Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

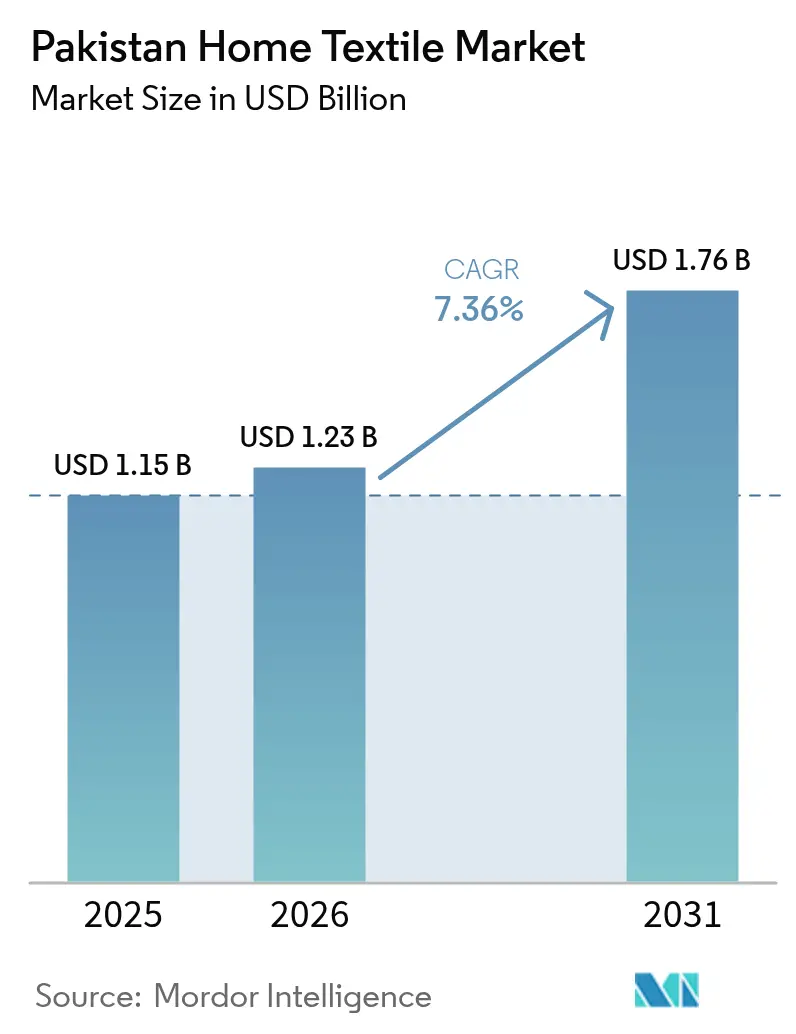

| Base Year Market Size (2025) | USD 1.15 Billion |

| Market Size (2026) | USD 1.23 Billion |

| Market Size (2031) | USD 1.76 Billion |

| Growth Rate (2026 - 2031) | 7.36% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pakistan Home Textile Market Analysis by Mordor Intelligence

The Pakistan home textile market size was valued at USD 1.15 billion in 2025 and estimated to grow from USD 1.23 billion in 2026 to reach USD 1.76 billion by 2031, at a CAGR of 7.36% during the forecast period (2026-2031). Healthy export receipts, vertically integrated mills, and an expanding urban middle class support this trajectory even as manufacturers grapple with electricity shortages and intensifying competition from Bangladesh and India. Pakistan remains the world’s fourth-largest cotton producer; however, domestic output slipped from 11.9 million bales in 2018 to 4.5 million bales in 2021, compelling firms to import larger volumes and to increase polyester and modal blending as a hedge against raw-material volatility [1]Kashif Shahzad et al., “Progress and Perspective on Cotton Breeding in Pakistan,” Journal of Cotton Research, jcottonres.biomedcentral.com. Faster broadband adoption, hotel construction pipelines, and escalating demand for Global Organic Textile Standard (GOTS)-certified merchandise add further lift, while the government’s duty-drawback scheme cushions price rivalry in key European and North American destinations. Headwinds stem from climate-related crop swings, steep power tariffs, and a looming 29% United States levy that could redirect trade flows.

Key Report Takeaways

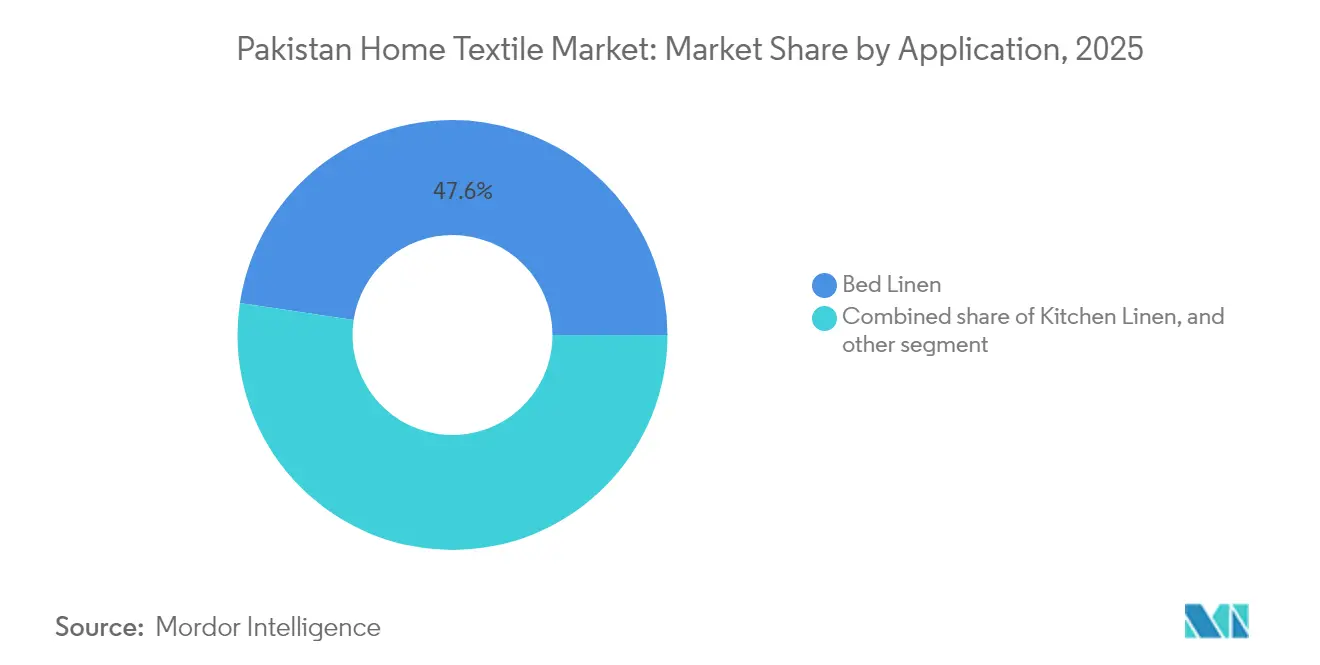

- By application, bed linen led with 47.62% of Pakistan home textile market share in 2025; upholstery is forecast to log an 11.52% CAGR through 2031.

- By material, cotton captured 63.78% of the Pakistan home textile market size in 2025, while synthetic fibers are rising at a 13.41% CAGR.

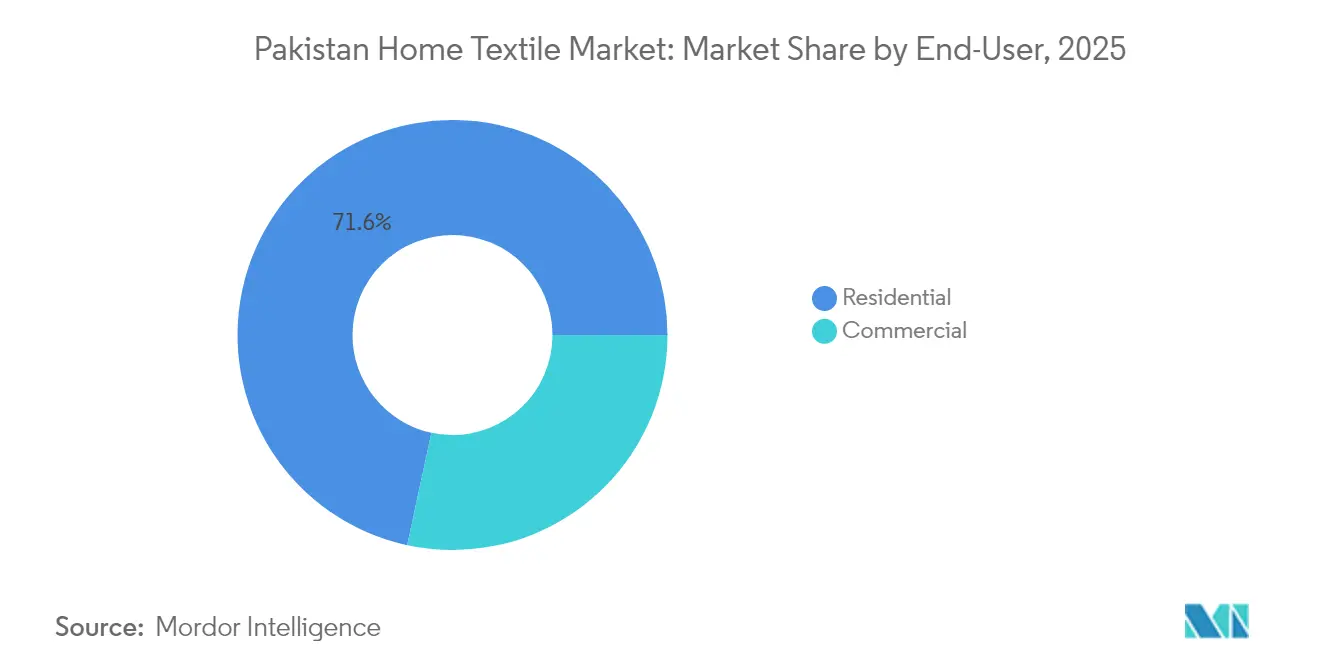

- By end-user, the residential segment accounted for 71.62% of the Pakistan home textile market revenue in 2025, whereas commercial demand is advancing at an 11.02% CAGR.

- By distribution channel, offline retail retained 81.74% share of the Pakistan home textile market in 2025, yet online sales are scaling at a 16.1% CAGR.

- By geography, Punjab delivered a 41.12% share of the Pakistan home textile market in 2025; Khyber Pakhtunkhwa is on track for a 13.32% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Pakistan Home Textile Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce penetration is accelerating domestic sales | +1.2% | Punjab, Sindh, Islamabad Capital Territory | Short term (≤ 2 years) |

| Rising hospitality and tourism investments | +0.8% | Punjab, Sindh, Islamabad Capital Territory | Medium term (2-4 years) |

| Government duty-drawback scheme for textile exports | +1.5% | National concentration in Punjab and Sindh | Long term (≥ 4 years) |

| Surge in eco-friendly fibre certifications | +0.9% | Global export markets; Punjab manufacturing clusters | Medium term (2-4 years) |

| Water-saving dyeing technologies adoption | +0.7% | Punjab, Sindh textile clusters | Long term (≥ 4 years) |

| Demand for customizable products | +0.6% | Urban centers: Karachi, Lahore, Islamabad | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-commerce Penetration Accelerating Domestic Sales

Online channels are climbing at a 16.76% CAGR, even though brick-and-mortar stores still dominate overall revenue. Consumers in Karachi, Lahore, and Islamabad rely on Daraz, Shopify storefronts, and brand-owned apps that now feature augmented-reality room visualizers and GSM disclosure tables. The Pakistan home textile market gains from cash-on-delivery services and micro-logistics fleets that reduce fulfilment times to less than forty-eight hours within Tier 1 cities. Digital shops also permit made-to-order sizing, embroidery, and monogramming, which lifts average order values and trims finished goods inventory. Small mills connect directly to households, capturing margins that formerly belonged to wholesalers and unlocking data analytics on color preference and reorder frequency. The government’s Digital Pakistan initiative has cut customs paperwork for e-commerce parcels, accelerating cross-border sample dispatch and shortening export sales cycles.

Rising Hospitality and Tourism Investments

Pakistan welcomed more than 1 million international visitors in 2024, and pipeline hotel keys are forecast to rise 14% by 2030, creating durable demand for high-thread-count bedding and institutional terry. Developers in Lahore’s central business district specify flame-resistant duvets and colorfast drapery, shifting procurement toward vertically integrated local mills that guarantee compliance. The Pakistan home textile market benefits because commercial buyers place year-round replenishment orders that stabilize spindle utilization and justify capital expenditure on shuttle-less looms. Boutique resorts in Gilgit-Baltistan now champion locally woven throws to highlight regional identity, strengthening domestic value addition. Event-led tourism, including ICC cricket fixtures, further raises linen turnover rates in metropolitan hotels. Consequently, commercial demand delivers higher margins than residential sales and creates a pull effect across spinning, weaving, and finishing segments.

Government Duty-Drawback Scheme for Textile Exports

Rebates of 5% on home textile invoice value shave production costs by up to USD 0.30 per kilogram, equating to a 1.5 percentage-point lift in projected CAGR. Although delays in processing once tied up PKR 30 billion in unpaid claims, a 2023 Federal Board of Revenue (FBR) circular introduced electronic submissions and expedited audits [2]Imran Rana, “PTEA Criticises Non-Payment of Tax Rebates and Duty Drawback,” The Express Tribune, tribune.com.pk. The Pakistan home textile market now sees improved liquidity that finances larger cotton-import letters of credit and broadens yarn inventory buffers ahead of peak European buying seasons. Duty-drawback continuity also signals policy stability to foreign buyers, sustaining multi-year sourcing contracts. Industry associations lobby for extending the scheme through 2030 to counter India’s Production Linked Incentive (PLI) rebates, which could otherwise erode Pakistan’s price edge. Consistent payouts amplify exporters’ confidence to invest in automated cutting lines and wastewater treatment plants.

Surge in Eco-friendly Fiber Certifications

More than fifteen mills have achieved GOTS or OEKO-TEX Standard 100 labels, enabling access to Scandinavian furniture chains and U.S. specialty retailers [3]ICEA, “GOTS Certified List,” icea.bio. Certification audits necessitate pesticide-free cotton, traceable supply chains, and zero-liquid-discharge effluent systems, raising capital intensity but commanding price premiums of 8-10%. The Pakistan home textile market thus pivots toward organic cotton, bamboo viscose, and Tencel lyocell to satisfy environmentally conscious end buyers. Marketing campaigns spotlight carbon-neutral weaving and solar-powered stitching floors, attracting Gen-Z consumers who attribute value to provenance. Certification also lowers compliance costs during U.S. Customs Withhold Release Orders, mitigating reputational risks. Over the medium term, adoption is expected to cascade into Tier 2 suppliers, embedding sustainability as a market entry prerequisite.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic energy shortages and high tariffs | –2.1% | National, acute in Punjab and Sindh | Short term (≤ 2 years) |

| Cotton crop volatility driven by climate change | –1.8% | Major cotton belts across the country | Medium term (2-4 years) |

| Fragmented domestic logistics | -0.9% | Nationwide, rural–urban corridors | Long term (≥ 4 years) |

| Regional price undercutting | -1.3% | Key export markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Chronic Energy Shortages and High Tariffs

Industrial electricity tariffs hover at 13-15 cents per kWh, nearly double subsidized rates in competing South Asian hubs. Unscheduled load shedding shaved 10% off sectoral output in FY 2024, hampering time-sensitive export deliveries. The Pakistan home textile market’s larger mills now install 5-10 MW rooftop solar arrays and lithium-ion storage systems that cover 30-40% of peak usage. Energy-intensive wet-processing units reschedule dyeing shifts to off-peak slots, yet capacity under-utilization erodes gross margins. Government packages that cap tariffs at USD 0.09 for export-oriented units lapse intermittently, breeding uncertainty for financial projections. Without grid reforms, mills risk deferring upgrades and losing share to Bangladeshi suppliers that enjoy steadier power at USD 0.07 per kWh.

Cotton Crop Volatility Driven by Climate Change

Heat stress episodes and pest infestations cut lint yields by 26% between 2020 and 2024, forcing Pakistan to import 1.192 million U.S. bales in 2024, the highest worldwide [4]Amjad Mahmood, “Pakistan Becomes Largest Importer of US Cotton,” Dawn, dawn.com. The Pakistan home textile market faces inflated working-capital needs because imported cotton requires cash-margin letters of credit priced in USD. Currency depreciation widens landed-cost gaps, prompting mills to blend polyester at record levels to protect price points. Farm-level pilot programs for heat-resistant seed varietals show promise but need three to five cropping cycles before widespread adoption. Meanwhile, buyers shift toward fixed-price orders with escalation clauses, transferring some raw-material risk back to suppliers. Climate-driven volatility, therefore, constrains forward-contracting appetite and complicates capacity planning for export-aligned firms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Bed Linen Sustains Volume Leadership while Upholstery Fast-Tracks Premium Growth

The Pakistan home textile market size attributable to bed linen stood at USD 0.55 billion in 2025, representing 47.62% of the overall value. European retailers replenish Pakistani cotton sheeting every season due to consistent shrinkage control and competitive free-on-board pricing. Larger orders let mills operate ring-spinning frames at 92-95% utilization, spreading overhead and sharpening cost curves. Value-addition through wrinkle-free chemical finishing and antimicrobial treatments lifts average selling prices without major loom reconfiguration. Export dependability cements long-term vendor agreements that smooth revenue cycles.

Upholstery, although only 8.52% of 2025 sales, advances to an 11.52% CAGR and is forecast to double its contribution by 2031. Rising urban incomes stimulate the domestic sofa and mattress market, where buyers demand stain-resistant jacquard and chenille weaves. Pakistan's home textile market size in upholstery is also propelled by contract furnishing for four-star hotels and co-working offices that standardize design palettes, enabling longer production runs. Air-jet looms and digital jacquard heads produce intricate patterns with shorter setup times, keeping changeover costs low. Pakistan’s access to polypropylene staple fiber in nearby Gulf markets further supports competitive input pricing for performance upholstery.

By Material: Cotton Retains Majority Share, yet Synthetic Fiber Blends Accelerate

Cotton accounted for 63.78% of Pakistan's home textile market share in 2025 on the strength of decades-old ginning networks and established farmer-mill relationships. Mills leverage long-staple imported lint to spin 40’s to 80’s count yarns for premium sateen and percale. However, lint price spikes and climate swings nurture polyester-cotton blends that clock a 13.41% CAGR. Spinners tailor 60/40 yarns that preserve cotton’s breathability while imparting wrinkle recovery, meeting U.S. hospitality benchmarks.

Pakistan's home textile market size attached to synthetic fibers is further buoyed by duty-free access to imported polyester under regional trade agreements, trimming raw-material differential versus pure cotton. Linen, bamboo, and hemp remain niche at less than 3.00% share, yet command unit prices 2-3 times cotton sheeting, underscoring potential for margin lift through eco-friendly storytelling.

By End-User: Residential Anchor Meets a Surging Commercial Stream

Residential purchases contributed 71.62% to the 2025 value, undergirded by Pakistan’s 240 million population and cultural predisposition for dowry sets comprising twelve-piece bedding assortments. Frequent festive sales events accelerate replacement cycles and create cross-sell opportunities for towel and kitchen linen bundles. Retailers deploy deferred payment plans to nudge average ticket sizes higher in Tier 2 cities.

Commercial customers—hotels, hospitals, universities, and corporate facility management firms—expand at an 11.02% CAGR through 2031. Institutional buyers stipulate tensile strength, bleach resistance, and ISO 9001 quality assurance, propelling mills to integrate laboratory testing and statistical process control. Higher contract volumes in the Pakistan home textile market translate into predictable loom loading, allowing manufacturers to amortize capital-intensive shuttle-less machines over larger throughput. Additionally, commercial demand elevates the value perception of Pakistan-origin goods, reinforcing international brand partnerships.

By Distribution Channel: Physical Stores Still Rule but Click-and-Deliver Gains Momentum

Offline formats retained an 81.74% share in 2025 due to consumer reliance on tactile inspection and same-day purchase gratification. Factory outlets clustered along Lahore’s Ferozepur Road liquidate export surplus, attracting footfall with bundle discounts and loyalty apps. Department stores partner with mills on shop-in-shop concepts that showcase coordinated bedding and curtain ensembles.

Online revenue, climbing to a 16.1% CAGR, benefits from skyrocketing smartphone penetration and simplified digital wallets like Easypaisa. Domestic direct-to-consumer labels offer free swatch delivery and 360-degree thread-count explainers, mitigating the sensory gap. Cross-border e-commerce pilots deliver cushion covers to Gulf expatriate communities within seventy-two hours, giving the Pakistan home textile market a diaspora-led growth lever. Live stream selling on social platforms also converts younger demographics, amplifying brand storytelling at minimal cost.

Geography Analysis

Punjab booked 41.12% of 2025 revenue, reflecting its dense value-chain ecosystem across Faisalabad, Lahore, and Multan. Integrated clusters host spinning, weaving, processing, and accessory units within a fifty-kilometer radius, minimizing freight and turnaround. The provincial government subsidizes Effluent Treatment Plants through soft loans, helping mills meet zero-discharge criteria demanded by Scandinavian buyers. Nonetheless, rising minimum wages and elevated grid tariffs motivate some manufacturers to scout new sites.

Sindh leverages Karachi’s Port Qasim and deep-draft berths, facilitating cotton imports from the United States and polyester staple fiber from the Gulf. Textile parks around Landhi export high-end terry towels and jacquard blankets to big-box retailers abroad. Local buying houses and testing labs compress sample lead times, anchoring foreign procurement teams in the city. Government incentives for solar installations further reduce effective energy costs for Sindh-based mills.

Khyber Pakhtunkhwa, expanding at a 13.32% CAGR, attracts investment via the Rashakai Special Economic Zone, which offers ten-year tax holidays and one-stop customs clearance. Hydel power availability slashes electricity bills by up to 25% versus Punjab, giving early movers a clear cost advantage. However, supply-chain depth is still maturing; mills must transport chemicals and dyes from Karachi, adding logistical complexity. Workforce training institutes backed by GIZ and local chambers now churn out sewing machine operators and lab technicians to bridge skill gaps.

Competitive Landscape

The Pakistan home textile market hosts more than twenty sizable mills, yet the leading firms now control the majority share of export receipts. Interloop Limited, originally a hosiery specialist, diversified into bedding and posted PKR 147 billion in FY 2024 textile exports, underscoring scale economies. Nishat Mills invested USD 20 million in automated cut-and-sew units linked to an enterprise resource planning platform that reduces fabric wastage by 8%.

Sustainability credentials differentiate suppliers in buyer shortlists. Kamal Textile and Al-Karam commissioned zero-liquid-discharge plants, achieving 90% water recycling. Gul Ahmed added a 30 MW solar park that trims scope-2 emissions and cushions against unpredictable grid outages. These moves align with European retailer scorecards that now allocate up to twenty compliance points to carbon footprint metrics.

Technology is accelerating. Digital color-matching cameras cut shade approval from forty-eight to six hours, while AI-driven defect-detection systems slash second-grade fabric by 3%. Product innovation centers on cotton-poly blends, water-repellent table linen, and hypoallergenic pillow protectors. Some firms pilot blockchain-based yarn tracing, offering QR codes that confirm farm origin. Prospective 29% U.S. tariffs spur scenario planning; exporters hedge with free-trade-agreement markets like Canada and the United Kingdom while eyeing joint ventures in Türkiye to exploit EU Customs Union preferences.

Pakistan Home Textile Industry Leaders

Nishat Mills Ltd.

Gul Ahmed Textile Mills Ltd.

Yunus Textile Mills Ltd.

Sapphire Textile Mills Ltd.

Al-Karam Textile Mills (Pvt) Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Swedwatch released a study that cataloged labor-rights gaps in Pakistani mills supplying European public-procurement contracts. The report urges Brussels to mandate social compliance clauses and recommends that buyers require traceability back to the farm level. Local industry bodies responded by announcing a voluntary code of conduct and inviting auditors to inspect wage documentation.

- April 2025: Arab News highlighted possible 29% reciprocal U.S. duties on Pakistani products. The Pakistan Textile Council drafted a contingency plan that involves targeting apparel buyers seeking alternatives to higher-tariffed Chinese suppliers. Stakeholders petitioned the Office of the U.S. Trade Representative for phased implementation, citing Pakistan’s role in Afghanistan reconstruction supply chains.

- November 2024: Dawn reported that Pakistan became the world’s largest importer of U.S. cotton, with 1.192 million bales shipped. Mills justified the purchase by pointing to superior fiber length and low contamination levels despite higher landed costs. Analysts warn that sustained dependence could expose the Pakistan home textile market to currency volatility during the Federal Reserve’s tightening cycle.

Pakistan Home Textile Market Report Scope

Home textiles are fabrics and clothes used specifically for furnishing a residence. the materials and design of each are defined by the functional and aesthetic uses of each. Pakistan's home textile market is segmented by product and by distribution channel. By product, the market is segmented into bed linen, bath linen, kitchen linen, upholstery, and floor covering. By distribution channel the market is segmented into, supermarkets & hypermarkets, specialty stores, online, and other distribution channels. The report offers market size and forecasts for the Pakistan home textiles market in value (USD) for all the above segments.

By Application

| Bed Linen |

| Bath Linen |

| Kitchen Linen |

| Upholstery |

| Others (Carpets and Area Rugs) |

By Material

| Cotton |

| Linen |

| Synthetic Fibers |

| Other Materials (Wool, Hemp, Silk, Jute, Bamboo etc.) |

By End-User

| Residential |

| Commercial |

By Distribution Channel

| Offline |

| Online |

By Geography

| Punjab |

| Sindh |

| Khyber Pakhtunkhwa |

| Balochistan |

| Islamabad Capital Territory |

| Rest of Pakistan |

| By Application | Bed Linen |

| Bath Linen | |

| Kitchen Linen | |

| Upholstery | |

| Others (Carpets and Area Rugs) | |

| By Material | Cotton |

| Linen | |

| Synthetic Fibers | |

| Other Materials (Wool, Hemp, Silk, Jute, Bamboo etc.) | |

| By End-User | Residential |

| Commercial | |

| By Distribution Channel | Offline |

| Online | |

| By Geography | Punjab |

| Sindh | |

| Khyber Pakhtunkhwa | |

| Balochistan | |

| Islamabad Capital Territory | |

| Rest of Pakistan |

Key Questions Answered in the Report

How large is the Pakistan home textile market in 2026?

The Pakistan home textile market size is USD 1.23 billion in 2026 and is projected to reach USD 1.76 billion by 2031.

What is the expected growth rate for Pakistani home textiles?

The market is forecast to grow at a 7.36% CAGR between 2026 and 2031.

Which application generates the most revenue?

Bed linen leads with 47.62% of 2025 revenue due to established export relationships and high reorder frequency.

Why are synthetic fiber blends gaining share?

Polyester-cotton blends mitigate cotton price volatility and deliver wrinkle recovery, supporting a 13.41% CAGR for synthetic fibers.

What geographic region is expanding fastest?

Khyber Pakhtunkhwa is poised for a 13.32% CAGR through 2031, propelled by economic-zone incentives and lower energy costs.

How are energy shortages being addressed by mills?

Leading manufacturers install rooftop solar arrays and lithium-ion storage systems, covering up to 40% of peak consumption to counter tariffs at 13-15 cents per kWh.

Page last updated on: