Mobile Cardiac Telemetry Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.07 Billion |

| Market Size (2031) | USD 3.84 Billion |

| Growth Rate (2026 - 2031) | 13.17% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mobile Cardiac Telemetry Systems Market Analysis by Mordor Intelligence

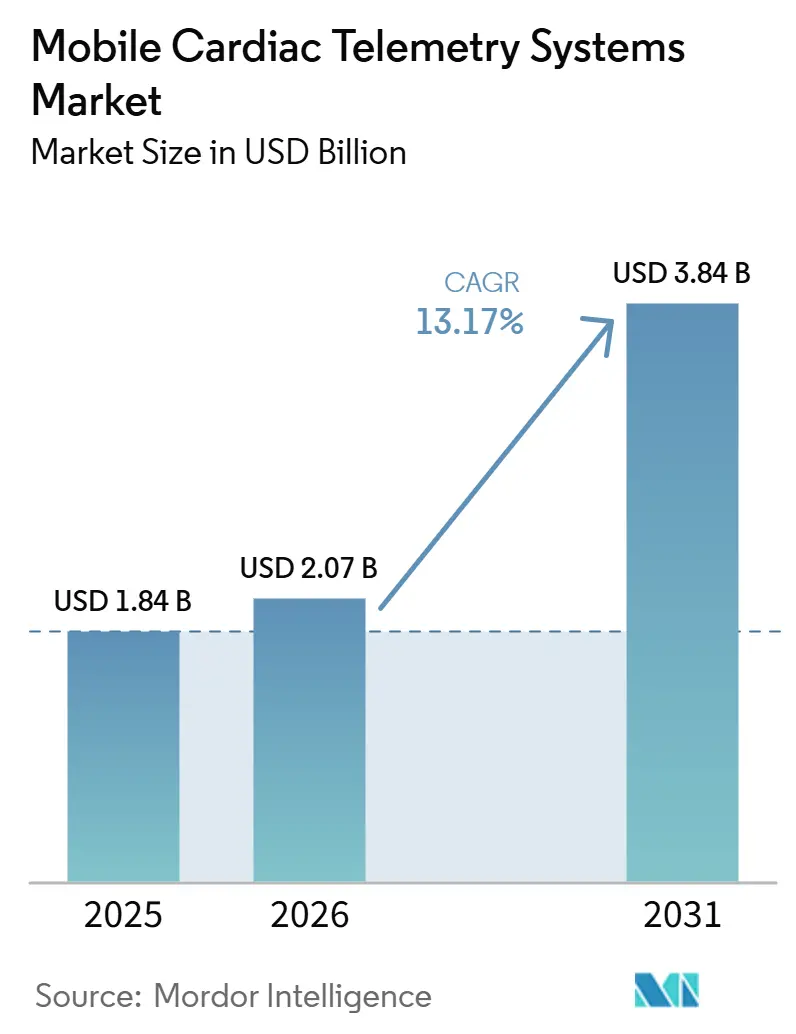

The mobile cardiac telemetry systems market is projected to expand from USD 1.84 billion in 2025 and USD 2.07 billion in 2026 to USD 3.84 billion by 2031, registering a CAGR of 13.17% between 2026 to 2031. The mobile cardiac telemetry systems market is being supported by the continued burden of cardiovascular disease and by care delivery models that are moving monitoring beyond hospital settings into ambulatory and home environments. The mobile cardiac telemetry systems market also reflects a clear shift in value creation, with software, monitoring workflows, and EHR-connected service layers carrying more strategic weight than hardware alone. The mobile cardiac telemetry systems market remains strongest in North America because reimbursement and monitoring center infrastructure are already established, while Asia-Pacific is advancing faster as health systems invest in digital and home-based cardiac care models. The mobile cardiac telemetry systems market is also becoming more selective, as vendors that reduce review burden, support interoperability, and meet regulatory standards are gaining a stronger commercial position than under-resourced entrants. The mobile cardiac telemetry systems market is therefore moving toward a more platform-led structure, where scale in clinical operations, software performance, and compliance can shape consolidation through the forecast period.

Key Report Takeaways

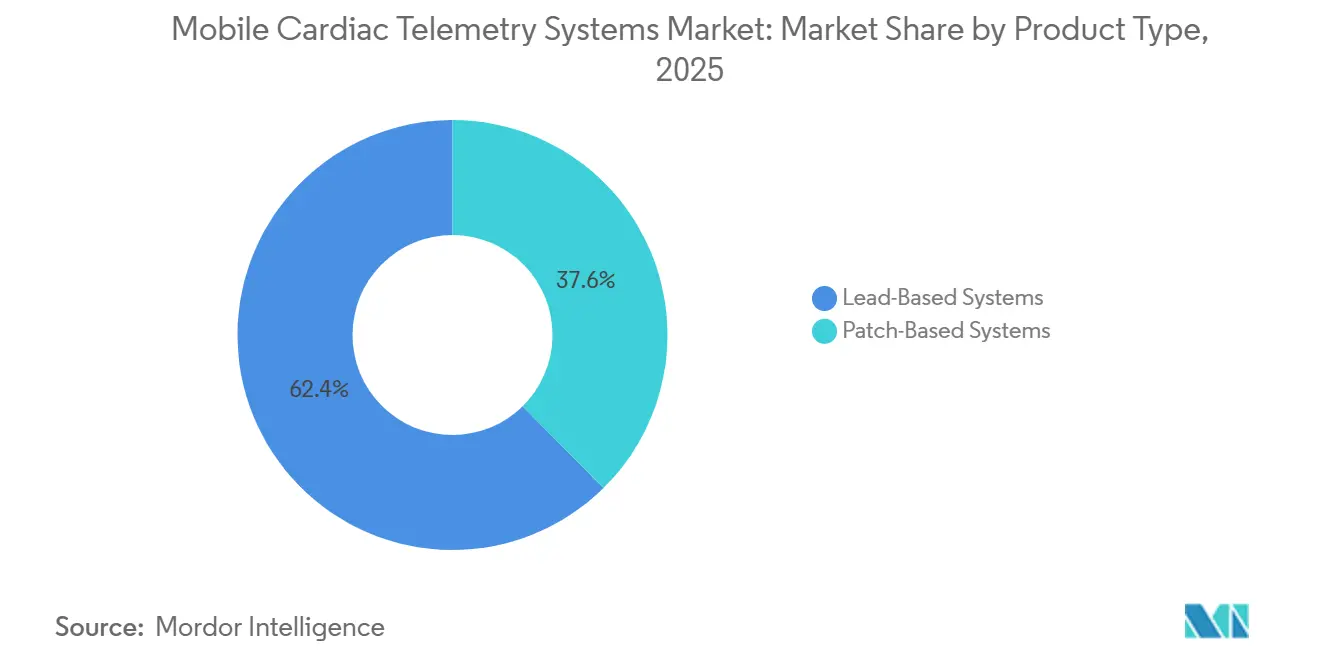

- By product type, lead-based systems held 62.22% of the mobile cardiac telemetry systems market size in 2025, while patch-based systems are forecasted to expand at a 13.45% CAGR through 2031.

- By component, software accounted for 53.33% share in 2025, while services recorded the highest projected CAGR at 13.74% through 2031.

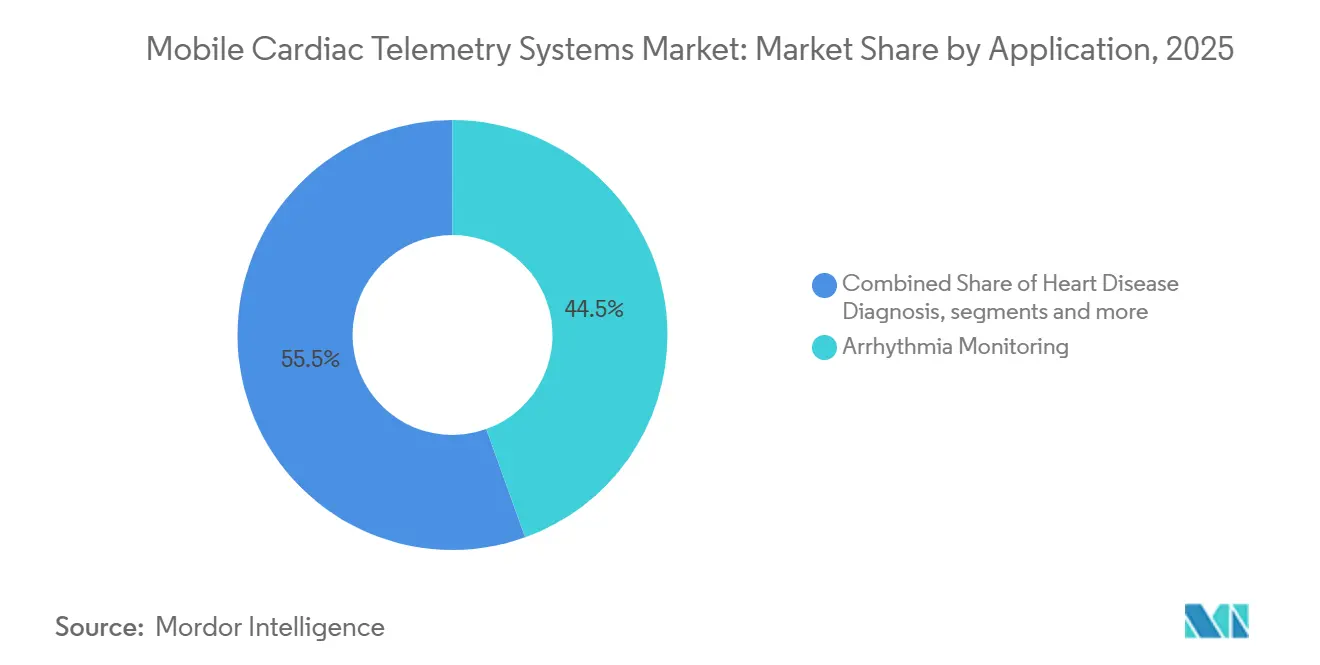

- By application, arrhythmia monitoring represented 44.52% of the mobile cardiac telemetry systems market size in 2025, while heart disease diagnosis is expected to advance at a 14.35% CAGR through 2031.

- By end user, hospitals and clinics captured 51.41% of the mobile cardiac telemetry systems market share in 2025, while home healthcare is projected to grow at a 14.17% CAGR through 2031.

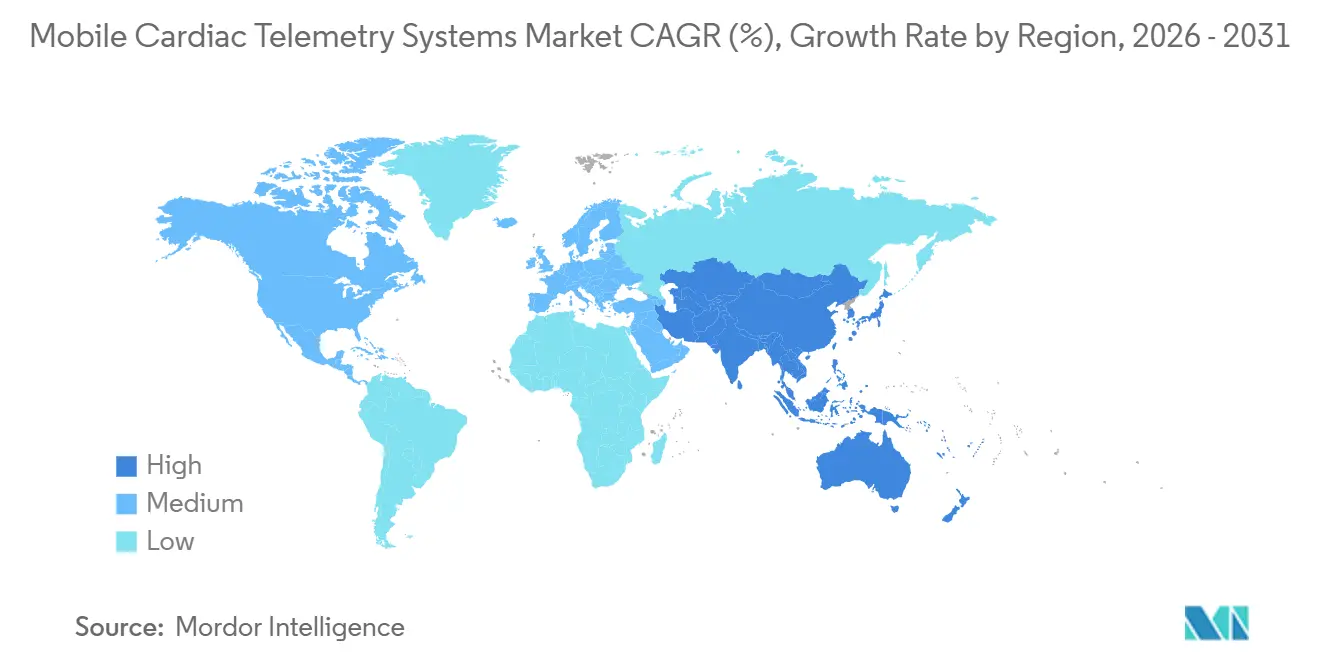

- By geography, North America held 50.27% of the mobile cardiac telemetry systems market share in 2025, while Asia-Pacific is forecasted to expand at a 15.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mobile Cardiac Telemetry Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Burden of Cardiac Disease and Arrhythmia Detection Needs | +2.8% | Global | Long term (≥ 4 years) |

| Shift to Continuous, Real-Time Remote Patient Monitoring | +2.5% | Global, with concentration in North America and Western Europe | Short term (≤ 2 years) |

| AI-Assisted Signal Review and Workflow Automation | +2.0% | North America and Europe, with early gains in Japan and Australia | Medium term (2-4 years) |

| Reimbursement Expansion for Ambulatory and Home-Based Cardiac Monitoring | +1.8% | North America, with spillover to Western Europe and Australia | Short term (≤ 2 years) |

| Integration With EHR, RPM, and Cloud Care Platforms | +1.5% | North America and Europe | Medium term (2-4 years) |

| Underused Primary Care and Post-Discharge Screening Pathways | +1.2% | North America and core APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Burden of Cardiac Disease and Arrhythmia Detection Needs

The mobile cardiac telemetry systems market continues to benefit from the fact that cardiovascular disease remains the leading cause of death worldwide. The mobile cardiac telemetry systems market is also supported by the uneven distribution of disease burden, because low- and middle-income countries account for more than three-quarters of cardiovascular deaths and often have limited specialist capacity. That imbalance makes continuous remote monitoring more useful as an efficiency tool, especially where specialist staffing is limited and hospital capacity is constrained. The mobile cardiac telemetry systems market is therefore not only expanding in already developed settings, but is also becoming relevant in healthcare systems that need scalable cardiac surveillance models. This broad disease backdrop keeps demand tied to long-cycle clinical need rather than to short-term device replacement patterns. It also strengthens the case for continuous monitoring in chronic disease management, secondary prevention, and post-discharge care across the mobile cardiac telemetry systems market.

Shift to Continuous, Real-Time Remote Patient Monitoring

The mobile cardiac telemetry systems market is being lifted by a steady move away from episodic Holter testing toward longer and continuous rhythm surveillance. CMS coverage rules support up to 30 days of continuous monitoring, which improves the ability to detect intermittent conditions that are often missed during short monitoring windows.[1]Centers for Medicare & Medicaid Services, “Billing and Coding: Temporary Nontherapeutic Ambulatory Cardiac Monitoring Devices – Article A60279,” CMS, cms.gov A 2025 multicenter stroke substudy showed that wearable ECG monitoring identified atrial fibrillation in patients with no prior AF history, which expands the clinical role of remote cardiac monitoring beyond routine cardiology use.[2]Frontiers in Neurology, “An Efficient Approach for Detecting Atrial Fibrillation in Ischemic Stroke Patients Using a Wearable Device: A Prospective Multicenter Substudy of the STABLED Trial,” Frontiers in Neurology, frontiersin.orgThe mobile cardiac telemetry systems market is therefore seeing its prescriber base widen into neurology and internal medicine, where follow-up rhythm surveillance is gaining clinical importance. This is helping the mobile cardiac telemetry systems market shift from a specialized diagnostic tool toward a more predictable service line linked to ongoing surveillance and prevention.

AI-Assisted Signal Review and Workflow Automation

The mobile cardiac telemetry systems market is increasingly influenced by AI tools that reduce the workload on technicians and interpreting clinicians. Peer-reviewed research in 2025 showed that modern deep learning models are improving arrhythmia detection accuracy and enabling real-time predictive analytics in telemetry settings.[3]Heart Failure Society of America, “New Scientific Statement Guides Clinicians on How to Integrate Digital Health Tools Into Heart Failure Care,” HFSA, hfsa.org In parallel, the FDA cleared Abbott’s Merlin.net MN7000 v2.0 with integrated neural network models for AF and pause detection, which shows that AI is now embedded inside regulated remote care platforms rather than added only as a separate software layer. The mobile cardiac telemetry systems market is responding to this shift because clinical review capacity has become a larger bottleneck than raw data capture. Vendors that can maintain diagnostic quality while cutting unnecessary review steps are in a stronger position to scale monitoring-as-a-service contracts in the mobile cardiac telemetry systems market.

Reimbursement Expansion for Ambulatory and Home-Based Cardiac Monitoring

The mobile cardiac telemetry systems market has a durable demand base in the United States because reimbursement for extended ambulatory monitoring is already established under existing CPT codes. The January 2025 CMS billing update clarified documentation requirements for independent diagnostic testing facilities, which supports operational consistency and billing confidence. The mobile cardiac telemetry systems market is likely to benefit most in systems where reimbursement, workflow, and remote interpretation capacity already work together. Europe shows the opposite pattern in many places, because academic research found that reimbursement for ambulatory cardiac monitoring still varies widely across national markets. That gap helps explain why the mobile cardiac telemetry systems market still scales faster where payment policy is clearer and monitoring pathways are easier to standardize.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Device and Monitoring Service Costs | -1.8% | Global, pronounced in Asia, Latin America, and Africa | Long term (≥ 4 years) |

| Clinical Training Gaps for Interpretation and Device Workflow | -1.5% | Core APAC, MEA, and South America | Short term (≤ 2 years) |

| Patient Adherence Issues in Wearable Monitoring | -1.0% | Global | Long term (≥ 4 years) |

| Integration Friction with Legacy Hospital IT and Data Governance Requirements | -1.2% | Global, pronounced in fragmented health systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Device and Monitoring Service Costs

The mobile cardiac telemetry systems market still faces a cost barrier in healthcare systems that do not support subscription, bundled, or well-defined reimbursement models. Continuous monitoring requires devices, connectivity, physician interpretation, and round-the-clock staffing, which pushes the total service cost well above the level that many uninsured or cost-sensitive patients can absorb. The mobile cardiac telemetry systems market also carries a structural cost floor because attended surveillance requirements make labor and monitoring center overhead difficult to remove. This favors larger operators with scale, while smaller testing facilities face weaker economics and less room to price competitively. In practical terms, the mobile cardiac telemetry systems market remains easier to penetrate in insured settings than in public systems with tight procurement budgets. Even where clinical demand is clear, cost can delay adoption in primary care and community settings that are less familiar with billing and service workflows.

Clinical Training Gaps for Interpretation and Device Workflow

The mobile cardiac telemetry systems market is also limited by the availability of trained monitoring technicians and interpreting clinicians outside major cardiology centers. Continuous attended monitoring needs a different operating model than standard Holter testing, and many community hospitals cannot sustain that model without outside service partners. The mobile cardiac telemetry systems market is feeling this gap most strongly in regions where specialist density has not kept pace with disease burden and digital tool availability. That creates a two-speed adoption pattern, with faster rollout in markets that already have centralized monitoring infrastructure and slower deployment elsewhere. Certification pathways help, but the mobile cardiac telemetry systems market is still likely to see workforce limitations hold back broader community-level adoption through much of the forecast period.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Lead-Based Dominance Persists as Patch Platforms Scale Commercially

Lead-based systems held 62.22% share in 2025, which kept them at the center of the mobile cardiac telemetry systems market because multi-lead configurations still offer stronger diagnostic resolution for arrhythmia classification. Their installed base also remains important, since lead-based systems fit more easily into existing interpretation workflows and hospital telemetry practices. In the mobile cardiac telemetry systems market, that combination of clinical familiarity and workflow compatibility continues to support demand from electrophysiologists and hospital-based cardiac teams. This means the mobile cardiac telemetry systems market still relies on lead-based devices for much of its current revenue base.

Patch-based systems, however, are projected to grow at a 13.45% CAGR through 2031, which makes them the faster-moving product line in the mobile cardiac telemetry systems market. Their appeal comes from simpler wearability, lower visibility on the body, and extended-use convenience, all of which can support adherence outside clinical settings. Over time, the mobile cardiac telemetry systems market is likely to move toward a mixed product structure, with patch formats taking more outpatient volume while lead-based systems remain important in complex and higher-acuity use cases.

By Component: Software Monetization Anchors Margins as Services Revenue Compounds

Software accounted for 53.33% of the mobile cardiac telemetry systems market size in 2025, which shows how much value has shifted from hardware into analytics, workflow orchestration, and decision support. This part of the mobile cardiac telemetry systems industry carries strong strategic weight because data review, triage, and reporting now shape clinical efficiency as much as sensors do. As a result, software remains the clearest anchor for margin and differentiation in the mobile cardiac telemetry systems market.

Services are forecasted to grow at a 13.74% CAGR through 2031, which reflects rising demand for managed monitoring, reading-center support, and integration work around remote care pathways. The Heart Failure Society of America also emphasized that better outcomes depend on seamless data flow among devices, EHRs, and care teams, which supports the role of service and integration layers in the mobile cardiac telemetry systems market. In this setting, the mobile cardiac telemetry systems industry is moving toward business models where recurring platform services matter more than one-time device sales.

By Application: Arrhythmia Monitoring Anchors Demand While Heart Disease Diagnosis Expands Use Cases

Arrhythmia monitoring represented 44.52% of the mobile cardiac telemetry systems market size in 2025, which kept it as the core application in current clinical practice. Atrial fibrillation remains the central use case because intermittent rhythm abnormalities are difficult to capture without longer monitoring windows. The mobile cardiac telemetry systems market still depends on this application for its most established referral pathways, reimbursement logic, and interpretation workflows.

Heart disease diagnosis is projected to grow at 14.35% CAGR through 2031, which makes it the fastest-growing application in the mobile cardiac telemetry systems market. This shift reflects broader use in post-MI follow-up, rehabilitation pathways, pre-procedure evaluation, and ongoing cardiac risk stratification. The mobile cardiac telemetry systems market is therefore widening from reactive diagnosis toward continuous risk management, and that change should expand use beyond traditional arrhythmia referrals. It also means the mobile cardiac telemetry systems market can capture more value from longitudinal care pathways rather than from one-time diagnostic episodes alone.

By End-User: Hospital Share Remains High While Home Healthcare Expands Access

Hospitals and clinics captured 51.41% of the mobile cardiac telemetry systems market share in 2025, which confirms that institutional settings still lead current utilization. They retain this position because they already have electrophysiology programs, specialist interpretation capacity, and established monitoring relationships. The mobile cardiac telemetry systems market remains closely tied to these settings because they are best positioned to integrate monitoring into broader cardiac workflows. This keeps hospitals and clinics as the main present-day base of the mobile cardiac telemetry systems market.

Home healthcare is forecasted to grow at 14.17% CAGR through 2031, which points to the clearest expansion path across the mobile cardiac telemetry systems market. A Mayo Clinic implementation study published in 2025 showed that wireless telemetry can complement hardwired hospital systems without losing alert reliability, which supports hybrid models that extend beyond inpatient settings. The mobile cardiac telemetry systems market is therefore shifting from a specialty service delivered mainly inside hospitals toward a broader care infrastructure that follows patients across discharge and recovery. That shift is changing device design priorities, service workflows, and access economics across the mobile cardiac telemetry systems market.

Geography Analysis

North America accounted for 50.27% of the mobile cardiac telemetry systems market share in 2025, which kept it as the largest regional contributor. The United States supports this lead through established CPT billing pathways and a dense independent diagnostic testing facility structure that is already familiar with extended ambulatory monitoring. The 2026 CMS local coverage determination provides clearer coverage rules for temporary nontherapeutic ambulatory cardiac monitoring devices, which can reduce administrative friction and support broader prescribing patterns. That gives the mobile cardiac telemetry systems market a strong operating base in North America, where reimbursement, interpretation capacity, and workflow standardization are more mature than in most other regions. Canada and Mexico contribute less, but the regional structure still favors companies that can work at scale across reimbursement, monitoring operations, and provider integration.

Europe remained the second-largest geography in the mobile cardiac telemetry systems market, supported by established healthcare systems and ongoing demand for ambulatory cardiac surveillance. Germany, the United Kingdom, France, Italy, and Spain continue to shape regional volume, while tariff variation still limits consistency in adoption across countries. Biotronik’s 2025 research partnership with Charité and the German Heart Center Foundation also points to Europe’s importance as an innovation base for AI-supported digital cardiology.

Asia-Pacific is projected to be the fastest-growing region in the mobile cardiac telemetry systems market at a 15.36% CAGR through 2031. Growth is being supported by aging populations in Japan and South Korea, expanding cardiovascular disease burden in India and China, and continued health system interest in digital and home-based monitoring pathways. The mobile cardiac telemetry systems market in this region is still less mature than in North America, but the growth pace reflects a wider opening for remote care and ambulatory diagnostics. Entry conditions remain selective because approval standards and local operating requirements differ across major markets, which means companies need both regulatory readiness and service adaptability to scale effectively.

Competitive Landscape

The mobile cardiac telemetry systems market remains moderately consolidated at the top, led by Philips, iRhythm Technologies, Medtronic, and Boston Scientific through broad monitoring coverage and established provider relationships. The mobile cardiac telemetry systems market now rewards platforms that combine device performance with software depth, reimbursement familiarity, and dependable clinical operations. That direction matters because review efficiency, alert quality, and workflow integration have become more important in the mobile cardiac telemetry systems market than hardware differentiation alone. Companies with strong regulatory depth and surveillance infrastructure still hold an advantage, since compliance standards create meaningful barriers for smaller entrants.

The mobile cardiac telemetry systems market is also seeing pressure from specialist firms that are trying to compete above the device layer. iRhythm’s cleared design modifications for the Zio Monitor strengthen its patch-based position, which keeps pressure on lead-based incumbents in ambulatory monitoring FDA. These moves show that the mobile cardiac telemetry systems market still offers room for focused competition where wearability, workflow speed, and service economics are improving.

Another important theme in the mobile cardiac telemetry systems market is the push toward interoperable care pathways and research-backed digital cardiology ecosystems. The Heart Failure Society of America stated in 2025 that device, EHR, and care-team integration is a foundational requirement for effective digital cardiac care, which supports platforms built around seamless data flow rather than isolated devices. The mobile cardiac telemetry systems market is therefore likely to remain competitive, but the advantage is increasingly shifting toward companies that can link devices, analytics, and clinical workflows into a single reliable operating model.

Mobile Cardiac Telemetry Systems Industry Leaders

Medtronic plc

Koninklijke Philips N.V.

iRhythm Technologies, Inc.

Boston Scientific Corporation

ZOLL Medical Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Implicity presented HRS 2026 data in Chicago, demonstrating its cloud-based AI algorithm reduced false ILR alerts by 61.6% on top of manufacturer-embedded AI, while maintaining 98.3% diagnostic sensitivity, results that extend earlier EHRA findings to next-generation AI-enabled implantable loop recorders.

- March 2026: Medtronic received FDA approval for its OmniaSecure defibrillation lead for left bundle branch placement, enabling conduction system pacing, following the lead's January 2026 US commercial launch for traditional right-ventricle placement, expanding indications for leadless cardiac device management and remote monitoring.

- February 2026: ZOLL Medical received EU MDR 2017/745 regulatory approval for its Zenix monitor/defibrillator, described as the company's most clinically advanced monitor, enabling broad European market commercialization across its cardiac patient management portfolio.

Global Mobile Cardiac Telemetry Systems Market Report Scope

According to the report’s scope, the mobile cardiac telemetry systems market refers to the segment of cardiac monitoring where wearable telemetry devices continuously record and transmit patient heart rhythms in real time to remote monitoring centers. These systems enable early detection of arrhythmias, support continuous patient monitoring outside hospital settings, and reduce reliance on traditional Holter or event monitors.

The mobile cardiac telemetry systems market is segmented into product type, component, application, end-user, and geography. By product type, the market is segmented into lead-based systems and patch-based systems. By component, the market is segmented into hardware, software, and services. By application, the market is segmented into arrhythmia monitoring, heart disease diagnosis, post-surgical monitoring, remote patient monitoring, and preventive healthcare. By end-user, the market is segmented into hospitals and clinics, home healthcare, ambulatory surgical centers, and diagnostic laboratories. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Lead-Based Systems |

| Patch-Based Systems |

| Hardware |

| Software |

| Services |

| Arrhythmia Monitoring |

| Heart Disease Diagnosis |

| Post-Surgical Monitoring |

| Remote Patient Monitoring |

| Preventive Healthcare |

| Hospitals and Clinics |

| Home Healthcare |

| Ambulatory Surgical Centers |

| Diagnostic Laboratories |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Lead-Based Systems | |

| Patch-Based Systems | ||

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Application | Arrhythmia Monitoring | |

| Heart Disease Diagnosis | ||

| Post-Surgical Monitoring | ||

| Remote Patient Monitoring | ||

| Preventive Healthcare | ||

| By End-User | Hospitals and Clinics | |

| Home Healthcare | ||

| Ambulatory Surgical Centers | ||

| Diagnostic Laboratories | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will mobile cardiac telemetry systems become by 2031?

The mobile cardiac telemetry systems market is projected to reach USD 3.84 billion by 2031 from USD 1.84 billion in 2025 to USD 2.07 billion in 2026, growing at a 13.17% CAGR over 2026 to 2031.

Which product format leads today, and which one is growing faster?

Lead-based systems led with 62.22% share in 2025, while patch-based systems are forecasted to grow faster at a 13.45% CAGR through 2031.

Which application creates the strongest current demand?

Arrhythmia monitoring remains the largest application with 44.52% share in 2025, while heart disease diagnosis is expected to be the fastest-growing use case at a 14.35% CAGR.

Why does North America lead this space?

North America held 50.27% share in 2025 because reimbursement pathways, IDTF infrastructure, and clinical workflows for extended ambulatory monitoring are already well established.

Page last updated on: