Distribution Feeder Automation System Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

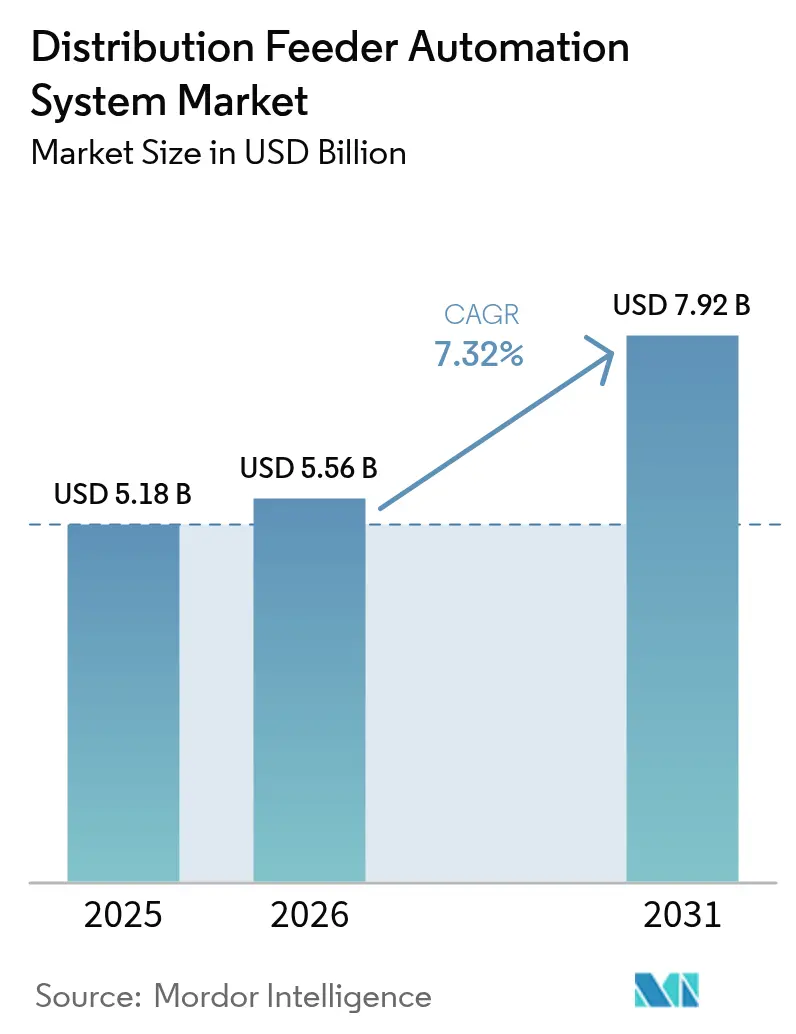

| Market Size (2026) | USD 5.56 Billion |

| Market Size (2031) | USD 7.92 Billion |

| Growth Rate (2026 - 2031) | 7.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Distribution Feeder Automation System Market Analysis by Mordor Intelligence

The Distribution Feeder Automation System Market size is expected to grow from USD 5.18 billion in 2025 to USD 5.56 billion in 2026 and is forecast to reach USD 7.92 billion by 2031 at 7.32% CAGR over 2026-2031.

Regulatory mandates that force utilities to modernize aging assets, the cost advantage of AI-powered fault-prediction analytics, and unprecedented public funding for climate-resilient grids combine to create sustained demand. North America remains the revenue leader, yet Asia-Pacific’s double-digit expansion rate indicates an impending geographic rebalancing. Utilities are increasingly prioritizing software-centric solutions that extend the value of installed hardware, while a surge of mergers among electrical distributors indicates that scale and technology integration now dictate competitive advantage.

Key Report Takeaways

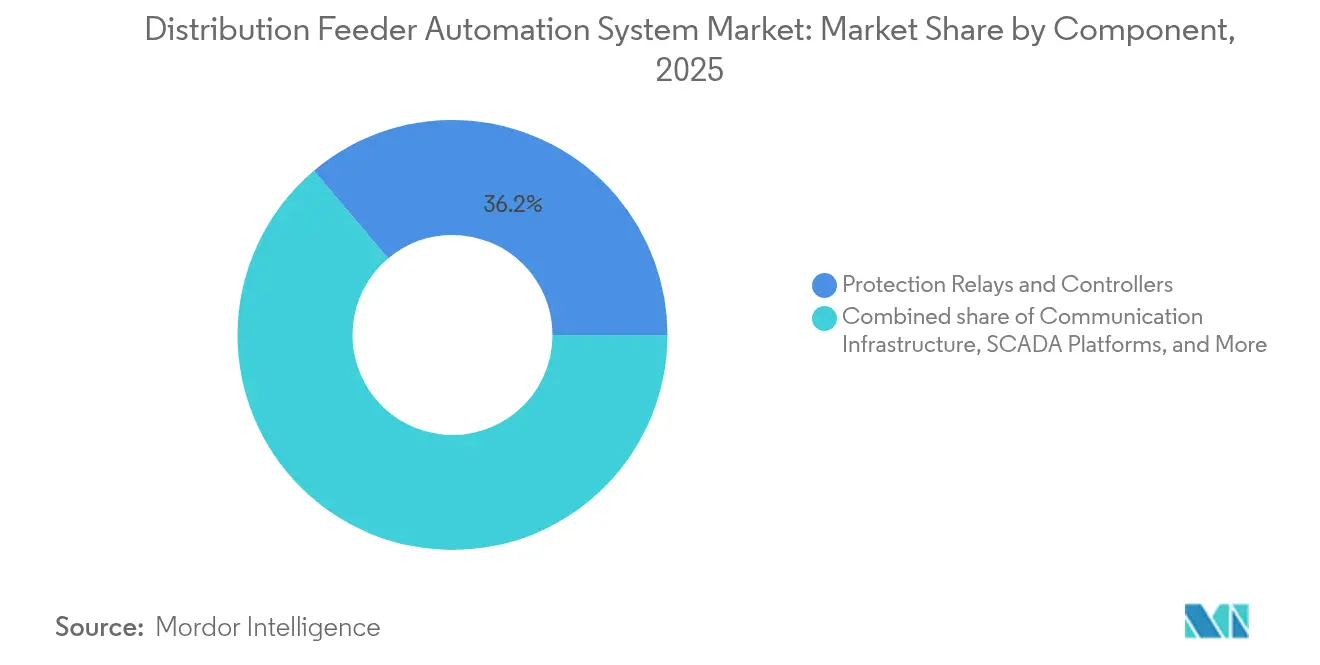

- By component, protection relays and controllers commanded a 36.15% market share of the distribution feeder automation system in 2025; communication infrastructure is projected to expand at a 10.6% CAGR through 2031.

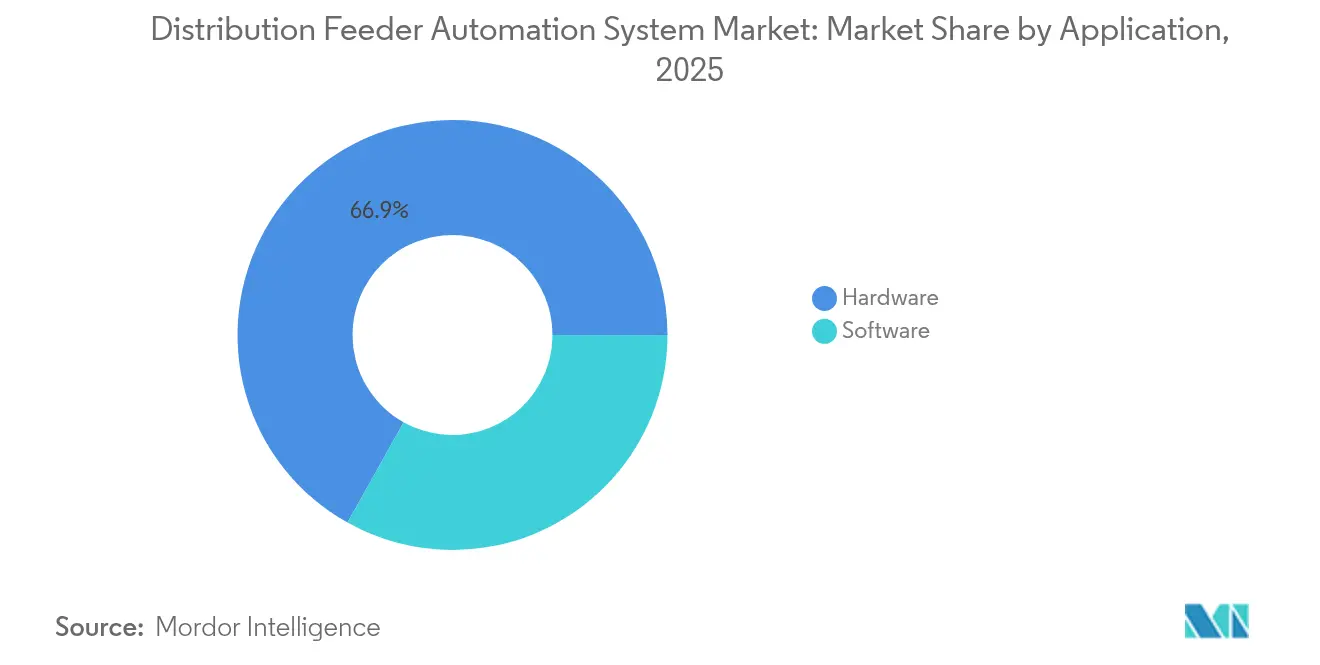

- By application, hardware accounted for 66.88% of the distribution feeder automation system market size in 2025, whereas software solutions are projected to advance at a 9.6% CAGR through 2031.

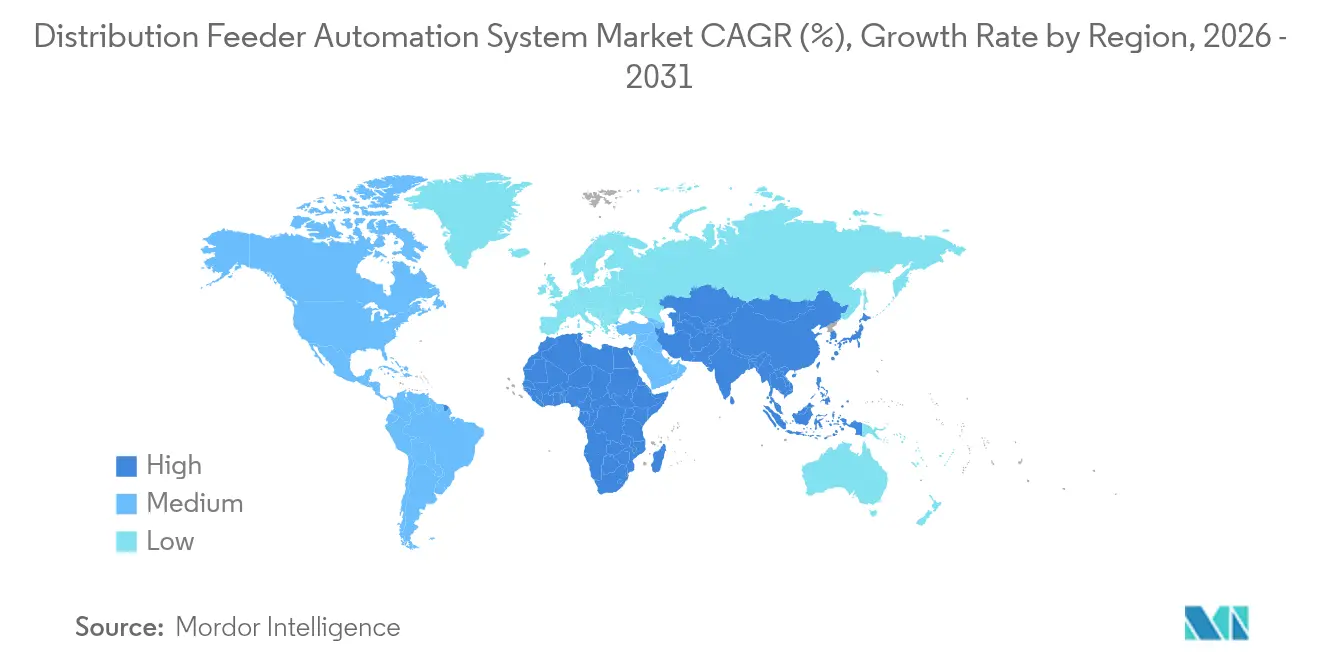

- By geography, North America led with a 31.75% revenue share in 2025, while the Asia-Pacific region is forecast to post the fastest growth of 10.1% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Distribution Feeder Automation System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid grid-modernization mandates | +1.8% | North America, EU, emerging APAC | Medium term (2-4 years) |

| Rising penetration of distributed generation (DER) | +1.5% | APAC and North America | Long term (≥ 4 years) |

| Ageing feeder infrastructure replacement cycles | +1.2% | North America, EU | Long term (≥ 4 years) |

| Utility-led digital-substation retrofit programs (OT-IT convergence) | +1.0% | Global developed markets | Medium term (2-4 years) |

| Surge in climate-resilient grid investment funds | +0.9% | Climate-vulnerable regions | Short term (≤ 2 years) |

| AI-driven fault-prediction analytics adoption | +0.7% | North America, EU, expanding APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Grid-Modernization Mandates

Federal and multilateral programs now channel record sums into grid resilience, providing utilities with budget certainty to invest in distribution feeder automation system projects. The U.S. Grid Resilience State and Tribal Formula Grant program alone disbursed USD 1.3 billion in 2024 to harden distribution networks against extreme weather.[1]U.S. Department of Energy, “Grid Resilience State and Tribal Formula Grants,” energy.gov European utilities face binding decarbonization targets that require annual distribution spending to double to EUR 67 billion (USD 73.7 billion) by 2050.[2]Eurelectric, “Power Sector Accelerates Distribution Grid Investment,” eurelectric.org Early adopters in both regions demonstrate fewer outages and lower operating costs, motivating lagging peers to accelerate procurement. Mandated spending translates into multi-year revenue visibility for suppliers and compresses utilities’ deferral options. Hardware vendors that bundle software analytics are more likely to qualify for competitive funding, as regulators increasingly measure reliability outcomes.

Rising Penetration of Distributed Generation (DER)

Solar, wind, and behind-the-meter storage are turning formerly passive distribution circuits into dynamic, two-way networks. California projects USD 4.28 billion in annual utility savings once its Integrated DER Management System scales statewide.[3]California Energy Commission, “Integrated DER Management System Savings Analysis,” energy.ca.gov The variability of DER output forces utilities to adopt advanced coordination algorithms that conventional automation cannot handle. As a result, software-driven schedulers and real-time optimizers gain traction across the distribution feeder automation system market. Suppliers capable of orchestrating thousands of inverters simultaneously win contracts in solar-rich regions, while hardware-only vendors risk commoditization.

Ageing Feeder Infrastructure Replacement Cycles

Distribution assets in the United States have an average service life of 40 years, and more than 79,000 substations require modernization to support digital operations. Utilities now pair asset renewal with automation upgrades to avoid locking in another multi-decade cycle of limited functionality. FirstEnergy’s USD 1.42 billion program in Pennsylvania exemplifies this bundling strategy, with spending on automated reclosers and advanced metering occurring concurrently with conductor replacements. Concentrated replacement demand in developed economies raises the prospect of supply bottlenecks, favoring suppliers that have already expanded production capacity.

Utility-Led Digital-Substation Retrofit Programs (OT-IT Convergence)

Substations that once hosted isolated protection devices now operate as data hubs feeding enterprise analytics platforms. Global digital substation revenue climbed from USD 7.3 billion in 2023 to USD 8.03 billion in 2024. IEC 61850 enables plug-and-play interoperability; however, rollouts can add cybersecurity complexity, inflating project costs by up to 30% if not managed effectively. Automation vendors with embedded security expertise capture a premium because utilities cannot afford prolonged vulnerability windows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inter-operability challenges across legacy protocols | -1.2% | North America | Medium term (2-4 years) |

| High capex for rural feeder automation | -0.8% | Developing economies | Long term (≥ 4 years) |

| Cyber-security liability & compliance costs | -0.6% | Developed markets | Short term (≤ 2 years) |

| Prolonged utility procurement cycles in developing economies | -0.4% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Inter-operability Challenges Across Legacy Protocols

Utilities often operate DNP3, IEC 61850, and proprietary protocols on the same circuit, doubling system-integration spend and slowing deployments. North American grids are most affected because of the historical reliance on DNP3, which complicates migration. Compatibility gaps increase vendor lock-in and hinder the distribution feeder automation system market from reaching full competitive tendering, adding up to 20 months to average project timelines.

High Capex for Rural Feeder Automation

Low customer densities drive per-meter costs above urban benchmarks by up to 60%. Ameren Missouri’s rural modernization program required tailored radio solutions that consumed nearly half of the total project budgets. Recovering costs through rates is politically challenging, so some utilities defer rural automation until unit prices decline or external grants become available. Technology providers that offer modular, low-maintenance devices are best positioned to close the rural viability gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Communication Infrastructure Drives Connectivity Revolution

The protection relays and controllers accounted for 36.15% of the market size in 2025, while the communication infrastructure is forecast to grow at a 10.6% CAGR through 2031. Utilities are increasingly viewing bandwidth and latency as strategic levers that unlock, which allow utilities to blanket circuits without triggering major capital budget expenditures, thereby leveraging the potential of software applications. Hitachi Energy’s private LTE and mesh-radio portfolios illustrate how dedicated networks ensure deterministic performance even during massive outage events. In parallel, 5G pilots by Honeywell and Verizon validate that public networks can securely carry supervisory traffic at scale. The competitive field, therefore, spans telecom carriers, industrial-wireless specialists, and traditional automation OEMs racing to bundle connectivity with edge devices.

Despite sustained relay demand tied to mandatory protection standards, price competition and long replacement cycles cap growth. Sensors and intelligent electronic devices benefit from falling unit costs that let utilities blanket circuits without triggering major capital-budget approvals.

By Application: Software Intelligence Reshapes Hardware Dominance

Hardware retained a 66.88% distribution feeder automation system market share in 2025 because physical assets—such as reclosers, sectionalizers, and voltage regulators—remain essential. Yet, software revenue is expanding at a 9.6% CAGR, twice the pace of hardware, as utilities shift from asset count to asset intelligence. Schneider Electric’s One Digital Grid Platform claims to cut outage minutes by 40% and shorten DER interconnection reviews by 25%—metrics that regulators value when approving rate recovery. Subscription pricing converts formerly lumpy capital expenditures into predictable operating expenditures, aligning with investor expectations for stable cash flows.

Edge computing further blurs boundaries: devices now embed micro-services that filter data locally, reducing backhaul traffic by 70% in some pilots. Hardware-centric vendors thus acquire or partner with cloud developers to maintain or strengthen their market positions. Over the forecast period, utilities are expected to allocate more than one-third of new automation budgets to analytics, cybersecurity, and platform integration.

Geography Analysis

North America generated 31.75% of global revenue in 2025, driven by the USD 2.2 billion Grid Resilience and Innovation Partnerships awards, which increased automation expenditures in 18 states. Canadian provinces add momentum through aggressive wildfire-mitigation investments, while Mexico upgrades feeders to accommodate cross-border solar exports. Regulatory frameworks that permit performance-based returns encourage utilities to pilot AI diagnostics and adaptive protection logic earlier than other regions.

The Asia-Pacific represents the fastest-growing distribution feeder automation system market, advancing at a 10.1% CAGR, as China, India, and Japan collectively outspend their developed peers. China’s State Grid committed 600 billion yuan (USD 84 billion) in 2024 for ultra-high voltage and distribution intelligence, dwarfing any single-country program. India’s USD 478.58 billion power-sector pipeline, along with 1.25 trillion rupees (USD 15 billion) earmarked for smart meters, creates a sustained order volume for at least five years. Meanwhile, Japanese utilities have pledged nearly EUR 1 trillion (USD 1.1 trillion) under the Green Transformation Plan to strengthen networks supporting data center growth. Such scale advantages lower component costs globally.

Europe maintains steady adoption on the back of binding climate directives. The requirement to double annual distribution spending to EUR 67 billion secures demand even if regional economies slow. Projects such as Hitachi Energy’s collaboration with TransnetBW in Germany and its € 80 million transformer expansion in Spain underscore supplier confidence. Dynamic Line Rating pilots demonstrate that grids can gain 20-40% extra capacity without requiring new conductors, making advanced sensors an attractive option for cost-constrained regulators.

South America and the Middle East & Africa display emerging potential; however, currency risks and limited sovereign credit profiles slow large-scale rollouts. Localized manufacturing incentives in Brazil and Saudi Arabia aim to cut equipment costs by up to 25%, improving project viability.

Competitive Landscape

The distribution feeder automation system market is moderately fragmented, with ABB, Schneider Electric, and Siemens leveraging decades of installed hardware while making decisive moves into cloud software. Supplier consolidation accelerated in 2024 when 20 electrical distributors—11 from the Electrical Wholesaling Top 100—changed hands, signaling a race for channel reach and inventory control. ABB’s purchase of the Gamesa Electric power-conversion unit added 40 GW of serviceable installed base and deepened renewable integration expertise. Schneider Electric invested USD 700 million to launch its AI platform, betting that analytics will anchor long-term service contracts. Siemens aligns with EnergyHub to integrate DER management into its automation stack, targeting utilities that seek single-vendor accountability.

White-space opportunities cluster around edge-based AI and cybersecurity. Start-ups offering transformer-level vibration sensing or feeder-breaker self-healing algorithms attract utility pilots because they promise measurable reductions in outages without incurring heavy capital expenditures. Incumbents respond through venture arms and minority stakes, hedging against disruption. Asian manufacturers primarily compete on cost and local content, whereas global buyers prioritize interoperability and security certifications, which limits the risk of commoditization in the near term.

Distribution Feeder Automation System Industry Leaders

ABB Ltd.

General Electric Company

Schneider Electric SA

Siemens AG

Eaton Corporation Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Hitachi Energy has committed an additional USD 250 million to expand transformer capacity, creating over 100 new domestic manufacturing jobs.

- March 2025: Schneider Electric, following a USD 700 million investment in its U.S. operations, unveiled the One Digital Grid Platform.

- March 2025: ABB acquired Siemens' Wiring Accessories business in China, gaining access to 230 city distribution channels. This acquisition is part of ABB's strategy to expand its market reach and strengthen its presence in the smart buildings sector within China.

- March 2025: Itron introduced IntelliFLEX, a grid-edge DER management system that unlocks 20% more feeder capacity.

Global Distribution Feeder Automation System Market Report Scope

The distribution feeder automation system market report includes:

| Protection Relays and Controllers |

| Sensors and Intelligent Electronic Devices |

| Communication Infrastructure |

| SCADA/HMI Platforms |

| Software |

| Hardware |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Component | Protection Relays and Controllers | |

| Sensors and Intelligent Electronic Devices | ||

| Communication Infrastructure | ||

| SCADA/HMI Platforms | ||

| By Application | Software | |

| Hardware | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the distribution feeder automation system market?

The distribution feeder automation system market size is valued at USD 5.56 billion in 2026 and is projected to reach USD 7.92 billion by 2031.

Which region leads the market today?

North America holds the largest 31.75% revenue share, supported by extensive federal grid-resilience funding.

Which region is growing the fastest?

Asia-Pacific is forecast to rise at a 10.1% CAGR through 2031 because of massive investments by China, India, and Japan.

Which component segment is expanding most rapidly?

Communication infrastructure is growing at an 10.6% CAGR as utilities prioritize robust connectivity for real-time data exchange.

How are utilities addressing aging infrastructure?

They combine replacement programs with automation upgrades, exemplified by FirstEnergy’s USD 1.42 billion modernization plan approved in 2024.

Why is software gaining share in this industry?

AI-powered analytics and edge intelligence help utilities cut outage minutes and integrate distributed generation, driving software’s 9.6% CAGR growth trajectory.

Page last updated on: