Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

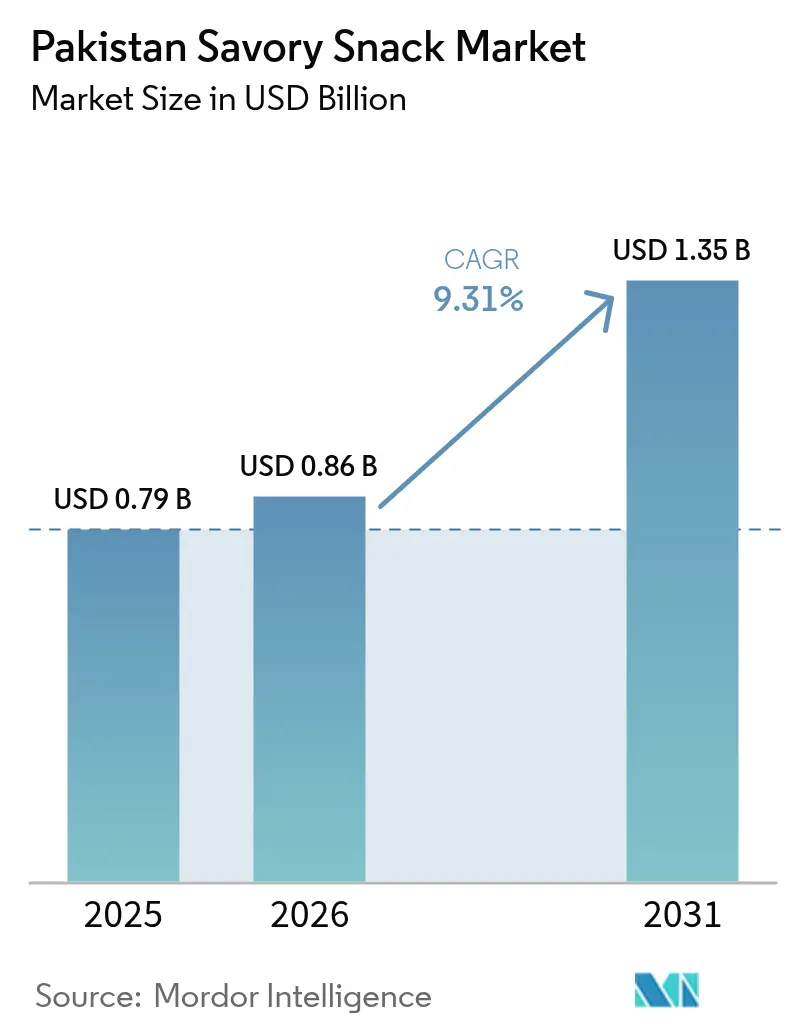

| Base Year Market Size (2025) | USD 0.79 Billion |

| Market Size (2026) | USD 0.86 Billion |

| Market Size (2031) | USD 1.35 Billion |

| Growth Rate (2026 - 2031) | 9.31% CAGR |

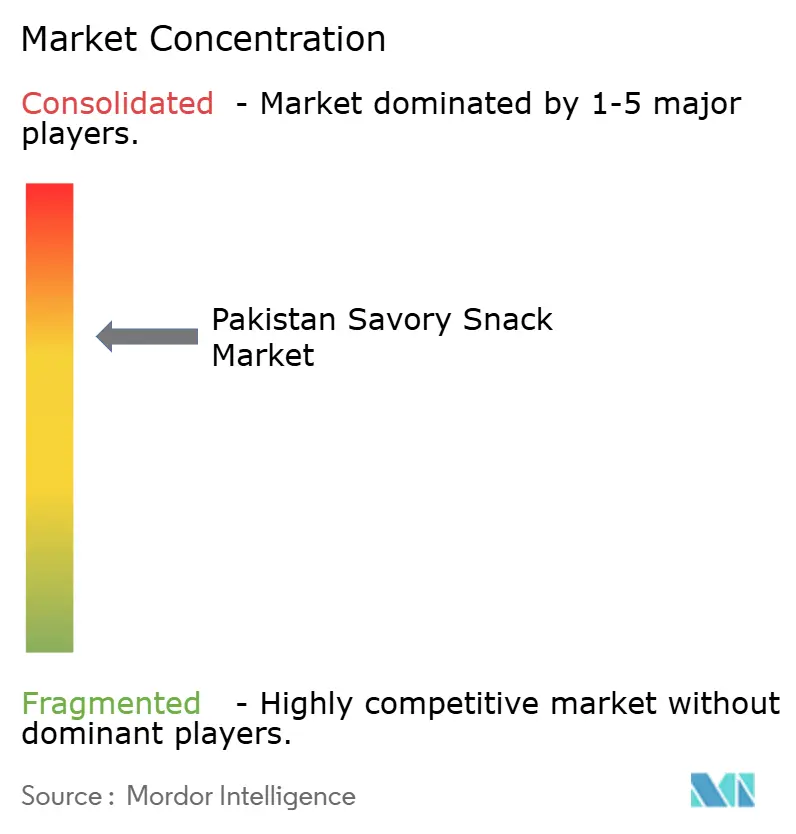

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pakistan Savory Snack Market Analysis by Mordor Intelligence

The Pakistan savory snacks market size was valued at USD 0.79 billion in 2025 and estimated to grow from USD 0.86 billion in 2026 to reach USD 1.35 billion by 2031, at a CAGR of 9.31% during the forecast period (2026-2031). The market is experiencing significant growth as urban populations embrace modern lifestyles, with consumers benefiting from increased purchasing power and evolving food preferences. Young consumers, in particular, are driving market expansion through their demand for convenient, on-the-go snacks that successfully blend international snacking concepts with traditional Pakistani taste preferences. Market participants are responding to these trends by introducing innovative flavor profiles and nutritionally enhanced products, while also leveraging quick-commerce platforms to improve product accessibility. The market structure maintains a balanced mix of international and local manufacturers, creating a dynamic competitive environment. Additionally, the Pakistan Standards & Quality Control Authority (PSQCA) has strengthened its regulatory framework, compelling manufacturers to invest in advanced production facilities and develop distinct market positioning strategies to meet higher quality standards [1]Source: Pakistan Standards & Quality Control Authority, “PSQCA Annual Report 2025,” psqca.gov.pk .

Key Report Takeaways

- By product type, chips and crisp-based snacks held 35.22% of the Pakistan savory snacks market share in 2025, whereas extruded and puffed snacks are forecast to expand at a 10.08% CAGR through 2031.

- By flavor profile, flavored variants captured 62.94% of the Pakistan savory snacks market size in 2025; the same segment is projected to grow at 10.08% CAGR between 2026-2031.

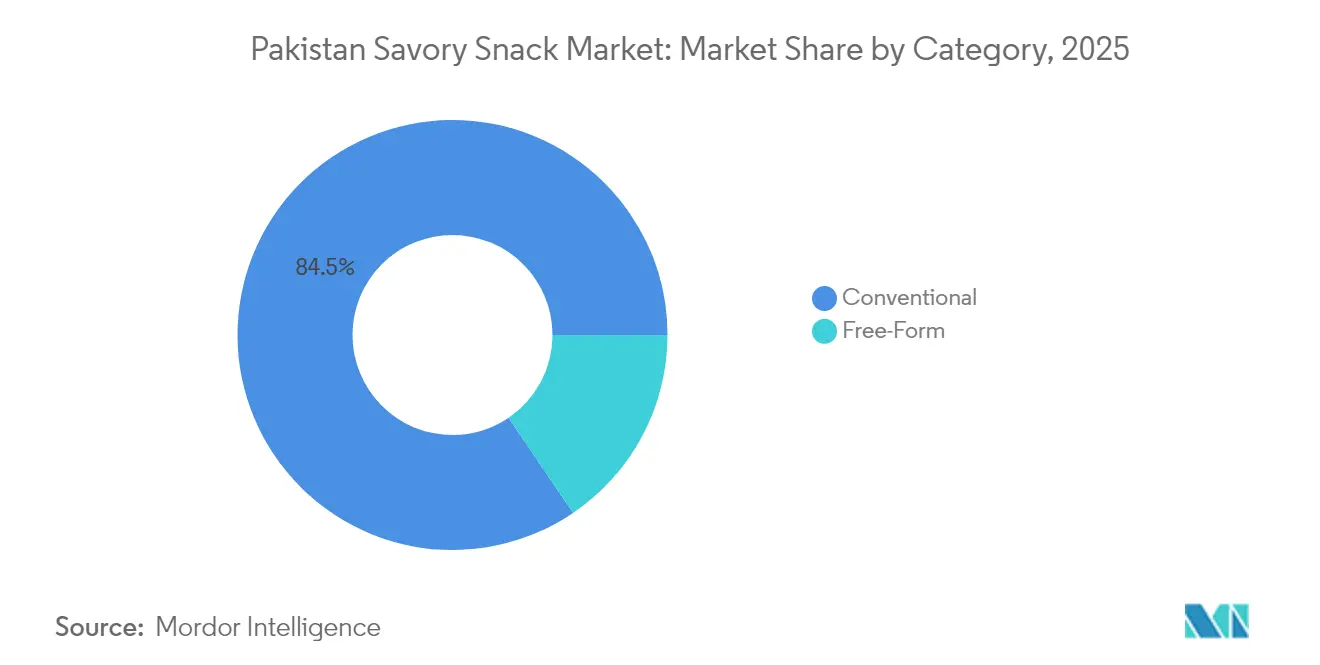

- By category, conventional products commanded 84.48% revenue share in 2025, while free-form snacks post the fastest 10.19% CAGR to 2031.

- By distribution channel, convenience and grocery stores accounted for 53.48% of 2025 sales; online retailers record the highest 10.01% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Pakistan Savory Snack Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanization and busy lifestyles increasing demand for convenient snacks | +2.1% | National, with early gains in Karachi, Lahore, Islamabad | Medium term (2-4 years) |

| Growth in on-the-go food consumption trends | +1.8% | Urban centers, expanding to tier-2 cities | Short term (≤ 2 years) |

| Innovating flavors, including fusion and local varieties | +1.5% | National, with regional taste preferences | Medium term (2-4 years) |

| Industry investment in fortified and healthier snacks | +1.2% | Urban affluent segments, health-conscious demographics | Long term (≥ 4 years) |

| Advent of microwaveable and ready-to-eat packaging formats | +0.9% | Urban households, working professionals | Medium term (2-4 years) |

| Increased digital commerce and online snack sales | +1.8% | Metropolitan areas, expanding to smaller cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Urbanization and Busy Lifestyles Increasing Demand for Convenient Snacks

Pakistan's growing urban population is transforming consumption patterns, particularly in metropolitan areas where packaged snack foods gain increasing acceptance. The country's economic indicators demonstrate positive momentum, strengthening urban consumer purchasing power and supporting premium product preferences. The transition from extended to nuclear family structures reduces traditional home cooking practices and increases the demand for convenient, ready-to-eat options. The rising number of working women in urban areas influences snacking habits, as time constraints lead consumers to choose convenient alternatives over traditional meal preparation. While this urbanization trend reflects global patterns, Pakistan's market uniquely combines local taste preferences with modern packaging. This transformation extends beyond major cities into tier-2 urban centers, supported by improving infrastructure and modern retail development.

Growth in On-the-Go Food Consumption Trends

The transformation of daily routines and work patterns in Pakistan is fundamentally reshaping snacking behaviors, with consumers increasingly gravitating toward portable and convenient food options. The expansion of office hours and extended commuting periods across major metropolitan areas has created multiple snacking occasions throughout the day, moving beyond conventional meal times. Educational institutions and corporate environments have emerged as significant consumption points, driving market demand for portion-controlled packaging solutions that minimize mess and maintain convenience. Single-serve and resealable packaging formats have gained substantial market traction, particularly as they address the challenge of preserving product freshness in Pakistan's demanding climate conditions. The integration of digital payment solutions, including Easypaisa and JazzCash, has streamlined purchase processes at modern retail outlets and vending locations, while food delivery platforms have expanded the market by positioning snacks both as meal complements and standalone orders during non-traditional consumption windows.

Innovating Flavors, Including Fusion and Local Varieties

Flavor innovation continues to drive differentiation in Pakistan's snack market, where traditional taste preferences combine with global culinary influences. Local manufacturers leverage their deep understanding of regional spice profiles to develop product variants that align with distinct provincial preferences - from the tangy flavor profiles preferred by consumers in Punjab to the spicier options favored by those in Sindh. The strategic partnership between Symrise and Shan Foods, established in September 2024, exemplifies this market evolution through their powder-blending facility, which focuses on Pakistan's expanding savory market segment with localized flavor development capabilities. Products incorporating international elements such as cheese, barbecue, and Asian-inspired seasonings increasingly attract younger consumer segments while maintaining familiar base flavors that resonate with the broader market. The innovation cycle continues to accelerate as brands actively compete for retail presence, with flavor variety emerging as a crucial differentiator against traditional loose snacks commonly found in kiryana stores.

Industry Investment in Fortified and Healthier Snacks

Rising health awareness drives market growth, particularly among urban, educated consumers who pay premium prices for nutritionally enhanced products. Manufacturers incorporate protein, fiber, and micronutrients into traditional snacks while reducing sodium and artificial additives. Government nutrition campaigns and increasing healthcare costs encourage preventive dietary choices. Local companies, such as Shan Foods, expand beyond their traditional product lines into health-focused categories, including products like Oatsom healthy oats. International companies use their research capabilities to develop fortified products that address Pakistani nutritional deficiencies, specifically iron and vitamin D supplementation. This health-focused positioning becomes crucial as regulations for health claims develop and urban consumers' understanding of functional foods increases. The market transformation reflects a broader societal shift towards preventive healthcare, with consumers actively seeking products that align with their wellness goals. Companies that successfully integrate health benefits into their product offerings while maintaining taste and convenience are well-positioned to capture this growing consumer segment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer health concerns about processed and high-calorie snacks | -1.4% | Urban educated segments, health-conscious demographics | Medium term (2-4 years) |

| Allergy, dietary restriction limits for nut-based, wheat-based snacks | -0.8% | National, with higher awareness in urban areas | Long term (≥ 4 years) |

| Quality control and standardization challenges | -1.1% | National, affecting export potential | Short term (≤ 2 years) |

| Counterfeit or substandard products impacting market credibility | -0.9% | Rural and semi-urban markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consumer Health Concerns About Processed and High-Calorie Snacks

The growing health awareness among Pakistani consumers continues to influence traditional high-calorie snack categories, as diabetes and obesity rates increase across urban populations. Medical professionals and nutrition experts consistently emphasize the potential health implications associated with trans fats, high sodium content, and artificial preservatives found in processed snacks. This heightened consciousness is particularly evident among educated, affluent consumer segments who carefully scrutinize ingredient labels and actively pursue alternatives to conventional fried products. The market experiences additional pressure as international health research findings receive extensive coverage in local media channels, fostering concerns about specific ingredients and processing methods. However, these evolving consumer preferences drive product innovation toward healthier formulations, creating substantial opportunities for manufacturers who successfully develop nutritious alternatives while preserving the authentic taste elements deeply embedded in local culinary traditions.

Quality Control and Standardization Challenges

The fragmented manufacturing landscape in Pakistan presents significant quality control challenges that erode consumer confidence and create barriers to entering premium international markets. The Pakistan Standards & Quality Control Authority (PSQCA) operates with limited resources, making it difficult to effectively monitor and enforce compliance across thousands of small-scale producers. This results in quality inconsistencies that damage product reliability in the market. The country's infrastructure gaps, particularly the lack of adequate temperature-controlled storage and transportation facilities, directly impact product consistency and shelf life. This is especially problematic for snack products containing sensitive ingredients like oils and fats. When manufacturers attempt to expand their distribution networks beyond local markets, these quality variations become increasingly apparent to consumers who demand consistent product standards. The situation is further complicated by substandard packaging materials that fail to provide adequate protection, leading to premature product deterioration. These quality issues ultimately result in poor consumer experiences, diminishing brand loyalty and reducing the likelihood of repeat purchases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Chips Drive Volume, Extruded Formats Capture Growth

Chips and crisp-based snacks dominate the Pakistani snack market with a substantial 35.22% market share in 2025. This significant market presence reflects the deep-rooted consumer preference for potato-based products, which naturally aligns with the country's traditional fried food consumption patterns. The category maintains its strong position through well-established supply chains, refined manufacturing processes developed over decades, and consistent appeal that transcends age groups, income levels, and geographical regions.

The extruded and puffed snacks segment demonstrates remarkable growth potential, advancing at a 10.08% CAGR through 2031. This growth stems from manufacturers' ability to create innovative texture profiles, maintain product freshness for extended periods, and implement flexible production methods that accommodate diverse flavor combinations. The market also sees increasing participation from health-conscious consumers who gravitate toward nuts, seeds, and trail mixes as protein-rich alternatives to conventional snacks. Additionally, the popcorn segment continues to expand its market presence by leveraging strategic cinema partnerships and capitalizing on the growing demand for ready-to-eat convenience formats.

By Flavor Profile: Spiced Variants Dominate Consumer Preference

Chips and crisp-based snacks dominate the Pakistani snack market with a substantial 35.22% market share in 2025. This significant market presence reflects the deep-rooted consumer preference for potato-based products, which naturally aligns with the country's traditional fried food consumption patterns. The category maintains its strong position through well-established supply chains, refined manufacturing processes developed over years of industry experience, and consistent appeal that resonates across various age groups and income segments.

The extruded and puffed snacks segment demonstrates remarkable growth potential, advancing at a 10.08% CAGR through 2031. This growth trajectory is underpinned by continuous innovation in product textures, improved shelf stability, and manufacturing processes that accommodate diverse flavor profiles. The market also sees increasing participation from health-conscious consumers who gravitate toward nuts, seeds, and trail mixes as protein-rich alternatives to conventional snacks. Meanwhile, the popcorn segment continues to expand its market presence by leveraging strategic cinema partnerships and capitalizing on the growing demand for ready-to-eat convenience formats.

By Category: Conventional Products Maintain Dominance Despite Free-Form Growth

Conventional snacks maintain a commanding 84.48% market share in 2025, reflecting decades of investment in manufacturing capabilities and production expertise. These traditional formats benefit from well-established supply chains, economies of scale in production, and deep consumer familiarity with standard product offerings. The operational efficiency of existing manufacturing infrastructure, combined with optimized distribution networks, enables companies to maintain competitive pricing while ensuring consistent product quality across large-scale production runs.

Free-form products, though currently occupying a smaller market segment, demonstrate remarkable growth potential with a projected CAGR of 10.19% through 2031. This growth trajectory is fueled by evolving consumer preferences toward premium snacking experiences. Consumers increasingly demonstrate willingness to pay premium prices for products that offer unique textural experiences, authentic artisanal characteristics, and innovative presentation formats. This shift in consumer behavior has created opportunities for manufacturers to explore creative product development and capitalize on the growing demand for distinctive snacking options.

By Distribution Channel: Traditional Retail Dominance Faces Digital Disruption

Convenience and grocery stores dominate Pakistan's retail landscape with a substantial 53.48% market share in 2025, highlighting the unwavering influence of kiryana stores and traditional retail formats. These establishments continue to serve as the primary shopping destinations for Pakistani consumers across urban and rural areas. The success of these traditional stores stems from their strategic locations within residential neighborhoods, well-established credit arrangements with regular customers, and adaptable payment systems that effectively accommodate the varying income patterns of local households.

The online retail segment is expected to grow at a CAGR of 10.01% through 2031, making it the fastest-growing distribution channel. This growth is driven by increased smartphone penetration, improved logistics infrastructure, and the expansion of quick-commerce platforms in Pakistan. These platforms have changed shopping patterns by offering deliveries in under 30 minutes, particularly attracting urban consumers. Pakistan's e-commerce market continues to expand, supported by 87.4 million internet subscribers and increasing mobile broadband coverage. While 95% of transactions remain cash-on-delivery, digital payment solutions like Raast are gaining traction in the market .

Geography Analysis

The savory snacks market in Pakistan is concentrated in urban areas, with Punjab and Sindh provinces being the primary consumption centers. In 2024, urban areas comprised 38.36% of Pakistan's total population, with an annual urban growth rate of 2.36% . These provinces' market dominance is attributed to their industrial infrastructure, higher disposable incomes, and concentrated population centers. Cities such as Karachi and Lahore serve as major consumption hubs due to their established retail networks and diverse consumer preferences. Companies typically use these metropolitan areas to test new and premium products before expanding to smaller markets. While urban consumers show a preference for packaged snacks, rural consumers maintain a strong preference for traditional loose snacks and homemade options, though this distinction is diminishing as retail networks expand into rural regions.

Each province's unique taste preferences create distinct market opportunities that influence how companies develop and market their products. Punjab's market responds well to tangy, chat-style flavors that incorporate ingredients like amchur, tamarind, and citric acid. Meanwhile, Sindhi consumers appreciate spicier options that align with their traditional cooking methods. The market shows promising growth potential in Khyber Pakhtunkhwa and Balochistan, where urbanization is increasing packaged food acceptance, despite challenges in infrastructure and consumer purchasing power. Companies are now actively targeting tier-2 cities experiencing economic growth, recognizing the advantages of establishing early market presence before competition intensifies.Border regions near Afghanistan and Iran present unique market dynamics, where informal trade networks influence how branded products perform. Companies are finding success in Middle Eastern markets, particularly in Saudi Arabia and UAE, by leveraging Pakistan's halal certification standards and cultural similarities. The government's support for international expansion is evident through initiatives like the Trade Development Authority of Pakistan's participation in Gulfood Manufacturing 2024 in Dubai. This international exposure brings additional benefits to the domestic market, as companies upgrade their quality standards and packaging to meet export requirements, ultimately improving product offerings across all regions.

Regulatory Landscape

Pakistan savory snack manufacturers operate under a split food-safety framework shaped by the 18th Constitutional Amendment, with enforcement primarily handled at the provincial level (for example, the Punjab Food Authority and the Khyber Pakhtunkhwa Food Safety and Halal Food Authority), alongside federal coordination on imports and SPS policy through the Ministry of National Food Security and Research (MNFSR). For packaged snacks, this typically results in provincial licensing and product registration pathways (such as Punjab Food Authority Certificate of Product Registration supported by sampling and lab analysis), in addition to federal requirements for imported ingredients and materials.

Standards and conformity assessment are anchored by the Pakistan Standards and Quality Control Authority (PSQCA), which issues Pakistan Standards across the agriculture and food division and supports compliance via its testing capabilities. A notable policy signal came in January 2025, when the federal cabinet approved a draft bill in principle to establish a National Food Safety, Animal and Plant Health Regulatory Authority aimed at aligning sanitary and phytosanitary controls with global trade requirements. This is particularly relevant for snack producers looking to scale beyond provincial markets and build export channels.

Competitive Landscape

The Pakistan savory snacks market features a balanced mix of players, where global giants and homegrown brands compete for consumer attention. PepsiCo holds a strong position with its diverse snack offerings, while Unilever Pakistan leverages its robust distribution channels and brand expertise across various product categories. Local players such as Kolson Foods, United Snacks, and Ismail Industries' SnackCity continue to thrive by understanding local tastes, maintaining cost-effective operations, and swiftly adapting their products to meet changing consumer needs.

Industry players are strengthening their market positions through investments in manufacturing facilities, new flavor development, and expanded distribution networks. The adoption of new technologies has become crucial for business success, as companies implement modern production lines, enhanced quality systems, and digital marketing solutions to improve efficiency and consumer connections. A notable example is the partnership between Symrise and Shan Foods, which established an advanced powder-blending facility to serve both local and international markets.

The market presents growth potential in health-conscious segments, premium product offerings, and digital sales channels, though traditional companies find it challenging to adapt to these new demands. Meeting Pakistan Standards and Quality Control Authority (PSQCA) requirements poses challenges for smaller businesses while giving established companies with proper quality systems and certifications a competitive edge.

Pakistan Savory Snack Industry Leaders

PepsiCo Inc.

Ismail Industries Ltd.

United Snacks (Pvt) Ltd.

Kolson Foods

Capital Foods (Pvt) Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Export-oriented product development and capacity-backed scaling stand out as opportunity areas as processed foods receive more attention in trade engagement. In June 2026, Pakistan food-sector engagement with Chinese importers under the second phase of CPEC highlighted commercial interest in value-added categories including potato chips and corn-based snacks, reinforcing whitespace for manufacturers that can deliver consistent quality, halal-aligned positioning, and export-ready packaging.

Supply chain localization and compliance-led modernization also support differentiation in a market where quality control and standardization remain uneven. PepsiCo Pakistan and Kerry established local flavoring manufacturing capability with Far Eastern Impex in Karachi (February 2025), supporting faster reformulation cycles and reducing reliance on imported seasonings, which is relevant for flavored variants that dominate consumption. In parallel, evolving policy discussions around tax and compliance digitization (including consultations on differentiated Federal Excise Duty tied to nutrition attributes and broader regulatory-reform initiatives such as CCoRR proposals in July 2026) shape the environment for nutritional labeling discipline and better-documented formulations.

Recent Industry Developments

- May 2026: PACRA highlighted Ismail Industries Limited capacity uplift to 316,416 MT for FY25, up from 298,356 MT in FY24. The higher capacity supports broader SKU coverage and a stronger presence in modern trade and online channels.

- February 2025: PepsiCo Pakistan inaugurated a local flavor production facility in collaboration with Kerry and Far Eastern Impex. The facility strengthens local sourcing of seasonings for savory snack portfolios and improves supply resilience amid imported-input volatility.

- October 2024: Ismail Industries Limited shareholders approved an investment of up to USD 10 million to establish Bisconni Middle East Manufacturing LLC in Abu Dhabi, UAE. The overseas manufacturing footprint diversifies export channels and expands scale economics for Pakistani-origin packaged foods.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of savory snacks sold in Pakistan, counted as packaged, ready-to-eat items with a mainly salty or spicy taste that are purchased for at-home or on-the-go consumption.

Scope exclusions: Excludes sweet snacks and desserts, and it also excludes fresh, made-to-order snack foods sold only through foodservice when they are not sold as packaged products.

Segmentation Overview

- By Product Type

- Chips and Crisp- Based Snacks

- Nuts, Seeds and Trail Mixes

- Pretzels

- Popcorn Snacks

- Meat and Jerky Snacks

- Extruded and Puffed Snacks

- Others

- By Flavor Profile

- Classic Salted/Plain

- Flavored

- By Category

- Conventional

- Free-Form

- By Distribution Channel

- Supermarket/Hypermarket

- Convenience and Grocery Stores

- Online Retailers

- Others

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries, build the Pakistan demand context, and gather the starting data series that explain snack consumption and trade flows. We typically refer to public sources such as Pakistan Bureau of Statistics releases, State Bank of Pakistan macro series, Pakistan Customs and UN Comtrade trade statistics, FAO food balance style indicators, and relevant food standards notes from PSQCA.

Beyond official statistics, we reviewed company annual reports and filings, investor presentations, product catalogs, and press coverage to understand category activity, route-to-market shifts, and pricing direction. Where needed, we used paid subscriptions for company financials and intelligence, plus patent databases for packaging and processing cues, mainly to validate signals that are not consistently visible in public reporting. These desk sources are illustrative, and other references were used to collect data, validate assumptions, and clarify open points during the study.

Primary Interviews and Surveys

Primary work focused on cross-checking demand drivers and pricing logic for packaged savory snacks in Pakistan, using interviews and short surveys with manufacturers, distributors, modern trade buyers, and channel-focused consultants. Because this is a country market, we covered key demand pockets across major cities as well as the secondary-city retail network, and we used the input to close gaps on channel mix, promotional intensity, and realistic volume-to-value conversion.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 21% | APAC: 42% |

| Mid tier: 51% | Functional/Unit leaders: 34% | EMEA: 37% |

| Smaller Players: 21% | Managers: 45% | Americas: 21% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where retail demand is reconstructed using category consumption signals, inflation-adjusted pricing movement, and the observable shift between traditional retail, modern trade, and online. We then corroborate totals using selective bottom-up approximations, such as sampled SKU price checks multiplied by implied sales velocity, and supplier and distributor roll-ups where respondents can share credible ranges.

Key inputs used in the model include packaged snack price bands by product type, the share of potato chips versus extruded snacks and nuts and seeds, retail channel mix (supermarkets and hypermarkets, convenience and grocery, and online), import exposure for certain items, and changes in promotion depth that can temporarily inflate value sales. Where bottom-up inputs are missing for smaller cities or informal outlets, assumptions are bridged using proxy penetration rates from interviews, followed by a conservative adjustment so the model does not overstate distribution reach.

Forecasts are produced using scenario analysis, which fits this market because price increases, currency moves, and changes in modern retail coverage can create step-changes rather than smooth trends. The scenarios are anchored to expert views on expected price progression, category trading-down behavior, and channel expansion, and then they are converted into one central case used for the final outlook.

Data Validation & Update Cycle

Validation is done through step-by-step checks that compare model outputs against independent signals, such as trade values for relevant snack inputs, macro food inflation patterns, and the implied affordability of common snack price points. If the model shows a sharp jump that is not supported by these indicators, the assumptions are rechecked and, when needed, respondents are contacted again to confirm what changed.

Before sign-off, the full workbook goes through an internal review so that calculations, currency handling, and scope boundaries are consistent across sections. Reports are refreshed annually, and interim updates are made when material events occur, such as policy shifts, large pricing resets, or major channel disruptions. Right before delivery, an analyst performs a final pass to ensure the newest public releases and news signals are reflected in the final numbers.

Mordor Intelligence's Pakistan Savory Snack Market Sizing Compared With Other Published Estimates

Different publications often show different market sizes for Pakistan savory snacks because they do not always count the same products, they pick different base years, and they handle pricing and currency timing in their own ways. Variance also comes from whether the work leans more on reported company sales, consumer spend proxies, or trade and retail channel indicators.

By tracking channel-level mix and refreshing price and promotion assumptions inside the model, Mordor Intelligence keeps the estimate centered on packaged savory snacks sold through defined retail routes in Pakistan, which reduces scope drift into broader snack food baskets or loosely defined traditional items.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.79 B (2025) | |

| Global Consultancy A | USD 3.90 B (2024) | Uses a broader category boundary that appears to fold in a wider set of ready-to-eat savory items, and the jump in value can also be influenced by different price-level handling and base-year selection. |

| Industry Portal B | USD 1.23 B (2025) | Likely reports a narrower forecast window and may apply a different inclusion rule for product types and channels, which can shift totals depending on how nuts and seeds, popcorn, and online retail are counted. |

The spread in the table is mainly explained by what gets included as a savory snack in Pakistan and how value is converted from volume using prices that move fast in inflationary periods. When scope is kept tight around packaged product types and retail channels, and assumptions are repeatedly checked with trade signals and channel experts, the final number becomes easier to trace and repeat over time.

Key Questions Answered in the Report

How large is the Pakistan savory snacks market in 2026?

The Pakistan savory snacks market size is valued at USD 0.86 billion in 2026, supported by strong urban demand.

What is the expected growth rate for savory snacks across Pakistan?

The market is forecast to post a 9.31% CAGR, taking value to USD 1.35 billion by 2031.

Which product category leads sales of savory snacks in Pakistan?

Chips and crisp-based snacks currently lead with 35.22% market share, followed by rapid growth in extruded and puffed formats.

Which distribution channel shows the fastest growth?

Online retailers exhibit the highest 10.01% CAGR as quick-commerce platforms scale nationwide.

Why are flavored snacks outperforming plain variants?

Pakistani consumers favor bold, spice-forward tastes, driving flavored variants to 62.94% share and an ongoing double-digit growth outlook.

Page last updated on: