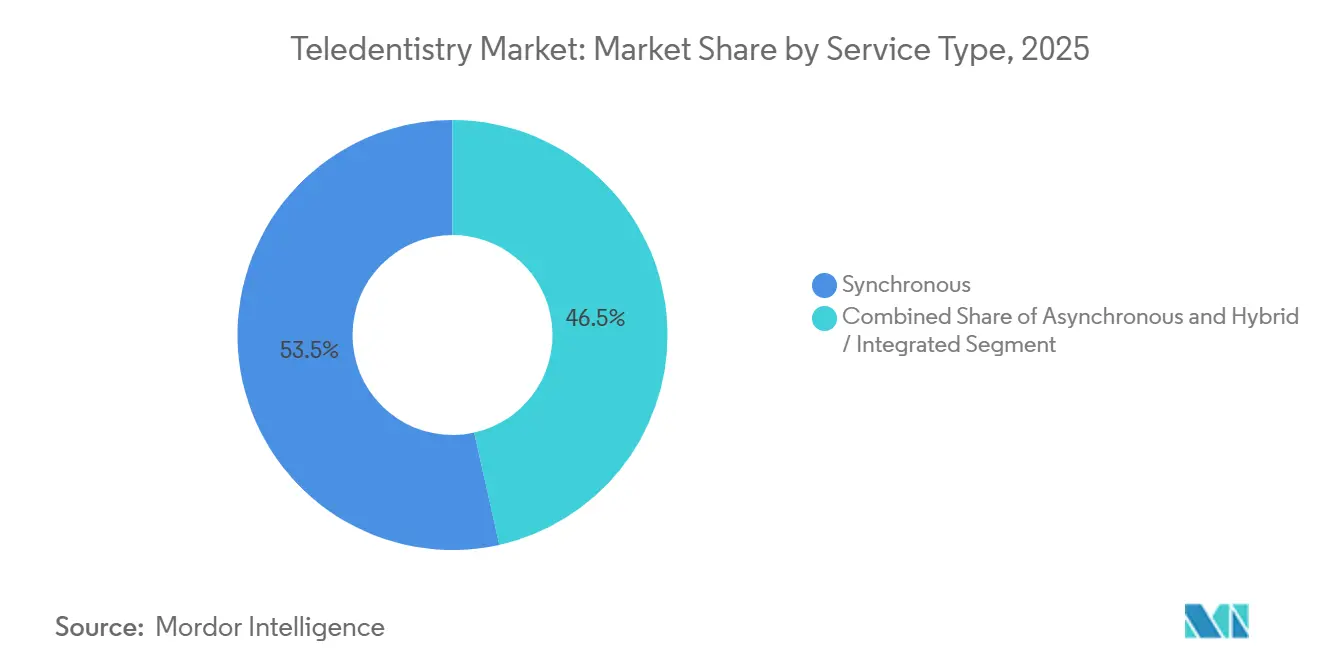

- By service type, synchronous consultations held 53.48% of 2025 revenue, yet asynchronous imaging is expected to post a 16.13% CAGR through 2031.

- By application, tele-consultation generated 43.26% of 2025 revenue; remote patient monitoring is poised for a 17.51% CAGR, the fastest across use cases.

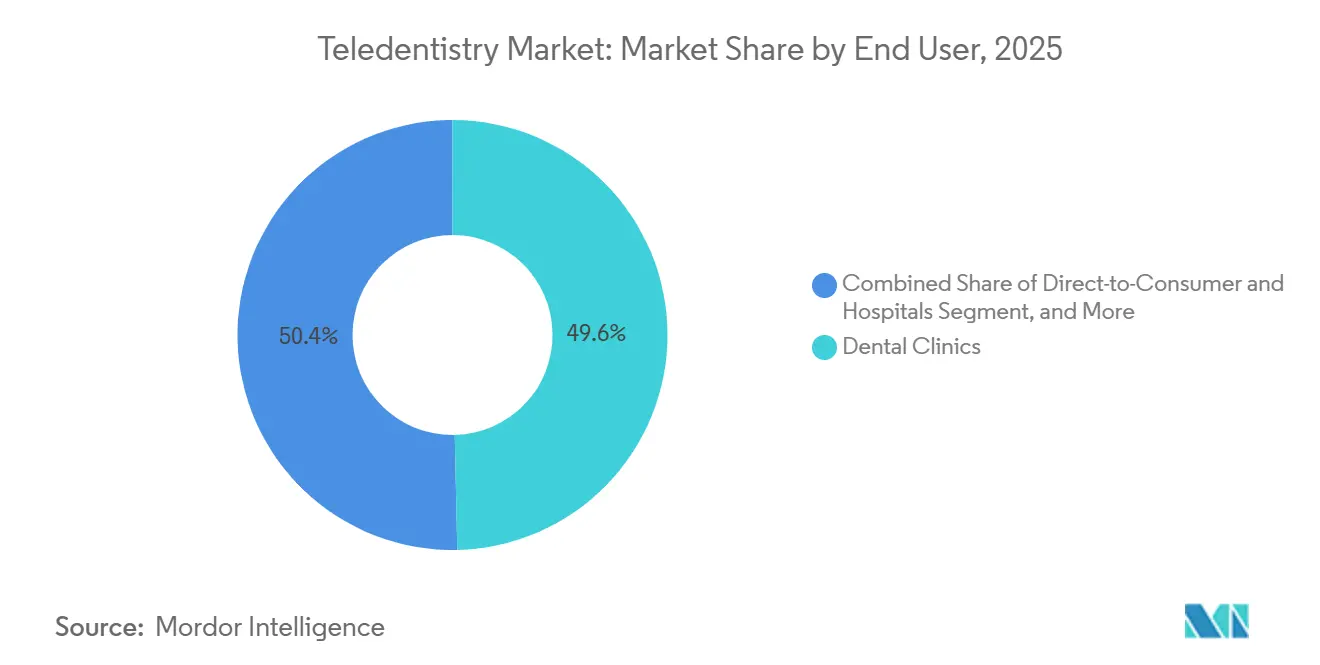

- By end user, dental clinics captured 49.64% of 2025 revenue, but direct-to-consumer platforms are positioned to advance at a 20.05% CAGR through 2031.

- By geography, North America commanded 44.53% of 2025 revenue, while Asia Pacific is projected to grow at a 15.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Teledentistry Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Oral Diseases & Aging Population | +2.8% | Global, strong in Asia Pacific & Sub-Saharan Africa | Long term (≥ 4 years) |

| Smartphone & Internet Penetration Enabling Remote Care | +3.2% | Asia Pacific core, spill-over to Middle East & Africa | Medium term (2-4 years) |

| COVID-19-Driven Telehealth Reimbursement Expansion | +1.9% | North America & Europe | Short term (≤ 2 years) |

| AI-Enabled Diagnostics & Imaging Boost Clinical Accuracy | +2.6% | North America, Europe, Urban Asia Pacific | Medium term (2-4 years) |

| IoT-Linked Consumer Dental Devices Create New Data Streams | +1.7% | North America & Western Europe | Long term (≥ 4 years) |

| Government Rural-Health Funding Targeting Oral Care Gaps | +1.5% | United States, India, Brazil | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Oral Diseases & Aging Population

Global untreated oral-disease prevalence affects 3.5 billion people and creates latent demand for continuous monitoring solutions that avoid unnecessary chair time.[1]World Health Organization, “Oral Health,” WHO.int Edentulism rates exceed 25% among adults 65+ in many low-income economies, and remote fit assessments for dentures now represent a cost-effective alternative to routine clinic visits. Chronic conditions such as diabetes heighten periodontal risk, prompting integrated medical-dental telehealth pathways that reward outcome-based care. U.S. data show that 46% of adults exhibit signs of gum disease, yet only 64% saw a dentist in 2024, underscoring an access gap that the teledentistry market can help narrow.[2]Centers for Disease Control and Prevention, “Adult Oral Health,” CDC.gov

Smartphone & Internet Penetration Enabling Remote Care

China’s 97% smartphone penetration and India’s 54% adoption enable asynchronous imaging to flourish in regions with dentist density below 1 per 10,000. National Digital Health missions mandate interoperable records that mobile apps can retrieve, lowering entry barriers for small practices. Rural broadband rollouts in Brazil and Indonesia have reduced latency to under 100 ms in most underserved districts, a technical threshold for smooth real-time consultations. Remaining challenges include data-plan costs, since intraoral images consume up to 10 MB per upload, straining low-income budgets.

COVID-19-Driven Telehealth Reimbursement Expansion

Emergency waivers allowed cross-state billing parity in the United States until January 31, 2026; their expiry forces providers to revisit their revenue mix. Medicaid parity laws remain in 38 states but now carry heavier prior-authorization requirements, raising administrative burden. European payers diverge sharply: France mandates full parity for follow-up visits, whereas Germany reimburses remote care at 80% of in-office rates, illustrating how policy flux shapes the trajectory of the teledentistry market.

AI-Enabled Diagnostics & Imaging Boost Clinical Accuracy

Deep-learning tools reading bitewing images have reached 92% sensitivity and 95% specificity, matching dentist performance and shortening diagnosis cycles. Align’s iTero Element 5D Plus visualizes tooth-movement scenarios in minutes, cutting revision rates by 18% at multi-site orthodontic chains. Dental Monitoring algorithms flag bracket debonding days earlier than legacy checkups, translating into fewer emergency appointments and steadier aligner compliance. Twelve FDA clearances since 2024 cement a regulatory pathway that most new software entrants now pursue.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory & Licensure Variability Across Regions | −1.8% | United States, European Union | Medium term (2-4 years) |

| Reimbursement Uncertainty for Virtual Dental Services | −2.1% | Most acute in U.S. commercial markets | Short term (≤ 2 years) |

| Limited Diagnostic Scope/Liability for Complex Cases | −1.3% | Global, higher in litigious markets | Long term (≥ 4 years) |

| Digital-Literacy & Image-Quality Barriers for Elders | −0.9% | North America, Europe, East Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory & Licensure Variability Across Regions

Fifty U.S. jurisdictions enforce separate dental-practice acts, forcing platforms to finance duplicate licenses that can exceed USD 5,000 per state each year. The Interstate Medical Licensure Compact streamlines physician credentialing but excludes dentists, amplifying compliance overhead. In Europe, GDPR data-localization clauses require in-country servers or explicit consent for cross-border transfers, inflating infrastructure costs for pan-regional vendors.

Reimbursement Uncertainty for Virtual Dental Services

Commercial insurers in the United States pay 15–30% below chairside rates for virtual exams and often deny asynchronous claims outright. Medicare’s reinstated originating-site rule from January 2026 limits coverage to rural beneficiaries, despite urban seniors making up four-fifths of enrollees. Current Procedural Terminology codes lack granularity for AI-assisted diagnostics, leading to underpayment disputes and slower adoption.[3]Centers for Medicare & Medicaid Services, “Calendar Year 2024 Medicare Physician Fee Schedule Final Rule,” CMS.gov

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Integration Accelerates

The teledentistry market size for hardware is projected to expand at a 13.88% CAGR as subscription plans make AI-equipped intraoral cameras accessible to single-chair clinics. Software & Services still accounted for 58.31% of 2025 revenue and maintained anchor sticky monthly billing, but proprietary file formats hinder seamless interoperability among vendors. Real-time caries-detection sensors integrated into scanners such as iTero Element 5D Plus reduce diagnostic lag by 2 days and enhance cement vendor loyalty through cloud storage contracts.

Recurring software subscriptions, often priced at USD 300 per provider per month, deliver 65–70% gross margins, dwarfing the 35–40% margins typical of one-time camera sales. Vendors that unify imaging, billing, and patient messaging on a single interface are capturing dislodged spend from piecemeal practice-management tools. Although DICOM underpins medical imaging, it lacks dental extensions for 3D surface scans, delaying truly open ecosystems.

By Delivery Mode: On-Premise Gains Traction

Cloud services captured 60.73% of 2025 teledentistry market share, favored by solo practitioners for low startup costs, yet large dental service organizations pivot toward hybrid or on-premise deployments to satisfy strict data-sovereignty statutes in Germany and specific U.S. hospital networks. National regulators codified rules requiring that protected health information remain on domestic soil, leading vendors to split identifiers locally while processing anonymized analytics in public clouds.

HIPAA compliance audits now cost cloud vendors about USD 120,000 annually, pushing them to raise subscription fees and eroding some price advantage. Browser-based platforms render most 2D radiographs seamlessly, but 3D CBCT studies still stutter on legacy hardware lacking WebGL acceleration, reinforcing the digital divide between urban and rural clinics.

By Service Type: Asynchronous Models Surge

Asynchronous imaging solutions are set to grow 16.13% annually, using AI triage to funnel only 18% of cases to real-time consults and freeing dentists to review files during downtime. Payers reimburse these store-and-forward encounters at USD 25–40, roughly half the synchronous rate, yet lower overhead preserves margins. Emergency-department dental visits fell 28% in a multi-state pilot that rerouted nociceptive pain cases to virtual triage within one hour.

Hybrid workflows emerge as a middle ground: patients send photos, receive AI-generated assessments, and schedule synchronous video follow-ups only if severe pathology appears. Orthodontic aligner programs already rely on weekly asynchronous uploads, cutting in-office checkups from 12 to four per course, a cost benefit now marketed aggressively to time-pressed adults.

By Application: Remote Monitoring Expands

Remote patient monitoring codes adopted in 2024 reimburse USD 50–65 per enrollee per month for 20 minutes of clinician review, fueling a 17.51% CAGR for the sub-segment. Bluetooth periodontal probes upload pocket-depth data, prompting intervention before irreversible bone loss. Tele-consultation still accounts for 43.26% of 2025 revenue; however, value creation is shifting toward continuous datasets rather than episodic advice.

Education & Training applications use haptic simulation to prepare dental students and require no PPE consumables, saving universities high costs. Triage & Emergency Care, especially in rural counties, lowered unnecessary ER trips by 35% after virtual first-contact programs were implemented. Clear-aligner monitoring accounts for the largest share of “Other Applications,” demonstrating consumers’ appetite for tech-enabled orthodontics.

By End User: Direct-to-Consumer Disruption

Dental Clinics remain the volume anchor at 49.64% of 2025 revenue, but direct-to-consumer channels are on track for a 20.05% CAGR as hybrid protocols gain regulator acceptance. Byte and Candid Co. now require an initial dentist scan, blunting liability and aligning with FDA guidance. Hospitals integrate kiosks into emergency departments to cut wait times, while insurers leverage teleconsult data to refine risk models and pre-empt costly restorative procedures.

Geography Analysis

North America generated 44.53% of 2025 turnover but faces reimbursement headwinds after Medicare reinstated rural-only telehealth coverage, which excludes 80% of urban seniors. Medicaid parity laws in 38 states offset some impact, yet add paperwork through stricter prior authorizations. Canada’s provincial patchwork slows platform scalability, and Mexico’s public-sector pilot demonstrates robust access gains but limited private-payer interest.

Germany reimburses at 80% of in-office rates but demands video documentation, while the United Kingdom’s triage helpline rerouted 1.2 million calls in 2025, freeing restorative slots. GDPR-driven localization adds EUR 80,000–150,000 in annual server costs per multi-state vendor, fostering consolidation among well-capitalized incumbents.

Asia Pacific will be the primary growth engine, expanding 15.91% annually through 2031. China’s 8,000 rural telehealth stations and India’s interoperable health-record push drive volume, while Japan’s aging population fuels demand for denture monitoring. Australia’s Royal Flying Doctor Service logged 14,000 remote consults in 2025, cutting emergency extractions by 31%. South Korea committed KRW 45 billion (USD 34 million) to rural teledentistry infrastructure, aiming to deliver half a million consultations annually by 2027.

Competitive Landscape

Global vendor concentration is modest: the five most prominent players collectively control about significant revenue, giving the teledentistry market a mid-level level of consolidation. Align Technology anchors its ecosystem with scanners that lock orthodontists into recurring cloud fees, securing predictable cash flows. Dental Monitoring built a 14-patent moat around AI tracking, while direct-to-consumer brands pivot to hybrid models under tighter FDA surveillance.

Regional startups differentiate through payer integration; platforms that bundle claims submission, prior authorizations, and outcomes dashboards shorten reimbursement cycles by 30–45%. Larger dental service organizations negotiate volume pricing for on-premises deployments, whereas solo practices gravitate toward cloud subscriptions at around USD 200 per month. Scale players able to align hardware, software, and payer contracts stand to seize an outsized stake of future teledentistry market growth.

Teledentistry Industry Leaders

Planmeca Oy

Dentsply Sirona

Carestream Dental LLC

Koninklijke Philips N.V.

Smile Virtual LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: OrisDX partnered with Teledentistry.com to embed molecular salivary-rinse cancer tests in virtual visits, widening early-detection access.

- April 2025: DentalMonitoring and Ormco unveiled an AI-enabled remote-monitoring alliance at the American Association of Orthodontists conference to streamline treatment oversight.

- October 2024: CareQuest Innovation Partners invested in Grin, expanding digital oral-care convenience through capital from Triventures and SpringRock Ventures.

- September 2024: Unilever Indonesia integrated AI Denta Scan into its “Tanya Dokter Gigi” service during National Oral Health Month, underscoring AI’s role in mass-market oral-care engagement.

Global Teledentistry Market Report Scope

The Teledentistry Market Report is Segmented by Component (Software & Services, Hardware), Delivery Mode (Cloud-based Platforms, Web/On-premise Platforms), Service Type (Synchronous, Asynchronous, Hybrid/Integrated), Application (Tele-consultation, Remote Patient Monitoring, Education & Training, Triage & Emergency Care, Other Applications), End User (Hospitals, Dental Clinics, Direct-to-Consumer, Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Software & Services |

| Hardware |

| Cloud-based Platforms |

| Web / On-premise Platforms |

| Synchronous |

| Asynchronous |

| Hybrid / Integrated |

| Tele-consultation |

| Remote Patient Monitoring |

| Education & Training |

| Triage & Emergency Care |

| Other Applications (Orthodontic Monitoring, Periodontic Care, among others) |

| Hospitals |

| Dental Clinics |

| Direct-to-Consumer |

| Other End Users (Payers & Insurers, Academic Research Institutes, among others) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software & Services | |

| Hardware | ||

| By Delivery Mode | Cloud-based Platforms | |

| Web / On-premise Platforms | ||

| By Service Type | Synchronous | |

| Asynchronous | ||

| Hybrid / Integrated | ||

| By Application | Tele-consultation | |

| Remote Patient Monitoring | ||

| Education & Training | ||

| Triage & Emergency Care | ||

| Other Applications (Orthodontic Monitoring, Periodontic Care, among others) | ||

| By End User | Hospitals | |

| Dental Clinics | ||

| Direct-to-Consumer | ||

| Other End Users (Payers & Insurers, Academic Research Institutes, among others) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the teledentistry market in 2031?

The teledentistry market size is forecast to reach USD 5.13 billion by 2031.

Which segment is expected to grow the fastest through 2031?

Remote Patient Monitoring is projected to register the highest CAGR at 17.51%.

Why are asynchronous consultations gaining traction?

They cut clinician scheduling conflicts and reduce payer costs, while AI triage routes only complex cases to live video visits.

How will regulatory changes in the United States influence adoption?

The reinstated originating-site rule limits Medicare reimbursement to rural patients, creating revenue pressure for urban-focused platforms.

Which region offers the strongest growth outlook?

Asia Pacific, propelled by high smartphone penetration and government digital-health mandates, is expected to expand at a 15.91% CAGR through 2031.

What technology trend underpins future hardware demand?

AI-integrated intraoral cameras that deliver real-time caries detection are driving a shift toward subscription-based equipment leasing.

Page last updated on: