Outsourced TIC Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

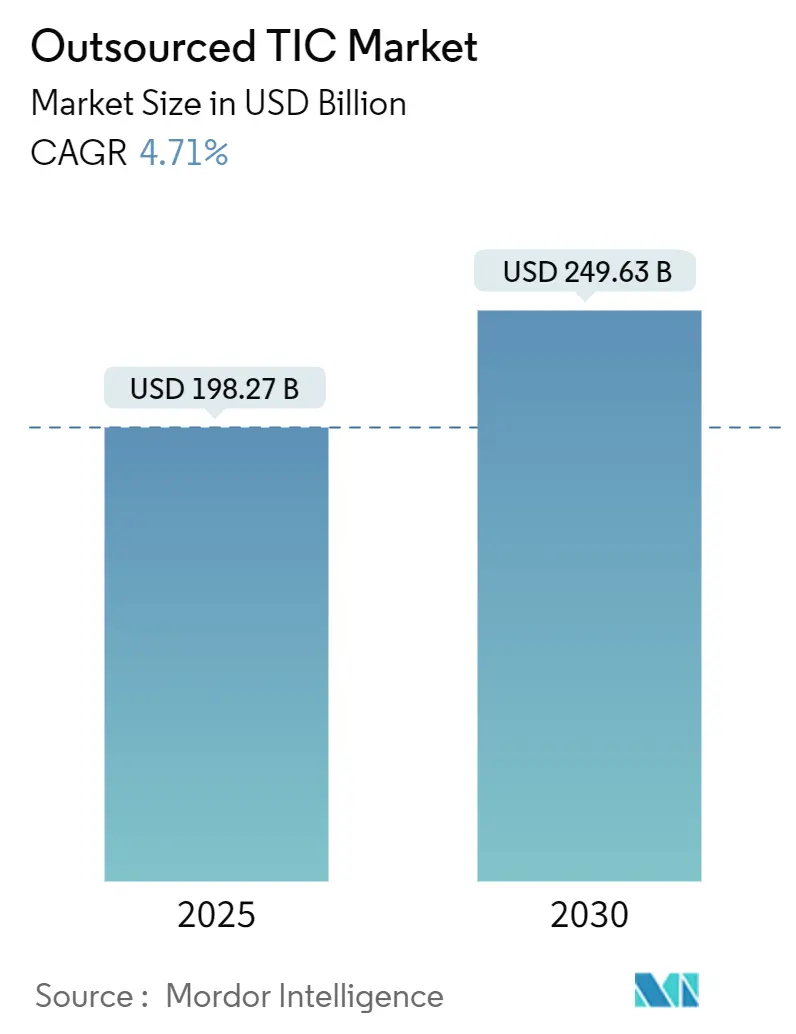

| Market Size (2025) | USD 198.27 Billion |

| Market Size (2030) | USD 249.63 Billion |

| Growth Rate (2025 - 2030) | 4.71% CAGR |

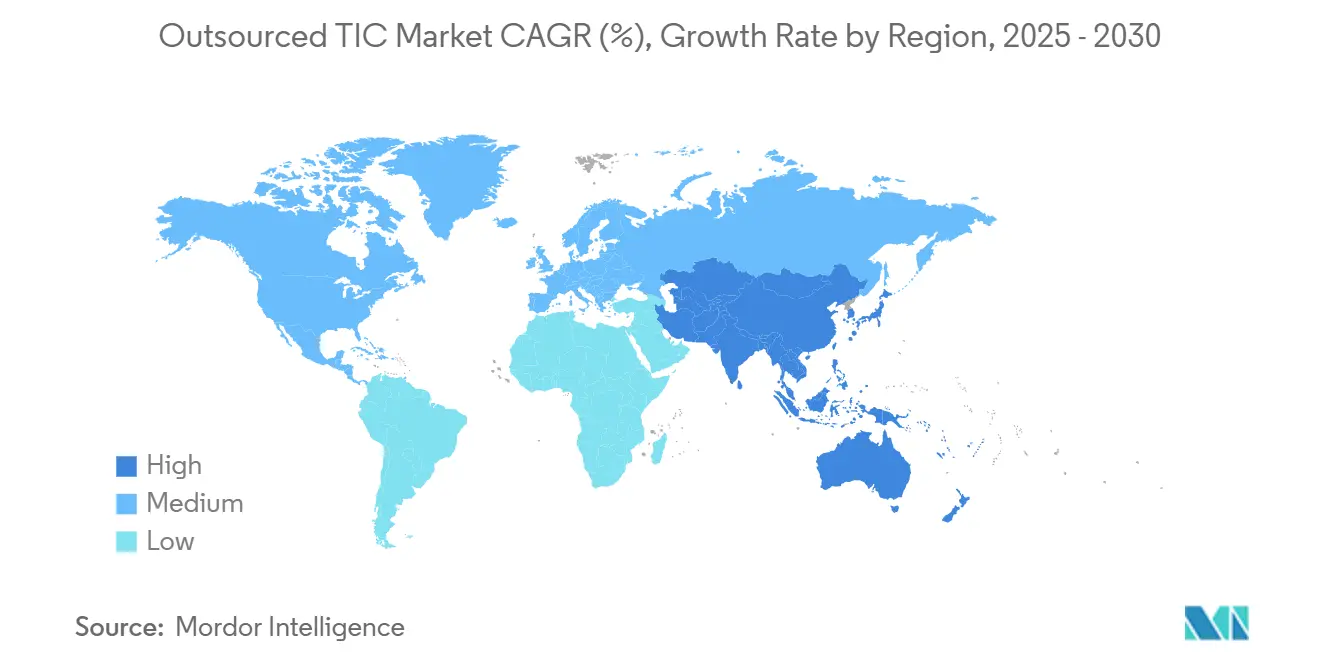

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

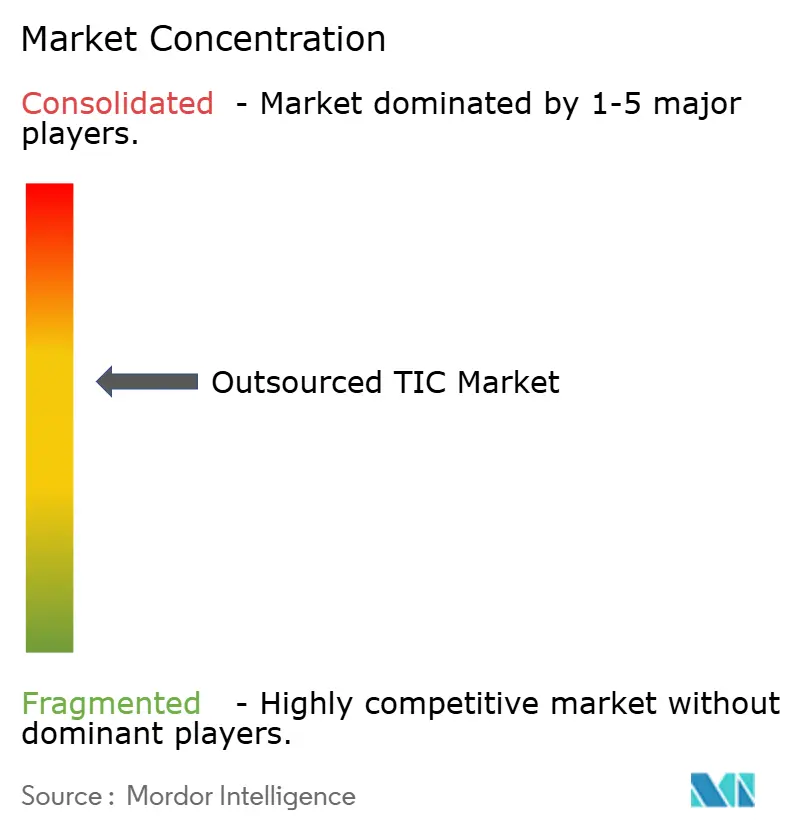

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Outsourced TIC Market Analysis by Mordor Intelligence

The global outsourced testing, inspection certification market size reached USD 198.27 billion in 2025 and is projected to climb to USD 249.63 billion by 2030, advancing at a 4.71% CAGR. Strengthening cross-border trade rules, proliferating ESG mandates, and the pivot to technology-enabled verification are together expanding the breadth of services companies demand, moving the focus from simple compliance checks to real-time supply-chain integrity, carbon disclosure assurance, and digital credentialing requirements. Testing remains the core service, but certification, underpinned by digital seals and sustainability labels, is accelerating. Asia-Pacific continues to anchor new revenue as regulatory harmonization cuts duplicate testing, while remote inspection tools, from IoT sensors to drone imaging, compress turnaround times and labor costs.[1]“Tech-Enabled Surveys,” Bureau Veritas Marine and Offshore, MARINE-OFFSHORE.BUREAUVERITAS.COM However, price competition in basic laboratories and shortages of specialists for EV battery and cybersecurity testing temper short-term growth prospects.

Key Report Takeaways

- By service type, Testing led with 55.6% of the Testing inspection certification market share in 2024, while Certification is advancing at a 5.1% CAGR through 2030.

- By industry vertical, Consumer Goods and Retail contributed 24.3% revenue in 2024; Food, Agriculture, and Beverage is forecast to expand at a 5.3% CAGR to 2030.

- By mode of service delivery, On-site commanded 55.3% of the Testing inspection certification market size in 2024, whereas Remote/Digital services recorded the highest projected 6.1% CAGR.

- By geography, Asia-Pacific accounted for 45.4% of 2024 revenue and is set to rise at a 5.6% CAGR during the outlook period.

Global Outsourced TIC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing cross-border regulations and trade volumes | +1.2% | Global, with early gains in the USMCA, EU-MERCOSUR corridors | Medium term (2-4 years) |

| Increasing supply-chain complexity in digital and physical goods | +0.9% | Asia-Pacific core, spill-over to North America and the EU | Long term (≥ 4 years) |

| Stringent regulatory standards in emerging markets | +0.8% | Asia-Pacific, Middle East, Latin America | Medium term (2-4 years) |

| Shift to remote and digital inspection enabled by IoT and AI analytics | +1.1% | Global, with North America and the EU leading adoption | Short term (≤ 2 years) |

| ESG and carbon-footprint verification mandates | +0.7% | EU leading, expanding to North America and Asia-Pacific | Medium term (2-4 years) |

| Rapid certification demand for additive-manufacturing supply chains | +0.4% | North America and EU aerospace/automotive hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Cross-Border Regulations and Trade Volumes

Escalating export-import checks are channeling fresh business toward the Testing, inspection certification market. Mexico’s complemento Carta Porte requirement and the forthcoming U.S. CPSC eFiling rule obligate electronic documentation and pre-clearance for millions of consignments.[2]“Simplifying Compliance with New U.S. CPSC eFiling Requirements,” SGS, SGS.COM Canada’s customs agency is intensifying tariff-classification audits, and the EU’s Carbon Border Adjustment Mechanism adds verified carbon data to the customs entry checklist. These synchronized policies elevate third-party inspection demand along the entire trade pipeline, especially among small exporters lacking in-house compliance teams. Sustained policy roll-outs across 2026-2028 keep the revenue tail long for service providers.

Increasing Supply-Chain Complexity in Digital and Physical Goods

Converging hardware, software, and connectivity pushes corporate buyers toward multipronged verification solutions that span safety, cybersecurity, and interoperability. ISO/ASTM 52920:2023 and UL’s Blue Card program formalize additive-manufacturing process control, while IoT devices require simultaneous electromagnetic, protocol, and data-integrity testing. Blockchain-based traceability frameworks must be audited for algorithmic accuracy as well as raw-data provenance, expanding the Testing, inspection, and certification market into software code review and AI model validation.

Stringent Regulatory Standards in Emerging Markets

Emerging economies now mirror advanced regulatory playbooks, creating new addressable pockets for international laboratories. China issued 47 food standards in 2024, covering adhesives to pre-cooked meals, while South Korea updated food-contact norms and Hong Kong pivoted to ASTM F963-23 toy safety benchmarks. African and Gulf nations have widened product-conformity schemes, prompting exporters to secure certificates before shipment. These policies funnel consistent, high-margin work toward accredited bodies with multi-country footprints, reinforcing the Testing, inspection certification market’s role in emerging trade lanes.

Shift to Remote and Digital Inspection Enabled by IoT and AI Analytics

Remote survey platforms cut travel costs, shrink downtime, and unlock specialist expertise on demand. Bureau Veritas operates more than 125 remote surveyors across eight hubs, augmenting them with automated defect recognition that converts video feeds into actionable data. Industrial users report 35% fewer detection errors and 50% faster cycle times when AI-vision tools replace manual checks. Savings such as Safran Aircraft Engines’ EUR 2 million annual reduction (USD 2.1 million) reinforce ROI narratives, accelerating remote adoption inside the Testing, inspection certification market. Yet cybersecurity assurance remains critical, as unauthorized video retrieval or sensor tampering can invalidate audit trails.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price pressure from the commoditization of basic testing services | -0.8% | Global, with intense competition in the Asia-Pacific | Short term (≤ 2 years) |

| High cost of acquiring and retaining specialized auditors | -0.6% | North America and the EU, expanding to the Asia-Pacific | Medium term (2-4 years) |

| Cybersecurity liability risk in remote inspection platforms | -0.4% | Global, with a higher impact in regulated industries | Short term (≤ 2 years) |

| Talent shortage for next-gen battery and EV safety testing | -0.5% | Global, concentrated in automotive hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Pressure from Commoditization of Basic Testing Services

Growing transparency in laboratory pricing erodes margins for routine analyses, pushing providers into price-based competition. Auction portals openly list assays, and clients down-select on cost rather than reputation, a trend that empirical research links to shrinking differentiation power. International networks must therefore pivot toward complex or integrated engagements to preserve value, re-bundling inspection and certification to offset unit-price erosion in the Testing, inspection certification market.

Talent Shortage for Next-Gen Battery and EV Safety Testing

Advanced chemistries and high-energy systems require qualified engineers who understand thermal runaway, software controls, and evolving UNECE regulations. Assessments show critical reading-of-graphics skills gaps even among degreed workers, exposing a latent risk to service quality.[3]“A Better Measure of Skills Gaps,” ACT, ACT.ORG Visa programs and digital training platforms are being scaled, yet the vacancy pipeline remains long. Limited staffing capacity delays project start dates and constrains revenue capture in high-value sectors inside the Testing, inspection certification market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Certification Gains Momentum through Digital Credentials

Testing captured 55.6% of the outsourced testing inspection certification market share in 2024, sustaining its primacy as the cornerstone of safety and performance validation across products and processes. The outsourced testing inspection certification market size for certification grew fastest, registering a 5.1% CAGR that is forecast to continue through 2030 as enterprises embrace blockchain-secured certificates, recycled-content labels, and ESG attestations to meet procurement requirements. Vendors are layering cybersecurity audits and supply-chain traceability seals onto core functional testing to offer integrated packages that address multi-disciplinary compliance.

Certification’s traction also reflects regulators’ preference for audited programs over post-hoc inspections. ISO/ASTM frameworks for additive manufacturing, for instance, stipulate qualified processes and personnel rather than spot testing of end parts, steering spend toward credential-based assurance. In marine and aviation, remote verification shortens lead times while feeding digital twins that archive evidence for regulators, amplifying value addition within this segment of the Testing, Inspection Certification industry.

By Industry Vertical: Food Standards Accelerate Agricultural Testing Demand

Consumer Goods and Retail retained top billing with 24.3% of 2024 revenue, reflecting large SKU counts and brand-risk exposure to safety lapses. Yet the food, agriculture, and beverage segment is scaling more rapidly at a 5.3% CAGR, lifting its contribution to the Testing inspection certification market size by the end of the decade. China’s 47 fresh food standards, South Korea’s revised contact-material rules, and Gulf conformity schemes all require multi-parameter laboratory support, boosting test volumes.

Traceability platforms leveraging QR codes and blockchain win adoption among growers and retailers aiming to demonstrate pesticide residue compliance and carbon intensity. This creates downstream demand for certificate issuance and data-quality audits, binding testing laboratories more tightly into digital supply chains. Adjacent momentum in automotive battery qualification and aerospace additive manufacturing also nudges aerospace and transportation to tap specialized laboratories, preserving the Testing, inspection certification market’s diversification profile.

By Mode of Service Delivery: Remote Platforms Reshape Inspection Economics

On-site visits still delivered 55.3% of 2024 revenue, but remote and digital offerings now post a 6.1% CAGR, reshaping customer expectations across the Testing inspection certification market. Real-time video streaming, autonomous drone capture, and AI-assisted analytics allow experts to diagnose faults without stepping onto the facility floor, trimming travel budgets and widening geographic reach.

Hybrid models that pair in-person vouching for critical safety points with remote follow-ups are gaining favor, especially in heavy-industry turnarounds and offshore energy. Off-site laboratories remain indispensable for complex metallurgical, chemical, and microbiological tests where controlled environments and specialized instruments are mandatory. Yet even these labs integrate cloud-based LIMS and data ports that feed dashboards used in remote audits, underscoring convergence inside the Testing, inspection certification industry.

Geography Analysis

Asia-Pacific generated 45.4% of 2024 revenue and is forecast to grow at a 5.6% CAGR, consolidating its lead in the outsourced testing, inspection certification market. Mutual recognition among 47 accreditation bodies eases cross-border product flow, while national authorities enact detailed sectoral rules from electronics to packaged food. China’s rapid new-standard pipeline and South Korea’s alignment with EU toy and food contact directives stoke laboratory utilization.

North America records steady demand, driven by ESG disclosures and digital filing mandates such as the U.S. CPSC eFiling system starting July 2026. Canada’s customs verification priorities and Mexico’s electronic transport documentation extend the compliance envelope along the USMCA corridor. European Union rules, notably the Corporate Sustainability Reporting Directive, add compulsory third-party assurance, anchoring a resilient revenue stream for providers positioned with ESG expertise.

The Middle East, Africa, and Latin America deepen their reliance on accredited conformity programs. SGS alone administers product-approval schemes across more than 20 African and Gulf states, lowering border delays and counterfeiting risks. Nearshoring trends propel Mexico’s laboratory footprint expansion, while Gulf infrastructure projects demand welding procedures and materials certifications. Collectively, these regions broaden the Testing inspection certification market’s growth runway beyond its historic power centers.

Competitive Landscape

The industry remains moderately concentrated, giving both conglomerates and specialists room to maneuver. Failed merger talks between SGS and Bureau Veritas in January 2025, valued near USD 35 billion, underscore integration risks in a regulation-fragmented arena. SGS instead pursues serial bolt-ons, adding Accutest for environmental assays and Beta Analytic for Carbon-14 dating to secure niche competencies.[4]“SGS Acquires US Enviro Lab Firm Accutest,” Environment Analyst, ENVIRONMENT-ANALYST.COM

Bureau Veritas differentiates through tech investments, fielding remote survey centers that blend AI defect detection with digital twins to shorten class-renewal cycles. Intertek scales battery and energy-storage labs, while Element extends IoT device validation that stitches together hardware, firmware, and cybersecurity tests. UL Solutions deepens additive-manufacturing credentials, issuing Blue Cards for 3D-printing materials and certifying end-use parts to streamline OEM approvals.

Competitive edges increasingly hinge on proprietary software, analytics, and data custody. Providers that assure chain-of-custody for emissions data or encrypt remote inspection streams at the edge can command premium rates. Conversely, low-barrier routine tests remain susceptible to price undercutting, pressuring laboratories to automate and digitize. The Testing inspection certification market’s next phase of consolidation is thus likely to pivot around technology portfolios rather than mere geographic overlap.

Outsourced TIC Industry Leaders

SGS SA

Bureau Veritas SA

Intertek Group plc

TÜV SÜD AG

TÜV Rheinland AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Xybion released LIMS 10.0, an AI-enabled laboratory information system that accelerates reporting timelines.

- January 2025: SGS and Bureau Veritas ended merger talks after exploring a potential USD 33–35 billion combination.

- January 2025: SGS bought Accutest Laboratories, adding 620 staff and bolstering PFAS testing capacity.

- January 2025: The U.S. CPSC finalized mandatory e-Filing for import compliance certificates, effective Jul 2026.

Global Outsourced TIC Market Report Scope

| Testing |

| Inspection |

| Certification |

| Consumer Goods and Retail |

| ICT and Telecom |

| Automotive and Transportation |

| Aerospace and Defense |

| Oil, Gas and Petrochemicals |

| Energy and Utilities |

| Industrial Manufacturing and Machinery |

| Chemicals and Materials |

| Construction and Infrastructure |

| Life Sciences and Healthcare |

| Food, Agriculture and Beverage |

| Other Industry Verticals (Environment, Sustainability, etc.) |

| On-site |

| Off-site/Laboratory |

| Remote / Digital |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | Testing | ||

| Inspection | |||

| Certification | |||

| By Industry Vertical | Consumer Goods and Retail | ||

| ICT and Telecom | |||

| Automotive and Transportation | |||

| Aerospace and Defense | |||

| Oil, Gas and Petrochemicals | |||

| Energy and Utilities | |||

| Industrial Manufacturing and Machinery | |||

| Chemicals and Materials | |||

| Construction and Infrastructure | |||

| Life Sciences and Healthcare | |||

| Food, Agriculture and Beverage | |||

| Other Industry Verticals (Environment, Sustainability, etc.) | |||

| By Mode of Service Delivery | On-site | ||

| Off-site/Laboratory | |||

| Remote / Digital | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the outsourced testing, inspection certification market by 2030?

The market is forecast to reach USD 249.63 billion in 2030.

Which service segment is growing fastest?

Certification services are posting the quickest expansion at a 5.1% CAGR.

Which region leads revenue contribution?

Asia-Pacific accounts for the largest share at 45.4% of 2024 revenue.

How fast are remote and digital inspection services expanding?

Remote/Digital delivery is advancing at a 6.1% CAGR through 2030.

What factor most pressures margins in basic testing?

Price competition driven by the commoditization of routine assays is the primary margin constraint.

Which vertical is adding the most new demand?

Food, agriculture, and beverage are the fastest-growing verticals, expanding at a 5.3% CAGR.

Page last updated on: