Packaging Sorting And Distribution Automation Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

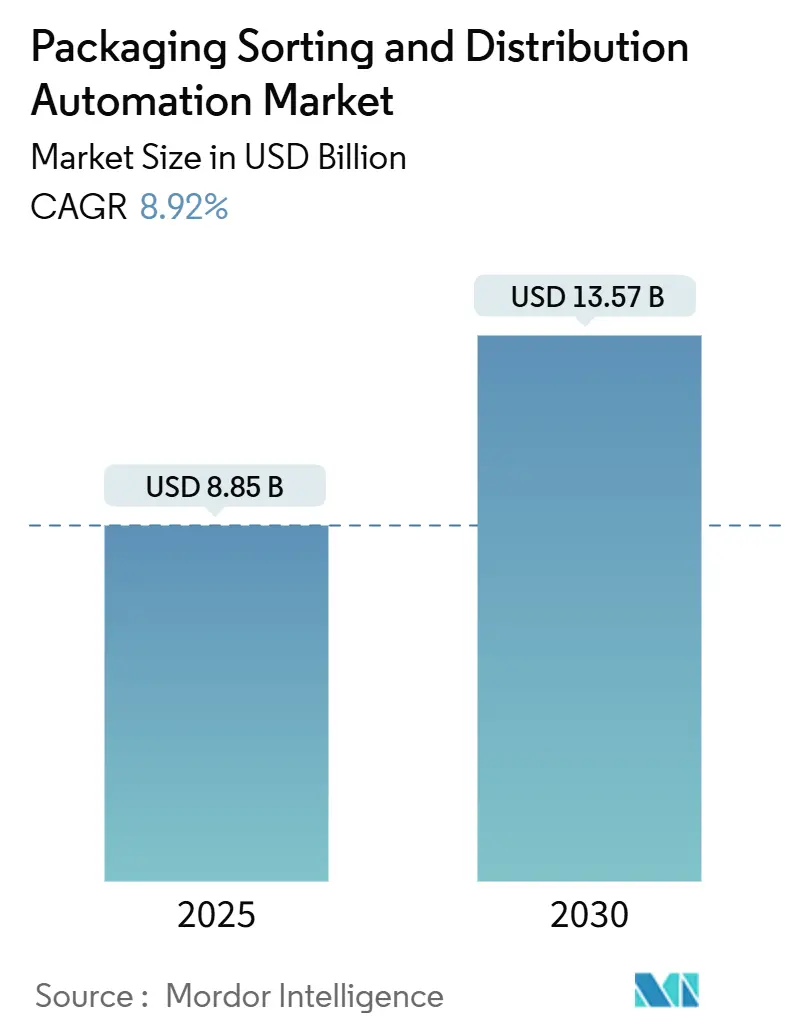

| Market Size (2025) | USD 8.85 Billion |

| Market Size (2030) | USD 13.57 Billion |

| Growth Rate (2025 - 2030) | 8.92% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

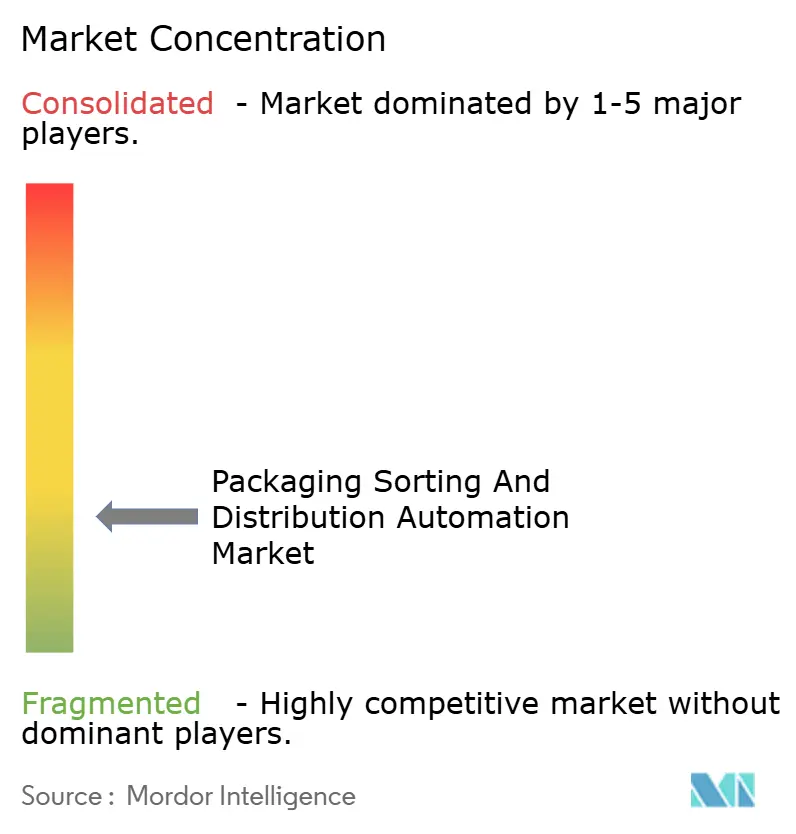

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Packaging Sorting And Distribution Automation Market Analysis by Mordor Intelligence

The packaging sorting and distribution automation market stands at USD 8.85 billion in 2025 and is forecast to reach USD 13.57 billion by 2030, advancing at an 8.92% CAGR. This expansion reflects surging e-commerce parcel volumes, persistent warehouse labor shortages, and sustained capital inflows into AI-centric supply-chain orchestration platforms. Technology vendors benefit from major carrier automation programs, such as UPS upgrading 200 U.S. facilities and Amazon allocating EUR 700 million (USD 763 million) for European fulfillment robotics, which accelerate replacement cycles for legacy systems . Competitive intensity rises as venture-backed robotics specialists introduce software-defined platforms that compress deployment timelines and reduce total cost of ownership. Policy incentives-ranging from North American accelerated depreciation schedules to Asia-Pacific subsidies-further underpin the adoption of energy-efficient equipment and cloud-native control software,

Key Report Takeaways

- By equipment type, conveyor sorters held 42.51% of the packaging sorting and distribution automation market share in 2024, while robotic sorters are projected to post a 14.25% CAGR through 2030.

- By sorting technology, linear systems accounted for 55.12% of the packaging sorting and distribution automation market size in 2024; vision-guided AI systems are expected to expand at a 17.86% CAGR over the same horizon.

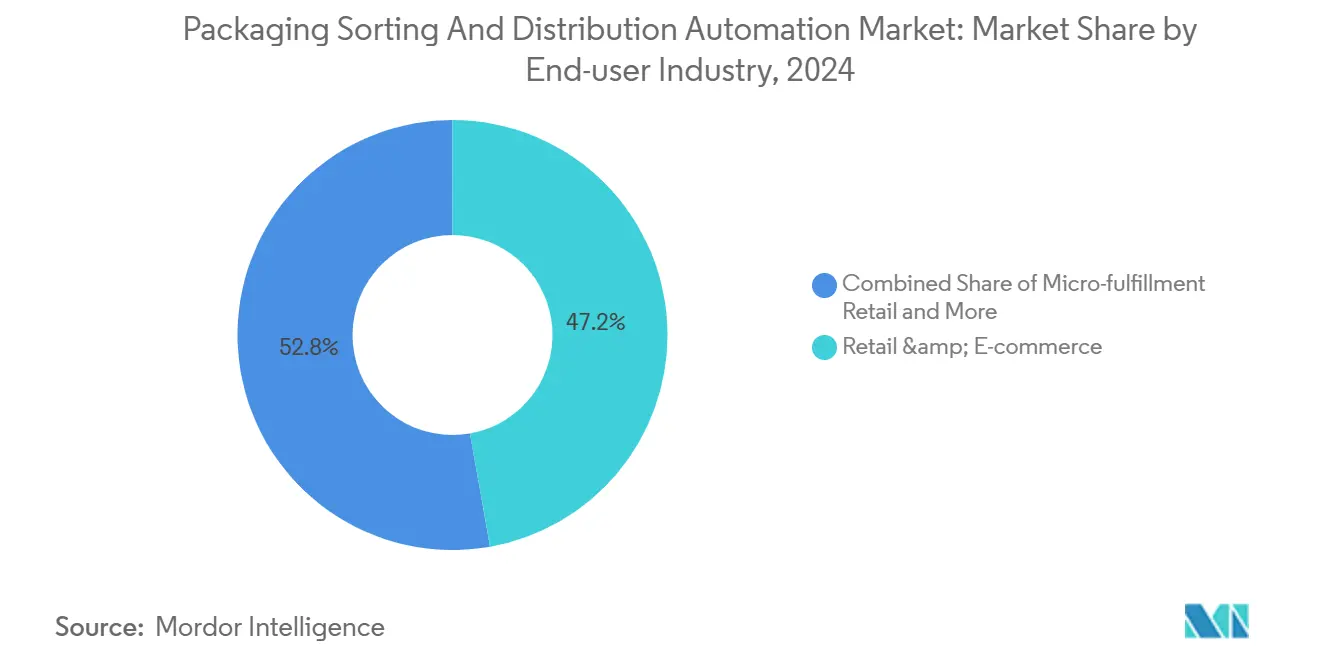

- By end-user industry, retail and e-commerce fulfillment commanded 47.21% of revenues in 2024, whereas micro-fulfillment retail segments are positioned to grow at an 18.54% CAGR to 2030.

- By mode of material flow, goods-to-person solutions led with 60.18% share in 2024, and hybrid orchestrated flows are forecast to climb at a 16.34% CAGR.

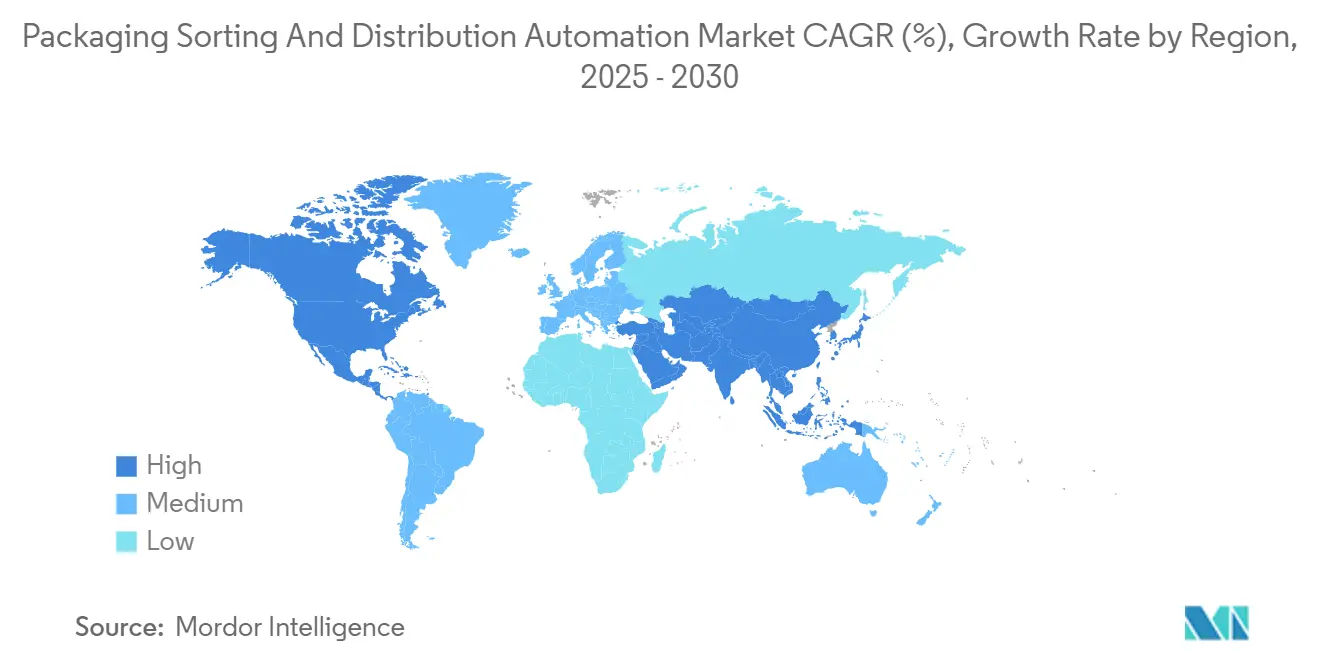

- By geography, North America retained 38.12% share in 2024, yet Asia-Pacific is set to register the fastest regional CAGR at 12.91% through 2030.

Global Packaging Sorting And Distribution Automation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce Parcel-Volume Explosion | +2.1% | Global, with peak impact in North America and Asia-Pacific | Medium term (2-4 years) |

| Labor Shortages in Warehousing and Logistics | +1.8% | North America and Europe core, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Investments in Supply-Chain Orchestration and AI | +1.5% | Global, led by developed markets | Long term (≥ 4 years) |

| Box-On-Demand and Right-Size Packaging Mandates | +0.9% | Europe and North America, spillover to Asia-Pacific | Medium term (2-4 years) |

| Sustainability-Linked Financing for Low-Energy Sorters | +0.7% | Europe core, expanding to North America | Long term (≥ 4 years) |

| AI-Driven Micro-Fulfillment Network Build-Outs | +1.2% | Urban centers globally, concentrated in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Parcel-Volume Explosion Drives Infrastructure Transformation

World parcel traffic climbed to 161 billion units in 2024, a 12% year-over-year jump, forcing logistics operators to abandon manual sortation in favor of systems that can process in excess of 50,000 parcels per hour. Same-day and next-day delivery promises compress processing windows and expose the limits of human throughput. Amazon’s deployment of Sparrow robotic arms in 175 fulfillment centers cut error rates below 0.1% and raised processing velocity by 40%. [1]Amazon Investor Relations, “Amazon Deploys Sparrow Robotic Arms for Fulfillment Automation,” Amazon, amazon.com Comparable automation programs at FedEx, valued at USD 5.2 billion through 2027, confirm that throughput capacity eclipses cost minimization as the primary investment rationale. The sustained rise in peak-season order spikes magnifies the value proposition of continuously operating robotic installations that do not require overtime wages. Consequently, integrators of high-speed cross-belt, tilt-tray, and vision-guided technologies record growing order backlogs as carriers reshape their hub-and-spoke architectures around automated nodes.

Labor Shortages Accelerate Automation Adoption Timelines

Warehousing vacancies in the United States reached 430,000 positions in 2024, with annual turnover rates around 75% and night-shift absenteeism exceeding 20%.[2]Bureau of Labor Statistics, “Job Openings and Labor Turnover Summary,” U.S. Department of Labor, bls.gov Similar mismatches appear in Europe as aging demographics and immigration constraints pinch recruitment pipelines. DHL responded by pledging EUR 2 billion (USD 2.18 billion) to expand automated sortation capacity in Germany and the Netherlands, citing payback periods below 24 months. Average warehouse wages rose 18% in 2024, heightening demand for robots that sustain 24/7 operations without productivity decay. Hybrid human-robot models gain traction because they blend robotic consistency with human oversight for exception handling, improving safety and retaining institutional knowledge amid tightening labor markets.

Investments in Supply-Chain Orchestration and AI Redefine Workflows

Retailers and third-party logistics providers pivot toward cloud-native control towers that synthesize IoT telemetry, predictive demand data, and real-time traffic inputs to allocate sortation capacity dynamically. Walmart’s AI platform forecasts demand 14 days ahead with 94% accuracy, reducing out-of-stock events and reallocating labor hours to higher-value tasks. Google Cloud processes 2.3 million routing decisions per second for its 3PL partners, enabling load balancing across distributed fulfillment nodes. Predictive maintenance overlays lower unplanned downtimes by 35% and extend conveyor system life to 12 years, offsetting high upfront capex. Such orchestration layers reshape competitive advantage from hardware ownership to data mastery, prompting traditional mechanization vendors to embed analytics modules and open API frameworks in their controllers.

AI-Driven Micro-Fulfillment Network Build-Outs Increase Urban Density

Retailers locate micro-fulfillment nodes within 3 miles of dense consumer clusters, equipping compact facilities of under 10,000 square feet with vertical storage and robotic picking to deliver 15-minute turnaround times. Kroger’s alliance with Ocado added 20 U.S. sites, each fulfilling 50,000 orders weekly without manual picking aisles. Industrial real estate investors allocated USD 4.7 billion to such properties in 2024, viewing automation-ready footprints as strategic last-mile assets. Micro-fulfillment favors modular sorters and pouch systems that excel at high-frequency, small-order profiles, pressuring conveyor-centric suppliers to miniaturize platforms and support software-defined routing.

High Capital Investment Requirements Constrain Market Entry

Turnkey sorter installations range from USD 2-8 million for mid-scale hubs and can reach USD 50 million for enterprise complexes. Over a 5-year horizon, software, maintenance, and integration inflate ownership costs by 40-60%. Access to affordable financing remains scarce for regional logistics providers in emerging economies, where currency volatility amplifies repayment risk. Although new leasing models and vendor-backed subscription tiers lower barriers, many operators defer projects until cash flows stabilize.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capex for automated systems | -1.4% | Global, particularly acute in emerging markets | Short term (≤ 2 years) |

| Systems-integration and legacy-IT complexity | -1.1% | North America and Europe where legacy systems prevail | Medium term (2-4 years) |

| Cyber-security and data-sovereignty compliance costs | -0.8% | Global with region-specific mandates | Long term (≥ 4 years) |

| Price pressure from low-cost Chinese vendors | -0.6% | Global, strongest in price-sensitive segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legacy System Integration Complexity Extends Implementation Timelines

Brownfield sites struggle with batch-oriented warehouse management software that cannot natively feed sub-second data to modern robotics. Integration projects therefore average 18-24 months and demand custom middleware budgets of USD 0.5-2 million per deployment. Additional staff retraining and NIST-mandated cyber-security audits prolong full-scale ramp-up by another 6-12 months.[3]National Institute of Standards and Technology, “Warehouse Automation Security Guidelines,” NIST, nist.gov These delays reduce near-term ROI visibility and occasionally lead operators to phase automation in smaller increments, moderating revenue potential for equipment vendors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Shift from Fixed Conveyors to Flexible Robotics

Conveyor sorters still anchor 42.51% of installations because they deliver predictable performance in high-volume hubs and integrate seamlessly with legacy chutes and in-feed lines. This dominance translates into the largest slice of the packaging sorting and distribution automation market. Robotic sorters, however, are projected to generate a 14.25% CAGR, outpacing every other equipment class as computer-vision accuracy reaches 99.8% in unstructured environments.

Growth momentum reflects customer interest in modular deployments that scale with demand spikes and reconfigure layouts without welding or civil works. AMR-based sorters, pouch pocket systems, and tilt-tray hybrids provide alternatives for small-parcel, apparel, and pharmaceutical uses where gentle handling supersedes raw throughput. Vendors therefore pivot R&D toward compact, plug-and-play cells that reduce commissioning from months to weeks, underscoring the packaging sorting and distribution automation market’s transition to flexible architectures.

By Sorting Technology: AI Vision Systems Gain Share

Linear sorters captured 55.12% of 2024 revenue, validating decades of optimization and operator familiarity. Yet AI-enhanced vision sorters are forecast to advance at 17.86% CAGR, the fastest among all technologies, as machine learning drives near-perfect read rates on poorly labeled parcels. [4]MIT Computer Science and Artificial Intelligence Laboratory, “Vision-Guided Sorting Algorithms 2024,” MIT, csail.mit.edu

Early adopters report 25-35% higher operating efficiency relative to conventional linear lines, even though capex remains 40-60% higher. Loop and carousel platforms retain relevance in pharma and electronics, while IoT-connected smart sorters adjust routing on the fly according to downstream congestion, especially where 5G connectivity supports millisecond latency. The packaging sorting and distribution automation market size tied to advanced vision systems is therefore set to expand materially as performance premiums offset steeper price tags.

By End-User Industry: Retail-Led Demand Raises Technology Bar

Retail and e-commerce fulfillment generated 47.21% of 2024 sales, benefiting from omnichannel strategies that blend store replenishment with direct-to-consumer shipping. Within this arena, micro-fulfillment retail is anticipated to post an 18.54% CAGR as city-centric dark stores multiply. Third-party logistics firms upgrade to manage higher parcel volumes with 50% lower average weights, thereby fueling investments in dynamic weight and dimension scanners that plug into robotic sorters.

Postal operators modernize as USPS allocates USD 3.8 billion for sorter retrofits, while food, beverage, and healthcare sectors specify climate-controlled and serialization-compliant lines that handle fragile or regulated items. This variety pushes manufacturers to design modular platforms that accept industry-specific tooling, strengthening their position in the packaging sorting and distribution automation market.

By Mode of Material Flow: Hybrid Orchestration Balances Efficiency and Flexibility

Goods-to-person systems represented 60.18% of 2024 deployments because they curb worker travel distances and sustain high pick rates. Person-to-goods persists in value-added assembly zones but loses share as ergonomic concerns mount. Hybrid orchestrated flow—where AI routes 85% of parcels robotically and diverts exceptions for manual handling—should climb at a 16.34% CAGR through 2030.

This design hedges against equipment outages and accommodates irregular items that confound pure automation. Amazon’s large network operates such hybrids, pairing autonomous mobile robots with human exception stations to optimize cost per parcel while protecting service levels. These use cases reinforce hybrid models as a strategic pillar of the packaging sorting and distribution automation market.

Geography Analysis

North America controlled 38.12% of 2024 revenue, helped by federal tax incentives and accelerated depreciation that offset robot capex. UPS alone budgeted USD 2.2 billion to automate 200 U.S. sites, installing cross-belt sorters and AI-enabled vision tunnels that elevate throughput and cut manual sort lanes. Canada’s Industry 4.0 grants further spur adoption, whereas near-shoring into Mexico prompts multimodal hubs along the U.S. border to modernize. Regional growth is forecast at 7.8% CAGR through 2030 as replacement cycles extend into tier-2 markets.

Asia-Pacific exhibits the highest velocity at 12.91% CAGR, sustained by China’s USD 2.3 billion National Smart Logistics Initiative and India’s 25% annual e-commerce expansion. Japanese conglomerates such as SoftBank automate 150 facilities, and South Korea channels USD 800 million in subsidies to help small logistics firms adopt robotics. Rising wages and government smart-manufacturing agendas make automation economically compelling, enlarging the packaging sorting and distribution automation market size across the region.

Europe maintains steady gains as labor regulations raise operating costs and the EU Green Deal mandates 30-40% carbon reductions, favoring low-energy sorters. Vanderlande and BEUMER leverage proximity to major customers to secure retrofit orders, while Eastern European logistics corridors attract fresh capital due to strategic geography and competitive labor pools. Brexit-related frictions motivate UK operators to automate for cost containment, further contributing to regional demand.

Competitive Landscape

The packaging sorting and distribution automation market shows moderate consolidation. Incumbents—Daifuku, Vanderlande, and KION Group—capitalize on large installed bases, selling multi-year service contracts that support R&D in AI and robotics. They integrate vertical stacks of conveyors, AS/RS, and software, positioning themselves as single-throat-to-choke suppliers.

Disruptors—GreyOrange, Geek+, and Locus Robotics—secure USD 1.8 billion in 2024 venture funding and emphasize open APIs, rapid deployment cycles, and SaaS revenue. Their mobile robotics challenge conveyor-centric paradigms by offering plug-and-play scalability. Patent filings for computer-vision routing rose 340% in 2024, underscoring a shift toward algorithmic differentiation.

Strategic collaborations multiply: hardware incumbents acquire niche AI firms to shorten learning curves, while software players partner with integrators to anchor proof-of-concepts in brownfield sites. Success increasingly hinges on combining equipment, orchestration software, and lifetime services into cohesive, data-rich ecosystems that adapt with customer strategy.

Packaging Sorting And Distribution Automation Industry Leaders

Daifuku Co., Ltd.

Vanderlande Industries B.V.

KION Group AG (Dematic)

Honeywell Intelligrated

BEUMER Group GmbH and Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Daifuku won a USD 180 million contract to automate five Walmart fulfillment centers with AI sorters handling 100,000 parcels per day.

- September 2024: KION Group completed its USD 320 million takeover of Robotics Plus, broadening Dematic’s vision-guided portfolio.

- August 2024: Vanderlande allocated EUR 250 million (USD 273 million) to expand Dutch manufacturing capacity and launch an in-house AI research hub.

- July 2024: Amazon rolled out Sparrow robotic arms across 175 sites, a USD 2.8 billion program that lifts processing speed by 40% while improving ergonomics.

Global Packaging Sorting And Distribution Automation Market Report Scope

The Packaging Sorting and Distribution Automation Market Report is Segmented by Equipment Type (Conveyor Sorters, Robotic Sorters, Pouch/Pocket Systems, Tilt-Tray/Cross-Belt, AMR-Based Sorters), Sorting Technology (Linear Sortation, Loop/Carousel Sortation, Vision-Guided AI Sortation, IoT-Enabled Smart Sortation), End-User Industry (Retail and E-commerce Fulfillment, Third-Party Logistics, Postal and Parcel Operators, Food and Beverage, Pharmaceuticals and Healthcare), Mode of Material Flow (Goods-to-Person, Person-to-Goods, Hybrid/Orchestrated Flow), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Conveyor Sorters |

| Robotic Sorters |

| Pouch / Pocket Systems |

| Tilt-Tray / Cross-Belt |

| AMR-Based Sorters |

| Linear Sortation |

| Loop / Carousel Sortation |

| Vision-Guided AI Sortation |

| IoT-Enabled Smart Sortation |

| Retail and E-commerce Fulfilment |

| Third-Party Logistics (3PL) |

| Postal and Parcel Operators |

| Food and Beverage |

| Pharmaceuticals and Healthcare |

| Goods-to-Person |

| Person-to-Goods |

| Hybrid / Orchestrated Flow |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Equipment Type | Conveyor Sorters | ||

| Robotic Sorters | |||

| Pouch / Pocket Systems | |||

| Tilt-Tray / Cross-Belt | |||

| AMR-Based Sorters | |||

| By Sorting Technology | Linear Sortation | ||

| Loop / Carousel Sortation | |||

| Vision-Guided AI Sortation | |||

| IoT-Enabled Smart Sortation | |||

| By End-User Industry | Retail and E-commerce Fulfilment | ||

| Third-Party Logistics (3PL) | |||

| Postal and Parcel Operators | |||

| Food and Beverage | |||

| Pharmaceuticals and Healthcare | |||

| By Mode of Material Flow | Goods-to-Person | ||

| Person-to-Goods | |||

| Hybrid / Orchestrated Flow | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the packaging sorting and distribution automation market?

The market totals USD 8.85 billion in 2025 and is forecast to grow to USD 13.57 billion by 2030.

Which equipment type is growing the fastest?

Robotic sorters are projected to post a 14.25% CAGR through 2030, reflecting demand for flexible, vision-guided systems.

Why is Asia-Pacific expected to outpace other regions?

China’s USD 2.3 billion Smart Logistics Initiative, India’s rapid e-commerce expansion, and rising labor costs spur automation adoption, driving a 12.91% CAGR in the region.

How do labor shortages influence automation investment?

High turnover and rising wages shorten payback periods to under two years, accelerating adoption timelines for automated sorters.

What role does AI play in modern sortation systems?

AI orchestrates multi-node networks, predicts demand with high accuracy, and improves routing decisions, reducing last-mile costs by up to 20%.

Are high capital costs a major barrier?

Yes, turnkey systems can cost USD 2-50 million, and integration plus maintenance add up to 60% over five years, delaying adoption for some operators.

Page last updated on: