Mining TIC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.76 Billion |

| Market Size (2031) | USD 5.90 Billion |

| Growth Rate (2026 - 2031) | 4.39% CAGR |

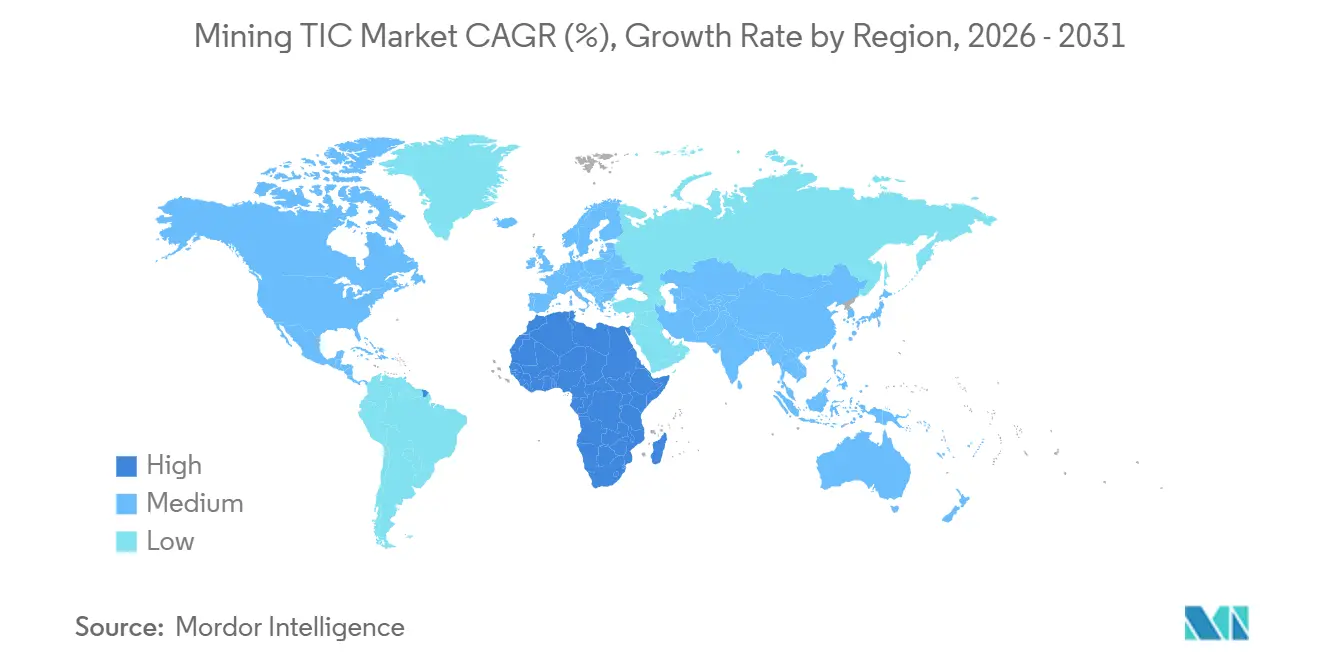

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mining TIC Market Analysis by Mordor Intelligence

The Mining testing, inspection, and certification (TIC) market size was valued at USD 4.56 billion in 2025 and is estimated to grow from USD 4.76 billion in 2026 to USD 5.90 billion by 2031, at a CAGR of 4.39% from 2026 to 2031. Growth is being led by a pivot toward battery-mineral projects, with laboratories reallocating capacity from copper and zinc to lithium, cobalt, and nickel. Outsourced providers are scaling up because junior explorers favor variable-cost models, while autonomous drones, cloud-based core scanners, and machine-learning loggers are compressing turnaround times and lowering inspection risk. Heightened environmental, social, and governance compliance is expanding demand for chain-of-custody certification, and the digital migration of pit-wall, tailings-dam, and conveyor inspections is widening the technical scope of the Mining testing, inspection and certification (TIC) market. Competitive pressure is intensifying as global majors race to acquire regional laboratories and specialized robotics suppliers in emerging battery-mineral corridors.

Key Report Takeaways

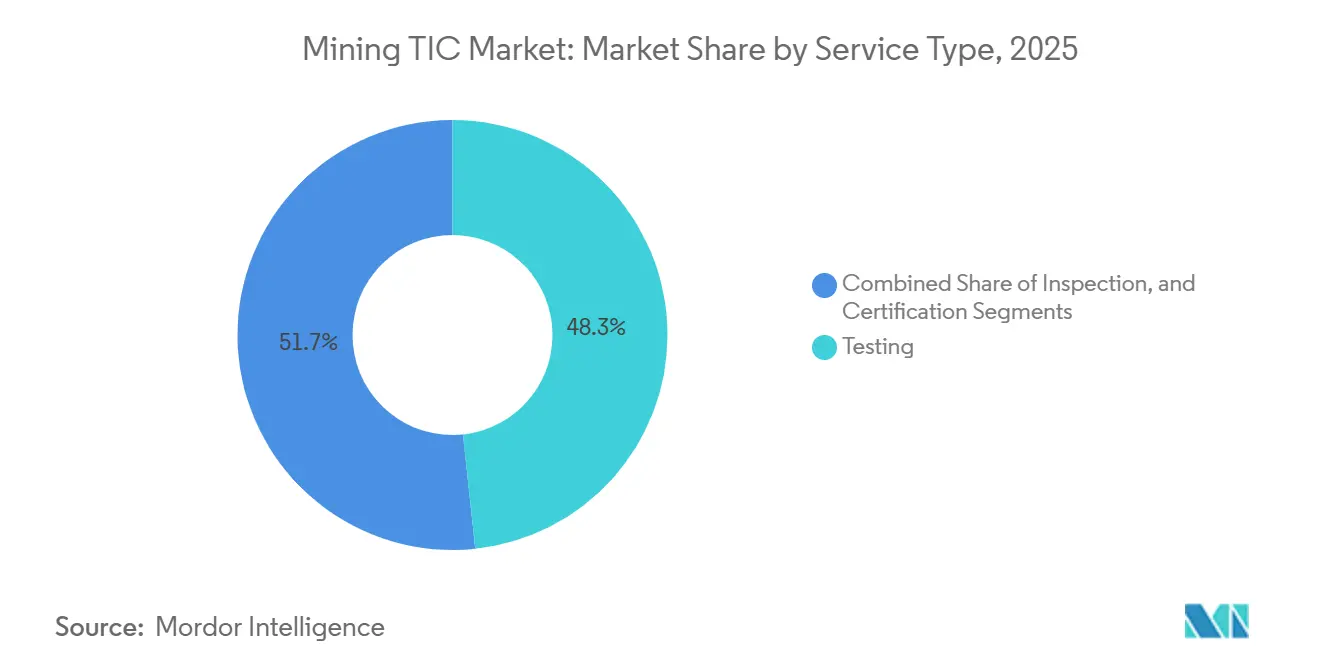

- By service type, testing held 48.31% of mining TIC market share in 2025, while certification is accelerating the fastest at a 4.48% CAGR through 2031.

- By sourcing type, outsourced services captured 64.18% of mining TIC market share in 2025 and are on course to expand at a 5.57% CAGR to 2031.

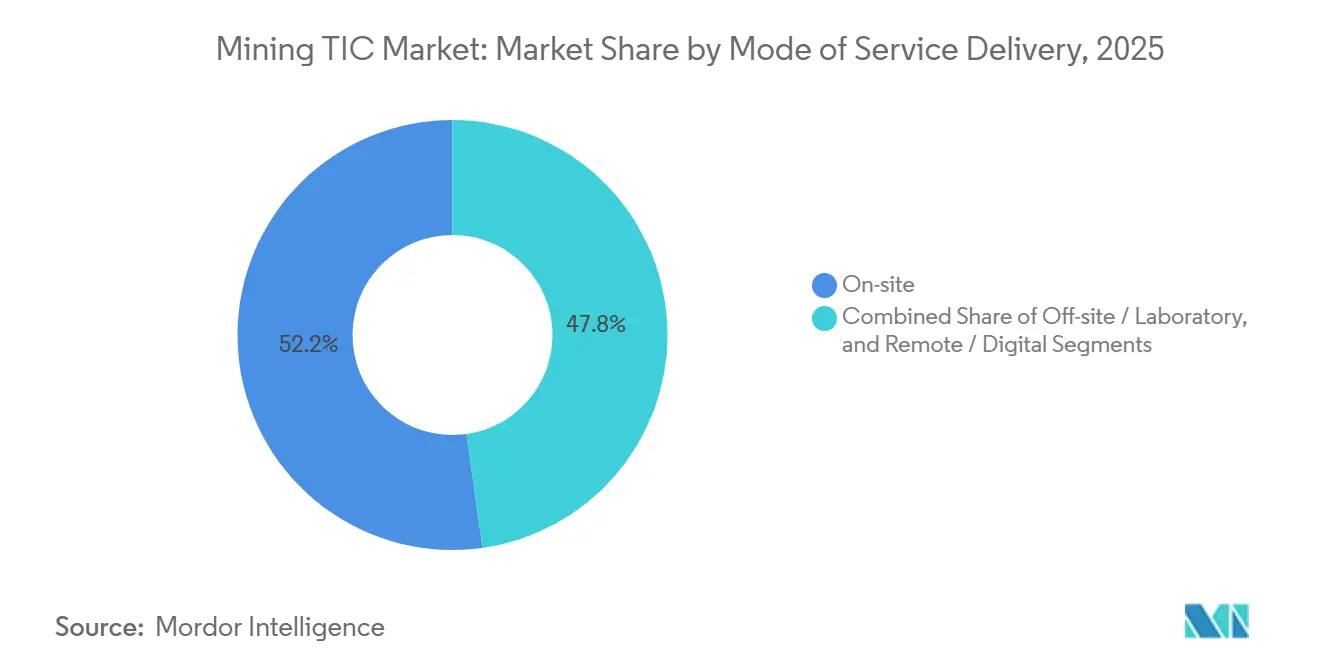

- By mode of service delivery, on-site solutions retained 52.22% of mining TIC market share in 2025, yet remote and digital inspection is advancing at a 5.81% CAGR across the same period.

- By geography, Asia-Pacific commanded 38.28% of mining TIC market share in 2025, whereas Africa is forecast to lead growth at a 5.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mining TIC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Battery-Mineral Exploration Capital | +1.2% | Africa, South America, Australia | Medium term (2–4 years) |

| Heightened ESG Compliance Requirements | +0.9% | Global (led by EU and North America) | Long term (≥4 years) |

| Digital Core Sampling and Automation Adoption | +0.7% | North America, Australia, global spillover | Medium term (2–4 years) |

| Rapid Uptake of Remote and Autonomous Inspections | +0.6% | Remote regions (Canada, Australia, Africa, South America) | Short term (≤2 years) |

| Increasing Depth and Complexity of Ore Bodies | +0.5% | Canada, Australia, South Africa | Long term (≥4 years) |

| Growing Demand for Outsourced TIC in Junior Firms | +0.5% | Canada, Australia, Africa | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Surge in Battery-Mineral Exploration Capital

Battery-mineral budgets climbed 11% across Africa in 2025, reversing a three-year slide in base-metal spending as automakers and battery manufacturers locked in offtake agreements that reduced funding risk for junior explorers. Venture and strategic investors directed USD 2.8 billion into Zimbabwe lithium and Democratic Republic of the Congo cobalt projects, prompting laboratories to add inductively coupled plasma mass spectrometry and X-ray diffraction workflows that command 20% to 30% price premiums over conventional fire assays.[1]SGS SA, “Mining Services Overview,” sgs.com Surge Battery Metals awarded ALS Limited a lithium-hydroxide leach-testing program in April 2026, extending turnaround times and highlighting chronic capacity constraints for complex hydrometallurgical analysis. Century Lithium drilled 12,000 meters and submitted 4,500 assay samples during its February 2026 feasibility study, illustrating the step change in assay volume when projects advance from exploration to pre-feasibility. Downstream pull is also visible, with Electra Battery Materials validating cobalt sulfate purity for automotive specifications in July 2025, drawing Mining TIC market participants deeper into chemical-engineering domains.

Heightened ESG Compliance Requirements

The European Union Corporate Sustainability Reporting Directive and International Sustainability Standards Board rules, effective January 2026, require miners to disclose Scope 3 emissions that encompass contracted laboratories and sample logistics. Anglo American completed Initiative for Responsible Mining Assurance surveillance audits at three operations between January and March 2026, cascading ISO 14064 greenhouse-gas inventories and ISO 50001 energy management requirements to testing, inspection and certification (TIC) providers. Albemarle met the same standard at its Salar de Atacama facility in April 2026, highlighting the tightening link between battery-mineral supply chains and verifiable ESG credentials. TÜV NORD’s CERA 4in1 scheme, launched in January 2026, bundles environmental, social, traceability, and circularity audits into a single engagement, trimming compliance costs for mid-tier producers and creating a new avenue of recurring revenue for Mining TIC market participants. Bureau Veritas responded by introducing an integrated Mine ESG Audit service that merges Towards Sustainable Mining protocols with ISO 26000 social guidance, further widening the certification opportunity set.

Digital Core Sampling and Automation Adoption

Epiroc’s CorePhoto system, deployed in March 2025, photographs drill core and generates automated logs, slashing geologist review time by 40% and reducing the need to ship physical core, a shift that shrinks assay backlogs and improves data fidelity. Orexplore’s GeoCore X10 provides mineral distribution maps within hours, allowing teams to defer non-priority intervals and cut laboratory outlays by up to 35%. Boart Longyear TruScan sends real-time geochemical data from the rig, letting managers adjust programs without multi-week laboratory delays. DMT’s ANCORELOG suite standardizes logging across multi-site campaigns and cuts manual errors by 60%. Sweden’s Vinnova-funded Autolyzer robots aim to reduce sample-preparation labor by 50% by 2027, a timely response to the geochemist shortage confronting the Mining TIC industry.

Rapid Uptake of Remote and Autonomous Inspections

SGS acquired MsMin in February 2026, integrating drone-based pit-wall surveys and autonomous ground rovers to deliver slope-stability and stockpile-volume data without human entry into active zones, saving 30% to 50% on mobilization costs. SafeSight’s DeepTraxx rover completed underground ventilation inspections in South Africa in 2025, streaming LiDAR and gas-sensor data to surface control rooms and eliminating exposure to high-risk stopes. Mistras Group launched its Data Solutions brand in April 2025, merging ultrasonic testing, acoustic monitoring, and robotic crawlers to cut unplanned downtime at Chilean copper sites by 20%. Aurelia Metals digitized contractor compliance via Avetta between 2024 and 2025, trimming administrative overhead 35% and improving regulatory audit trails. Regulators are pushing the trend; Australia raised penalties for confined-space incidents in 2024, spurring operators to adopt robotic inspection wherever technically feasible.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Commodity Price Cycles Curtailing Exploration Budgets | -0.8% | South America (copper), Africa (copper-cobalt), Australia (iron ore) | Short term (≤ 2 years) |

| Shortage of Qualified Geochemists and Inspectors | -0.6% | North America, Australia, Europe, emerging in Africa and South America | Medium term (2-4 years) |

| Rising Cost of On-site Sample Logistics in Remote Regions | -0.3% | Africa, northern Canada, remote Australia, Andean South America | Long term (≥ 4 years) |

| Fragmented Global Regulatory Regimes | -0.2% | Cross-border projects (notably West Africa, Central Asia) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Commodity Price Cycles Curtailing Exploration Budgets

Lithium carbonate prices dropped 46% between early 2024 and late 2025, while nickel slid 37% and cobalt 41%, leading to a 15% to 20% fall in assay volumes at laboratories focused on battery minerals. BHP pared capital spending after a 27% decline in metallurgical coal prices, shifting from greenfield to near-mine work that needs fewer, lower-value assays.[2]BHP Group, “Exploration Budget Update 2025,” bhp.com Junior explorers, which drive more than 80% of outsourced demand, lost USD 1.2 billion in committed financing during 2H 2025, forcing drilling meterage cuts of 25% to 30% and pushing laboratories toward extended payment terms. The pivot to lower-risk programs reduces the need for premium rare-earth or platinum-group-metal assays, which can be 3 times as lucrative as routine work, compressing Mining TIC market margins.

Shortage of Qualified Geochemists and Inspectors

The United States Geological Survey expects 27% of domestic geoscientists to retire by 2029, leaving a 130,000-worker gap that directly affects laboratory throughput and inspection scheduling. The Society for Mining, Metallurgy, and Exploration estimates the industry must replace 221,000 positions by 2029, yet university enrollments fell 15% between 2020 and 2025. Australia’s National Association of Testing Authorities reported in 2025 that 40% of accredited geochemical laboratories faced critical staffing shortfalls, forcing overflow subcontracting to Chile and South Africa with attendant currency and logistics risk. Wage inflation for geochemists hit 8% to 12% in Canada and Australia during 2025, and remote-site premiums add another 30%, straining provider margins. Longer turnaround windows, now stretching from 3 weeks to 6 weeks in peak season, erode client confidence and encourage investment in robotics and automation across the Mining TIC market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Testing Anchors, Sustainability Drives Certification

Testing controlled 48.31% of the Mining TIC market share in 2025, reflecting the centrality of geochemical assays and metallurgical testwork to resource estimation. Certification, although smaller, is expanding at a 4.48% CAGR as ESG pressures draw miners toward third-party chain-of-custody credentials. Inspection sits between the two, growing steadily as automation lowers per-inspection cost and expands technical scope. Testing volume intensity remains high; a mid-tier gold campaign can generate 20,000 samples at USD 30 to USD 80 each, underpinning predictable cash flow for laboratories. Certification demand accelerated after Anglo American, Albemarle, and others embedded the Initiative for Responsible Mining Assurance into annual audit cycles, signaling a structural, not episodic, revenue stream for accredited bodies.

Laboratory operators are upgrading to high-throughput inductively coupled plasma mass spectrometry rigs that accommodate lithium, cobalt, and rare-earth workflows, aligning capacity with surging battery-mineral budgets. TÜV NORD’s CERA 4in1 launch offers a one-stop ESG credential, attracting mid-tier producers that wish to avoid multiple overlapping audits. Drone-assisted pit inspections and rover-based stockpile surveys, gained via SGS’s MsMin acquisition, are extending inspection cycles without adding headcount, boosting contribution margins. As ISO IWA 45:2024 rolls out, certification backlogs are forming, prompting miners to reserve auditor slots a year in advance, a pattern that underpins robust order visibility for Mining TIC market participants.

By Sourcing Type: Variable Costs Drive Outsourcing

Outsourced providers captured 64.18% of the Mining TIC market share in 2025 and will grow at a 5.57% CAGR through 2031, reflecting junior explorers’ avoidance of fixed laboratory overheads. Even integrated majors are divesting non-core labs and retaining only fast-turnaround grade-control units, while routing specialized assays to external experts. More than 80% of juniors already outsource core analysis, saving 30% to 50% versus running captive laboratories. Bureau Veritas bought GeoAssay in March 2025 to anchor itself in Chile’s lithium belt, demonstrating how consolidation is chasing outsourced flows.[3]Bureau Veritas SA, “GeoAssay Acquisition Completion,” bureauveritas.com

In-house capacity still makes sense in high-volume iron-ore hubs such as Australia’s Pilbara, where on-site labs process up to 1,000 samples a day and return results within four hours, an interval impossible for off-site services given transport delays. However, rare-earth-element or platinum-group-metal assays need million-dollar inductively coupled plasma mass spectrometry units that only centralized facilities can justify, reinforcing the outsourcing trend. SGS opened new laboratories in Namibia and Saudi Arabia in 2025 to pre-empt outsourcing flows from nascent lithium, cobalt, and phosphate pipelines in Africa and the Middle East. With financing conditions tightening, venture investors are mandating variable-cost operating models, locking in further demand for outsourced Mining TIC market services.

By Mode of Service Delivery: On-Site Dominates, Drones Accelerate

On-site services accounted for 52.22% of the Mining TIC market share in 2025 because grade-control and equipment-integrity checks require immediate feedback. Remote and digital services, though smaller, are the fastest-growing segment, with a 5.81% CAGR to 2031, driven by drones, autonomous rovers, and cloud-based scanning platforms. Off-site laboratories hold the residual, servicing exploration programs where sample volume justifies centralized throughput. The Mining TIC market for remote inspection is expanding as safety regulations tighten and operators seek to reduce mobilization costs by up to 50% through robotics.

MsMin’s drone fleet, now under SGS, delivers pit-wall data to cloud dashboards, enabling geotechnical engineers to run stability models from city offices rather than onsite. SafeSight’s DeepTraxx rover streams real-time gas and LiDAR data from underground workings, preventing human exposure to hazardous stopes and meeting strict occupational-health mandates. Digital core scanners such as Orexplore GeoCore X10 and Epiroc CorePhoto couple high-resolution imagery with artificial intelligence, enabling remote logging and compressing decision cycles from weeks to days. Off-site laboratories are investing in premium equipment to maintain relevance; inductively coupled plasma mass spectrometry and laser-ablation units support specialty assays at 40% below the cost of temporary onsite setups, keeping them integral to the Mining TIC market size growth story.

Geography Analysis

Asia-Pacific generated 38.28% of Mining TIC market revenue in 2025, anchored by China’s rare-earth refining audits, Australia’s iron-ore grade-control protocols, and India’s coal export inspections. Eurofins and SGS operate dense laboratory networks in China to meet purity and traceability checks demanded by downstream magnet manufacturers. SGS also commissioned a Pilbara facility in January 2025 to process up to 1,000 iron-ore samples daily, ensuring a four-hour turnaround for major producers.[4]SGS SA, “Pilbara Iron Ore Laboratory Opening,” sgs.com Portable X-ray fluorescence adoption across Australian gold campaigns is reducing reliance on off-site assays, reflecting a shift toward real-time decision-making. India’s move toward third-party verification of iron-ore cargo, evident in Cotecna’s 2025 port contracts, reflects the region’s growing preference for neutral validation.

Africa is the fastest-expanding region, projected to grow at 5.22% CAGR through 2031, driven by lithium finds in Zimbabwe and cobalt capacity in the Democratic Republic of the Congo. Exploration budgets rose 11% in 2025 as strategic investors committed fresh capital despite global price volatility. SGS opened a Namibia laboratory in September 2025 and is adding inductively coupled plasma mass spectrometry to meet demand for rare-earth assays, underscoring its first-mover advantage in nascent jurisdictions. Cobalt sulfate purity testing is intensifying as automakers impose stricter specs, driving premium assay demand in the Copperbelt. Logistics hurdles remain acute; sample flights can cost USD 2,000 per shipment, and currency swings prompt USD-denominated contracts to protect provider margins.

North America and Europe represent mature yet still-growing pockets of the Mining TIC market. The United States faces a 130,000-position gap in geoscience by 2029, motivating labs to accelerate automation investments. SGS partnered with Quebec stakeholders in April 2026 to expand lithium and nickel testing capacity, aligning with Canada’s ambitions for the battery supply chain. Europe’s Corporate Sustainability Reporting Directive, effective January 2026, is pushing demand for Scope 3 emission inventories, while TÜV NORD’s CERA 4in1 rollout offers a harmonized certification path for producers seeking European Union market access. The Middle East is emerging as a niche growth pocket, and SGS’s October 2025 Saudi Arabia opening is designed to capture Vision 2030 mining investments.

Competitive Landscape

The Mining TIC market is moderately concentrated, with SGS, Bureau Veritas, Intertek, and ALS Limited together holding a significant share of global revenue. Strategic logic centers on locking in regional labs near battery-mineral corridors, bolstering remote-inspection capabilities, and adding ESG certification depth. SGS’s February 2026 purchase of MsMin adds drone and ground-rover services that reduce inspection mobilization cost 50% and widen safety margins, differentiating its offer. Bureau Veritas’s March 2025 GeoAssay buyout anchors Chilean lithium brine capacity and complements its newly launched bismuth-based fire-assay method that eliminates lead emissions, a response to stricter European Union and Canadian environmental rules.

ALS Limited is moving beyond routine assays into flotation, leach, and comminution testwork, chasing higher-margin metallurgical mandates for lithium hydroxide, nickel sulfate, and cobalt refining flowsheets.[5]ALS Limited, “Flotation and Leach Testwork Expansion,” alsglobal.com Intertek’s Copiapó laboratory serves cross-border Andean lithium and copper projects, underlining the importance of location near altitude-challenged operations. TÜV NORD’s CERA 4in1 has created fresh competition in sustainability audits, bundling multi-standard compliance into a single visit and undercutting modular frameworks on price and time.

Smaller specialists such as Cotecna and Mistras Group are gaining traction in trade inspection and asset-integrity monitoring, respectively, side-stepping direct showdowns with global majors yet securing strong recurring revenue streams. Early adopters of ISO IWA 45:2024 accreditation are already commanding 10% to 15% fee premiums for upstream traceability audits, reinforcing first-mover advantage in the Mining TIC market.

Mining TIC Industry Leaders

SGS SA

Bureau Veritas SA

Intertek Group plc

ALS Limited

Eurofins Scientific SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Albemarle’s Salar de Atacama operation cleared an Initiative for Responsible Mining Assurance audit, securing ESG credentials for European supply chains.

- April 2026: Surge Battery Metals enlisted ALS Limited for lithium hydroxide leach testing on Nevada brine, underscoring demand for specialized hydromet services.

- March 2026: SGS partnered with Quebec’s mining ecosystem to expand lithium and nickel testing capacity, backing the province’s battery-materials strategy.

- March 2026: Anglo American completed the Initiative for Responsible Mining Assurance surveillance at Sishen and Kolomela iron-ore mines.

- February 2026: ALS Limited rolled out expanded metallurgy services for battery-mineral projects.

Global Mining TIC Market Report Scope

The Mining TIC Market Report is Segmented by Service Type (Testing, Inspection, and Certification), Sourcing Type (In-house, and Outsourced), Mode of Service Delivery (On-site, Off-site/Laboratory, and Remote/Digital), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

| Testing |

| Inspection |

| Certification |

| In-house |

| Outsourced |

| On-site |

| Off-site / Laboratory |

| Remote / Digital |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Testing | |

| Inspection | ||

| Certification | ||

| By Sourcing Type | In-house | |

| Outsourced | ||

| By Mode of Service Delivery | On-site | |

| Off-site / Laboratory | ||

| Remote / Digital | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the Mining TIC market size and its forecast growth?

The Mining TIC market size is projected to rise from USD 4.56 billion in 2025 and USD 4.76 billion in 2026 to USD 5.90 billion by 2031, reflecting a 4.39% CAGR over 2026-2031.

Which service category leads revenue in the Mining TIC market?

Testing services led with 48.31% of Mining TIC market share in 2025, underpinned by the high sample intensity of resource-estimation and feasibility studies.

Why is outsourcing growing faster than in-house testing?

Outsourced solutions already hold 64.18% of Mining TIC market share and are expanding at a 5.57% CAGR because junior explorers and even some majors prefer variable-cost models that avoid heavy laboratory capital outlays.

What technology trends are transforming inspection workflows?

Autonomous drones, ground rovers, cloud-based core scanners, and AI-driven logging platforms are cutting mobilization costs up to 50% and compressing decision cycles from weeks to days, reshaping demand for remote inspection.

Which region is forecast to grow the fastest?

Africa is expected to record the highest regional CAGR at 5.22% through 2031, powered by lithium projects in Zimbabwe and cobalt expansion in the Democratic Republic of the Congo.

How are ESG standards influencing the Mining TIC market?

New European Union and global disclosure rules effective January 2026 are compelling miners to secure third-party certification for environmental and social metrics, making ESG audits one of the fastest-growing revenue streams for TIC providers.

Page last updated on: