Tendonitis Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

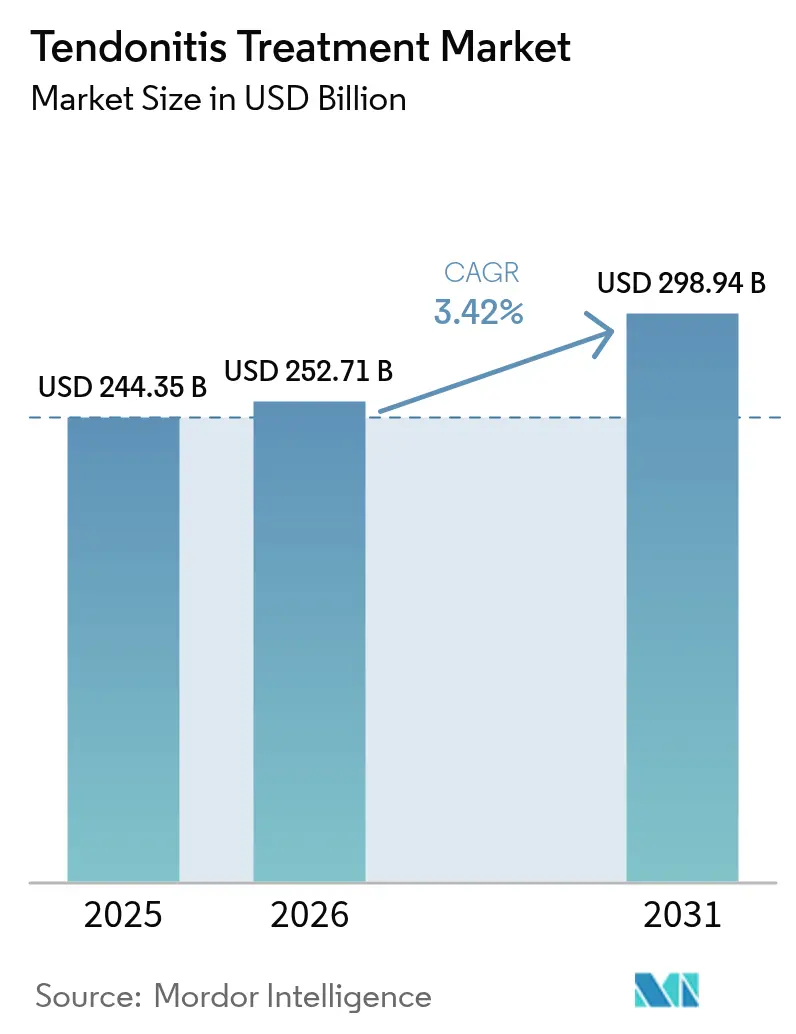

| Market Size (2026) | USD 252.71 Billion |

| Market Size (2031) | USD 298.94 Billion |

| Growth Rate (2026 - 2031) | 3.42% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tendonitis Treatment Market Analysis by Mordor Intelligence

The tendonitis treatment market size is expected to grow from USD 244.35 billion in 2025 to USD 252.71 billion in 2026 and is forecast to reach USD 298.94 billion by 2031 at 3.42% CAGR over 2026-2031. The growth reflects a rise in sports‐related injuries, persistent workplace ergonomics issues, and wider access to AI-enabled imaging that catches tendon damage earlier than legacy modalities. Military-grade biomaterials are also crossing into civilian orthopedics, enhancing healing outcomes and stimulating premium product adoption. On the regional front, North America continues to command spending power, yet Asia-Pacific is outpacing the global average thanks to rapid hospital build-outs and widespread uptake of digital rehabilitation platforms. Across conditions, Achilles injuries remain numerically dominant while patellar tendinopathy leads future volume gains as ultrasound guidance improves diagnostic accuracy. Non-surgical care[1]Corporate Communications, “Johnson & Johnson MedTech Announces Strategic Agreement with Responsive Arthroscopy to Expand Sports Soft Tissue Solutions,” Johnson & Johnson MedTech, jnjmedtech.com now anchors treatment decisions, supported by validated regenerative and photobiomodulation options that shorten recovery, keep athletes on the field, and lower payer costs.

Key Report Takeaways

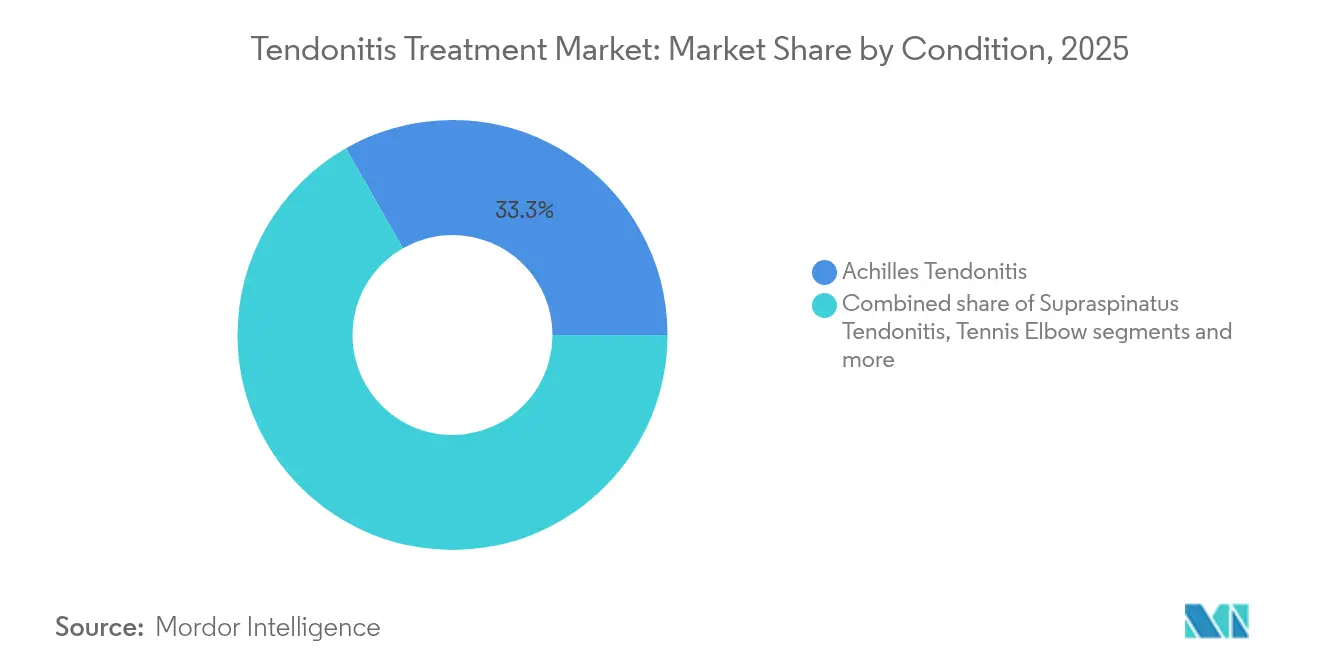

- By condition, Achilles tendonitis captured 33.25% of the tendonitis treatment market share in 2025, while patellar tendinopathy is projected to grow at a 4.78% CAGR through 2031.

- By treatment modality, non-surgical care held 61.48% of the tendonitis treatment market in 2025; surgical alternatives trail but advanced at a 3.75% CAGR through 2031.

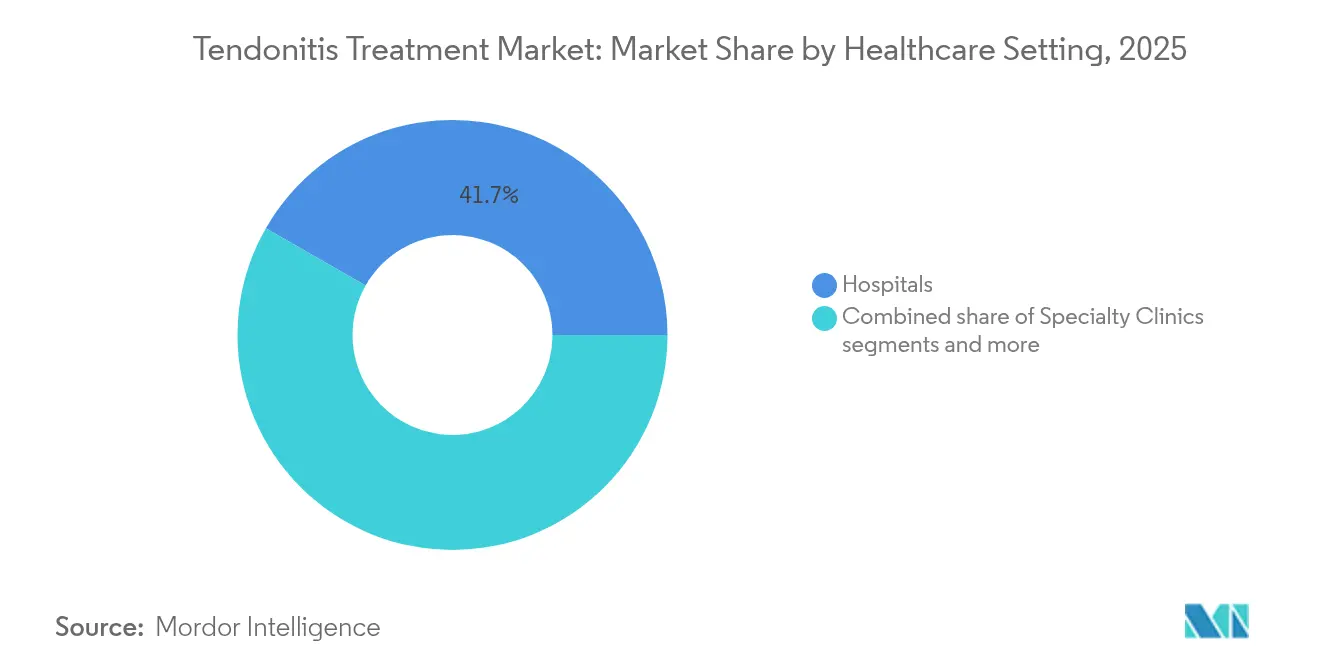

- By healthcare setting, hospitals accounted for 41.74% share of the tendonitis treatment market size in 2025, whereas rehabilitation centers are expanding at a 4.18% CAGR between 2026-2031.

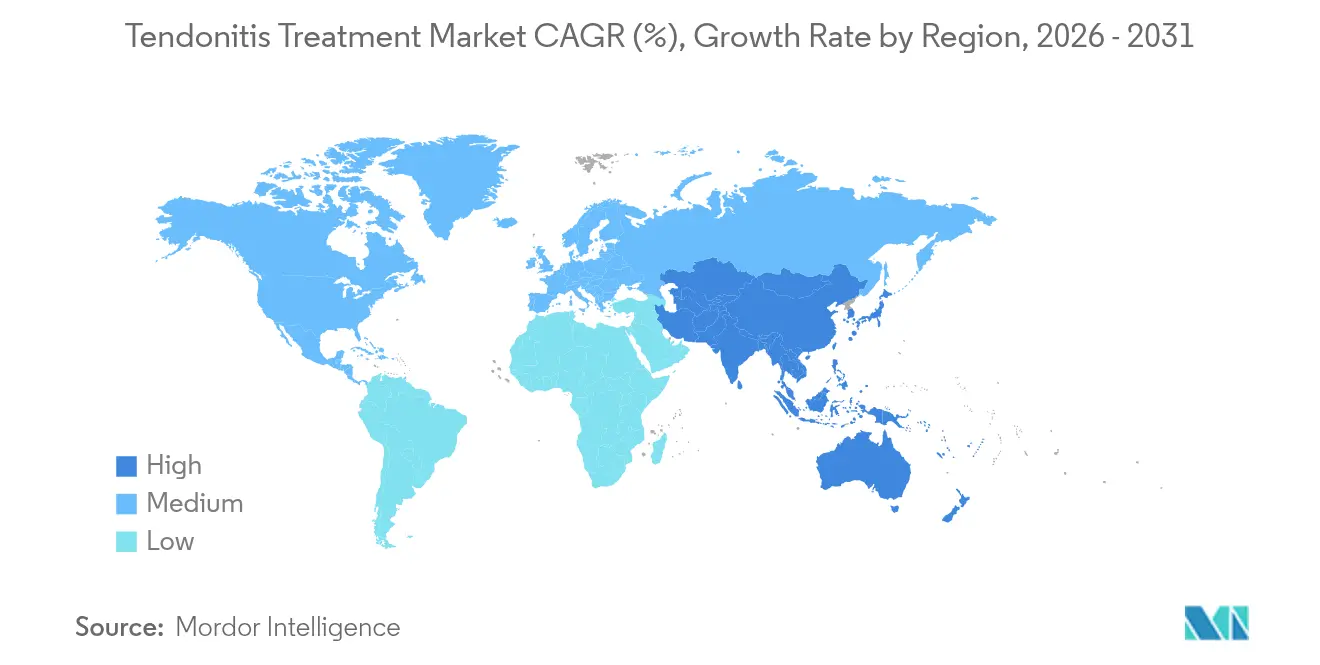

- By geography, North America led with 38.17% revenue share in 2025; Asia-Pacific is forecast to post the highest regional CAGR at 4.28% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tendonitis Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sports & occupational injury incidence boom | +0.8% | Global; most acute in North America & Europe | Medium term (2-4 years) |

| AI-powered ultrasound enabling early diagnosis | +0.6% | North America & Asia-Pacific core; spill-over to EU | Short term (≤ 2 years) |

| Reimbursement expansion for outpatient repair | +0.5% | North America & EU; select Asia-Pacific markets | Medium term (2-4 years) |

| Military-grade biomaterials in civilian care | +0.4% | North America; scaling to Asia-Pacific | Long term (≥ 4 years) |

| Direct-to-Consumer Tele-Physiotherapy Platforms | +0.4% | Global, with APAC showing highest adoption | Short term (≤ 2 years) |

| Wearable Neuromodulation for Pain-Free Rehab | +0.3% | Global, led by North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sports & Occupational Injury Incidence Boom

Rising participation in organized sports among adults over 40 and worsening desk-bound work habits inflate global tendon injury risk. Musculoskeletal diseases now affect 1.7 billion people, and tendon problems account for up to 40% of game-related incidents. Corporate wellness programs have begun treating tendon health as a productivity metric, incentivizing earlier intervention. As a result, providers are extending clinic hours, payers are adding preventive coverage, and device firms are launching pre-emptive bracing products tailored for older weekend athletes.

AI-Powered Ultrasound Enabling Early Diagnosis

Machine-learning image analysis identifies micro-tears long before they trigger overt symptoms, boosting conservative cure rates above 80% for early-stage cases. Hospitals in the United States and Japan have added portable AI scanners to standard sport-medicine workups, reducing unnecessary MRI referrals and lowering per-episode costs. Vendors are embedding predictive algorithms into cloud dashboards that notify therapists when image patterns suggest pre-rupture stress, reinforcing proactive care models.

Reimbursement Expansion for Outpatient Tendon Repair

Commercial insurers now reimburse minimally invasive bioinductive implantation in outpatient suites, citing Smith+Nephew's economic analysis[2]Marketing Team, “REGENETEN Bioinductive Implant: Disease Progression and Economic Evidence,” Smith+Nephew, smith-nephew.com that linked the approach to faster return-to-work and lower mid-term re-tear rates. This policy shift lifts patient throughput in ambulatory surgery centers and encourages surgeons to adopt regenerative implants earlier in the care pathway.

Military-Grade Biomaterials Entering Civilian Care

Materials first deployed for battlefield injuries demonstrate superior load-bearing strength[3]Leilei Qin, “Prospects and challenges for the application of tissue engineering technologies in the treatment of bone infections,” Bone Research, nature.com and biocompatibility in chronic tendon tears, yielding near-complete functional restoration in early civilian case series. Government dual-use grants accelerate regulatory submissions, and orthopedic firms are co-branding next-generation grafts with defense labs to highlight durability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low clinician awareness of biologic options | −0.4% | Global; most pronounced in emerging markets | Medium term (2-4 years) |

| High failure rates of first-line conservative therapy | −0.3% | Global; variation by local protocol | Short term (≤ 2 years) |

| Supply-Chain Bottlenecks for Medical-Grade Collagen Grafts | -0.2% | Global, with acute impact in North America & Europe | Medium term (2-4 years) |

| Limited Long-Term Data on Emerging Energy-Based Devices | -0.1% | North America & Europe, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Low Clinician Awareness of Biologic/Regenerative Options

A 2024 survey showed only 66.1% of sports physicians offered at least one orthobiologic, citing limited training and inconsistent reimbursement. In low-resource settings, physicians rely on legacy anti-inflammatory regimens, delaying uptake of platelet-rich plasma or stem-cell injections. Device sponsors are funding fellowship programs and open-access outcome registries to close knowledge gaps.

High Failure Rates of First-Line Conservative Therapy

Systematic reviews reveal[4]Haleigh M Hopper, “Decreased Strength, Complication Rate and Higher Satisfaction in Conservative Treatment of Partial Distal Biceps Tendon Rupture Compared to Surgical Treatment: A Systematic Review,” Orthopedic Reviews, orthopedicreviews.openmedicalpublishing.org that standard rest-and-brace protocols underperform in chronic distal biceps tears, forcing many patients toward surgery after months of deterioration. The added cost and frustration erode confidence in conservative care and drive demand for improved initial modalities such as photobiomodulation or high-energy shockwave.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Condition: Achilles Dominance Masks Patellar Surge

Achilles tendonitis held a 33.25% tendonitis treatment market share in 2025, reflecting its high prevalence among runners, basketball players, and occupations that demand prolonged standing. Patellar tendinopathy is advancing at a 4.78% CAGR, outpacing overall tendonitis treatment market growth as volleyball, soccer, and pickleball gain popularity worldwide. Supraspinatus tears maintain steady volumes due to aging demographics and repetitive overhead activity, while tennis elbow benefits from renewed recreational sports uptake among middle-aged consumers. De Quervain’s tenosynovitis growth links to the widespread use of smartphones that encourage repetitive thumb extension.

Ultrasound-guided interventions now underpin many condition-specific pathways. Percutaneous needle tenotomy systems such as Tenex deliver significant functional gains for lateral epicondylitis, documented in short- and long-term follow-up cohorts. Bioinductive collagen implants accelerate mid-foot and lower-limb tendon healing, helping athletes resume play sooner. These advances suggest precision protocols will differentiate providers and spur premium pricing.

By Treatment: Non-Surgical Supremacy Reinforced

Non-surgical options commanded 61.48% of the tendonitis treatment market size in 2025 and are expanding at 3.75% CAGR as patients favor less invasive therapy. Wearable neuromodulation and photobiomodulation are entering mainstream guidelines after meta-analyses confirmed pain score reductions and faster functional recovery. Surgical demand persists for full-thickness tears, yet minimally invasive procedures—arthroscopy or percutaneous repair—are displacing open surgery because of shorter rehabilitation and lower infection risk.

Grafts and implants represent the fastest surgical subsegment, powered by bioinductive and synthetic scaffold breakthroughs. The tendonitis treatment market size for grafts is projected to scale in tandem with sports medicine fellowship adoption of these materials. AI tools that match patient variables with optimal treatment algorithms further improve outcomes, reinforcing the non-surgical lead.

By Healthcare Setting: Rehabilitation Centers Accelerate

Hospitals retained 41.74% share of the tendonitis treatment market size in 2025, supported by emergency capacity and operating rooms. Rehabilitation centers, however, are expanding at 4.18% CAGR on the back of technology-enhanced environments that combine robotics, virtual reality, and tele-monitoring. Specialty clinics carve out niches by focusing on single-joint or athlete-centric programs that promise quicker return-to-sport metrics.

The proliferation of digital health applications fuels the rehabilitation boom. Centers now pair smartphone-based range-of-motion tracking with AI analytics to flag suboptimal progress and adjust plans instantly. Direct-to-consumer studio models offer bundled assessments, home equipment rentals, and live virtual coaching, expanding access and compressing downstream hospital volumes.

Geography Analysis

North America commanded 38.17% of the tendonitis treatment market share in 2025 and is projected to progress at a 3.18% CAGR to 2031. Strong insurer coverage, high sports participation, and early adoption of regenerative implants keep procedure volumes elevated. The United States accounts for the bulk of spend, while Canada’s universal payer system is opening tendinopathy centers of excellence to accommodate an aging worker base. Mexico offers growth upside as private hospitals upgrade imaging fleets and promote weekend sports packages.

Asia-Pacific is the fastest-growing geography, advancing at a 4.28% CAGR through 2031. China leads capital deployment into smart hospitals and musculoskeletal AI startups, driving procedure expansion beyond tier-one cities. Japan leverages its robotics leadership to refine post-operative rehab protocols, supporting premium pricing. India’s vast population and digital health push create a fertile market for smartphone-delivered physio programs, lowering entry barriers for rural consumers. Australia and South Korea showcase high elective surgery rates, fueling graft and implant sales.

Europe records a 3.43% CAGR as Germany, the United Kingdom, and France emphasize evidence-based protocols and cross-border value-based care pilots. Providers prioritize regenerative treatments backed by randomized controlled trials, accelerating biologic penetration. Middle East and Africa deliver 2.57% CAGR; Gulf Cooperation Council states invest in sports medicine hubs to capture medical tourism spill-over. South America shows 2.88% CAGR, with Brazil and Argentina expanding private orthopedic suites and partnering with device makers to pilot AI ultrasound services.

Competitive Landscape

The tendonitis treatment market features moderate fragmentation. Top orthopedic device manufacturers integrate surgical implants, regenerative patches, and imaging software to provide end-to-end solutions. Smith + Nephew’s REGENETEN implant cuts re-tear risk by 68% compared with standard care, giving the firm a credentialed flagship in biologic repair. Johnson & Johnson MedTech’s November 2024 deal with Responsive Arthroscopy extends its reach into shoulder, foot, and ankle soft-tissue solutions, highlighting the importance of portfolio breadth.

Emerging contenders target digital rehabilitation and minimally invasive devices. Platforms such as TENZR supply motion-tracking biosensors that quantify tendon load and transmit alerts to therapists, while CoNextions Medical promotes a suture-based ligament repair system optimized for outpatient settings. Investors reward models that combine hardware, software, and services to lock in data-driven recurring revenue.

White-space prospects center on AI-guided personalized care, integrated remote-to-in-clinic treatment pathways, and collated real-world evidence registries that underpin faster reimbursement for novel biologics. Partnerships among material scientists, sports leagues, and payer analytics teams will likely accelerate product validation cycles and tip competitive advantage toward data-rich incumbents.

Tendonitis Treatment Industry Leaders

Enovis Corporation

Ossur hf

Smith+Nephew plc

Stryker Corporation

Zimmer Biomet Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Atreon Orthopedics received FDA 510(k) clearance to extend its ROTIUM Bioresorbable Wick to all tendon repairs, broadening use beyond rotator cuff procedures.

- January 2025: Bioventus sold its Advanced Rehabilitation business to Accelmed Partners for USD 45 million, freeing capital for core orthobiologic projects.

- November 2024: Johnson & Johnson MedTech forged a strategic agreement with Responsive Arthroscopy to enhance its sports soft tissue offering.

- February 2024: Smith + Nephew expanded its REGENETEN implant line with new sizing and instrumentation to serve diverse patient anatomies.

Global Tendonitis Treatment Market Report Scope

As per the scope of this report, tendonitis is the inflammation of a tendon that happens when a person overuses or injures a tendon during sports or any other physical activity. It is linked to an acute injury with inflammation. It mostly affects the elbow, wrist, finger, thigh, and other body parts where tendons are present.

The Tendonitis Treatment Market is segmented by Condition (Achilles Tendonitis, Supraspinatus Tendonitis, Tennis Elbow, and Other Conditions), Treatment (Surgical Treatment, Physical (Non-surgical) Therapy, and Other Treatments), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value in USD million for the above segments.

| Achilles Tendonitis |

| Supraspinatus Tendonitis |

| Tennis Elbow (Lateral Epicondylitis) |

| Patellar Tendinopathy |

| de Quervain's Tenosynovitis |

| Other Conditions |

| Surgical Treatment | Open Surgery |

| Minimally-Invasive Surgery | |

| Grafts & Implants | |

| Non-Surgical Treatment | Physiotherapy & Rehabilitation |

| Extracorporeal Shock-Wave Therapy (ESWT) | |

| Orthotics & Supports | |

| Regenerative Therapies | |

| Photobiomodulation & Red-light Therapy | |

| Pharmacologic Pain Management | |

| Other Treatments | Nutraceuticals & Anti-inflammatory Supplements |

| Wearable Neuromodulation Devices |

| Hospitals |

| Specialty Clinics |

| Rehabilitation Centers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Condition | Achilles Tendonitis | |

| Supraspinatus Tendonitis | ||

| Tennis Elbow (Lateral Epicondylitis) | ||

| Patellar Tendinopathy | ||

| de Quervain's Tenosynovitis | ||

| Other Conditions | ||

| By Treatment | Surgical Treatment | Open Surgery |

| Minimally-Invasive Surgery | ||

| Grafts & Implants | ||

| Non-Surgical Treatment | Physiotherapy & Rehabilitation | |

| Extracorporeal Shock-Wave Therapy (ESWT) | ||

| Orthotics & Supports | ||

| Regenerative Therapies | ||

| Photobiomodulation & Red-light Therapy | ||

| Pharmacologic Pain Management | ||

| Other Treatments | Nutraceuticals & Anti-inflammatory Supplements | |

| Wearable Neuromodulation Devices | ||

| By Healthcare Setting | Hospitals | |

| Specialty Clinics | ||

| Rehabilitation Centers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What factor is strengthening demand for non-surgical tendonitis therapies?

Wider clinical acceptance of regenerative options—such as platelet-rich plasma, stem cell injections, and photobiomodulation—has increased patient preference for conservative care because these modalities shorten rehabilitation time and lower complication risk.

How are tele-physiotherapy platforms reshaping post-injury rehabilitation?

App-based programs now combine real-time motion tracking with AI coaching, enabling continuous monitoring outside the clinic and reducing the need for frequent in-person sessions, which improves adherence and lowers overall treatment costs.

Why are military-grade biomaterials gaining traction in civilian tendon repair?

These advanced scaffolds offer superior load-bearing strength and biocompatibility, delivering faster tissue integration and reduced inflammatory response compared with legacy graft materials, which improves long-term functional outcomes.

These advanced scaffolds offer superior load-bearing strength and biocompatibility, delivering faster tissue integration and reduced inflammatory response compared with legacy graft materials, which improves long-term functional outcomes.

Increased participation in jumping sports such as volleyball and basketball, coupled with broader use of ultrasound for early diagnosis, is pushing more patients toward targeted interventions before chronic degeneration sets in.

How are reimbursement policies influencing outpatient tendon repair procedures?

Insurers are expanding coverage for minimally invasive tendon repairs that demonstrate faster return-to-activity and fewer revision surgeries, prompting providers to shift surgical volumes from hospital operating rooms to cost-efficient ambulatory centers.

In what way is artificial intelligence improving tendon injury diagnosis?

AI-enhanced ultrasound algorithms detect micro-tears and early tendinopathy changes that conventional imaging often misses, enabling earlier intervention and reducing progression to complex, hard-to-treat cases.

Page last updated on: