Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 29.28 Billion |

| Market Size (2031) | USD 46.77 Billion |

| Growth Rate (2026 - 2031) | 9.82% CAGR |

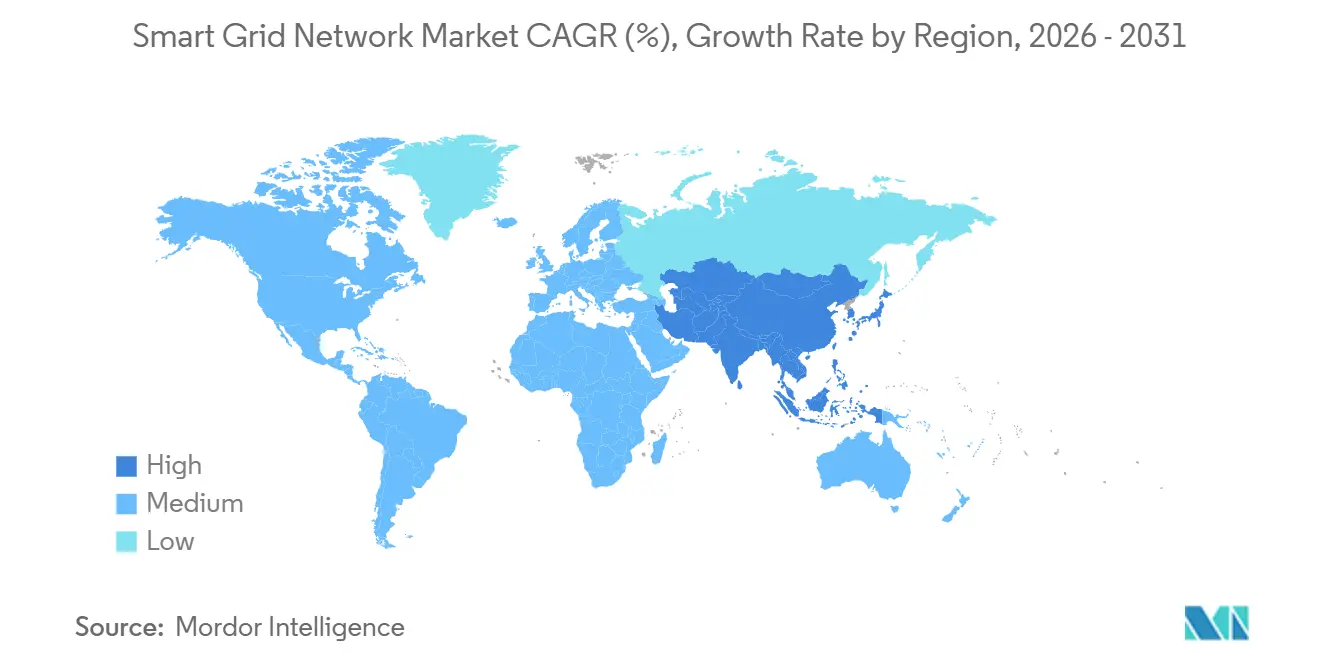

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Grid Network Market Analysis by Mordor Intelligence

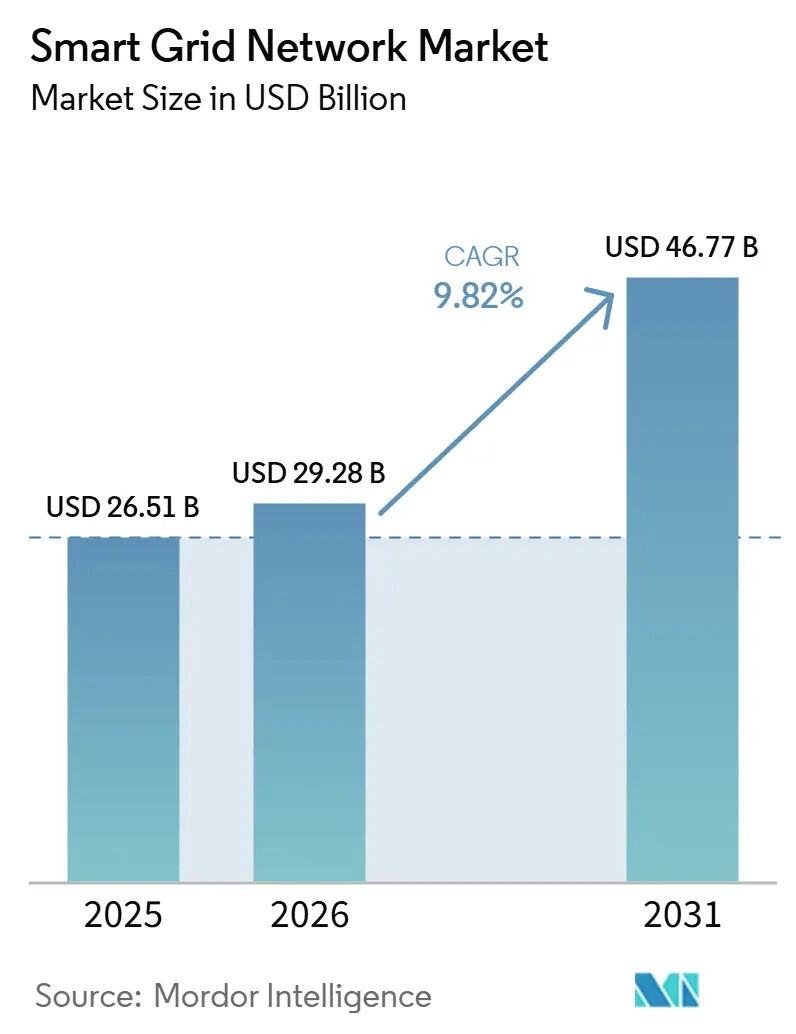

The Smart Grid Network Market size is expected to increase from USD 26.51 billion in 2025 to USD 29.28 billion in 2026 and reach USD 46.77 billion by 2031, growing at a CAGR of 9.82% over 2026-2031.

The smart grid network market is expanding because electricity systems now face heavier loads from AI data centers, electric vehicles, and more variable renewable generation, which raises the need for real-time visibility and control across networks.[1]G. He, “Renewable Integration and AI Demand Reshaped Power Grids in 2025,” Nature Reviews Clean Technology, nature.com The smart grid network market is also gaining support from direct public funding and regulator-backed modernization programs, with the U.S. Department of Energy releasing USD 1.9 billion through SPARK in 2026 and France’s energy regulator reporting EUR 1.7 billion, or USD 1.94 billion, in cumulative savings from smart grid deployments between 2017 and 2024.[2]U.S. Department of Energy, “Energy Department Announces USD 1.9B Investment in Critical Grid Infrastructure,” Energy.gov, energy.gov Competitive positioning in the smart grid network market has moved beyond metering hardware toward integrated software, grid intelligence, and cybersecurity platforms, as shown by acquisitions and product launches from Honeywell, Accenture, and utility technology vendors during 2025 and 2026.[3]Honeywell, “Honeywell Acquires SparkMeter’s Data Platform and Software Technologies to Strengthen Its Portfolio of Utility Solutions,” Honeywell, honeywell.com The strongest opportunities in the smart grid network market sit where advanced metering, distribution automation, wireless field networks, and software analytics are deployed together rather than as isolated projects.[4]Ericsson, “Drivers of Mission-Critical Mobile Networks for Utilities,” Ericsson, ericsson.com The main limits on the smart grid network market remain high upfront spending, vendor integration gaps, and the execution burden of connecting legacy systems with newer digital platforms.

Key Report Takeaways

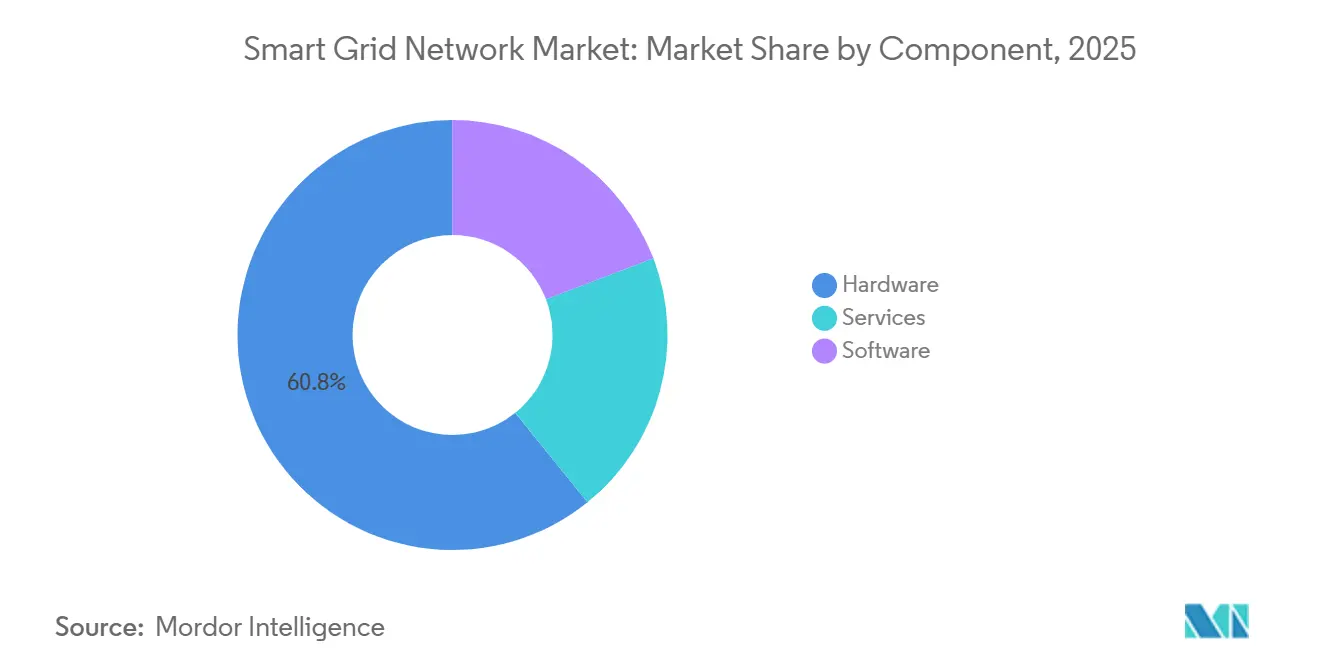

- By component, hardware held 60.8% of the smart grid network market share in 2025, while software is forecast to expand at 13.5% CAGR through 2031.

- By grid stage, distribution accounted for 48.0% of revenue in 2025, while the consumption and prosumer segment is projected to grow at 12.6% CAGR through 2031.

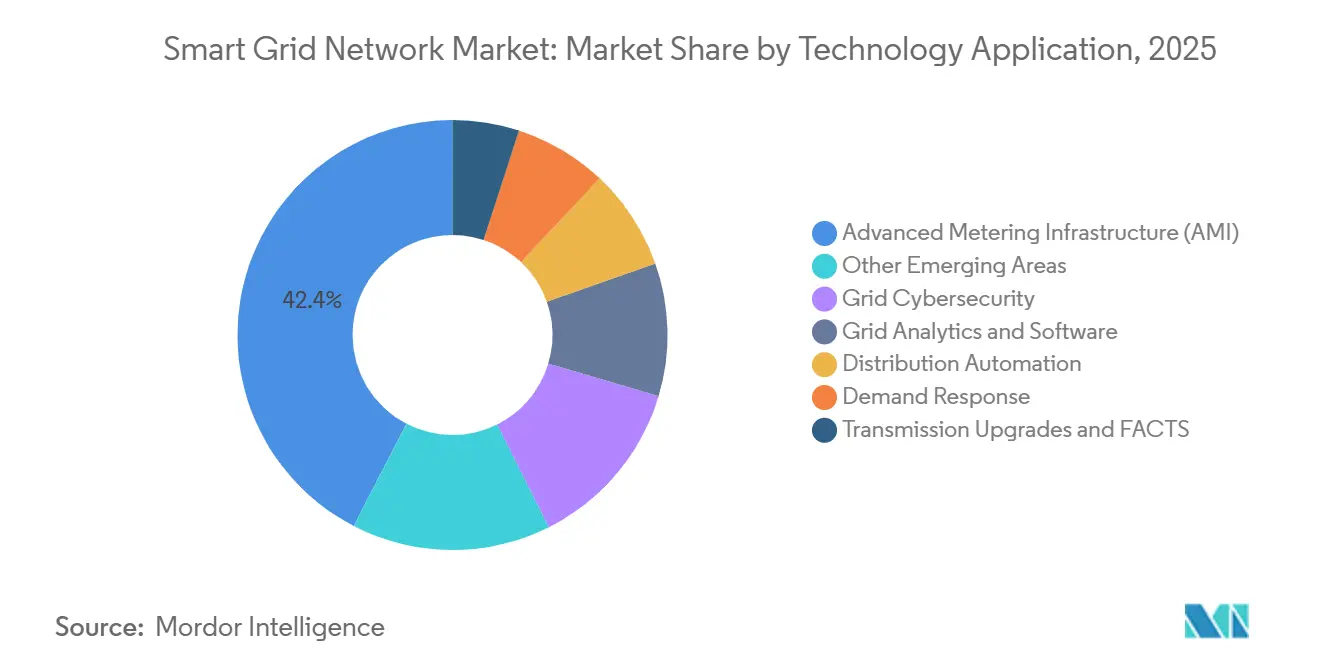

- By technology application area, Advanced Metering Infrastructure accounted for 42.4% of the smart grid network market size in 2025, while other emerging application areas are forecast to advance at 14.3% CAGR through 2031.

- By communication technology, wired systems led with 55.1% share in 2025, while wireless systems are projected to grow at 13.1% CAGR through 2031.

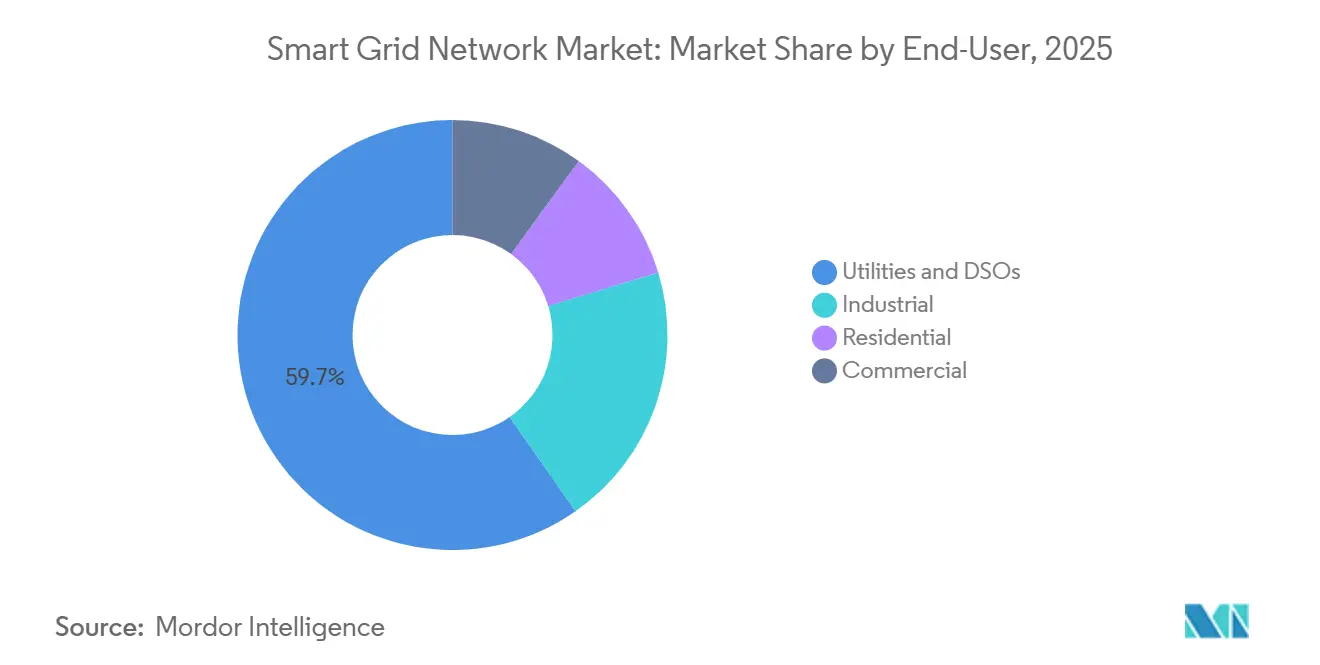

- By end user, utilities and Distribution System Operators (DSOs) represented 59.7% of revenue in 2025, while industrial users are forecast to expand at 12.2% CAGR through 2031.

- By geography, North America held 35.5% of the smart grid network market share in 2025, while Asia-Pacific is expected to grow at 14.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Smart Grid Network Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-Funded Grid Digitization Mandates | +2.5% | Global, led by North America, Asia-Pacific, Europe | Medium term (2-4 years) |

| Rapid Advanced Metering Infrastructure (AMI) Rollouts for Demand-Side Management | +1.5% | Global, concentrated in Asia-Pacific, North America | Short term (≤ 2 years) |

| Renewable and Distributed Energy Resources (DER) Integration Pressure | +1.8% | Global, most acute in Europe, Asia-Pacific (APAC) core, spillover to South America | Medium term (2-4 years) |

| AI-Based Predictive Maintenance Adoption | +1.0% | North America and Europe, early adoption in APAC | Medium term (2-4 years) |

| 5G and Low Power Wide Area (LPWA) Connectivity Enabling Edge Intelligence | +0.7% | Asia-Pacific, North America, spillover to Middle East & Africa (MEA) | Long term (≥ 4 years) |

| Blockchain-Enabled Transactive Energy Platforms | +0.3% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-Funded Grid Digitization Mandates

Government-backed grid spending has moved from policy signaling into direct procurement support, which shortens utility decision cycles in the smart grid network market. In March 2026, the U.S. Department of Energy announced the USD 1.9 billion Spark Initiative funding opportunity under the Grid Resilience and Innovation Partnerships (GRIP) program, including USD 614 million for smart grid deployments and USD 862 million for grid innovation. In Europe, the business case for digital grid upgrades is stronger because France’s regulator reported EUR 1.7 billion in cumulative savings from smart grid deployments between 2017 and 2024. Germany also showed the scale of commitment required, as TenneT Germany invested EUR 10.047 billion, or USD 11.1 billion, in 2025 to expand and modernize power infrastructure. These programs lift demand in the smart grid network market because utilities can commit to long-cycle automation, communications, and software projects with more confidence. They also push utilities toward interoperable digital systems, since public funding programs increasingly favor platforms that can connect substations, field devices, and customer-side assets across the full network.

Renewable & Distributed Energy Resources (DER) Integration Pressure

The generation mix is changing fast, and that raises control requirements across the smart grid network market because utilities must manage more variable and bidirectional power flows. Global renewable electricity generation exceeded coal-fired generation for the first time in 2025, which marked a major shift in how grids must balance supply and demand. In Germany, TenneT Germany raised investment to EUR 10.047 billion, or USD 11.1 billion, in 2025 to support offshore wind integration and major transmission corridors, showing how renewable buildout now drives core network spending. The pressure is now strongest at the distribution edge, where rooftop solar, EV charging, storage, and smart inverters turn customers into active grid participants rather than passive loads. That shift increases the value of advanced metering, DER management, and demand response in the smart grid network market because operators need more granular data and faster control loops. It also makes curtailment, local voltage management, and flexible load orchestration practical priorities rather than secondary planning topics.

AI-Based Predictive Maintenance Adoption

Utilities are moving from scheduled maintenance toward condition-based and AI-assisted asset management, and that is creating a clear growth path in the smart grid network market. In June 2026, San Diego Gas and Electric, Qualcomm Technologies, and UC San Diego launched the Edge Alert Sentinel initiative to apply edge AI for wildfire and extreme-weather response directly on grid infrastructure. In June 2025, Indiana Municipal Power Agency selected Tantalus’ TRUGrid analytics platform to improve fault identification, transformer performance, and capital prioritization across member utilities. These moves matter for the smart grid network market because predictive maintenance depends on continuous field data, reliable communications, and software that can turn events into operational actions. Utilities also value these tools because they help manage outage risk, asset stress, and field response with less manual review across stretched workforces. As these deployments scale, the value pool in the smart grid network market shifts further toward analytics, event management, and software-led resilience services.

5G/ Low-Power Wide-Area (LPWA) Connectivity Enabling Edge Intelligence

Wireless communications are becoming more important in the smart grid network market because utilities need low-latency, scalable links across wide and uneven service territories. Ericsson noted that utility mission-critical mobile networks can use 5G network slicing to support time-sensitive grid control, metering backhaul, and workforce communications on one managed infrastructure. Nokia also reported that private Long-Term Evolution (LTE) and 5G systems can replace several legacy communications layers while supporting higher-bandwidth field applications such as inspection video and real-time protection signaling. This matters because the smart grid network market increasingly depends on hybrid architectures, where fiber carries high-priority traffic and wireless systems extend visibility and automation to the field edge. Wireless growth is strongest where utilities need cost-effective automation in low-density or difficult terrain, and where fiber running to every endpoint is not practical. As more intelligence moves to field devices, secure wireless connectivity becomes part of the operating backbone rather than an optional add-on in the smart grid network market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CapEx Requirements | -2.8% | Global, most acute in South America and MEA | Long term (≥ 4 years) |

| Protocol and System Interoperability Gaps | -1.6% | Global, acute in multi-vendor brownfield environments | Medium term (2-4 years) |

| Shortage of Cyber-Physical Talent | -1.2% | North America and Europe, most acute in mature markets | Medium term (2-4 years) |

| Geopolitical Supply-Chain Restrictions | -1.0% | Global, concentrated in semiconductor and hardware supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High CapEx Requirements

High capital intensity remains one of the clearest limits on the smart grid network market because utilities must fund hardware, communications, software, and systems integration at the same time. TenneT Germany invested EUR 10.047 billion, or USD 11.1 billion, in 2025 alone, which shows the scale required even in mature and well-funded grid systems. The Department of Energy's (DOE's) SPARK funding round also shows that public support is often needed to accelerate projects that would otherwise move more slowly through utility capital plans. In the smart grid network market, this spending burden is heavier for mid-tier utilities because they often face narrower financing options and slower cost recovery. The result is that many operators can justify grid digitization strategically but still phase projects more slowly than system needs would suggest. That constraint is strongest in markets where regulatory support, rate recovery, or local manufacturing depth are still catching up with modernization targets.

Protocol & System Interoperability Gaps

Interoperability problems continue to slow the smart grid network market because utilities rarely replace entire networks at once and must connect new digital layers to old equipment. Electro-Federation Canada’s 2026 survey work showed that high upfront costs remained the top adoption barrier for many vendors, with interoperability continuing to complicate procurement, deployment, and vendor lock-in decisions. In the smart grid network market, these issues often appear late in projects, when engineering teams begin testing multi-vendor devices, communication standards, and system interfaces across brownfield environments. That means the extra cost is not always visible during procurement, even though it can extend commissioning and weaken return timelines once projects move into deployment. The problem is deeper in systems shaped by years of utility-specific specifications and single-vendor architectures, because those legacy choices do not align well with newer open, data-rich network models. As a result, the smart grid network market can grow quickly in funded programs while still losing speed at the project execution stage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Holds Volume; Software Reshapes the Value Chain

Hardware accounted for 60.8% of revenue in 2025, which reflects the physical scale of meter deployment, feeder automation, relays, and substation equipment across the smart grid network market. That position remains strong because utilities still need large installed bases of field devices before they can unlock the full value of software-led orchestration and analytics. Smart meters, automation devices, and protection systems continue to absorb a large share of capital budgets because many utilities are replacing first-generation installations or extending automation into new parts of their networks. This keeps hardware central to the smart grid network market even as competitive value moves further into software layers. Hardware demand also remains tied to the practical need for dependable sensing and communications across transmission, distribution, and customer endpoints.

Software is forecast to grow at 13.5% CAGR through 2031, which makes it the fastest-growing component in the smart grid network market. That growth reflects rising demand for Advanced Distribution Management System (ADMS), Distributed Energy Resource Management System (DERMS), outage analytics, and other platforms that help utilities turn field data into operating decisions across more dynamic grid conditions. The shift is visible in vendor strategy, because Honeywell expanded its utility portfolio in August 2025 by acquiring SparkMeter’s Praxis, GridScan, and GridFin software assets. The hardware side is also facing price pressure, with Chinese manufacturers holding a 30%-to-40%-unit cost advantage in smart meters through vertical integration, which raises the need for margin protection through software and services. Services support both segments in the smart grid network market because utilities increasingly need integration, cybersecurity operations, and managed support to connect OT and IT systems at scale.

By Grid Stage: Distribution Commands Investment; Prosumer Layer Redefines the Grid Edge

Distribution held 48.0% of revenue in 2025, which shows where utilities still concentrate the largest share of practical modernization spending in the smart grid network market. That allocation reflects the operational reality that outages, losses, and customer-facing reliability issues are often most visible on distribution networks rather than on generation or long-distance transmission assets. Feeder automation, outage management, Advanced Metering Infrastructure (AMI), and voltage control therefore remain central purchase areas in the smart grid network market. Distribution also serves as the connection point where utility systems meet prosumer assets, commercial loads, and new electrified demand from transport and digital infrastructure. This gives it a structural role that is likely to remain larger than other grid stages over the forecast period.

The consumption and prosumer segment is forecast to grow at 12.6% CAGR through 2031, making it the fastest-moving grid stage in the smart grid network market. The reason is clear: rooftop solar, EV chargers, residential batteries, and smart inverters are increasing the volume of two-way flows and local decision points that utilities must monitor and control. In markets with high distributed energy adoption, these customer-side assets are becoming useful grid sensors as well as sources of demand flexibility. Transmission modernization still matters, and TenneT Germany’s 2025 investment program shows how renewable integration can lift backbone network spending at the same time. Even so, the most dynamic part of the smart grid network market now sits at the grid edge, where customer behavior, DER participation, and localized control requirements are changing the operating model of utilities.

By Technology Application Area: AMI Anchors Revenue; Emerging Areas Lead the Next Wave

Advanced Metering Infrastructure accounted for 42.4% of application revenue in 2025, which gave AMI the largest role in the smart grid network market size across technology application areas. This leadership is structural because AMI provides the continuous, high-resolution data needed for billing, outage visibility, demand response, asset planning, and customer-side flexibility programs. Without AMI-scale data collection, many downstream applications in the smart grid network market would operate with less granularity and lower response quality. AMI therefore remains more than a standalone segment, since it acts as the base data layer for several higher-value control and analytics functions. It also supports utility expansion into multi-utility digital metering models, which broadens the addressable use case over time.

Other emerging technology application areas are forecast to grow at 14.3% CAGR through 2031, which makes them the fastest-rising application cluster in the smart grid network market. This group includes Vehicle-to-Grid (V2G) communication, real-time carbon accounting, AI-led analytics, digital twins, and newer grid-edge coordination tools that build on the data layer created by AMI. Cybersecurity is becoming part of this next wave, and Accenture’s June 2026 move to build an end-to-end OT security platform through Dragos, runZero, and NetRise shows that vendors see grid security as a primary buying category rather than a side feature. In the smart grid network market, these emerging areas attract spending because utilities need tools that can coordinate distributed assets, monitor cyber risk, and support more adaptive network operations. Over time, application-level growth is likely to become a bigger source of differentiation than basic hardware deployment alone.

By Communication Technology: Wired Backbones Hold Ground; Wireless Narrows the Gap

Wired systems held 55.1% of communication technology revenue in 2025, which keeps them in the lead across the smart grid network market. Fiber and power line communication remain important because utilities still prefer highly reliable and low-latency links for protection-grade traffic, digital substations, and high-voltage applications. This gives wired infrastructure a durable role even as utilities push more intelligence toward the field edge. In the smart grid network market, wired systems still set the backbone for mission-critical control and time-sensitive data flows. They also provide the stable core that allows utilities to combine security, performance, and deterministic communication where response tolerance is low.

Wireless communication is projected to grow at 13.1% CAGR through 2031, which makes it the faster-moving side of the smart grid network market size within communications. Ericsson has shown that utilities can use 5G network slicing to run time-critical control, metering backhaul, and workforce communication on one infrastructure, which improves scalability and network management. Nokia also found that a managed LTE or 5G private wireless network can replace multiple legacy communication layers while supporting richer field applications. Hybrid designs are therefore gaining ground in the smart grid network market because they combine wired backhaul with cost-effective wireless field coverage across difficult or uneven service territories. As utilities automate more field devices, communication strategy becomes a larger part of product selection, cybersecurity planning, and long-term operating cost control.

By End User: Utilities Lead; Industrial Segment Accelerates

Utilities and DSOs accounted for 59.7% of revenue in 2025, which makes them the largest end-user group in the smart grid network market. Their leading role reflects control over the core infrastructure budget for AMI, substation automation, Supervisory Control and Data Acquisition (SCADA) upgrades, communications, and software platforms used across network operations. Utilities also act as the main organizers of standards, system integration, and long-cycle capital planning, which keeps their share high even as other users become more active. Residential participation in the smart grid network market remains linked mainly to utility-led smart metering, home energy coordination, and demand response enablement. Commercial users are becoming more relevant as data centers and other power-sensitive facilities seek better load visibility and more dynamic power arrangements.

The industrial segment is projected to grow at 12.2% CAGR through 2031, which makes it the fastest-expanding end-user segment in the smart grid network market. Energy-intensive sites are adopting demand response, on-site renewable generation, storage, and microgrid controls to improve cost visibility and power quality, which turns them into more active grid participants. India’s Central Electricity Authority has targeted 100 million smart meter installations by FY27 and 350 million by 2035, with smart metering linked to broader efficiency and demand management goals. In the smart grid network industry, this shift matters because industrial sites are no longer just loads, they can also offer flexibility, localized generation, and data-rich operating signals. That broadens the customer base of the smart grid network market beyond utilities and supports more direct sales of analytics, DER management, and control platforms to enterprise users.

Geography Analysis

North America held 35.5% of revenue in 2025, which gave it the largest regional position in the smart grid network market. The region benefits from a large installed smart meter base, ongoing second-wave AMI replacement, and a broad utility focus on feeder automation and digital control. The U.S. Department of Energy strengthened that demand path in March 2026 by releasing USD 1.9 billion under SPARK, including USD 614 million for smart grid deployments and USD 862 million for grid innovation. Europe follows a different path in the smart grid network market, with strong decarbonization pressure but tighter capital discipline around how fast operators can build. France’s regulator reported EUR 1.7 billion in cumulative smart grid savings between 2017 and 2024, while TenneT Germany invested EUR 10.047 billion, or USD 11.1 billion, in 2025, which shows that digital and transmission upgrades are both moving into core utility spending plans.

Asia-Pacific is forecast to expand at 14.8% CAGR through 2031, making it the fastest-growing region in the smart grid network market size. The region combines large network expansion programs with faster rollout architectures, which supports both basic electrification upgrades and newer digital grid layers. India’s transmission and distribution investment reached USD 26 billion in 2026 after growing at 15% annually over the prior five years, and the country is pushing large smart meter targets that support broader grid digitization. China remains the other major volume engine in the smart grid network market because state-backed infrastructure planning continues to support renewable integration and digital network investment. Across the region, utilities are moving quickly toward fiber-to-the-meter, wireless field-area networks, and software-enabled control, which helps Asia-Pacific compress modernization timelines relative to more incremental replacement cycles elsewhere.

South America remains a high-potential but underpenetrated part of the smart grid network market, where modernization needs are clear but rollout speed is uneven. Mexico has announced 163,540 million pesos, or USD 9.5 billion, in transmission modernization projects under its 2025 to 2030 strategic plan, while Brazil’s CEMIG partnered with Huawei on a private 450 MHz Long-Term Evolution (LTE) network to improve grid automation over challenging terrain. In the Middle East and Africa, digital grid investment is tied more closely to energy diversification, remote operations, and leapfrog deployment models than to replacement of dense legacy communication networks. That creates room in the smart grid network market for wireless automation, intelligent substations, and remote monitoring solutions where conventional wireline expansion would take longer or cost more.

Competitive Landscape

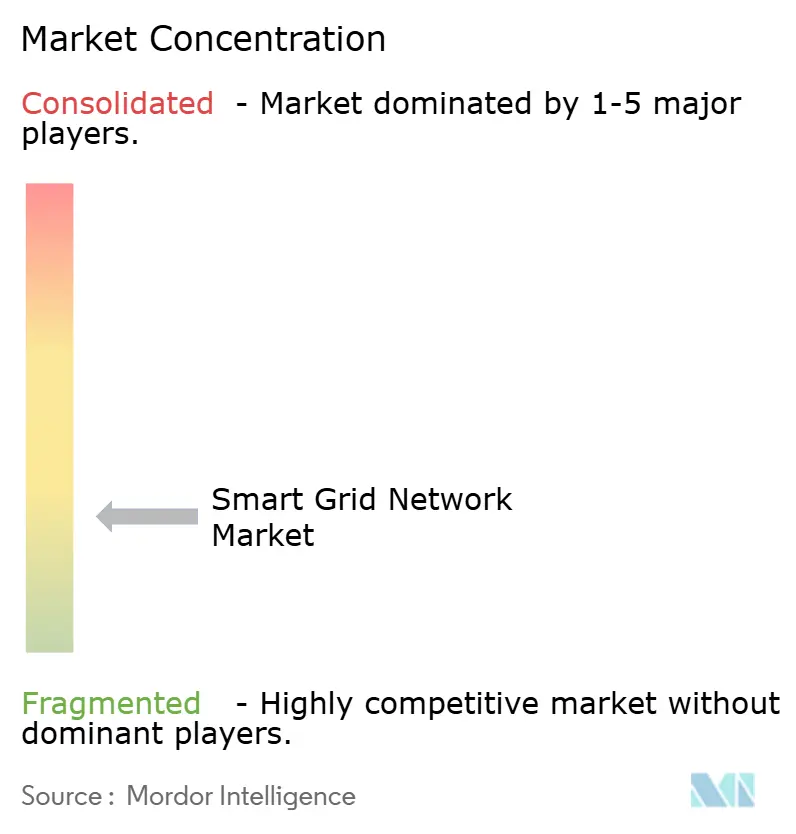

The smart grid network market remains fragmented, with the top 10 vendors accounting for 36% of total revenue in 2025. This structure shows that scale still matters, but it also leaves room for specialized software, communications, and cybersecurity providers to win share through focused capabilities rather than pure breadth. In the smart grid network market, leadership is shifting away from standalone hardware supply and toward integrated operating platforms that combine data capture, control, analytics, and security in one utility workflow. That is why vendor competition now centers more on system architecture, recurring software value, and operational outcomes than on device shipment volume alone. It also explains why partnerships, acquisitions, and portfolio restructuring became more visible across 2025 and 2026.

Honeywell’s August 2025 acquisition of SparkMeter’s Praxis, GridScan, and GridFin assets shows how established industrial vendors are building stronger positions in utility analytics, distribution monitoring, and financial performance management. Accenture’s June 2026 move to acquire a majority stake in Dragos, alongside the full acquisitions of runZero and NetRise, shows the same trend from the services and cybersecurity side. In the smart grid network market, these moves matter because utilities increasingly want fewer vendors to manage wider sets of operational, cyber, and data responsibilities. The result is that competition is tightening around platform depth and the ability to connect Operational Technology (OT) and IT environments without adding more integration risk.

New opportunity spaces are still opening inside the smart grid network market, especially around grid-edge AI, prosumer orchestration, and secure digital energy transactions. A framework published in Energy Informatics showed that blockchain-enabled collaborative power management increased transaction volume by 30% and reduced transaction costs by 1.5% against bilateral trading, which shows why peer-to-peer and transactive energy models continue to attract interest. The smart grid network market also rewards vendors that can combine device data, communications, and automation into field-ready workflows, as shown by Tantalus’s utility analytics deployment and San Diego Gas & Electric's (SDG&E's) edge AI initiative. Even with moderate concentration, the smart grid network market still leaves meaningful space for companies that solve one hard utility problem well and then expand from that foothold.

Smart Grid Network Industry Leaders

ABB Ltd

Schneider Electric SE

Siemens AG

General Electric Company

Itron Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Accenture announced acquiring a majority stake in Dragos, along with full acquisitions of runZero and NetRise. This integrates its USD 10 billion cybersecurity business with Dragos's OT security platform, creating a critical infrastructure security solution. Targeting power grid operators, the move positions Accenture as a key competitor in utility IT/OT security convergence.

- June 2026: San Diego Gas & Electric, Qualcomm Technologies, and UC San Diego launched the Edge Alert Sentinel (EAS) collaboration, using edge AI on the Qualcomm Dragonwing IQ9 processor at Mt. Palomar to forecast wildfire and extreme-weather grid impacts in real time. Expansion to additional sites is planned from 2027.

Global Smart Grid Network Market Report Scope

The global smart grid network market is dedicated to revolutionizing traditional electricity grids. By harnessing advanced digital technologies, these grids now facilitate two-way communication, real-time monitoring, and intelligent control over power generation, transmission, distribution, and consumption. Integrating components like advanced metering infrastructure (AMI), sensors, communication networks, data analytics, automation systems, and grid management software, smart grid networks enhance the efficiency, reliability, and resilience of power systems.

The global smart grid network market is segmented by component, grid stage, technology application, communication technology, end-user, and geography. By component, the market is segmented by hardware, software, and services. By grid stage, the market is divided into generation, transmission, distribution and consumption/prosumer. By technology application, the market is segmented into AMI, distribution automation, transmission upgrades and FACTS, demand response, grid cybersecurity, grid analytics and software and other emerging areas. By communication technology, the market is segmented into wired, wireless, and hybrid architectures. By end-user, the market is segmented into residential, commercial, industrial, and utilities & DSOs. The report also covers the market size and forecasts for the subsea systems market across major regions. Market sizing and forecasts have been done for each segment based on revenue (USD billion).

By Component

| Hardware |

| Software |

| Services |

By Grid Stage

| Generation |

| Transmission |

| Distribution |

| Consumption/Prosumer |

By Technology Application Area

| Advanced Metering Infrastructure (AMI) |

| Distribution Automation |

| Transmission Upgrades and FACTS |

| Demand Response |

| Grid Cybersecurity |

| Grid Analytics and Software |

| Other Emerging Areas |

By Communication Technology

| Wired (Fiber, PLC) |

| Wireless (RF Mesh, Cellular IoT, 5G, LPWA) |

| Hybrid Architectures |

By End User

| Residential |

| Commercial |

| Industrial |

| Utilities and DSOs |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Grid Stage | Generation | |

| Transmission | ||

| Distribution | ||

| Consumption/Prosumer | ||

| By Technology Application Area | Advanced Metering Infrastructure (AMI) | |

| Distribution Automation | ||

| Transmission Upgrades and FACTS | ||

| Demand Response | ||

| Grid Cybersecurity | ||

| Grid Analytics and Software | ||

| Other Emerging Areas | ||

| By Communication Technology | Wired (Fiber, PLC) | |

| Wireless (RF Mesh, Cellular IoT, 5G, LPWA) | ||

| Hybrid Architectures | ||

| By End User | Residential | |

| Commercial | ||

| Industrial | ||

| Utilities and DSOs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the smart grid network market in 2026?

The market stands at USD 29.28 billion in 2026 and is projected to reach USD 46.77 billion by 2031.

Which segment is growing fastest by grid stage?

Spending tied to consumption and prosumer assets is rising at a 12.6% CAGR as rooftop solar, batteries, and EV chargers scale.

What drives rapid wireless adoption in utility grids?

Cheaper 5G, NB-IoT, and LPWA modules cut last-mile connectivity costs and deliver sub-10-millisecond latency for protection schemes.

Why are industrial customers investing in smart-grid solutions?

Manufacturers and data centers use microgrids and demand response to lower peak charges and earn ancillary-service revenue, pushing 12.2% annual growth.

How are utilities addressing cybersecurity risk?

Spending on intrusion detection, network segmentation, and compliance monitoring now claims 8-12% of IT budgets as NIS2 and NERC CIP standards tighten.

Which regions provide the strongest growth outlook?

Asia-Pacific leads with a 14.8% CAGR through 2031, driven by large-scale investment programs and faster deployment models.

Page last updated on: