Passenger Emergency Oxygen Deployment Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

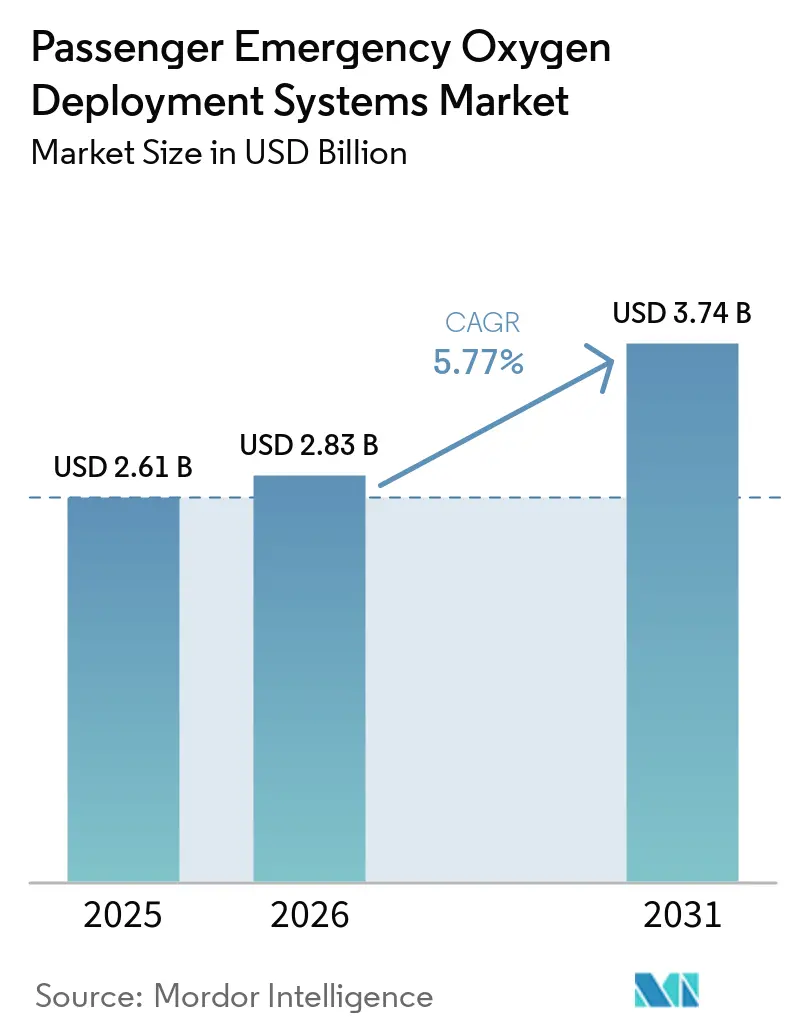

| Market Size (2026) | USD 2.83 Billion |

| Market Size (2031) | USD 3.74 Billion |

| Growth Rate (2026 - 2031) | 5.77% CAGR |

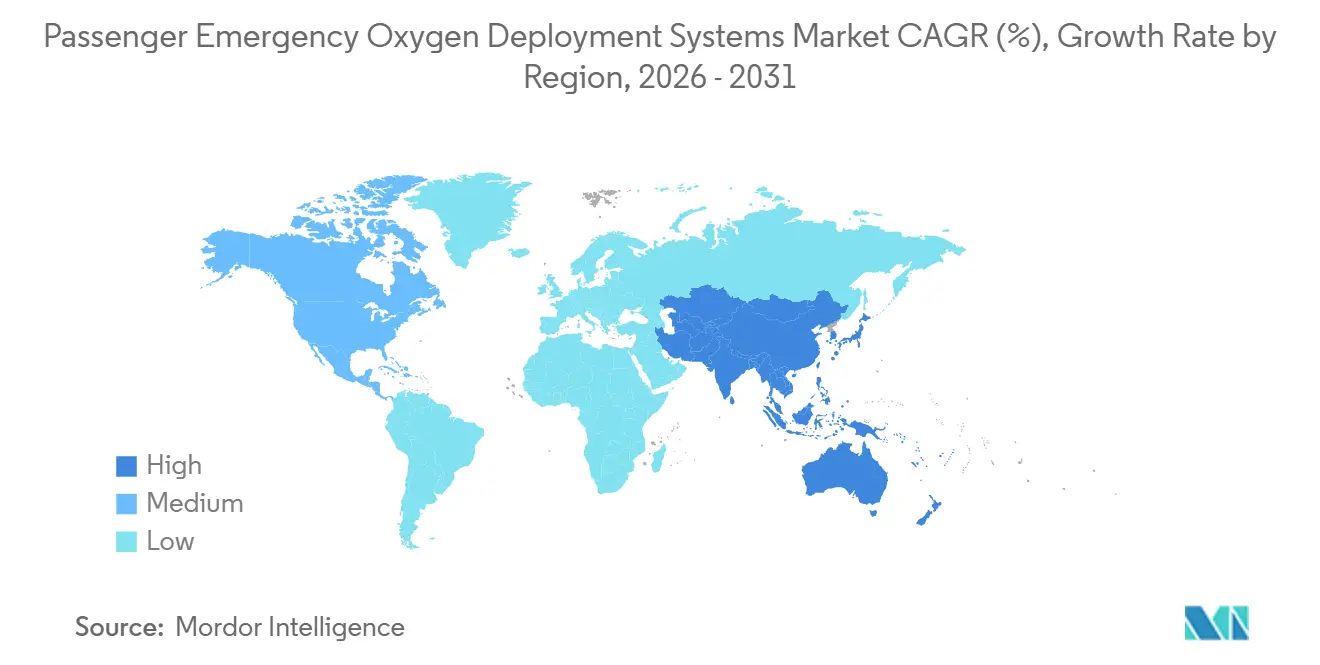

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Passenger Emergency Oxygen Deployment Systems Market Analysis by Mordor Intelligence

The passenger emergency oxygen deployment systems market size is expected to grow from USD 2.61 billion in 2025 to USD 2.83 billion in 2026 and is forecast to reach USD 3.74 billion by 2031 at a 5.77% CAGR over 2026-2031. Market growth is primarily driven by fleet expansion, regulatory compliance, and retrofit cycles, rather than significant product innovations. Airlines are focusing on weight-saving delivery modules, such as pulse-demand regulators, to reduce fuel costs, although most cabins continue to utilize traditional chemical generators. Stricter FAA and EASA regulations are reducing replacement intervals, while North American and European carriers work to update dispatch rules in line with evolving bleed-air and cybersecurity standards. Concurrently, the rapid addition of aircraft in the Asia-Pacific region is driving high linefit volumes, which are expected to sustain aftermarket demand for years to come. Meanwhile, unresolved issues with the military’s On-Board Oxygen Generation Systems (OBOGS) continue to limit the adoption of pressure-swing adsorption technology in the commercial sector, thereby maintaining the dominance of chemical oxygen systems in the installed base.

Key Report Takeaways

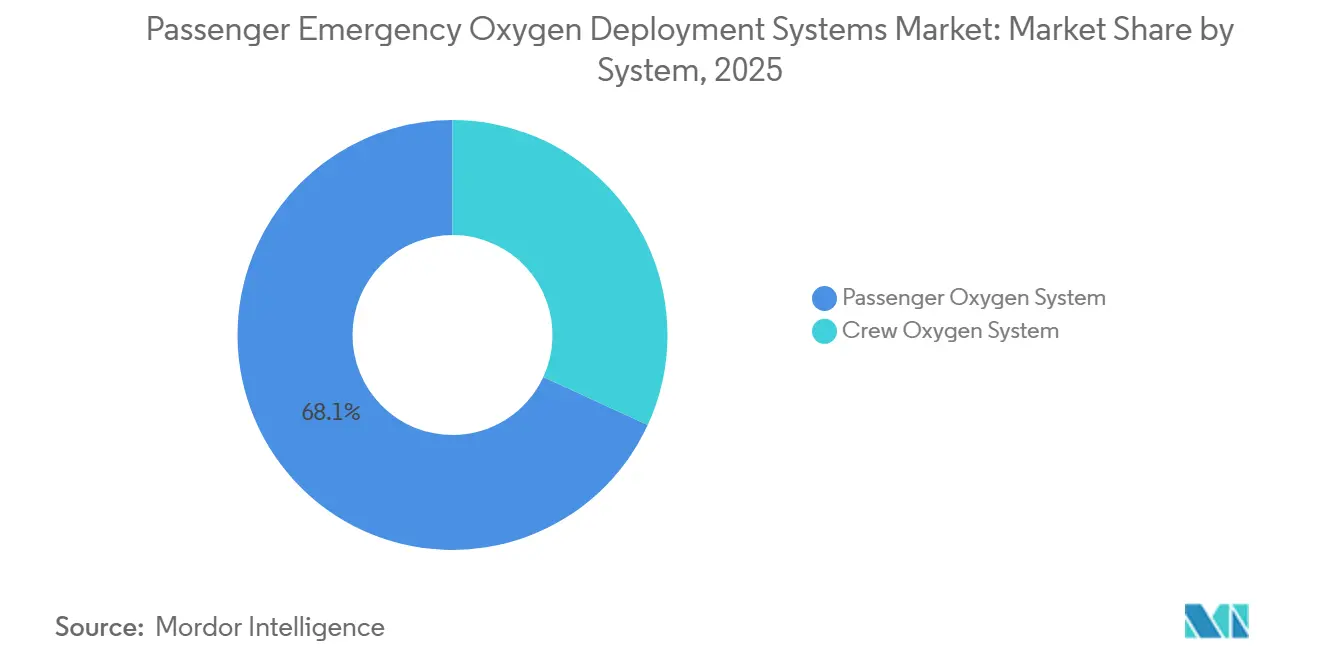

- By system, passenger oxygen accounted for 68.12% of the passenger emergency oxygen deployment systems market share in 2025, while crew oxygen is projected to have the fastest growth rate of 6.02% from 2026 to 2031.

- By aircraft type, commercial platforms accounted for 74.35% of revenue share in 2025; general aviation is forecast to expand at a 6.24% CAGR through 2031.

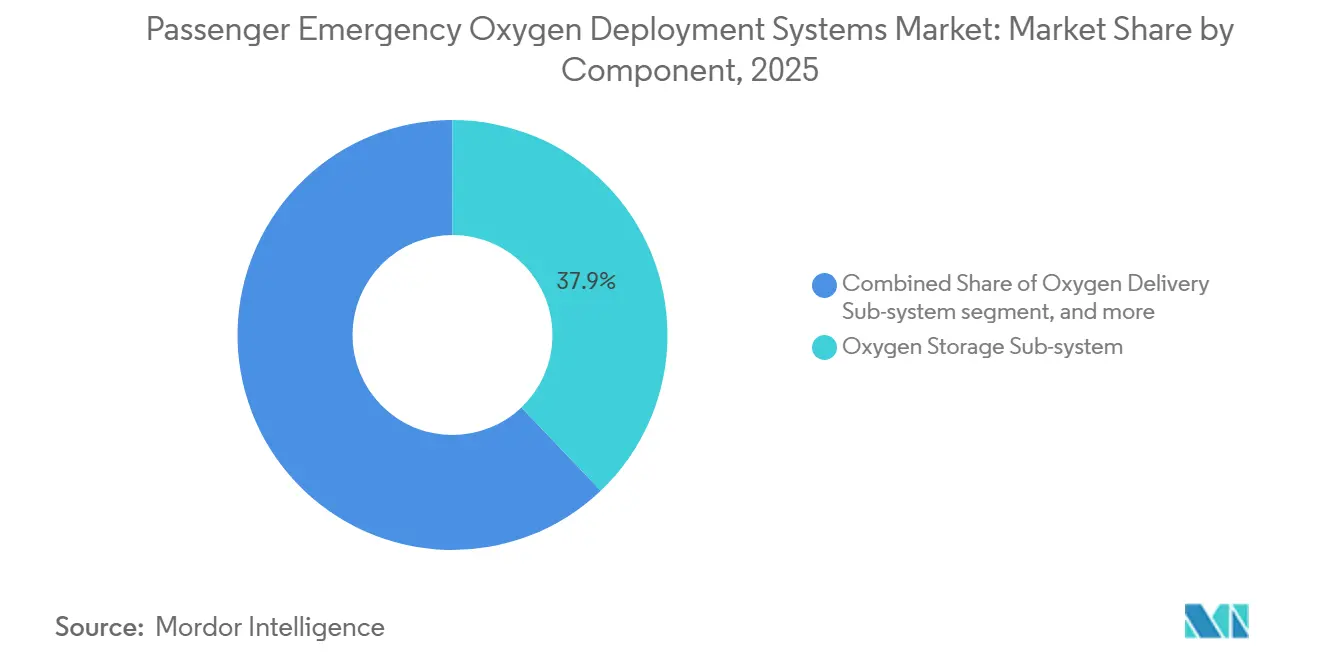

- By component, oxygen storage subsystems accounted for 37.89% of 2025 revenue, whereas delivery subsystems are forecast to grow at a 5.99% CAGR.

- By end-user, linefit commanded a 75.12% share in 2025; retrofit demand is forecast to grow at a brisk 6.85% CAGR, led by Gulf carrier widebody programs.

- By geography, North America led with 34.17% revenue in 2025, while the Asia Pacific is projected to post the strongest CAGR of 6.08% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Passenger Emergency Oxygen Deployment Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging global passenger traffic | +1.20% | Global with Asia-Pacific core and spill-over to Middle East | Medium term (2-4 years) |

| Stricter FAA/EASA safety mandates | +1.00% | North America and Europe, cascading to Asia-Pacific | Short term (≤ 2 years) |

| Accelerated fleet-modernization cycles | +0.90% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Commercial adoption of OBOGS | +0.60% | North America and Europe, limited Asia-Pacific penetration | Long term (≥ 4 years) |

| Smart-sensor predictive maintenance | +0.50% | North America and Europe, early adopters in Middle East | Medium term (2-4 years) |

| PEODS for eVTOL and urban air mobility | +0.30% | North America and Europe pilot programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Global Passenger Traffic

According to the International Air Transport Association (IATA), global enplanements are projected to reach 5.2 billion in 2025, a 6.7% increase from 2024. Each new single-aisle aircraft requires 150-180 drop-down masks, while widebody aircraft need 250-400 units. Airbus forecasts that the global fleet will double to 49,210 aircraft by 2044, ensuring steady demand for passenger emergency oxygen deployment systems in linefit orders. Growth is particularly prominent in India and South Asia, with 2,835 additional aircraft expected by 2043, securing long-term spares contracts. As passenger volumes grow faster than crew hiring, airlines face increased exposure to in-flight medical events. However, many carriers continue to opt for low-cost chemical oxygen generators over longer-lasting gaseous systems. This imbalance supports demand for both initial installations and compliance-driven replacements.

Stricter FAA/EASA Safety Mandates

Between 2024 and 2025, the FAA issued three significant airworthiness directives affecting 2,600 B737 generators, 3,777 Safran/AVOX valves, and 80,000 protective-breathing units, necessitating unscheduled replacements and boosting the passenger emergency oxygen deployment systems market.[1]“Airworthiness Directives 2024-14-09, 2024-21-08, 2025-25-12,” FAA, faa.gov EASA followed with directives addressing generator thermal runaway and related hazards, including AD 2023-0209, 2024-0186, and 2024-0198.[2]“Airworthiness Directives 2023-0209, 2024-0186, 2024-0198,” EASA, easa.europa.eu ICAO harmonization ensures that these regulations will be extended globally within two to three years, impacting fleets in the Asia-Pacific and the Middle East. Additionally, the FAA's December 2025 directive amended donning procedures, highlighted training gaps, and drove cockpit-system upgrades with integrated diagnostics. These developments collectively accelerate replacement cycles and shift operator budgets toward established, regulator-approved suppliers.

Accelerated Fleet-Modernization Cycles

Shortened retirement ages, ranging from 22 to 24 years for single-aisle aircraft and 18 to 20 years for widebody aircraft, are driving increased aircraft retirements, thereby fueling demand for both linefit and retrofit oxygen systems. Emirates’ USD 5 billion program for 219 jets and flydubai’s B737-800NG overhauls illustrate this trend, with each widebody retrofit generating USD 150,000 to USD 250,000 in oxygen-system revenue. Innovations like Collins Aerospace’s PulseOx regulators reduce the weight of the centralized gaseous system by 450 lbs and cut fuel consumption by 0.03% on 12-hour flights, achieving a 4-year payback period.[3]“Oxygen Systems Product Portfolio 2025,” Collins Aerospace, collinsaerospace.com These weight-saving benefits, combined with bundled cabin-upgrade budgets, ensure that fleet modernization remains a key growth driver even when new aircraft deliveries slow.

Commercial Adoption of OBOGS

Pressure-swing-adsorption technology offers an unlimited in-flight oxygen supply, but safety concerns persist due to 603 unexplained physiological episodes in F/A-18s (2010-2015) and 323 in T-6 trainers (2010-2020). NASA identified regulator hysteresis and CO₂ spikes as contributing factors. While Honeywell’s GENOX and Collins’ cBRAG systems now include real-time diagnostics, they remain limited to military applications. Civil certification faces delays of 12 to 18 months due to FAA Advisory Circular 20-144A’s cyber-hardening requirements. Once the US Department of Defense (DoD) addresses its backlog of corrective actions, early commercial adopters, likely widebody freighters or premium-cabin operators, could initiate a new high-margin product cycle in the passenger emergency oxygen deployment systems market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High certification and qualification costs | -0.8% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Expensive retrofit programs | -0.6% | Global, concentrated in mature fleets | Medium term (2-4 years) |

| Sodium-chlorate supply risk | -0.4% | Global, supply concentration in Asia-Pacific | Medium term (2-4 years) |

| Cyber-hardening delays | -0.3% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Certification and Qualification Costs

Compliance with TSO-C99b and TSO-C78a standards requires altitude-chamber, flammability, and human-factors testing, which costs between USD 2 million and USD 5 million per variant. EASA’s duplicative ETSO regulations further increase costs. FAA Advisory Circular 20-144A adds cybersecurity compliance under DO-326A and DO-356A, extending timelines and encouraging consolidation among smaller suppliers. For example, Safran’s EROS family benefits from grandfathered approvals, providing a competitive cost advantage. In response, Aerox has acquired Omnigas, Sky-Ox, and Fluid Power to pool certifications and distribute fixed costs across a broader product line. These high costs deter new entrants and delay the introduction of innovative designs.

Expensive Retrofit Programs

Widebody retrofits require 250-400 new masks and generator replacements, with a 15-year life expectancy, adding USD 150,000-USD 250,000 per aircraft to cabin-upgrade budgets. Narrow-body retrofits cost USD 80,000 to USD 120,000, straining the cash flows of low-cost carriers. Operators often postpone replacements until mandated by airworthiness directives, leading to rushed parts orders and extended aircraft downtime. While Collins’ PulseOx system offers annual fuel savings of USD 50,000 to USD 80,000 with a three-year payback period, financially constrained carriers may still hesitate to invest. Additionally, long lead times for parts, such as Safran’s 6 to 9-month LAVOX installation kits, complicate planning and execution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System: Crew Oxygen Outpaces Passenger Growth

The crew oxygen systems market is projected to grow at a CAGR of 6.02% through 2031, surpassing the passenger segment's growth rate, although the latter remains larger in absolute terms. The December 2025 FAA Airworthiness Directive (AD) highlighted training deficiencies, prompting airlines to adopt diagnostic-equipped cockpit regulators to enhance compliance and maintenance efficiency. Collins Aerospace's cBRAG system, currently deployed in military fleets, exemplifies advanced technology awaiting civil certification. Despite this, passenger cabins accounted for 68.12% of the 2025 revenue, driven by widebody aircraft that require up to 400 masks per unit. Safran's Hi-EFF chemical generators continue to dominate the market despite EASA-issued thermal-runaway alerts, thanks to their low ownership costs.

Crew oxygen demand is further supported by test deployments of miniature On-Board Oxygen Generation System (OBOGS) cartridges, which limit the impact of failure to the cockpit, providing a testing ground for regulators before approving full-cabin systems. North American and European carriers are leading these trials, while Asia-Pacific operators focus on bulk passenger installations to meet rising demand. These differing priorities ensure growth in both sub-markets, though the technology mix and certification timelines vary significantly across regions.

By Aircraft Type: General Aviation Leads CAGR

General aviation is expected to achieve a CAGR of 6.24% through 2031, outpacing commercial and military segments. However, commercial aviation remains dominant, accounting for 74.35% of 2025 revenue. Business jet operators are retrofitting older Gulfstream and Bombardier models to comply with FAA altitude dispatch rules, with retrofit costs ranging from USD 40,000 to USD 80,000 per aircraft. Aerox’s acquisitions of Omnigas and Sky-Ox aim to consolidate this fragmented market.

Commercial fleets exhibit stronger absolute spending power, with each A321neo or B737 MAX carrying USD 300,000 to USD 500,000 worth of oxygen systems at the linefit stage. Linefit volumes are heavily concentrated in orders from the Asia-Pacific region. The military segment remains tied to OBOGS maturity timelines, with lessons from combat applications translating slowly into civil aviation options.

By Component: Delivery Sub-systems Gain Ground

Delivery modules are projected to grow at a CAGR of 5.99% through 2031, challenging storage sub-systems, which accounted for 37.89% of 2025 revenue. Pulse-demand regulators, which reduce weight and improve carbon efficiency, are gaining traction. Emirates incorporated PulseOx into its widebody fleet overhaul to achieve immediate fuel savings. Masks and dispensing units align with overall market growth due to their predictable replacement cycles, with Safran shipping 2.5 million masks over five years.

Storage technologies are growing more slowly as operators assess the risks associated with sodium-chlorate concentration and thermal runaway. With limited certified alternatives, carriers continue to use existing chemistries while increasing inspection intervals, resulting in steady but slower demand.

By End-User: Retrofit Momentum Builds

Linefit systems accounted for 75.12% of 2025 revenue, driven by the significant narrow-body aircraft backlog. However, retrofit systems are growing faster, with a projected CAGR of 6.85%. The passenger emergency oxygen deployment systems market benefits from cabin overhauls by airlines such as Emirates, flydubai, and Qatar Airways, which combine mandatory generator replacements with connectivity upgrades. North American and European fleets, averaging 12-14 years in age, are nearing the 15-year generator life limit, triggering a wave of replacements through 2031.

Linefit systems remain strategically crucial for suppliers, as their installation secures decades of aftermarket revenue and positions vendors to offer predictive maintenance software as carriers digitize safety equipment. Retrofit systems, however, provide opportunities for challenger brands, provided they meet certification and production requirements to address tight AD-driven schedules.

Geography Analysis

North America accounted for 34.17% of 2025 revenue, driven by an aging fleet and recent FAA airworthiness directives that accelerate replacements. Operators serving high-elevation hubs, such as Denver, are upgrading regulators to maintain cabin altitude limits, creating a USD 1.2-2 billion opportunity over five years. The region leads OBOGS research, positioning domestic vendors to transition technology to civil programs once certification is achieved.

Asia-Pacific is expected to grow at the fastest CAGR of 6.08%, fueled by record aircraft deliveries in India, China, and Southeast Asia. Boeing forecasts 2,835 new aircraft for South Asia alone, with each linefit generating a long-term spares revenue stream. While the CAAC has yet to mandate FAA-level cybersecurity reviews, operators are monitoring developments from EASA and ICAO, indicating a potential compliance phase post-2027 that could drive additional retrofits.

Europe mirrors the FAA’s regulatory approach, with three recent ADs and a fleet averaging 11-13 years in age, signaling imminent generator replacements. The Middle East offsets its younger fleet age with large-scale upgrades, as Emirates manages 140 B777s and 116 A380s, each requiring up to 400 masks, ensuring a steady pipeline of retrofits. South America and Africa contribute smaller volumes but are expected to align with global standards by 2028, providing a delayed but visible growth opportunity.

Competitive Landscape

Safran, Collins Aerospace, and Cobham collectively hold an estimated 55%-65% share of the passenger emergency oxygen deployment systems market, supported by long-standing sole-source contracts for A320, A350, B737, B777, and B787 programs. These installed bases provide predictable aftermarket revenue and deter new entrants, as certification costs per variant range from USD 2 million to USD 5 million. However, recent ADs addressing chemical-generator incidents are eroding incumbents’ advantages, prompting carriers to explore lighter pulse-delivery units.

Aerox’s acquisitions of Omnigas, Sky-Ox, and Fluid Power highlight consolidation trends among smaller firms aiming to scale in the retrofit aftermarket. Honeywell is positioning for future market share with its GENOX OBOGS platform, but must address the 32 corrective actions identified in the DoD’s 2021 audit of physiological episodes. Meanwhile, Safran is diversifying with LAVOX lavatory oxygen modules, which address niche compliance requirements but require airframe-specific kits with extended lead times.

Cybersecurity is emerging as a critical factor under AC 20-144A. Collins Aerospace has invested in DO-326A processes, giving it an advantage as connected diagnostics become mandatory. Suppliers lacking robust cybersecurity strategies risk losing linefit contracts, intensifying competition in an otherwise stable market.

Passenger Emergency Oxygen Deployment Systems Industry Leaders

Cobham Limited

Diehl Stiftung & Co. KG

Eaton Corporation plc

Safran SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Honeywell introduced a new technology designed to assist military pilots of high-performance fighter jets in managing their breathing under extreme conditions. The Connected Breathing Regulator and Anti-G (cBRAG) technology improves breathing regulation to support pilots exposed to high G-forces during intense acceleration. High G-forces can strain the body’s circulatory and respiratory systems, potentially causing physiological issues such as G-force-induced loss of consciousness. Honeywell’s cBRAG addresses these challenges in extreme flight conditions by utilizing an electro-mechanical anti-G valve and programmable pressure breathing schedules. This technology enables precise adjustments to aircrew oxygenation and G-force protection based on real-time flight parameters.

- February 2025: Aerox Aerospace Group announced the acquisition of Medley, FL-based Omnigas Systems, Inc., a provider of aftermarket services for aerospace oxygen and fire suppression systems catering to commercial aviation, business aviation, and military customers. This acquisition highlights Aerox's commitment to offering comprehensive aviation oxygen solutions to the global aerospace industry. The addition of Omnigas strengthens Aerox's ability to support a broader in-service fleet and a wider range of oxygen system manufacturers. This marks the fourth acquisition by Aerox Aerospace Group, following the acquisitions of Aerox Aviation Oxygen Systems in 2020, Sky-Ox Aviation Oxygen in 2022, and Fluid Power, Inc. in 2023. Alderman & Company acted as the exclusive financial advisor for the sale of Omnigas Systems to Aerox Aerospace Group.

Global Passenger Emergency Oxygen Deployment Systems Market Report Scope

Passenger emergency oxygen deployment systems (PEODS) are assemblies designed to store, regulate, and deliver breathable oxygen to passengers and crew in the event of cabin pressure loss or in-flight medical emergencies, ensuring adherence to global safety and airworthiness standards. The study of PEODS encompasses the design, production, installation, maintenance, and overhaul of oxygen equipment for passengers and crew. This includes storage cylinders, chemical generators, delivery regulators, masks, and dispensing units used on commercial, military, and general aviation aircraft worldwide. The market scope also includes component-level inspections and replacement cycles associated with scheduled maintenance or airworthiness directives.

The passenger emergency oxygen deployment systems market is segmented by system type, aircraft type, component, end user, and geography. By system type, the market is categorized into passenger oxygen systems and crew oxygen systems. By aircraft type, the segmentation includes commercial, military, and general aviation platforms. By component, the market encompasses oxygen storage subsystems, oxygen delivery subsystems, and oxygen masks and dispensing units. By end-user, the market is segmented into linefit installations and retrofit programs. The report also provides market size and forecasts for passenger emergency oxygen deployment systems in leading countries worldwide. For each segment, the market size and forecast are provided in terms of value (USD).

| Passenger Oxygen System |

| Crew Oxygen System |

| Commercial Aircraft |

| Military Aircraft |

| General Aviation Aircraft |

| Oxygen Storage Sub-system |

| Oxygen Delivery Sub-system |

| Oxygen Masks and Dispensing Units |

| Linefit |

| Retrofit |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By System | Passenger Oxygen System | ||

| Crew Oxygen System | |||

| By Aircraft Type | Commercial Aircraft | ||

| Military Aircraft | |||

| General Aviation Aircraft | |||

| By Component | Oxygen Storage Sub-system | ||

| Oxygen Delivery Sub-system | |||

| Oxygen Masks and Dispensing Units | |||

| By End-User | Linefit | ||

| Retrofit | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the passenger emergency oxygen deployment systems market in 2026?

The passenger emergency oxygen deployment systems market is valued at USD 2.83 billion in 2026 and is projected to reach USD 3.74 billion by 2031, indicating a 5.77% CAGR.

Which system type commands the most revenue?

Passenger oxygen solutions held 68.12% of 2025 revenue, reflecting the high number of masks and generators installed in cabins.

Which region will record the fastest growth to 2031?

Asia-Pacific is forecast to advance at a 6.08% CAGR, underpinned by more than 2,800 new aircraft deliveries across India and South Asia.

What is driving the surge in retrofit demand?

Widebody cabin upgrades by Gulf carriers plus North American fleets reaching the 15-year generator life limit are accelerating retrofit activity.

Why has commercial OBOGS uptake been slow?

Hundreds of unexplained physiological events in military platforms have prompted regulators to impose extended certification and cybersecurity reviews on pressure-swing-adsorption technology.

Which component category is growing quickest?

Oxygen delivery sub-systems, led by pulse-demand regulators that cut system weight by 450 lb, are on track for a 5.99% CAGR through 2031.

Page last updated on: