Optical Ceramics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

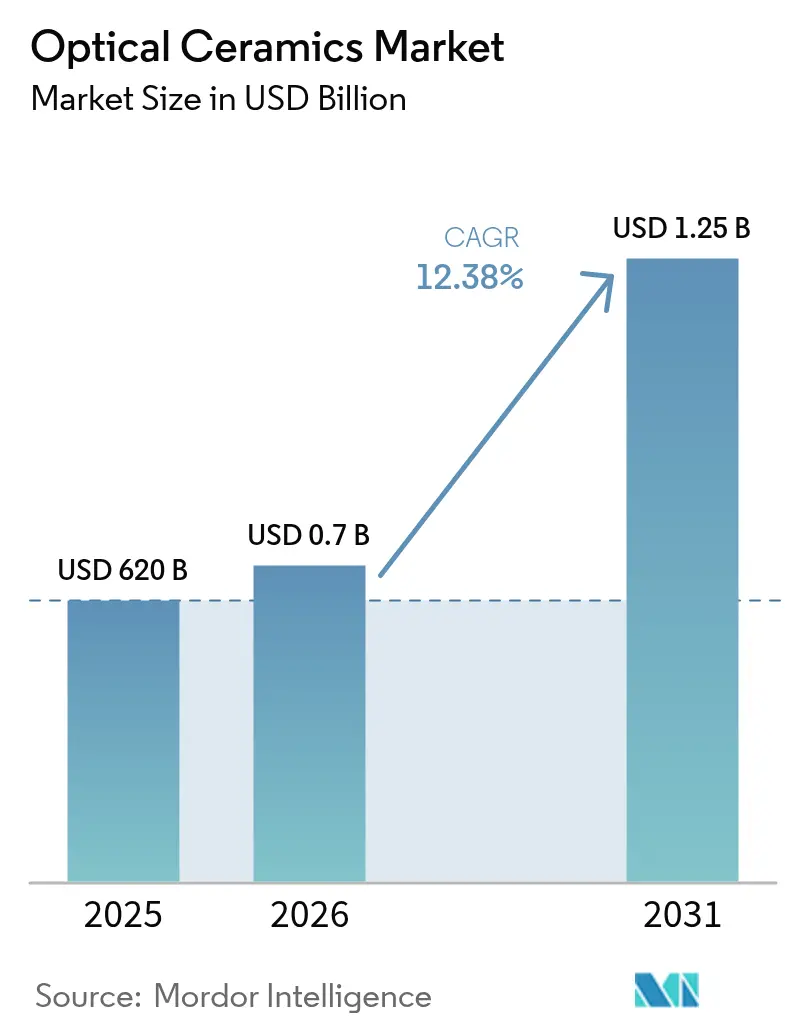

| Market Size (2026) | USD 0.7 Billion |

| Market Size (2031) | USD 1.25 Billion |

| Growth Rate (2026 - 2031) | 12.38% CAGR |

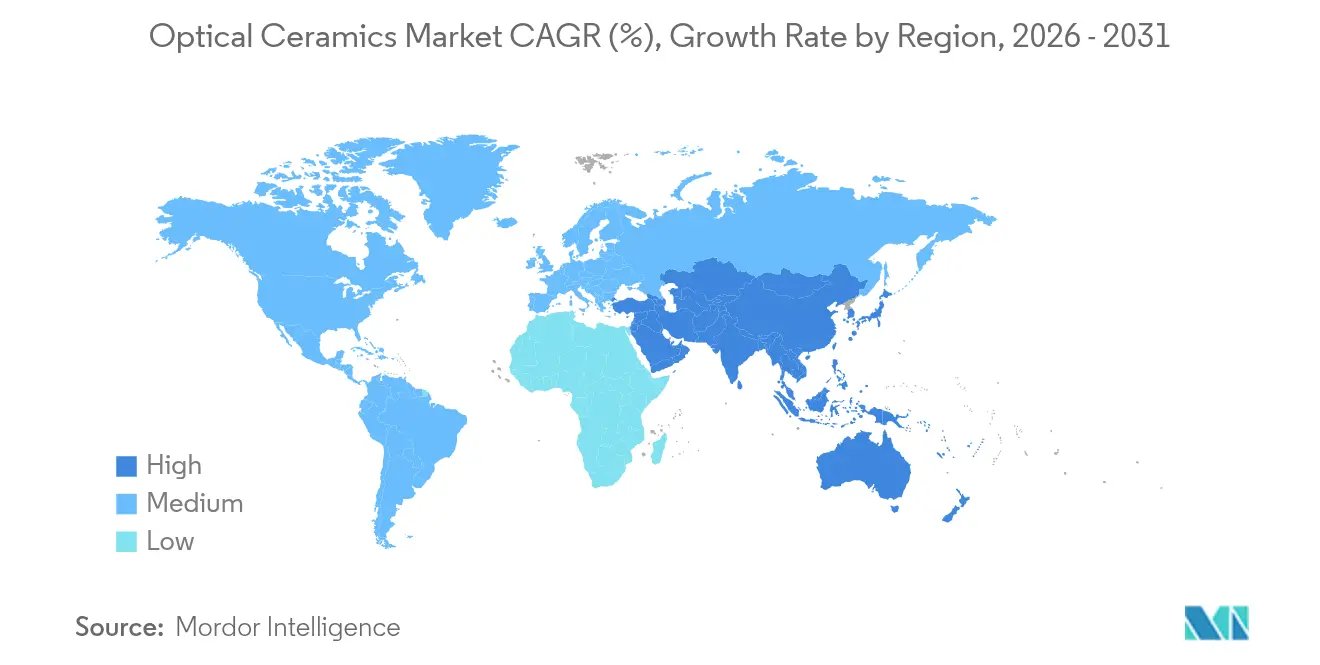

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

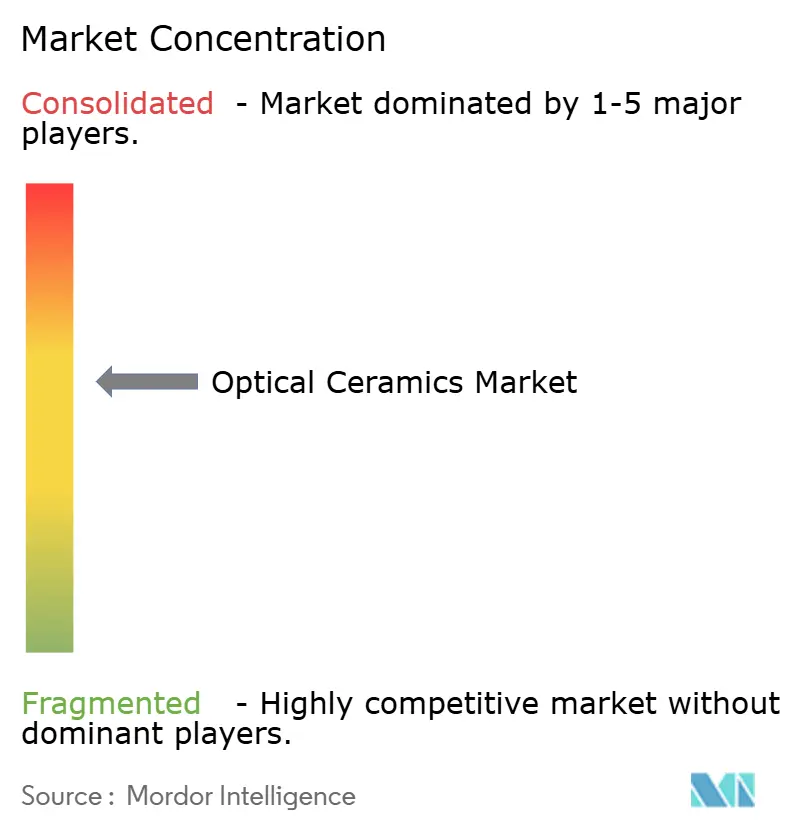

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Optical Ceramics Market Analysis by Mordor Intelligence

The optical ceramics market size was valued at USD 620 million in 2025 and estimated to grow from USD 696.8 million in 2026 to reach USD 1.25 billion by 2031, at a CAGR of 12.38% during the forecast period (2026-2031). Strong defense procurement for lighter, infrared-transparent armor, rising use of polycrystalline YAG in surgical lasers, and stricter performance demands in extreme-temperature energy systems supported this momentum. Production innovations such as ‘Clean HIP’ and vacuum sintering lifted optical clarity while lowering defect rates, encouraging wider use in large-area components. Meanwhile, intellectual-property consolidation and persistently high yield losses for parts above 120 mm diameters limited new entrants, keeping the field moderately concentrated. The intersection of defense, medical, and energy requirements accelerated material transfer across sectors, compressing typical innovation cycles.

Key Report Takeaways

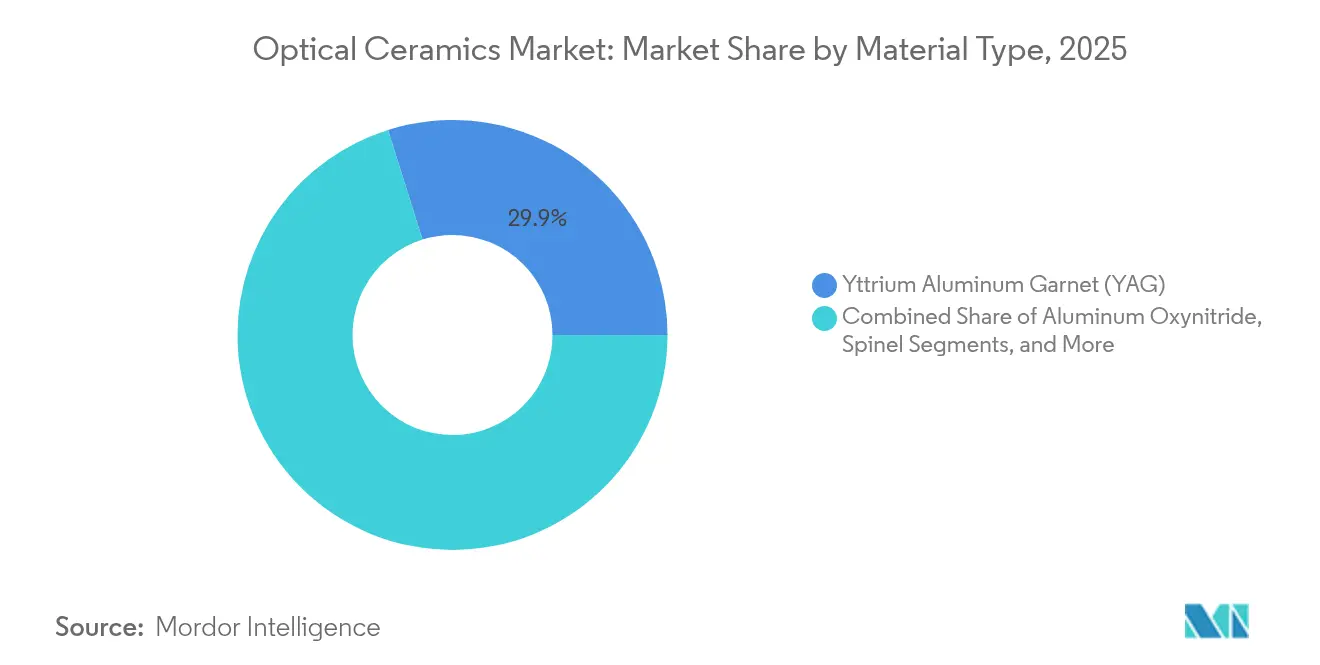

- By material type, YAG led with 29.85% of the optical ceramics market share in 2025; ALON is projected to expand at a 12.86% CAGR to 2031.

- By fabrication method, hot isostatic pressing held 40.70% of 2025 revenue; vacuum sintering is forecast to grow at an 10.96% CAGR through 2031.

- By product type, polycrystalline grades accounted for 67.90% share of the optical ceramics market size in 2025, while monocrystalline variants record a 9.56% CAGR outlook to 2031.

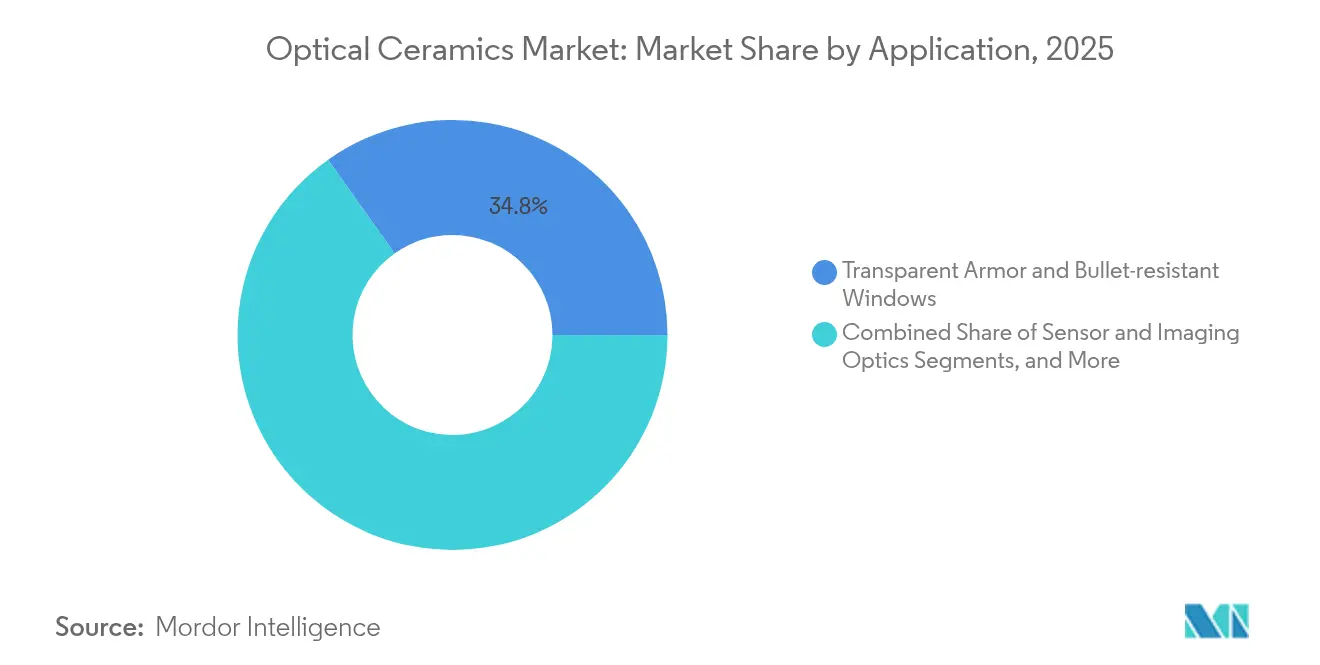

- By application, transparent armor captured 34.82% optical ceramics market share in 2025; laser and lighting components advance at 12.88% CAGR to 2031.

- By end-use industry, aerospace and defense dominated with 39.60% revenue in 2025; healthcare is set to grow at 12.29% CAGR through 2031.

- By geography, Asia-Pacific commanded 37.90% of 2025 revenue; the Middle East and Africa post the quickest 10.98% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Optical Ceramics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of infrared transparent armor in next-gen combat vehicles | 3.2% | North America | Medium term (2-4 years) |

| Surge in UV-LED and laser-based medical devices demanding polycrystalline YAG optics | 2.8% | Asia-Pacific | Medium term (2-4 years) |

| Growth of high-temperature gas-turbine inspections that require sapphire windows | 1.9% | Europe | Long term (≥ 4 years) |

| Spacecraft light-weighting drives ALON/spinel viewports in LEO satellites | 1.7% | North America and Asia-Pacific | Long term (≥ 4 years) |

| Large-area Li-ion battery pack lasers using ceramic flash lamps | 1.5% | Asia-Pacific | Short term (≤ 2 years) |

| Military modernization budgets earmarked for airborne IR sensors with ceramic domes | 2.3% | Middle East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of IR-Transparent Armor in Next-Gen Combat Vehicles

Defense programs integrated ALON and spinel windows that cut weight up to 60% versus laminated glass while maintaining ballistic stop levels, enhancing fuel efficiency, and crew mobility. Components grew to panel sizes of eight square feet, making full-vehicle glazing practical. Machine-learning-guided stacking schemes lowered thickness 22.2% yet raised transmission 42.3%, proving the concept’s scalability. Supply contracts from the U.S. Army accelerated the qualification of larger parts and shortened testing cycles. As a result, procurement agencies issued multi-year orders that locked in volume and stabilized pricing.

Surge in UV-LED and Laser-Based Medical Devices Demanding Polycrystalline YAG Optics

Minimally invasive therapies increasingly relied on Ho:YAG and Nd:YAG lasers whose wavelengths are strongly absorbed by water, ensuring precise tissue removal with limited collateral heating.[1]Coherent Corporation, “What Is a Holmium Laser?,” coherent.com Polycrystalline YAG offered improved thermal conductivity over glass, enabling higher pulse-energy operation and longer component lifetimes. Process innovations delivered 83.7% transmittance at 1064 nm, lifting wall-plug efficiency and facilitating portable surgical platforms well suited to outpatient clinics. Asian contract-device makers expanded production, accelerating regional adoption curves.

Growth of High-Temperature Gas-Turbine Inspections That Require Sapphire Windows

Energy producers installed sapphire viewports that resisted 2,000 °C flue-gas streams and harsh pressure regimes, enabling real-time combustion imaging without shutdown. Predictive-maintenance platforms linked to the sensors cut unplanned downtime by 45%, translating to major fuel savings in combined-cycle installations. Turbine OEMs specified sapphire exclusively for new inspection ports after trials showed zero crack propagation across two-year service intervals, validating lifetime cost benefits over glass alternatives.

Spacecraft Light-Weighting Drives ALON/Spinel Viewports in LEO Satellites

Satellite primes replaced quartz with ALON windows, trimming mass 40% and allowing larger apertures within fixed launch budgets. ALON’s 300 MPa flexural strength endured launch vibration and micrometeoroid impacts, while radiation tolerance preserved optical throughput over multiple orbits. Commercial constellation operators adopted the material to meet aggressive cost-per-kilogram thresholds, prompting component vendors to scale production lines in Japan and the United States.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capex-intensive hot-isostatic pressing lines limiting emerging-market entry | -1.4% | Global, with higher impact in Asia-Pacific, and Middle East and Africa | Long term (≥ 4 years) |

| Yield losses (>15 %) above 120 mm diameter keep unit costs uncompetitive vs. glass | -1.8% | Global | Medium term (2-4 years) |

| Limited transmittance in the 5-7 µm band constrains long-wave IR adoption | -0.8% | North America and Europe | Short term (≤ 2 years) |

| IP consolidation—over 120 active U.S. patents block new formulations | -1.2% | Global, with higher impact in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Capex-Intensive Hot-Isostatic-Pressing Lines Limiting Emerging-Market Entry

Commercial HIP installations often exceeded USD 15 million, creating high financial thresholds for newcomers. Expertise in pressure-vessel design and controlled-atmosphere operations remained concentrated in mature industrial regions, widening the capability gap. Upgrades such as ‘Clean HIP’ and ‘Steered Cooling’ improved performance but also raised capital intensity, reinforcing incumbent advantages.

Yield Losses Above 15% for 120 mm-Diameter Components Keep Unit Costs Uncompetitive vs. Glass

Large optical ceramic blanks suffered micro-crack formation and non-uniform densification, pushing rejection rates past 15%. Each discarded part consumed significant energy and long furnace cycles, inflating the cost of goods. Vacuum-sintered alumina reached 99% relative density in pilot runs, yet scaling these gains to mass production remained elusive, delaying parity with glass in price-sensitive segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: YAG Sustained Lead as ALON Accelerated

YAG retained 29.85% dominance within the optical ceramics market in 2025 through versatility across industrial lasers, scintillators, and sensing optics. Multiple sintering refinements elevated its 1064 nm transmittance, improving beam quality in 10 kW-class laser cutters. ALON posted a 12.86% CAGR by fulfilling aggressive defense and space specifications for lightweight yet ballistic-grade windows. Sapphire maintained energy-sector loyalty thanks to unmatched hardness (Mohs 9) and 2,000 °C thermal stability. Spinel’s cubic lattice removed birefringence, supporting airborne imaging. Yttria expanded steadily for plasma-etch chamber liners in semiconductor fabs. Emerging lutetium-based garnets showed promise in next-generation scintillators.

The optical ceramics market size for YAG systems is projected to rise at 11.38% annually, while ALON share gains are forecast to elevate total industry value without materially eroding YAG volumes. Supply chains now routinely dual-source YAG and ALON to tailor mixed-material assemblies, reflecting design optimization rather than strict substitution.

By Fabrication Method: HIP Dominated, While Vacuum Sintering Gained Momentum

Hot isostatic pressing secured 40.70% revenue in 2025 by producing near-theoretical-density parts with low porosity, essential for ballistic armor and high-power optics. Process refinements like gas-purified chambers raised yield in large panels, reinforcing HIP’s economic edge in premium products. Vacuum sintering, however, posted the highest 10.96% CAGR outlook by delivering 70% transmittance in transparent alumina at lower unit energy, appealing to cost-sensitive sectors. Solid-state sintering kept relevance for simpler geometries, while additive manufacturing joined the “Others” category as researchers printed gradient-index elements.

Through 2031, the optical ceramics market share for HIP may slip modestly as vacuum sintering scales, yet overall output from HIP furnaces will climb because larger armor sets drive volume. Hybrid flows that combine vacuum pre-sintering with final HIP densification are under evaluation to balance clarity and cost.

By Product Type: Polycrystalline Volume Leadership and Monocrystalline Growth

Polycrystalline grades held 67.90% of 2025 revenue by offering higher dopant loading, easier net-shape forming, and sound mechanical strength. Improved powder dispersion and two-step sintering lifted transparency near single-crystal levels, broadening suitability for armor and industrial lasers. Monocrystalline optics grew at a 9.56% CAGR, driven by superior scintillation performance in medical detectors and deep trap depths beneficial to high-energy physics sensors.

The optical ceramics market size for polycrystalline components is forecast to grow at significant pace by 2031, as defense and laser verticals expand. Monocrystalline revenue is set to outpace polycrystalline in percentage terms, aided by maturing crystal-pulling furnaces that trim scrap and cycle times.

By Application: Transparent Armor Led while Laser Components Surged

Transparent armor contributed 34.82% optical ceramics market share in 2025, reflecting global vehicle-fleet upgrades. Panel weight reduction of up to 60% allowed designers to maintain ballistic rating yet cut fuel consumption and increase payload. Laser and lighting parts posted the strongest 12.88% CAGR outlook as ceramic gain media enabled higher-power industrial and surgical systems. Imaging optics, medical diagnostics, and power-plant viewports created steady mid-single-digit expansion. Energy-sector optics remained niche but important for extreme-temperature monitoring.

By 2031, laser components are expected to close the revenue gap with armor, underpinned by demand for semiconductor wafer cutting, additive manufacturing, and outpatient surgery devices.

By End-Use Industry: Aerospace and Defense Held Sway, Healthcare Accelerated

Aerospace and defense owned 39.60% of 2025 revenue, leveraging ceramics’ survival in hypersonic flight, missile domes, and armored glazing. Programs for airborne IR sensors and LEO satellite viewports locked multi-year offtake for ALON and spinel. Healthcare showed the fastest 12.29% CAGR as surgeons adopted ceramic-based lasers for minimally invasive procedures, and diagnostics embraced higher-resolution scintillators.

Energy, consumer electronics, and industrial machinery applied optical ceramics for robustness under heat, wear, and chemical attack, each posting mid-single-digit growth. Research laboratories chose the materials for stability in high-precision instruments, rounding out demand.

Geography Analysis

Asia-Pacific led the optical ceramics market with 37.90% 2025 revenue thanks to China’s rapid battery-pack laser expansion and Japan’s focus on light-weighted satellite optics. South Korea and Taiwan added fabs specializing in ceramic flash lamps and sensor windows. Government initiatives such as Japan’s Fine Ceramics Roadmap 2050 mapped long-range technology needs.

North America leveraged strong defense spending, particularly U.S. programs upgrading transparent armor and laser systems, maintaining a sizeable share. Collaborative clusters involving Sandia National Laboratories and private industry shortened development cycles by replacing trial-and-error with physics-based modeling. Canada and Mexico contributed specialized production and R&D, securing resiliency in North American supply chains.

The Middle East and Africa recorded the fastest 10.98% CAGR, with Saudi Arabia and the United Arab Emirates funding airborne IR sensor domes built from ALON. Israel’s Ceramic and Silicate Institute enabled regional know-how transfer, fostering domestic ballistic-grade armor developments.

Europe retained critical expertise in high-temperature sapphire windows for turbines and precision optics for scientific research. Germany and the United Kingdom drove product innovation, while the Nordic cluster pioneered hydrogen-fired kilns to cut carbon footprints in ceramic processing. South America grew from a small base as Brazil and Argentina introduced sapphire inspection ports in refining and healthcare sectors, leveraging local mineral resources.

Competitive Landscape

The optical ceramics market exhibited moderate concentration. Surmet Corporation and CeramTec GmbH led transparent armor and medical laser components, respectively, through proprietary sintering formulas and vertical integration. Surmet scaled ALON panel manufacture to eight-square-foot sheets under a USD 25 million U.S. DoD contract. CeramTec introduced enhanced-thermal-management YAG parts, reinforcing its medical franchise. Coherent Corp. unified diode and ceramic gain media assets, releasing 50W pump lasers that trimmed the bill of materials for industrial fiber lasers.

CoorsTek invested USD 30 million into Colorado capacity to produce larger transparent armor blanks, pursuing economies of scale. Schott AG debuted ceramic-glass composites blending thermal stability with manufacturability, targeting harsh-environment avionics. Saint-Gobain’s acquisition of Monofrax expanded fused refractory capabilities for extreme-heat optics. Additive-manufacturing start-ups explored gradient-index optics that sidestep some of the 120 plus active U.S. patents blocking classical formulations.[4]Google Patents, “Ceramic Coating Comprising Yttrium Resistant to Reducing Plasma,” patents.google.com

Competition centered on yield-improvement, IP defense, and vertical collaboration. Suppliers diversified rare-earth sources to hedge volatility, while joint ventures with furnace builders reduced commissioning times in emerging regions. The optical ceramics market continued to balance consolidation in defense applications against an expanding ecosystem of niche healthcare and energy suppliers.

Optical Ceramics Industry Leaders

Surmet Corporation

CoorsTek Inc.

CeramTec GmbH

Schott AG

Kyocera Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Coherent Corp. launched 50 W pump laser diodes that boosted fiber-laser output power by 40%, reducing diode count per system and improving materials-processing economics.

- April 2025: CoorsTek Inc. committed USD 30 million to expand optical ceramics production in Colorado, focusing on large transparent armor panels.

- March 2025: Surmet Corporation won a USD 25 million U.S. DoD contract to develop lighter ALON armor for military vehicles.

- February 2025: CeramTec GmbH introduced high-performance ceramic YAG parts for medical lasers with superior heat dissipation.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the optical ceramics market as all newly manufactured, fully dense crystalline or polycrystalline parts that transmit ultraviolet, visible, or infrared light and are supplied as windows, lenses, domes, or armor plates to original-equipment makers and system integrators. According to Mordor Intelligence, electronics-grade glass, phosphors, glazing ceramics, and recycled or repair-grade material lie outside this scope.

Scope Exclusion: Refabrication services and scrap recovery are not valued.

Segmentation Overview

- By Material Type

- Yttrium Aluminum Garnet (YAG)

- Aluminum Oxynitride (ALON)

- Spinel

- Sapphire

- Yttria

- Others

- By Fabrication Method

- Solid-state Sintering

- Hot Isostatic Pressing (HIP)

- Vacuum Sintering

- Others

- By Product Type

- Polycrystalline

- Monocrystalline

- By Application

- Transparent Armor and Bullet-resistant Windows

- Sensor and Imaging Optics

- Laser and Lighting Components

- Medical Imaging and Diagnostics

- LEDs and Phosphors

- Energy and Power Generation Optics

- Others

- By End-Use Industry

- Aerospace and Defense

- Healthcare

- Energy

- Consumer Electronics

- Industrial and Manufacturing

- Research and Instrumentation

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Nordics (Sweden, Finland, Norway, Denmark)

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- Taiwan

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts speak with furnace engineers, defense procurement officers, industrial-laser OEM buyers, and Asian sapphire-boule vendors across North America, Europe, and APAC. These interviews confirm price spreads, scrap ratios, and adoption curves that secondary sources only suggest.

Desk Research

We first map global output using open customs codes, defense contract logs, and trade-group bulletins such as SPIE optics proceedings, the European Ceramic Society yearbook, U.S. ITC import tables, and Japan METI production data. Company 10-Ks, investor decks, and national patent gazettes illustrate capacity shifts, while D&B Hoovers and Dow Jones Factiva supply revenue splits and plant counts that anchor preliminary estimates. The sources listed are illustrative; numerous other public and subscription datasets support data collection, cross-checks, and clarification.

Market-Sizing & Forecasting

We reconstruct demand top-down from production and trade volumes, then validate totals with sampled average-selling-price × volume roll-ups for key suppliers. Inputs such as HIP furnace throughput, transparent-armor penetration rates, laser-diode shipments, aerospace budget cycles, typical 150 mm plate yields, and regional ASP gaps feed a multivariate regression that projects values to 2030. Selective bottom-up supplier checks close residual gaps.

Data Validation & Update Cycle

Outputs pass anomaly scans, peer reviews, and a senior sign-off. Reports refresh each year, with interim updates triggered by material events like large defense awards or new high-pressure sintering capacity.

Why Mordor's Optical Ceramics Baseline Commands Confidence

Published figures vary because some studies count only sapphire optics, others fold in all advanced ceramics, and currency bases or refresh cadences differ.

Key gap drivers include inconsistent scope, unverified ASP paths, and outdated source years. Mordor's disciplined segmentation, annual refresh, and dual-path modeling minimize these pitfalls and keep our baseline dependable for planners.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 620 million (2025) | Mordor Intelligence | - |

| USD 348 million (2024) | Regional Consultancy A | Omits infrared-armor demand; optics-only scope |

| USD 250 million (2024) | Trade Journal B | Relies on patent-count proxies, lacks producer financials |

| USD 1.8 billion (2023) | Global Consultancy C | Bundles structural, electronic, and optical ceramics |

The comparison shows that, by selecting the right boundary, validating each driver with field specialists, and refreshing data promptly, Mordor Intelligence delivers a transparent, repeatable market baseline that decision-makers can trust.

Key Questions Answered in the Report

What was the optical ceramics market size in 2026, and how fast will it grow?

The optical ceramics market size reached USD 696.8 million in 2026 and is projected to expand at a 12.38% CAGR to USD 1.25 billion by 2031.

Which material type dominates the optical ceramics market?

YAG led with 29.85% market share in 2025, valued for its versatility across lasers, scintillators, and industrial optics.

Why are transparent ceramics preferred over glass in armor applications?

ALON and spinel panels cut weight by up to 60% while maintaining ballistic protection, improving vehicle mobility, and fuel efficiency.

Which region is the fastest-growing market for optical ceramics?

The Middle East and Africa region is the fastest, posting an 10.98% CAGR between 2026-2031, driven by airborne sensor and defense upgrades.

What are the main manufacturing challenges in large optical ceramic components?

Yield losses above 15% for parts exceeding 120 mm in diameter raise costs, largely due to micro-crack formation and densification issues during sintering.

Page last updated on: