Electronics And Electrical Testing, Inspection, And Certification Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

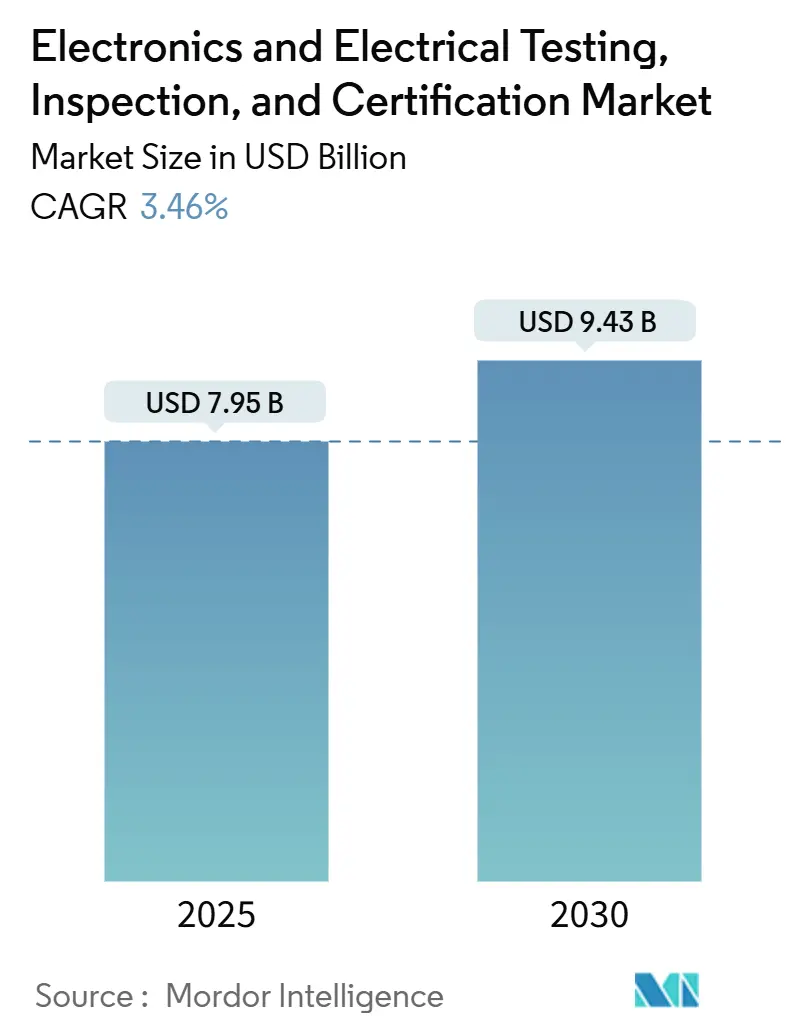

| Market Size (2025) | USD 7.95 Billion |

| Market Size (2030) | USD 9.43 Billion |

| Growth Rate (2025 - 2030) | 3.46% CAGR |

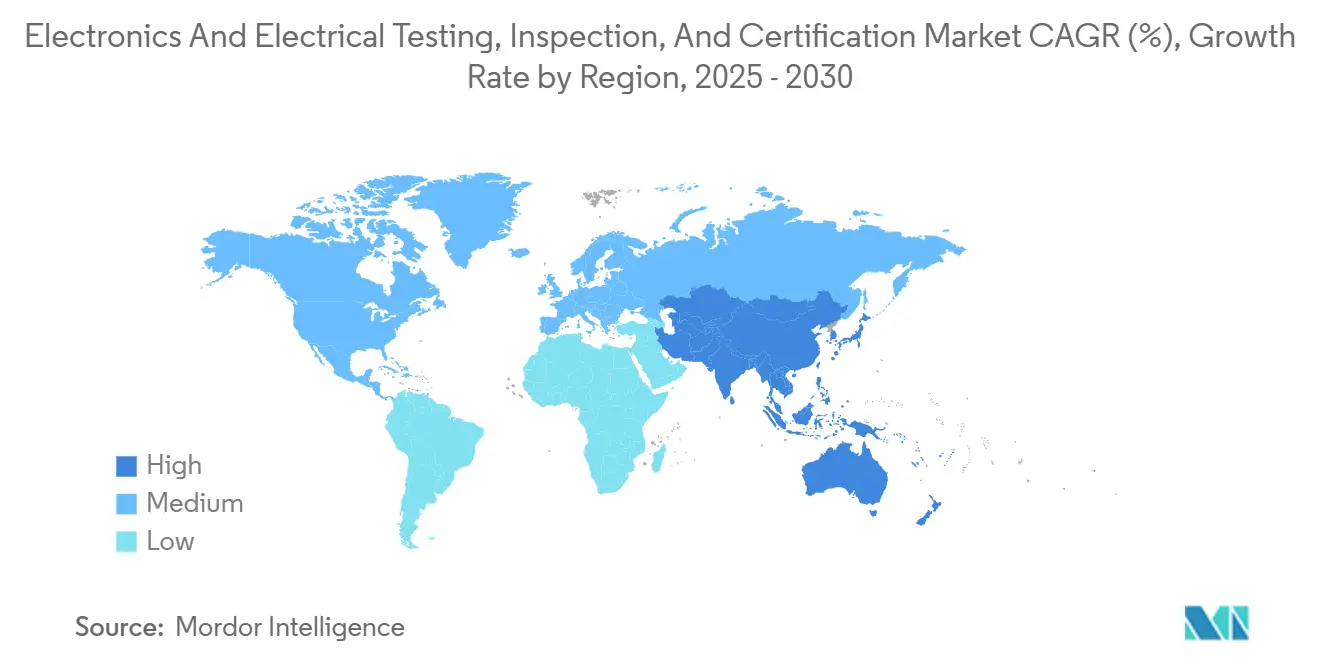

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

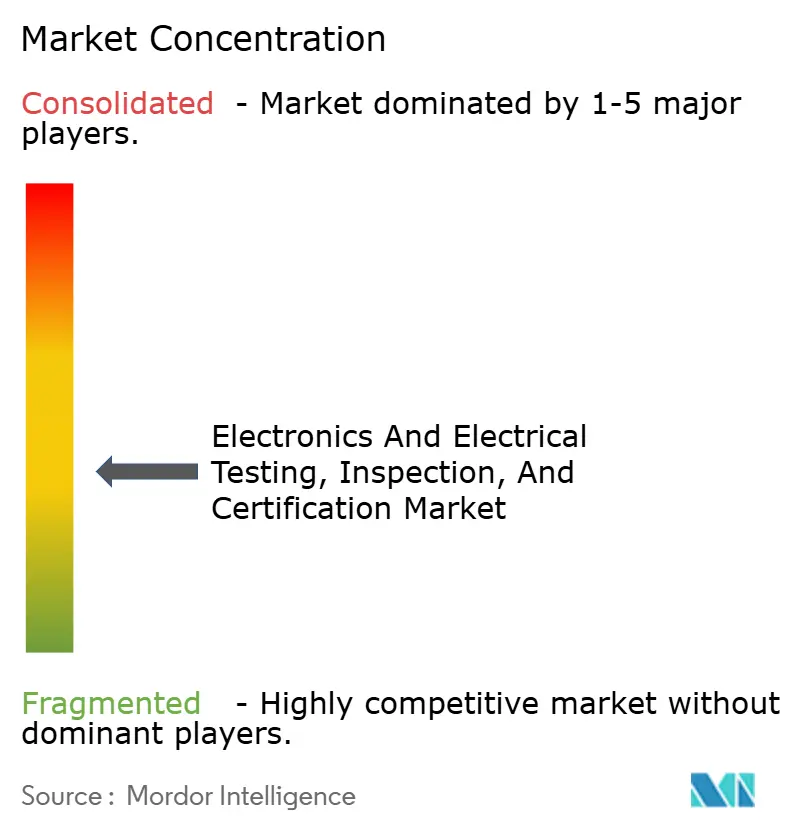

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electronics And Electrical Testing, Inspection, And Certification Market Analysis by Mordor Intelligence

The electronics and electrical testing, inspection, and certification market size was USD 7.95 billion in 2025 and is projected to reach USD 9.43 billion by 2030, representing a 3.46% CAGR over the forecast period. This steady expansion relies on mandatory safety and electromagnetic-compatibility (EMC) assessments that cannot be postponed when new consumer devices, automotive modules, or industrial controls are introduced. Intensifying global regulations, most notably the European Union’s Radio Equipment Directive and the United States Cyber Trust Mark program, add new certification layers that increase testing volumes. Asia-Pacific manufacturing output, renewable-energy electronics deployment, and ESG-linked product traceability rules combine to preserve demand even when hardware cycles cool. Providers with multi-jurisdictional accreditations secure a structural advantage because they can deliver a single test program that satisfies diverse national rules. Digital investments in automated inspection, remote witness testing, and AI-enabled quality analytics further boost provider margins by trimming labor time while improving throughput.

Key Report Takeaways

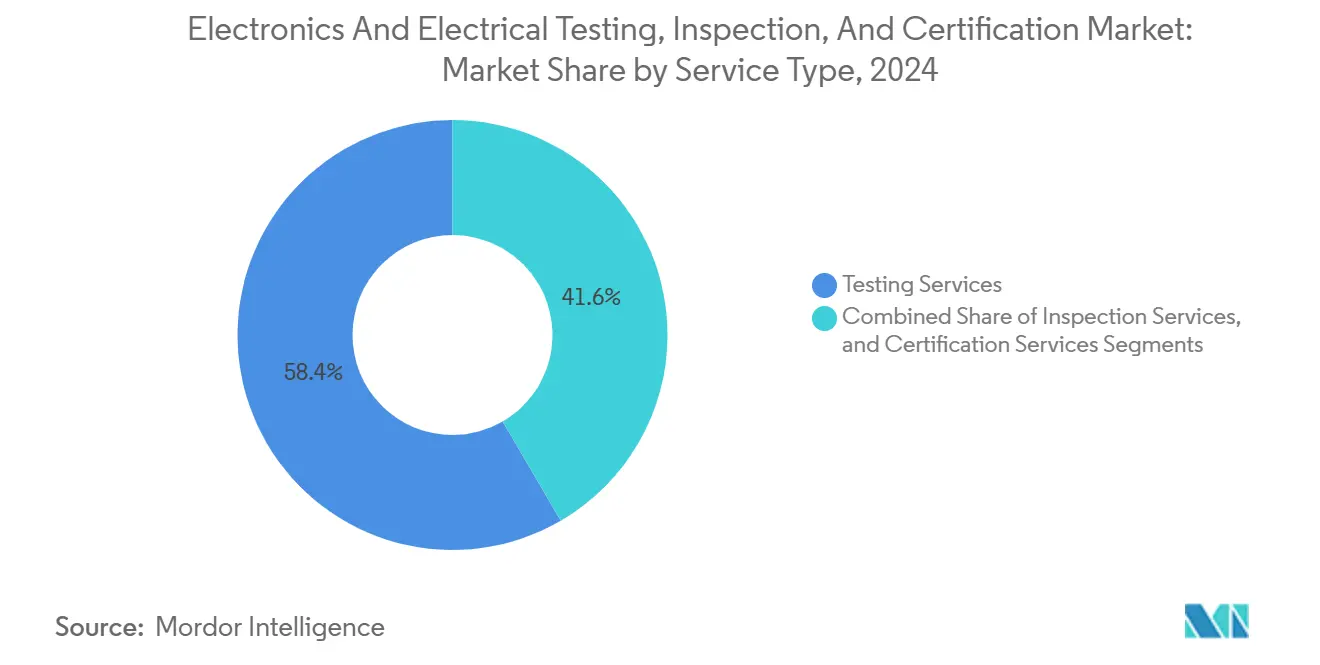

- By service type, testing services led with 58.4% revenue share of the electronics and electrical testing, inspection, and certification market in 2024, while certification services are projected to advance at a 4.2% CAGR to 2030.

- By sourcing type, outsourced programs captured 72.4% of the electronics and electrical testing, inspection, and certification market share in 2024 and are forecast to post a 3.7% CAGR through 2030.

- By geography, the Asia-Pacific region accounted for a 47.9% revenue share of the electronics and electrical testing, inspection, and certification market in 2024 and is projected to grow at a 4.5% CAGR through 2030.

Global Electronics And Electrical Testing, Inspection, And Certification Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Compliance stringency for safety and EMC norms | +0.8% | Global, with the EU and North America leading | Medium term (2-4 years) |

| Rapid IoT-linked device proliferation | +0.9% | Asia-Pacific core, spill-over to North America and the EU | Short term (≤ 2 years) |

| Outsourcing trend to neutral third-party labs | +0.6% | Global, particularly strong in Asia-Pacific manufacturing hubs | Long term (≥ 4 years) |

| Expansion of renewable-energy electronics | +0.7% | EU and North America leading, Asia-Pacific following | Medium term (2-4 years) |

| Edge-AI-driven automatic inspection adoption | +0.5% | North America and the EU early adoption, Asia-Pacific scale deployment | Long term (≥ 4 years) |

| ESG-led demand for circular-electronics auditing | +0.4% | EU regulatory leadership, North America corporate adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Compliance-Stringency for Safety and EMC Norms

Tighter regional statutes and faster update cycles oblige manufacturers to run more test iterations before product launch. Laboratories accredited for multiple standards leverage this trend because customers prefer consolidated reporting that accelerates market entry.[1]SGS, “About SGS TIC,” sgs.com Sales of combined safety-plus-cybersecurity assessment packages expanded throughout 2024 as vendors sought one-stop solutions for new smart-home and medical devices. Authorities in the EU and the United States continue to widen the scope of mandatory conformity, which effectively turns testing into a recurrent operational cost rather than a discretionary engineering task.

Rapid IoT-Linked Device Proliferation

The count of connected endpoints grows every quarter, multiplying the radio-frequency permutations that must be proven interference-free. Bureau Veritas reported double-digit growth in projects involving products that host Bluetooth, Wi-Fi, and cellular radios on a single board during 2024. Each additional protocol raises EMC complexity because mutual coexistence tests cover dozens of power-level and frequency scenarios as 5G modules become mainstream, laboratory backlogs lengthen, prompting suppliers to reserve capacity months ahead, which secures predictable test revenues.

Expansion of Renewable-Energy Electronics

Grid-tied solar inverters and battery-energy-storage controllers require anti-islanding, harmonic, and cyber-resilience evaluations unavailable in many legacy EMC chambers. TÜV Rheinland invested in purpose-built power-electronics benches at its Massachusetts site in 2024 to meet this niche demand.[2]TÜV Rheinland, “Renewable Energy Laboratory Investments,” tuv.com Utility operators now request third-party validation before allowing new hardware onto distribution networks, turning renewable-energy electronics into a premium test segment insulated from consumer-device seasonality.

ESG-Led Demand for Circular-Electronics Auditing

Corporate pledges and pending EU Digital Product Passport rules drive audits that trace component sourcing, recyclability, and carbon footprint. UL Solutions expanded its verification programs to cover recycled plastics and hazardous-substance elimination in 2024. These audits rely on chemical spectroscopy, documentary review, and on-site inspections, adding high-margin engagements on top of core performance tests. Because sustainability claims face public scrutiny, brands are increasingly insisting on accredited labs, thereby bolstering the electronics and electrical testing, inspection, and certification market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cap-ex for state-of-the-art labs | -0.4% | Global, particularly challenging for emerging markets | Long term (≥ 4 years) |

| Fragmented global regulatory regimes | -0.3% | Global, with complexity highest in cross-border operations | Medium term (2-4 years) |

| Shortage of certified TIC professionals | -0.2% | North America and the EU have acute concerns, and the Asia-Pacific has emerging concerns. | Short term (≤ 2 years) |

| Cybersecurity liability for connected devices | -0.3% | Global, with regulatory leadership in the EU and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cap-Ex for State-of-the-Art Labs

Millimeter-wave test chambers, high-frequency vector network analyzers, and climate-stress rigs now cost up to USD 10 million per line. TÜV Rheinland disclosed a multi-million-dollar outlay for its Massachusetts expansion in 2024, reflecting the capital wall newcomers face. The expense prolongs payback periods and sidelines smaller regional labs from next-generation projects, slowing capacity growth even while demand rises.

Fragmented Global Regulatory Regimes

Manufacturers shipping worldwide must navigate mutually inconsistent rules such as the EU EN 303 645 cyber standard, the US Cyber Trust Mark, and divergent Asian specifications. The World Trade Organization flagged a rise in technical trade barriers during 2024, highlighting regulatory divergence as a cost amplifier for exporters.[3]World Trade Organization, “World Trade Report 2023,” wto.org Additional test loops and documentation cycles inflate budgets and delay product launches, tempering overall market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Testing Services Remain the Revenue Anchor While Certification Gains Speed

Testing services accounted for 58.4% of 2024 revenue, confirming their bedrock role in qualifying designs before shipment. The electronics and electrical testing, inspection, and certification market size for this segment is forecast to increase at a 3.1% CAGR, supported by recurring EMC refreshes whenever wireless protocols evolve. Certification, although smaller, is expected to grow faster at 4.2% because new rules frequently require third-party attestation rather than manufacturer self-declaration. The electronics and electrical testing, inspection, and certification market share commanded by certification service providers is expected to increase as firms require harmonized marks to access multiple jurisdictions within a single launch window. Inspection holds the middle ground by verifying factory controls and supply-chain conformance that anchor both test validity and certification integrity.

Providers are bundling all three activities to lock clients into multiyear frameworks. Element Materials Technology, for example, expanded environmental test chambers in early 2024 to complement its safety and functional testing suites. Integrated service offerings reduce logistical friction and compress project timelines, which is crucial as design-to-launch cycles for smart devices shorten. Price competition is tight for basic vibration or temperature tests, but margins rise sharply when cybersecurity, functional safety, or ESG documentation must be wrapped into the same engagement. The electronics and electrical testing, inspection, and certification market benefits because many small and medium-sized manufacturers lack internal compliance teams and are willing to outsource the entire package.

By Sourcing Type: Outsourcing Dominates as Complexity Outpaces In-House Budgets

Outsourced assignments captured 72.4% of the revenue in 2024 and are expected to expand at a rate of 3.7% annually through 2030, reflecting a structural shift from OEM labs to specialized third parties. The electronics and electrical testing, inspection, and certification market size linked to outsourced work eclipses in-house spending because accredited bodies can amortize equipment over hundreds of customers. Hybrid models are emerging in which providers embed engineers within client plants for prototype debug, then route formal conformity tests to centralized hubs. This setup trims travel delays, helps maintain intellectual property boundaries, and shortens iteration loops.

In-house capabilities persist mainly at top-tier electronics conglomerates that protect proprietary designs. Even these players increasingly seek external accreditation to satisfy regulators who favor impartial verification. super.AI’s document automation, deployed at Bureau Veritas in 2024, reduced turnaround time by 75% and data-entry costs by 80%, illustrating how digital tooling enhances the efficiency of outsourced workflows. As test suites expand to include cyber-resilience, AI logic validation, and life-cycle carbon metrics, the cost gap between dedicated labs and in-house benches will widen further, reinforcing the outsourcing trend across the electronics and electrical testing, inspection, and certification market.

Geography Analysis

Asia-Pacific delivered 47.9% of 2024 revenue and is projected to post a 4.5% CAGR to 2030, outpacing global averages on the back of intensive consumer-electronic and automotive supply-chain activity. China’s regulatory reforms and Japan’s updates to the Product Safety Electrical Appliance and Material Act require multi-round retesting for even minor design tweaks, thereby increasing the test volume per SKU. South Korea’s rising safety certification demands and India’s Wireless Planning and Coordination approvals amplify regional workloads. Because language barriers and nation-specific online portals complicate paperwork, multinational brands place significant value on labs with bilingual staff and established authority liaisons.

North America shows slower unit growth but enjoys premium billing as test scopes widen into renewable-energy electronics, automotive autonomous-drive modules, and official cybersecurity labeling. The United States Cyber Trust Mark, effective since mid-2024, already funnels IoT product lines into dedicated certification pipelines. Parallel incentives for reshoring electronics assembly promote local test capacity, ensuring laboratories remain near both design centers and new factories. Canadian rule alignment with U.S. standards lowers duplication, enabling cross-border providers to leverage equipment continuously.

Europe anchors global thought leadership in ESG and circular-economy criteria. Laboratories here increasingly bundle material-traceability audits with standard EMC checks, responding to upcoming Digital Product Passport mandates. Germany’s power-electronics hubs request complex grid-interconnection simulations, while France and the Netherlands push suppliers to verify recyclability percentages. Post-Brexit, the United Kingdom runs its own UKCA conformity path, adding one more obligatory mark for exporters. European expertise in sustainability testing travels well; several labs license methods abroad, extending the electronics and electrical testing, inspection, and certification market footprint beyond regional borders.

Competitive Landscape

More than 500 entities compete globally, and the top five capture a significant share of turnover, indicating a diffuse structure in which regional specialists thrive beside diversified multinationals.[4]TIC Council, “What Is the TIC Sector,” tic-council.org SGS maintains the broadest geographic network, with a focus on digital customer portals that enable instant scheduling of tests and downloading of reports. Bureau Veritas sharpened its differentiation by integrating AI-driven document processing through super.AI, which cut administrative costs and cemented repeat contracts.

Intertek leverages its Green Services suite to capture ESG compliance work, including verification of recycled content for consumer electronics. Dekra, meanwhile, targets mobility, unveiling specialized certification for Advanced Driver Assistance Systems in 2024 that positions it for autonomous-vehicle safety programs. Eurofins complements breadth with depth; its EAG Laboratories subsidiary supplies materials science failure analysis that few broad-spectrum labs can match, ensuring pull-through contracts whenever contamination or micro-defect crises emerge.

Acquisition momentum persists as major companies seek domain talent and regional footholds that are faster to acquire than to build. Many niche players respond by doubling down on high-complexity tests such as quantum-device cryogenic measurements or chiplet-level electromagnetic modeling. Digital platforms, blockchain-secured certificates, and remote-witness video feeds move from novelty to baseline requirement. Providers lacking these tools risk relegation to low-value commodity tests in the electronics and electrical testing, inspection, and certification market.

Electronics And Electrical Testing, Inspection, And Certification Industry Leaders

SGS Société Générale de Surveillance SA

Bureau Veritas SA

Intertek Group plc

TÜV SÜD AG

TÜV Rheinland AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: EMC Directory projected the global EMC testing segment to reach USD 34.42 billion by 2030 on the strength of 5G, electric-vehicle, and IoT rollouts.

- September 2024: Force Technology upgraded its notified-body designation 0200, maintaining EU Radio Equipment Directive coverage.

- August 2024: NICET expanded technician certification programs to ease workforce shortages in TIC fields.

- July 2024: Eurofins broadened materials science services through its EAG Laboratories division.

Global Electronics And Electrical Testing, Inspection, And Certification Market Report Scope

The Electronics and Electrical Testing, Inspection, and Certification Market Report segments its analysis by Service Type, encompassing Testing, Inspection, and Certification Services. It also differentiates by Sourcing Type, dividing into In-House and Outsourced categories. Geographically, the report spans North America (including the United States, Canada, and Mexico), South America (covering Brazil, Argentina, and the rest of the region), Europe (with a focus on Germany, the United Kingdom, France, Italy, Spain, Russia, and other European nations), Asia-Pacific (highlighting China, Japan, India, South Korea, Southeast Asia, and beyond), and the Middle East and Africa (noting Saudi Arabia, the United Arab Emirates, Turkey, and other nations in the region). All market forecasts are expressed in USD value terms.

| Testing Services |

| Inspection Services |

| Certification Services |

| In-house |

| Outsourced |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | Testing Services | ||

| Inspection Services | |||

| Certification Services | |||

| By Sourcing Type | In-house | ||

| Outsourced | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What value will global electronics and electrical testing, inspection, and certification market generate by 2030?

The electronics and electrical testing, inspection, and certification market size is forecast to reach USD 9.43 billion by 2030, achieving a 3.46% CAGR from 2025.

Which region contributes the most to electronics conformity revenue today?

Asia-Pacific accounted for 47.9% of 2024 revenue, reflecting dense electronics manufacturing hubs and diverse regulatory regimes.

Why are manufacturers increasing reliance on third-party labs?

Expanding regulatory complexity and high cap-ex for advanced chambers make outsourced testing the cost-effective route, which captured 72.4% market share in 2024.

How do sustainability rules influence test demand?

ESG directives such as the EU Digital Product Passport trigger lifecycle auditing requirements that add material-traceability and recycling verification tasks to standard safety tests.

What technologies are reshaping inspection services?

Edge-AI vision systems, blockchain certificate tracking, and remote witness video links are lifting throughput and lowering manual labor across the electronics testing, inspection, and certification market.

Page last updated on: