Testing, Inspection, and Certification for the Metals and Minerals Industry Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

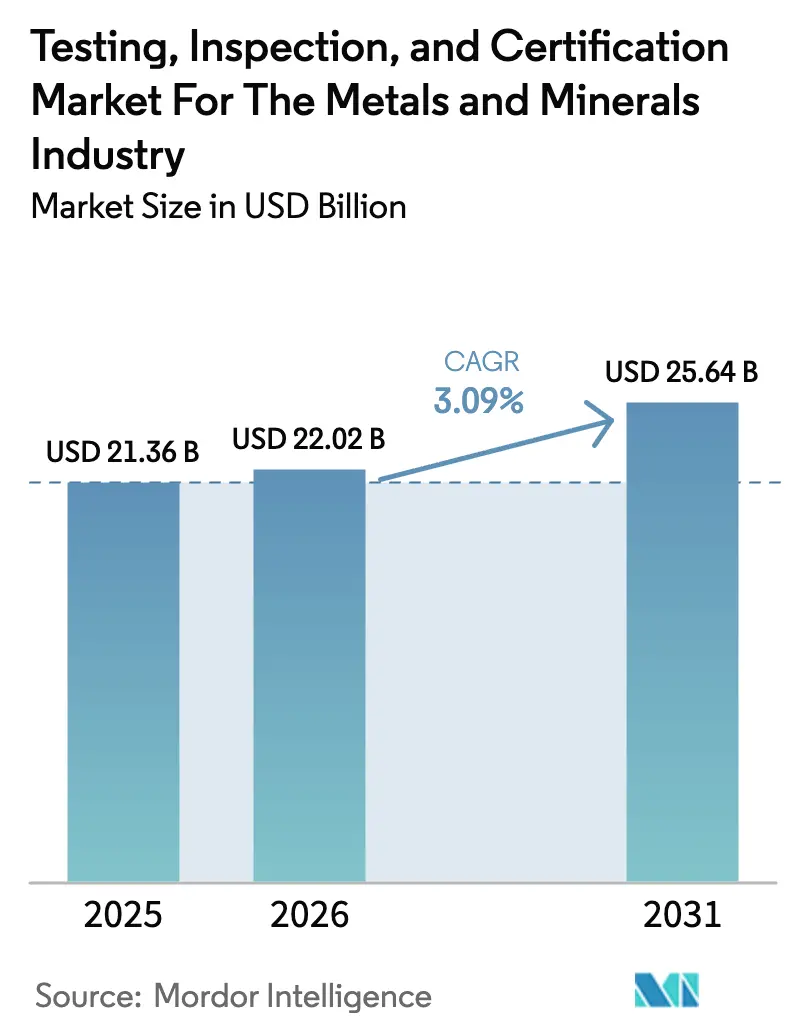

| Market Size (2026) | USD 22.02 Billion |

| Market Size (2031) | USD 25.64 Billion |

| Growth Rate (2026 - 2031) | 3.09% CAGR |

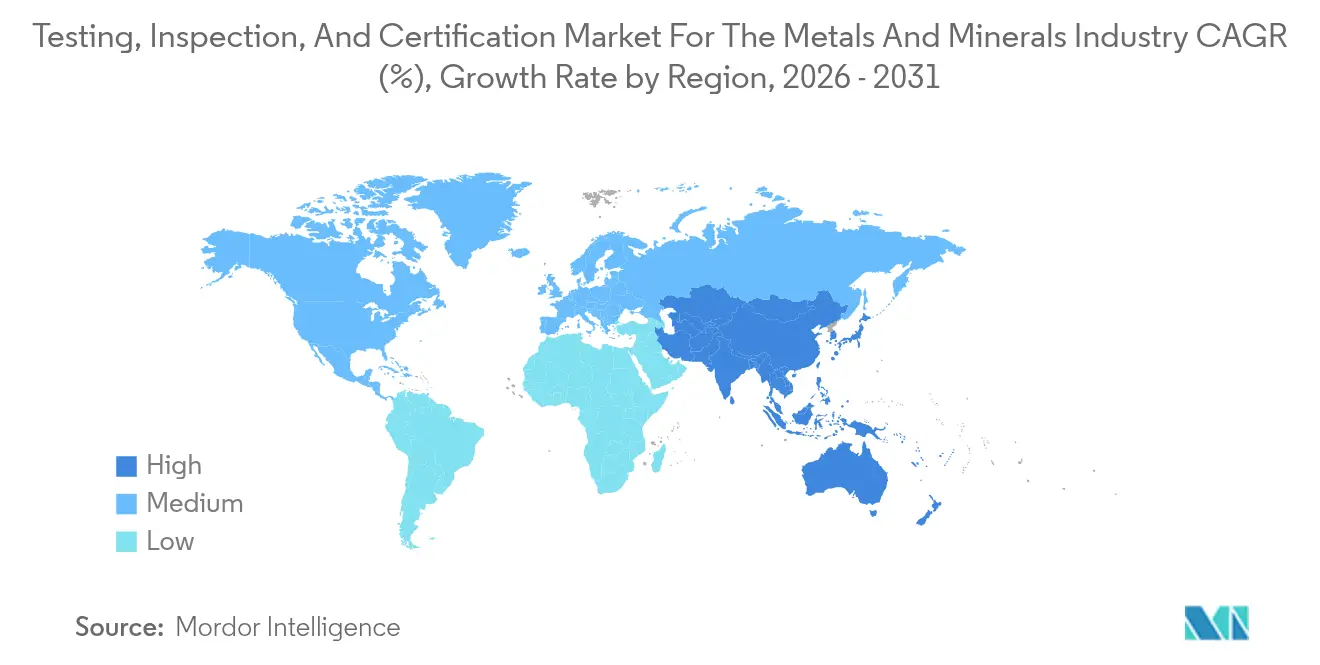

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

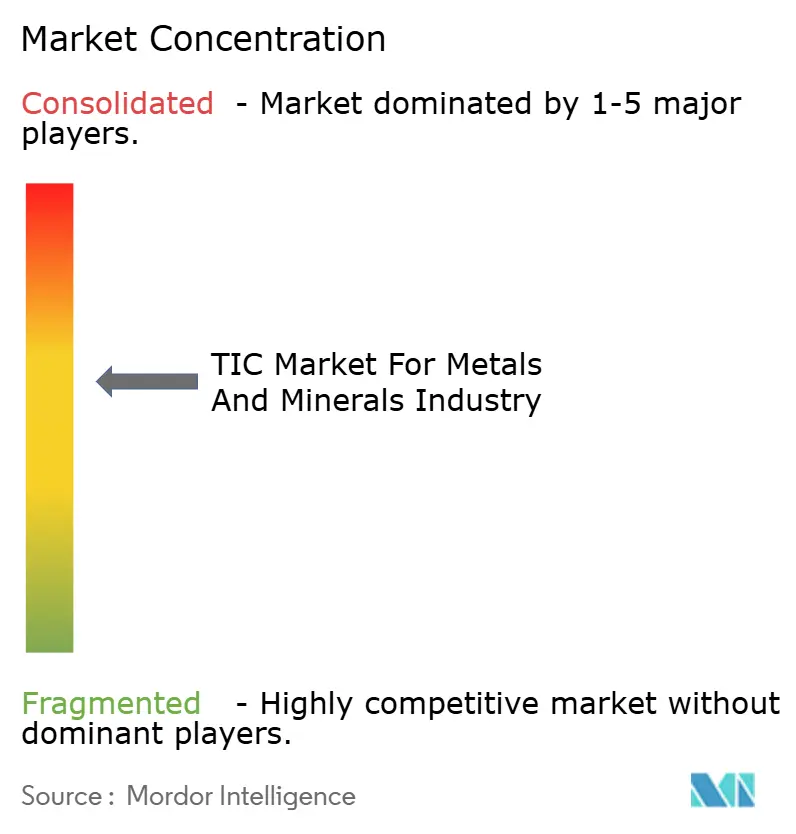

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Testing, Inspection, and Certification for the Metals and Minerals Industry Analysis by Mordor Intelligence

The Testing, Inspection, and Certification market size for the metals and minerals industry is expected to grow from USD 21.36 billion in 2025 to USD 22.02 billion in 2026 and is forecast to reach USD 25.64 billion by 2031 at 3.09% CAGR over 2026-2031. Compliance-driven demand for grade control, environmental assurance, and traceability solutions keeps the industry structurally resilient even as cyclical metal prices fluctuate. Buyers are increasingly specifying third-party verification for Scope 3 emissions, biodiversity impacts, and critical-mineral provenance, which sustains high testing volumes despite gains in automation. Consolidation among global TIC providers enhances service consistency and digital connectivity, providing miners with access to harmonized protocols across jurisdictions. At the same time, automated laboratories, portable XRF analyzers, and blockchain-enabled audits are redefining workflows, prompting providers to embed robotics, AI-driven sample scheduling, and API-based data exchange into their offerings.[1]SGS, “Geochemistry,” SGS.com

Key Report Takeaways

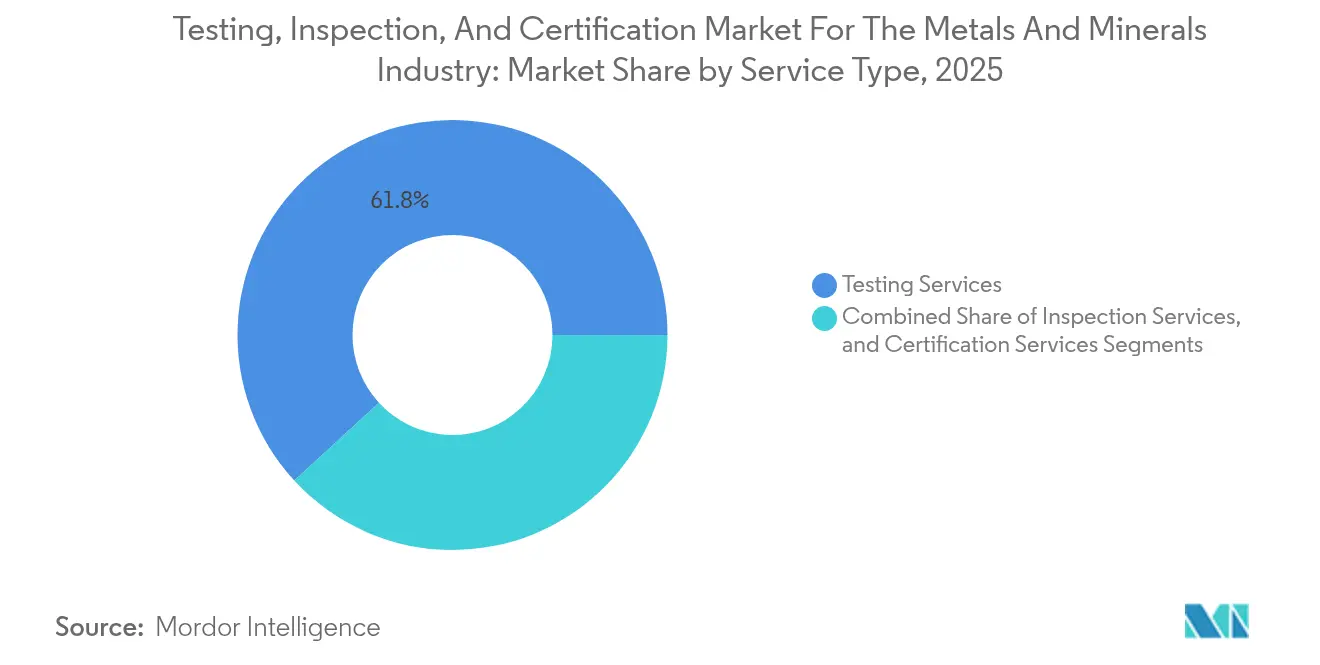

- By service type, Testing Services captured 61.84% of the Testing, Inspection, and Certification for the Metals and Minerals Industry market share in 2025, while Certification Services is set to grow the fastest at a 3.72% CAGR through 2031.

- By sourcing type, the outsourced model commanded a 73.48% share of the Testing, Inspection, and Certification for the Metals and Minerals Industry in 2025 and is projected to expand at a 3.42% CAGR.

- By geography, the Asia-Pacific region led the Testing, Inspection, and Certification for the Metals and Minerals Industry with a 38.42% revenue share in 2025, growing at a 3.76% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Testing, Inspection, and Certification for the Metals and Minerals Industry Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consolidation of global mining supply chains | +0.8% | Global, with a concentration in Asia-Pacific and South America | Medium term (2-4 years) |

| Stricter sustainability and trace-metal disclosure norms | +1.2% | Global, led by EU CSRD requirements and North American ESG mandates | Long term (≥ 4 years) |

| Rising downstream demand for battery-grade metals | +0.9% | Asia-Pacific core, spill-over to South America and Africa | Medium term (2-4 years) |

| Digitalisation of on-site laboratories | +0.6% | North America and the EU, expanding to the Asia-Pacific | Short term (≤ 2 years) |

| Blockchain-enabled provenance audits | +0.4% | Global, early adoption in premium metal supply chains | Long term (≥ 4 years) |

| Geopolitical resource nationalism | +0.5% | Critical mineral-producing regions, particularly Africa and South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter Sustainability and Trace-Metal Disclosure Norms

The EU Corporate Sustainability Reporting Directive now subjects more than 50,000 firms to mandatory third-party assurance, compelling miners to commission external experts for Scope 3 emissions, water stewardship, and biodiversity studies. Major providers, notably SGS, broadened CSRD-aligned services in 2024 to tap an estimated USD 2.3 billion addressable pool for sustainability verification. Institutional investors reference these audits when ranking producers, so mining multinationals replicate the strictest EU formats across global assets. This harmonization makes sustainability testing non-negotiable in contract bidding, effectively locking TIC demand into long-term budgets. It also accelerates the uptake of digital chain-of-custody tools that shorten audit cycles while providing immutable data sets for regulators and financiers. As regional ESG statutes converge, the Testing, Inspection, and Certification for the Metals and Minerals Industry registers stable fee escalations for specialized environmental assays.

Rising Downstream Demand for Battery-Grade Metals

Electric-vehicle OEMs and battery makers tighten impurity thresholds for lithium, nickel, and rare earths, forcing upstream suppliers to prove 99.5% plus purity and sub-ppm contaminant levels. Tesla’s 2024 procurement code mandates independent verification of every critical-mineral batch, while CATL requires full trace-element profiles to ensure cathode longevity. These stricter specifications spawn advanced ICP-OES, mass-spectrometry, and laser-ablation programs within TIC labs, alongside tailored reference materials for solid-state and sodium-ion chemistries. Providers monetise premium turnaround guarantees, enabling miners to secure higher-margin offtake agreements. In parallel, battery recyclers employ identical protocols for black-mass input streams, further broadening the Testing, Inspection, and Certification for the Metals and Minerals Industry.

Consolidation of Global Mining Supply Chains

Major miners reduce approved vendor lists, channeling spend toward companies offering integrated testing, inspection, and certification across continents. Rio Tinto cut its TIC supplier base by 35% in 2024, rewarding firms with multi-regional labs and API-enabled data portals. This rationalisation drives M&A among TIC leaders; SGS executed 11 deals in 2024 and 3 more in early 2025 to enhance cross-border capacity. The resulting scale advantages include unified LIMS platforms, standardised QA/QC protocols, and shared talent pools, all of which translate into cost efficiencies for miners and sticky multi-year contracts for service providers. The trend directly lifts revenue density per client within the Testing, Inspection, and Certification for the Metals and Minerals Industry.

Digitalization of On-Site Laboratories

Automated sample preparation, robotic XRF cells, and cloud-based result dashboards compress assay cycles from days to minutes. Cotecna del Perú deployed EDOX remote validation and COTECNA EYE inspection tracking at its Lima hub in 2024, letting customers download chain-of-custody certificates in real time.[2]Cotecna, “Cotecna del Perú promotes innovation, accuracy and reliability in key analytical processes for modern mining,” cotecna.com Faster insights help operators calibrate mill feed, cut reagent use, and minimise metal losses, translating into direct cash-cost gains that far exceed incremental assay fees. Providers diversify revenue by licensing data analytics and predictive-maintenance modules embedded in their LIMS suites. These capabilities deepen client lock-in and raise the digital skill bar for new entrants, shoring up the Testing, Inspection and Certification Market For Metals And Minerals Industry industry against commoditisation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in commodity prices | -0.7% | Global, with an acute impact on resource-dependent economies | Short term (≤ 2 years) |

| Shortage of certified laboratory professionals | -0.9% | Global, most severe in North America and Australia | Medium term (2-4 years) |

| Consolidation of mining majors reduces vendor count | -0.3% | Global, concentrated in mature mining jurisdictions | Long term (≥ 4 years) |

| Emerging in-pit real-time sensors bypassing traditional labs | -0.5% | North America and Australia, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Commodity Prices

Sharp price swings alter exploration budgets, deferring drilling campaigns and cut-backs in non-essential assays. Copper slid 23% between Q1 and Q4 2024, prompting Freeport-McMoRan to scale back sampling in marginal pits. Similar retrenchment cascades through contractor labs, eroding utilisation rates and pressuring margins. Providers hedge by structuring output-based contracts and offering modular service tiers that miners can ramp up in bullish cycles. Although volatility curtails near-term volumes, compliance-critical testing remains obligatory, cushioning downside exposure for the Testing, Inspection, and Certification Market for Metals and Minerals Industry.

Shortage of Certified Laboratory Professionals

The U.S. will need 221,000 replacement mining workers by 2029, yet it produced only 327 mining-engineering graduates in 2020.[3]Jurgen Brune, “A Novel Job Similarity Index for Career Transition in the Mining Industry,” springer.com Comparable deficits exist in Australia. Scarcity inflates salary expectations and magnifies recruitment lead-times for chemists holding ISO/IEC 17025 signatory status. TIC firms respond by automating wet-chemistry lines, partnering with universities on vocational pipelines, and relocating routine tasks to lower-cost hubs. While automation offsets some gap, high-complexity metallurgical analysis still demands human oversight, capping throughput growth and raising operating costs within the Testing, Inspection, and Certification for the Metals and Minerals Industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Testing Retains Scale while Certification Accelerates

Testing Services accounted for 61.84% of 2025 revenue, anchoring the Testing, Inspection, and Certification Market for Metals and Minerals Industry market size through indispensable grade-control and environmental monitoring obligations. High-volume assays for iron ore, copper, and gold continue despite automation because regulators require externally validated data for export permits and royalty calculations. Certification Services, although smaller, is expanding at a 3.72% CAGR as downstream buyers insist on ESG credentials and blockchain-verified provenance. Providers package carbon-neutral mine labels, responsible-sourcing audits, and ISO 14067 footprints, raising ticket sizes per engagement. Inspection Services occupies a steady middle ground, supported by mandatory conveyor, tailings dam, and rail-wagon integrity checks. Robotics-enabled visual tools and drone-based photogrammetry enrich inspection value propositions and mitigate workforce hazard exposure.

Testing’s dominance endures in bulk-commodity jurisdictions where assay density defines ore-body economics. Yet certification will shape margin dynamics because its deliverables command premium pricing and entail higher IP content. Over the forecast period, integrated solutions blending chemical assays with carbon-accounting verification will blur boundaries, allowing providers to upsell certification modules to existing testing clients. For miners, a single supplier simplifies compliance, bolstering stickiness across the Testing, Inspection, and Certification for the Metals and Minerals Industry.

By Sourcing Type: Outsourced Share Widens on Capability Gaps

Outsourced laboratories captured 73.48% of 2025 spend, reflecting miners’ preference for variable-cost structures and external expertise. Skills shortages make internal labs costly; capex for ICP-MS lines, fire-assay furnaces, and ISO accreditation often exceeds the benefit of immediate on-site turnaround. Key players have responded with mobile container labs and pick-up courier models that narrow timing differences, eroding the historical advantage of in-house facilities. Advances in portable XRF and LIBS devices further allow miners to perform daily control checks in-pit, reserving high-precision assays for off-site specialists. As a result, outsourced providers deepen penetration, and their 3.42% CAGR eclipses that of internal labs.

In-house labs persist in remote, high-grade operations where minute-by-minute feedback drives recovery optimization. Even there, hybrid approaches emerge: automated samplers shuttle pulps to nearby satellite labs operated by third-party staff but housed within mine fences. This model broadens outsourced billings while preserving decision speed. Overall, flexibility, accreditation breadth, and technology investments sustain the outsourced segment’s leadership in the Testing, Inspection, and Certification for the Metals and Minerals Industry.

Geography Analysis

Asia-Pacific held 38.42% of global revenue in 2025 and is growing at a 3.76% CAGR, the quickest among all regions. China’s rare-earth processing complex alone generates over USD 3.2 billion in annual TIC demand, driven by stringent wastewater and radionuclide regulations. Indonesia’s surge in nickel HPAL projects and Australia’s mature iron-ore mines add continuous assay volumes, making the region the core engine for the Testing, Inspection, and Certification Market for Metals and Minerals Industry. Multinationals such as SGS buttress their footprint through acquisitions like RTI Laboratories, ensuring ready access to battery-metal expertise for regional clients.

North America maintains a strong demand anchored in rigorous EPA and MSHA frameworks. Canadian miners leverage high-tech flotation and hydrometallurgical flowsheets that necessitate intricate mineralogical testing. Labor shortages, however, tip the balance toward external labs, especially for high-throughput automation investments that single mines cannot justify. This outsourcing trend ensures stable revenue even as commodity cycles sway exploration volumes. Meanwhile, digital twins, AI-assisted process control, and real-time sensor fusion proliferate across U.S. sites, opening consultancy and calibration add-ons for TIC providers.

Europe gains momentum from the CSRD’s far-reaching disclosure requirements. Even non-EU producers exporting into the bloc adopt EU reporting templates, creating spill-over demand into Africa and South America. The Middle East and Africa contribute rising volumes via greenfield copper, lithium, and phosphate ventures, spurred by energy-transition supply deficits. TIC companies harness local partnerships to align with governmental content mandates while importing global QA protocols. Together, these dynamics confirm geography-based opportunities for cross-selling and reinforce the diversified revenue profile of the Testing, Inspection, and Certification for the Metals and Minerals Industry.

Competitive Landscape

Industry concentration is moderate. SGS, Bureau Veritas, Intertek, and ALS combine deep commodity expertise, extensive lab networks, and unmatched accreditation portfolios, resulting in high switching costs for miners. SGS posted CHF 6.794 billion (USD 7.48 billion) sales in 2024, recording 7.5% organic growth on the back of 11 acquisitions plus three more deals in early 2025.[4]SGS, “Full-Year 2024 Results,” webdisclosure.com Bureau Veritas scaled Latin-American coverage by buying GeoAssay in March 2025, adding three robotic copper-analysis labs and 264 staff skilled in automation.

Technology has become the principal differentiator. Leading companies invest in robotics, AI-driven image analytics, and blockchain integrations, enabling sub-24-hour assay cycles and tamper-proof provenance ledgers. Intertek’s Pilbara hub runs fully automated sample prép lines that operate 24-7, while ALS deploys photon-assay units to eliminate fire-assay consumables. Smaller tech start-ups offer hand-held XRF libraries and edge-processed hyperspectral imaging, nibbling at routine business, but their lack of global accreditation constrains acceptance for high-stakes trade transactions.

Competitive strategy focuses on total-solution bundles. Providers couple lab testing with inspection, certification, and data-hosting SLAs, creating annuity-like revenue. Miners sign multiyear deals to lock in price grids and secure capacity during commodity upswings. As integration deepens, the Testing, Inspection, and Certification for the Metals and Minerals Industry gravitates toward fewer well-capitalised players that can finance continuous R&D and maintain compliance across over 100 national standards.

Testing, Inspection, and Certification for the Metals and Minerals Market Leaders

SGS SA

Bureau Veritas SA

Intertek Group PLC

TÜV SÜD AG

TÜV Rheinland AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Image Resources NL shipped its first heavy-mineral concentrate from the Atlas project, realizing USD 4.2 million in Quarterly-Activities-Report.html.

- April 2025: QES Technology Philippines introduced SPECTROGREEN ICP-OES, expanding local lab capability for soil and mineral assays.

- March 2025: Multiple miners reported metallurgical testwork milestones at SGS Lakefield and Base Metallurgical Laboratories.

- March 2025: Bureau Veritas acquired GeoAssay, adding three fully automated laboratories and 264 robotics-trained staff to reinforce its Chilean copper presence.

Global Testing, Inspection, and Certification for the Metals and Minerals Industry Report Scope

The report on the Testing, Inspection, and Certification for the Metals and Minerals Industry segments the market by Service Type, including Testing, Inspection, and Certification Services. It also categorizes by Sourcing Type, distinguishing between In-House and Outsourced services. Geographically, the report spans North America (covering the United States, Canada, and Mexico), South America (including Brazil, Argentina, and others), Europe (with a focus on Germany, the United Kingdom, France, Italy, Spain, and the rest of Europe), Asia-Pacific (highlighting China, Japan, India, South Korea, Southeast Asia, and beyond), and the Middle East and Africa (notably Saudi Arabia, the United Arab Emirates, Turkey, and other regions). The market forecasts are expressed in USD value terms.

| Testing Services |

| Inspection Services |

| Certification Services |

| In-house |

| Outsourced |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | Testing Services | ||

| Inspection Services | |||

| Certification Services | |||

| By Sourcing Type | In-house | ||

| Outsourced | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the Testing, Inspection, and Certification for the Metals and Minerals Industry?

The sector is valued at USD 22.02 billion in 2026, with a forecast to reach USD 25.64 billion by 2031.

Which service type generates the highest revenue?

Testing Services lead, accounting for 61.84% of 2025 spend, owing to grade-control and environmental-compliance requirements.

How fast is Certification Services expanding?

Certification Services is projected to post a 3.72% CAGR between 2026 and 2031, outpacing other service lines.

Why is Asia-Pacific the largest regional market?

China’s rare-earth processing dominance, Indonesia’s nickel projects, and Australia’s iron-ore output underpin 38.42% regional share and a 3.76% CAGR.

What is driving TIC outsourcing among miners?

Skills shortages and high capex for accredited labs push miners to external partners, giving outsourced models a 73.48% share and 3.42% CAGR growth.

How are TIC firms addressing sustainability regulations?

They bundle CSRD-aligned audits, blockchain traceability, and carbon-footprint verification to meet expanding ESG disclosure mandates.

Page last updated on: