Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

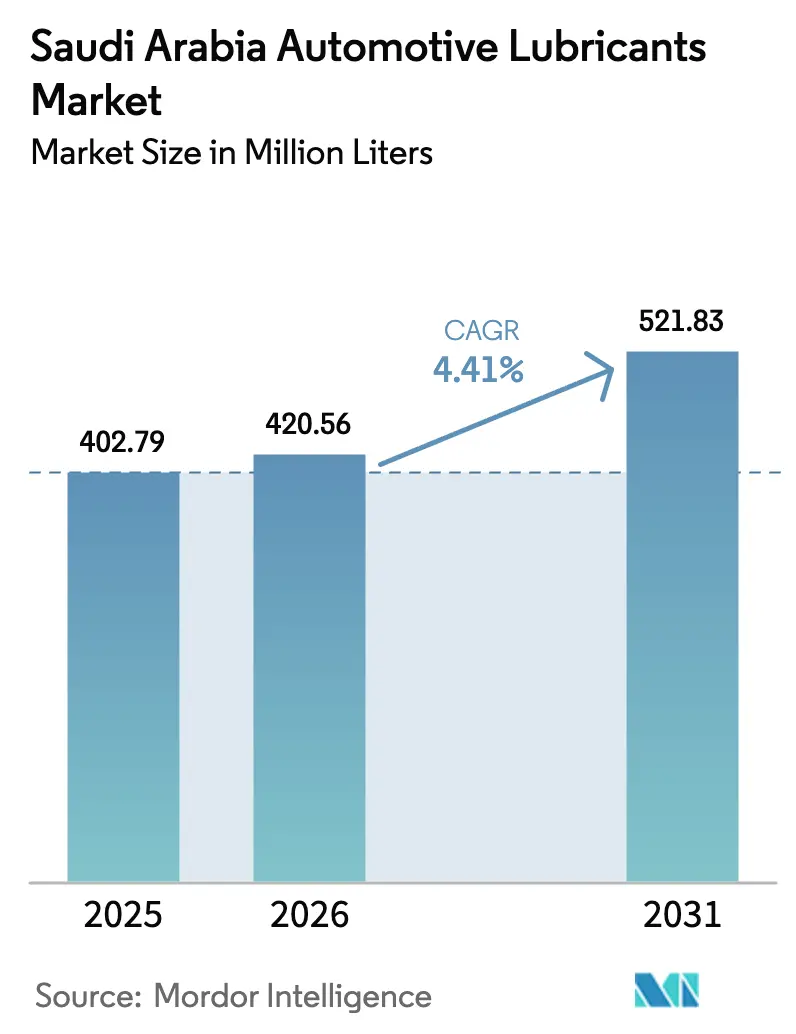

| Base Year Market Size (2025) | 402.79 Million liters |

| Market Volume (2026) | 420.56 Million liters |

| Market Volume (2031) | 521.83 Million liters |

| Growth Rate (2026 - 2031) | 4.41% CAGR |

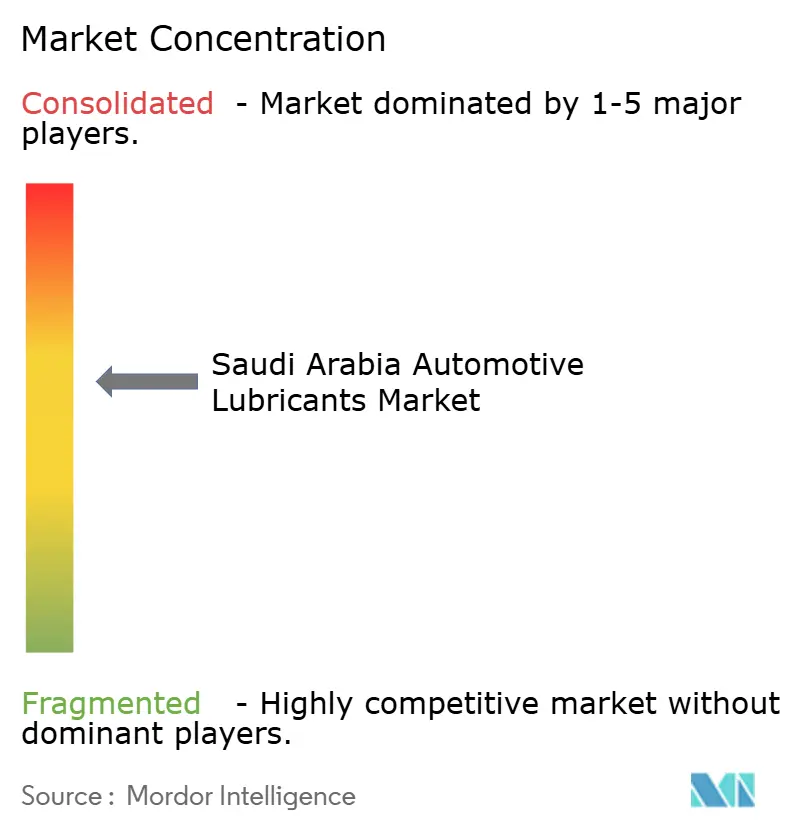

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Automotive Lubricants Market Analysis by Mordor Intelligence

The Saudi Arabia Automotive Lubricants Market size was valued at 402.79 Million liters in 2025 and is estimated to grow from 420.56 Million liters in 2026 to reach 521.83 Million liters by 2031, at a CAGR of 4.41% during the forecast period (2026-2031). This trajectory reflects steady additions to vehicle parc, persistent 10,000-kilometer service-interval enforcement, and a gradual shift toward synthetic and low-ash formulations that temper, but do not erase, electrification headwinds. Market leaders are deepening vertical integration - Aramco’s downstream push and potential Castrol bid illustrate the view that the Saudi Arabia Automotive Lubricants market remains a growth prize, not a sunset territory. E-commerce channels, same-day delivery, and multi-vehicle OEM-approved fluids widen access and raise competitive stakes, while emerging re-refining capacity introduces a medium-term substitution threat. Against that backdrop, private-car dependency, mega-project construction demand, and stringent warranty clauses ensure baseline volume growth and support premiumization.

Key Report Takeaways

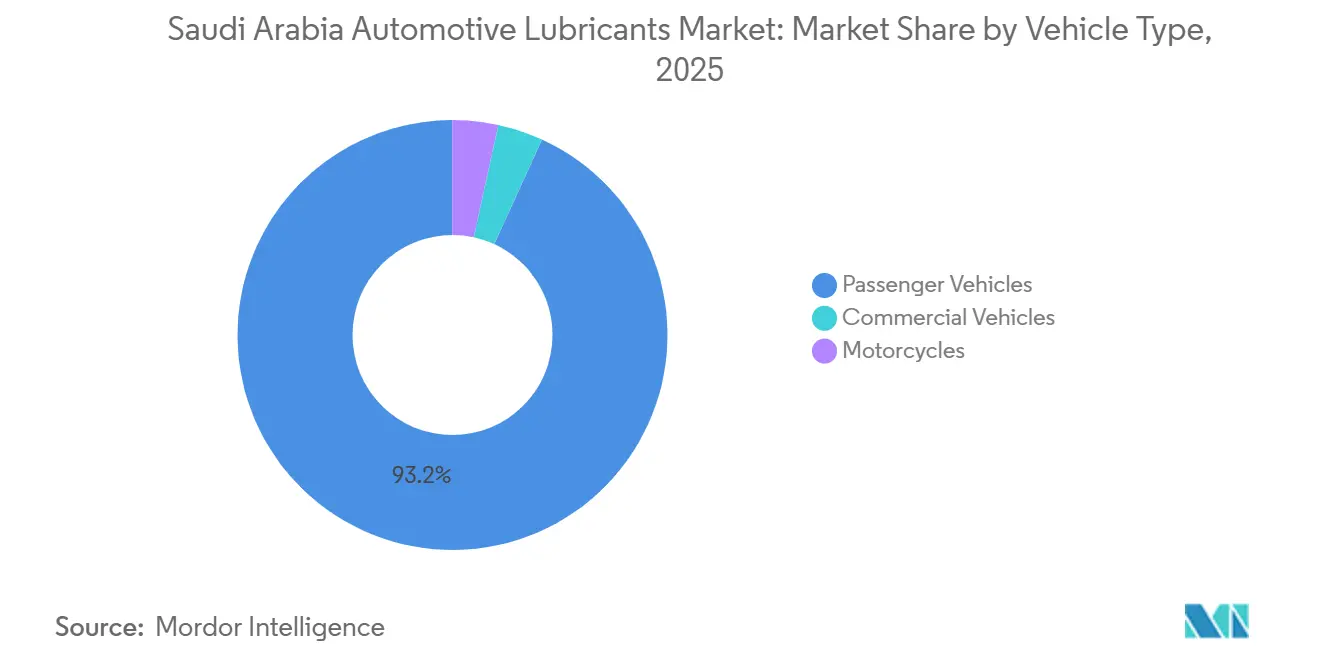

- By vehicle type, passenger vehicles held 93.17% of the Saudi Arabian Automotive Lubricants market share in 2025. Commercial vehicles are forecast to register a 6.89% CAGR in the Saudi Arabia Automotive Lubricants market size through 2031, the fastest among vehicle types.

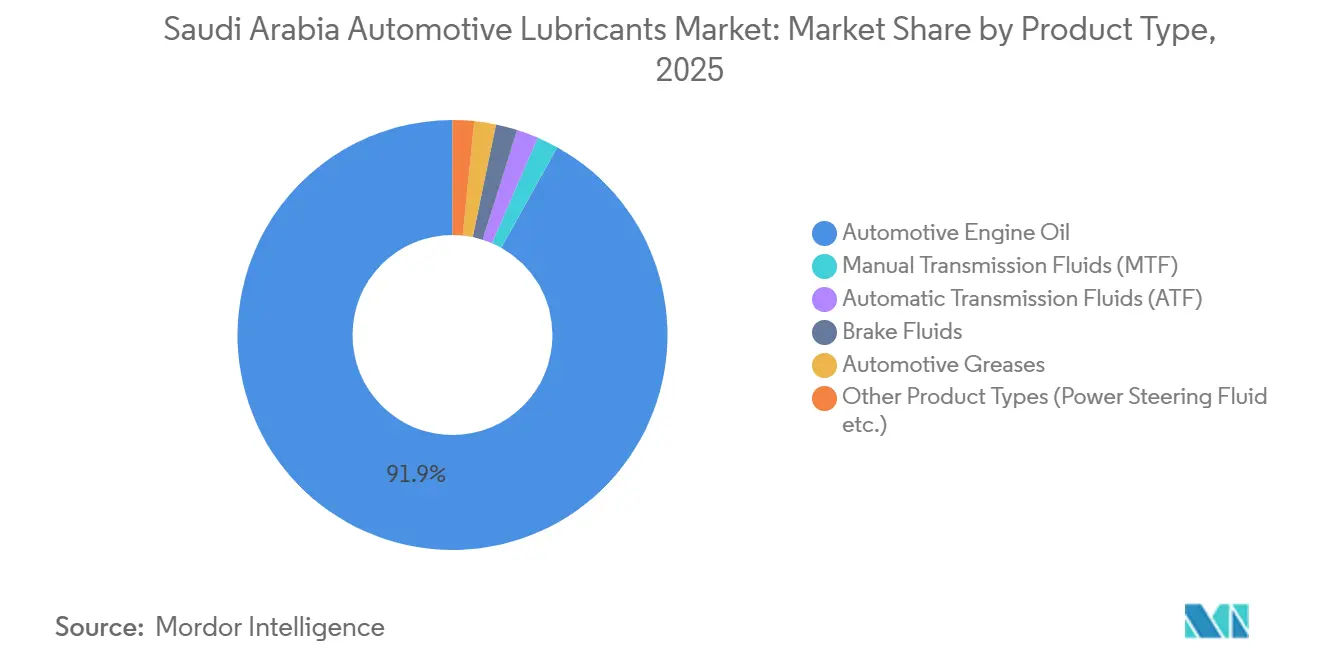

- By product type, automotive engine oils commanded 91.88% of 2025 volume, the largest product-type share in the Saudi Arabia Automotive Lubricants market. Automatic Transmission Fluids are set to expand at a 6.30% CAGR, leading product-type growth in the Saudi Arabia Automotive Lubricants market size.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging light-duty vehicle parc | +1.2% | National, concentrated in Riyadh, Jeddah, Dammam | Medium term (2–4 years) |

| Mandatory 10,000-km oil-change reminder program | +0.6% | National, enforced via SASO technical regulations | Short term (≤ 2 years) |

| Growing synthetic-oil penetration in harsh-climate fleets | +0.8% | National, acute in Eastern Province desert operations | Long term (≥ 4 years) |

| E-commerce platforms offering same-day lubricant delivery | +0.4% | Urban centers—Riyadh, Jeddah, Khobar | Short term (≤ 2 years) |

| Military fleet modernization requiring low-ash fluids | +0.3% | National, defense procurement hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Light-Duty Vehicle Parc

In 2024, Saudi Arabia's vehicle count surged, marking a significant year-on-year increase. This growth is fueled by a rising population, increasing disposable incomes, and a limited mass transit system. With Euro 5 regulations in play, OEMs are mandated to use low-SAPS API SP or ILSAC GF-6A oils, steering buyers towards premium products right from the first change.[1]Saudi Standards, Metrology and Quality Organization, “Technical Regulation for Lubricating Oils,” saso.gov.sa Ride-hailing fleets, often clocking high mileage, are shortening their drain cycles to as frequently as 30 days, resulting in a per-unit consumption that's notably higher than the average private car. Furthermore, the market's inclination towards gasoline engines not only favors passenger-car motor oils but also enhances profitability for blenders, given the higher margins compared to diesel formulations.

Mandatory 10,000-Kilometer Oil-Change Reminder Program

SASO’s technical regulation links dashboard alerts to mineral and synthetic drain intervals, standardizing consumption and closing the gap exploited by cost-conscious drivers who once stretched intervals. OEM warranty clauses make adherence non-negotiable, indirectly enforcing compliance without heavy government policing. Quick-lube chains and dealership bays capture stable traffic, as seen in Petromin’s expanding network that now serves both internal-combustion and EV customers. The 10,000-kilometer threshold nudges fleets toward mid-priced semi-synthetics that meet interval rules at modest premiums, balancing cost and protection.

Growing Synthetic-Oil Penetration in Harsh-Climate Fleets

In the Eastern Province, where summer temperatures soar past 50 °C, mineral oils degrade rapidly, limiting practical drain intervals under severe duty[2]Lubrizol Corporation, “High-Temperature Engine-Oil Performance,” lubrizol.com. In contrast, fully-synthetic PAO or Group III+ oils resist oxidative stress, allowing for extended drain intervals. This not only reduces downtime but also comes at a price premium. Major automakers like Audi, Volkswagen, and Jaguar Land Rover have taken a firm stance, voiding powertrain warranties if non-synthetic oils are used, further solidifying the trend of synthetic adoption in premium vehicle segments. On the ground, construction and logistics fleets are opting for synthetic oils to sidestep expensive engine failures, especially on high-stakes mega-project sites. Meanwhile, Aramco is strategically supplying Group II/III base oils to local blenders, effectively capturing an integrated margin in the process.

E-Commerce Platforms Offering Same-Day Lubricant Delivery

Noon.com, with its roster of multiple API-approved brands, ensures swift deliveries to Riyadh and Jeddah within hours. This service spares do-it-yourself buyers from the hassle of workshop visits. While shipping fees apply, the advantages of time savings and clear specifications tilt the pricing power in favor of consumers. Traditional distributors now face pressure to either align with online pricing or enhance their offerings, such as introducing services like used-oil disposal. Furthermore, the marketplace model paves the way for niche brands, leading to a fragmented market share and heightened competition.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising EV share in government fleets | -0.7% | NEOM, Riyadh, Jeddah urban cores | Medium term (2–4 years) |

| Counterfeit lubricant crackdown shrinking gray market | -0.4% | National, acute in border regions, and informal retail | Short term (≤ 2 years) |

| Industrial re-refining capacity eating into virgin demand | -0.5% | Yanbu, Jeddah industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising EV Share in Government Fleets

Lucid has struck a deal to supply electric vehicles (EVs), while the Public Investment Fund has committed significantly to battery-electric mobility. These moves indicate a significant shift in the fleet landscape. NEOM, with its charging stations and a pioneering robotaxi initiative, is actively testing operations devoid of traditional lubricants. Riyadh aims for increased penetration of EVs by 2030. This ambition translates to the removal of engine and transmission lubricants from vehicles, driving per-unit lubricant consumption close to zero. While blenders are introducing e-axle greases and thermal-management fluids, the volumes remain modest. Moreover, as OEMs increasingly bundle these fluids within service contracts, the potential for aftermarket sales diminishes.

Counterfeit-Lubricant Crackdown Shrinking Gray Market

SAIP and the Ministry of Commerce confiscated counterfeit items. Penalties have escalated, accompanied by potential jail time. Retailers in border areas, previously selling unbranded oils at significant discounts, are now exiting the market. This shift diminishes headline volume but enhances overall quality. The SABER platform, introduced by SASO, mandates viscosity and flash-point reports prior to customs clearance. This requirement not only inflates compliance costs but also favors established brands that can easily obtain the necessary certifications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Passenger Dominance Persists, Commercial Growth Accelerates

Passenger vehicles generated 93.17% of the 2025 volume, underlining the private-car reliance that shapes the Saudi Arabia Automotive Lubricants market. Ride-hailing fleets amplify lubricant intensity, cycling through oil changes every 30–45 days. An aging passenger fleet tilts toward mineral and semi-synthetic oils, yet warranty rules on newer models sustain synthetic demand.

Commercial vehicles contribute a smaller absolute volume yet are forecast to expand at a 6.89% CAGR, outpacing the overall Saudi Arabia Automotive Lubricants market size as NEOM, the Red Sea Project, and King Abdullah Port propel freight and off-highway equipment needs. OEM-approved heavy-duty formulations and extended drain intervals make commercial demand more service-channel dependent and less sensitive to counterfeit supply.

By Product Type: Automatic Transmission Fluids Lead Growth

Automotive Engine oils held 91.88% of the 2025 volume, reflecting universal usage across the fleet. Automatic-transmission high penetration drive a 6.30% CAGR for automatic transmission fluids, which require tighter OEM-specific fluid tolerances. The Saudi Arabia Automotive Lubricants market size for transmission fluids benefits from higher price points and more frequent changes triggered by thermal stress in stop-start urban traffic.

Greases and other product types serve niche industrial and construction segments where volumes are modest, but margins are rich. In response to re-refined displacement in hydraulics, blenders pivot toward higher-spec transmission fluids where OEM approvals preserve pricing power.

Geography Analysis

Riyadh, Jeddah, and the Eastern Province, together accounting for the majority of the nation's consumption, anchor Saudi Arabia's automotive lubricants market. While Riyadh sets an EV target for 2030, presenting a localized challenge, the city's extensive intercity travel ensures that internal-combustion vehicles remain prevalent in corporate fleets.

During Hajj and Umrah, Jeddah sees a surge in lubricant demand. Rental fleets and tour buses, aiming to cater to the influx of pilgrims, hasten their service intervals. To sidestep shortages, distributors are advised to pre-stock, especially with the 5W-30 low-SAPS oils favored by newer gasoline sedans.

In the Eastern Province, a thriving petrochemical hub fuels the demand for high-viscosity hydraulic and gear oils. Additionally, with the desert's sweltering heat, fleets are increasingly opting for synthetic formulations that retain viscosity even at high temperatures.

With NEOM's construction phase underway, there's a pronounced demand for off-highway lubricants. This demand is more closely linked to equipment service hours than traditional mileage metrics. Moreover, the commercial-vehicle lubricant turnover sees a boost from the Red Sea Project and the freight corridors of King Abdullah Port.

While rural areas still host informal workshops, the Saudi Authority for Intellectual Property's (SAIP) crackdown on counterfeits is bridging the quality divide. As a result, even those with tighter budgets are gravitating towards certified semi-synthetics.

Value Chain Analysis

Saudi Arabia's automotive lubricants value chain is anchored by domestic base-oil production and increasingly localized downstream manufacturing. Saudi Aramco Base Oil Company (Luberef) is a key upstream node, supplying base oils from Yanbu into local and in-country blending ecosystems that include Al Jomaih & Shell Lubricating Oil Company (JOSLOC), Petromin Corporation, and international brands operating through local entities and distributors. Feedstock reliability and integration are central themes, with Luberef executing a scheduled turnaround at Yanbu in late 2025 and resuming operations in January 2026 after a 45-day shutdown that also included expansion-related work.

Midstream blending, packaging, and distribution depend on branded service networks (dealerships, quick-lube, and service centers) and on rising e-commerce fulfillment in major cities, which compresses traditional distributor margins while widening SKU availability. On the downstream side, partnerships that tie OEM- or fleet-linked demand to local production and service points are gaining visibility, exemplified by JOSLOC's agreement with Abdul Latif Jameel for Oils to produce and supply Toyota Genuine Oils in Saudi Arabia. Cross-border imports still support certain high-spec fluids and additive components, but conformity and customs clearance requirements under SASO technical regulations (including CoC documentation) add compliance steps that tend to favor established suppliers and formal channels.

Competitive Landscape

The Saudi Arabian automotive lubricants market is moderately consolidated. Global majors compete with regional leaders, leveraging OEM endorsements and retail breadth to hold share. E-commerce disruptors like noon.com erode distributor margins yet expand consumer choice, forcing incumbents to bundle installation and disposal services. Samref's 2025 petrochemical upgrade underscores capital intensity and the strategic importance of feedstock self-sufficiency. The absence of recycled-content mandates shields virgin-oil incumbents for now, but a policy pivot could quickly alter cost dynamics.

Saudi Arabia Automotive Lubricants Industry Leaders

Shell plc

Exxon Mobil Corporation

BP plc (Castrol)

Petromin Corporation

TotalEnergies

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Premiumization opportunities are most visible where OEM warranty clauses, harsh operating conditions, and tighter specifications intersect, supporting demand for higher-performance engine oils and OEM-specific fluids, particularly for automatic transmissions. As SASO-linked conformity requirements tighten, including Certificate of Conformity needs for customs clearance, volume continues to shift toward branded and certified lubricants away from informal supply. This creates room for players that can sustain documented quality, traceability, and consistent availability.

On the supply side, in-Kingdom industrialization initiatives and new downstream building blocks support further localization of the lubricant bill of materials beyond blending. Luberef is advancing capacity and ecosystem enablement in Yanbu, including its LubeHUB value park with piped base-oil access for tenant manufacturers, while new agreements such as Apar Industries Middle East Limited signing a base oil supply agreement with Luberef (June 2026) position Yanbu as a feedstock and manufacturing hub. In additives, the Farabi Downstream Petrochemical Company and Xinxiang Richful Lube Additive Co. project in Yanbu to localize detergent, dispersant, and ZDDP production signals a pathway to reduce dependence on imported additive packages, which can improve lead times and support faster rollout of newer API and ILSAC-aligned formulations in the Saudi aftermarket and service-channel landscape.

Recent Industry Developments

- June 2026: Al Jomaih & Shell Lubricating Oil Company (JOSLOC) expanded its co-branded service center network with Leader Express across Saudi Arabia. The move strengthens route-to-market control by linking lubricant supply to installed service capacity, supporting repeat oil-change capture and brand preference at the point of service.

- February 2026: Al Jomaih & Shell Lubricating Oil Company (JOSLOC) signed a strategic lubricants supply agreement with Al Nakhlah National Company (NANCO) to support fleet operations. Fleet-linked supply arrangements consolidate volumes into formal channels and increase the importance of OEM-appropriate specifications and consistent availability across multi-site operations.

- January 2025: Al Jomaih & Shell Lubricating Oil Company (JOSLOC) agreed with Abdul Latif Jameel for Oils to produce and supply Toyota Genuine Oils in Saudi Arabia. Localizing an OEM-branded lubricant program tightens the connection between warranty-driven service behavior and domestically supplied product, increasing competitive pressure on third-party engine-oil brands in dealership-adjacent channels.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers lubricants consumed in on-road vehicles in Saudi Arabia, counted as product volumes used during maintenance and repair cycles across passenger vehicles, commercial vehicles, and motorcycles.

Scope exclusions: This sizing excludes industrial lubricants, marine and aviation lubricants, and lubricants used in off-highway equipment where the use is not tied to road vehicles.

Segmentation Overview

- By Vehicle Type

- Passenger Vehicles

- Commercial Vehicles

- Motorcycles

- By Product Type

- Automotive Engine Oils

- 0W-XX

- 5W-XX

- 10W-XX

- 15W-XX

- Monogrades

- Other Grades

- Manual Transmission Fluids (MTF)

- Automatic Transmission Fluids (ATF)

- Brake Fluids

- Automotive Greases

- Other Product Types (Power Steering Fluid etc.)

- Automotive Engine Oils

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clear demand context, so we reviewed public vehicle and mobility indicators and then mapped them to lubricant use in the country. Common sources used include official statistics and policy releases such as the General Authority for Statistics (GASTAT), Saudi Central Bank (SAMA) macro series, and transport and road safety updates from the Ministry of Transport and the national traffic authority.

To keep the product side grounded, we also checked trade and flow signals such as UN Comtrade for lubricant-related import and export patterns, and technical references from SAE and API for viscosity grades and service categories that influence drain intervals. Company annual reports, investor presentations, association websites, and reputable press coverage helped confirm channel mix and portfolio focus, followed by selective use of paid subscriptions for company financials and intelligence, patent coverage, and shipment-level import-export views where it supported cross-checking. The desk sources listed here are illustrative rather than exhaustive, and many other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary discussions were used to pressure-test the demand model against real service behavior, especially for oil change frequency, average sump fill, and differences between retail and workshop-led purchasing. We spoke with a mix of lubricant suppliers, distributors, workshop operators, fleet and maintenance leads, and informed industry experts across the major demand centers in the country, and then we rechecked any wide spreads in assumptions through follow-up calls.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 18% | |

| Mid tier: 43% | Functional/Unit leaders: 23% | |

| Smaller Players: 19% | Managers: 59% |

Market-Sizing & Forecasting

Sizing is built mainly from a top-down demand pool, where the national vehicle parc and annual usage patterns are translated into lubricant consumption in liters, and then split across the main automotive product families. To keep the outputs realistic, the totals are corroborated using selective bottom-up checks such as sampled workshop throughput, channel checks on pack sizes, and supplier shipment directionality, and then the model is adjusted when the two views do not align.

Key inputs used in the model include the in-use vehicle population by vehicle type, annual mileage and utilization trends (especially for fleets), typical drain intervals by engine oil service category, average sump fill and top-up behavior, and the share of synthetic versus mineral blends that affects change frequency and volume per service. Transmission fluid and grease volumes are estimated using replacement cycles and maintenance intensity, and gaps are handled by using ranges from interviews and then narrowing them based on consistency across multiple respondent groups.

For the forecast, we used scenario analysis supported by simple time-series smoothing on the core drivers, because lubricant demand is influenced by both vehicle growth and maintenance norms. The scenarios were anchored to expected changes in vehicle parc growth, vehicle usage, and service interval evolution, and then reconciled with what interviewees consider plausible in the next five years.

Data Validation & Update Cycle

Model outputs are checked against independent signals, including vehicle parc movement, lubricant trade direction, and implied per-vehicle consumption levels, so any extreme outcomes are flagged early. When a mismatch shows up, we revisit the driver assumptions, check unit consistency, and re-contact relevant participants to confirm whether the change is real or an input issue.

Before sign-off, the work goes through step-by-step analyst review, including variance checks versus historical patterns and cross-segment totals. Reports are refreshed annually, and interim updates are done when material events can shift demand, such as policy changes, sharp import swings, or major shifts in vehicle sales and usage. Before delivery, a final analyst pass is completed so clients receive an up-to-date view.

Mordor Intelligence's Saudi Arabia Automotive Lubricants Market Estimate Compared With Other Published Estimates

Published market sizes can vary even when they use similar labels, because some sources size only engine oils, others report total lubricants, and several mix workshop consumption with retail sell-in without stating it clearly. Differences also come from whether the number is shown as volume or revenue, and how currency timing is handled when prices are volatile.

By tracking drain intervals, average sump fill, and annual vehicle parc updates, Mordor Intelligence keeps the Saudi Arabia automotive lubricants total tied to liters consumed across engine oils, transmission fluids, brake fluids, greases, and other in-vehicle fluids, rather than leaving out smaller product types.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 402.79 M (2025) | |

| Industry Association A | USD 365.00 M (2025) | Often reflects a narrower basket that leans toward engine oils and may exclude smaller automotive product types such as brake fluids and greases, which lowers the total when expressed as a single market number. |

| Trade Journal B | USD 455.00 M (2026) | Commonly uses revenue proxies or distributor sell-in signals and then converts to an implied volume, which can overstate demand when pricing assumptions, currency timing, or channel stocking effects are not separated. |

The spread in the table is mainly explained by what is counted as automotive lubricants and whether the estimate follows consumption in use or a sales-value proxy. Our approach stays traceable because each step links back to vehicle activity, maintenance cycles, and product replacement behavior, which makes the final total easier to replicate and update.

Key Questions Answered in the Report

What is the size of the Saudi Arabian Automotive Lubricants market?

Volume reached 420.56 million liters in 2026 and is expected to reach 521.83 million liters by 2031, registering a CAGR of 4.41%.

How fast will commercial-vehicle lubricant demand grow?

Commercial-vehicle consumption is forecast to post a 6.89% CAGR through 2031.

Why are synthetics gaining share?

OEM warranty mandates and high-temperature stability drive a projected 6.49% CAGR for fully-synthetic oils.

How is e-commerce affecting lubricant sales?

Same-day delivery from platforms like noon.com widens access and compresses distributor margins.

Page last updated on: