Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 38.53 Billion |

| Market Size (2026) | USD 40.12 Billion |

| Market Size (2031) | USD 49.14 Billion |

| Growth Rate (2026 - 2031) | 4.14% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Packaging Market Analysis by Mordor Intelligence

Brazil packaging market size in 2026 is estimated at USD 40.12 billion, growing from 2025 value of USD 38.53 billion with 2031 projections showing USD 49.14 billion, growing at 4.14% CAGR over 2026-2031. Growth stems from e-commerce adoption, demographic shifts that favor convenience packs, and sustained investments in pulp-based capacity that offer a domestic alternative to imports. Accelerating online retail boosts corrugated demand, while plastic-substitution mandates channel spend toward paper and molded-fiber formats.[1]Diário Oficial da União, “Decreto 12.063,” in.gov.br Nearshoring of consumer-goods production into Brazil tightens links with North American supply chains and raises the need for export-compliant packaging. Persistent port congestion and resin price volatility temper earnings, yet continuous capital deployment by Suzano, Klabin, and Braskem confirms long-run confidence in the Brazil packaging market.

Key Report Takeaways

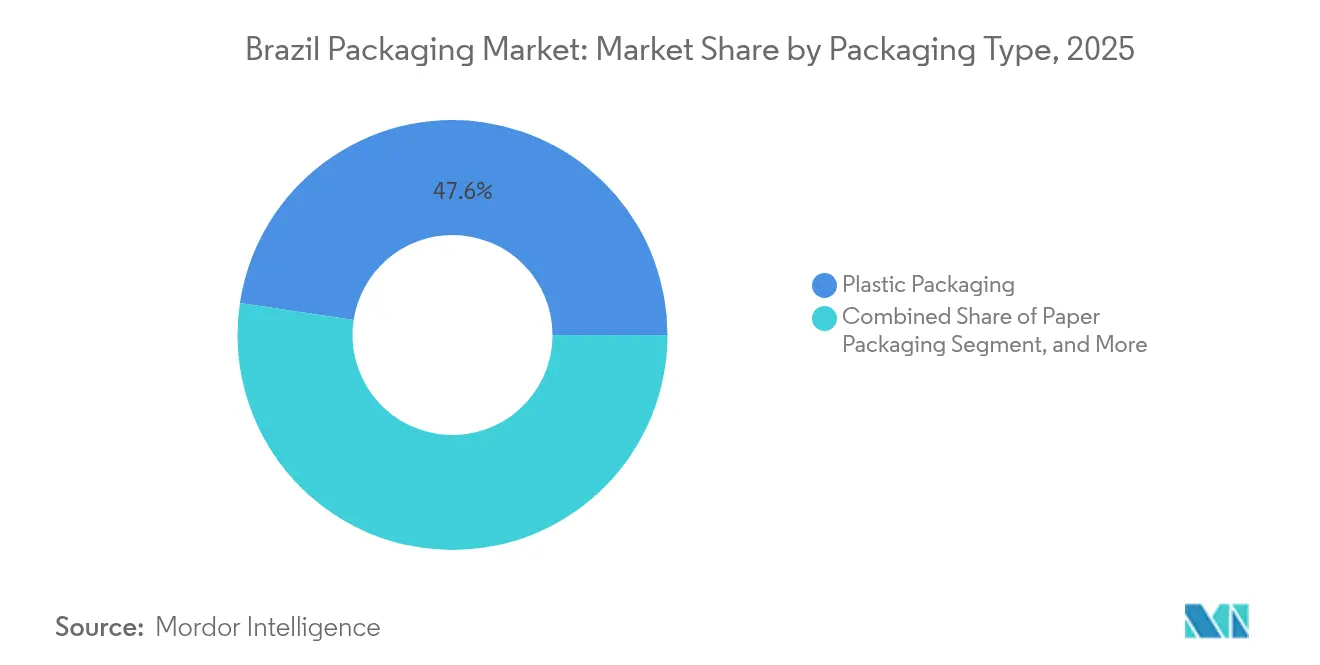

- By packaging type, plastic held 47.62% of Brazil packaging market share in 2025, whereas paper packaging is forecast to advance at a 6.05% CAGR through 2031.

- By packaging format, flexible solutions captured 54.25% share of the Brazil packaging market size in 2025 and are projected to grow at 5.6% CAGR to 2031.

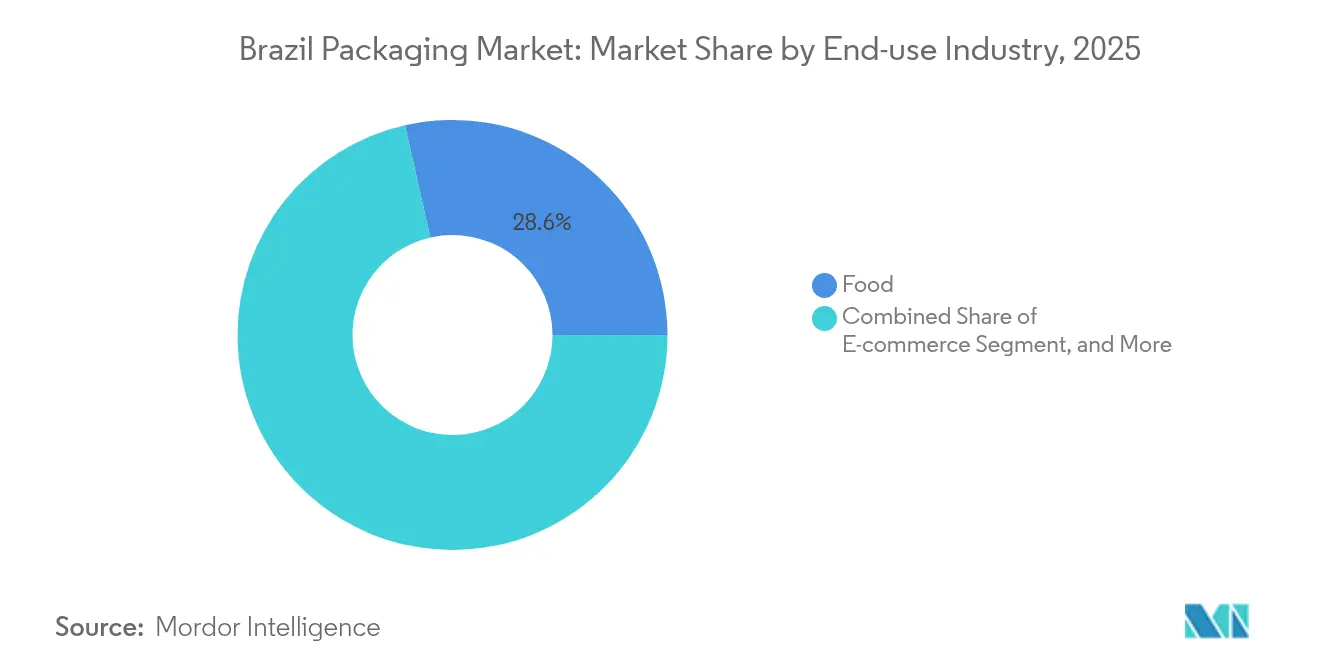

- By end-use industry, food applications accounted for 28.55% of Brazil packaging market size in 2025, while e-commerce packaging is poised for a 7.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic Substitution Mandates In Food Service | +0.8% | National, concentrated in São Paulo, Rio de Janeiro metropolitan areas | Medium term (2-4 years) |

| E-Commerce Led Surge In Protective Packaging | +1.2% | National, with early gains in São Paulo, Rio de Janeiro, Belo Horizonte | Short term (≤ 2 years) |

| Demographics-Driven Demand For Portion Packs | +0.6% | National, urban centers leading adoption | Long term (≥ 4 years) |

| Nearshoring Of Consumer-Goods Production | +0.9% | South and Southeast regions, industrial corridors | Medium term (2-4 years) |

| Smart Packaging Pilots By Brazilian Retailers | +0.3% | Major metropolitan areas, premium retail segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Plastic Substitution Mandates Drive Food-Service Transformation

Federal and municipal decrees are tightening single-use plastic limits, compelling restaurants to replace polystyrene clamshells with molded-fiber trays. São Paulo and Rio de Janeiro require a 30% reduction in disposable plastic use by 2026, accelerating demand for compostable paperboard solutions. Consumer sentiment reinforces the shift: 67% of shoppers accept higher prices for sustainable packs. Quick-service chains now test fiber bowls sourced from Klabin that meet ANVISA food-contact rules, reducing reliance on imported PLA cutlery. Suppliers that certify products under the Green Seal Program gain preferred-vendor status with national retailers.

E-Commerce Expansion Accelerates Protective Packaging Demand

Brazilian online sales exceeded BRL 185 billion in 2024, lifting corrugated shipments 29% year over year. Fulfillment centers specify crush-resistant board grades and void-fill cushions that survive multileg journeys across 5,000 km distribution chains. Sealed Air’s Jaguariúna hub showcases automated right-size pack stations that raise throughput 25% . Corrugated converters that adopt digital printing capture unboxing-experience contracts from premium beauty brands targeting social-commerce shoppers. As last-mile delivery stretches into Amazonia and the Northeast, moisture-barrier coatings gain traction to protect electronics from humidity.

Demographics Fuel Portion Pack Growth

Brazil’s median age climbs to 35 years, and single-person households rise 18% since 2020, lifting demand for single-serve yogurt, ready-to-drink coffee, and on-the-go condiments. Flexible stand-up pouches with laser-scored easy-open features now dominate premium nuts and dried-fruit lines. Food majors JBS and BRF reformulate SKUs into 150 g portions and rely on high-barrier PE/PA films that extend chilled shelf life to 28 days. Smaller pack sizes improve affordability for lower-income consumers and shrink food waste in urban apartments. Portion packs also spur demand for convenience closures such as press-to-close zippers, produced domestically to avoid duty surcharges on imported sliders.

Nearshoring Reshapes Manufacturing and Packaging Demand

Tariff friction between the United States and Asia has prompted automotive, electronics, and processed-food brands to relocate output to Mercosur nations. Brazil’s export-linked plants require ISTA-certified cartons and RFID-enabled labels that simplify U.S. Customs compliance. Paperboard mills in Paraná now allocate 15% of runs to export-grade linerboard, a leap from 6% in 2022. Government investment incentives, such as the Sudene tax credit, reduce CAPEX for facility upgrades that install servo-controlled case formers. Nearshoring also introduces U.S. Food Safety Modernization Act documentation standards, heightening demand for tamper-evident seals and hygienic flexible films.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Resin Prices | -0.7% | National, petrochemical clusters in Rio de Janeiro, São Paulo | Short term (≤ 2 years) |

| Strict Extended-Producer-Responsibility (EPR) Targets | -0.5% | National, with stricter enforcement in major metropolitan areas | Medium term (2-4 years) |

| Chronic Port-Side Logistics Bottlenecks | -0.4% | Coastal regions, Santos, Vitoria, Rio de Janeiro ports | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Resin Price Volatility Squeezes Margins

Import duties on polyethylene, polypropylene, and PVC rose to 20% in 2024, inflating spot resin quotes by 23% inside one quarter. Flexible converters coping with cost swings renegotiate contracts every 60 days, yet brand owners resist price hikes amid soft consumer spending. Rigid-pack producers counter by light-weighting preforms, shaving 1.8 g per 2 L PET bottle without compromising top-load. Some SMEs exit the Brazil packaging market after failing to hedge feedstock through swap agreements with Braskem.

EPR Compliance Raises Cost Burden

Brazil’s National Solid Waste Policy obliges producers to collect or offset 22% of plastic sold by 2025 and 55% by 2030.[2]Planalto, “Lei 12.305,” planalto.gov.br Reverse-logistics consortia emerge, pooling box makers, brand owners, and recyclers to share transport costs for post-consumer materials. Paper converters meet the 60% target via well-established cartonboard recovery streams; flexible-film reclaim lags at 18%. Firms that certify recyclability under ABNT 17001 earn shelf-placement incentives from modern-trade retailers. Non-compliance risks monthly fines up to BRL 50,000, squeezing thin-margin producers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Transition from Plastic to Paper Gains Pace

Plastic retained the largest 47.62% Brazil packaging market share in 2025, anchored in beverages, household chemicals, and pharmaceuticals. However, surging e-commerce and regulatory scrutiny lift paperboard, propelling the segment toward a 6.05% CAGR. This shift enlarges Brazil packaging market size for paper producers by USD 4.45 billion by 2031. Pulp integrators invest in oxygen-delignification and barrier-coating lines that turn kraft into freezer-grade burger boxes. Meanwhile, recyclate-content targets spur plastic converters to blend 30% PCR into detergent bottles, keeping demand for HDPE steady.

The Brazil packaging industry introduces advanced metallized OPP films that deliver high oxygen barriers while reducing gauge by 12%. Metal packaging benefits from ABNT NBR 17194, which codifies performance standards for aluminum cans and raises consumer trust. Glass retains a premium niche in craft spirits, yet lighter PET liquor bottles penetrate duty-free shelves. Multipack shrink film now fights optical haze issues through bi-axially oriented PE, enabling shelf-ready clarity.

By Packaging Format: Flexible Packs Dominate Omni-Channel Retail

Flexible structures occupied 54.25% of Brazil packaging market size in 2025 and are forecast to post 5.6% CAGR through 2031. High-barrier stand-up pouches eclipse rigid jars in spreads and sauces, cutting logistics costs by 25%. Mono-material structures compatible with mechanical recycling advance from 6% to 19% unit share within flexible output. Rigid packaging remains vital in carbonated drinks where pressure resistance is critical; new rPET grades raise recycled content to 50% without yellowing.

The crossover from store shelf to doorstep drives a hybrid pack landscape. All-paper mailers with internal honeycomb cushions replace bubble envelopes for apparel, winning brand kudos for easy curbside recycling. Injection-molded thin-wall cups integrate IML barcodes that automate checkout at cashier-less stores. Flexible films printed in short runs via digital presses accelerate SKU proliferation for craft coffee roasters targeting regional tastes.

By End-Use Industry: Food Remains Anchor as E-Commerce Surges

Food manufacturers consumed 28.55% of Brazil packaging market size in 2025, relying on retort pouches, aseptic cartons, and hot-fill PET to service domestic and export trade. Shelf-stable meat exports to the Middle East demand multilayer EVOH laminates that withstand 121 °C sterilization. Beverage lines add tethered caps to comply with EU-bound export mandates, driving mold conversions. E-commerce parcels register the fastest 7.28% CAGR, adding nearly USD 2.06 billion to Brazil packaging market by 2031.

Healthcare spends on cold-chain pouches and child-resistant cartons as Brazil’s vaccine program expands. Cosmetics leverage matte-finish folding cartons with soy-based inks to reinforce sustainability messaging. Industrial clients invest in bulk FIBCs with antistatic liners to ship lithium concentrate from Minas Gerais mines, diversifying away from single-trip drums.

Geography Analysis

Demand clusters in the Southeast, where São Paulo and Rio de Janeiro anchor 64.60% of the Brazil packaging market. Dense consumer bases, diversified manufacturing, and the Santos port complex make the region the natural hub for converters. The South follows as the fastest-growing zone with a 4.72% CAGR, fueled by agribusiness exports and automotive parts plants across Paraná and Santa Catarina. Paperboard mills here enjoy proximity to pine plantations, reducing wood costs by 10% versus northern competitors.

The Northeast advances at 4.42% CAGR, supported by special-economic-zone incentives in Suape and Pecém that attract flexible-film extrusion. Logistics gaps lengthen delivery lead times, so shippers favor triple-wall corrugated crates for electronics that travel through unpaved stretches. The Central-West leverages soybean and corn output, prompting growth in woven-PP sacks and BOPP labels for bulk feed. In the North, river transport challenges push demand for moisture-resistant laminated sacks that endure week-long barge trips on the Amazon.

Competitive Landscape

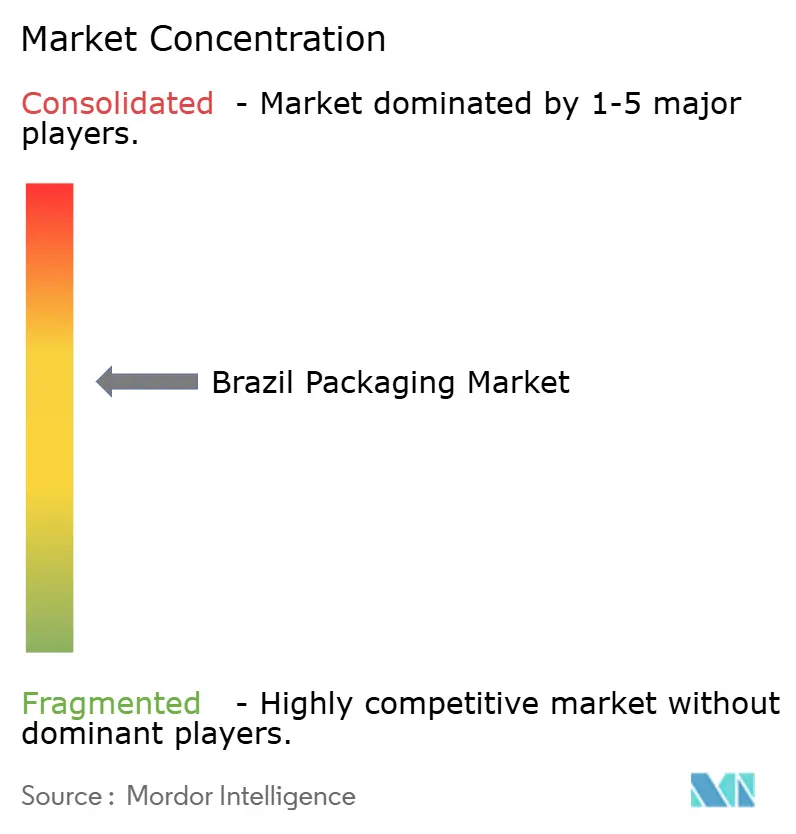

The top five players command roughly 55% of the Brazil packaging market, signaling moderate concentration. Suzano’s USD 15 billion pursuit of International Paper assets broadens its corrugated reach and integrates North-American clients.[3]Packaging Insights, “Suzano’s US Acquisitions,” packaginginsights.com Klabin’s BRL 14.5 billion Puma II project adds 450,000 t of kraftliner, supporting Amazon’s paper-only shipping pledge. Braskem cooperates with Neste to scale 200,000 t of chemically recycled PE, supplying converters that need food-grade PCR. Ball Corporation boosts Jacareí can output 15% to serve craft-beer demand and secure long-term supply contracts.

Private equity eyes specialty niches: Bain Capital backed Packem to build a 50,000 t molded-fiber tray plant in Bahia, aiming at quick-service restaurants exiting polystyrene. Multinational flexibles group Amcor debuts AmFiber recyclable paper structures for OTC pharma, targeting import substitution. Sonoco’s take-over of Zaraplast strengthens industrial film presence in automotive and chemical verticals. Competitive pressure spurs digital transformation: WestRock digitizes three corrugated sites with autonomous guided vehicles, cutting internal transport labor 30%.

Brazil Packaging Industry Leaders

Amcor plc

Ball Corporation

Braskem S.A.

International Paper Company

Graphic Packaging International, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Huhtamäki received ANVISA clearance for a molded-fiber line producing compostable fast-food bowls in Rio Grande do Sul.

- January 2025: Suzano entered exclusive talks to acquire International Paper worldwide operations for USD 15 billion.

- January 2025: Ball Corporation expanded Jacareí aluminum-can capacity by 15% to meet craft-beverage growth.

- December 2024: Brazil published ABNT NBR 17194, the world’s first comprehensive aluminum-can quality code.

Brazil Packaging Market Report Scope

The packaging industry in Brazil is of paramount importance and plays a vital role in the international trade of goods. Packaging can be classified based on the type of use, which includes primary packaging, secondary packaging, tertiary packaging, and ancillary packaging. The study on Brazil's packaging industry tracks demands for the major material types such as plastic (flexible and rigid), metals, glass, and paper and paperboard, along with corresponding industry verticals and revenue accrued from the sales of packaging products.

The Brazilian packaging market is segmented by material type and end-user industry. By material type, the market is segmented into paper and paperboard, plastic, metal, and glass. By end-user industry, the market is segmented into food, beverage, pharmaceutical, consumer electronics, personal/homecare, and other end-user industries. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Packaging Type

| Plastic Packaging | By Type | Rigid Plastic Packaging | By Material Type | Polyethylene (PE) |

| Polypropylene (PP) | ||||

| Polyethylene Terephthalate (PET) | ||||

| Polyvinyl Chloride (PVC) | ||||

| Polystyrene (PS) and Expanded Polystyrene (EPS) | ||||

| Other Material Types | ||||

| By Product Type | Bottles and Jars | |||

| Caps and Closures | ||||

| Trays and Containers | ||||

| Other Product Types | ||||

| By End-use Industry | Food | |||

| Beverage | ||||

| Pharmaceutical | ||||

| Cosmetics and Personal Care | ||||

| Industrial | ||||

| Other End-use Industries | ||||

| Flexible Plastic Packaging | By Material Type | Polyethylene (PE) | ||

| Biaxially Oriented Polypropylene (BOPP) | ||||

| Cast Polypropylene (CPP) | ||||

| Other Material Types | ||||

| By Product Type | Pouches and Bags | |||

| Films and Wraps | ||||

| Other Product Types | ||||

| By End-use Industry | Food | |||

| Beverage | ||||

| Pharmaceutical | ||||

| Cosmetics and Personal Care | ||||

| Industrial | ||||

| Other End-use Industries | ||||

| By Product Type | Bottles and Jars | |||

| Pouches and Bags | ||||

| Bulk-Grade Products | ||||

| Other Product Types | ||||

| By End-use Industry | Food | |||

| Beverages | ||||

| Cosmetics and Personal Care | ||||

| Pharamceuticals | ||||

| Industrial | ||||

| Other End-use Industries | ||||

| Paper Packaging | By Product Type | Folding Carton | ||

| Corrugated Boxes | ||||

| Liquid Paperboard | ||||

| Other Product Types | ||||

| By End-use Industry | Food | |||

| Beverages | ||||

| E-commerce | ||||

| Other End-use Industries | ||||

| Container Glass | By Color | Green | ||

| Amber | ||||

| Flint | ||||

| Other Colors | ||||

| By End-use Industry | Food | |||

| Alcoholic | ||||

| Non-Alcoholic | ||||

| Personal Care and Cosmetics | ||||

| Pharmaceuticals (excluding Vials and Ampoules) | ||||

| Perfumery | ||||

| Metal Cans and Containers | By Material Type | Steel | ||

| Aluminum | ||||

| By Product Type | Cans | |||

| Drums and Barrels | ||||

| Caps and Closures | ||||

| Other Product Types | ||||

| By End-use Industry | Food | |||

| Beverage | ||||

| Chemicals and Petroleum | ||||

| Industrial | ||||

| Paints and coatings | ||||

| Other End-use Industries | ||||

By Packaging Format

| Flexible |

| Rigid |

By End-use Industry

| Food |

| Beverage |

| Pharmaceuticals and Healthcare |

| Personal Care and Cosmetics |

| Industrial |

| E-commerce |

| Other End-use Industries |

| By Packaging Type | Plastic Packaging | By Type | Rigid Plastic Packaging | By Material Type | Polyethylene (PE) |

| Polypropylene (PP) | |||||

| Polyethylene Terephthalate (PET) | |||||

| Polyvinyl Chloride (PVC) | |||||

| Polystyrene (PS) and Expanded Polystyrene (EPS) | |||||

| Other Material Types | |||||

| By Product Type | Bottles and Jars | ||||

| Caps and Closures | |||||

| Trays and Containers | |||||

| Other Product Types | |||||

| By End-use Industry | Food | ||||

| Beverage | |||||

| Pharmaceutical | |||||

| Cosmetics and Personal Care | |||||

| Industrial | |||||

| Other End-use Industries | |||||

| Flexible Plastic Packaging | By Material Type | Polyethylene (PE) | |||

| Biaxially Oriented Polypropylene (BOPP) | |||||

| Cast Polypropylene (CPP) | |||||

| Other Material Types | |||||

| By Product Type | Pouches and Bags | ||||

| Films and Wraps | |||||

| Other Product Types | |||||

| By End-use Industry | Food | ||||

| Beverage | |||||

| Pharmaceutical | |||||

| Cosmetics and Personal Care | |||||

| Industrial | |||||

| Other End-use Industries | |||||

| By Product Type | Bottles and Jars | ||||

| Pouches and Bags | |||||

| Bulk-Grade Products | |||||

| Other Product Types | |||||

| By End-use Industry | Food | ||||

| Beverages | |||||

| Cosmetics and Personal Care | |||||

| Pharamceuticals | |||||

| Industrial | |||||

| Other End-use Industries | |||||

| Paper Packaging | By Product Type | Folding Carton | |||

| Corrugated Boxes | |||||

| Liquid Paperboard | |||||

| Other Product Types | |||||

| By End-use Industry | Food | ||||

| Beverages | |||||

| E-commerce | |||||

| Other End-use Industries | |||||

| Container Glass | By Color | Green | |||

| Amber | |||||

| Flint | |||||

| Other Colors | |||||

| By End-use Industry | Food | ||||

| Alcoholic | |||||

| Non-Alcoholic | |||||

| Personal Care and Cosmetics | |||||

| Pharmaceuticals (excluding Vials and Ampoules) | |||||

| Perfumery | |||||

| Metal Cans and Containers | By Material Type | Steel | |||

| Aluminum | |||||

| By Product Type | Cans | ||||

| Drums and Barrels | |||||

| Caps and Closures | |||||

| Other Product Types | |||||

| By End-use Industry | Food | ||||

| Beverage | |||||

| Chemicals and Petroleum | |||||

| Industrial | |||||

| Paints and coatings | |||||

| Other End-use Industries | |||||

| By Packaging Format | Flexible | ||||

| Rigid | |||||

| By End-use Industry | Food | ||||

| Beverage | |||||

| Pharmaceuticals and Healthcare | |||||

| Personal Care and Cosmetics | |||||

| Industrial | |||||

| E-commerce | |||||

| Other End-use Industries | |||||

Key Questions Answered in the Report

What is the current value of the Brazil packaging market?

The Brazil packaging market size reached USD 40.12 billion in 2026.

How fast is the sector expected to grow?

It is projected to expand at a 4.14% CAGR through 2031.

Which packaging format leads unit demand?

Flexible formats hold 54.25% share and are forecast for a 5.6% CAGR.

Why is paper packaging gaining ground?

Plastic-reduction mandates and e-commerce logistics favor recyclable paperboard solutions.

Which region shows the fastest growth?

The South region is set to post a 4.72% CAGR thanks to agribusiness and automotive exports.

What key regulation affects producer responsibility?

Brazil’s National Solid Waste Policy requires 22% plastic recovery by 2025 and 55% by 2030.

Page last updated on: