Paraffin Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 6.13 Billion |

| Market Size (2031) | USD 7.62 Billion |

| Growth Rate (2026 - 2031) | 4.45% CAGR |

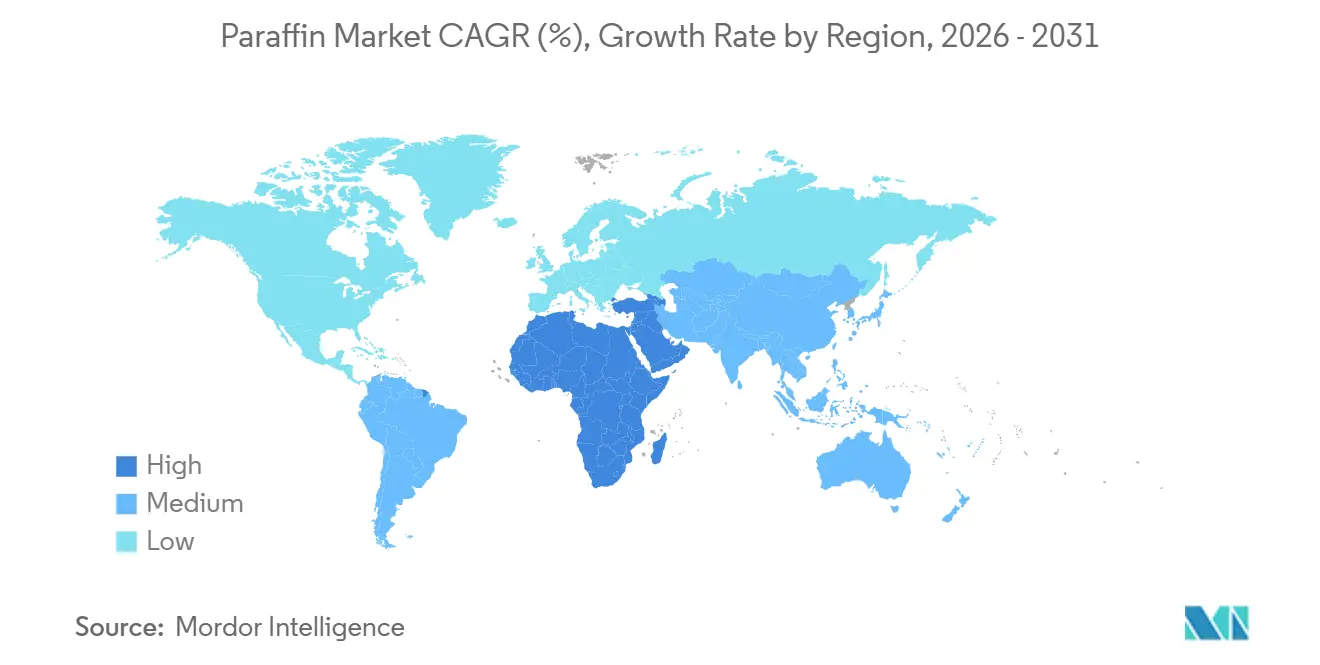

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Paraffin Market Analysis by Mordor Intelligence

The Paraffin Market size is estimated at USD 6.13 billion in 2026, and is expected to reach USD 7.62 billion by 2031, at a CAGR of 4.45% during the forecast period (2026-2031). Demand continues to pivot away from commodity candle wax toward higher-margin liquid and Fischer–Tropsch (FT) grades, even as candles and packaging remain volume anchors. Liquid paraffin is gaining traction on the back of pharmaceutical and cosmetic formulations that value its regulatory clearance and long shelf life. Premium FT waxes capture price uplifts thanks to near-zero sulfur and aromatic content, while precision metal-casting patterns secure margins two to three times higher than bulk wax. Concurrently, bio-based substitutes are gaining visibility, and trade remedies are reshaping regional supply chains, creating a complex growth landscape for the paraffin market.

Key Report Takeaways

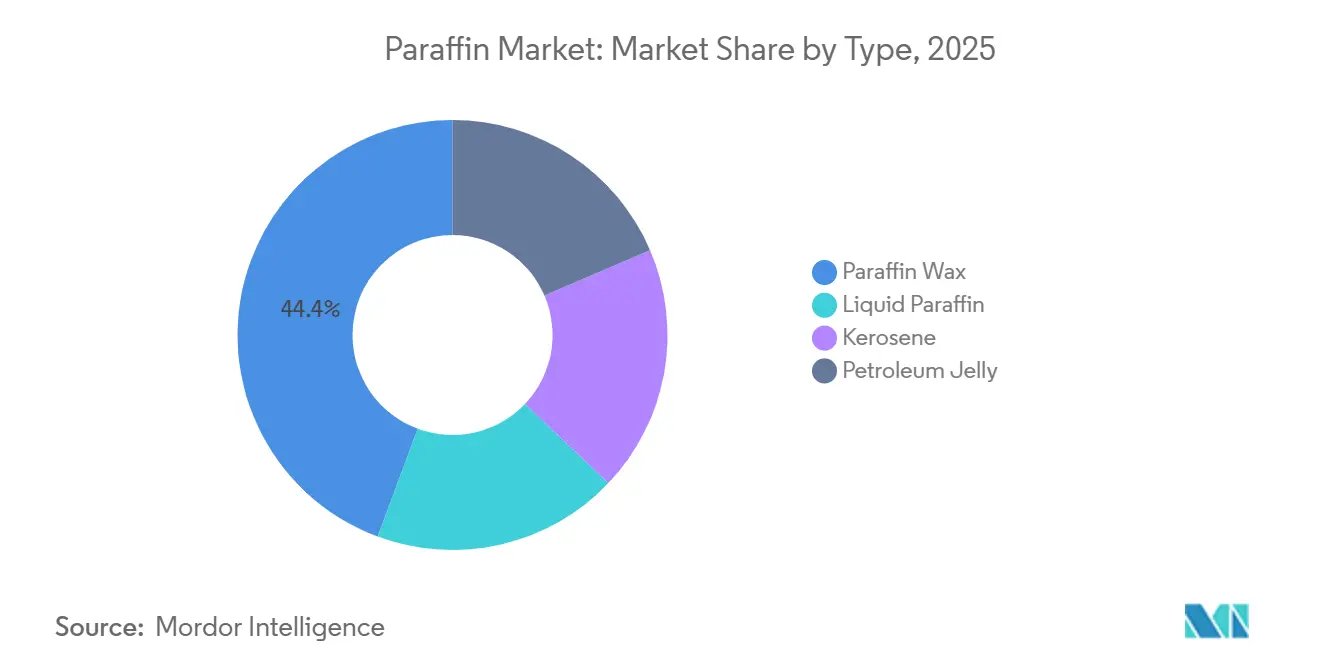

- By type, paraffin wax led with 44.36% of paraffin market share in 2025, while liquid paraffin is expanding at a 5.42% CAGR through 2031.

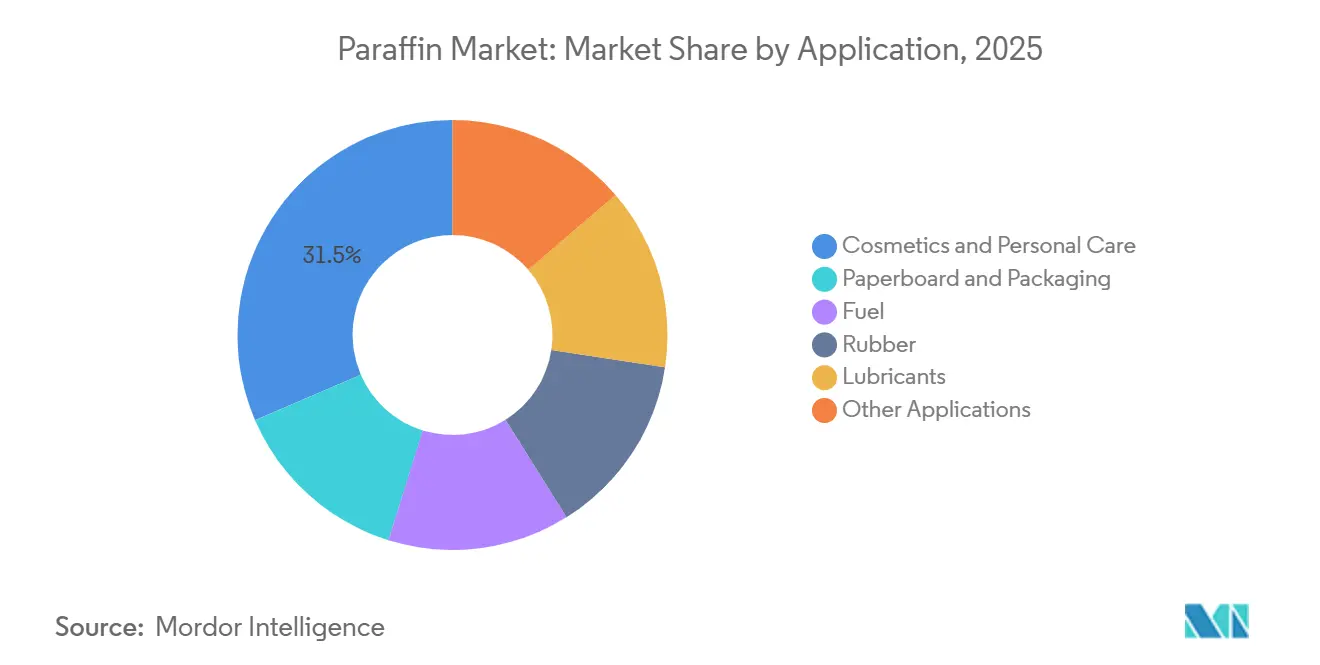

- By application, cosmetics and personal care held 31.48% of the paraffin market share in 2025, whereas paperboard and packaging are advancing at a 5.54% CAGR to 2031.

- By geography, Asia-Pacific accounted for 46.27% of the paraffin market share in 2025, and the Middle-East and Africa region is forecast to grow at a 5.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Paraffin Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand from candle manufacturing | +1.2% | North America, Europe, Asia-Pacific | Medium term (2–4 years) |

| Expansion of personal-care and cosmetics production | +1.5% | Asia-Pacific core, spillover to Middle East and Africa | Long term (≥ 4 years) |

| Growth of e-commerce-led flexible packaging | +1.3% | Global | Short term (≤ 2 years) |

| Commercialisation of ultra-pure FT-based grades | +0.8% | Middle East, North America, Europe | Long term (≥ 4 years) |

| Adoption of paraffin patterns in precision casting | +0.6% | North America, Europe, Asia-Pacific | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Demand from Candle Manufacturing

Paraffin retains a significant share of raw-material volume in the global candle sector despite mounting competition from soy and beeswax alternatives[1]National Candle Association, “Industry Statistics 2024,” candles.org. Mass-market brands favor paraffin because of its scent throw consistency, lower melting point variance, and price advantage over plant waxes. Feedstock costs account for a significant portion of total candle unit economics, so producers that lock in slack-wax contracts with integrated refiners can protect margins during crude swings. Sustainability positioning now shapes premium segments, yet value-tier and seasonal lines in North America and Europe still rely on commodity paraffin. Ongoing EU scrutiny of low-priced Chinese candles adds supply uncertainty, further motivating regional manufacturers to secure long-term wax contracts.

Expansion of Personal-Care and Cosmetics Production, Especially in Asia

Asia-Pacific’s expanding middle class underpins liquid paraffin consumption in moisturizers, lip balms, and hair-care products. BASF ramped emollient capacity in Shanghai to align with this trajectory. Liquid paraffin, listed as “paraffinum liquidum,” satisfies EU Regulation 1223/2009 and FDA 21 CFR 172.880, giving multinational brands the compliance confidence to scale formulations[2]U.S. Food and Drug Administration, “21 CFR 172.880 – Petrolatum,” fda.gov . Although clean-beauty narratives spur trials of jojoba and shea butter, liquid paraffin’s cost-effectiveness and microbiological stability keep it embedded in mass-market SKUs. Established suppliers with vertically integrated refineries benefit from REACH rules that demand full refining traces, limiting opportunistic imports.

Growth of E-Commerce-Led Flexible Packaging

Surging parcel volumes elevate demand for paraffin-coated paperboard that resists humidity and rough handling. Wax coatings offer moisture and grease barriers at lower capital intensity than polyethylene lamination, especially for custom runs. Online grocery and meal-kit growth amplifies consumption of FDA-compliant wax liners for frozen shipments. Bio-based coatings from rice bran and sunflower waxes are emerging, yet converters report paraffin lines operate faster owing to favorable viscosity profiles. As e-commerce deepens in Asia-Pacific and Latin America, localized shortages may arise where refining infrastructure is scarce, strengthening pricing power for regional paraffin market suppliers.

Commercialisation of Ultra-Pure FT-Based Paraffin Grades

Shell and Sasol’s Oryx GTL venture in Qatar delivers FT paraffins with negligible sulfur and aromatics, enabling pharmaceutical ointments and food-contact coatings that fetch premiums. ExxonMobil’s Resid Upgrade in Singapore widens high-purity supply for Asian customers starting 2025. FT technology requires multibillion-dollar capital outlays and proprietary cobalt or iron catalysts, limiting competitive entry to supermajors and state-owned enterprises. Regulators in Europe and North America set strict thresholds for polycyclic aromatic hydrocarbons, accelerating substitution from conventional slack wax to FT alternatives. As India and China tighten excipient standards, demand growth for ultra-pure grades is expected to outpace the overall paraffin market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid development of bio-based wax substitutes | -0.9% | North America, Europe | Medium term (2–4 years) |

| Volatility in crude-oil-derived feedstock costs | -0.7% | Global | Short term (≤ 2 years) |

| EU anti-dumping duties curbing Chinese candle exports | -0.5% | Europe, China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Development of Bio-Based Wax Substitutes

Cargill’s NatureWax line supplies soy, coconut, palm, and rapeseed waxes that slot into container candles and wax melts without major process tweaks. Iowa State University trials show soy blends can match paraffin’s burn time, shrinking the historical performance gap. California Proposition 65 warnings on petroleum-derived candles and EU circular-economy goals steer procurement toward renewables. Soy-wax costs have fallen since 2024 on crushing-efficiency gains, eroding paraffin’s price lead. Scaling constraints remain, as agri-feedstocks must balance food, biodiesel, and wax demand, but commodity candle-wax producers still face margin pressure.

Volatility in Crude-Oil-Derived Feedstock Costs

Paraffin wax output hinges on refinery slate decisions that respond to crude prices. In November 2025, Brent crude prices were influenced by waning demand from China and an uptick in supply from non-OPEC sources. Slack wax often diverts to fuel blending when refining margins narrow, triggering sporadic shortages that squeeze independent processors. Integrated majors such as ExxonMobil and Shell mitigate volatility through internal feedstock flows, but spot buyers face erratic pricing. As the energy transition trims conventional refining capacity over the decade, North American and European buyers could see longer lead times and higher freight costs, adding risk to the paraffin market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Specialty Grades Outpace Commodity Wax

Paraffin wax controlled 44.36% of the paraffin market share in 2025, anchored by candle manufacturing and packaging coatings. Growth for the segment lags the paraffin market size expansion because bio-based options are chipping away at commodity volumes. Liquid paraffin is advancing at a 5.42% CAGR, with formulators rewarding its compliance under FDA 21 CFR 172.880 and EU Regulation 1223/2009. Ultra-pure FT waxes from the Oryx GTL plant command premiums and align with pharmaceutical and food-contact applications that demand near-zero sulfur. Petroleum jelly, dominated by Unilever’s Vaseline, remains a niche yet steady sub-segment. Kerosene stays tangential to the paraffin market, as aviation fuel dynamics drive most demand rather than wax extraction. The contrast in growth rates shows volume gravitating toward high-purity, application-specific grades that justify premiums, while commodity paraffin wax endures gradual erosion.

Widening specialty supply further shifts the landscape. ExxonMobil’s Prowaxx line spans from fully refined to slack waxes, monetizing its integrated value chain. REACH registration in Europe limits market entry to refiners with full feedstock traceability. FT output requires a multibillion-dollar investment, stalling new capacity outside state-backed or supermajor ventures. These structural hurdles reinforce a bifurcated paraffin market in which specialty producers grow profitability even if commodity volumes flatten.

By Application: Cosmetics Lead, Packaging Accelerates

Cosmetics and personal care generated 31.48% of paraffin market revenue in 2025. Liquid paraffin’s occlusive properties make it a staple in moisturizers, lip balms, and hair products, particularly across Asia’s expanding middle class. Regulatory clarity under FDA and EU rules shields incumbent suppliers and deters non-compliant imports. Paperboard and packaging are the fastest-growing applications at a 5.54% CAGR, lifted by e-commerce logistics that require moisture-resistant liners and corrugated boxes. Wax coatings enable quick line speeds and cost savings over polymer laminates, giving paraffin advantages in high-volume operations. Fuel applications are mature, while rubber manufacturing still uses paraffin to improve processing flow, but faces competition from synthetic oils.

Investment casting rounds out the smaller yet lucrative applications. Specialty wax blends used for turbine blades and orthopedic implants command two-to-three-times the margins of candle wax due to strict ash and thermal-expansion limits. Lubricants and cable-filling compounds add incremental demand, valuing paraffin’s stability and insulating attributes. The application mix demonstrates a paraffin market split: legacy high-volume uses grow modestly, whereas technical-grade niches post stronger gains that enhance overall profitability.

Geography Analysis

Asia-Pacific held 46.27% of the paraffin market revenue in 2025, underpinned by China’s refining scale and India’s rising capacity. In the first half of 2024, Sinopec’s crude throughput supported regional wax availability; however, changes in EU VAT have restricted its ability to underprice exports. India's refining system produces paraffin wax in Gujarat, Panipat, and Barauni. Yet due to limited domestic upgrading, the country still relies on specialty imports. Japan’s ENEOS channels high-purity waxes to electronics and pharmaceutical manufacturers that demand consistent quality. South Korea and ASEAN nations are emerging as alternative hubs as Chinese companies reroute production to avoid potential EU duties, reshaping regional supply networks.

The Middle East and Africa paraffin market is growing at a 5.23% CAGR. Saudi Arabia’s downstream expansion, South Africa’s Sasol FT output, and abundant low-sulfur feedstock support competitive pricing. Shell and Sasol’s Oryx GTL complex in Qatar provides ultra-pure waxes that meet global pharmaceutical specifications. North America and Europe grow more slowly but boast higher per-capita consumption due to specialty applications that value quality and compliance. ExxonMobil’s Singapore and Rotterdam hydrocracker upgrades add Group II capacity, reinforcing the supply of high-purity waxes for both regions. South America, led by Brazil’s Petrobras, offers incremental growth linked to economic development, while Africa, beyond South Africa, focuses on exporting to Europe.

The geographic split illustrates a paraffin market in which volume growth concentrates in Asia-Pacific and the Middle East, whereas North America and Europe pursue profitability via specialty grades. Supply-chain complexity will intensify as trade policies evolve, making regional integration and logistics capabilities critical to value capture.

Competitive Landscape

The global paraffin market is moderately fragmented in nature. Bio-based suppliers are eroding commodity candle-wax share, offering renewable inputs that attract sustainability-minded buyers. EU anti-dumping scrutiny of Chinese candles may push exporters to relocate, shifting wax demand toward ASEAN refiners. Strategic moves center on upgrading capacity and technology leadership. Smaller innovators focus on niche value. As specialty growth widens profit gaps, commodity suppliers will face consolidation pressure unless they move up the value chain.

Paraffin Industry Leaders

China Petroleum & Chemical Corporation (Sinopec)

Exxon Mobil Corporation

China National Petroleum Corporation (CNPC)

Shell plc

Sasol Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Farabi Petrochemicals opened its fourth integrated LAB plant in Yanbu, Saudi Arabia, bringing 120,000 t/yr of capacity and strengthening its global N-paraffin platform.

- April 2025: Repsol invested EUR 2.5 million (~USD 2.84 million) to add a paraffin pearl line at its Palencia specialty plant, boosting capacity 33% and adding jobs in candle, tire, and board feedstock supply chains.

Global Paraffin Market Report Scope

Paraffin is a white or colorless waxy material consisting of a mixture of saturated hydrocarbons, mainly produced as a product or byproduct from a petroleum refinery. It is mainly used in candle making, personal care products like petroleum jelly, and wax coating on papers, among others.

The paraffin market is segmented by type, application, and geography. By type, the market is segmented into paraffin wax, liquid paraffin, kerosene, and petroleum jelly. By application, the market is segmented into cosmetics and personal care, paperboard and packaging, fuel, rubber, lubricants, and other applications. The report also covers the market size and forecasts for the paraffin market in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Paraffin Wax |

| Liquid Paraffin |

| Kerosene |

| Petroleum Jelly |

| Cosmetics and Personal Care |

| Paperboard and Packaging |

| Fuel |

| Rubber |

| Lubricants |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | South Africa |

| Saudi Arabia | |

| Rest of Middle-East and Africa |

| By Type | Paraffin Wax | |

| Liquid Paraffin | ||

| Kerosene | ||

| Petroleum Jelly | ||

| By Application | Cosmetics and Personal Care | |

| Paperboard and Packaging | ||

| Fuel | ||

| Rubber | ||

| Lubricants | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | South Africa | |

| Saudi Arabia | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the paraffin market?

The paraffin market size is USD 6.13 billion in 2026, with a forecast to reach USD 7.62 billion by 2031, registering a CAGR of 4.45%.

Which segment is expanding fastest?

Liquid paraffin is growing at a 5.42% CAGR, the highest among type segments through 2031.

Which application holds the largest revenue share?

Cosmetics and personal care account for 31.48% of total revenue in 2025.

Which region contributes the most revenue?

Asia-Pacific generated 46.27% of global revenue in 2025.

What drives demand in e-commerce packaging?

Wax-coated paperboard provides low-cost moisture resistance essential for last-mile delivery and frozen-food logistics.

How are bio-based waxes impacting the market?

Soy, coconut, and other plant waxes are narrowing the cost gap with paraffin, pressuring commodity candle-wax margins, especially in North America and Europe.

Page last updated on: