Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

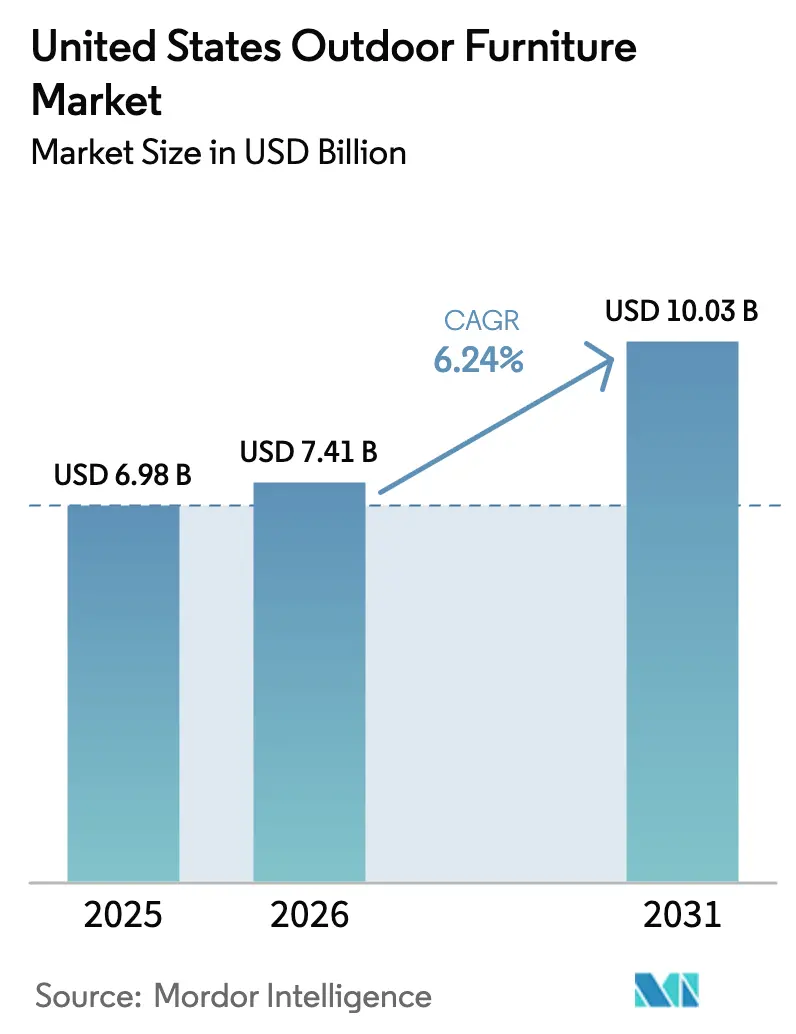

| Base Year Market Size (2025) | USD 6.98 Billion |

| Market Size (2026) | USD 7.41 Billion |

| Market Size (2031) | USD 10.03 Billion |

| Growth Rate (2026 - 2031) | 6.24% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Outdoor Furniture Market Analysis by Mordor Intelligence

The United States outdoor furniture market size is expected to grow from USD 6.98 billion in 2025 to USD 7.41 billion in 2026 and is forecast to reach USD 10.03 billion by 2031 at 6.24% CAGR over 2026–2031. Consumer spending momentum is supported by sustained household focus on patio, porch, and backyard upgrades that convert underused areas into functional living zones. Commercial demand remains anchored by hospitality and foodservice operators that have embedded permanent outdoor seating into their layouts. Input costs and labor constraints shape pricing and delivery strategies as manufacturers balance procurement hedging with streamlined production. Digital discovery remains influential for product research and configuration, while distributors secure large project wins by solving code compliance and durability requirements for high-traffic settings.

Key Report Takeaways

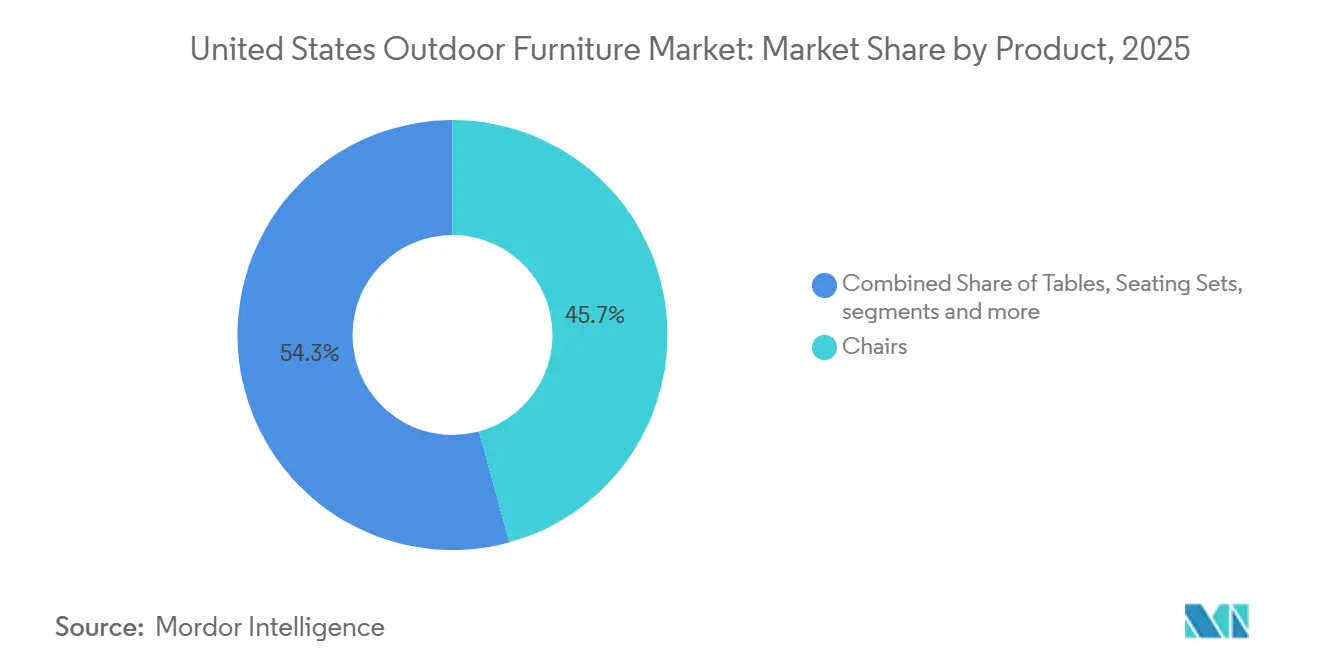

- By product, chairs captured 45.74% of the United States outdoor furniture market share in 2025, while the United States outdoor furniture market size for loungers and daybeds is projected to expand at a 9.78% CAGR through 2031.

- By material, wood led with a 51.36% share in 2025, and metal recorded the fastest 8.76% CAGR through 2031, underscoring durability-led choices in the United States outdoor furniture market.

- By end user, the commercial segment held 62.37% share in 2025, while the United States outdoor furniture market size for residential applications is projected to grow at a 9.87% CAGR through 2031.

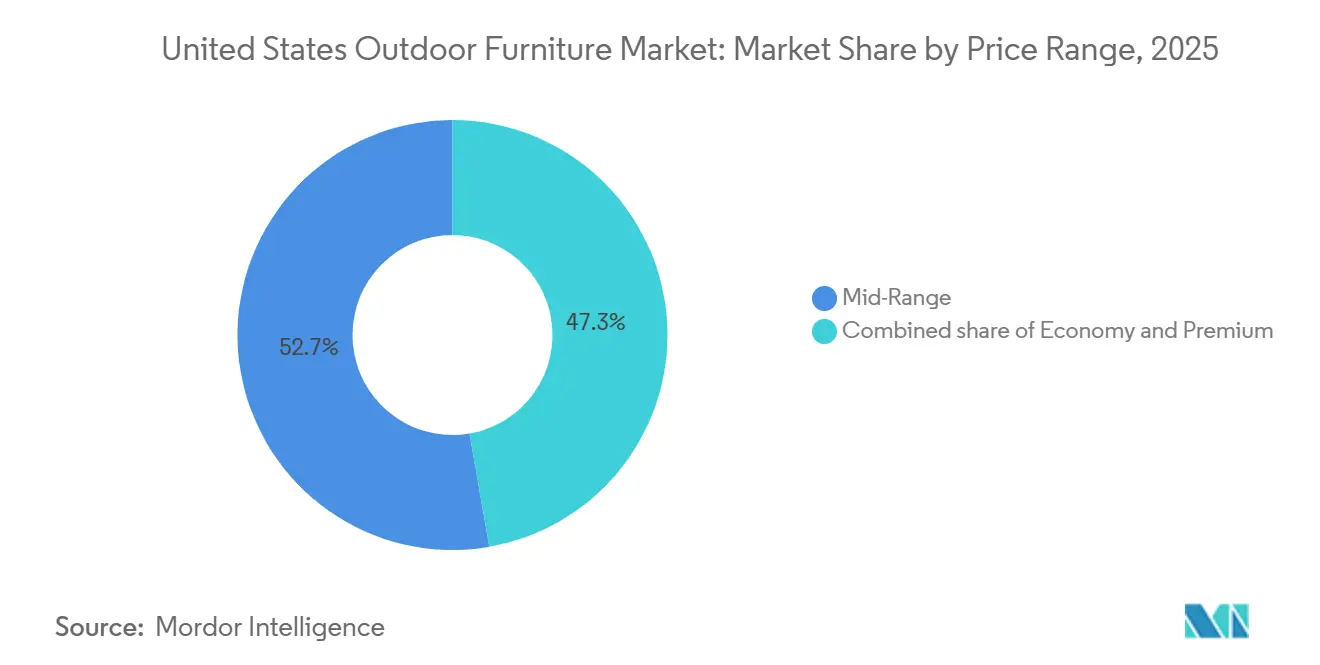

- By price range, mid-range options accounted for a 52.73% share in 2025, while the premium tier shows the highest 9.35% CAGR to 2031 within the United States outdoor furniture market.

- By distribution channel, B2B accounted for a 59.87% share in 2025, and online retail recorded the fastest 10.32% CAGR to 2031 in the United States outdoor furniture market.

- By geography, the South captured 46.34% of the United States outdoor furniture market share in 2025, while the United States outdoor furniture market size for the West is projected to grow at a 7.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Outdoor Furniture Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Remote work-driven outdoor renovations | +1.2% | National tech-focused metros | Medium term (2-4 years) |

| Hospitality shift to expanded outdoor dining | +0.8% | Urban centers and tourist areas | Short term (≤ 2 years) |

| Eco mandates boosting certified wood and recycled plastics | +0.7% | Coastal states | Long term (≥ 4 years) |

| Sunbelt housing boom raising patio spending | +1.0% | Florida, Texas, Arizona, California | Medium term (2-4 years) |

| Smart-enabled furniture with lighting and charging features | +0.5% | Affluent suburbs and cities | Medium term (2-4 years) |

| Online retail surge powered by AR visualization tools | +0.6% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Remote work-driven outdoor renovations

Remote work normalization has reshaped how households use exterior areas by making patios and porches extensions of daily life. In 2025, 59% of United States consumers indicated plans to buy new outdoor furniture, with Millennials showing the highest intent at 76%, which reinforced the role of seating and dining pieces in home-based entertaining and work-from-home routines[1]ICFANET.ORG https://www.icfanet.org/news/2025_trend_report. Consumers who upgrade outdoor spaces report spending more time relaxing and entertaining after installations, which keeps the category on replacement cycles instead of being a one-off seasonal purchase. Preferences in the South and West emphasize covered outdoor rooms, fire features, and outdoor kitchens, which support demand for both weather-resistant materials and comfort-focused upholstery. The residential segment benefits from these patterns and maintains the fastest growth outlook through 2031 as household use of outdoor assets becomes a standard part of American home life.

Hospitality shift to expanded outdoor dining

Operators in restaurants and hotels have moved temporary outdoor seating into standard operating configurations by using codified permit programs. Dining Out NYC rules set clear parameters for placement, safety, and structures, while cities like Portland have established permit types with annual fees and area-based charges that formalize year-round outdoor operations[2]PORTLAND.GOV https://www.portland.gov/transportation/permitting/business-support/outdoor-dining. Accessibility rules require clear floor space at fixed tables and compliant surface heights, which pushes operators toward commercial-grade furniture that meets ADA guidance. The industry has also advanced outdoor performance testing by consolidating standards for structural integrity and accelerated weathering through BIFMA’s OF-2025 framework. These policies and standards align with high utilization in urban and resort locations and support volume orders of durable seating, tables, and shade systems.

Eco mandates boosting certified wood and recycled plastics

Compliance requirements for composite wood products cap formaldehyde emissions at specific levels, which aligns with independent certification and responsible sourcing. California’s consumer product rules restrict volatile organic compounds in maintenance products and prohibit high global warming potential compounds for furniture care, which shapes product selection in commercial settings. Industry scorecards show a mix of leaders and laggards on wood sourcing, with a subset of retailers and brands achieving high marks and others documenting progress plans. For wood, FSC certification and audited chains of custody give buyers documentation that supports procurement policies and municipal requirements. Together, these rules and market initiatives have increased interest in recycled resin, certified solid wood, and low-emissions finishes[3]FSC.ORG https://fsc.org/en/businesses/furniture.

Sunbelt housing boom raising patio spending

New residential construction activity concentrates in the South and West, where detached homes and townhomes often include patios or covered outdoor spaces. In August 2025, the South recorded 667,000 starts on a seasonally adjusted annual basis, representing roughly half of national activity, which supports higher per-household purchases of chairs, dining sets, and integrated shade. The West also saw a rebound in single-family activity during 2025, which correlates with increased procurement of premium materials that perform in heat and sun exposure. Builders have included patios in a large share of new single-family starts in recent years, which aligns with homeowner interest in covered rooms and outdoor kitchens. These structural tailwinds maintain the South’s share leadership and support the West’s above-market growth profile.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lumber and aluminum price swings | -0.6% | Nationwide, heavier for domestic makers | Short term (≤ 2 years) |

| Skilled labor shortages in furniture manufacturing | -0.4% | North Carolina, Michigan, California hubs | Medium term (2-4 years) |

| Fire-safety and VOC compliance costs for cushions | -0.3% | California and aligned states | Long term (≥ 4 years) |

| Distribution hub reductions and logistic bottlenecks | -0.2% | National freight corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lumber and aluminum price swings

Commodity input movements have pressured margins and pricing strategies for wood and metal-based outdoor furniture. Manufacturers increased emphasis on hedging, supplier diversification, and design optimizations to manage bill-of-materials exposure in 2025. Inventory positions in furniture categories rose during 2025 as companies balanced the risk of delays with carrying cost tradeoffs, which points to cautious stock planning across the value chain. Tiered assortments and premiumization have partially offset cost inflation by differentiating performance and lifespan, while contract-grade categories use specifications to justify higher price points. These conditions encourage the use of recycled resin, aluminum alloys with favorable cost-performance profiles, and engineered wood alternatives where appropriate.

Skilled labor shortages in furniture manufacturing

Furniture producers faced ongoing hiring challenges that reduced capacity utilization in several manufacturing hubs during 2025. Employment within furniture manufacturing declined in late 2025, and firms reported difficulty recruiting upholsterers, skilled woodworkers, and CNC technicians. Wage differentials relative to other trades and the perception of limited long-term career pathways have weighed on recruitment, which has led companies to explore automation and targeted training partnerships. Industry employment statistics show notable job losses across the year, which aligns with reports of extended build and delivery times for complex products. Training investments and targeted programs are underway, yet official projections suggest modest long-term declines in certain occupations due to productivity gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Volume Leaders Meet Fast-Growing Niches

Chairs accounted for 45.74% of the United States outdoor furniture market in 2025, driven by high sales, diverse formats in dining and lounge sets, and steady replacement cycles. In 2024, lounge seating gained popularity, boosting demand for comfort-focused designs with quick-dry cushions and weather-resistant upholstery. Accessibility guidelines for public seating areas, requiring compliance with floor space and height standards, supported demand for commercial fixtures. Dining and conversation sets benefited from coordinated purchases, creating cohesive outdoor spaces for homes and restaurants. Loungers and daybeds grew at a 9.78% CAGR, reflecting consumer preferences for relaxation, poolside use, and seamless indoor-outdoor transitions.

Product preferences in the United States outdoor furniture market balance availability, durability, and aesthetics. Chairs remain essential for residential patios and commercial terraces, accommodating daily meals and large gatherings with minimal adjustments. The rise in loungers and daybeds aligns with the trend toward multifunctional outdoor spaces for leisure and social activities. Tables anchor dining and coffee areas, while modular seating sets attract coordinated-buy shoppers. Hospitality and municipal buyers sustain demand for contract-grade pieces by standardizing specifications to simplify maintenance and replacement.

By Material: Wood Dominance Meets Metal’s Momentum

Wood held a 51.36% market share in 2025, driven by natural aesthetics, repairability, and premium species like teak. Metal achieved an 8.76% CAGR due to its corrosion resistance and structural strength in the United States outdoor furniture market. While few companies excelled in responsible wood practices, leading retailers advanced certified sourcing and traceability. Salt spray and thermal cycling tests differentiate contract and residential-grade offerings. Plastics and polymers, such as recycled HDPE, dominate the economy and mid-range segments, reducing maintenance without compromising weatherability. Composite lumber suppliers emphasize recycled content and heat-mitigating innovations for hot climates.

Regulatory limits on formaldehyde emissions influence material and coating choices. Procurement policies in the West Coast and Northeast markets favor certified wood and low-VOC products. Recycled resin adoption grows as municipalities and commercial buyers align with eco-labeling and lifecycle considerations. Metals gain popularity in coastal and humid regions, with aluminum frames and powder coating offering durability and predictable maintenance. Advances in powder-coat chemistry and fastener selection address corrosion and thermal expansion. The material mix reflects practical use cases, building codes, and sustainability commitments in the United States outdoor furniture market.

By End User: Commercial Scale Meets Residential Growth

The commercial segment held a 62.37% share in the United States outdoor furniture market in 2025, driven by hospitality dining, corporate campuses, and public spaces. The residential segment is expected to grow at a 9.87% CAGR through 2031. Permanent outdoor dining programs and ADA regulations favor durable, contract-grade pieces that meet structural and weathering standards, ensuring safety and compliance. Residential buyers are investing in patios and porches for work and leisure, supported by widespread access to outdoor spaces. This dual-track demand supports both bulk procurement and consumer purchases.

Homeowners prioritize covered areas, fire features, and outdoor kitchens, increasing demand for durable tables, lounge seating, and dining sets. Commercial customers focus on maximizing seating while maintaining access routes, favoring stackable chairs, stable tables, and modular shade systems. Supply partners differentiate through specification support and installation services for multi-site rollouts. Residential buyers use digital tools and in-store visits to compare finishes, cushions, and frame materials across price tiers. These preferences shape assortments and stocking strategies in the United States outdoor furniture industry.

By Price Range: Mid-Range Volume Meets Premium Acceleration

Mid-range products accounted for 52.73% of the market in 2025, driven by consumer demand for affordability and durability. Premium offerings in the United States outdoor furniture market are projected to grow at a 9.35% CAGR through 2031. Luxury collections emphasize exclusive designs, premium materials, and long warranties, attracting affluent households with higher price points and repeat purchases. Composite brands focus on recycled content and heat-diffusing technologies for sunlit environments. Consumers prioritize practicality and invest in exact-match items, stabilizing mid-range demand through coordinated sets and replacement cushions. Economy assortments remain relevant for budget-conscious buyers in rentals, second homes, and seasonal use.

Premium growth is supported by technology integrations, designer collaborations, and curated catalogs showcasing complete outdoor setups. Mid-range volumes flow through home centers, specialty retailers, and direct-to-consumer platforms, leveraging material mixes and streamlined logistics to manage price points. Premium segments differentiate through warranties and service levels, while value tiers focus on ease of assembly and availability. Retailers adjust assortments to suit regional climates and code requirements for multi-family and hospitality projects. This price segmentation enables targeted marketing and efficient inventory planning across the United States outdoor furniture market.

By Distribution Channel: B2B Scale Meets Online Disruption

B2B accounted for a 59.87% share in 2025 as distributors and contract partners outfitted hospitality sites and public spaces, while online retail posted a 10.32% CAGR to 2031 in the United States outdoor furniture market. Distribution agreements expanded geographic coverage for composite railing and decking systems, which support integrated projects that include furniture zones. Municipal and campus buyers rely on specification support and installation expertise, which bolsters the role of contract-focused channels. Retail B2C and specialty stores capture residential volume through immediate availability and curated set presentations with companion shade and fire features. Direct-to-consumer brands pair digital discovery with selected showrooms to compress delivery timelines and simplify configuration.

Omnichannel strategies bridge catalogs, e-commerce, and experience centers where buyers can assess finishes, textiles, and ergonomics. Contract teams focus on ADA compliance and ingress protection for powered elements, which drives selection toward proven SKUs in high-traffic locations. Retailers expand private-label programs at key price points, while brands refine packaging and last-mile services to reduce damages and returns. Online research behaviors influence in-store conversion through QR-guided configuration and swatch sampling. This mix of channels continues to evolve as buyers expect consistent information and reliable lead times in the United States outdoor furniture market.

Geography Analysis

The South held a 46.34% market share in 2025, driven by favorable climates, household migration, and single-family construction emphasizing outdoor spaces. Housing starts in the South reached 667,000 in August 2025 (seasonally adjusted annual basis), sustaining demand for dining sets, lounge seating, and shade structures. Hospitality deployments in resort corridors and urban centers transitioned outdoor seating from temporary to permanent infrastructure. Legacy manufacturing resources and trade associations in southern hubs guide sustainability practices and compliance. High import reliance for key categories influences sourcing strategies during cost volatility.

The West is projected to achieve a 7.03% CAGR through 2031, supported by rising construction activity and demand for premium products in coastal metros. Single-family starts rebounded in 2025, driving purchases of durable, low-maintenance materials suited for heat and sunlight. Municipal outdoor dining frameworks in western cities align with increased use of public plazas and parklets. Composite suppliers expanded distribution networks to improve product availability. Innovations in heat management and UV protection technologies are gaining traction among Western buyers.

The Midwest and Northeast contribute smaller shares with steady replacement demand and shorter outdoor seasons. The Midwest recorded 220,000 housing starts in August 2025 (seasonally adjusted annual basis), maintaining demand for patio and porch installations. Northeastern markets balance urban density and historic districts with outdoor spaces requiring specific accessibility considerations. Manufacturers and distributors support four-season use cases with durable, modular, and weather-resistant materials, protective covers, and compact configurations for limited spaces.

Competitive Landscape

The United States outdoor furniture market comprises established brands, niche players, and direct-to-consumer entrants competing on durability, design, and service. Trex Company utilizes composite technologies with high recycled content to expand into related categories and accessories. The company announced capital investments for facility expansions and heat-mitigating surface technologies, set for 2026. Partnerships with regional building products distributors have extended its reach across Western states, enabling Trex to offer integrated solutions combining furniture zones with decking and railing.

RH differentiates itself in the luxury segment with exclusive designer collections, premium materials, and complete outdoor room setups[4]RH, “RH Unveils 2025 Outdoor Sourcebook With Over 40 Exclusive Collections by Acclaimed Designers From Around the World,” ir.rh.com. Its 2025 Outdoor Sourcebook introduced over 40 collections, emphasizing premium teak, aluminum, and all-weather wicker in refined styles. Collaborations with designers and shade manufacturers ensure cohesive aesthetics and flexible specifications. Catalogs and galleries serve as effective selling tools, promoting set-based purchases like lounge, dining, and poolside arrangements. This premium focus drives higher order values and brand loyalty in the U.S. outdoor furniture market.

Polywood and Yardbird highlight the role of material innovation and omnichannel strategies in shaping competition. Polywood scales domestic manufacturing and introduces proprietary lumber technologies that enhance surface performance and color retention, supported by multi-year warranties. Yardbird combines a digital-first approach with growing physical touchpoints, emphasizing reclaimed and ocean-bound plastics. Large retailers rely on private-label programs and nationwide distribution, while specialty dealers focus on custom configurations and curated assortments. The market remains moderately fragmented, with differentiation driven by materials science, brand design, and channel strategies.

United States Outdoor Furniture Industry Leaders

Ashley Furniture Industries Inc.

Brown Jordan Inc.

Home Depot Product Authority LLC

Lowe’s Companies Inc.

Williams-Sonoma Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Trex expanded its Western United States presence by partnering with International Wood Products, adding a Salt Lake City facility to its six distribution centers. These centers now exclusively stock Trex Select™ aluminum and Trex Enhance™ steel railing systems.

- May 2025: POLYWOOD®, a pioneer in sustainable, American-made outdoor furniture, unveiled POLYWOOD Select™, a new line designed to elevate the aesthetic of any outdoor setting.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United States outdoor furniture market as revenue from new seating, dining, storage, and accessory pieces purpose-built for open-air residential or commercial settings; products may be wood, metal, recycled plastics, wicker, stone, or hybrid composites provided they are intended for year-round external use.

Scope exclusion: Used goods, indoor-only furniture, and camping gear sit outside this perimeter.

Segmentation Overview

- By Product

- Chairs

- Tables

- Seating Sets

- Loungers and Daybeds

- Dining Sets

- Other Products

- By Material

- Wood

- Metal

- Plastic & Polymer

- Other Materials

- By End User

- Residential

- Commercial

- By Price Range

- Economy

- Mid-Range

- Premium

- By Distribution Channel

- Retail/B2C Channels

- Home Centers

- Specialty Stores

- Online

- Other Distribution Channels

- B2B Channel/Contractors

- Retail/B2C Channels

- By Geography

- Northeast

- Midwest

- South

- West

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed specialty retailers, hospitality buyers, contract installers, material suppliers, and regional wholesalers across the Sunbelt, Midwest, and Coastal corridors. These discussions clarified average selling prices, seasonal inventory swings, recycled-material adoption, and the online share of orders, allowing us to triangulate survey findings with desk evidence.

Desk Research

We began with United States Census Bureau retail and housing-starts files, Bureau of Economic Analysis consumer-spending tables, International Casual Furnishings Association shipment surveys, and USITC customs data for HS 9403 articles. Environmental Protection Agency recycling reports, American Hotel & Lodging Association pipeline trackers, company 10-K splits, and reputable business press added context on material shifts and contract wins. Paid databases, notably D&B Hoovers for supplier revenues and Dow Jones Factiva for transaction news, helped verify channel dynamics. The sources cited are illustrative; many additional references supported data collection and validation.

Market-Sizing & Forecasting

A top-down build starts with 2024 consumer and commercial furniture expenditure, rebased to outdoor share using housing completions, restaurant patio square footage, distributor shipments, and ICFA penetration ratios. Selective bottom-up checks sampled supplier revenues and channel sell-through scans calibrate totals for direct-to-consumer volumes. Key inputs include housing starts, hotel outdoor dining investments, material-wise average prices, tariff movements on wood and metal frames, and e-commerce share. Forecasts rely on multivariate regression blended with scenario analysis so disposable-income elasticity and raw-material indices temper growth paths through 2030. Any missing small-supplier data is patched with peer averages linked to disclosed capacities.

Data Validation & Update Cycle

Before release, a second analyst reconciles model outputs with shipment and trade signals; variances above three percent trigger re-checks. Reports refresh each year, with interim updates for tariff shifts, building-code revisions, or extreme weather events that materially sway demand.

Why Mordor's United States Outdoor Furniture Baseline Commands Reliability

Published estimates often diverge because firms mix product lines, apply differing average prices, or lock exchange rates to a single month. Mordor Intelligence counts only first-sale value of durable outdoor pieces, applies U S-specific prices, and updates on a disciplined annual cadence, which keeps our baseline current while avoiding short-lived spikes.

Key gap drivers include competitors folding outdoor kitchens into scope, using global prices rather than U S benchmarks, or projecting directly off housing starts without discounting replacements; some also translate revenues at fixed 2022 dollars whereas we convert monthly movements.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.53 B (2025) | Mordor Intelligence | |

| USD 12.76 B (2022) | Regional Consultancy A | Includes grills and built-in kitchens; historic base year not rebased to 2025 |

| USD 14.30 B (2024) | Global Consultancy B | Uses global average selling price, limited primary checks, no duty adjustment |

In summary, the disciplined scope selection, transparent variables, and multi-step validation followed by Mordor analysts deliver a balanced, repeatable figure that decision-makers can trust.

Key Questions Answered in the Report

What is the size and growth outlook of the United States outdoor furniture market by 2031?

The United States outdoor furniture market size is USD 7.41 billion in 2026 and is forecast to reach USD 10.03 billion by 2031 at a 6.24% CAGR.

Which product categories lead demand in the United States outdoor furniture market?

Chairs lead on volume with a 45.74% share in 2025, and loungers and daybeds show the fastest 9.78% CAGR as households invest in comfort-oriented seating.

Which regions contribute most to sales within the United States outdoor furniture market?

The South held a 46.34% share in 2025, supported by strong housing starts, while the West recorded the fastest projected 7.03% CAGR to 2031.

How are sustainability and compliance affecting the United States outdoor furniture market?

Emissions caps for composite wood and VOC limits in maintenance products, alongside FSC certification and recycled materials, are shaping sourcing and product specifications.

What channels are growing fastest in the United States outdoor furniture market?

B2B channels led with 59.87% share in 2025, and online retail is the fastest-growing channel with a 10.32% CAGR to 2031.

What challenges could slow growth in the United States outdoor furniture market?

Volatile input costs and skilled labor shortages weigh on margins and production timing, although inventory and sourcing strategies are helping firms absorb near-term pressure.

Page last updated on: