Patient-controlled Analgesia Pumps Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 518.66 Million |

| Market Size (2031) | USD 678.19 Million |

| Growth Rate (2026 - 2031) | 5.51% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Patient-controlled Analgesia Pumps Market Analysis by Mordor Intelligence

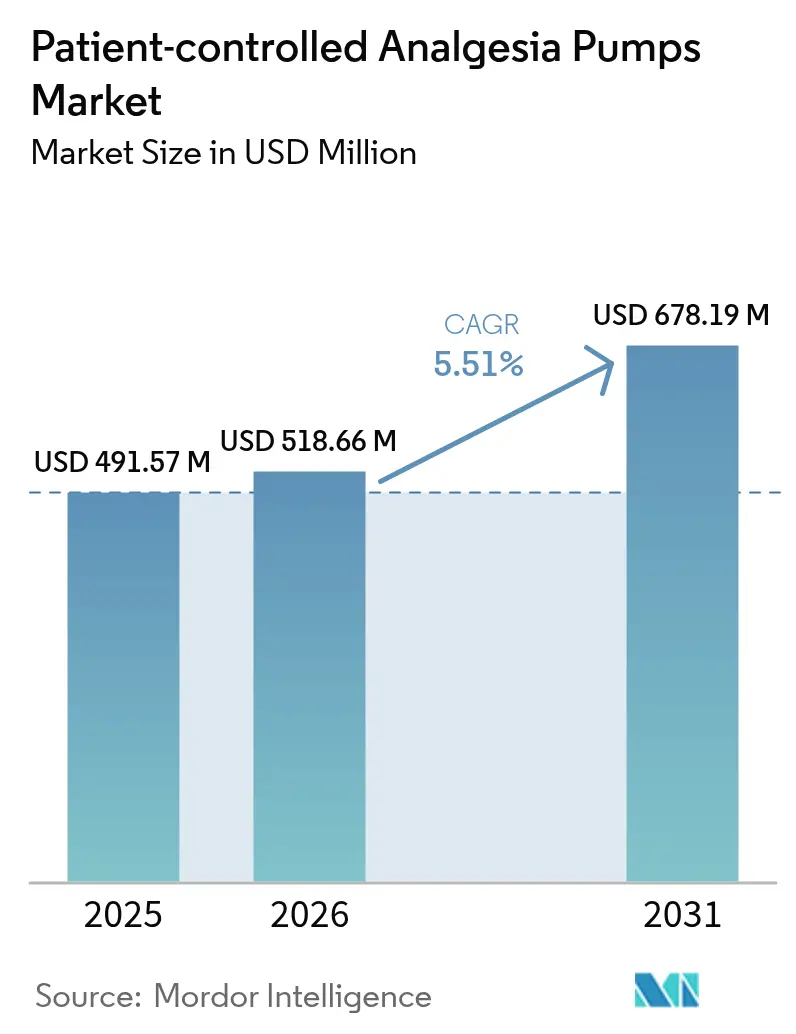

The patient controlled analgesic pumps market size is expected to grow from USD 491.57 million in 2025 to USD 518.66 million in 2026 and is forecast to reach USD 678.19 million by 2031 at 5.51% CAGR over 2026-2031. The upward trajectory reflects the transition from inpatient to outpatient and home-based care, the growing need for precision pain control, and a technology shift toward smart pumps that cut infusion-related drug errors by up to 80% Hospitals continue to anchor early adoption, yet reimbursement reforms under the NOPAIN Act are tilting demand toward the home-care channel. Regulatory recalls have simultaneously accelerated replacement cycles, driving demand for next-generation connected pumps with dose-error reduction software and cybersecurity upgrades. Product innovation remains intense as manufacturers press interoperability, advanced analytics, and wearable form factors to differentiate in a moderately fragmented arena. As a result, the patient controlled analgesic pumps market increasingly sits at the center of the broader infusion equipment ecosystem and is poised to benefit from the rising global chronic pain burden.

Key Report Takeaways

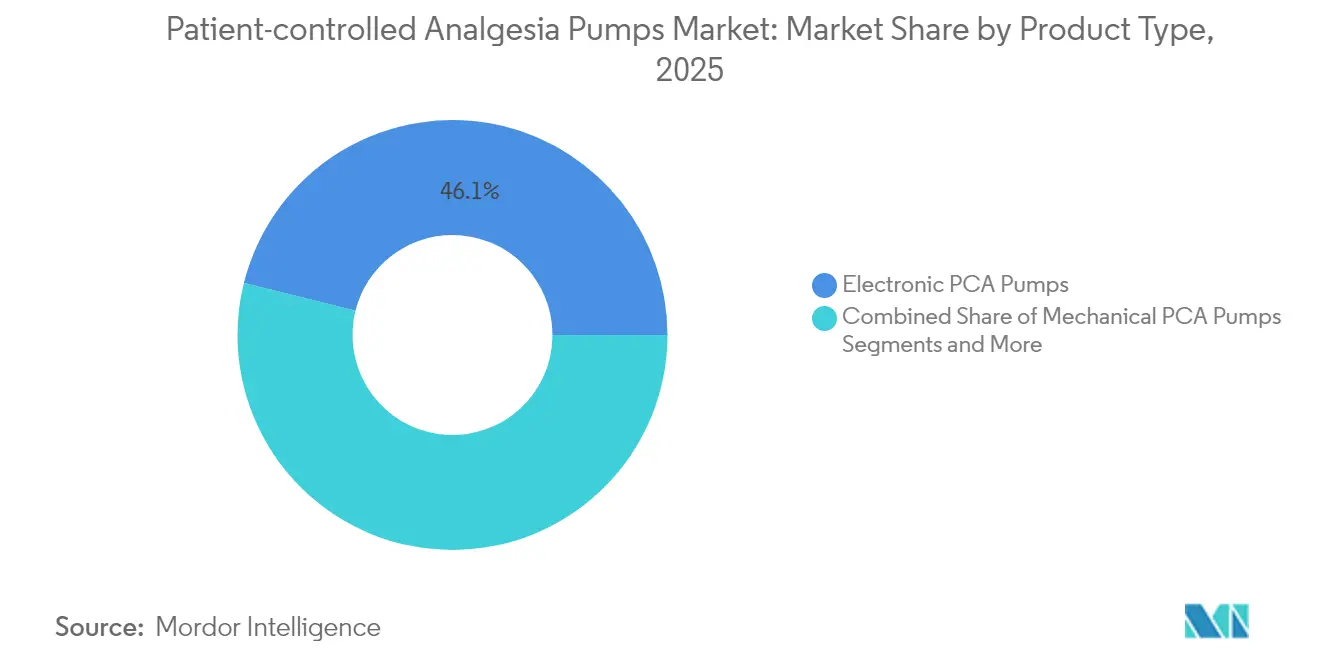

- By product type, electronic PCA pumps led with 46.12% of patient controlled analgesic pumps market share in 2025, while wearable and single-use pumps are forecast to expand at a 6.14% CAGR through 2031.

- By technology, intravenous delivery maintained 54.78% share of the patient controlled analgesic pumps market size in 2025; subcutaneous systems are growing the fastest at 6.65% CAGR.

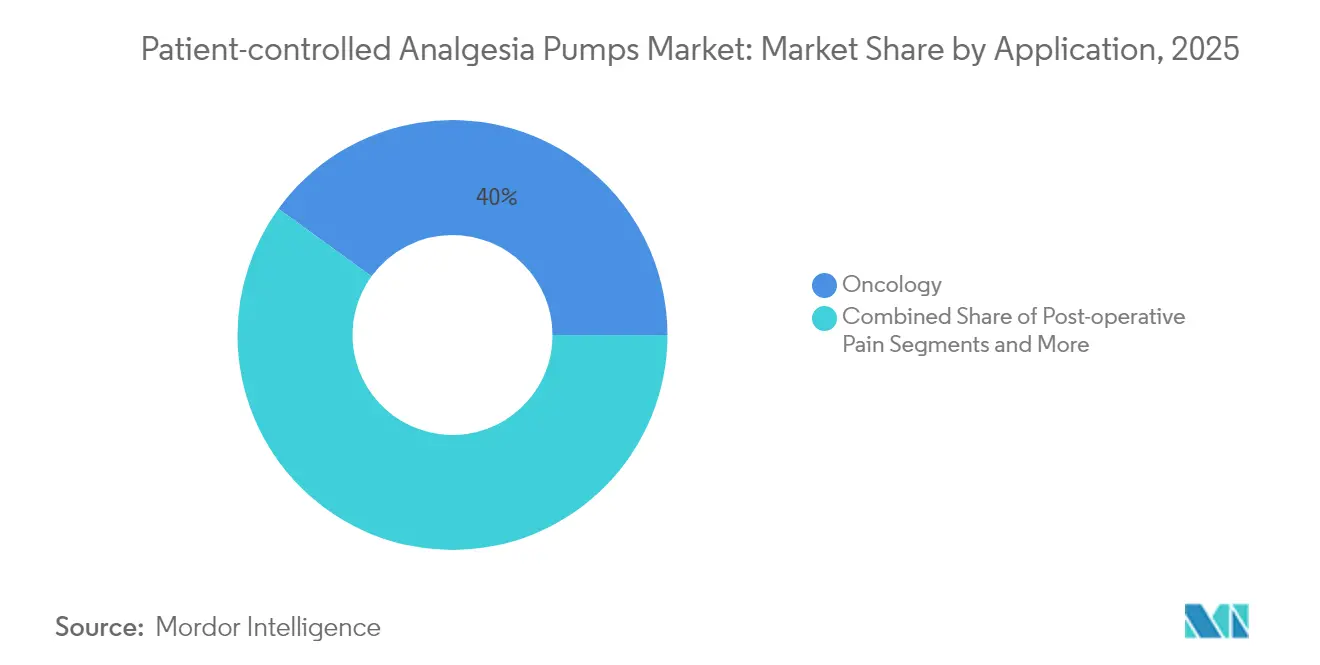

- By application, oncology captured 40.02% revenue share in 2025; diabetes-related pain management is projected to grow at a 6.86% CAGR to 2031.

- By end user, hospitals held 31.96% share in 2025, whereas home care settings are climbing at a 7.02% CAGR through 2031.

- By geography, North America accounted for 42.08% of the patient controlled analgesic pumps market in 2025; Asia-Pacific is the fastest-growing region at 7.29% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Patient-controlled Analgesia Pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ )% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart PCA pumps with advanced safety features | +1.2% | North America, EU, Global roll-out | Medium term (2-4 years) |

| Rising prevalence of chronic pain & cancer | +1.0% | Global; highest in aging economies | Long term (≥ 4 years) |

| Growing volume of surgical procedures | +0.8% | Asia-Pacific, Global | Medium term (2-4 years) |

| Growth of home & ambulatory pain management | +0.9% | North America, EU, Asia-Pacific | Medium term (2-4 years) |

| EHR-integrated dose-error reduction software | +0.6% | North America, EU | Short term (≤ 2 years) |

| Wearable single-use PCA devices | +0.7% | Developed markets first | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Smart PCA Pumps With Advanced Safety Features

Smart pumps embed drug libraries and dose-error reduction systems that intercepted nearly 37,000 deviations in a single ICU study, underscoring their preventive value [1]Peter H. S. Pelzman, “Impact of Smart Pump Interoperability on Medication Errors,” Journal of Patient Safety, journals.lww.com. Baxter’s Novum IQ platform, cleared by the FDA in 2024, exemplifies the market shift toward bi-directional EHR interoperability that pre-populates pump settings and feeds actual delivery data back into clinical records [2]Baxter International Inc., “FDA Clears Novum IQ Syringe Infusion Pump,” Baxter International, baxter.com. Evidence indicates that smart interoperability can reduce medication administration errors by 15.4%–90.5%. Consequently, healthcare systems weigh quantifiable safety outcomes over interface features when selecting vendors, reinforcing demand in the patient controlled analgesic pumps market.

Rising Prevalence Of Chronic Pain & Cancer

Cancer incidence is climbing in an aging world, driving long-term reliance on PCA modalities that preserve quality of life. Intrathecal pumps show high efficacy in refractory oncology pain. Diabetic peripheral neuropathy affects up to 40% of diabetics, with subcutaneous hydromorphone PCA titrating pain four times faster than oral opioids. These epidemiological forces create durable volume growth for the patient controlled analgesic pumps market.

Growing Volume Of Surgical Procedures

Enhanced-recovery protocols now embed PCA as standard, cutting nursing workload and shortening postoperative stays. Electronic pumps outperform elastomeric devices under temperature swings, pushing hospitals to upgrade fleets. Rising surgical throughput in Asia-Pacific adds incremental unit demand, sustaining the patient controlled analgesic pumps market expansion.

Growth Of Home & Ambulatory Pain Management

Separate Medicare reimbursement of up to USD 2,284.98 per non-opioid pump under the NOPAIN Act removes a key economic hurdle for home infusion. Portable pumps such as ON-Q and ambIT allow earlier discharge without sacrificing analgesia. Adoption requires robust patient training and connected monitoring, giving a competitive edge to vendors offering complete home-care ecosystems within the patient controlled analgesic pumps market.

EHR-Integrated Dose-Error Reduction Software

Closed-loop medication management lowers transcription errors, with one multi-hospital study seeing a 16% error reduction after EHR-pump integration. Barcode medication administration drove pump start-up compliance from 15.3% to 45.8%. Facilities now rank seamless integration among top purchasing criteria, reinforcing demand for advanced systems in the patient controlled analgesic pumps market.

Restraints Impact Analysis*

| Restraint | ( ~ )% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulation & frequent recalls | -0.8% | FDA, EU MDR regions | Short term (≤ 2 years) |

| Medication errors from poor patient education | -0.5% | Global; higher in home care | Medium term (2-4 years) |

| Cybersecurity risks in connected pumps | -0.4% | Developed markets | Short term (≤ 2 years) |

| Semiconductor & battery supply shortages | -0.6% | Global supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulation & Frequent Recalls

Class I recalls covering 52,328 Nimbus pumps in 2024 illustrate the cost of non-compliance, with six injuries and one death reported [3]U.S. Food & Drug Administration, “Class I Recall of Nimbus Infusion Pumps,” fda.gov. Warning letters to ICU Medical and Fresenius Kabi underscore rigorous oversight across design, manufacturing, and post-market surveillance. These events raise compliance spending and elongate development cycles, tempering near-term growth in the patient controlled analgesic pumps market.

Medication Errors From Poor Patient Education

Among 82,698 surgical patients, PCA device errors occurred in 0.19%, with 63% causing adverse outcomes. Home infusion magnifies user-error risk, obliging vendors to invest in intuitive interfaces and robust training support. Persistent education gaps may slow home-care penetration in segments of the patient controlled analgesic pumps market.

Cybersecurity Risks In Connected Pumps

The U.S. Cybersecurity and Infrastructure Security Agency flagged vulnerabilities in BD Alaris software that could allow unauthorized access to dose settings. Hospitals now demand validated cybersecurity architectures, putting pressure on legacy platforms and adding unforeseen cost layers to the patient controlled analgesic pumps market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Electronic Precision Sustains Leadership While Wearables Propel Growth

The patient controlled analgesic pumps market size for electronic pumps stood at USD 226.67 million in 2025, equal to 46.12% share, reaffirming provider preference for programmable accuracy. Smart logic maintains flow consistency despite ambient changes, a benefit absent in elastomeric systems. Improving battery life, color touchscreens, and network connectivity strengthen electronic incumbency. At the same time, wearable single-use devices, though representing a smaller baseline, are expanding at 6.14% CAGR. They cater to ambulatory and home scenarios where light weight and disposability trump advanced programmability. Mechanical elastomeric pumps remain fixtures in cost-sensitive settings, while implantable models serve refractory chronic pain. Accessories and disposables supply recurring revenue that offsets capital-equipment cyclicality, improving vendor resilience within the patient controlled analgesic pumps market.

Competitive strategies now hinge on broad product families that let facilities standardize on a single vendor. B. Braun’s Perfusor PCA Syringe Pump couples KeyGuard narcotic security with weight-based dosing, illustrating incremental innovation. Meanwhile, startups emphasize wearable convenience, amplifying segment diversification. Collectively, these dynamics make product breadth and service wraparounds decisive factors for share capture across the patient controlled analgesic pumps market.

By Technology: IV Supremacy Faces Subcutaneous Momentum

Intravenous systems generated 54.78% of patient controlled analgesic pumps market share in 2025, driven by broad surgical and critical care use. Clinicians value rapid onset and dose titration, attributes well documented in postoperative pain literature. Yet subcutaneous devices are scaling fastest at 6.65% CAGR, aided by lower infection risk and suitability for home use. Successful hydromorphone titration within 5.5 hours underscores clinical appeal. Epidural and transdermal approaches occupy specialized niches, supported by microneedle advances that promise non-invasive delivery. Vendors winning in this space focus on formulation science and patient comfort, steadily shifting technology mix within the patient controlled analgesic pumps market.

By Application: Oncology Holds the Lead as Diabetes Surges

Oncology account for 40.02% of the patient controlled analgesic pumps market in 2025, reflecting the high analgesic demand in cancer care. Intrathecal drug delivery offers relief where systemic regimens fail, reinforcing device relevance. Diabetes-related pain is climbing at a 6.86% CAGR on rising neuropathy prevalence. Clinicians increasingly adopt PCA for flexible dosing, boosting overall device throughput in the patient controlled analgesic pumps market. Post-operative needs remain foundational, while pediatric pain and chronic non-cancer applications add incremental volume. Manufacturers supplying pathology-specific protocols and clinical evidence strengthen competitive positioning.

By End User: Hospital Control Shifts Toward Home Care

Hospitals contributed 31.96% of patient controlled analgesic pumps market size in 2025, underpinned by complex cases, central pharmacies, and IT infrastructure. The home-care segment, however, is expanding fastest at 7.02% CAGR, buoyed by NOPAIN Act reimbursement and patient preference for self-care. Ambulatory surgical centers and pain clinics also escalate demand as outpatient procedures and chronic pain programs grow. Vendors integrating remote monitoring, cloud dashboards, and 24/7 support gain traction with non-hospital buyers across the patient controlled analgesic pumps market.

Geography Analysis

North America led the patient controlled analgesic pumps market with 42.08% revenue share in 2025, propelled by advanced health systems, clear reimbursement, and early smart-pump adoption. The NOPAIN Act encourages shift to non-opioid devices and home settings, feeding domestic uptake through at least 2027. Canada mirrors U.S. trends at smaller scale, while Mexico’s ongoing hospital upgrades fuel mid-single-digit gains. These dynamics keep North America at the technological frontier of the patient controlled analgesic pumps market.

Asia-Pacific represents the fastest expansion at 7.29% CAGR to 2031. Rising surgical volumes, wider cancer screening, and escalating chronic disease rates underpin device demand. Terumo’s Rika platform, with 98 U.S. installations as of August 2024, showcases Japanese engineering now targeting 20-25% share through multiphase rollout. China’s public hospital modernization and India’s private sector growth together anchor regional momentum. Yet diverse regulatory regimes require localized strategies, making strong distributor networks critical for capturing growth in the patient controlled analgesic pumps market.

Europe maintains material presence thanks to robust quality standards and social insurance coverage. Germany, France, and the United Kingdom serve as innovation hubs, whereas Southern and Eastern Europe trail in adoption pace. National health systems weigh cost-effectiveness heavily, setting a high bar for value demonstration. South America and Middle East & Africa contribute limited volume but hold long-term promise as infrastructure matures, creating a multi-speed map for the patient controlled analgesic pumps market.

Competitive Landscape

The patient controlled analgesic pumps market is moderately fragmented. Baxter International, ICU Medical, and BD anchor the top tier, leveraging scale, service, and regulatory muscle. Mid-sized specialists such as Micrel Medical and Epic Medical compete through niche innovations, while technology entrants push connectivity and analytics. FDA recalls in 2024 sent a compliance shockwave that elevated quality management as a decisive differentiator. Smart pump platforms demonstrating up to 90.5% error reduction and EMR interoperability yield measurable cost avoidance for providers, shifting competition toward outcomes rather than price.

Strategic moves illustrate differing playbooks. Baxter secured FDA clearance for Novum IQ syringe pumps with bi-directional EMR links in 2024. Terumo scales global footprint by exporting its Rika syringe system on the back of established cardiology relationships. B. Braun refreshes its Perfusor line with KeyGuard access controls to address opioid diversion concerns. Partnerships with EHR vendors, cybersecurity certification, and remote support platforms now headline investment priorities as vendors fight for sticky, long-term contracts across the patient controlled analgesic pumps market.

Moderate consolidation is likely as regulatory pressure inflates compliance costs and smaller players struggle to keep pace. Yet open interfaces and cloud-based analytics lower entry barriers for software-centric innovators, sustaining competitive churn and continuous differentiation in the patient controlled analgesic pumps market.

Patient-controlled Analgesia Pumps Industry Leaders

B. Braun SE

BD (Becton Dickinson, and Company)

Baxter

Fresenius SE & Co. KGaA

ICU Medical, Inc (Smiths Medical)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2023: Stevenson Memorial Hospital Foundation received a USD 10,000 donation from Alectra Inc. toward the purchase of a PCA pump.

- August 2022: The FDA granted 510(k) clearance for Baxter’s Novum IQ syringe infusion pump with Dose IQ Safety Software.

- March 2022: Shanghai MicroPort Lifesciences obtained NMPA approval for its AutoEx chemotherapy infusion pump, the first product in its intelligent oncology pain portfolio.

Global Patient-controlled Analgesia Pumps Market Report Scope

As per the scope of the report, patient-controlled analgesia (PCA) pumps are devices that can help patients control their pain by regulating the amount of medication used in managing pain. These PCA pumps contain a pain medication syringe that delivers a small amount of prescribed medication at a constant flow rate to the patient. The patient-controlled analgesia pumps market is segmented by product type (PCA pumps and pump accessories), application (oncology, diabetes, neonatology, and other applications), end users (hospital, ambulatory surgical centers, and home-care settings), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends of 17 countries across major regions globally. The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| Electronic PCA Pumps |

| Mechanical PCA Pumps |

| Wearable / Single-use PCA Pumps |

| Implantable / Intrathecal PCA Systems |

| Pump Accessories & Disposables |

| Intravenous PCA |

| Epidural PCA |

| Subcutaneous PCA |

| Transdermal / Alternative Routes |

| Oncology |

| Post-operative Pain |

| Chronic Non-cancer Pain |

| Diabetes-related Pain |

| Pediatrics & Neonatology |

| Palliative & End-of-life Care |

| Hospitals |

| Ambulatory Surgical Centers |

| Home-care Settings |

| Pain Clinics & Specialty Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Electronic PCA Pumps | |

| Mechanical PCA Pumps | ||

| Wearable / Single-use PCA Pumps | ||

| Implantable / Intrathecal PCA Systems | ||

| Pump Accessories & Disposables | ||

| By Technology | Intravenous PCA | |

| Epidural PCA | ||

| Subcutaneous PCA | ||

| Transdermal / Alternative Routes | ||

| By Application | Oncology | |

| Post-operative Pain | ||

| Chronic Non-cancer Pain | ||

| Diabetes-related Pain | ||

| Pediatrics & Neonatology | ||

| Palliative & End-of-life Care | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Home-care Settings | ||

| Pain Clinics & Specialty Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current Patient-controlled Analgesia Pumps Market size?

The patient controlled analgesic pumps market stands at USD 518.66 million in 2026 and is on track to reach USD 678.19 million by 2031.

Who are the key players in Patient-controlled Analgesia Pumps Market?

B. Braun SE, BD (Becton Dickinson, and Company), Baxter, Fresenius SE & Co. KGaA and ICU Medical, Inc (Smiths Medical) are the major companies operating in the Patient-controlled Analgesia Pumps Market.

Which is the fastest growing region in Patient-controlled Analgesia Pumps Market?

Asia-Pacific is projected to post the highest CAGR at 7.29% thanks to rapid surgical volume growth and expanding healthcare infrastructure.

How are regulatory recalls influencing the market?

Frequent FDA recalls raise compliance costs, shorten replacement cycles, and favor vendors with robust quality systems.

Page last updated on: