Oscillating Positive Expiratory Pressure (OPEP) Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

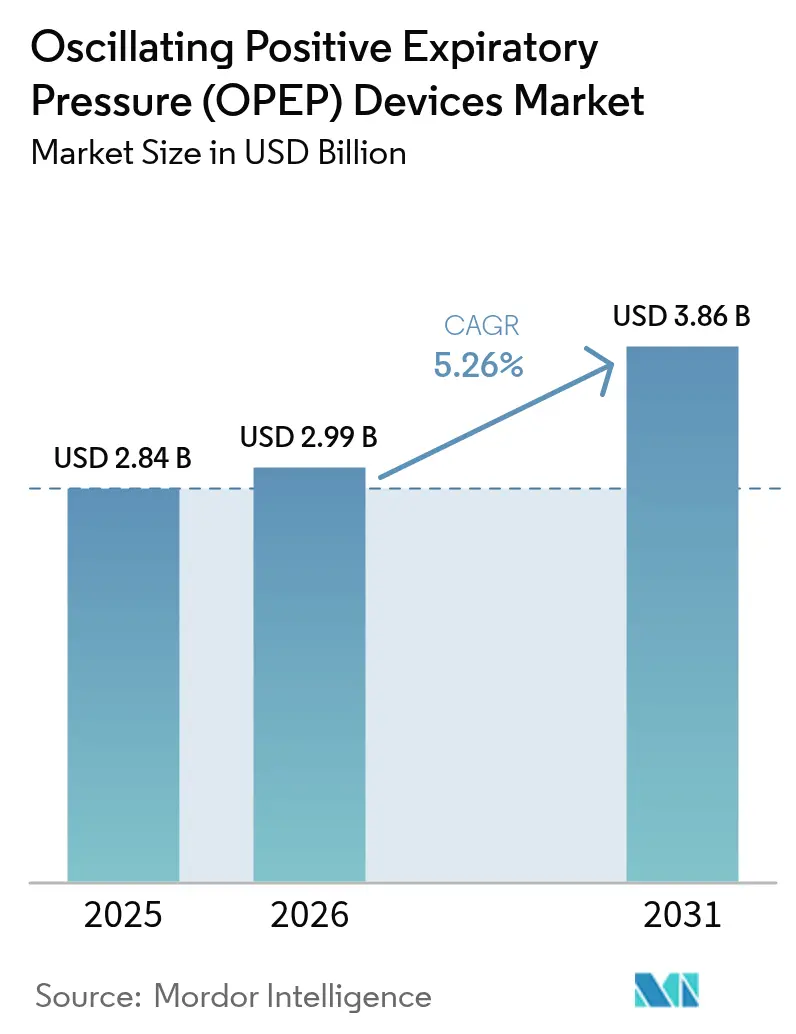

| Market Size (2026) | USD 2.99 Billion |

| Market Size (2031) | USD 3.86 Billion |

| Growth Rate (2026 - 2031) | 5.26% CAGR |

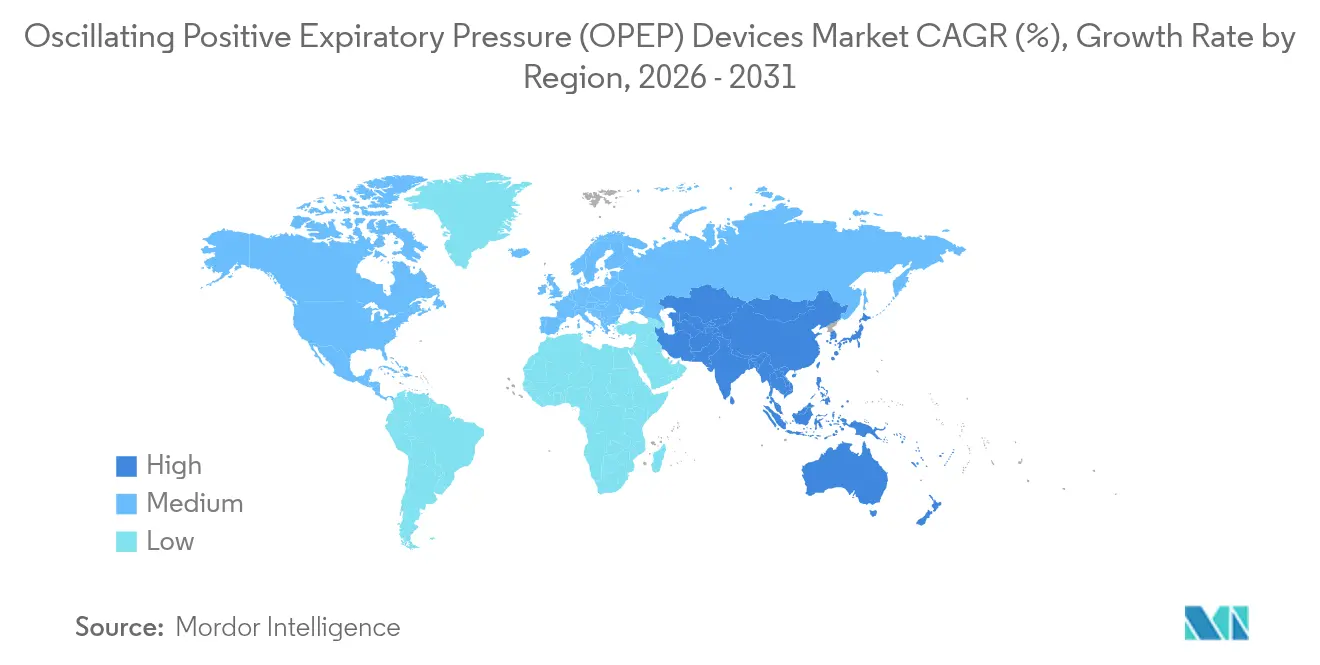

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oscillating Positive Expiratory Pressure (OPEP) Devices Market Analysis by Mordor Intelligence

The oscillating positive expiratory pressure (OPEP) devices market size was valued at USD 2.84 billion in 2025 and estimated to grow from USD 2.99 billion in 2026 to reach USD 3.86 billion by 2031, at a CAGR of 5.26% during the forecast period (2026-2031). Demographic aging, surging chronic respiratory disease incidence, and steady technology upgrades combine to keep demand on an upward path. Growth also benefits from gravity-independent engineering that frees patients from posture constraints, expanding real-world usability. Digital connectivity features now capture adherence and lung-function data for clinicians, supporting payer evidence needs and guiding remote therapy adjustments. Major manufacturers emphasise clinical-outcome proof and FDA clearances to differentiate, while regional reimbursement revisions and precision-medicine protocols sustain a broad opportunity set for the oscillating positive expiratory pressure (OPEP) devices market.

Key Report Takeaways

- By product type, mouthpiece devices led with 44.88% revenue share of the oscillating positive expiratory pressure (OPEP) devices market in 2025; gravity-independent units are set to advance at a 9.14% CAGR through 2031.

- By indication, COPD and asthma accounted for 55.01% of oscillating positive expiratory pressure (OPEP) devices market share in 2025, while bronchiectasis is forecast to expand at a 9.43% CAGR to 2031.

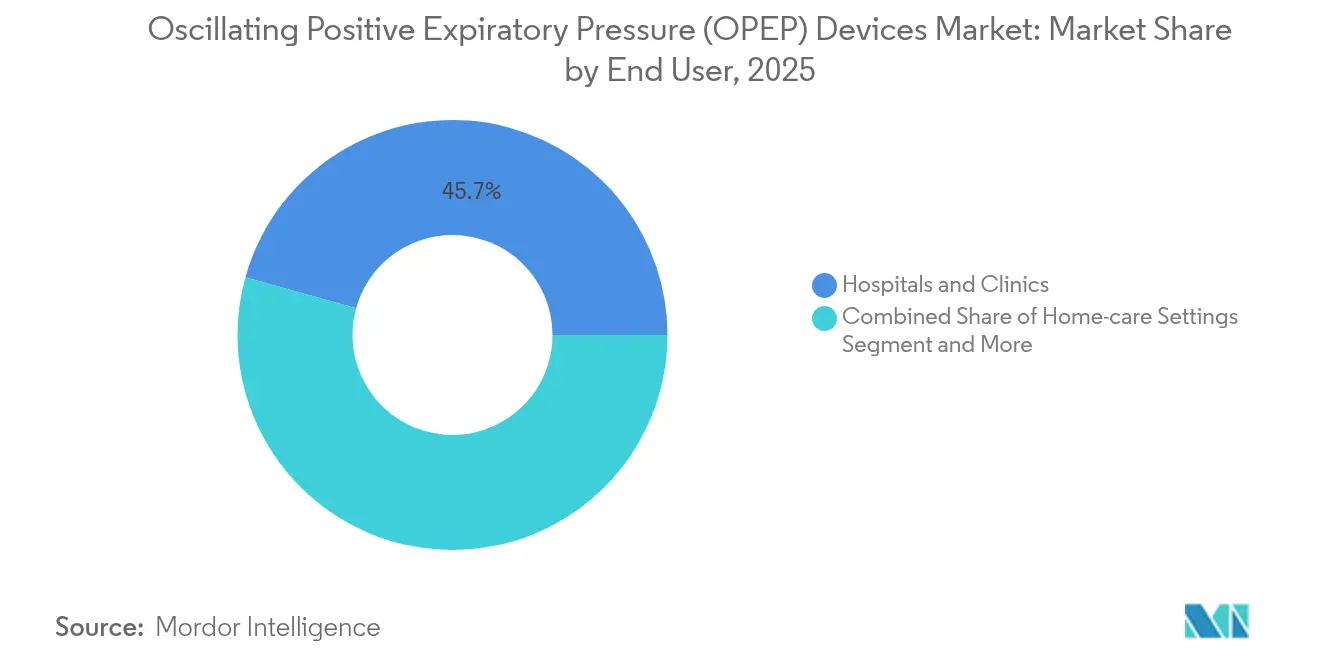

- By end user, hospitals and clinics held 45.67% of the oscillating positive expiratory pressure (OPEP) devices market size in 2025 and home-care settings are progressing at a 10.21% CAGR through 2031.

- By distribution channel, offline retail captured 51.54% of 2025 revenue, whereas online platforms register the fastest growth at 9.19% CAGR to 2031.

- By geography, North America commanded 38.05% of global revenue in 2025; Asia-Pacific leads in momentum with an 8.27% CAGR forecast through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Oscillating Positive Expiratory Pressure (OPEP) Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of COPD & asthma | +1.2% | North America & Europe lead | Long term (≥ 4 years) |

| Advancements in portable, gravity-independent devices | +0.9% | North America & Asia-Pacific | Medium term (2-4 years) |

| Inclusion in GOLD & ERS guidelines | +0.7% | Global | Short term (≤ 2 years) |

| Growth of home-based respiratory care | +0.8% | North America & Europe expanding to Asia-Pacific | Medium term (2-4 years) |

| Reimbursement for digital monitoring bundles | +0.6% | North America & Europe | Medium term (2-4 years) |

| Employer-funded COPD wellness benefits | +0.4% | North America, emerging Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence Of COPD & Asthma

COPD affects 11.7 million insured adults ≥ 40 years in the United States, creating large-scale, persistent demand for airway-clearance solutions[1]Bazell C. et al., “Variation in Prevalence and Burden of COPD,” copdfoundation.org. Higher mortality among Medicare-insured patients underscores the clinical and financial urgency behind earlier, continuous therapy adoption. Aging drives progressive respiratory-muscle weakness that magnifies mucus retention risk and pushes health systems to favor mechanical aids that minimise exacerbations. As payers scrutinise hospital readmission penalties, hospitals increasingly prioritise oscillating positive expiratory pressure (OPEP) devices market products to keep COPD and asthma patients stable at home. Public-health campaigns now highlight airway-clearance adherence as a preventive measure, broadening device familiarity among primary-care physicians and patients alike.

Technological Advancements In Portable, Gravity-Independent OPEP Devices

Gravity-independent engineering removes posture limits that once curtailed bedside and ambulatory use. Trials show T-PEP systems boosting FVC by 10.25% and FEV₁ by 7.06% versus baseline, plus lower exacerbation incidence after three months. Battery-powered oscillators automate frequency and amplitude based on real-time airflow sensing, personalising mucus mobilisation while collecting usage analytics for clinicians. Bluetooth-enabled dashboards link into respiratory-management apps, letting providers verify adherence and intervene remotely, a capability that aligns with U.S. remote-physiologic-monitoring CPT codes. Collectively, such innovations reposition devices as data-rich platforms, underpinning a premium tier within the oscillating positive expiratory pressure (OPEP) devices market.

Inclusion In Global GOLD & ERS Clinical Guidelines

The 2025 GOLD update explicitly lists oscillatory PEP among recommended non-pharmacologic COPD interventions, giving physicians a clear mandate to prescribe the modality. Parallel guidance from the European Respiratory Society endorses OPEP for bronchiectasis, providing cross-border harmonisation around best practice. Such endorsements convert OPEP from optional to standard-of-care, shifting procurement decisions from discretionary to obligatory and shortening adoption lag time. Hospitals now bundle devices into COPD discharge kits to align with quality-metric audits, while outpatient clinics integrate OPEP training into pulmonary-rehabilitation curricula. This guideline validation fortifies payer confidence, smoothing reimbursement approvals and accelerating volume growth within the oscillating positive expiratory pressure (OPEP) devices market.

Rapid Growth Of Home-Based Respiratory Care Programs

Remote-monitoring studies show 77% adherence to daily spirometry in interstitial-lung-disease cohorts, confirming patient willingness to follow decentralised regimens. U.S. analysts estimate USD 265 billion of hospital services could shift home by 2030, redirecting capital toward portable therapeutic devices[2]Noel A., “Future of Remote Patient Monitoring,” ctel.org. Manufacturers respond with lightweight, app-linked OPEP products that transmit usage metrics and symptom scores to clinicians who can adjust therapy plans virtually. Medicare reimbursement for remote monitoring provides a financial pathway, and COVID-19-era flexibility has durably raised patient and provider comfort with home-centric care models. Collectively, these forces lift penetration of connected devices and reinforce double-digit growth expectations for the oscillating positive expiratory pressure (OPEP) devices market in the home-care channel.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of trained respiratory therapists | -0.8% | Global, pronounced in rural areas | Long term (≥ 4 years) |

| Limited clinical evidence versus other ACTs | -0.6% | Emerging markets most affected | Medium term (2-4 years) |

| Device reuse safety concerns in low-income settings | -0.4% | Asia-Pacific, Middle East & Africa | Short term (≤ 2 years) |

| Patent expiries prompting price competition | -0.5% | Mature markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage Of Trained Respiratory Therapists

Many countries face tight labour markets for respiratory therapists, restricting capacity to teach airway-clearance techniques. A U.S. partnership launched in 2024 aims to graduate more professionals in 18 months, yet such programs remain rare and localised. Urban concentration of existing therapists leaves rural COPD clusters underserved, hampering equipment utilisation rates even when devices are supplied. Reimbursement gaps for pulmonary rehabilitation discourage some hospitals from expanding staff rosters, further constraining uptake. Device makers are consequently embedding audiovisual coaching features to guide self-management and offset clinician shortages.

Limited Clinical Evidence Versus Alternative ACTs

Head-to-head trials comparing OPEP with high-frequency chest-wall oscillation or autogenic drainage remain sparse and yield mixed conclusions, fuelling payer hesitation[3]Kloni M., “HFCWO Effectiveness in COPD,” pneumon.org. Precision-medicine guidelines for bronchiectasis highlight individualised selection, yet the data gaps complicate algorithmic decision support. Consequently, some physicians default to traditional techniques, delaying OPEP prescription. Manufacturers investing in multicentre superiority trials could unlock higher reimbursement tiers and secure formulary preference, but current evidence scarcity modestly dampens oscillating positive expiratory pressure (OPEP) devices market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Mouthpiece Devices Drive Market Leadership

Mouthpiece units delivered 44.88% of 2025 revenue, maintaining leadership due to ease of sealing and broad adult suitability. Gravity-independent models are scaling fastest at 9.14% CAGR because they operate reliably regardless of patient orientation, a feature valued in home and post-operative wards. In monetary terms, this sub-segment is forecast to add USD 362 million to oscillating positive expiratory pressure (OPEP) devices market size by 2031. Face-mask interfaces remain essential for paediatric and neuro-muscular cohorts that cannot sustain effective mouth closure, while bottle-type devices keep a low-cost niche where clinicians require fine pressure adjustment.

Competitive rivalry now centres on integrating sensors that verify pressure targets, collect usage data, and sync with hospital EHRs. Vendors that bundle cloud dashboards demonstrate higher formulary preference, even at price premiums, because they arm clinicians with compliance reports for payers. Consequently, gravity-dependent legacy designs are losing shelf space across tertiary centres, although they still serve budget-constrained facilities in Latin America and Africa.

By Indication: COPD Dominance Drives Bronchiectasis Innovation

COPD and asthma collectively held 55.01% of oscillating positive expiratory pressure (OPEP) devices market share in 2025, driven by guideline-backed positioning in exacerbation management. The broncho-pulmonary specialist community expects adoption to deepen as payers reward home-monitoring bundles. Bronchiectasis, with a 9.43% forecast CAGR, enjoys higher clinical urgency amid precision-medicine trends that match airway-clearance modalities to radiologic pattern and sputum phenotype.

As electronic-health-record flags prompt pulmonologists to consider OPEP earlier in bronchiectasis, manufacturers are co-funding registry studies to capture phenotype-specific outcomes. Post-operative pulmonary-complication prevention forms a secondary growth pocket as enhanced-recovery protocols require non-pharmacologic mucus clearance to shorten length of stay. Meanwhile, cystic-fibrosis demand plateaus as the patient base stabilises under CFTR modulators, yet lifelong therapy needs ensure steady volume.

By End User: Home Care Acceleration Transforms Distribution

Institutional settings such as hospitals and clinics supplied 45.67% of 2025 revenue because they remain initiation points for therapy and training. The migration of chronic-care management to residences underpins a 10.21% CAGR in the home segment, adding an estimated USD 302 million to oscillating positive expiratory pressure (OPEP) devices market size by 2031. Payers reward remote-physiologic monitoring, so home-care organisations increasingly source devices featuring cellular or Wi-Fi modules that automatically transmit usage logs.

Ambulatory surgery centres represent a tertiary outlet where same-day discharge protocols rely on OPEP to prevent atelectasis. Pulmonary-rehab centres purchase multipacks for supervised sessions, but revenue growth is capped by limited reimbursement. Nursing homes and long-term-care facilities slowly adopt auto-tuned OPEP devices that minimise staff burden, illustrating how design simplicity can widen user bases even in low-ratio care environments.

By Distribution Channel: Digital Platforms Gain Momentum

Offline wholesalers and durable medical equipment outlets still accounted for 51.54% of 2025 dollars thanks to entrenched referral pathways. Yet patients seeking convenience and price transparency are fuelling a 9.19% CAGR for online channels. Direct-to-consumer websites now include tele-consult bookings, prescription handling, and video tutorials, reducing the learning curve and lowering abandonment rates.

Regulators caution that prescription-only devices must involve licensed oversight; consequently, hybrid fulfilment models partner e-commerce storefronts with tele-health physicians. Internationally, India’s new code of conduct for device marketing tightens digital advertising claims, yet provides clearer rules that reassure multinationals considering web-first launches. As cross-border sales grow, vendors integrate multilingual apps and offer local-currency payment plans to expand reach in Southeast Asia and the Middle East.

Geography Analysis

North America kept its 38.05% leadership stake in 2025 by virtue of comprehensive insurance coverage and early adoption of connected respiratory technologies. U.S. hospitals discharge COPD patients with bundled OPEP kits that synchronise to cloud dashboards, while Canada’s provincial systems reimburse devices under durable-medical-equipment lists. Still, reimbursement cuts to pulmonary-rehab programmes strain hospital budgets, nudging growth towards outpatient and home-care providers that can leverage telemonitoring codes. Mexico, propelled by universal-coverage expansion, imports cost-optimised mouthpiece units and may double its installed base by 2030.

Europe benefits from harmonised CE-mark rules and strong evidence-based culture. Germany and the United Kingdom integrate oscillating positive expiratory pressure (OPEP) devices market products into bronchiectasis pathways, while Spain and Italy accelerate procurement for home-oxygen patients. Eastern-European uptake lags because training shortages slow guideline implementation, yet EU recovery funds earmarked for digital health could hasten closing the gap. Region-wide, payer scrutiny emphasises proven cost offsets, favouring vendors armed with real-world evidence archives.

Asia-Pacific posts the fastest 8.27% CAGR, anchored by China’s chronic-disease strategy that subsidises airway-clearance devices in community clinics. Japan’s super-aged society values gravity-independent models that seniors can operate supine, while South Korea channels digitised national-insurance data to monitor adherence. India tightens quality norms, fostering trust among pulmonologists to switch from improvised bottle PEP to FDA-cleared imports. Australia’s remote rural communities benefit from tele-health reimbursement that pairs indigenous patients with metropolitan respiratory therapists, underpinning steady adoption of connected devices.

Competitive Landscape

The oscillating positive expiratory pressure industry features moderate fragmentation: top-tier companies combine mechanical design heritage with embedded software and data-analytics roadmaps. Monaghan Medical promotes its Aerobika line with peer-reviewed outcome studies emphasising exacerbation reduction, while ResMed leverages its cloud-architecture expertise to integrate OPEP data alongside CPAP adherence dashboards. Smiths Medical targets post-operative applications, positioning its devices within enhanced-recovery supply bundles purchased by ambulatory surgery networks.

New entrants employ AI-driven coaching apps to guide users and flag non-response for clinical review, a value-add that resonates with employer-sponsored COPD programmes. Inogen secured FDA 510(k) clearance for its SIMEOX 200 in 2025, demonstrating the regulator’s acceptance of digital-heavy designs. Strategic M&A also reshapes distribution reach: Owens & Minor’s USD 1.36 billion purchase of Rotech Healthcare boosts home-delivery capability and strengthens negotiation power with payers.

Price pressure intensifies where patent expiries invite low-cost entrants, yet premium brands defend share through data packages that support reimbursement appeals. Collaboration with pharmaceutical firms exploring inhaled antibacterials for bronchiectasis may open co-bundling pathways, while joint ventures with tele-health providers facilitate subscription-based device supply integrated into virtual-care contracts. Leading players reinvest 7-9% of revenue into R&D, notably in sensor miniaturisation and battery-life optimisation, to lock in long-term differentiation.

Oscillating Positive Expiratory Pressure (OPEP) Devices Industry Leaders

PARI GmbH

ICU Medical (Smiths Medical)

Monaghan Medical / Trudell

D-R Burton Healthcare

AirPhysio

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: ICU Medical and VisionHealth release MyAcapella, a mobile app that guides and logs OPEP therapy sessions for chronic-lung-disease patients.

- July 2024: Owens & Minor acquires Rotech Healthcare for USD 1.36 billion, enlarging the company’s home-care respiratory-equipment footprint.

Global Oscillating Positive Expiratory Pressure (OPEP) Devices Market Report Scope

An OPEP device refers to a device that uses Oscillating Positive Expiratory Pressure or OPEP to help clear secretions from the airways. People with chronic bronchitis, bronchiectasis, COPD, and cystic fibrosis often produce excessive mucus. As they exhale through the OPEP device, they can feel vibrations or 'pulses,' which loosen the mucus from the walls of the lungs, making it easier to cough up the secretions. The Oscillating Positive Expiratory Pressure (OPEP) Devices market is Segmented by Product Type (Face Mask PEP Devices, Mouthpiece PEP Devices, and Bottle PEP Devices), Indication (COPD and Asthma, Bronchitis, Cystic Fibrosis, and Others), End-User (Hospital and Clinics, Ambulatory Surgical Centers, and Others), and Geography (North America, Europe, Asia-Pacific, and Rest of the World (ROW)). The report offers the value (in USD million) for the above segments.

| Face Mask PEP Devices |

| Mouthpiece PEP Devices |

| Bottle/Water-column PEP Devices |

| Gravity-Dependent OPEP Devices |

| Gravity-Independent OPEP Devices |

| COPD & Asthma |

| Bronchitis |

| Bronchiectasis |

| Cystic Fibrosis |

| Post-operative Pulmonary Complications |

| Others |

| Hospitals & Clinics |

| Home-care Settings |

| Ambulatory Surgical Centers |

| Pulmonary Rehabilitation Centers |

| Others |

| Offline Retail |

| Online Platforms |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Face Mask PEP Devices | |

| Mouthpiece PEP Devices | ||

| Bottle/Water-column PEP Devices | ||

| Gravity-Dependent OPEP Devices | ||

| Gravity-Independent OPEP Devices | ||

| By Indication | COPD & Asthma | |

| Bronchitis | ||

| Bronchiectasis | ||

| Cystic Fibrosis | ||

| Post-operative Pulmonary Complications | ||

| Others | ||

| By End User | Hospitals & Clinics | |

| Home-care Settings | ||

| Ambulatory Surgical Centers | ||

| Pulmonary Rehabilitation Centers | ||

| Others | ||

| By Distribution Channel | Offline Retail | |

| Online Platforms | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the growth outlook for the oscillating positive expiratory pressure (OPEP) devices market?

The market is projected to rise from USD 2.99 billion in 2026 to USD 3.86 billion by 2031 at a 5.26% CAGR, driven by aging demographics, chronic-disease prevalence, and digital integration of airway-clearance devices.

Which product type generates the most revenue?

Mouthpiece devices accounted for 44.88% of 2025 revenue and remain the leading product category because they balance clinical efficacy with user convenience.

Why are gravity-independent devices growing faster?

They eliminate patient-position constraints, incorporate real-time pressure algorithms, and sync with monitoring apps, supporting a 9.14% forecast CAGR through 2031.

How important is home-care to future demand?

Home-care is the fastest-growing end-user segment at 10.21% CAGR as payers reward remote monitoring and patients prefer at-home management of chronic respiratory conditions.

Which region will see the highest growth?

Asia-Pacific is forecast to expand at an 8.27% CAGR through 2031 because of rising healthcare investment, increased chronic-disease awareness, and regulatory support for medical-device adoption.

Page last updated on: