Commercial Aircraft Evacuation System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

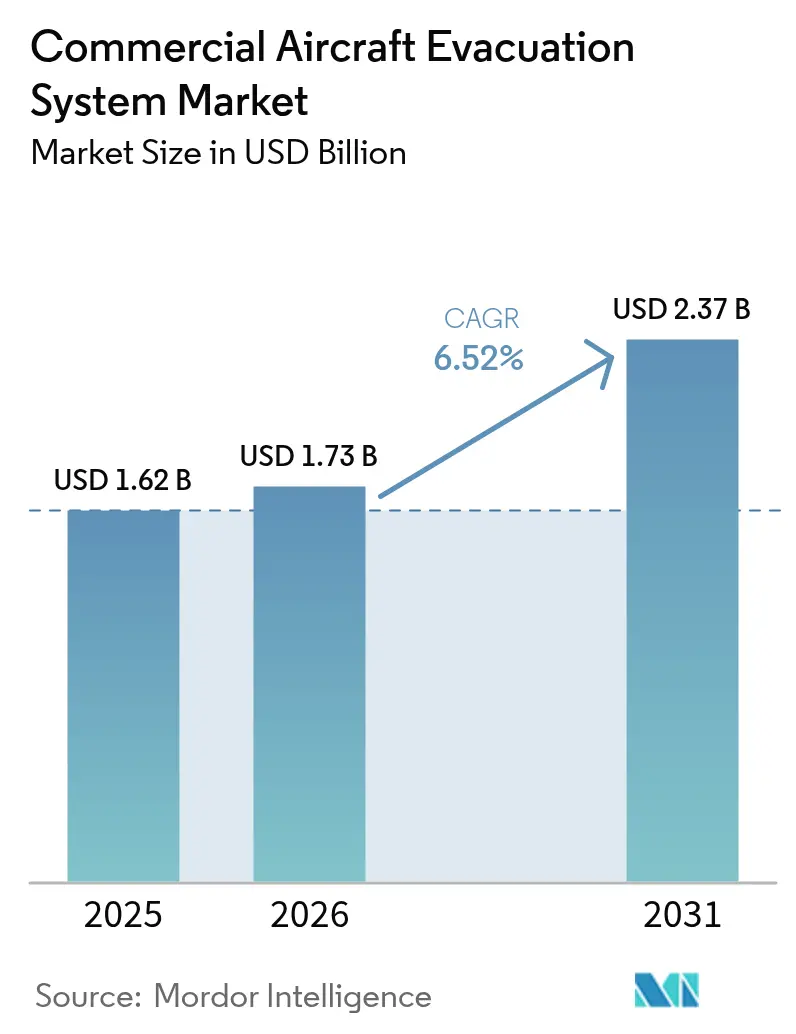

| Market Size (2026) | USD 1.73 Billion |

| Market Size (2031) | USD 2.37 Billion |

| Growth Rate (2026 - 2031) | 6.52% CAGR |

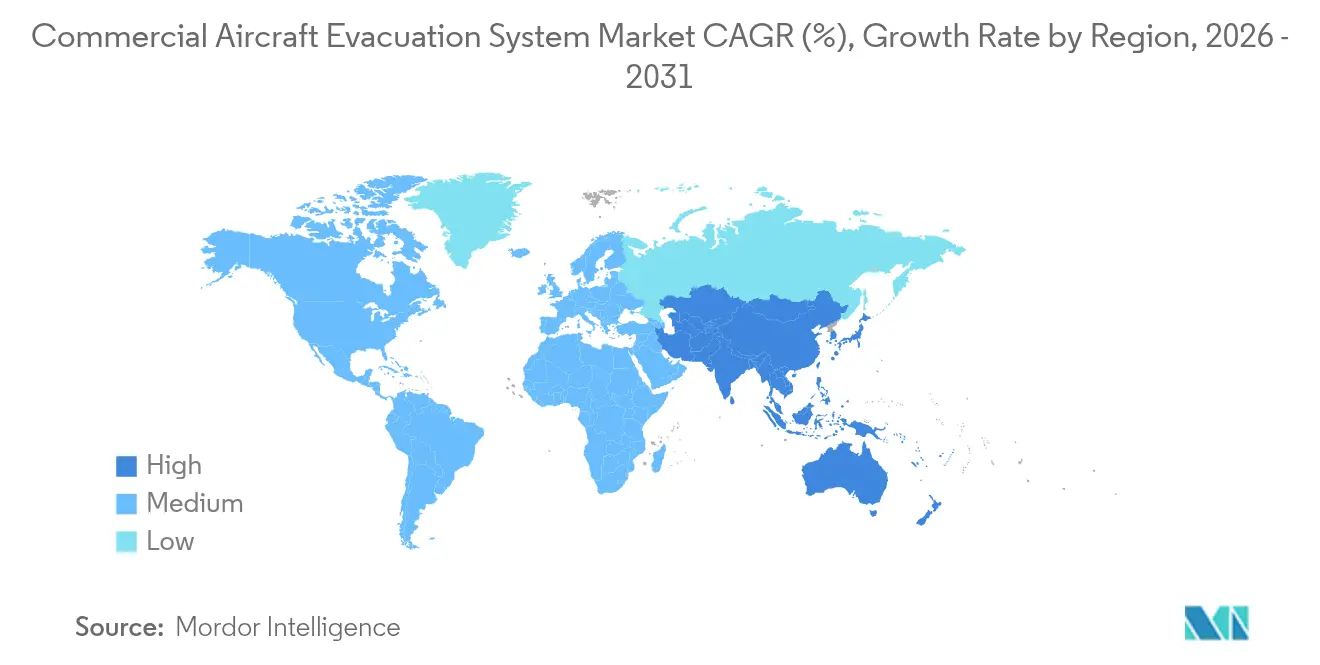

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Commercial Aircraft Evacuation System Market Analysis by Mordor Intelligence

The commercial aircraft evacuation systems market size was valued at USD 1.62 billion in 2025 and estimated to grow from USD 1.73 billion in 2026 to reach USD 2.37 billion by 2031, at a CAGR of 6.52% during the forecast period (2026-2031). Growth is propelled by rapid fleet renewal, stringent post-2024 FAA/EASA testing protocols, and widespread adoption of battery-powered smart-sensor slides that cut unscheduled maintenance events. Escalating titanium and specialty-steel costs compress supplier margins, yet spur material-efficiency innovations that reinforce competitive barriers. Asia-Pacific leads demand creation through low-cost-carrier (LCC) expansion and a projected 19,500 new-aircraft intake by 2043, equal to 46% of global deliveries. Concurrently, North America commands the most significant regional foothold owing to mature MRO infrastructure, long-standing OEM supply contracts, and accelerated slide retrofits that align mixed-reality crew-training mandates.

Key Report Takeaways

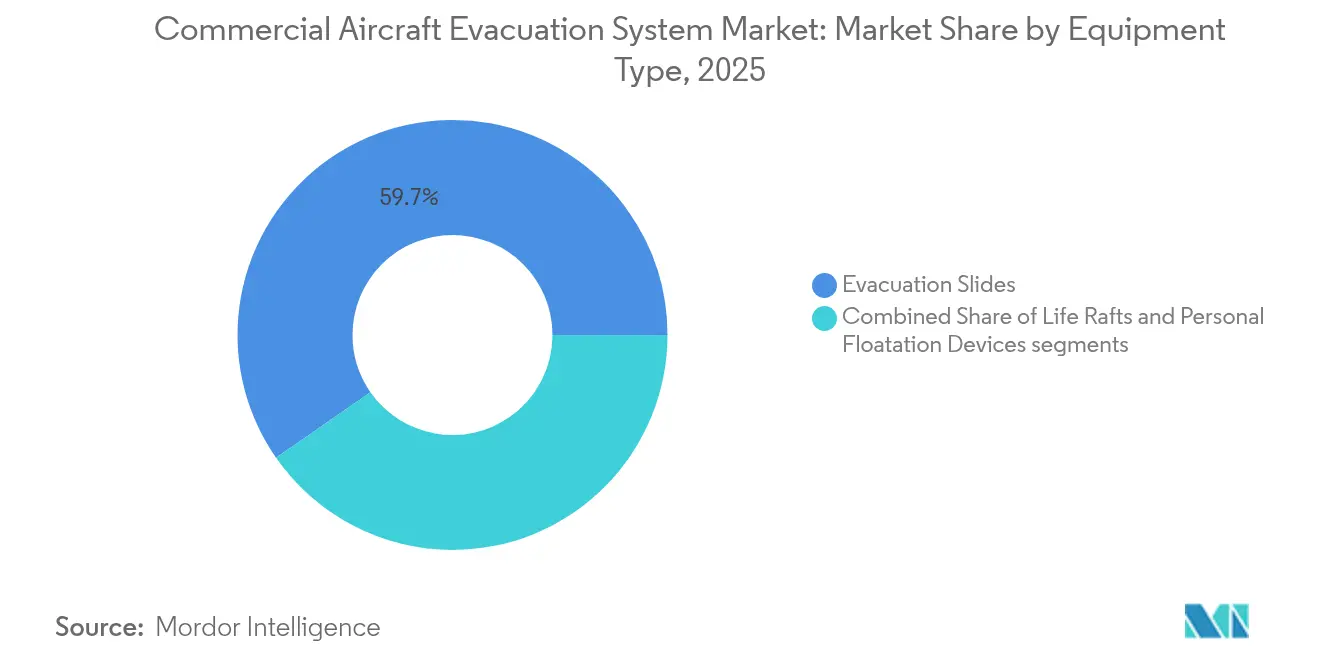

- By equipment type, evacuation slides captured 59.68% of the commercial aircraft evacuation systems market share in 2025 and are projected to expand at a 6.89% CAGR to 2031.

- By aircraft type, regional jets accounted for the fastest 7.12% CAGR within the commercial aircraft evacuation systems market size over 2026-2031, while narrowbodies held 48.25% value share in 2025.

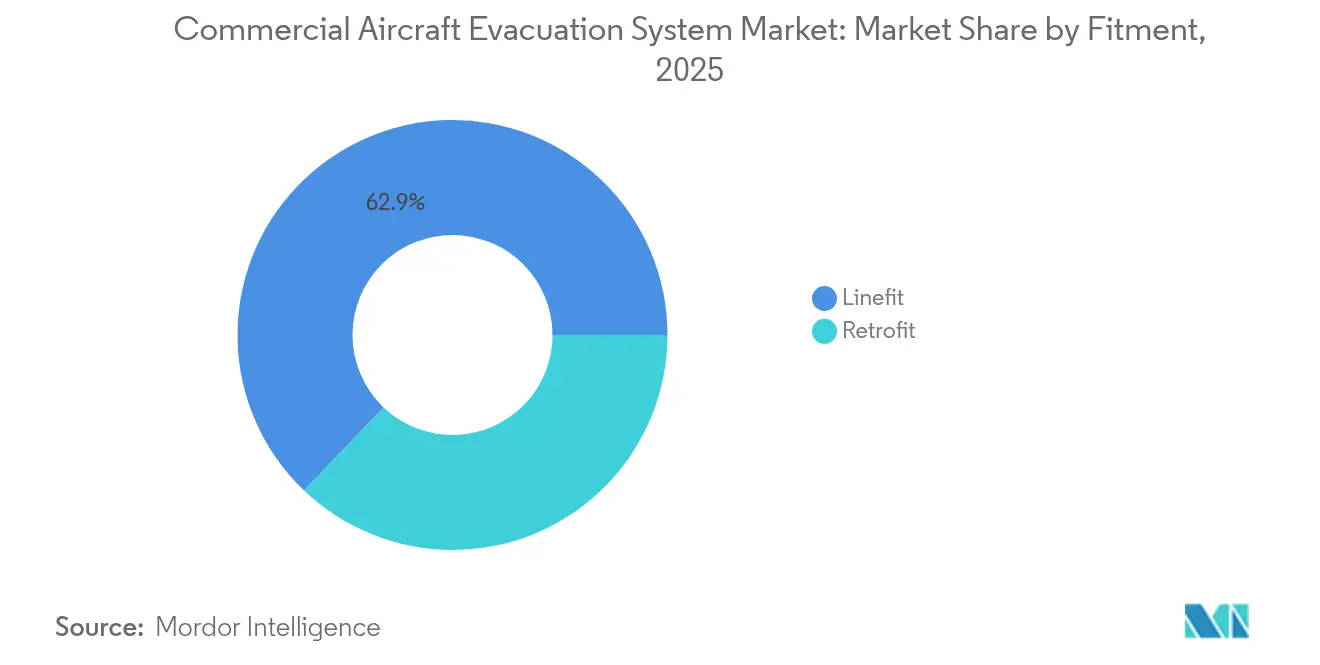

- By fitment, linefit installations dominated with 62.88% of 2025 revenue, whereas retrofit applications are forecasted to register a higher 7.05% CAGR through 2031.

- By geography, Asia-Pacific is set to log the quickest 7.23% CAGR, whereas North America retained a 29.55% revenue share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Commercial Aircraft Evacuation System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fleet renewal cycles across narrowbody and widebody aircraft programs | +1.8% | Global, focus on North America and Asia-Pacific | Long term (≥ 4 years) |

| Stricter FAA and EASA evacuation testing standards post-2024 | +1.2% | Global, mainly North America and Europe | Medium term (2-4 years) |

| Growing MRO demand for evacuation slide overhauls in aging aircraft | +0.9% | North America and Europe, spreading to Asia-Pacific | Medium term (2-4 years) |

| Expansion of low-cost carriers (LCCs) fueling new evacuation system installations | +1.1% | Asia-Pacific core, spill-over to South America and MEA | Long term (≥ 4 years) |

| Integration of battery powered smart sensor evacuation slides reducing maintenance requirements | +0.7% | Global, early adoption in North America and Europe | Long term (≥ 4 years) |

| Adoption of mixed-reality crew training mandates to enhance evacuation readiness | +0.4% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fleet renewal cycles accelerate equipment-replacement demand

Airlines worldwide are retiring legacy airframes in favor of fuel-efficient A320neo and B737 MAX variants, each delivered with state-of-the-art evacuation slides engineered for high-density cabins. Safran recorded a 35% year-over-year jump in A320 slide shipments during 1H 2024, underscoring OEM pull-through. Replacement also stimulates aftermarket retrofits because operators strive for fleetwide equipment uniformity to ease crew training. Higher-seat-count layouts increase required exit-rate performance, pushing suppliers to integrate lightweight fabrics and rapid-inflation valves. Regulatory compliance timing further nudges carriers to retrofit ahead of certification deadlines rather than absorb disruptive mid-life upgrades.

Post-2024 regulatory standards reshape testing protocols

Section 365 of the 2024 FAA Reauthorization Act orders real-world evacuation studies covering smoke, low-visibility, and baggage interference variables.[1]Federal Aviation Administration, “FAA Reauthorization Act 2024,” faa.gov EASA mirrored the shift, compelling slide makers to validate performance at extreme temperature and structural-damage thresholds. The JAL A350 incident revealed behavior-driven delays and spurred demands for crew-coordination data during certification. Compliance costs elongate product-development cycles yet confer scale advantages on incumbents fluent in multi-jurisdictional approval. Suppliers capable of digital-twin simulation and mixed-reality testing gain early-mover credibility, jointly elevating overall market standards.

MRO demand intensifies for aging-fleet overhauls

Oliver Wyman projects global aviation MRO spend rising to USD 124 billion by 2034, with evacuation slides occupying a mandatory overhaul niche. Material fatigue and fabric porosity drive recurrent replacements every 10 to 12 years, creating annuity-like revenue streams. Survitec leverages over 400 service locations to capture slide refurbishment contracts, citing rising work scopes across 2025 booking pipelines. Bottlenecks emerge because FAA-approved facilities are scarce and technician certification demands are stringent. Longer lead times elevate operator costs, prompting airlines to schedule proactive overhauls during heavy checks.

Low-cost-carrier expansion drives installation volume

Asia-Pacific LCCs such as IndiGo and Scoot sustain high fleet-growth trajectories, prioritizing rapid turnarounds and seat-dense cabins. Evacuation systems must balance minimal maintenance demands with enhanced exit speed to meet certification. Embraer’s forecast of 10,500 sub-150-seat aircraft through 2044 amplifies the regional jet opportunity for evacuation slide providers. Used-aircraft acquisitions by LCCs unlock retrofit contracts as operators harmonize safety equipment and satisfy insurer requirements. Digital monitoring also resonates with cost-sensitive carriers eager to limit unscheduled slide removals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long-term OEM evacuation system supply contracts limiting new entrants | -0.8% | Global, notably North America and Europe | Long term (≥ 4 years) |

| Persistent cabin baggage evacuation delays increasing liability and safety risks | -0.6% | Global, higher in North America and Europe | Medium term (2-4 years) |

| Rising raw material costs squeezing manufacturer margins | -1.1% | Global, peaking in North America and Europe | Short term (≤ 2 years) |

| Limited FAA-approved independent MRO capacity constraining aftermarket growth | -0.7% | North America, extending worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Long-term OEM contracts create market-entry barriers

Collins Aerospace’s 50-year distribution pact with Satair typifies enduring supply agreements that govern airframe life cycles.[2]Collins Aerospace, “Satair and Collins extend distribution agreement,” collinsaerospace.com Airbus and Boeing lean on legacy partners to minimize certification risk, confining opportunities for newcomers who face USD 10 million-plus platform-qualification costs. Safran’s 2024 divestiture of its North American actuation unit to Woodward demonstrates portfolio reshaping as incumbents consolidate rather than yield share. Airlines prefer vendors with global spares networks and proven safety pedigrees, cementing entry hurdles. Consequently, only niche play remains for start-ups specializing in lightweight textiles or modular raft canisters.

Persistent cabin-baggage delays elevate liability risk

Passenger non-compliance in retaining carry-ons during emergencies slowed recent evacuations, prompting insurers to question risk-pricing models. Regulators study design tweaks such as overhead-bin locking mechanisms and illuminated slide-path signage to mitigate retrieval attempts. Operators confront training challenges and public-awareness campaigns, but behavioral unpredictability persists, occasionally offsetting system-design gains. Liability exposure can escalate post-event settlements, nudging carriers to adopt stricter boarding-bag policies that indirectly impact time-to-slide deployment metrics, tempering market optimism.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Slides Dominate Through Innovation Integration

Evacuation slides generated the largest 59.68% market share of commercial aircraft evacuation systems in 2025 and propelled a 6.89% CAGR. Slides couple lightweight polyurethane fabrics with dual-lane architecture to improve exit-rate efficiency; embedded IoT nodes transmit pressure, temperature, and deployment-readiness status to airline dashboards. Real-time health monitoring underpins condition-based maintenance, slashing unscheduled removals by more than 25% on early adopter fleets.

Life rafts are the second-largest contributing line, buoyed by EASA’s tightened ditching-survivability criteria for extended diversion routes. Survitec’s 152-person Seahaven raft showcases advances in compact valise form factors and quadruple-redundant CO2 inflation valves. Although the smallest in revenue, personal flotation devices register steady renewals given heightened passenger-capacity metrics and regulatory calls for adult-infant size standardization. Growth headwinds arise from weight-reduction pressures, pushing suppliers to adopt ultra-high-molecular-weight polyethylene (UHNWP) fabrics. Yet slides maintain clear dominance through 2031, due to mandatory fitment on every exit door and competitive tech roadmaps.

By Aircraft Type: Regional Jets Accelerate Growth Trajectory

Regional jets platforms are forecasted to advance at a 7.12% CAGR through 2031, surpassing narrowbody and widebody peers. Embraer E-Jet E2 variants and De Havilland Dash-8 replacements underpin the surge, requiring compact slide geometries compatible with lower sill heights. Slide suppliers engineer inflation trajectories that avoid ground impact while achieving 1.5-second deployment.

Narrowbodies continue to anchor total demand, with 48.25% 2025 market share, primarily via A320neo and B737 MAX production pipelines. LCC seating densities magnify exit-rate design margins, compelling two-lane slide retrofits on forward doors. Widebodies represent a mature, slower-growing niche, though higher passenger counts and over-water segments sustain steady raft and PFD demand. Suppliers differentiate through low-drag slide-pack bay doors that curtail maintenance-induced fuel burn penalties, essential for long-haul economics.

By Fitment: Retrofit Gains Momentum Through Modernization

Linefit deliveries held 62.88% share of 2025 revenue, yet retrofit demand is climbing at a 7.05% CAGR as airlines synchronize mixed fleets under unified safety-equipment standards. Retrofit projects leverage modular pack-in-pack slide designs to avoid door-cutting and reduce out-of-service days. Lufthansa Aviation Training’s VR simulation upgrade created parallel retrofits for sensor-enabled slides to feed data into training analytics.

Smart-technology-ready kits integrate plug-and-play battery modules and BLE beacons, allowing incremental upgrade paths without wholesale slide replacement. FAA-approved Supplemental Type Certificates (STCs) streamline retrofit adoption on late-model NG fleets, though backlog persists due to limited MRO dock slots. Operators justify investment through up to 30% savings in unscheduled maintenance and enhanced insurance ratings tied to sensor-based compliance logs.

Geography Analysis

North America comprised 29.55% of the 2025 value, driven by entrenched aerospace OEM clusters in Seattle, Wichita, and Montréal that expedite certification cycles and sustain proximity supply chains. The region also houses the densest network of Part 145 slide-repair stations, cutting turnaround times and fortifying aftermarket stability. FAA leadership in rule-making shapes global benchmarks, giving US suppliers early technical foresight.

Asia-Pacific is forecasted to be the fastest climber with a 7.23% CAGR, propelled by Airbus’s 19,500 aircraft delivery outlook and China’s 5.7% annual RPK growth. Indian carriers logged double-digit traffic rebounds, ordering next-generation narrowbodies outfitted with predictive-maintenance slides. Regional governments court local assembly lines, pressing suppliers to establish joint ventures in Tianjin and Hyderabad that comply with offset policies yet retain IP control.

Europe remains technologically influential through EASA’s rigorous human-factor testing and composite-material programs originating in Toulouse and Hamburg. Brexit-related customs frictions temporarily hampered cross-Channel slide sub-component flows, though dual-site warehousing alleviated delays. Middle East and Africa, while smaller, witness steady uptake among Gulf mega-carriers expanding widebody fleets; however, political instability tempers sub-Saharan activity. South America benefits from LCC penetration in Brazil and Argentina, but macro-economic volatility caps fleet-renewal cadence.

Competitive Landscape

The commercial aircraft evacuation systems market is highly concentrated, with a handful of multinationals controlling core technology and certification portfolios. Safran and Collins Aerospace headline the tier-one cohort, blending slide, raft, and actuation product lines to cross-sell within broader interiors packages. Safran’s acquisition of Collins’s flight-control businesses deepens systems integration and unlocks cabin-safety joint solutions.

Mid-tier specialists like Survitec Group Limited carve out raft-centric niches leveraged by oil-rig helicopter and military segments, yet increasingly partner with tier-one firms for commercial jet penetration. Intellectual-property filings, such as Airbus’s US9248918B2 on acceleration-sensor fault detection, signal intensifying convergence between avionics health-monitoring and evacuation systems. Digital aftermarket platforms offering serialized component tracking appeal to airlines prioritizing on-time performance metrics.

Supply-chain volatility remains the foremost competitive threat as titanium and high-performance textile bottlenecks necessitate dual-source strategies. Players with vertically integrated fabric weaving and gas-inflation canister production gain resilience and pricing leverage. Overall, competition tilts toward those able to package smart sensors, predictive analytics, and global MRO services into unified lifetime-value propositions.

Commercial Aircraft Evacuation System Industry Leaders

Survitec Group Limited

Trelleborg AB

Collins Aerospace (RTX Corporation)

Safran SA

EAM Worldwide

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2023: HAECO Group entered into an agreement with Safran Aerosystems to maintain the evacuation slide on the C919 aircraft. As per the terms of the agreement, HAECO's Component Repair and Overhaul (CRO) division would be authorized to develop the capability of the C919 evacuation slide in Asia-Pacific. As part of the collaboration, Safran Aerosystems will extend its support to HAECO by assisting in the development of HAECO's repair capability related to the product, including the supply of spare parts, the sale of tooling and test equipment, as well as the training and technical documentation necessary to perform maintenance services for the C919 evacuation slides.

- June 2022: Air Partner partnered with Kenyon International Emergency Services, a US-based disaster management company that provides comprehensive emergency response services. The collaboration focuses on developing and implementing customized air evacuation plans to support individuals during disasters.

- January 2022: Collins Aerospace secured a support agreement with Spairliners for evacuation slides, which includes testing, inspection, repair, modification, and replacement services for evacuation systems.

Global Commercial Aircraft Evacuation System Market Report Scope

The evacuation system comprises evacuation equipment that will aid in the emergency evacuation of passengers from an aircraft either on the ground or in water and remain afloat in the event of an over-water deplaning. The market study includes evacuation slides, life rafts, and personal floatation devices (such as life vests, inflatable armbands, and other components for passenger safety).

The commercial aircraft evacuation system market is segmented by equipment type, aircraft type, and geography. By Equipment type, the market is segmented into evacuation slides, life rafts, and personal floatation devices. By aircraft type, the market is segmented into narrow-body, wide-body, and regional jets. The report also covers the market sizes and forecasts for the commercial aircraft evacuation system market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Evacuation Slides |

| Life Rafts |

| Personal Floatation Devices |

| Narrowbody |

| Widebody |

| Regional Jets |

| Linefit |

| Retrofit |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Equipment Type | Evacuation Slides | ||

| Life Rafts | |||

| Personal Floatation Devices | |||

| By Aircraft Type | Narrowbody | ||

| Widebody | |||

| Regional Jets | |||

| By Fitment | Linefit | ||

| Retrofit | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the commercial aircraft evacuation systems market in 2026?

The commercial aircraft evacuation systems market size stands at USD 1.73 billion in 2026 and is projected to reach USD 2.37 billion by 2031, advancing at a 6.52% CAGR.

Which region drives the fastest demand growth for evacuation systems?

Asia-Pacific is expected to record a 7.23% CAGR from 2026-2031, buoyed by LCC expansion and 19,500 forecast aircraft deliveries.

What equipment segment leads revenue share today?

Evacuation slides dominate with 59.68% share in 2025 and benefit from 6.89% forecast CAGR.

Why are retrofit installations accelerating?

Aging fleet overhauls, mixed-reality training mandates, and the desire to standardize equipment across diverse aircraft are pushing retrofit demand at a 7.05% CAGR.

How do smart-sensor slides improve airline economics?

Continuous health monitoring reduces unscheduled removals and allows predictive maintenance, cutting slide-related operational disruptions by more than 25% on early adopter fleets.

What is the main barrier for new evacuation-system entrants?

Long-term OEM supply contracts and high certification costs—often exceeding USD 10 million per aircraft platform—present formidable hurdles for newcomers.

Page last updated on: