Processor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

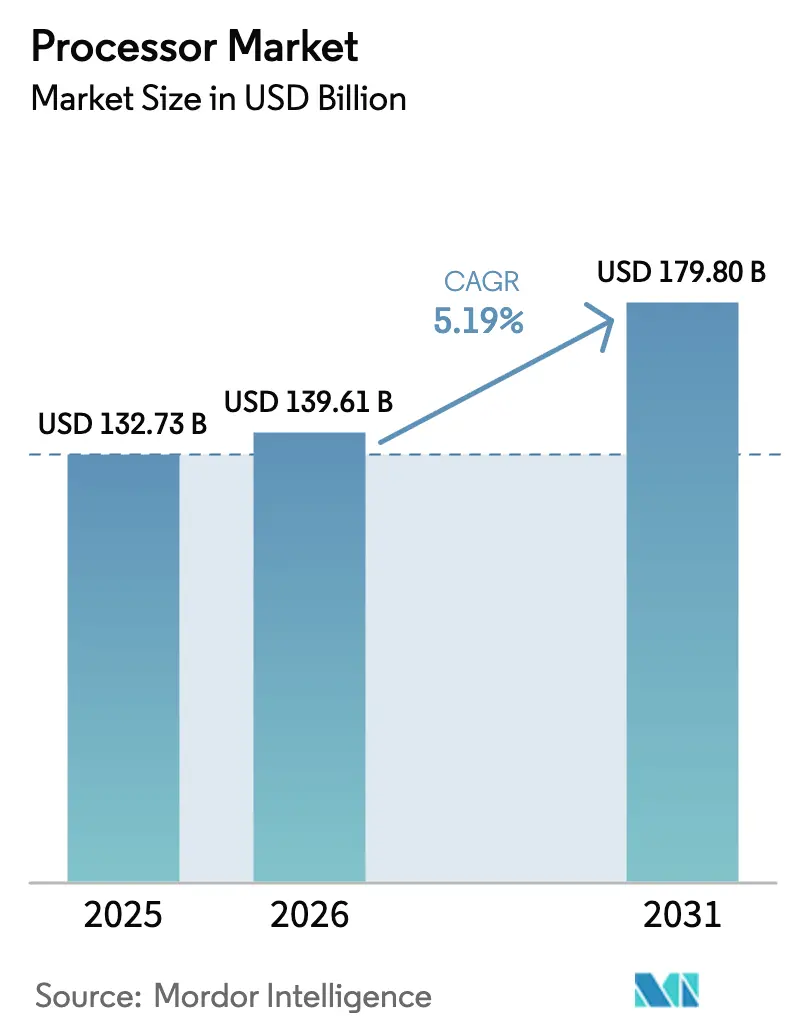

| Market Size (2026) | USD 139.61 Billion |

| Market Size (2031) | USD 179.8 Billion |

| Growth Rate (2026 - 2031) | 5.19% CAGR |

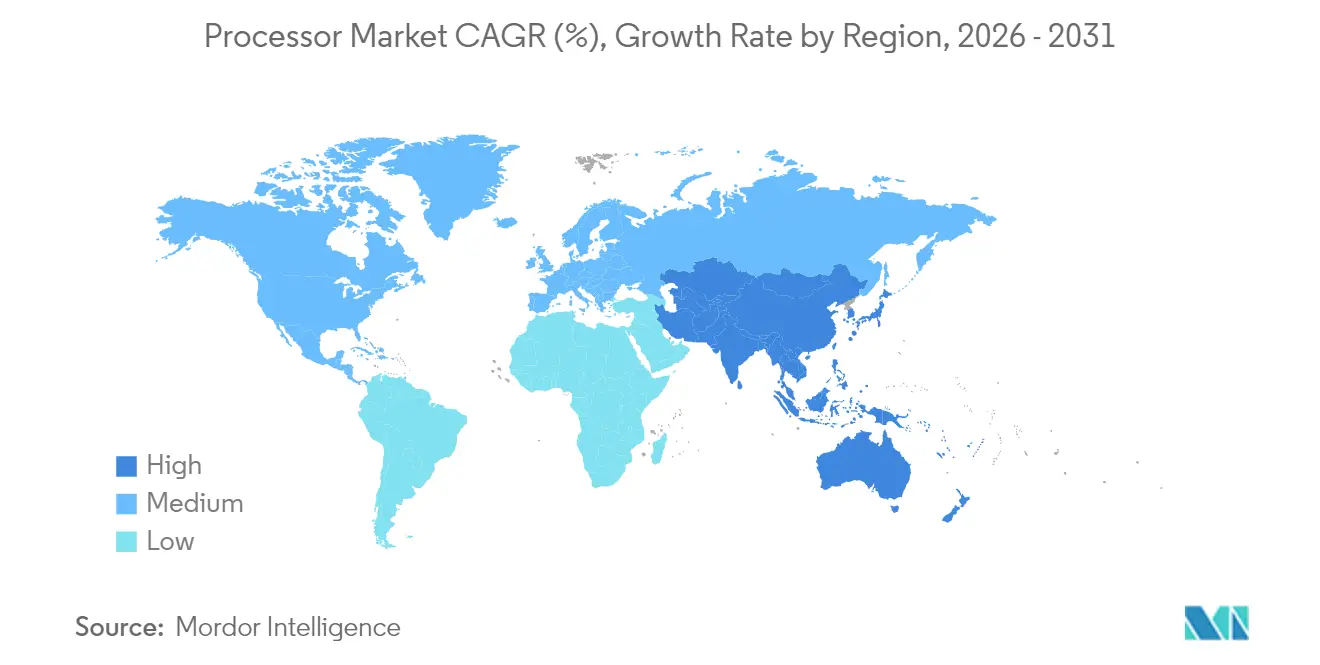

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Processor Market Analysis by Mordor Intelligence

The processor market size was valued at USD 132.73 billion in 2025 and estimated to grow from USD 139.61 billion in 2026 to reach USD 179.8 billion by 2031, at a CAGR of 5.19% during the forecast period (2026-2031). Growth rests on a transition from general-purpose designs to AI-optimized architectures, an upswing in custom silicon from hyperscalers, and government incentives that expand domestic fabrication capacity. North America anchors demand on the back of data-center investments and CHIPS Act incentives, while Asia-Pacific leads in pace as India, China, and Japan scale fabrication capacity. Architectural competition intensifies as x86’s long-held lead confronts ARM and RISC-V designs that deliver higher performance per watt. M&A activity worth more than USD 50 billion in 2025 highlights an industry pivot toward vertical integration, advanced packaging, and chiplet strategies that lower cost and raise performance per area.

Key Report Takeaways

- By product type, CPUs held 63.70% of the processor market share in 2025; APUs are projected to expand at a 6.32% CAGR to 2031.

- By micro-architecture, x86 captured 54.10% of the processor market size in 2025, while RISC-V recorded the fastest 6.47% CAGR through 2031.

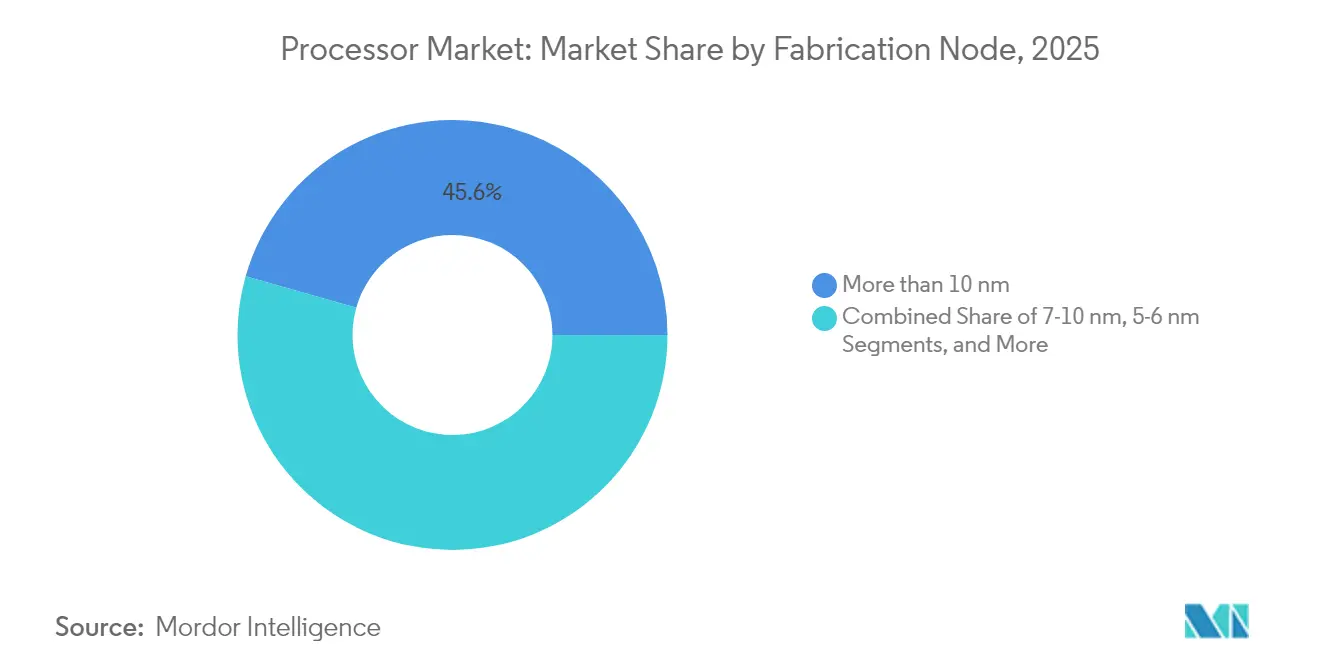

- By fabrication node, processes at 4 nm and below account for the highest 7.88% CAGR between 2026 and 2031, although nodes >10 nm still command 45.60% of 2025 revenue.

- By end-use application, consumer electronics led with a 37.90% share of the processor market size in 2025; automotive and ADAS is the fastest-growing segment at 7.49% CAGR to 2031.

- North America commanded 41.75% of the processor market share in 2025, whereas Asia-Pacific displays the highest 8.25% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Processor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising penetration of smartphones | +1.20% | Global, with strongest impact in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Growing adoption of cloud, AI and big-data workloads | +1.80% | Global, concentrated in North America and Europe data centers | Short term (≤ 2 years) |

| Expanding edge-computing deployments | +0.90% | Global, with early adoption in industrial and automotive sectors | Medium term (2-4 years) |

| Government incentives for semiconductor capacity | +0.70% | North America, Europe, Asia-Pacific core regions | Long term (≥ 4 years) |

| AI-optimized instruction-set extensions | +0.60% | Global, spill-over from data centers to consumer electronics | Short term (≤ 2 years) |

| Chiplet-based heterogeneous integration cost savings | +0.40% | Global, with concentration in advanced manufacturing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing adoption of cloud, AI and big-data workloads

Hyperscalers now design and deploy custom chips that lift performance-per-dollar versus merchant silicon. AWS Trainium2 improves AI training cost efficiency by 30-40% compared with GPU instances, while Google’s Ironwood TPU hits 4,614 TFLOPS per chip and scales to 42.5 exaflops per pod.[1]Wylie Wong, “AWS Launches Trainium2 Custom AI Chip,” datacenterknowledge.com The resulting USD 45 billion custom-chip opportunity is eroding margins for traditional CPU vendors as cloud operators internalize silicon design. Data-sovereignty mandates in Europe and parts of Asia are reinforcing regional processor preferences, further segmenting demand patterns.

Rising penetration of smartphones

Application processors now ship with dedicated NPUs as handset makers push on-device AI. Apple’s A18 Pro integrates matrix coprocessors, and Qualcomm’s Snapdragon 8 Gen 4 targets a 40% performance uplift through NPU advancements.[2]Tyson Mark, “Google Has Developed Its Own Data Center Server Chips,” tomshardware.com The monolithic integration of 5G modems has cut the bill-of-materials cost by 15-20% and lifted battery efficiency. Slower replacement cycles shift emphasis to sustained efficiency, pushing leading-edge nodes below 5 nm into volume for premium tiers.

Expanding edge-computing deployments

Industrial and automotive edge workloads outstrip legacy MCU capabilities, prompting adoption of server-class cores. Ampere’s 512-core processor targets compact data-center-in-a-box deployments, while Tesla’s Dojo die clocks 362 BF16 TFLOPS for autonomous inference at the vehicle edge.[3]Prickett Morgan Timothy, “Ampere Arm Server CPUs to Get 512 Cores,” nextplatform.com Edge designs now co-support deterministic control and AI inference, raising demand for heterogeneous compute fabrics that blend CPUs, GPU tiles, and packet-processing engines.

Government incentives for semiconductor capacity

The CHIPS and Science Act unlocked USD 52.7 billion to spur domestic fabs, triggering TSMC’s USD 165 billion Arizona complex and Intel’s USD 100 billion multi-site expansion.[4]TSMC, “Arizona Plant Expansion,” tsmc.com Similar schemes in the EU (EUR 43 billion) and India (USD 10 billion) encourage localized supply chains. Long approval cycles and construction timelines mean benefits accrue over a four-year horizon, but the policy momentum already influences site selection and long-term capacity planning.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Talent shortage in advanced node design | -1.10% | Global, most acute in North America and Europe | Medium term (2-4 years) |

| Geopolitical export controls on EDA/IP | -0.80% | Global, with concentration in US-China technology corridors | Short term (≤ 2 years) |

| Thermal design limits in sub-3 nm nodes | -0.60% | Global, affecting advanced manufacturing regions | Long term (≥ 4 years) |

| Supply-chain emissions compliance costs | -0.30% | Global, with stricter enforcement in Europe and California | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Talent shortage in advanced node design

Chipmakers face difficulty hiring engineers qualified for 3 nm and below. Intel reported 3,000 open roles despite USD 200,000 starting packages, and TSMC moved 1,000 Taiwanese staff to Arizona to train local hires. Academia’s slower curriculum cycles add a 5-7 year skills lag, especially in verification, critical as chiplet counts soar. Visa caps in the U.S. further tighten supply, prompting companies to relocate design centers to India and Southeast Asia.

Geopolitical export controls on EDA/IP

U.S. rules restricting advanced EDA tools and IP to China split design roadmaps. Alibaba’s T-Head must maintain separate EDA flows, adding 15-25% to cost and schedule, while ARM license uncertainties complicate x86 cross-licensing deals. RISC-V’s open model gains traction for export-control resilience, though high-performance toolchains remain immature. Companies, therefore, shoulder duplicated verification and restricted foundry access, dampening near-term growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Integration Redefines Value

CPUs retained 63.70% of the processor market share in 2025, yet APUs’ 6.32% CAGR underscores demand for unified CPU-GPU fabrics that handle AI inference locally. The processor market size for APUs is projected to increase in tandem with rising creator workloads that need on-chip graphics acceleration. Smartphone SoCs branch into automotive and IoT, extending their lifetime value, while smart-TV processors ride 8 K content and AI upscaling tailwinds. Commodity pressure on tablets persists as phone-class silicon narrows the performance delta.

Apple’s M-series exemplifies a shift toward shared-memory architectures that erase PCIe bottlenecks, while Intel’s Core Ultra integrates a 48 TOPS NPU to preserve x86 relevance in AI PCs. Specialty categories, smartwatch, AR/VR, and automotive, gain share from regulatory pushes on safety and assisted driving. Certification paths such as ISO 26262 lengthen development by up to 24 months but allow premium pricing and higher margin retention.

By Micro-architecture: Open Standards Gain Ground

x86 still dominates the processor market, holding 54.10% in 2025, but ARM and RISC-V architectures thrive on efficiency and licensing flexibility. Processor market size for ARM cores benefits from hyperscaler adoption: AWS Graviton4 and Google Axion yield up to 60% better energy efficiency over equivalent x86 instances. Intel’s AMX extensions aim to offset the gap but hinge on a two-year software-enablement curve.

RISC-V’s 6.47% CAGR rests on openness; SiFive and GlobalFoundries bring automotive-grade designs that challenge Power architecture’s niche in high-reliability systems. However, tooling gaps delay mainstream workloads by three to five years. Regulatory shifts that favor export-control-free IP accelerate pilot deployments, hinting at deeper market penetration after 2028.

By Fabrication Node: Premium Nodes Capture Growth

Mature nodes (>10 nm) still control 45.60% of 2025 revenue, serving cost-sensitive automotive and RF devices, but nodes at 4 nm and below post the fastest 7.88% CAGR as AI density demands escalate. Processor market size for advanced nodes rises with every generation because transistor gains outweigh growing mask costs. Sub-4 nm chips push thermal limits beyond 200 W/cm², forcing liquid cooling and advanced packaging that add USD 50–100 per package. Samsung and TSMC’s roadmaps to 2 nm by late 2025 center on backside power delivery to ease current density.

Mid-range nodes (5–6 nm) become mainstream for premium mobile and PC devices, balancing cost and efficiency, while 7-10 nm offers a bridge for designers migrating from 12 nm without incurring reticle-cost spikes. Environmental rules in California and the EU raise compliance costs 3–5% annually, nudging some volume to regions with looser emission ceilings.

By End-use Application: Automotive Momentum Builds

Consumer electronics retained 37.90% of 2025 revenue, but the processor market size in automotive and ADAS grows at a 7.49% CAGR on the path to Level 3 autonomy. Tesla’s USD 16.5 billion Samsung deal secures capacity for self-driving compute from 2026. Hyperscale data centers remain the second-largest outlet as AI training nodes expand, yet edge deployments in factories and telecom sites close the gap by distributing inference workloads.

Industrial IoT shifts to application processors that crunch data locally, cutting backhaul latency. Aerospace and defense demand processors that meet ITAR and DO-178C, adding 12-18 months to design cycles but commanding higher ASPs. Gaming consoles and cloud-gaming back-ends prolong the life of monolithic APUs that fuse ray tracing cores with scalar engines.

Geography Analysis

North America controlled 41.75% of the processor market share in 2025, thanks to the CHIPS Act funding and hyperscaler concentration. Volume ramped at TSMC Arizona’s 4 nm line in early 2025, supplying Apple and NVIDIA, while Intel pledged USD 100 billion through 2029 for foundry expansion. Talent gaps and visa limits remain structural impediments, forcing companies to import expertise from Asia.

Asia-Pacific posts the fastest 8.25% CAGR as China’s indigenous designs and India’s USD 10 billion incentives build regional self-reliance. Japan’s TSMC-JASM fab and South Korea’s System Semiconductor Vision 2030 further tilt global output eastward. Export controls restrict high-end EDA flows to Chinese firms, spurring RISC-V adoption in domestic designs.

Europe sustains growth via the EUR 43 billion Chips Act that backs GlobalFoundries’ Dresden expansion and Intel’s prospective Magdeburg fab. Automotive processors form the continent’s core demand, aligning with a robust Tier-1 supply chain. Environmental and GDPR rules steer OEMs toward regionally located fabs despite higher labor costs.

The Middle East and Africa enter assembly-and-test segments using sovereign investment funds, but advanced fabrication remains nascent.

Competitive Landscape

Competition in the processor market centers on three vectors: architectural innovation, vertical integration, and packaging leadership. Intel’s delays open the share for AMD and ARM-based vendors, while NVIDIA’s Grace Hopper unites CPU and GPU into a single module for AI training supremacy. Hyperscalers, having deployed over 50 million in-house chips, now influence instruction-set roadmaps and foundry capacity reservations.

Qualcomm’s USD 2.4 billion Alphawave Semi acquisition broadens high-speed interconnect IP, underscoring a shift toward chiplet-era integration. GlobalFoundries’ plan to buy MIPS adds RISC-V IP for edge and autonomous workloads. Strategy converges on owning silicon, packaging, and software stacks that lock in ecosystem value. FTC scrutiny of large deals creates regulatory overhead, but vendors perceive consolidation as essential to finance multi-billion-dollar node migrations.

White-space opportunities persist in edge-AI ASICs, automotive-grade HPC, and post-quantum cryptography accelerators. Vendors with deep software ecosystems and packaging know-how gain leverage as transistor scaling alone plateaus.

Processor Industry Leaders

Advanced Micro Devices Inc. (AMD)

Intel Corporation

Qualcomm Technologies Inc.

Apple Inc.

NVIDIA Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Qualcomm agreed to acquire Alphawave Semi for USD 2.4 billion to secure high-speed connectivity IP for cloud AI processors, strengthening its vertical stack.

- August 2025: TSMC announced USD 38-42 billion capex for 2025 to build eight fabs and an advanced-packaging plant, ensuring node leadership and meeting surging AI demand.

- July 2025: Tesla signed a USD 16.5 billion chip supply deal with Samsung to fabricate AI6 processors, locking in 2026-2033 capacity for full self-driving compute.

- July 2025: GlobalFoundries agreed to acquire MIPS, expanding customizable RISC-V IP for edge and automotive use-cases, with closure slated for H2 2025.

Global Processor Market Report Scope

A processor refers to an integrated electronic circuit that performs the calculations that run a computer. It performs arithmetical, logical, I/O, and other basic instructions that are passed from an operating system.

The processor market is segmented by type of product (CPU (client (desktop and laptop), server) and APU (smartphone, tablet, smart television, smart speakers)) and geography (China (including Hong Kong), Taiwan, United States, Rest of the World)). The market sizes and forecasts are provided in terms of value (in USD) for all the above segments.

| CPU |

| Client (Desktop and Laptop) |

| Server |

| APU |

| Smartphone |

| Tablet |

| Smart Television |

| Smart Speakers |

| Other (Smartwatch, Notebook, AR/VR, Automotive) |

| x86 |

| Arm |

| RISC-V |

| Power |

| More than 10 nm |

| 7-10 nm |

| 5-6 nm |

| Equal to and less than 4 nm |

| Consumer Electronics |

| Data Center and Cloud |

| Industrial and IoT Edge |

| Automotive and ADAS |

| Aerospace and Defense |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | CPU | ||

| Client (Desktop and Laptop) | |||

| Server | |||

| APU | |||

| Smartphone | |||

| Tablet | |||

| Smart Television | |||

| Smart Speakers | |||

| Other (Smartwatch, Notebook, AR/VR, Automotive) | |||

| By Micro-Architecture | x86 | ||

| Arm | |||

| RISC-V | |||

| Power | |||

| By Fabrication Node | More than 10 nm | ||

| 7-10 nm | |||

| 5-6 nm | |||

| Equal to and less than 4 nm | |||

| By End-Use Application | Consumer Electronics | ||

| Data Center and Cloud | |||

| Industrial and IoT Edge | |||

| Automotive and ADAS | |||

| Aerospace and Defense | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the processor market in 2026?

The processor market size stood at USD 139.61 billion in 2026.

What CAGR is forecast for processors through 2031?

The market is projected to grow at a 5.19% CAGR between 2026 and 2031.

Which region grows fastest for processor demand?

Asia-Pacific is expected to post an 8.25% CAGR, the highest among regions.

What segment is expanding quickest in end-use applications?

Automotive and ADAS processors are forecast to rise at 7.49% CAGR to 2031.

Which micro-architecture shows the strongest growth?

RISC-V leads with a 6.47% CAGR, reflecting interest in open, customizable IP.

Why are hyperscalers designing their own chips?

Custom silicon improves performance-per-dollar and aligns with data-sovereignty mandates, creating a USD 45 billion internal market.

Page last updated on: