Construction And Infrastructure Testing, Inspection, And Certification Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 23.97 Billion |

| Market Size (2030) | USD 30.09 Billion |

| Growth Rate (2025 - 2030) | 4.65% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Construction And Infrastructure Testing, Inspection, And Certification Market Analysis by Mordor Intelligence

The construction and infrastructure testing, inspection, and certification market size is USD 23.97 billion in 2025 and is forecast to grow to USD 30.09 billion by 2030, representing a 4.65% CAGR over the period. Investments earmarked under stimulus packages, the gradual retirement of aging infrastructure, and the continued tightening of building‐code regimes together generate a steady stream of mandatory inspections that anchor demand. The market’s technology profile is also shifting as advanced non-destructive testing (NDT), IoT sensor arrays, and cloud-based analytics migrate from pilot deployments into commercial scale. Service providers that combine compliance expertise with data-driven insights are gaining pricing power, while traditional visual inspections are gradually being commoditized. On the demand side, green-building certification, climate resilience mandates, and predictive maintenance programs are all increasing the depth and frequency of inspection touchpoints across asset life cycles.

Key Report Takeaways

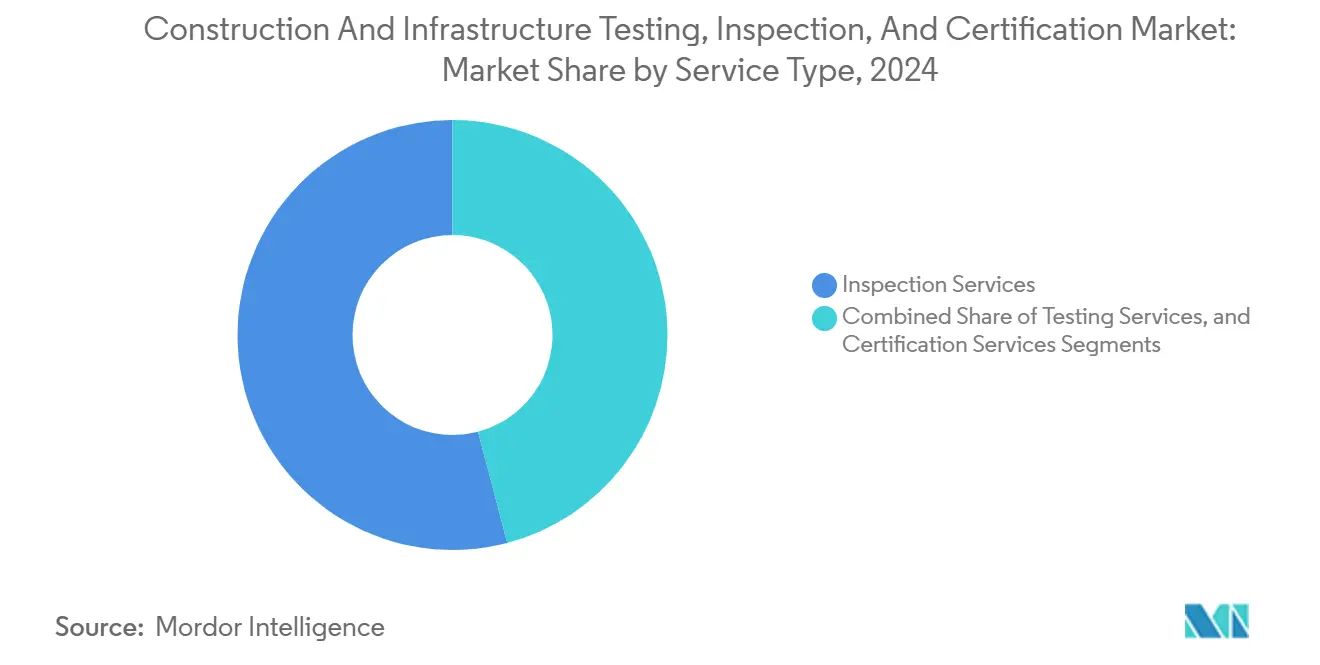

- By service type, inspection services led with 54.1% of the construction and infrastructure testing, inspection, and certification market share in 2024, whereas certification services exhibited the fastest growth of 4.9% CAGR through 2030.

- By sourcing type, the outsourced delivery model accounted for 69.5% of the global construction and infrastructure testing, inspection, and certification market size in 2024 and is projected to expand at a 4.8% CAGR.

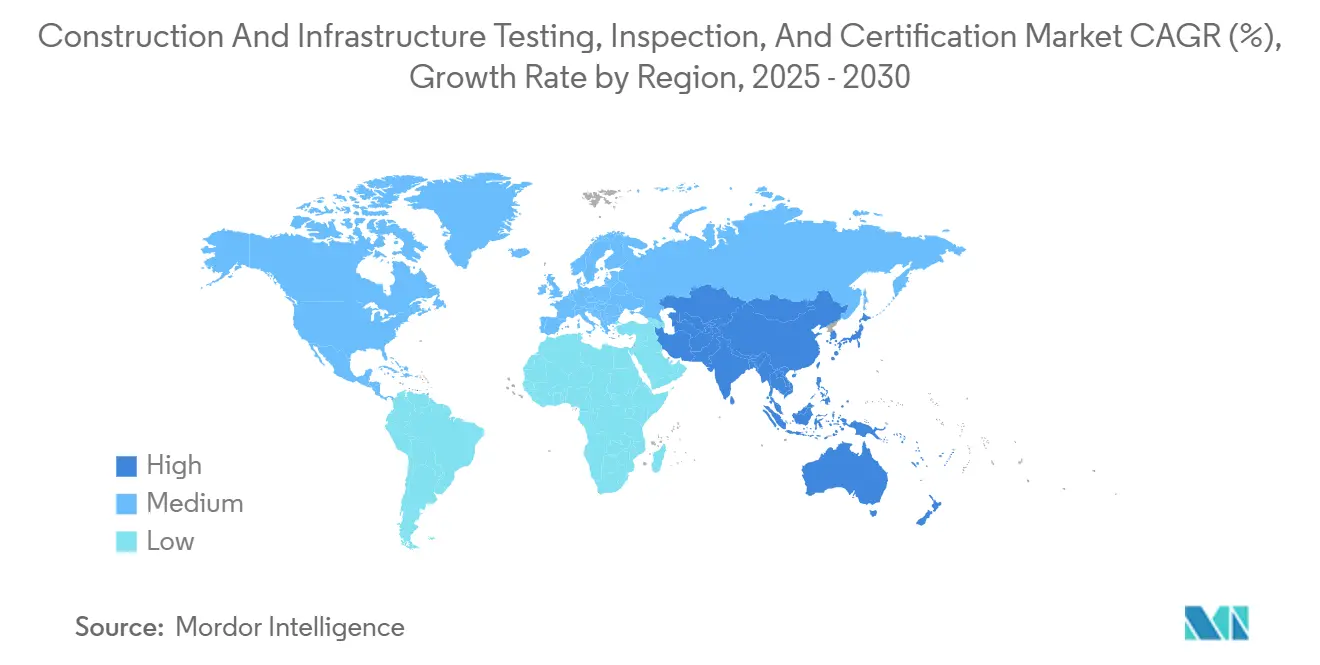

- By geography, the Asia-Pacific region captured a 44.7% revenue share in 2024 and is projected to grow at a 5.1% CAGR through 2030.

Global Construction And Infrastructure Testing, Inspection, And Certification Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent building-code enforcement | +1.2% | Global (North America, EU lead) | Medium term (2-4 years) |

| Aging infrastructure renewal cycles | +1.0% | North America, Europe, and spillover to the Asia-Pacific | Long term (≥4 years) |

| Sustainable green-building certification | +0.8% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Government stimulus for emerging infrastructure | +0.7% | Asia-Pacific core, Latin America, and MEA secondary | Medium term (2-4 years) |

| AI-driven predictive failure analytics | +0.5% | North America, EU early adoption | Long term (≥4 years) |

| Climate-resilient design standards | +0.4% | Global coastal and climate-vulnerable regions | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Stringent Building-Code Enforcement

Regulators are embedding wider safety, energy, and accessibility provisions into state and national codes, expanding inspection checkpoints from plan approval to post-occupancy operation. Michigan’s adoption of the 2021 International Building Code, Virginia’s 2024 energy-efficiency mandates, and Tennessee’s updated plumbing standards collectively illustrate how diverse jurisdictions are expanding the scope of mandatory inspections.[1]Michigan Department of Licensing and Regulatory Affairs, “Building Codes,” michigan.gov More rigorous seismic, wind-load, and flood-protection clauses contained in ASCE 7-22 likewise spur specialized structural testing demand. These changes lift baseline revenue visibility for providers and accelerate outsourcing as project owners seek proof of independent compliance.

Aging Infrastructure Renewal Cycles

Roughly 50,000 U.S. bridges require repair or replacement, representing a USD 125 billion backlog, while post-war commercial buildings across Western Europe have reached end-of-life thresholds. Each rehabilitation contract triggers a cascade of materials analysis, load-bearing verification, and safety recertification tasks that extend well beyond new-build phase inspections. Because retrofits often unfold within live operational environments, owners increasingly schedule predictive inspections to minimize downtime, reinforcing a durable, counter-cyclical demand pattern.

Sustainable Green-Building Certification Demand

Global green-building registrations increased by 43% in 2024, as investors linked utility savings and ESG ratings to asset valuations.[2]BREEAM USA, “Annual Report 2024,” breeam.com Programs such as LEED and BREEAM are transitioning from one-off audits to longitudinal performance verification, which requires ongoing sensor-based data collection. Continuous commissioning, indoor-air-quality sampling, and carbon-footprint tracking increase the volume of laboratory tests and onsite inspections per facility, thereby strengthening recurring revenue models for specialized providers that can integrate environmental science, IoT telemetry, and data analytics.

AI-Driven Predictive Failure Analytics Adoption

Machine-learning classifiers built into phased-array ultrasonic, digital radiography, and thermal imaging systems are flagging micro-cracks and corrosion zones long before human inspectors can detect them. Robotics paired with AI enables inspectors to cover larger surface areas safely, while cloud analytics convert raw inspection data into repeatable risk scores. Early adopters differentiate on turnaround time and diagnostic depth, command premium rates, and free up scarce NDT technicians to focus on complex failure modes. Over time, algorithmic triage is poised to compress low-skill visual inspection fees while raising the competency bar across the sector.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced NDT and skilled labor | –0.8% | Global, most acute in developed markets | Short term (≤2 years) |

| Project delays reducing inspection scope | –0.5% | Global construction hotspots | Short term (≤2 years) |

| Fragmented accreditation requirements | –0.3% | Multi-jurisdictional operations | Medium term (2-4 years) |

| Cybersecurity risks in remote inspections | –0.2% | Digitally advanced markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced NDT and Skilled Labor

A single phased-array ultrasonic unit can cost USD 200,000–500,000, while technician certification through bodies such as the American Society for Non-destructive Testing demands multi-year apprenticeships and recurrent testing. Smaller firms struggle to amortize such capital and talent expenditures, which curbs market entry and drives selective consolidation. Until equipment prices decline or training pipelines expand, service availability in secondary cities will remain constrained.

Fragmented Accreditation Requirements

While ISO/IEC 17020 sets a baseline, many jurisdictions overlay local accreditation layers, forcing global providers to relicense capabilities country by country. [3]Inter-American Accreditation Cooperation, “Specifying Accreditation in Regulation – Fact Sheet,” iaac.org.mx Duplicate audits increase compliance costs and prolong the time-to-market for cross-border contracts. The absence of harmonized reciprocity, especially in large infrastructure projects financed by multinational consortia, nudges owners toward regional specialists who are steeped in domestic rules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Inspection Services Retain Foundational Share

Inspection services generated 54.1% of 2024 revenue, anchoring the construction and infrastructure testing, inspection, and certification market through mandatory site visits, structural walk-downs, and code conformance checks that regulators and insurers require before occupancy. Testing services follow, providing laboratory analysis of concrete cores, steel welds, soil compaction, and environmental contaminants that substantiate engineering assumptions. Certification services, while accounting for a smaller slice of the 2024 construction and infrastructure testing, inspection, and certification market size, are forecast to expand at a 4.9% CAGR as green-building and net-zero targets proliferate.

Digital workflows are amplifying certification uptake. Platforms that ingest continuous energy, water, and carbon data meet emerging Zero-Carbon and NABERS standards, turning traditional one-off audits into recurring subscriptions. Providers able to overlay analytics atop field data convert static records into performance dashboards requested by landlords and investors. As a result, certification revenue is expected to narrow the gap with inspection revenue over the forecast horizon, even though inspections will likely remain the volume core of the building inspection and testing services market.

By Sourcing Type: Outsourcing Extends Lead

The outsourced model accounted for 69.5% of 2024 revenue, reflecting owners’ preference for independent third-party assurance and the escalating complexity of inspection technology. High capital hurdles for advanced NDT gear and rising liability exposure push even large contractors to rely on specialized firms for critical path verifications. Insurance carriers increasingly stipulate independent sign-offs, further entrenching outsourcing.

Hybrid arrangements are emerging, wherein facility managers conduct low-skill visual checks in-house but contract out specialized scans, drone flyovers, or certification audits. Although this hybrid approach tempers growth in pure-play outsourcing volume, the outsourced share remains structurally advantaged as deep technical expertise and 24/7 data infrastructure are costly to sustain internally. Consequently, outsourced revenue is projected to outgrow in-house equivalents by a modest margin yet still capture the bulk of incremental spending through 2030.

Geography Analysis

Asia-Pacific dominates the construction and infrastructure testing, inspection, and certification market with a 44.7% share and continues to outpace all other regions at a 5.1% CAGR through 2030. China’s inspection reforms, introduced in 2024, mandate third-party verification across structural, materials, and environmental scopes, pulling advanced NDT providers into provincial tender lists. India’s infrastructure pipeline adds predictable inspection milestones tied to state-funded expressways, metros, and renewable plants, while Southeast Asian governments embed safety audits into FDI approvals for logistics and manufacturing complexes.

North America sustains a mature but robust demand profile. The USD 1.2 trillion Infrastructure Investment and Jobs Act allocates funds to highway and bridge modernization, water utilities, and broadband, each of which requires milestone inspections before drawdowns. States, including Michigan and Virginia, have updated building codes, expanding the scope of inspections to include energy benchmarks and accessibility checks. The regional market also leads in AI-enabled predictive analytics, driving the early adoption of drone surveys, 3D twin models, and cloud dashboards, which increase spend per inspection.

Europe’s market is anchored by the EU Green Deal, which ties renovation subsidies to documented energy savings, thereby multiplying onsite blower-door tests, thermal imaging scans, and operational carbon assessments.[4]Intertek, “H1 2024 Results Presentation,” intertek.com Member states differ in accreditation timelines, prompting multinational service providers to maintain decentralized compliance teams. Emerging European economies boost growth via EU cohesion funds that require strict quality-assurance protocols, while high-income countries focus on deep retrofit programs for municipal buildings and housing stock.

Competitive Landscape

The competitive field is moderately fragmented. SGS, Bureau Veritas, and Intertek together command a minimal share of global revenue, leaving ample headroom for regional specialists. SGS operates over 2,500 laboratories across 115 countries and continues its acquisition-led expansion, including the 2025 purchases of RTI Laboratories and Aster Global Environmental Solutions, which bolster its greenhouse gas verification capabilities. Bureau Veritas maintains strength in marine and offshore certification, while Intertek leverages its RiskAware platform to deliver predictive maintenance solutions to industrial clients.

Technology investment is a principal differentiator. Robotics, IoT sensors, and AI analytics are migrating from capex exploration to mainstream budget lines. Intertek’s digital inspection management suite enables asset owners to compare inspection frequency, severity of findings, and budget across facilities in real-time, delivering cost avoidance insights that underpin premium contract renewals. Smaller firms defend share through hyper-local code expertise, quick mobilization, and targeted vertical specialization, such as façade safety in high-rise urban cores.

Consolidation pressures are mounting. The terminated merger talks between SGS and Bureau Veritas in February 2025 underscored both the strategic logic and regulatory hurdles of large-scale combinations. Private-equity interest remains keen, evidenced by KKR’s 2024 acquisition of Marmic Fire and Safety, suggesting that recurring inspection cash flows and low capital intensity align well with leveraged buyout strategies. Overall, the market is likely to evolve toward a barbell structure featuring a handful of globally diversified platforms and a long tail of niche, tech-enabled regional specialists.

Construction And Infrastructure Testing, Inspection, And Certification Industry Leaders

Intertek Group PLC

Bureau Veritas SA

SGS SA

TÜV SÜD AG

TÜV Rheinland AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: SGS announces plans to accelerate acquisition activity during 2025 following the end of merger discussions with Bureau Veritas.

- January 2025: SGS acquires RTI Laboratories (78% stake) and Aster Global Environmental Solutions (41% stake), strengthening North American sustainability services.

- December 2024: SGS completes acquisition of CertX AG (74% stake), expanding European certification platforms.

- July 2024: UL Solutions acquires TestNet Group for testing and certification expansion.

Global Construction And Infrastructure Testing, Inspection, And Certification Market Report Scope

The scope of the study on construction TIC covers the services rendered for building and infrastructure-related activities across the entire project lifecycle. Global Construction TIC Market is segmented by Service (Testing and Inspection Service, Certification Service), by Sourcing Type (Outsourced, In-house), and by Geography.

| Testing Services |

| Inspection Services |

| Certification Services |

| In-house |

| Outsourced |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | Testing Services | ||

| Inspection Services | |||

| Certification Services | |||

| By Sourcing Type | In-house | ||

| Outsourced | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the construction and infrastructure Testing, Inspection, and Certification market?

The market is valued at USD 23.97 billion in 2025 and is projected to reach USD 30.09 billion by 2030.

Which region is growing the fastest?

Asia-Pacific leads with a 5.1% CAGR thanks to large infrastructure pipelines in China and India.

Which service type is expanding most quickly?

Certification services, propelled by green-building mandates, are posting a 4.9% CAGR through 2030.

Why is outsourcing preferred for inspections?

High equipment costs, rising liability exposure, and the need for specialized expertise push owners toward third-party providers.

What key technology trends are reshaping inspections?

AI-powered predictive analytics, robotics, and IoT sensor integration are boosting diagnostic precision and recurring revenue models.

Page last updated on: