Outage Management Systems Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

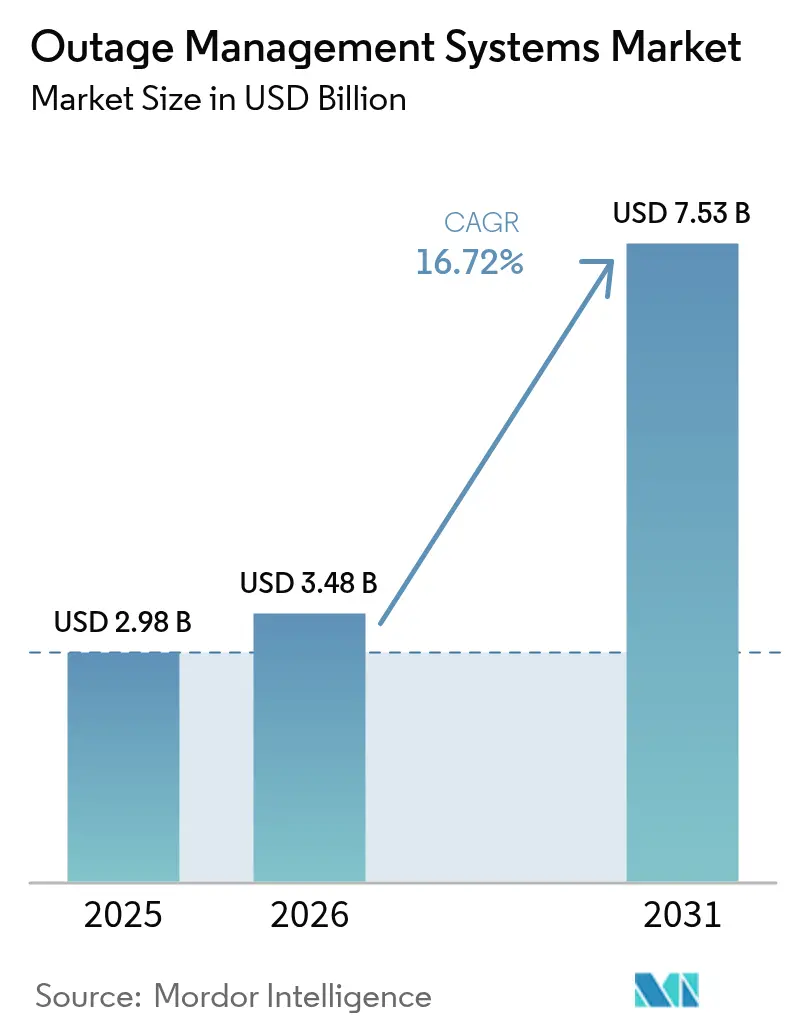

| Market Size (2026) | USD 3.48 Billion |

| Market Size (2031) | USD 7.53 Billion |

| Growth Rate (2026 - 2031) | 16.72% CAGR |

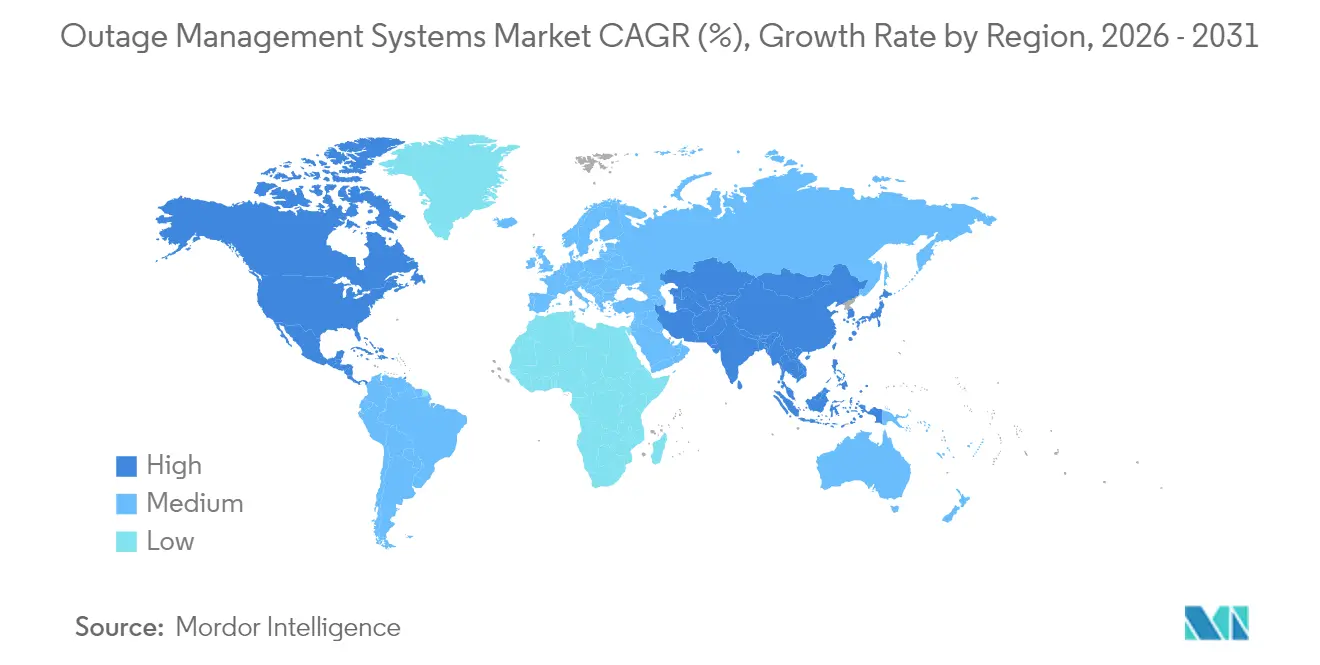

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Outage Management Systems Market Analysis by Mordor Intelligence

The Outage Management Systems Market size was valued at USD 2.98 billion in 2025 and estimated to grow from USD 3.48 billion in 2026 to reach USD 7.53 billion by 2031, at a CAGR of 16.72% during the forecast period (2026-2031).

Demand accelerates as utilities deploy AI-enabled grid orchestration to counter rising climate-driven disruptions, integrate rapidly growing distributed energy resources (DERs), and meet increasingly stringent reliability metrics, such as SAIDI and SAIFI. Regulatory mandates now require utilities to replace legacy fault-location tools with predictive analytics platforms that ingest real-time data from smart inverters, AMI, and SCADA networks, resulting in sustained capital expenditures. Integrated solutions dominate because they consolidate fault detection, crew dispatch, and customer communications inside one vendor ecosystem, reducing data-silo friction and accelerating restoration cycles. Although on-premise deployments still prevail, hybrid and cloud architectures are gaining ground, offering scalable AI processing for vegetation management and predictive maintenance while addressing cybersecurity through Zero-Trust designs. Geographically, North America anchors spending with federal transmission investments, whereas Asia-Pacific emerges as the fastest-growing market, propelled by China’s record grid modernization funding and Japan’s large-scale infrastructure upgrades.

Key Report Takeaways

- By type, Integrated platforms held 61.90% of the Outage Management System market share in 2025, while standalone solutions declined in relative importance.

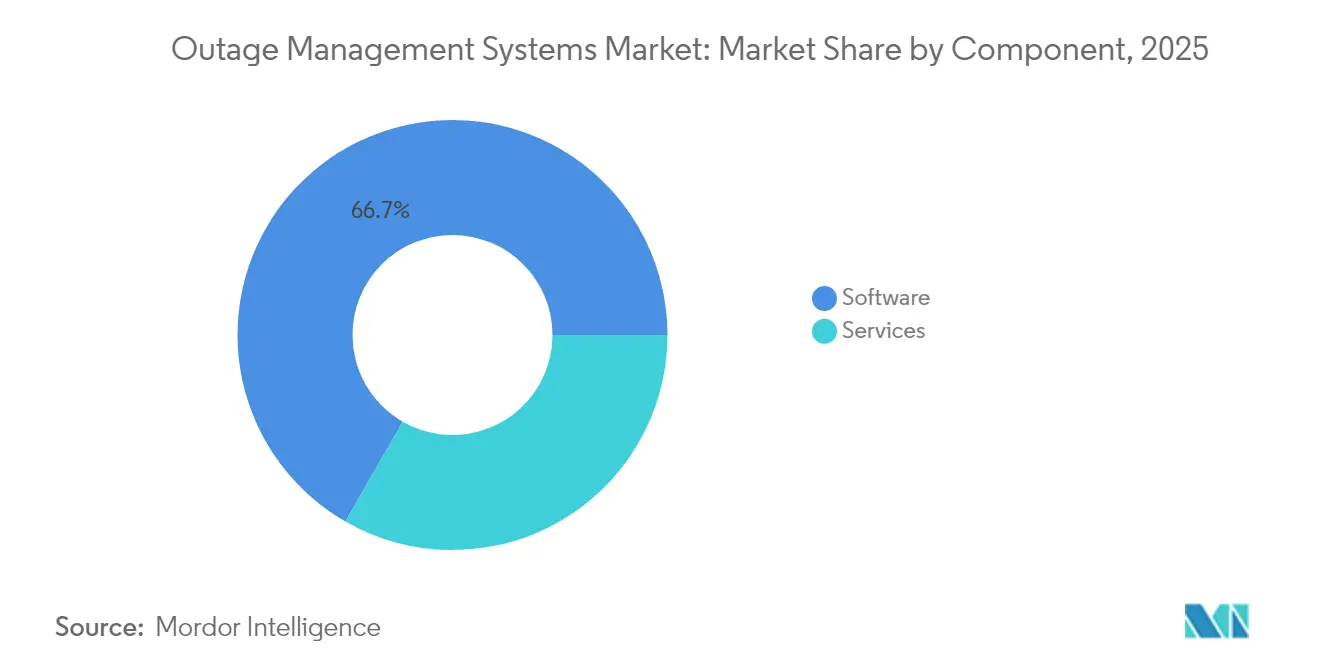

- By component, software captured 66.70% of the revenue in 2025; the services segment is advancing at a 18.02% CAGR to 2031 as utilities seek AI/ML expertise.

- By deployment mode, On-premise deployments retained a 63.10% share in 2025; however, cloud-based options are rising at a 20.05% CAGR, driven by hybrid adoption strategies.

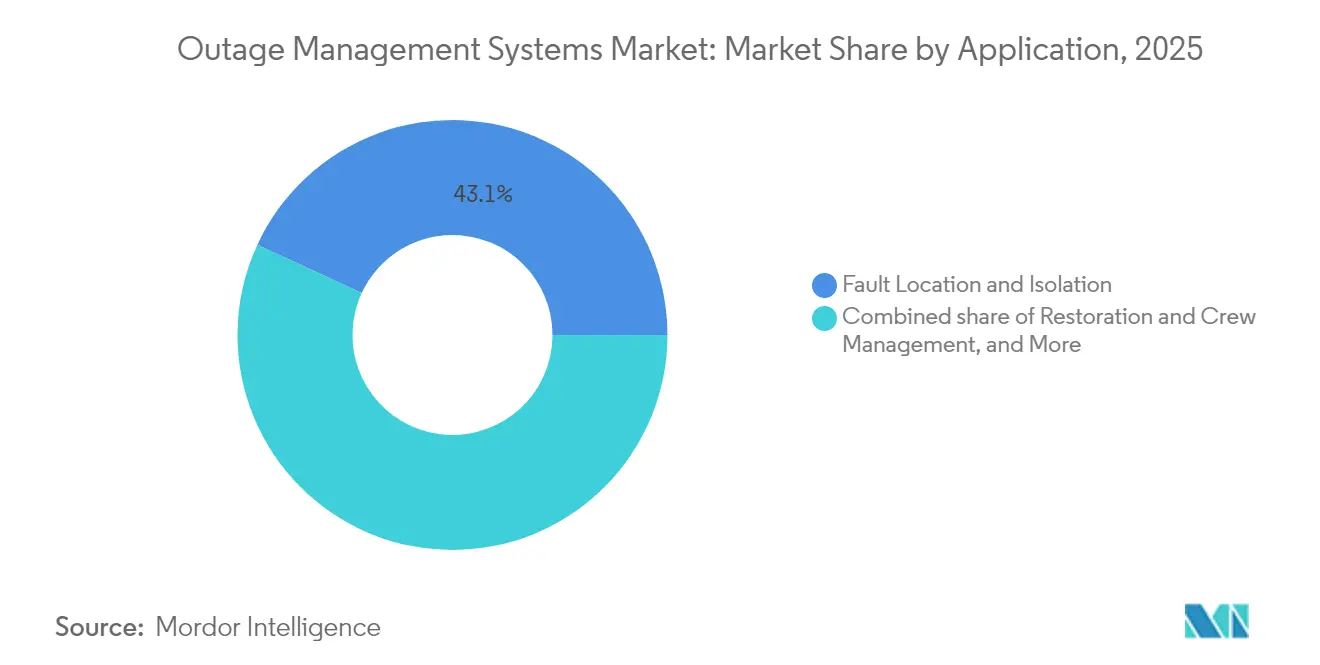

- By application, fault location and isolation accounted for 43.10% of the 2025 Outage Management System market size, while restoration and crew management led growth at 18.35%.

- By geography, North America accounted for 37.00% of the revenue in 2025; the Asia-Pacific region is projected to grow at a 19.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Outage Management Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying climate-related outages boosting grid-resilience spend | 4.20% | High in North America and Asia-Pacific coastal markets | Medium term (2-4 years) |

| Smart-grid & ADMS roll-outs across Tier-1 utilities | 3.80% | North America, Europe, expanding into Asia-Pacific core markets | Long term (≥ 4 years) |

| Reliability-index (SAIDI/SAIFI) compliance mandates | 2.90% | Global, variable enforcement | Short term (≤ 2 years) |

| AI-driven predictive outage analytics adoption | 3.10% | Early uptake in North America and Europe | Medium term (2-4 years) |

| DER proliferation demanding real-time visibility | 2.40% | Global, strongest in renewable-heavy grids | Long term (≥ 4 years) |

| Shift to cloud-native OMS & mobile workforce tools | 1.80% | Faster uptake in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Intensifying Climate-Related Outages Boosting Grid-Resilience Spend

Weather now drives nearly 80% of major outages, prompting utilities to invest heavily in grid-hardening initiatives, such as automated sectionalizers, undergrounding, and AI-based vegetation analytics(1)Source: Laila Sharpless & Christine Byrne, “Powering Up Resilience,” T&D World, tdworld.com . CenterPoint Energy alone has allocated USD 21 billion over five years to bolster storm resilience, illustrating the large-scale capital currently being invested in preventive technologies(2)Source: CenterPoint Energy, “Collaboration with Technosylva,” centerpointenergy.com . OMS platforms have evolved from fault location tools into comprehensive resilience hubs that integrate weather feeds, asset health data, and automated switching. The economic stakes are evident as multi-day outages repeatedly impose multi-billion-dollar losses on regional economies, strengthening return-on-investment arguments for predictive solutions. Utilities also recognize that preventing customer interruptions enhances satisfaction metrics more effectively than merely accelerating restoration, which in turn prompts accelerated OMS upgrades.

Smart-Grid & ADMS Roll-Outs Across Tier-1 Utilities

Large utilities are replacing siloed applications with unified ADMS-OMS suites that can process SCADA, GIS, and AMI data in real-time. GE Vernova’s GridOS and Schneider Electric’s One Digital Grid platforms exemplify the shift, promising outage reductions of up to 40% through automated fault isolation and DER coordination(3)Source: GE Vernova, “GridOS Software Announcement,” gevernova.com . As bidirectional power flows rise, integrated solutions become indispensable, explaining their premium pricing and faster adoption curve. Utilities increasingly embed Zero-Trust security, reflecting regulators’ insistence on cyber-resilient architectures.

AI-Driven Predictive Outage Analytics Adoption

Artificial intelligence is moving utilities from reactive notification to predictive mitigation. Eversource reported avoiding 40,000 customer interruptions within two months of deploying AI algorithms trained on historical faults and weather patterns. California’s statewide adoption of AI-enabled outage management underscores regulatory confidence in machine-learning--based decision support. Accuracy rates ranging from 75% to 88% in identifying vulnerable grid assets are attainable; yet, 43% of utilities cite skill gaps as the primary obstacle to scaling AI use(4)Source: Marina Donovan, “Workforce Readiness Gap,” itron.com . Consulting and training, therefore, form a fast-growing services revenue pool.

DER Proliferation Demanding Real-Time Visibility

Rapid DER uptake requires OMS platforms to manage bidirectional flows and coordinate with virtual power plants. Sunrun’s network aggregated 80 MW of residential solar-plus-storage capacity in 2024, demonstrating DERs’ ability to deliver peak-support services(5)Source: Sunrun Inc., “Virtual Power Plant Programs,” sunrun.com . Utilities must therefore upgrade OMS solutions to maintain situational awareness and to dispatch distributed assets alongside traditional feeders. Vendors with DER-aware architectures are gaining a competitive advantage, particularly in markets enabling aggregator participation in wholesale settlements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex & legacy integration hurdles | -2.1% | Global with higher impact in regions with aging infrastructure | Medium term (2-4 years) |

| Cyber-security vulnerabilities in connected OMS | -1.7% | Global with heightened concerns in critical infrastructure regions | Short term (≤ 2 years) |

| GIS data-quality gaps undermining algorithms | -1.3% | Global with acute impact in utilities with legacy mapping systems | Medium term (2-4 years) |

| Workforce skill shortage in AI/ML analytics | -1.5% | North America & EU primary, expanding to APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capex & Legacy Integration Hurdles

Enterprise-grade OMS deployments often exceed USD 50 million for large investor-owned utilities. Cost escalates when integrating decades-old SCADA, GIS, and CIS assets that lack modern APIs, forcing custom middleware development and long data-migration projects. Organizational change management further complicates roll-outs as frontline crews adapt to automated workflows. Regulatory scrutiny remains intense because utilities must uphold reliability metrics during system migrations, amplifying execution risk.

Cyber-Security Vulnerabilities in Connected OMS

Expanding connectivity has magnified the attack surface across more than 23,000 grid entry points tracked by NERC in 2024, up from roughly 21,000 two years earlier. Academic studies show that coordinated strikes on smart inverters can destabilize grids, even at modest penetration levels(6)Source: Xiangyu Hui et al., “Destabilizing Power Grid,” arxiv.org . Utilities face talent shortages in cyber disciplines, making it difficult to implement Zero-Trust, continuous-monitoring frameworks at scale. Consequently, some operators delay cloud migrations or limit remote access, tempering short-term adoption of fully connected architectures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Integrated Solutions Drive Market Consolidation

Integrated platforms commanded 61.90% of the revenue in 2025 and are forecast to grow at a 19.12% CAGR to 2031, reflecting utilities’ drive to consolidate multiple point tools into a single pane of glass. This leadership position underscores how integrated suites cut vendor-management overhead, eliminate data-silo latency, and streamline restoration workflows. Utilities that deploy integrated offerings report 30-40% shorter average outage durations compared to users of fragmented systems.

Oracle’s Energy & Water Data Intelligence exemplifies the trend, fusing operational telemetry, weather intelligence, and customer analytics to automate decision logic. As a result, the Outage Management System market size attributed to integrated solutions is set to widen its lead over standalone deployments through 2031. Vendors with comprehensive portfolios, therefore, obtain negotiating leverage, while niche point-solution providers increasingly seek partnerships or acquisitions to remain relevant.

By Component: Services Surge as AI Complexity Grows

Software maintained a 66.70% share in 2025, anchored by mature codebases from ABB, GE Vernova, and Schneider Electric. Yet services are expanding at 18.02% CAGR because utilities need guidance in AI model training, cyber-hardening, and multi-system data alignment. Consulting captures the fastest growth as utilities confront jurisdiction-specific reliability rules and cloud-sovereignty statutes.

Implementation and support also scale briskly because software procurement accounts for only about one-third of total project spend. The transition toward subscription models reinforces vendor annuity streams. Schneider Electric recorded a 140% jump in SaaS revenue in 2024, signaling utilities’ willingness to trade capital expenditures (capex) for operational expenditures (opex). Consequently, service providers wield outsized influence over project outcomes, nudging the Outage Management System market toward higher lifetime-value economics.

By Deployment Mode: Cloud Adoption Accelerates Despite Security Concerns

On-premise installations retained a 63.10% share in 2025 because utilities prize local control of mission-critical data and have invested in hardened data centers. Nevertheless, cloud-hosted deployments are rising at a 20.05% CAGR. Hybrid topologies are now common: operational controls remain on-site while heavy-compute analytics run in Amazon Web Services or Microsoft Azure environments.

Hitachi Energy’s tie-up with AWS exemplifies this model, utilizing satellite imagery and AI to forecast vegetation-caused outages while maintaining real-time SCADA loops on utility premises. Vendors that offer flexible data-sovereignty options, therefore, find receptive audiences, and utilities increasingly stipulate Zero-Trust architectures and immutable-log capabilities as baseline procurement criteria.

By Application: Restoration Management Gains Momentum

Fault location and isolation generated 43.10% of 2025 revenues, cementing its role as a foundational capability. However, restoration and crew management tools are expanding at 18.35% CAGR as utilities aim to minimize customer minutes interrupted by optimizing workforce routing. These modules integrate real-time traffic feeds, crew skill profiles, and inventory data to prioritize repair tasks, steadily increasing the Outage Management System's market share for restoration applications.

Customer communication functions, while essential, face commoditization because multi-channel messaging frameworks are now ubiquitous. Consequently, differentiation shifts to AI-enabled crew dispatch and predictive asset inspection. Vendors embedding mobile workforce apps that operate during severe weather secure premium contract values and lock-in through continuous feature updates.

Geography Analysis

North America generated 37.00% of the Outage Management System market revenue in 2025, driven by USD 8 billion in federal transmission grants and a series of severe weather events that compelled utilities to strengthen their grids. Investors reward the procurement of integrated solutions because it visibly improves SAIDI/SAIFI performance. Canada supports regional momentum through provincial-level modernization, as illustrated by Énergie NB Power’s AI-based outage prediction program, which restored 90% of customers within 24 hours during a 2024 ice storm.

The Asia-Pacific region is the fastest-growing, with a 19.18% CAGR. China’s State Grid budgeted more than 600 billion yuan in 2024 for digital substations and ultra-high-voltage corridors, fuelling large OMS tenders. Japan committed upwards of 150 billion yen to reinforce its network in anticipation of AI-driven data-center expansion. India presents additional upside, as Hitachi Energy has earmarked INR 2,000 crore to scale its domestic manufacturing and digital solutions capabilities.

Europe, Latin America, and the Middle East & Africa show steady though lower growth. In Latin America, Chile’s 2050 carbon-neutrality roadmap requires USD 431 billion in distribution spending by 2040, thereby expanding the addressable OMS budgets. European utilities emphasize DER integration and storm-resilience upgrades but face slower revenue expansion given their matured grid-modernization baselines. Across all secondary regions, government policy support and multilateral climate finance mechanisms play pivotal roles in the pace of OMS adoption.

Competitive Landscape

Competition spans global conglomerates, mid-tier domain specialists, and AI-native startups, yielding moderate market fragmentation. ABB, GE Vernova, Schneider Electric, and Siemens anchor the top tier with comprehensive end-to-end portfolios that cover OMS, ADMS, SCADA, and cybersecurity. Their long-standing utility relationships, robust service arms, and ongoing R&D investments underpin their sticky market positions. Mid-sized players, such as Survalent Technology and Milsoft Utility Solutions, win business by offering configurable software tailored to the needs of municipal and cooperative utilities.

Strategically, incumbents are acquiring AI capabilities: GE Vernova’s purchase of Alteia adds computer-vision analytics for predictive maintenance. Oracle’s recent launch of an AI-powered customer-service module further illustrates the pivot toward data intelligence. Vendors also forge cloud partnerships—such as Hitachi Energy with AWS and Itron with Microsoft—to accelerate the time-to-market for advanced analytics. Startups specializing in vegetation-risk AI challenge traditional players but often partner with them instead of competing head-to-head, given utilities’ preference for proven vendors.

The Outage Management System market rewards vendors that marry domain depth with AI agility. As utilities standardize on integrated suites, smaller point-solution providers may face pressure to consolidate or specialize in niche areas. Cyber-resilience capabilities and DER orchestration functions are emerging as decisive evaluation criteria in ongoing RFPs.

Outage Management Systems Industry Leaders

ABB Ltd.

General Electric Company

Schneider Electric SA

Siemens AG

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: GE Vernova acquired France-based Alteia to deepen AI analytics for predictive outage management.

- May 2025: Oracle launched an AI-powered utility customer-service module integrating directly with OMS instances for proactive outage communication.

- March 2025: Hitachi Energy partnered with AWS to deliver satellite-based vegetation analytics for U.S. utilities.

- March 2025: Itron and Schneider Electric collaborated with Microsoft to enhance grid-edge intelligence and transformer-to-meter mapping.

Global Outage Management Systems Market Report Scope

The outage management systems market report include:

| Stand-alone |

| Integrated |

| Software |

| Services |

| On-premise |

| Cloud |

| Fault Location and Isolation |

| Restoration and Crew Management |

| Customer Information and Call Handling |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Stand-alone | |

| Integrated | ||

| By Component | Software | |

| Services | ||

| By Deployment Mode | On-premise | |

| Cloud | ||

| By Application | Fault Location and Isolation | |

| Restoration and Crew Management | ||

| Customer Information and Call Handling | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecasted CAGR for the Outage Management System market from 2026 to 2031?

The market is projected to grow at a 16.72% CAGR, reaching USD 7.53 billion by 2031.

Which region is growing fastest in the Outage Management System market?

Asia-Pacific is expanding at 19.18% CAGR, supported by large-scale grid modernization in China, Japan, and India.

Why are integrated OMS platforms preferred over standalone solutions?

Integrated suites cut vendor-management overhead, unify data streams, and have demonstrated 30-40% reductions in outage duration versus fragmented toolsets.

How significant is cloud deployment in the Outage Management System industry?

While on-premise still holds 63.10% share, cloud-hosted OMS is expanding at 20.05% CAGR as utilities adopt hybrid architectures for AI-driven analytics.

What is driving demand for services within the Outage Management System market?

Utilities require expertise in AI model development, cyber-resilience, and complex legacy-system integration, pushing services growth to an 18.02% CAGR.

Which application segment is advancing fastest?

Restoration and crew management solutions lead with an 18.35% CAGR as utilities prioritize rapid resource allocation to minimize customer-minute interruptions.

Page last updated on: