Water-based Alkyd Coatings Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.04 Billion |

| Market Size (2031) | USD 5.20 Billion |

| Growth Rate (2026 - 2031) | 5.14% CAGR |

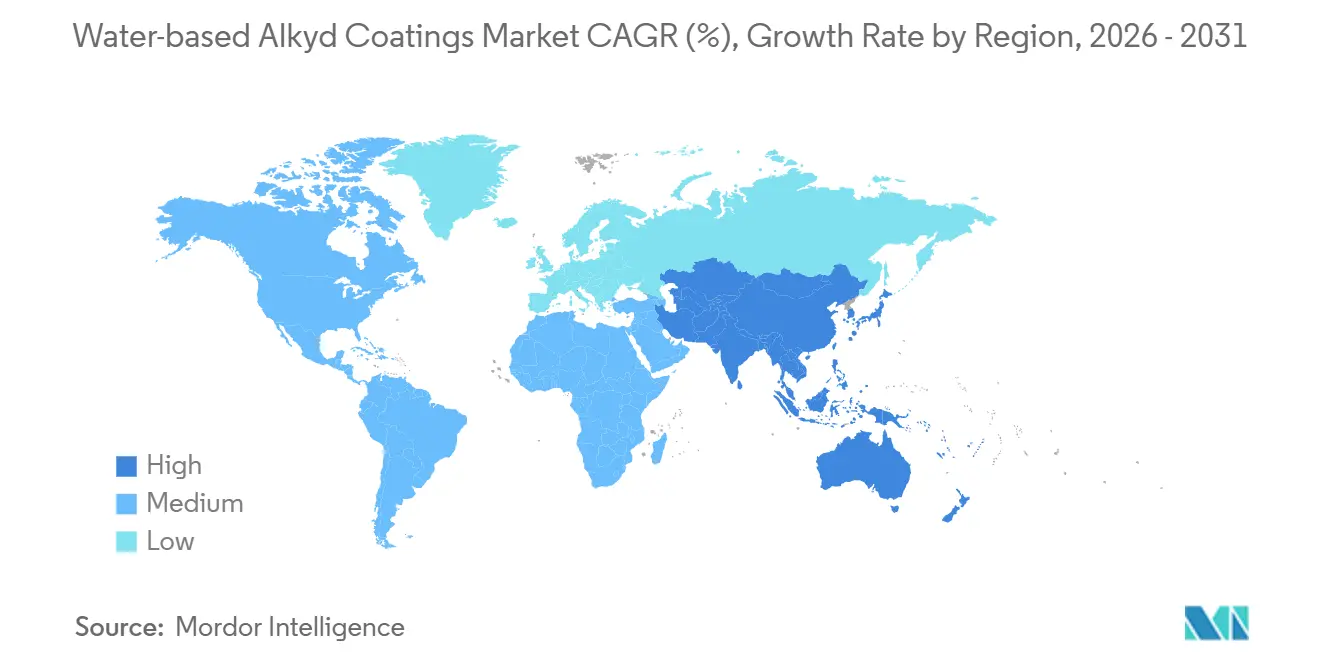

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

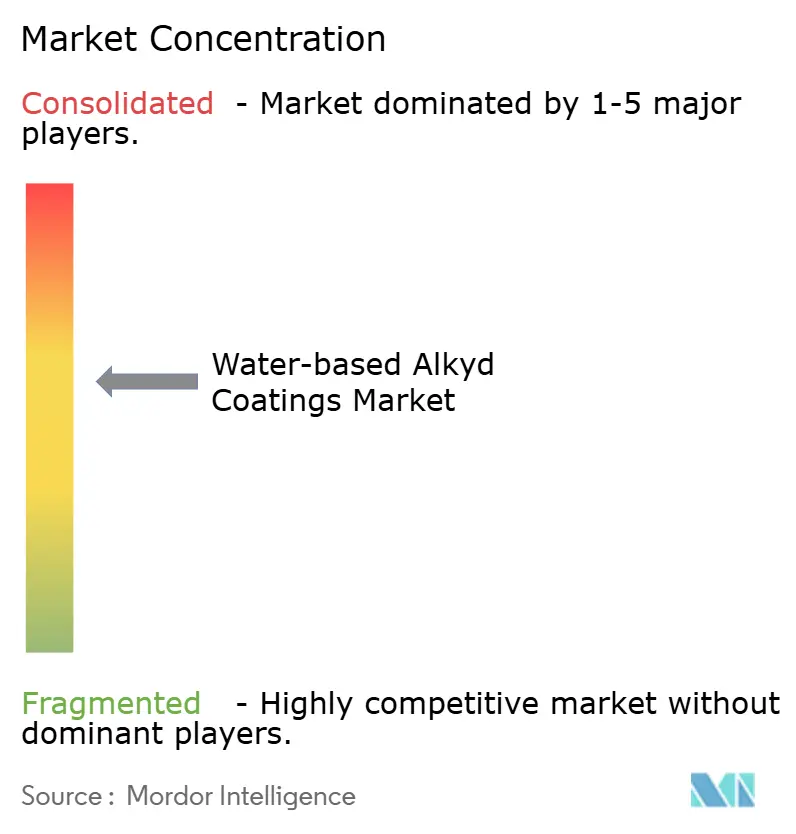

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Water-based Alkyd Coatings Market Analysis by Mordor Intelligence

The Water-based Alkyd Coatings Market size is expected to grow from USD 3.86 billion in 2025 to USD 4.04 billion in 2026 and is forecast to reach USD 5.20 billion by 2031 at a 5.14% CAGR over 2026-2031. Architectural coatings commanded 46.51% of 2025 demand as renovation activity recovered, while automotive refinish is advancing at 6.56% annually with collision-repair shops switching to water-borne basecoats to comply with tightening VOC (Volatile Organic Compound) rules in California, the European Union, and China. Construction and infrastructure end-users accounted for 52.16% of 2025 revenue, yet the automotive and transportation vertical is projected to expand 6.73% each year as OEMs (original equipment manufacturers) adopt low-emission primers. Asia-Pacific remains the market share leader at 41.32% in 2025, supported by China’s target for water-borne formulations to exceed 60% of architectural paint sales and by India’s and ASEAN’s megaproject pipelines. Capacity build-outs in North America, PPG’s USD 300 million investments across Tennessee, Ohio, and Mexico, and Sherwin-Williams’ USD 300 million expansion in North Carolina, signal confidence in sustained regional demand.

Key Report Takeaways

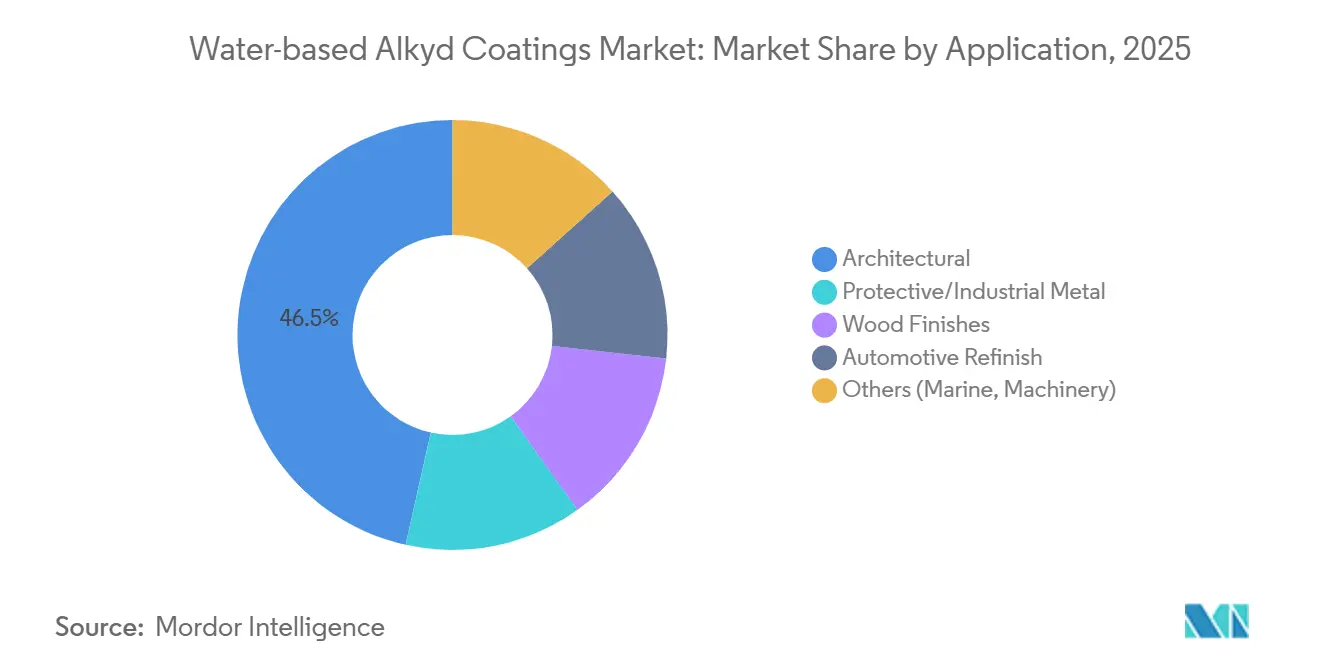

- By application, architectural coatings captured 46.51% of the Water-based Alkyd Coatings market share in 2025; automotive refinish is projected to expand at a 6.56% CAGR during the forecast period (2026-2031).

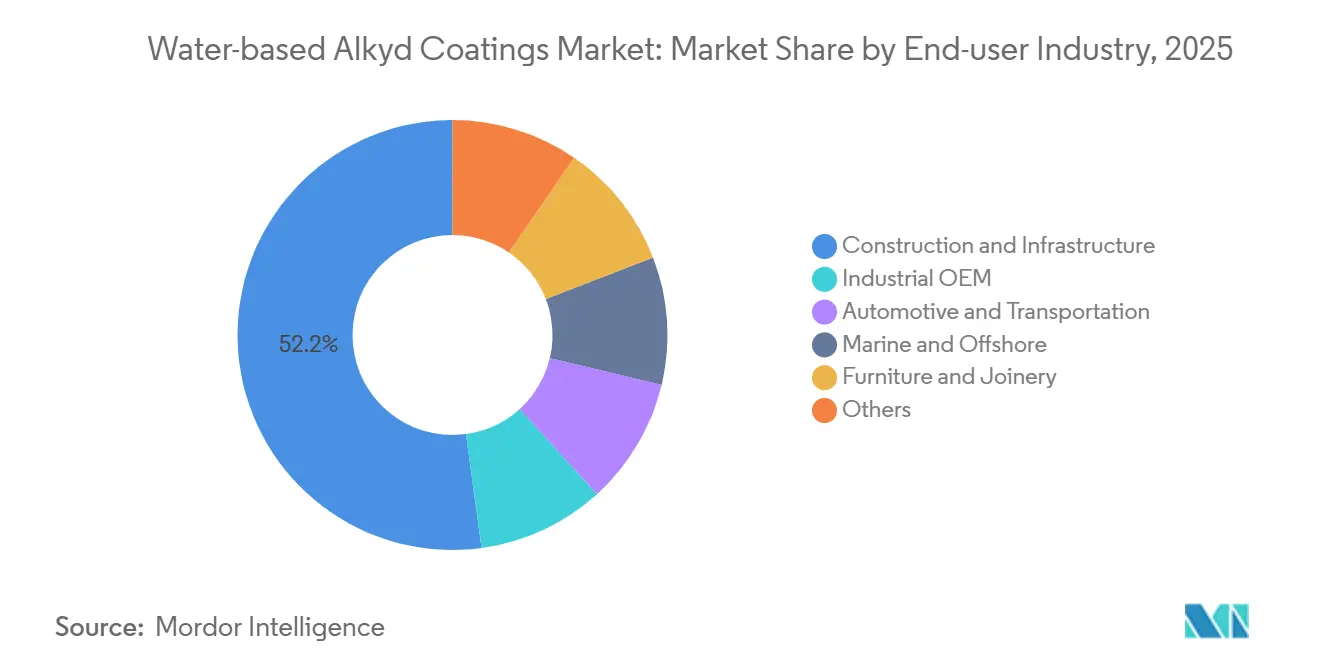

- By end-user industry, construction and infrastructure accounted for 52.16% of the Water-based Alkyd Coatings market size in 2025, and automotive and transportation are set to post the fastest 6.73% CAGR during the forecast period (2026-2031).

- By geography, Asia-Pacific held a 41.32% share of the total market and is expected to post the fastest 5.68% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Water-based Alkyd Coatings Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift from solvent-borne to water-borne alkyds | +1.5% | Global; EU and China lead | Medium term (2–4 years) |

| Construction-sector repaint cycles rebound | +1.2% | North America, Europe, India, ASEAN | Short term (≤ 2 years) |

| Stricter global VOC/HAP caps | +1.0% | EU, California, China, Saudi Arabia | Long term (≥ 4 years) |

| Bio-based alkyd binders reach scale | +0.6% | North America, Europe | Medium term (2–4 years) |

| Nano-hybrid water-borne alkyds hit 2-K parity | +0.4% | APAC, Europe (industrial metal, automotive OEM) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift from Solvent-borne to Water-borne Alkyds

Regulatory mandates dominate the transition narrative. The European Union (EU)’s 2004/42/CE directive caps decorative matt paint VOCs at 30 g/L, Saudi Arabia’s 2025 Environmental Law introduced binding limits at Yanbu and Jubail, and China aims for water-borne coatings to exceed 60% of architectural paint sales by 2025. United States states such as Indiana, North Carolina, and Ohio lowered VOC thresholds in 2024 revisions of State Implementation Plans, nudging contractors toward compliant water-borne systems even outside California[1]U.S. Environmental Protection Agency, “State Implementation Plan Revisions 2024,” epa.gov. Industrial-metal applicators pursuing NESHAP (National Emission Standards for Hazardous Air Pollutants) exemptions are embracing water-borne epoxy-ester hybrids to avoid the 10 tons per year HAP trigger. Scale economies and cross-regional product harmonization attract investment, positioning early movers to benefit as laggard jurisdictions tighten standards over the next decade.

Construction-Sector Repaint Cycles Rebound

Deferred maintenance from 2020-2023 unwound in 2025, lifting global architectural repaint demand beyond 55% of decorative-coatings consumption. Commercial landlords in North America and Europe favor low-odor water-borne products that enable same-day occupancy and align with LEED (Leadership in Energy and Environmental Design) and BREEAM (Building Research Establishment Environmental Assessment Method) certification targets[2]Sherwin-Williams Co., “2025 Form 10-K,” sherwin-williams.com. Asia-Pacific megaprojects, China’s USD 10 billion Pinglu Canal and the proposed USD 21.6 billion Xianggui Canal, specify water-borne primers for steel components under rigorous environmental impact assessments. India’s National Infrastructure Pipeline and ASEAN connectivity corridors mirror this low-VOC bias, driving protective-coating demand for bridges and rail corridors. The rebound extends beyond architectural segments into infrastructure, expanding the water-borne alkyd resins market’s installed base.

Stricter Global VOC/HAP Caps

New compliance layers emerge in waves. The European Chemicals Agency added cobalt salts to the SVHC (Substance of Very High Concern) list in 2024, prompting shifts to manganese or zirconium driers. California’s South Coast AQMD (Air Quality Management District) tightened industrial-maintenance VOC caps to 100 g/L in 2024, and Saudi Arabia’s 2025 Environmental Law spurred Jazeera Paints’ ultra-low-VOC interior line, which captured 48.41% national share within six months. As regional thresholds converge downward, formulators investing today in compliant water-borne platforms skip costly reformulation later, creating a durable competitive advantage across the water-borne alkyd resins market.

Bio-based Alkyd Binders Reach Commercial Scale

Corporate net-zero roadmaps and public-procurement preferences are mainstreaming renewable content. Arkema’s Synaqua 4856, certified 97% bio-based by the USDA (United States Department of Agriculture), entered full production in 2024 and is gaining decorative-paint adoption without durability trade-offs. Relement secured 2024 offtake agreements for renewable methylphthalic anhydride, enabling formulators to swap out fossil anhydrides while preserving fast-dry kinetics. Perstorp’s 100% bio-based Voxtar M100 polyol, launched in 2025, is being trialed by European brands under retailer pressure to exceed 50% renewable content by 2027. As the feedstock premium narrowed from 15-25% in 2023 to 5-10% in 2025, the economic hurdle to bio-based adoption in the water-borne alkyd resins market fell sharply.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Longer drying/curing time vs solvent systems | -0.8% | Global; acute in humid ASEAN and Middle East climates | Short term (≤ 2 years) |

| End-user price sensitivity in emerging markets | -0.5% | India, Southeast Asia, South America, Middle East | Medium term (2–4 years) |

| Volatile tall-oil fatty-acid supply | -0.4% | North America, Scandinavia, global spillover | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Longer Drying/Curing Time Versus Solvent Systems

Water-borne alkyds often take 30-50% longer to through-dry, limiting throughput in body shops and furniture lines. AkzoNobel’s Sikkens Autowave Optima, launched in February 2025, halves flash-off time and cuts booth energy by 60%, but many competitors lag. Furniture makers in humid Southeast Asia report 16-24-hour sandable hardness versus 6-8 hours for solvent systems, forcing costly drying-oven upgrades. The productivity gap remains stark in marine settings with tidal scheduling, where Jotun’s Hardtop XP II stays solvent-borne despite doubled hardness claims, underscoring technical hurdles.

End-User Price Sensitivity in Emerging Economies

A 20-30% product-cost premium persists due to higher solids and specialty surfactants. Contractors in India and South America resist unless regulators enforce compliance. Saudi Arabia’s USD 240 million specialty-coatings market reveals a 20-30% installed-cost hike for advanced water-borne systems, further strained by scarce skilled applicators. Fragmented South American regulations allow cheaper solvent products outside Brazil’s urban centers, diluting the water-borne alkyd resins market momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Refinish Outpaces Architectural Growth

Architectural coatings retained 46.51% of the 2025 demand. Automotive refinish accounted for a 6.56% CAGR during the forecast period (2026-2031). Sikkens Autowave Optima’s 50% faster application boosted body-shop productivity, underpinning refinish momentum. The water-borne alkyd resins market size for refinish is projected to rise steadily as repair volumes normalize post-pandemic. Protective metal applications pursue water-borne epoxy-ester hybrids to dodge NESHAP thresholds, though edge-protection performance still anchors some users to solvent two-component systems.

Wood finishes post consistent adoption driven by formaldehyde rules and retailer mandates. AkzoNobel’s RUBBOL WF 3350, featuring 20% bio-content, targets premium European joineries. Marine uptake remains niche yet strategic: Hempel’s Hempaguard NB enables advanced antifouling at the shipyard stage, shortening newbuild cycles. Closing the drying-time gap remains pivotal; once parity emerges, high-volume OEM and industrial machinery lines are likely to deepen penetration within the water-borne alkyd resins market.

By End-User Industry: Automotive Vertical Accelerates

Construction and infrastructure still contributed 52.16% of 2025 revenue, underpinned by backlog-clearing repaint cycles and Asia-Pacific megaprojects. Automotive and transportation is forecast to expand 6.73% annually during the forecast period (2026-2031), outpacing the broader market as OEMs adopt water-borne primers to satisfy stricter VOC limits and as refinish shops demand faster drying. The segment accounted for a growing slice of the water-borne alkyd resins market share alongside electrification-driven low-emission manufacturing.

Industrial OEMs appreciate single-component epoxy primers that remove pot-life waste, enhancing throughput in labor-constrained fabrication plants. Marine operators value silicone-hybrid antifouling’s fuel-savings guarantee; Jotun’s dock-to-dock warranty under its Hull Performance Solutions 2.0 resonates with shipowners focused on decarbonization targets. Furniture and joinery segments continue migrating to low-odor systems, yet throughput penalties hinder universal adoption until drying-time technology matures.

Geography Analysis

Asia-Pacific accounted for 41.32% of the market share in 2025, and the regional water-based alkyd coatings market is forecast to expand 5.68% annually during the forecast period (2026-2031). China’s policy that water-borne coatings exceed 60% of architectural sales by 2025 anchors demand, and steel-intensive canals such as Pinglu and Xianggui specify low-VOC primers. India’s National Infrastructure Pipeline and ASEAN transport corridors echo the specification trend, lifting regional consumption. Japan and South Korea show slower decorative growth as penetration already tops 65%, but marine programs spur niche demand. Jotun’s Hull Performance Solutions 2.0, launched in June 2025, demonstrates this momentum with integrated antifouling and performance analytics.

North America experiences a capacity-investment surge. PPG’s USD 300 million outlay across Tennessee, Ohio, and Mexico by 2028 boosts regional supply by 11 million gallons annually, while Sherwin-Williams’ Statesville expansion adds capacity and 180 jobs. Regulatory fragmentation persists: California’s strict caps contrast with more lenient Midwest limits, enabling formulators to tailor VOC-optimized portfolios. Canadian and Mexican automotive producers accelerate water-borne adoption as electric-vehicle facilities prioritize low-emission processes.

Europe’s share stabilizes after early decorative penetration. Growth pivots toward protective-coatings contracts such as Germany’s inland-waterway refurbishments, where moisture-curing single-component polyurethanes win over epoxies in humid locks. The Middle East paints and coatings market is expanding majorly due to Vision 2030 megaprojects like NEOM. Jotun’s AED 450 million Abu Dhabi plant, announced January 2026, signals commitment to regional growth. South America remains fragmented; Brazil dominates the regional market share, but non-harmonized VOC rules allow solvent-borne holdouts elsewhere.

Competitive Landscape

The Water-based Alkyd Coatings market is moderately consolidated. Portfolio premiumization dominates R&D (research and development); Arkema, Perstorp, and Relement feed bio-based binder demand, and hybrid architectures that marry alkyd with acrylic or silicone backbones enter the mainstream. Smaller innovators fill white spaces; Chemetall’s VIANT single-layer nano-hybrid primer lowers energy costs for metal fabricators, while digital hull-performance analytics differentiate Jotun’s service-led propositions.

Water-based Alkyd Coatings Industry Leaders

The Sherwin-Williams Company

Jotun

Akzo Nobel N.V.

PPG Industries Inc.

NIPSEA Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: PPG Industries, Inc., started up a dedicated waterborne automotive coatings plant, including water-based alkyd coatings, in Thailand, citing strong regional demand for sustainably advantaged products.

- August 2024: PPG completed an expansion of its Yen Phong (Vietnam) industrial-coatings plant, adding a new line for AQUACRON waterborne decorative and functional coatings which also includes alkyd water-borne coatings.

Global Water-based Alkyd Coatings Market Report Scope

Water-based alkyd coatings, heralded as eco-friendly and low in volatile organic compounds (VOCs), stand out as modern alternatives to conventional oil-based paints. These coatings not only deliver a high gloss finish but also boast remarkable durability and robust adhesion on both wood and metal surfaces. By utilizing water as their primary solvent, they ensure a fast-drying and low-odor application, making them ideal for a range of settings, from interior spaces to industrial sites and architectural projects.

The Water-based Alkyd Coatings market is segmented by application and end-user industry. By application, the market is segmented into architectural, protective/industrial metal, wood finishes, automotive refinish, and others (marine, machinery). By end-user industry, the market is segmented into construction and infrastructure, industrial OEM, automotive and transportation, marine and offshore, furniture and joinery, and others. The Water-based Alkyd Coatings market report also provides market sizing and forecasts within 16 countries across regions worldwide in value (USD).

| Architectural |

| Protective/Industrial Metal |

| Wood Finishes |

| Automotive Refinish |

| Others (Marine, Machinery) |

| Construction and Infrastructure |

| Industrial OEM |

| Automotive and Transportation |

| Marine and Offshore |

| Furniture and Joinery |

| Others |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Application | Architectural | |

| Protective/Industrial Metal | ||

| Wood Finishes | ||

| Automotive Refinish | ||

| Others (Marine, Machinery) | ||

| By End-User Industry | Construction and Infrastructure | |

| Industrial OEM | ||

| Automotive and Transportation | ||

| Marine and Offshore | ||

| Furniture and Joinery | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the global water-borne alkyd resins market be by 2031?

It is forecast to reach USD 5.20 billion by 2031, expanding at a 5.14% CAGR from 2026.

Which end-user vertical is growing fastest?

Automotive and transportation is projected to expand at 6.73% annually through 2031 as OEMs and refinish shops migrate to low-VOC primers and basecoats.

What drives Asia-Pacific demand for water-borne alkyd resins?

Regional growth stems from China’s 60% water-borne mandate for decorative sales, India’s and ASEAN’s infrastructure spending, and rapid industrialization.

Why do water-borne alkyds cost more than solvent systems?

Higher resin solids, specialty surfactants, and corrosion inhibitors push costs 20-30% above solvent equivalents, a premium that narrows with scale and regulation.

How are suppliers addressing long drying times?

Innovations such as fast-evaporating co-solvents, nano-hybrid architectures, and ambient-cure single-layer primers are cutting through-dry times by up to 50%.

Page last updated on: