Pediatric Home Healthcare Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

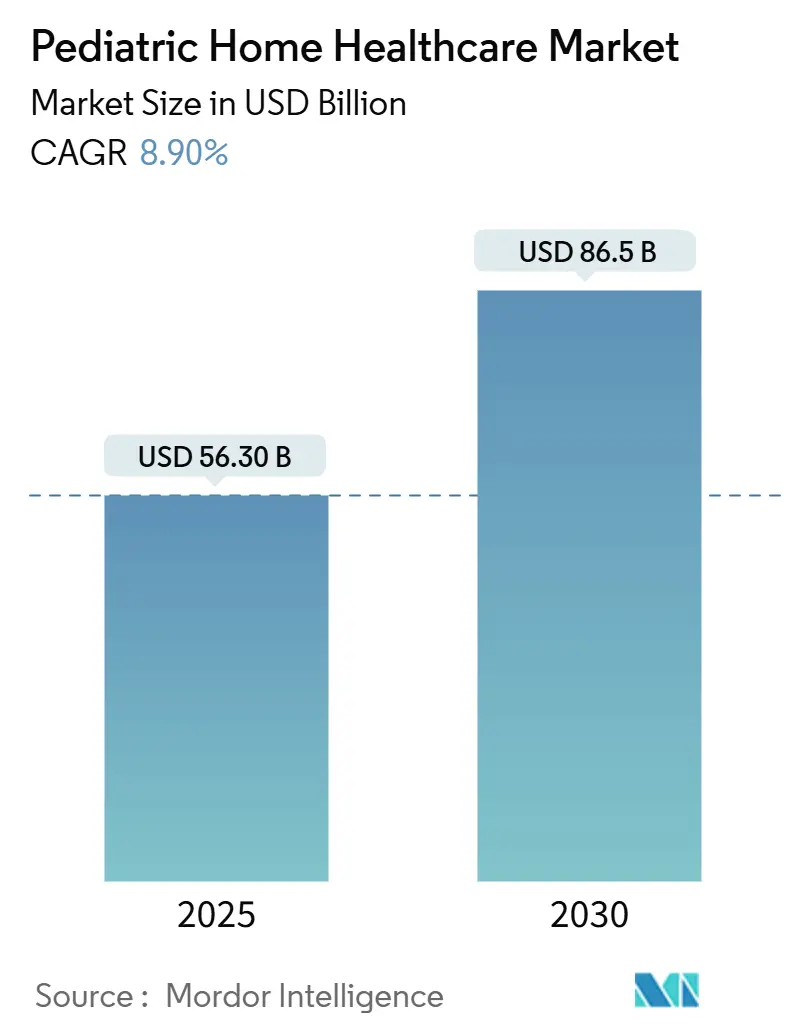

| Market Size (2025) | USD 56.30 Billion |

| Market Size (2030) | USD 86.5 Billion |

| Growth Rate (2025 - 2030) | 8.90% CAGR |

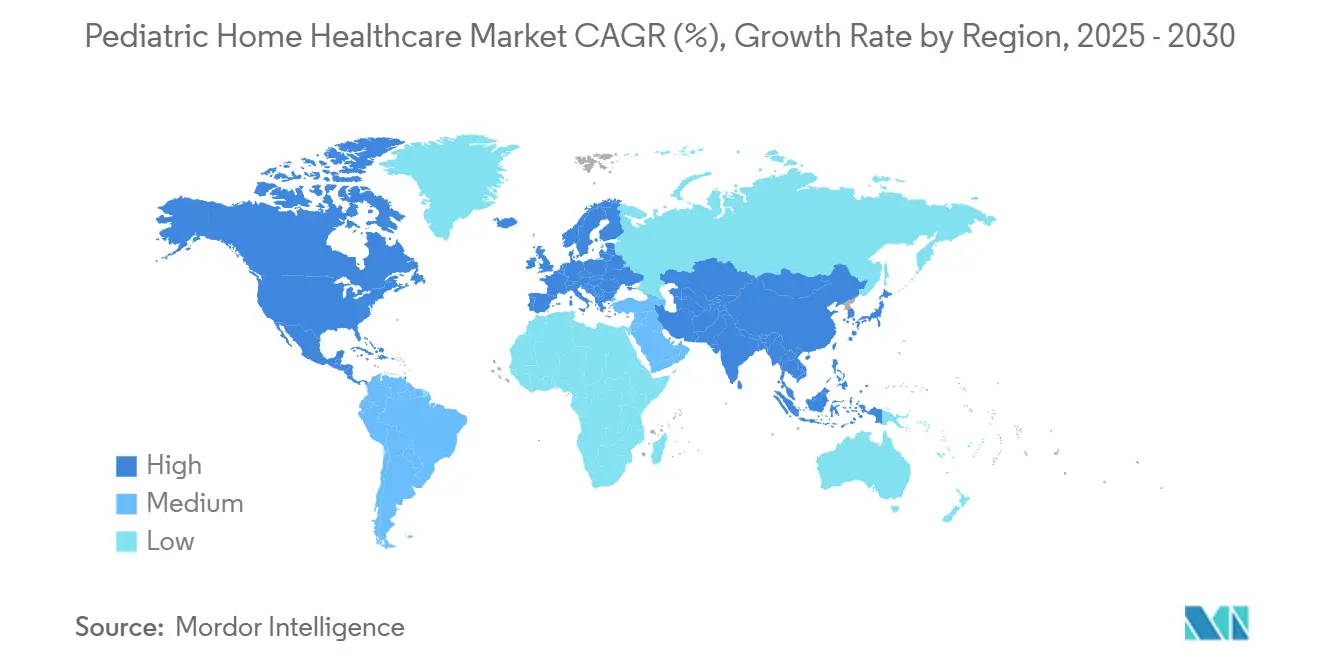

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pediatric Home Healthcare Market Analysis by Mordor Intelligence

The pediatric home healthcare market size reached USD 56.3 billion in 2025 and is on track to post an 8.90% CAGR, lifting value to USD 86.5 billion by 2030. Rising prevalence of medically complex children, widening policy support, and rapid device innovation are expanding the pediatric home healthcare market across advanced and emerging economies. Persistent hospital bed shortages and the proven cost-efficiency of community-based models are reinforcing demand, while AI-enabled monitoring systems and portable life-support equipment are broadening service breadth. North America remains the commercial anchor owing to Medicaid waiver expansion, although Asia Pacific is building momentum as infrastructure investments multiply. Competitive dynamics are shifting as providers pursue scale, diversify clinical portfolios, and embed technology that improves outcomes and productivity.

Key Report Takeaways

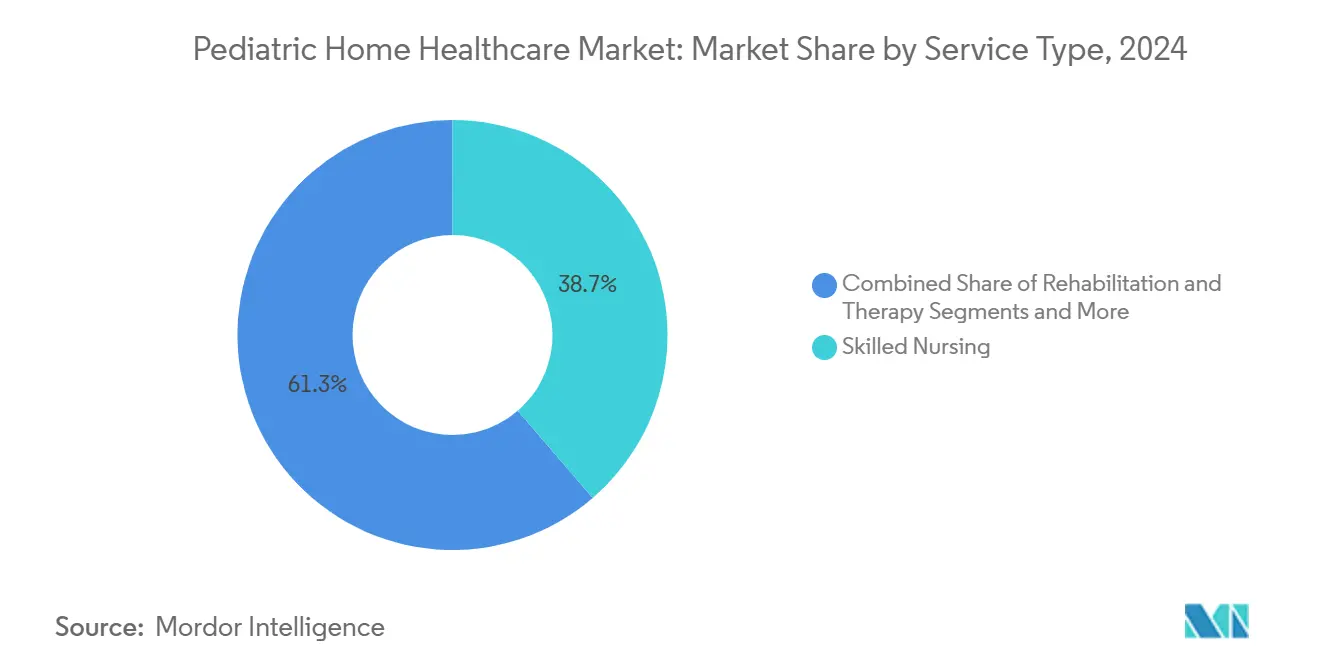

- By service type, skilled nursing held 38.7% of the pediatric home healthcare market share in 2024, while AI-enabled remote monitoring is advancing at a 12.6% CAGR through 2030.

- By age group, the 5-12 year cohort commanded 31.4% of the pediatric home healthcare market size in 2024, whereas neonatal services are projected to expand at a 10.5% CAGR to 2030.

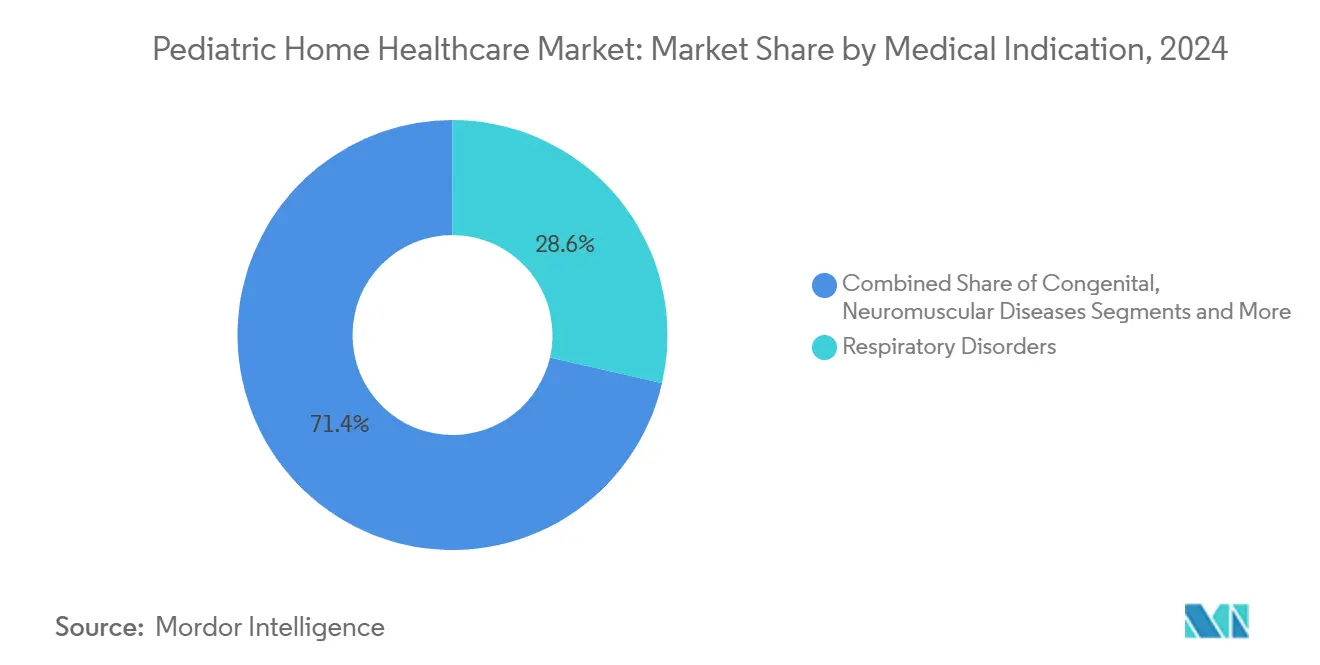

- By medical indication, respiratory disorders accounted for 28.6% of the pediatric home healthcare market size in 2024 and neuromuscular diseases are growing at an 11.8% CAGR over the same horizon.

- By payer, Medicaid and CHIP funded 46.2% of total spending in 2024, compared with private insurance which is rising at a 9.3% CAGR through 2030.

- By geography, North America led with 45.1% revenue share in 2024, yet Asia Pacific is forecast to register a 10.2% CAGR during 2025-2030.

Market Trends and Insights

Drivers Impact Analysis of Pediatric Home Healthcare Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Prevalence Of Chronic Pediatric Conditions | +2.10% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Expansion Of Medicaid Waivers & Insurance Coverage | +1.80% | North America, with spillover to developed markets | Medium term (2-4 years) |

| Shortage Of Pediatric Hospital Beds Drives Home-Based Alternatives | +1.50% | Global, particularly acute in North America & APAC | Short term (≤ 2 years) |

| Advances In Portable Ventilators & Infusion Pumps | +1.30% | Global, led by North America & Europe | Medium term (2-4 years) |

| AI-Enabled Remote Patient Monitoring For Children | +1.20% | North America & Europe, expanding to APAC | Long term (≥ 4 years) |

| Retail-Pharmacy Entry Into Pediatric Home Services | +0.90% | North America, with early expansion to Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Chronic Pediatric Conditions

Complex disorders such as spinal muscular atrophy and congenital anomalies are becoming more common, creating sustained demand for high-acuity home services. Japan alone supports approximately 60,000 medically complex children requiring continuous care, and similar patterns are unfolding across Europe and North America.[1]株式会社 Make Care, “『訪問看護ステーションくるみ』重症心身障害児及び医療的ケア児の訪問看護開始,” PR TIMES, prtimes.jp Gene therapies extend survival yet increase long-term monitoring needs, prompting health systems to codify home-based clinical pathways. The United Kingdom’s respiratory guidelines for Duchenne muscular dystrophy emphasize multidisciplinary teams that visit homes early in disease progression, reflecting how protocols are adapting. Reimbursement rates have trended upward to mirror the skill intensity involved, anchoring revenue predictability for providers. Equipment suppliers are responding with pediatric-specific ventilators and suction devices that can be managed by families after short training sessions. The trend is therefore converting clinical complexity into a commercial opportunity for the pediatric home healthcare market.

Expansion of Medicaid Waivers & Insurance Coverage

Mandatory 12-month continuous eligibility for children in Medicaid and CHIP programs took effect in January 2024, closing historical coverage gaps that disrupted care continuity. Five states now guarantee coverage until age 6, and New York’s waiver alone safeguards access for 66,177 children each year at a cost of USD 60 million.[2]New York State Department of Health, “Final Amendment Request,” health.ny.gov Home and Community-Based Services additions under CHIP, effective January 2025, further widen benefit scope. These reforms standardize revenue streams and lower administrative friction, positioning the pediatric home healthcare market for durable growth. Private insurers are mirroring public policy by adding in-home alternatives to benefit schedules, a shift that is raising commercial payer penetration.

Shortage of Pediatric Hospital Beds Drives Home-Based Alternatives

Residency vacancies that left 30% of U.S. pediatric positions unfilled in 2024 underscore a systemic capacity crunch. Subspecialty vacancies exceed 40%, delaying discharges by an average of 15 days for patients awaiting home nursing coverage. Health systems are reacting by scaling hospital-at-home programs; Advocate Health’s Levine Children’s Hospital at Home delivers IV medications, breathing therapies, and post-operative monitoring within family residences. Cost savings, bed turnover benefits, and higher family satisfaction are motivating further rollouts. Technology platforms that transmit vital signs to command centers strengthen clinical oversight, allowing earlier transition from acute wards. Collectively, these factors escalate uptake of home-based models within the pediatric home healthcare market.

Advances in Portable Ventilators & Infusion Pumps

The Newport HT70 Plus ventilator operates for up to 10 hours on internal power and needs no external gas, matching the practical constraints of family homes. Neurally adjusted ventilatory assist has cut re-intubation rates for neonates to 14% in Australian trials, supporting safer early discharge. Supply chain disruptions, like Cardinal Health’s discontinuation of key feeding pumps, are opening the door for alternate device suppliers and rental models. As hardware becomes lighter and smarter, children across acuity levels can remain at home, enlarging the pediatric home healthcare market size tied to respiratory and nutritional support services.

Restraints Impact Analysis of Pediatric Home Healthcare Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Reimbursement Rules Across States | -1.40% | North America, with variations across state jurisdictions | Medium term (2-4 years) |

| Limited Pediatric-Trained Home-Care Workforce | -1.10% | Global, particularly acute in rural and underserved areas | Long term (≥ 4 years) |

| Cyber-Security Risks In Connected Pediatric Devices | -0.80% | Global, with heightened concerns in North America & Europe | Short term (≤ 2 years) |

| Heightened Parental Liability Concerns | -0.60% | North America & Europe, emerging in APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Reimbursement Rules Across States

While UnitedHealthcare dropped prior-authorization for home health in April 2025, providers still navigate a patchwork of Medicaid rules that diverge on visit limits, reimbursement ceilings, and documentation. CMS updated the Home Health Prospective Payment System for 2025, adding acceptance-to-service checks that raise administrative overhead.[3]Centers for Medicare & Medicaid Services, “Medicare Program; Calendar Year (CY) 2025 Home Health Prospective Payment System (HH PPS) Rate Update,” Federal Register, federalregister.govSmall operators face compliance costs that erode margins, slowing geographic expansion. Multi-state providers struggle to standardize care pathways, limiting economies of scale in the pediatric home healthcare industry.

Limited Pediatric-Trained Home-Care Workforce

Families report an average shortfall of 40 nursing hours weekly for children needing complex care, demonstrating acute labor scarcity. The Institute of Pediatric Nursing warns that reduced pediatric clinical placements weaken future supply. Japan logged 886 home-nursing station closures in 2025 due to staffing gaps. Certification differences across jurisdictions further restrict mobility, amplifying workforce friction. Without decisive investment in training pipelines and retention incentives, capacity constraints could temper the expansion rate of the pediatric home healthcare market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Pediatric Home Healthcare Market Segment Analysis

By Service Type:

Technology Integration Reshapes Traditional CareThe skilled nursing arm of the pediatric home healthcare market size reached USD 21.8 billion in 2024, equal to 38.7% of global revenue, driven by the need for ventilator management, tracheostomy care, and complex medication administration. AI-enabled remote monitoring, projected to post a 12.6% CAGR, extends clinician reach and cuts travel overhead, unlocking new margin pools. Rehabilitation therapies remain essential for developmental gains, and respiratory and ventilation services are rising in tandem with neuromuscular disease prevalence.

Personal care assistance is expanding as children with developmental disabilities survive into adulthood, triggering long-duration support needs. Digital auscultation platforms embedded in remote visits improve triage accuracy, shrinking specialist queues. Portable ventilators with integrated cloud dashboards blend into standard nursing protocols, illustrating how traditional and digital models converge. Providers that integrate AI analytics within care plans are achieving earlier intervention metrics and differentiated payer contracts, bolstering their share of the pediatric home healthcare market.

By Age Group:

Neonatal Care Drives InnovationChildren aged 5-12 years generated USD 17.7 billion in 2024, equivalent to 31.4% of the pediatric home healthcare market share. This cohort benefits from structured school programs that coordinate with home care teams, stabilizing visit schedules. Neonatal services, the fastest growing at 10.5% CAGR, capitalize on safer early discharges supported by lightweight ventilators and continuity protocols.

Advances in neonatal transport monitoring allow physicians to visualize vitals in real time during ambulance transfers, making home initiation feasible within days of birth. Infants for up to 12 months represent a parallel growth corridor as portable feeding systems empower parents to manage complex nutrition plans. Adolescents transitioning to adult care prompt tailored support models that bridge pediatric and adult specialties. Age-aligned customization remains vital for providers seeking persistent relevance in the pediatric home healthcare market.

By Medical Indication:

Respiratory Disorders Lead Complex CareRespiratory disorders generated USD 16.1 billion, amounting to 28.6% of the pediatric home healthcare market size in 2024. Portable non-invasive ventilation and airway clearance devices have broadened home eligibility, moving patients out of intensive care earlier. Neuromuscular diseases, projected to expand 11.8% annually, require lifelong respiratory support complemented by gene-therapy monitoring.

Congenital disorders propel steady demand as surgical survival improves, while oncology services blend symptom management with infusion therapies delivered at home. Emerging telemonitoring for congenital heart disease demonstrates how sensor networks can support complex physiology outside hospitals. Providers that assemble indication-specific clinical bundles enhance payer alignment and defend share in the pediatric home healthcare market.

By Payer:

Government Programs Dominate FundingMedicaid and CHIP accounted for USD 26.0 billion in reimbursements during 2024, equal to 46.2% of market revenue, confirming public programs as financial linchpins. Continuous eligibility rules stabilize cash flow and improve care continuity, encouraging provider investment. Private insurance payments, climbing at 9.3% CAGR, reflect broader benefit coverage of in-home alternatives, which insurers view as cost-saving relative to lengthy hospitalizations.

Military and federal schemes supply niche volumes with consistent reimbursement schedules, and charitable funding cushions families facing benefit gaps. Value-based care pilots tie payouts to readmission avoidance and functional gains, rewarding clinically integrated models. Diversified payer mixes shield providers from policy shocks and reinforce the revenue base of the pediatric home healthcare industry.

Geography Analysis

North America Pediatric Home Healthcare Market

North America produced USD 25.4 billion in 2024, accounting for 45.1% of total revenue thanks to established Medicaid waivers, mature device supply chains, and robust telehealth legislation. Extended continuous eligibility in five states ensures uninterrupted coverage, underpinning service stability. Providers continue to invest in AI triage tools that comply with HIPAA statutes, reinforcing regional leadership within the pediatric home healthcare market.

APAC Pediatric Home Healthcare Market

Asia Pacific recorded the fastest expansion, registering a 10.2% CAGR outlook through 2030 as governments steer funds toward home-based solutions aligned with capacity build-out. India’s broader healthcare sector is set to reach USD 612 billion by 2025, building a receptive environment for pediatric services, while Japan’s home nursing network is scaling at 8.8% per year to meet demographic pressure. Regulatory reforms that authorize telemedicine and remote monitoring are accelerating cross-border technology transfers, enlarging the pediatric home healthcare market size in the region.

EMEA and South America Pediatric Home Healthcare Market

Europe maintains steady growth fostered by the European Health Data Space, which harmonizes data standards and eases device certification. Middle East and Africa show emerging promise, highlighted by the UAE’s early vision-screening program and Saudi Arabia’s USD 57.04 billion health budget that earmarks home care pilots. South America trails but can climb as economic recovery funds infrastructure upgrades in Brazil and Argentina. Collectively, geographic diversification is tempering cyclic risk and unlocking white-space potential for the pediatric home healthcare market

Competitive Landscape

Market structure remains moderately fragmented although consolidation is accelerating. Aveanna Healthcare’s USD 75 million acquisition of Thrive Skilled Pediatric Care added 23 sites and deepened specialty expertise, illustrating the race for scale. Private equity continues to target specialty providers; Varsity Healthcare Partners’ sale of Angels of Care Pediatric Home Health to Nautic Partners signals sustained investor confidence.

Technology capabilities are decisive differentiators. DispatchHealth’s merger with Medically Home establishes the largest advanced at-home care platform, embedding hospital-level services and AI monitoring that elevate clinical benchmarks. CMS regulations covering home infusion therapy and quality reporting are raising compliance thresholds, favoring groups with dedicated regulatory teams.

White-space opportunities include underserved rural counties and nascent telemonitoring categories. Retail pharmacies forming joint ventures with children’s hospitals bring distribution muscle and prescription data to the field, intensifying rivalry. Firms that demonstrate superior outcomes, caregiver satisfaction, and payer cost savings are capturing premium contracts, reinforcing competitive moats within the pediatric home healthcare market.

Pediatric Home Healthcare Industry Leaders

BAYADA Home Health Care

Aveanna Healthcare

Maxim Healthcare Services

Pediatric Home Service (PHS)

Angels of Care Pediatric Home Health

- *Disclaimer: Major Players sorted in no particular order

Pediatric Home Healthcare Market Companies Covered in this Report

- BAYADA Home Health Care

- Aveanna Healthcare

- Pediatric Home Service (PHS)

- Maxim Healthcare

- PSA Healthcare

- Lincare Holdings

- Interim HealthCare

- Encompass Health

- BrightStar Care

- Kindred at Home

- Angels of Care Pediatric Home Health

- Team Select Home Care

- Johns Hopkins Pediatric Home Care

- Trinity Health At Home

- Children's Home Healthcare

- Suncoast Pediatric Homecare

- Tender Care Home Health

- Caring Hands Pediatric Homecare

- Adara Home Health

- Thrive Skilled Pediatric Care

Recent Industry Developments in Pediatric Home Healthcare Market

- April 2025: Aveanna Healthcare completed the USD 75 million acquisition of Thrive Skilled Pediatric Care, adding 23 new locations.

- April 2025: Advocate Health launched the Atrium Health Levine Children’s Hospital at Home program in Charlotte, North Carolina.

- March 2025: DispatchHealth and Medically Home merged, creating the largest advanced at-home care provider in the U.S.

Global Pediatric Home Healthcare Market Report Scope

Segmentation Overview

| Skilled Nursing |

| Rehabilitation & Therapy |

| Personal Care Assistance |

| Respiratory & Ventilation Services |

| Other Clinical Services |

| Neonates (0-28 days) |

| Infants (1-12 months) |

| Toddlers (1-4 yrs) |

| Children (5-12 yrs) |

| Adolescents (13-18 yrs) |

| Congenital Disorders |

| Neuromuscular Diseases |

| Respiratory Disorders |

| Oncology |

| Others (Trauma, Post-Surgical, etc.) |

| Medicaid / CHIP |

| Private Insurance |

| Military & Federal Programs |

| Out-of-Pocket |

| Charitable / Non-profit Funding |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Skilled Nursing | |

| Rehabilitation & Therapy | ||

| Personal Care Assistance | ||

| Respiratory & Ventilation Services | ||

| Other Clinical Services | ||

| By Age Group | Neonates (0-28 days) | |

| Infants (1-12 months) | ||

| Toddlers (1-4 yrs) | ||

| Children (5-12 yrs) | ||

| Adolescents (13-18 yrs) | ||

| By Medical Indication | Congenital Disorders | |

| Neuromuscular Diseases | ||

| Respiratory Disorders | ||

| Oncology | ||

| Others (Trauma, Post-Surgical, etc.) | ||

| By Payer | Medicaid / CHIP | |

| Private Insurance | ||

| Military & Federal Programs | ||

| Out-of-Pocket | ||

| Charitable / Non-profit Funding | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current valuation of the pediatric home healthcare market?

The market is valued at USD 56.3 billion in 2025.

How fast is the pediatric home healthcare market expected to grow?

It is projected to register an 8.90% CAGR, reaching USD 86.5 billion by 2030.

Which service category leads spending?

Skilled nursing services command the largest revenue share at 38.7% in 2024.

Which region offers the highest growth potential?

Asia Pacific is forecast to grow at a 10.2% CAGR through 2030.

Who pays for most pediatric home healthcare services?

Medicaid and CHIP fund 46.2% of total spending, making government programs the dominant payer.

What technology trend is reshaping care delivery?

AI-enabled remote monitoring is advancing at a 12.6% CAGR, expanding virtual oversight capabilities.

Page last updated on: