Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

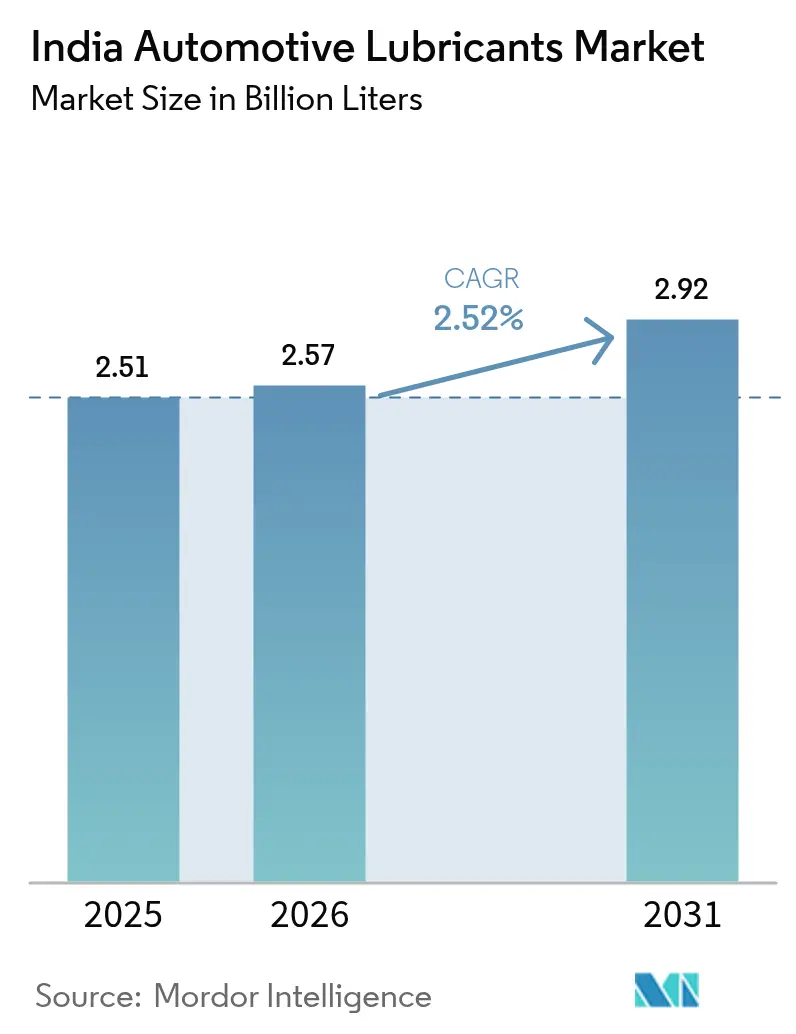

| Base Year Market Size (2025) | 2.51 Billion liters |

| Market Volume (2026) | 2.57 Billion liters |

| Market Volume (2031) | 2.92 Billion liters |

| Growth Rate (2026 - 2031) | 2.52% CAGR |

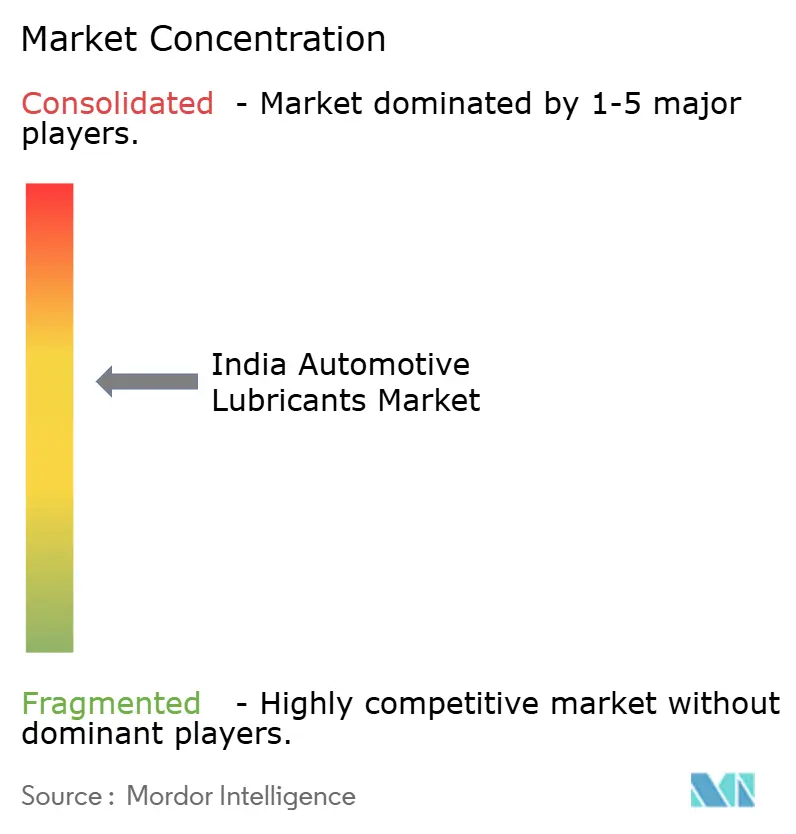

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Automotive Lubricants Market Analysis by Mordor Intelligence

The India Automotive Lubricants Market size was valued at 2.51 billion liters in 2025 and estimated to grow from 2.57 billion liters in 2026 to reach 2.92 billion liters by 2031, at a CAGR of 2.52% during the forecast period (2026-2031). Continuing vehicle parc growth, premiumization triggered by BS-VI emission norms, and OEM factory-fill tie-ups underpin volume stability despite the escalating electrification. Synthetic formulations command higher average selling prices, lifting value even as drain intervals lengthen. Supply-side competition is intensifying as international majors expand blending capacity and state-owned oil marketing companies (OMCs) increase their rural reach. Margin management remains challenging because India imports most of its base oil requirements, exposing blenders to volatile global prices and exchange rate swings.

Key Report Takeaways

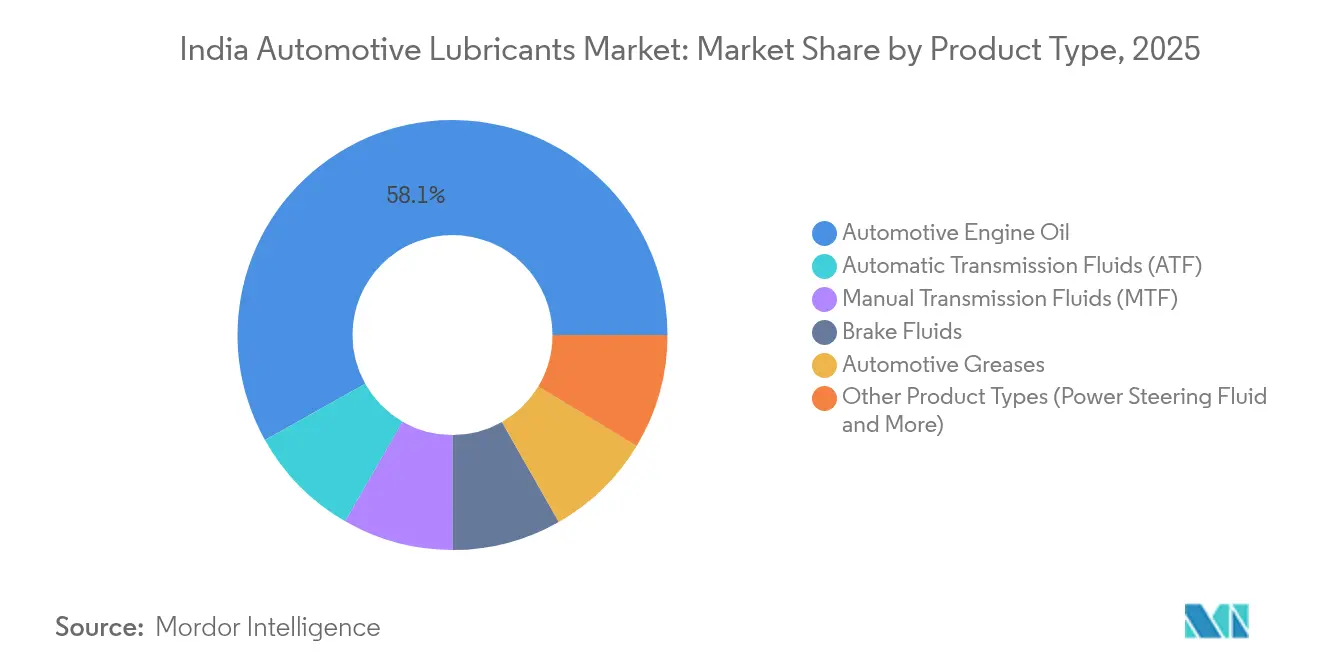

- By product type, automotive engine oils led with 58.12% of India automotive lubricants market share in 2025. Automatic transmission fluids (ATF) are forecast to expand at a 2.63% CAGR to 2031.

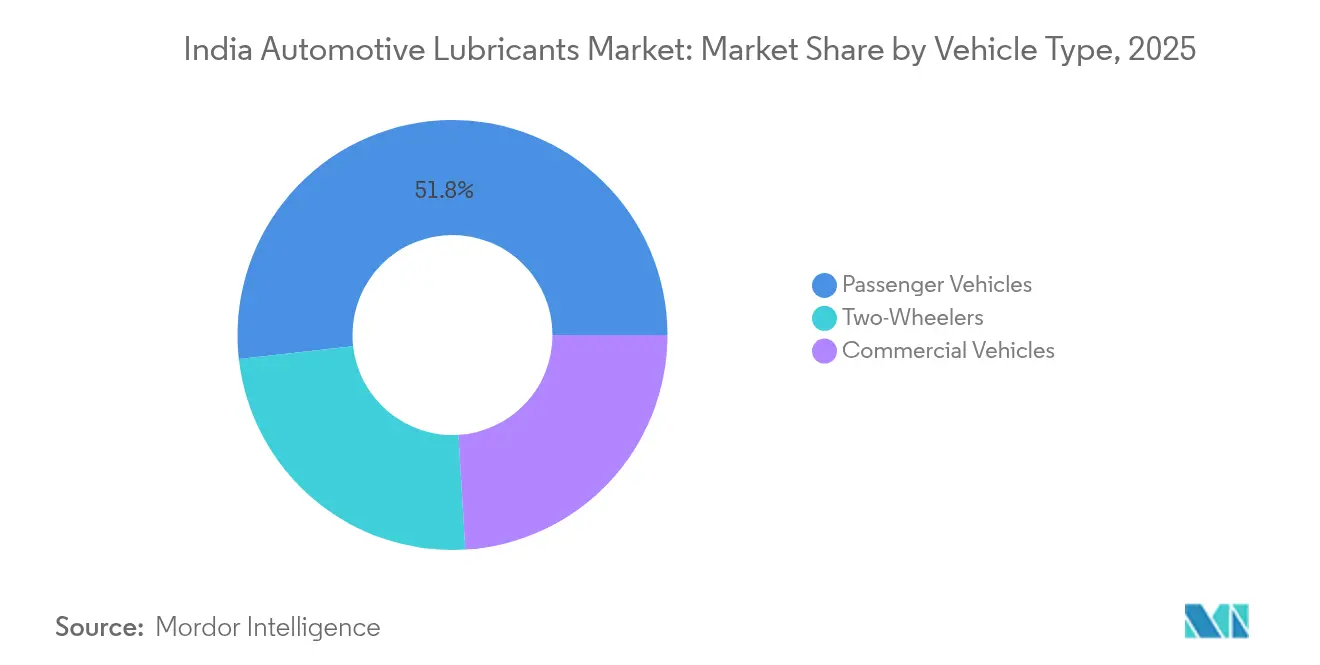

- By vehicle type, passenger vehicles captured 51.78% of India automotive lubricants market share in 2025. Commercial vehicles are projected to post the fastest 2.69% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising vehicle parc and passenger-car sales | +1.2% | National, with concentration in Tier-1 and Tier-2 cities | Medium term (2-4 years) |

| Two-wheeler penetration surge in rural India | +0.8% | Rural India, particularly North and East regions | Long term (≥ 4 years) |

| Shift to high-performance synthetics post-BS-VI | +0.9% | National, with early adoption in urban centers | Short term (≤ 2 years) |

| OEM factory-fill tie-ups expanding lubricant volume | +0.6% | Manufacturing hubs: Chennai, Pune, Gurgaon, Aurangabad | Medium term (2-4 years) |

| Growth of shared-mobility fleets driving higher churn | +0.4% | Metro cities and Tier-1 urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Vehicle Parc and Passenger-Car Sales

Passenger-car production rebounded 9.9% in FY 2024 as GDP grew 8.2% and consumer sentiment recovered[1]World Bank, “India Development Update,” worldbank.org. New models, especially compact SUVs, stimulate first-fill demand for API SP synthetics, and higher power-to-weight ratios necessitate premium lubricants for thermal stability. Recurring aftermarket volumes follow because the average Indian light vehicle clocks 12,000 km annually, still requiring two to three oil changes a year despite extended drain intervals. Dealer service programs bundle branded lubricants, improving compliance with OEM-recommended grades. Consequently, India automotive lubricants market benefits from both initial factory fills and sustained workshop demand cycles.

Two-Wheeler Penetration Surge in Rural India

Rising rural incomes and improved road connectivity, facilitated by the Pradhan Mantri Gram Sadak Yojana, continue to boost two-wheeler ownership, with motorcycles and scooters serving as the primary means of mobility. Frequent oil-change intervals of 3,000-4,000 km generate recurring lubricant demand. Penetration remains highest for 100-125 cc models, many of which still use mineral or semi-synthetic oils, preserving volume even as urban consumers shift to electric variants. Market leaders Hero MotoCorp and Honda sustain outreach programs through village-level mechanics, enabling branded lubricant companies to deepen rural distribution. The two-wheeler segment, therefore, anchors volume resilience for the India automotive lubricants market in lower-income geographies.

Shift to High-Performance Synthetics Post-BS-VI

BS-VI norms lowered the diesel sulfur content to below 10 ppm and tightened NOx limits, driving OEM specifications toward low-SAPs and high-VI synthetic oils. Laboratory studies show that multifunctional hydrocarbon additives reduce friction by 55% and improve brake thermal efficiency by 15.2%, validating the shift to API SP and ILSAC GF-6 lubricants. Synthetic formulations command a 25-35% price premium yet enable longer drain intervals—up to 15,000 km for premium cars—improving lifetime cost of ownership. As consumer awareness of engine durability rises, penetration of fully synthetic passenger-car motor oils climbs in metros and gradually spreads to Tier-2 cities, lifting value across India automotive lubricants market.

OEM Factory-Fill Tie-Ups Expanding Lubricant Volume

Automakers are increasingly nominating exclusive lubricant partners to ensure supply chain certainty and secure co-branding benefits. Savita Oil Technologies, for example, aims to capture a 5% share of the India automotive lubricants market by 2028 through alliances with Hero MotoCorp, Mahindra & Mahindra, and Tata Motors[2]Autocar Professional, “Savita Oil Targets 5% Share via OEM Tie-ups,” autocarpro.in. Factory-fill contracts lock in baseline volumes and enhance aftermarket pull, because owners often repeat the same brand during scheduled services. Partnerships now extend beyond engine oils to transmission fluids and coolants, widening product breadth. For lubricant suppliers, dedicated OEM channels serve as a hedge against retail price wars and provide a platform for launching next-generation EV fluids.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid electrification of 2- & 3-wheelers | -0.7% | Urban centers and government fleet programs | Medium term (2-4 years) |

| Base-oil price volatility | -0.4% | National, affecting all market segments | Short term (≤ 2 years) |

| Push toward re-refined base oils reducing virgin demand | -0.2% | Industrial clusters and environmentally conscious regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Electrification of 2- & 3-Wheelers

FAME-II incentives and state-level subsidies have accelerated the adoption of electric scooters and three-wheelers for last-mile deliveries. Electric powertrains eliminate engine oil requirements and reduce transmission fluid volumes, thereby reducing traditional lubricant consumption. Still, EVs introduce new niches—dielectric coolants for battery thermal management and low-viscosity gear oils for single-speed reducers. Savita Oil Technologies recently commercialized synthetic ester fluids targeting these applications. While overall volume impact remains modest to 2030, the restraint trims growth of conventional segments within India automotive lubricants market.

Base-Oil Price Volatility

India imported 2.71 million tonnes of base oils in 2024, a 14.6% year-over-year jump, with South Korea supplying 1.15 million tonnes. Supply disruptions from refinery turnarounds and geopolitical tensions swing Group II and Group III prices, compressing blender margins. OMCs hedge through long-term contracts, but independent players face working capital strains and may pass costs on to distributors, risking share losses in the price-sensitive retail channel. Volatility therefore suppresses near-term profitability and dampens aggressive capacity additions in India automotive lubricants market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine Oil Dominance Amid ATF Acceleration

India automotive lubricants market size for engine oils totaled 58.12% share of total volumes in 2025. API SP and ILSAC GF-6 formulations are gaining traction because BS-VI engines require improved oxidation resistance and piston cleanliness. Fully synthetic variants fetch 30% higher prices, lifting segment value despite flat volumes. Fleet trials show a 2 % fuel-economy gain using low-viscosity 0W-20 oils, encouraging adoption across ride-hailing fleets in metropolitan areas. Historical comparisons reveal that the share of engine oil is declining marginally as specialty fluids expand, yet the segment remains the anchor of India's automotive lubricants market.

Automatic transmission fluids constitute a smaller but fastest-growing pocket, with projected volumes rising at a 2.63% CAGR through 2031. Growth stems from the rising penetration of CVT and AMT gearboxes in compact cars and SUVs. OEMs also shift city-bus fleets to six-speed automatics, spurring demand for TES-295-grade fluids capable of 120,000 km service intervals. Blenders invest in premium Group III and PAO-based ATFs to meet torque-converter oxidation tests. As a result, ATFs increasingly diversify product portfolios and improve average realizations within India automotive lubricants market size calculations.

By Vehicle Type: Commercial Vehicles Drive Growth Momentum

Passenger cars accounted for 51.78% of volumes in 2025, driven by urbanization and gains in disposable income. OEM-authorized service networks encourage the use of warranty-compliant synthetics, and maintenance package subscriptions enhance stickiness. Yet, growth moderates because electrification and ride-sharing curb new-car sales in some metropolitan areas. Consequently, passenger-car lubricant volumes expand slowly, although premium grades sustain value.

Commercial vehicles are expected to deliver the fastest growth, with segment volumes forecasted to rise at a 2.69% CAGR to 2031, outpacing the overall India automotive lubricants market growth rate. Government infrastructure spending under PM Gati Shakti expands road freight, and fleet owners adopt API CK-4 oils, which allow for 60,000 km drain intervals, thereby lowering downtime. Despite lengthier intervals, high annual mileage keeps lubricant consumption buoyant. The transition to multi-axle tractors and higher-tonnage urban delivery trucks also increases fill volumes per vehicle. These trends ensure commercial vehicles remain critical demand drivers for India automotive lubricants market share evolution.

Geography Analysis

Western India led consumption, anchored by automotive hubs in Pune, Aurangabad, and the Mumbai-Ahmedabad industrial corridor. The close proximity to Jawaharlal Nehru Port facilitates base-oil imports, and a dense dealer network supports aftermarket sales. In Northern India, Delhi-NCR is a logistics hub, while Punjab and Haryana contribute significant volumes of agricultural machinery that require high-temperature greases for the harvest seasons. Harsh winters intensify the demand for multi-grade 5W-30 oils, reinforcing the trend toward premiumization.

In Southern India, Chennai’s manufacturing cluster stimulates factory-fill demand, and Bangalore’s tech workforce favors SUVs with synthetic oils. Southern consumers exhibit higher brand loyalty, which benefits premium players. Eastern India, comprising West Bengal, Odisha, and Jharkhand, shows above-average growth as highway projects improve connectivity. Coal mining and steel plants in Odisha generate ancillary industrial-lubricant demand that shares logistics infrastructure with automotive products, enabling cost synergies for distributors.

Regional share patterns have shifted marginally since 2020: western and southern regions remain stable, while northern and eastern footprints rise as vehicle ownership spreads beyond metros. To win in emerging corridors, blenders prioritize rural retail outlets, vernacular mechanic training, and smaller pack sizes. Sustained geographic diversification thus underpins longer-term resilience of India automotive lubricants market size.

Regulatory Landscape

India's automotive lubricants market operates under the Ministry of Petroleum and Natural Gas (MoPNG) oversight for lubricating oils and greases through the Lubricating Oils and Greases (Processing, Supply and Distribution Regulation) Order, 1987, which was amended in May 2024 (GSR 178(E)). Alongside this, BS-VI-driven emissions and fuel-quality compliance has reinforced demand for low-SAPS and higher-performance formulations, increasing the importance of meeting updated lubricant specifications in OEM service channels.

The Bureau of Indian Standards (BIS) shapes standards development and conformance, including the PCD 25 sectional committee covering lubricants and related products. Recent reference points include IS 19110:2025 for hydraulic fluids and ongoing work on specifications for virgin and re-refined base oils (PCD 25 (22088)). Public procurement is also guided by the Public Procurement (Preference to Make in India) Order, 2017, updated as recently as March 2024, which supports localization across base oils, additives, blending, and packaging for suppliers serving government-linked fleets and entities.

Value Chain Analysis

The value chain runs from crude and base oil production, through additive supply, blending, and packaging, to distribution via OEM factory fill, dealerships, workshops, and fuel-station retail. India depends heavily on imported base oils (commonly cited at 60-70% of requirements), with inflows concentrated through major gateways such as Jawaharlal Nehru Port (JNPT) and Chennai, exposing blenders to freight costs, foreign exchange movements, and global Group II/III tightness. Additives and high-VI synthetic components are supplied through a mix of domestic production and imports, and they matter more for API SP/ILSAC GF-6 and premium ATF formulations.

Downstream execution is led by OMC networks and large private marketers with nationwide footprints, supported by blending plants, depots, and workshop connectivity. For example, BPCL's lubricant operations include plants such as Loni and Tondiarpet (Chennai), supporting broad SKU coverage, while Castrol India uses a large network of outlets and workshops to extend retail access. A key evolving link is used oil collection and re-refining, where formal aggregation from workshops and fleets is becoming a competitive capability to reduce reliance on virgin base oils and improve compliance readiness within circularity and EPR-oriented initiatives.

Competitive Landscape

India automotive lubricants market is moderately concentrated. Oil Marketing Companies (OMCs) operate over 80,000 fuel-station forecourts nationwide, offering loyalty rewards and price promotions. International majors differentiate themselves through Group III-plus synthetics, co-branded OEM lines, and extended drain guarantees. TotalEnergies and FUCHS target niche markets, such as transmission fluids and mining greases, by gaining footholds through industrial OEM approvals. Sustainability emerges as a battleground, with re-refined base-oil blends and bio-based esters featuring in new launches. Collectively, these strategies indicate a market evolving toward higher value and technological sophistication.

India Automotive Lubricants Industry Leaders

Indian Oil Corporation Ltd

BP p.l.c.

Bharat Petroleum Corporation Limited

HP Lubricants

Shell plc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Import dependence in base oils, together with the shift toward higher-spec synthetic lubricants aligned to BS-VI service needs, is creating scope for more local Group II/III base stock production, specialty additives, and premium finished lubes. Capacity and capability investments across the supply chain support this, including CPCL beginning work on a lube oil base stock unit at Manali Refinery (Rs 1,600 crore) to produce Group II and III base oils (242,000 tonnes per annum), and LANXESS announcing a Rs 150 crore specialty lubricant additives blending plant at Jhagadia, Gujarat. Expansion activity at finished-lube manufacturers also indicates room for deeper localization and faster lead times for premium engine oils, ATFs, and specialty fluids.

Circularity further opens an opportunity in used oil collection, re-refined base oil integration, and compliant take-back models that connect OMCs, OEMs, workshops, and recyclers. Recent partnerships, including HPCL with Tata Motors on used lubricant collection and recycling pilots and BPCL with IFP Petro on used oil collection and re-refining, point to efforts to convert fragmented used-oil flows into predictable RRBO feedstock. For lubricant marketers, these steps can underpin more differentiated propositions around sustainability and quality assurance for re-refined inputs, alongside ongoing premium product pushes such as newer synthetic portfolios and OEM-aligned service grades.

Recent Industry Developments

- July 2026: Bharat Petroleum Corporation Limited (BPCL) signed an MoU with IFP Petro Products Pvt. Ltd. to build a nationwide used lubricating oil (ULO) collection and re-refining ecosystem. The collaboration formalizes feedstock collection and processing pathways, strengthening circular supply options for base oil inputs and supporting compliance-led initiatives in the lubricants value chain.

- June 2026: IndianOil launched the SERVO HYPER SERIES premium lubricant portfolio, developed at its Faridabad R&D Centre and positioned around advanced synthetic base oils and additive technology. The launch expands IndianOil's premium lineup for BS-VI-aligned service requirements and increases competitive intensity in higher-margin synthetic engine oil segments.

- July 2025: Shell acquired 100% equity in Mumbai-based Raj Petro Specialities from Brenntag Group, adding manufacturing facilities in Chennai and Silvassa. The acquisition strengthened Shell's India lubricants footprint through added local manufacturing capacity and a wider product and customer base, supporting faster response to OEM and aftermarket requirements.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers automotive lubricants consumed in India for on-road vehicles, measured as lubricant volume sold into OEM fill and the replacement market, across passenger vehicles, commercial vehicles, and two-wheelers.

Scope exclusions: It excludes industrial lubricants and process oils, along with lubricants used mainly in marine, rail, aviation, agriculture, mining, and construction equipment.

Segmentation Overview

- By Product Type

- Automotive Engine Oil

- 0W-XX

- 5W-XX

- 10W-XX

- 15W-XX

- Monogrades

- Other Grades

- Manual Transmission Fluids (MTF)

- Automatic Transmission Fluids (ATF)

- Brake Fluids

- Automotive Greases

- Other Product Types (Power Steering Fluid etc.)

- Automotive Engine Oil

- By Vehicle Type

- Passenger Vehicles

- Commercial Vehicles

- Two-Wheelers

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the demand context and to anchor the model inputs to public data series. We reference official datasets such as the Ministry of Road Transport and Highways vehicle registrations, Society of Indian Automobile Manufacturers production and sales releases, Petroleum Planning and Analysis Cell fuel consumption indicators, and customs trade statistics that signal base oil and additive flows. Where it supports assumption building, standards direction from BIS and technical references such as SAE publications are reviewed to understand drain intervals and lubricant grades.

On top of that, company annual reports, investor presentations, and reputed press items are reviewed to track channel shifts (OEM versus aftermarket) and pricing signals over time. A paid subscription for company financials and intelligence helps verify manufacturer and distributor scale, and a lubricants-specific market database is used selectively for product mapping and blend type context. The sources listed here are illustrative, and many other public references were also used for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary interviews are used to test assumptions that are not directly visible in public datasets, especially around drain intervals, sump fills, top-up behavior, and trade margins by channel. We speak with lubricant formulators and blenders, distributors and workshops, fleet operators, and OEM-adjacent stakeholders across major consuming corridors in India so the model reflects real buying patterns and service behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 13% | |

| Mid tier: 48% | Functional/Unit leaders: 30% | |

| Smaller Players: 16% | Managers: 57% |

Market-Sizing & Forecasting

Sizing starts with a top-down demand pool build using India vehicle parc and annual activity indicators, and then it is translated into lubricant consumption by applying service intervals, sump capacities, and typical top-up behavior by vehicle class. The key inputs include active vehicle parc by category, annual kilometers or utilization patterns, average drain intervals influenced by BS-VI service practices, product mix across engine oil versus transmission and gear oils and greases, and pack-size mix that affects apparent volume movement through retail.

The totals are then checked with selective bottom-up approximations, such as sampling major channel flows, using workshop and distributor throughput checks, and testing implied liters per vehicle against service norms. When a data point is missing for a smaller sub-pocket, we use proxy ratios from similar vehicle cohorts and then correct them through interview feedback so the overall number does not get overstated. Forecasts rely on scenario-based modeling tied to expected vehicle parc changes, utilization trends, and drain interval normalization. The pace of mix shift toward higher performance grades is treated as a separate sensitivity rather than assumed flat.

Data Validation & Update Cycle

Outputs are validated through multi-step checks, starting with unit consistency tests and variance reviews across vehicle categories and lubricant types. We compare implied consumption per vehicle with service practice benchmarks, and then recheck the largest assumptions when the model shows unusual jumps versus historical vehicle activity and lubricant movement signals.

Before sign-off, a second analyst review is completed to confirm formulas, conversions, and whether any assumption is double counted across OEM fill and replacement. Reports are refreshed annually, and interim revisions are made when material events occur, such as regulation-led grade changes or sharp shifts in vehicle production. Prior to delivery, a final pass is done so clients receive an updated view that reflects the latest public releases and re-validated inputs.

Mordor Intelligence's India Automotive Lubricants Market Size Versus Other Published Estimates

Published estimates for India automotive lubricants can look far apart because the scope is not always kept the same, and the unit of measure is sometimes mixed between liters and USD. Differences also come from how firms treat channel coverage (OEM fill versus aftermarket), how they apply pricing changes, and whether the vehicle parc and service interval assumptions are re-checked with industry participants.

Some external figures present the market as a value number that can fold in adjacent fluids and retail margin effects, and then the total moves mainly with price and mix assumptions. Estimates on a liters basis stay closer to vehicle parc, drain intervals, and sump fills, which reduces distortion from short-term price swings and keeps the total tied to service behavior.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.51 B (2025) | |

| Industry Data Provider A | USD 3.60 B (2024) | Reported in USD value and appears to include a broader product basket and channel margin assumptions, so the total can rise with pricing and mix even if underlying liters grow slowly. |

| Industry Research Publisher B | USD 2.74 B (2025) | Value-based estimate that can be sensitive to assumed price progression and grade upgrade rates, and it may treat distribution shifts as direct market expansion rather than separating volume from value effects. |

The table points to a unit and scope gap, since value-based totals can move quickly with pricing, mix, and margin assumptions. Some sources also group in adjacent automotive fluids, and Mordor Intelligence counts only lubricant consumption tied to vehicle parc and service intervals, which keeps the model traceable to liters and repeatable checks.

Key Questions Answered in the Report

How fast is India automotive lubricants market expected to grow to 2031?

Volumes are projected to rise from 2.57 billion liters in 2026 to 2.92 billion liters by 2031, reflecting a 2.52% CAGR.

Which product segment generates the most demand?

Engine oils dominate with 58.12% share in 2025 due to India’s large ICE vehicle base and BS-VI-driven switch to synthetics.

What is the biggest growth opportunity by vehicle category?

Commercial-vehicle lubricants are forecast to expand at 2.69% CAGR through 2031, benefiting from freight growth under PM Gati Shakti.

How will electrification affect lubricant sales?

EV adoption trims engine-oil volumes, especially in two- and three-wheelers, but opens niches for dielectric coolants and low-viscosity gear oils.

Page last updated on: