Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | 502.63 Million liters |

| Market Volume (2026) | 513.49 Million liters |

| Market Volume (2031) | 571.62 Million liters |

| Growth Rate (2026 - 2031) | 2.16% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pakistan Lubricants Market Analysis by Mordor Intelligence

Pakistan Lubricants Market size in 2026 is estimated at 513.49 million liters, growing from 2025 value of 502.63 million liters with 2031 projections showing 571.62 million liters, growing at 2.16% CAGR over 2026-2031. Stable industrial recovery, infrastructure spending tied to the China-Pakistan Economic Corridor, and steady vehicle parc growth are anchoring demand. Heightened power generation activity, capacity additions in refining and blending, and a gradual shift toward synthetic grades are further supporting volume expansion. Strategic retail and blending investments by multinationals underline long-run confidence despite currency volatility and energy constraints. A surge in e-commerce-driven logistics, stricter equipment performance standards, and supportive tariff reforms are opening premium opportunities for early movers within the Pakistan lubricants market.

Key Report Takeaways

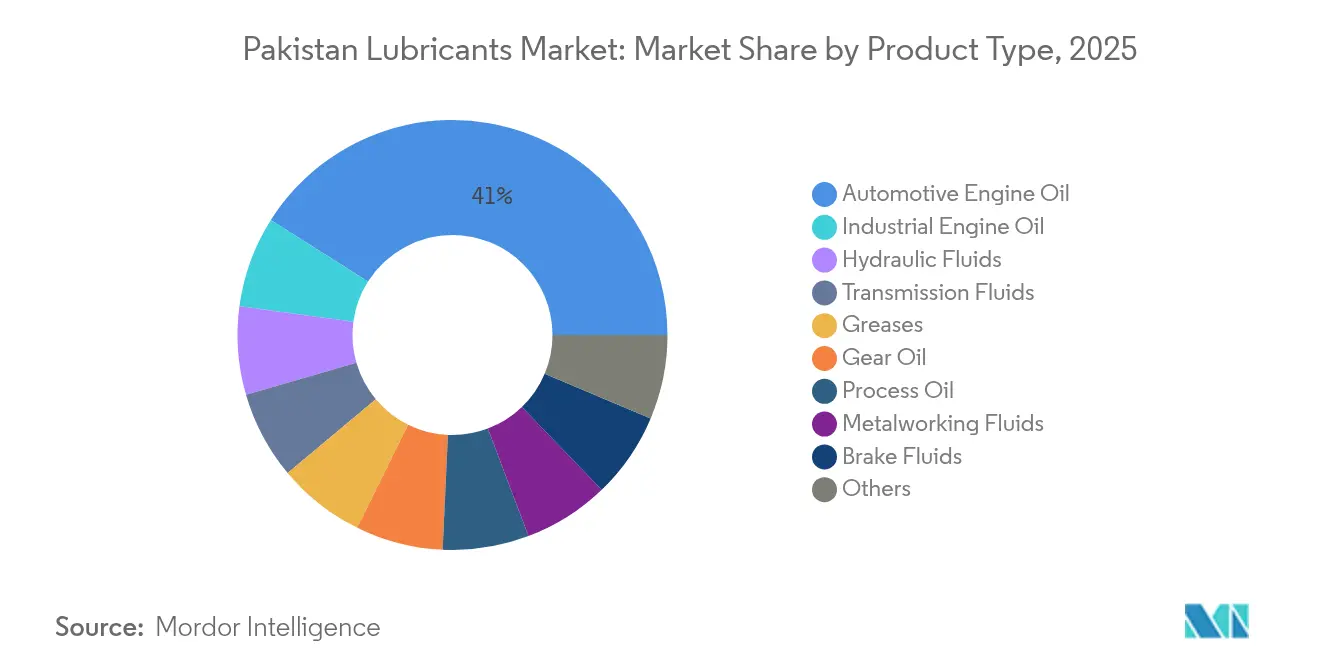

- By product category, automotive engine oil led with a 41.02% share of the Pakistani lubricants market in 2025; industrial engine oil is forecast to expand at a 2.29% CAGR through 2031.

- By end-user industry, the automotive segment accounted for 54.01% of the Pakistan lubricants market size in 2025, while industrial applications are projected to advance at a 2.18% CAGR through 2031.

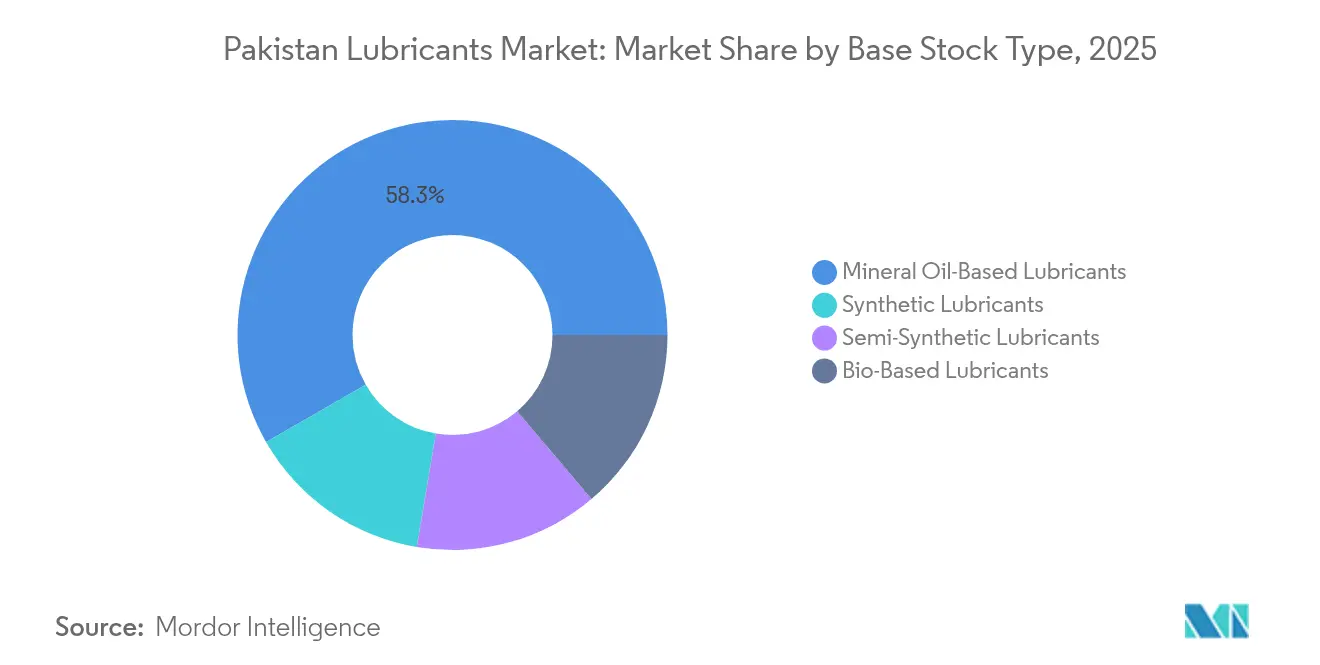

- By base stock, mineral oils captured 58.29% of Pakistan's lubricants market share in 2025; bio-based lubricants posted the fastest growth at a 3.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Pakistan Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Steady recovery in industrial and transportation sectors post-COVID-19 | +0.8% | Punjab and Sindh industrial hubs | Medium term (2-4 years) |

| CPEC-linked growth in trucking and logistics corridors | +0.5% | Along Gwadar–Kashgar route | Long term (≥ 4 years) |

| Industrialisation and new power projects boosting lube consumption | +0.4% | Industrial zones and power sites | Long term (≥ 4 years) |

| Increasing shift toward synthetic lubricants for extended drain intervals | +0.3% | Urban centers and commercial fleets | Medium term (2-4 years) |

| Government incentives for local blending and packaging plants | +0.2% | Karachi, Lahore, Faisalabad | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Steady Recovery in Industrial and Transportation Sectors Post-COVID-19

Manufacturing utilization has rebounded, spurring lubricant offtake in textiles, steel, and petrochemicals. Trucking mileage has normalized, lifting demand for heavy-duty engine oils across Pakistan's lubricants market routes. PSO reported 9.7% growth in lubricant sales for FY 2024, outpacing overall volume expansion, underscoring a resilient end-use demand[1]Pakistan State Oil Company Limited, “PSO leads the market with resilience and growth – posts a profit of 13.4 billion in 9MFY24,” psopk.com . Freight operators are refreshing their fleets, which require higher-specification oils, while power plants running on furnace oil maintain a steady draw for turbine and generator lubricants. Together, these trends sustain baseline volume and tilt usage toward mid-tier synthetic blends across the Pakistan lubricants market.

CPEC-Linked Growth in Trucking and Logistics Corridors

The 3,000 km corridor from Gwadar to Kashgar is creating a dense network of logistics lanes. Extended-haul trucks require premium multigrade oils that can withstand higher thermal loads, which increases the value per liter sold. The construction of roads, ports, and special economic zones requires hydraulic fluids and gear oils for excavators and cranes deployed on site. Chinese contractors often specify global OEM-approved lubricants, positioning international suppliers with local blending ties to capture share. As cross-border freight costs rise, fleet operators favor extended drain formulations that reduce downtime, deepening synthetic penetration within the Pakistani lubricants market.

Industrialisation and New Power Projects Boosting Lube Consumption

Planned and operating thermal plants demand transformer oils, turbine lubricants, and gas-engine oils. Caltex fields GST and HDAX lines that target these niches. Refinery upgrading programs, such as Cnergyico’s USD 1 billion modernization, will require specialty process oils during shutdowns and restart phases. Gains in broader manufacturing sectors, including steel, textiles, and chemicals, increase the demand for metalworking fluids and gear lubricants. Premium formulations are increasingly preferred for critical equipment, helping to migrate volume from basic mineral oils to higher-value lines in the Pakistani lubricants market.

Increasing Shift Toward Synthetic Lubricants for Extended Drain Intervals

Fleet owners and industrial operators are adopting synthetic lubricants to reduce maintenance cycles and improve fuel economy. Shell unveiled “Shell Lubricant Solutions” in May 2024 to capitalize on this shift toward premium grades. New-generation engines entering Pakistan’s vehicle mix mandate API SP and ACEA C3 classifications that require synthetic or semi-synthetic base stocks. Lower oil change frequencies are compelling for long-haul trucks, where workshop access along rural routes remains limited. As additive technology and local blending sophistication improve, synthetics are poised to capture incremental points of Pakistan's lubricants market share.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Base-oil import dependency impacting cost stability | -0.6% | Coastal refineries and blenders | Short term (≤ 2 years) |

| High prevalence of counterfeit and unorganised brands | -0.4% | Rural and semi-urban markets | Medium term (2-4 years) |

| Energy shortages and inflationary pressure curbing industrial output | -0.3% | Energy-intensive industries nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Base-Oil Import Dependency Impacting Cost Stability

Nearly all Group II and Group III feedstocks are imported, exposing blenders to currency swings and freight shocks. The National Tariff Policy 2025-30 maintains an 11% duty on base oils versus 20% on finished lubes, nudging firms to blend locally yet still leaving them vulnerable to volatile import bills. Exchange rate depreciation compresses margins for players unable to pass costs downstream. Inventory buffers become pricier, straining working capital and occasionally tightening supply, especially for premium synthetics within the Pakistan lubricants market.

High Prevalence of Counterfeit and Unorganised Brands

Informal recyclers re-refine used oils with minimal processing, flooding the market with cheap, counterfeit packs. Research shows 61% of collected engine oil is repurposed directly as commercial fuel or sub-standard lubricant[2]Mohammad Nafees et al., “Production, Re-use and Recycling of used engine oil in Pakistan: A Case Study,” xisdxjxsu.asia . Counterfeits erode trust and reduce willingness to pay for branded synthetics, particularly outside major cities. Legitimate players must invest in tamper-proof packaging and consumer education, thereby increasing marketing spend and complexity in rural channels of the Pakistani lubricants market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine Oils Maintain Leadership as Industrial Grades Accelerate

Automotive engine oil retained a 41.02% share of the Pakistan lubricants market in 2025, reflecting a large and aging vehicle parc that follows traditional maintenance practices. Industrial engine oil, driven by power and manufacturing investments, is the fastest-growing segment, with a 2.29% CAGR through 2031. Transmission fluids and gear oils are benefiting from the increased deployment of heavier off-road machinery on CPEC projects, while hydraulic fluids are tracking the sales of construction equipment. Brake fluids and greases, although smaller in volume, are gaining relevance as vehicle safety standards become increasingly stringent. Specialty grades such as turbine oil and transformer oil serve critical power assets, with OEM approvals driving premium pricing. Premium synthetics now permeate multiple product lines, elevating average selling prices in the Pakistan lubricants market.

The rising adoption of synthetic products is reshaping product mix dynamics. OEM drain-interval guidance is lengthening, and fleet operators prefer multigrade full synthetics for diesel engines that travel high mileages on the Karachi–Lahore corridor. Industrial buyers are migrating to anti-wear hydraulic oils that extend component life under intermittent power outage conditions. Process oils, used in rubber and plastic goods, correlate with localized consumer manufacturing. Metalworking fluids are seeing incremental demand from steel mill overhauls and export-oriented light engineering clusters, broadening product diversity within the Pakistani lubricants market.the production of

By End-User Industry: Automotive Dominates, Industrial Consumption Gains Traction

The automotive channel accounted for 54.01% of Pakistan's lubricants market share in 2025, encompassing passenger cars, buses, trucks, and a substantial two-wheeler segment. Industrial usage is expanding at a 2.18% CAGR as energy and manufacturing investment drive higher lubricant intensity. Construction and mining machinery are increasingly relying on high-load gear oils and EP greases, while growing urbanization is fueling the use of these products in generator sets. Marine volumes are modest but increasing, driven by the renewal of the coastal fleet and the activity at Gwadar port. Aerospace remains a nascent market but may grow if national carrier fleet modernization proceeds, hinting at future niche volumes for high-specification turbine oils in the Pakistani lubricants industry.

Power generation stands out as a key industrial sub-segment. Turbine and transformer fluids experience a dependable demand from legacy thermal plants with long-term fuel supply contracts. Textile processing needs high-speed spindle oils that resist oxidation at elevated loom temperatures. Steel production growth sustains demand for open-gear lubricants in continuous casting and rolling mills. Oil and gas drilling requires mud motor oils and downhole lubricants that withstand high pressure, adding premium pockets to the Pakistan lubricants market.

By Base Stock Type: Mineral Oils Lead but Sustainable Alternatives Outpace

Mineral oil products captured 58.29% of the Pakistani lubricants market in 2025, due to their price competitiveness and established supply chains. Bio-based lubricants, though small, post the quickest climb at 3.02% CAGprovide oxidative stability and cold-start performance, which are essential for engine longevity and crucial for fleets facing risks of fuel adulteration, supported by global sustainability mandates that filter into multinational fleet procurement policies. Full synthetics gain market share in power, mining, and long-haul trucking, as local blenders secure Group III and import blends, and invest in additive packages. Semi-synthetics serve as a cost-effective bridge, offering drain interval benefits at mid-range price points.

Bio-lubricants leverage waste cooking oil and crop residue feedstocks, aligning with circular economy goals. Government clean-fuel initiatives and potential green procurement clauses could accelerate the growth of this niche. Synthetics deliver oxidative stability and cold-start performance, which are crucial for engine longevity and vital for fleets facing fuel adulteration risks. As OEM warranty compliance becomes tighter, demand for factory-approved synthetic grades is expected to continue gaining market share in Pakistan's lubricants market.

Geography Analysis

Pakistan's lubricants market demand is concentrated along the Karachi–Lahore–Islamabad industrial belt that houses most manufacturing, processing, and service activities. Karachi anchors import logistics through Port Qasim and hosts the PSO’s Lubricants Manufacturing Terminal, ensuring a reliable supply to the southern and central regions. Punjab, with its dominance in the textile and agribusiness sectors, consumes high volumes of diesel engine oils, hydraulic fluids, and gear lubricants for its agro-processing equipment. Sindh’s petrochemical base drives specialized process oil demand, while port and shipping operations require marine cylinder oils and greases.

Khyber Pakhtunkhwa is emerging as a strategic transit province because of the CPEC road alignments. Hi-Tech Lubricants’ retail expansion to twelve new stations in the province enhances product reach for long-haul fleets navigating mountainous terrain. Balochistan remains relatively under-penetrated; yet, Gwadar’s deep-sea port is poised to trigger increased sales of lubricants for cargo handling equipment and ancillary logistics chains. Cross-border trucking with Afghanistan also channels incremental volumes of heavy-duty engine oils.

Retail footprint intensity mirrors regional demand. PSO operates 3,580 outlets nationwide, providing unrivaled last-mile reach, while Attock Petroleum’s 800-plus sites reinforce competitive presence in northern corridors. Aramco’s branded entry through its stake in Gas and Oil Pakistan brings an additional 1,200 stations under international supply protocols, which is likely to lift lubricant quality benchmarks. Rural markets still favor low-cost mineral oils; however, education campaigns by major lubricant manufacturers are slowly shifting preferences in the Pakistani lubricants market toward certified grades.

Competitive Landscape

The market is moderately consolidated. Strategic alliances are proliferating. ENOC signed an exclusive distribution agreement with Flow Petroleum, reflecting the international appetite for Pakistan’s rising oil volumes. White-space opportunities remain in bio-lubricants and high-performance industrial fluids where local competitors lag in formulation capability. Counterfeit mitigation, aided by OGRA’s stricter licensing regime, is likely to favor branded players that can authenticate supply chains. Product innovation and technical services differentiate contenders. Chevron leverages Caltex Havoline and Delo branding to pursue passenger car and heavy-duty segments, respectively, while also offering turbine and gas-engine lubricants for power plants. Collectively, technology, network reach, and service quality will shape competitive positions in the Pakistan lubricants market through 2030.

Pakistan Lubricants Industry Leaders

Shell plc

PARCO Gunvor Limited (PGL)

Chevron Pakistan Lubricants

Pakistan State Oil

Hi-Tech Lubricants Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Chevron committed USD 30 million for an automated lubricants blending plant in Pakistan, aiming to scale production beyond its current 70 million-litre annual volume.

- June 2025: BP p.l.c. initiated the sale of its Castrol lubricants division, valued at nearly USD 10 billion, setting the stage for potential ownership shifts in regional supply networks.

Pakistan Lubricants Market Report Scope

A lubricant is a substance that helps to reduce friction between surfaces in mutual contact, which ultimately reduces the heat generated when the surfaces move. It may also transmit forces, transport foreign particles, or heat or cool the surfaces.

Pakistan's Lubricants market is segmented by product type and end-user industry. By product type, the market is segmented into engine oil, transmission and hydraulic fluid, general industrial oil, gear oils, grease, and other product types (process oil and turbine oil). By end-user industry, the market is segmented into power generation, automotive and transportation, heavy equipment, food and beverage, and other end-user industries (construction and food and beverage industry).

For each segment, the market sizing and forecasts have been done based on volume (liters).

By Product Type

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

By End-user Industry

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-Use Industries |

By Base Stock Type

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-Use Industries | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

Key Questions Answered in the Report

What is the forecast volume for lubricant demand in Pakistan by 2031?

The market is projected to reach 571.62 million litres by 2031, advancing at a 2.16% CAGR.

Which product category currently holds the largest share in Pakistan?

Automotive engine oil accounts for a 41.02% share of the total volume.

Which segment shows the fastest growth through 2031?

Industrial engine oil is projected to post the highest product-level CAGR at 2.29%.

How significant is the growth in demand for bio-based lubricants in Pakistan?

Bio-based grades record a 3.02% CAGR, outpacing all other base stock categories.

What key factor restrains the cost stability of lubricant producers?

Heavy reliance on imported base oils exposes blenders to currency and freight volatility.

Page last updated on: