Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

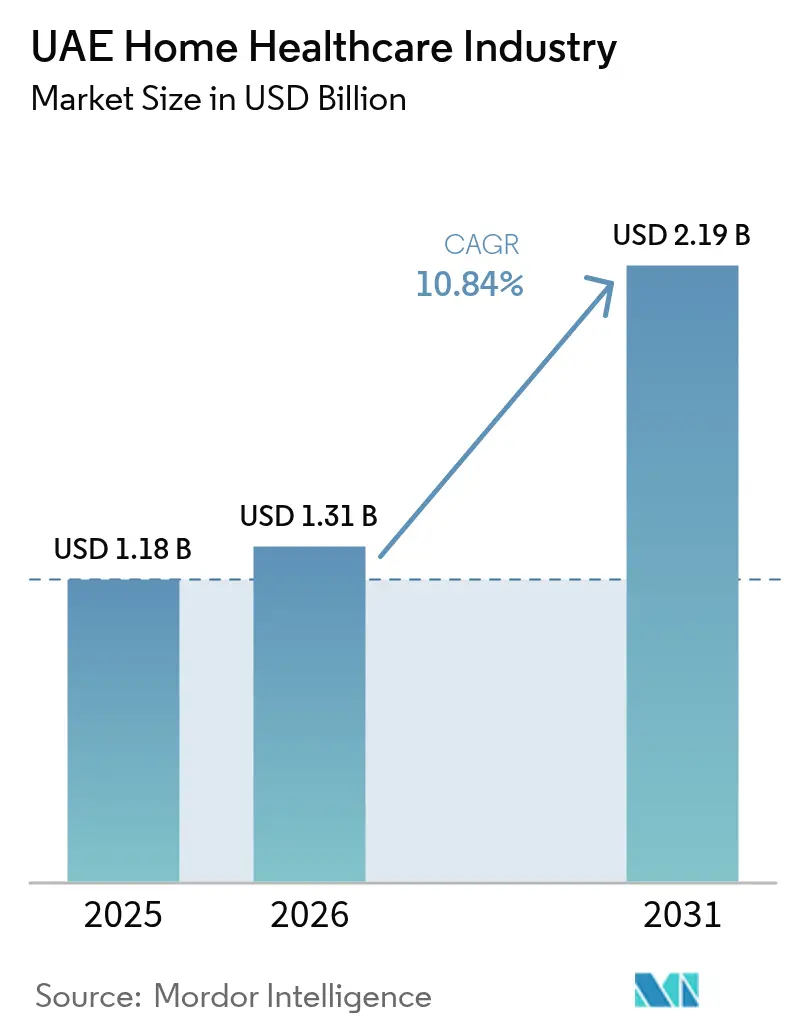

| Base Year Market Size (2025) | USD 1.18 Billion |

| Market Size (2026) | USD 1.31 Billion |

| Market Size (2031) | USD 2.19 Billion |

| Growth Rate (2026 - 2031) | 10.84% CAGR |

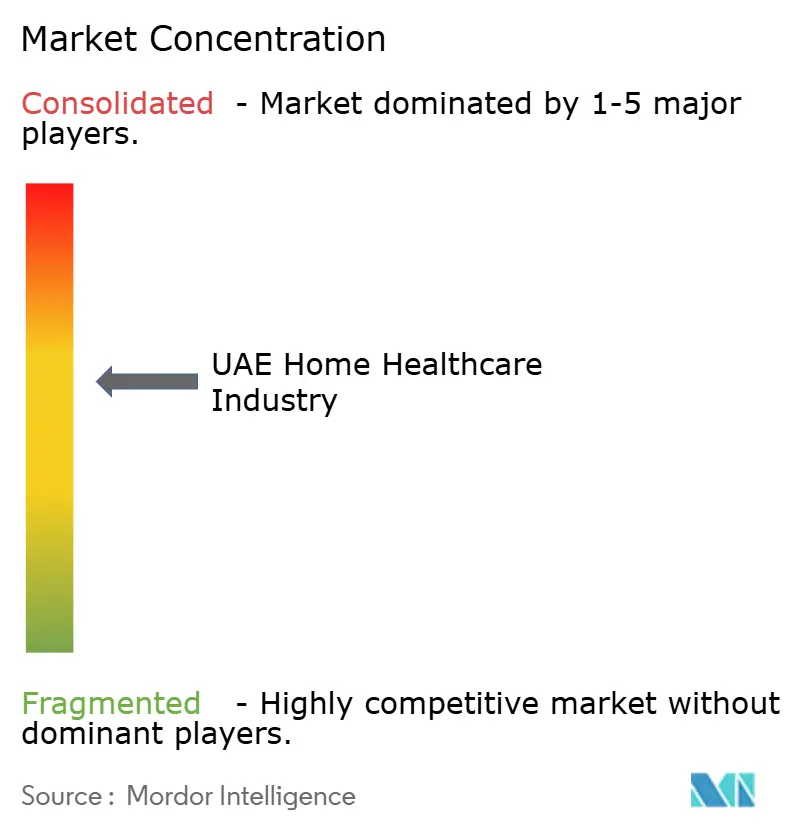

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Home Healthcare Industry Analysis by Mordor Intelligence

The UAE Home Healthcare Industry size is projected to expand from USD 1.18 billion in 2025 and USD 1.31 billion in 2026 to USD 2.19 billion by 2031, registering a CAGR of 10.84% between 2026 to 2031.

Steady expansion reflects compulsory national health insurance, which came into force on 1 January 2025, rising chronic disease prevalence, and rapid uptake of digital health tools. Private equity inflows, particularly from PureHealth and other regional investors, continue to consolidate service capacity, while AI-driven telehealth platforms increasingly shape patient expectations. Growth potential is further reinforced by Abu Dhabi and Dubai initiatives that promote virtual nursing, predictive analytics, and unified licensing to streamline clinician deployment across emirates. Medium-term opportunities will emerge in the Northern Emirates, where newly insured expatriate workers broaden the eligible user base for home-based therapies.

Key Report Takeaways

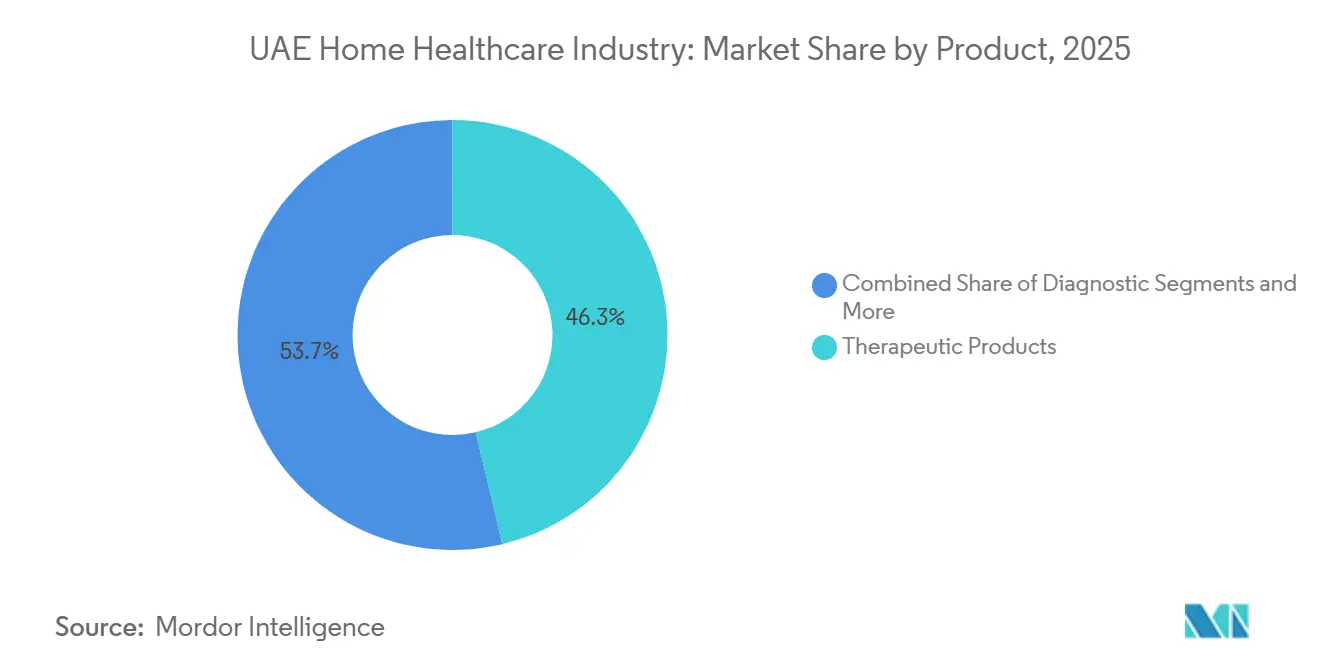

- By product category, therapeutic products led with 46.28% revenue share in 2025, while mobility care products are expected to expand at an 11.21% CAGR through 2031.

- By service, rehabilitation therapy services accounted for 37.74% of the UAE home healthcare market share in 2025; respiratory therapy services exhibit the highest projected CAGR at 11.37% through 2031.

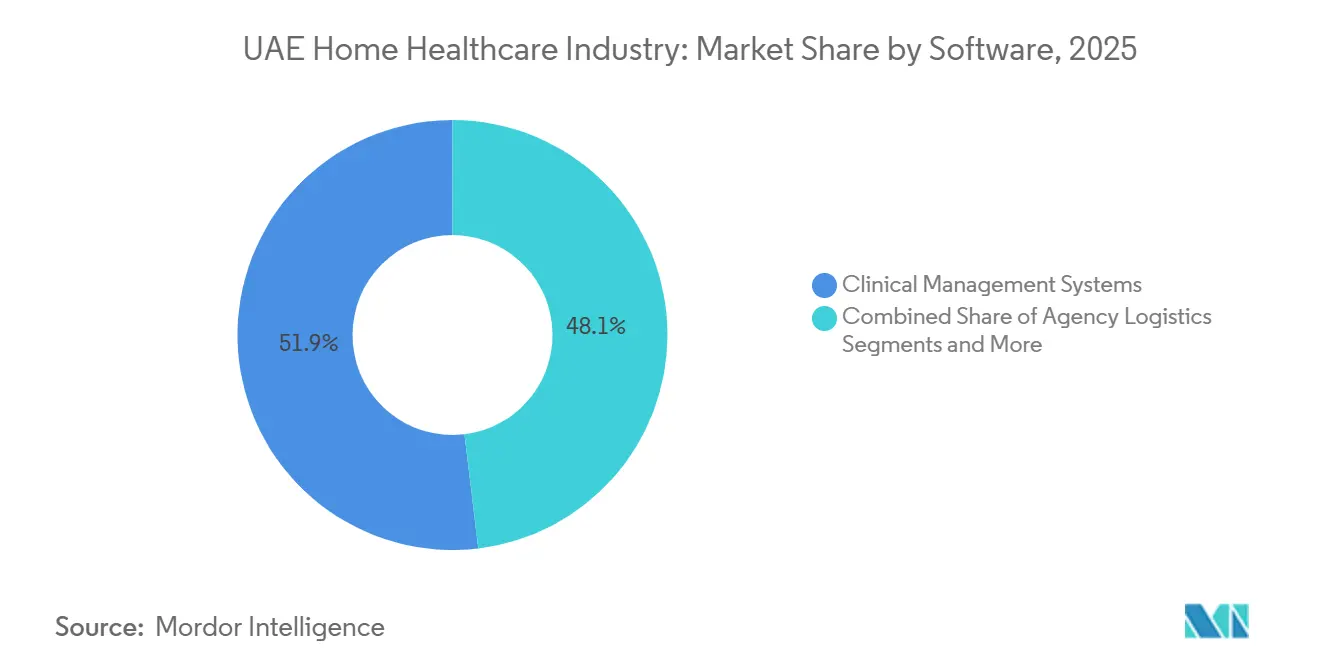

- By software, clinical management systems captured 51.92% of the UAE home healthcare market in 2025, while agency software platforms are poised to grow at a 10.96% CAGR through 2031.

- By patient condition, chronic respiratory diseases accounted for 40.98% of market activity in 2025, and cancer & palliative care services are set to advance at a 11.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Home Healthcare Industry Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Nationwide mandatory health insurance rollout (2025) | 2.8% | UAE (all emirates) | Short term (≤ 2 years) |

| Aging resident base & chronic-disease burden | 2.1% | UAE, with concentration in Abu Dhabi and Dubai | Long term (≥ 4 years) |

| Digitally enabled remote-monitoring initiatives | 1.9% | UAE (Abu Dhabi, Dubai, Sharjah) | Medium term (2-4 years) |

| Post-covid preference for in-home care | 1.5% | UAE (all emirates) | Short term (≤ 2 years) |

| Private-equity & PPP inflows into home care | 1.4% | UAE, primarily Abu Dhabi and Dubai | Medium term (2-4 years) |

| AI-powered triage & predictive-care platforms | 1.1% | UAE (Abu Dhabi, Dubai) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Nationwide Mandatory Health Insurance Rollout (2025)

Compulsory basic coverage, priced at AED 320 (USD 87.0) per beneficiary, now extends to roughly 3 million workers who previously lacked formal access to healthcare services. The scheme standardizes home-care benefits across all seven emirates, eliminating gaps that once deterred expatriates from seeking professional in-home support. Co-payments have been set at 20% for inpatient and 25% for outpatient episodes, with no waiting periods for pre-existing conditions, a notable catalyst for broader adoption of domiciliary chronic-disease programs. Providers anticipate an immediate volume increase, especially among low-income migrant families in the Northern Emirates. Early insurance claims data show a surge in reimbursed home nursing visits, confirming latent demand previously suppressed by cost barriers.

Aging Resident Base & Chronic-Disease Burden

Cancer remains the UAE’s third leading cause of death; breast, colorectal, and thyroid malignancies together represent a growing caseload that benefits from post-acute home programs. The UAE has a rapidly aging population, with individuals aged 65 and above comprising approximately 1.77% of the total population as of 2024, a figure that has steadily increased for 15 consecutive years. While still a young nation, the number of seniors is projected to grow significantly, with residents aged 60 and older estimated to increase twelvefold by 2050. Diabetes afflicts 1 in 20 residents, creating a sustained need for medication reconciliation services and glucose monitoring in domestic settings. The National Policy for Senior Citizens emphasizes mobile clinics and caregiver training, prompting providers to bundle physiotherapy and nutritional counseling into turnkey home packages. As the median age rises, demand is concentrating in Abu Dhabi and Dubai but spreading to peripheral emirates through outreach partnerships. Long-term care strategies, therefore, hinge on scalable workforces trained in geriatrics, wound care, and palliative support.

Digitally Enabled Remote-Monitoring Initiatives

Abu Dhabi’s Malaffi health-information exchange now connects 3,500+ facilities, allowing clinicians to track patient vitals and medication adherence in real time.[1]Department of Health – Abu Dhabi, “DoH to Integrate AI-Powered Technologies,” doh.gov.aeEmirates Health Services piloted a virtual nurse that triages symptoms via natural-language queries and pushes alerts to human staff if anomaly thresholds are breached.[2]Zawya, “Emirates Health Services Unveils the ‘Virtual Nurse’ Project,” zawya.com Device connectivity spans wearable sensors, Bluetooth-enabled spirometers, and AI-assisted radiology tools that interpret chest images before formal review. Providers deploying these systems report shorter hospital readmissions and higher patient‐reported satisfaction scores. Middle-term impact centers on Dubai, Sharjah, and Abu Dhabi, where fiber connectivity and smartphone penetration exceed 95%.

Post-Covid Preference For In-Home Care

Surveys conducted in 2024 found that 69.4% of UAE respondents used home delivery of medication at least once, citing convenience and infection control as key motivations. Tele-consult volumes at Dubai Health Authority grew 4-fold between 2022 and 2024, accelerating the shift toward domiciliary IV infusion and physiotherapy models. Patients now expect seamless digital scheduling, app-based follow-ups, and integrated diagnostic delivery, such as at-home ECG kits. The trend is especially pronounced among expatriate professionals balancing demanding work schedules with chronic-disease management.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Shortage of licensed home-care clinicians | -1.6% | UAE (all emirates) | Long term (≥ 4 years) |

| Limited device reimbursement by insurers | -1.2% | UAE (Dubai, Abu Dhabi, Northern Emirates) | Medium term (2-4 years) |

| Fragmented emirate-level regulations | -0.9% | UAE (inter-emirate operations) | Medium term (2-4 years) |

| Hospital-centric cultural preferences | -0.7% | UAE (Emirati nationals, older cohorts) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage Of Licensed Home-Care Clinicians

The UAE has 29,860 physicians and 63,366 nurses serving 11.35 million residents, an insufficient ratio for the rising caseload of in-home therapy. Tax-free wages up to USD 270,000 entice expatriate specialists, yet turnover persists due to cultural adjustments, language gaps, and housing costs. The October 2024 unified licensing reform eases credential transfers but cannot offset nationwide supply constraints. Providers therefore rely on tele-supervision models and international recruitment drives, especially for ICU and geriatric nurses.

Limited Device Reimbursement By Insurers

Insurers seldom cover costly durable equipment; registration alone costs AED 5,000 (USD 1,360) per device and can take 45 days. The new basic plan caps drug co-pays at AED 1,500 (USD 408), suggesting parallel limits for oxygen concentrators or CPAP units. This encourages out-of-pocket expenditure or employer-funded riders. Smaller agencies struggle to finance inventory, hindering scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Therapeutic Products Lead Market Consolidation

Therapeutic products held 46.28% of the UAE home healthcare market share in 2025. The segment benefits from high chronic-disease incidence that necessitates medication management and IV infusions at home. Device safety standards under ISO 13485 and Ministry registration requirements favor established vendors with robust quality dossiers. Mobility care products follow in revenue, yet they post the fastest 11.21% CAGR thanks to growing post-operative rehab demand and the senior citizen policy that supports assistive technologies.

Diagnostic products remain a smaller but strategic niche, capitalizing on telemedicine and AI image-analysis innovations. The UAE home healthcare market size attached to diagnostic kits will scale as insurance begins to reimburse remote testing bundles. Stakeholders therefore invest in Bluetooth glucometers and portable spirometry lines, betting on AI algorithms that flag anomalies before outpatient visits.

By Service: Rehabilitation Therapy Drives Service Innovation

Rehabilitation therapy commanded 37.74% of the UAE home healthcare market size in 2025. Early hospital discharge policies and value-based reimbursement tilt volumes into the community, making physiotherapy and occupational therapy core revenue lines. Respiratory therapy, at an 11.37% CAGR, is lifted by COPD, post-Covid fibrosis, and environmental allergens.

Infusion therapy, though niche, rides oncology and long-term antibiotic protocols. Amana Healthcare’s regional expansion showcases profitable complex case management frameworks that integrate pharmacy logistics, nurse call centers, and emergency back-up teams. Other ancillary services, including wound and ostomy care, add cross-sell potential, forging comprehensive care plans that insurers increasingly favor.

By Software: Clinical Management Systems Enable Digital Transformation

Clinical management systems accounted for 51.92% of the UAE home healthcare market share in 2025. Mandatory e-record compliance and Malaffi interoperability mandates drive adoption. Providers integrate scheduling, billing, and medication tracking into unified dashboards, cutting administrative overhead. Agency software posts an 10.96% CAGR, propelled by franchised nursing networks seeking mobile apps for route optimization and digital consent capture.

Hospice software, a smaller slice, benefits from rising palliative-care caseloads. AI plug-ins offer predictive symptom management, flagging pain-score spikes for timely interventions. Long-run differentiation will stem from analytics capabilities aligned with upcoming value-based reimbursement KPIs.

By Patient Condition: Chronic Respiratory Diseases Shape Service Delivery

Chronic respiratory diseases represented 40.98% of 2025 volumes, anchoring oxygen therapy, nebulization, and pulmonary rehab programs across the UAE home healthcare market. Dust storms and smoking prevalence prolong demand. Cancer and palliative care claim the fastest 11.62% CAGR, spurred by the National Cancer Registry’s transparent data and growing survivorship cohorts seeking comfort at home.

Diabetes and renal disorders also generate steady caseloads, requiring multi-disciplinary teams for foot care, dietetic advice, and peritoneal dialysis support. Post-operative orthopedic patients add cyclical demand for physiotherapy and pain management, translating hospital innovation into domiciliary protocols.

Geography Analysis

Abu Dhabi and Dubai jointly absorb the lion’s share of the UAE home healthcare market, owing to dense infrastructure, higher disposable incomes, and policy incentives. Abu Dhabi’s HealthX program incubates 30 global life-science start-ups that accelerate AI adoption in domiciliary care. Dubai leverages its medical-tourism brand and launched an AI medical claims platform that automates revenue cycles for 300+ providers.

The Northern Emirates represent a high-growth frontier. Sharjah and Ajman now access compulsory insurance, unlocking latent demand across expatriate worker camps. Emirates Health Services operates 132 facilities that serve as referral nodes, from which mobile nurse teams dispatch to outlying communities . Inter-emirate telemedicine integration reduces physician bottlenecks and ensures continuity.

Population clustering drives operational hubs near urban corridors, yet 88.1% urbanization masks care gaps in peri-urban outskirts. As digital health literacy rises, providers bundle smartphone monitoring kits and multilingual chatbots, extending reach without building costly bricks-and-mortar outposts.

Competitive Landscape

The UAE home healthcare market hosts a moderate level of fragmentation. PureHealth’s contemplated acquisition of NMC Healthcare signals consolidating momentum, while its organic revenue reached AED 18.9 billion (USD 5.1 billion) in the first nine months of 2024. Burjeel Holdings introduced IMed Technologies to embed AI across its continuum and posted AED 540 million (USD 146.9 million) net profit for 2023.

The merger between G42 Healthcare and Mubadala Health creates a vertically integrated powerhouse combining data analytics, genomics, and service delivery. Smaller specialists differentiate via rapid response times, multilingual staff, or oncology focus, capturing niche patient segments. Licensing unification has lowered expansion costs, prompting new entrants like ES Healthcare Centre to scale across emirates.

Technology partnerships remain a primary competitive lever: Manzil Healthcare aligned with Spectator Healthcare Technology to enhance real-time vitals tracking; M42 collaborated with Amaze Health to co-develop digital therapeutics. Agencies also vie for clinician loyalty through continuous professional development and housing subsidies to curb turnover—central to sustaining service quality.

UAE Home Healthcare Market Leaders

NMC Healthcare

Sublime Nursing

DB Health Group

Emirates Home Nursing

THB Home Health Care LLC.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Philips introduced AI-powered diagnostic and monitoring tools at Arab Health 2025, showcasing precision care solutions designed to extend hospital services into patients' homes.

- February 2025: Respircare launched a comprehensive range of respiratory therapy devices for home use at Arab Health 2025, enhancing patient access to hospital-grade ventilation and airway clearance equipment.

- May 2025: First Response Healthcare unveiled the “Drect” mobile app, aimed at streamlining patient scheduling and reinforcing the company’s technology-driven strategy.

- October 2025: Cipla expanded its Breathefree initiative to the UAE, implementing pharmacist-led educational programs focused on asthma self-management.

- October 2025: Right Health introduced “Healthcare @Home” along with an upgraded website, aiming to improve patient access to chronic disease management and post-acute recovery services.

UAE Home Healthcare Industry Report Scope

As per the scope of this report, home health care (HHC) is intended to deliver various health services and equipment to the patient while at home. HHC services are helpful when an individual requires a prolonged stay in a healthcare facility. These HHC services include various equipment, therapies, diagnostics, and software to help physicians plan efficient treatment procedures in home care settings.

The United Arab Emirates home healthcare market is segmented by product, services, software, and patient condition. By product, the market is segmented as diagnostic products, therapeutic products, and mobility care products. By service, the market is segmented as rehabilitation therapy services, respiratory therapy services, infusion therapy services, and other services. By software, the market is segmented as clinical management systems, agency software, and hospice software. By patient condition, the market is segmented into chronic respiratory diseases, diabetes and renal disorders, cancer and palliative care, and post-operative and rehabilitation. The report offers the value (USD) for the above segments.

By Product

| Diagnostic Products |

| Therapeutic Products |

| Mobility Care Products |

By Service

| Rehabilitation Therapy Services |

| Respiratory Therapy Services |

| Infusion Therapy Services |

| Palliative & Elderly Care |

By Software

| Clinical Management Systems |

| Agency Logistics & Scheduling Software |

| Hospice & Outcome-tracking Software |

By Patient Condition

| Chronic Respiratory Diseases |

| Diabetes & Renal Disorders |

| Cancer & Palliative Care |

| Post-operative / Rehab |

| By Product | Diagnostic Products |

| Therapeutic Products | |

| Mobility Care Products | |

| By Service | Rehabilitation Therapy Services |

| Respiratory Therapy Services | |

| Infusion Therapy Services | |

| Palliative & Elderly Care | |

| By Software | Clinical Management Systems |

| Agency Logistics & Scheduling Software | |

| Hospice & Outcome-tracking Software | |

| By Patient Condition | Chronic Respiratory Diseases |

| Diabetes & Renal Disorders | |

| Cancer & Palliative Care | |

| Post-operative / Rehab |

Key Questions Answered in the Report

How big is the Home Healthcare Industry In UAE Market?

The Home Healthcare Industry In UAE Market size is expected to reach USD 1.31 billion in 2026 and grow at a CAGR of 10.84% to reach USD 2.19 billion by 2031.

Which product segment holds the highest share?

Therapeutic products lead with 46.28% market share in 2025.

Who are the key players in Home Healthcare Industry In UAE Market?

NMC Healthcare, Sublime Nursing, DB Health Group, Emirates Home Nursing and THB Home Health Care LLC. are the major companies operating in the Home Healthcare Industry In UAE Market.

Which service category is expanding fastest?

Respiratory therapy services post the highest 11.37% CAGR forecast to 2031.

Page last updated on: