Market Overview

| Study Period | 2021 - 2031 |

|---|---|

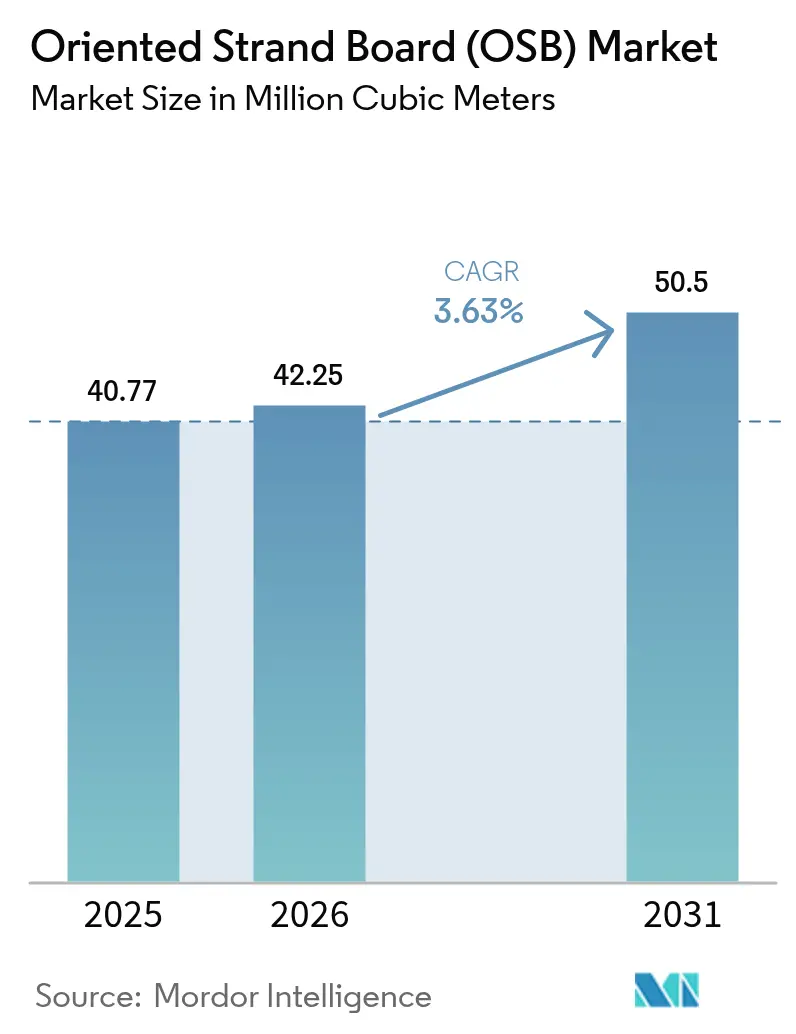

| Market Volume (2026) | 42.25 Million cubic meters |

| Market Volume (2031) | 50.5 Million cubic meters |

| Growth Rate (2026 - 2031) | 3.63% CAGR |

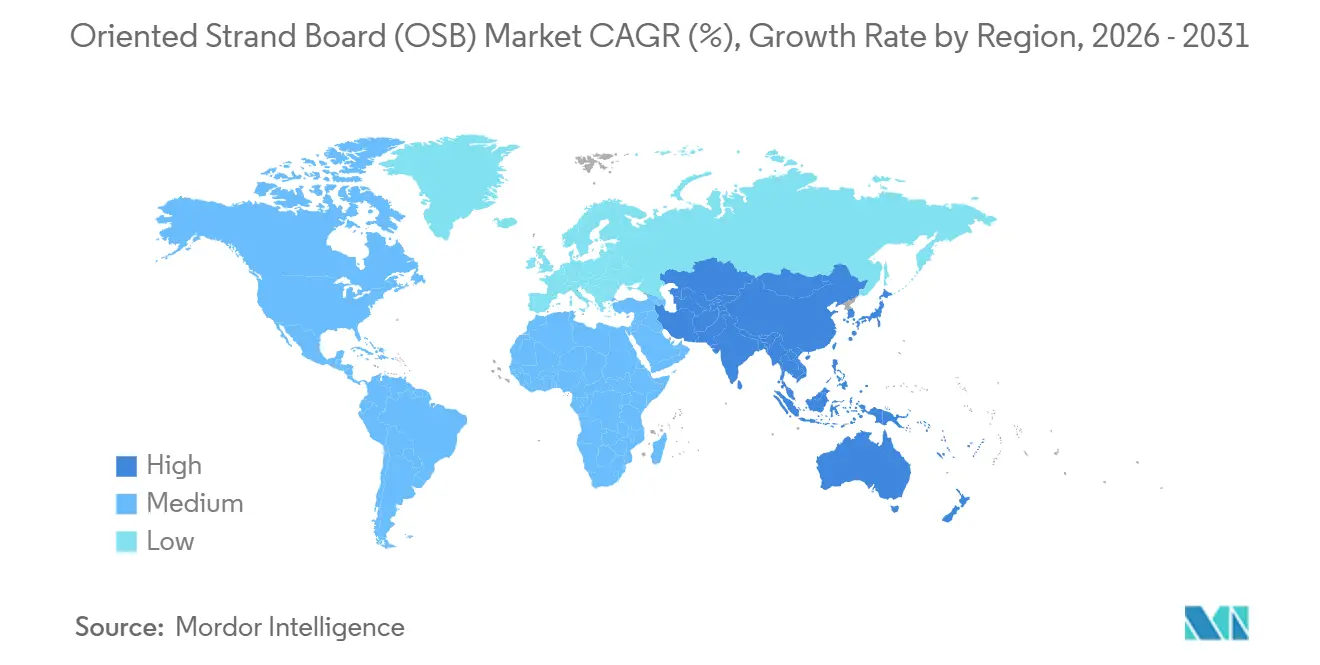

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oriented Strand Board (OSB) Market Analysis by Mordor Intelligence

The Oriented Strand Board Market size is projected to expand from 40.77 million cubic meters in 2025 and 42.25 million cubic meters in 2026 to 50.50 million cubic meters by 2031, registering a CAGR of 3.63% between 2026 to 2031. Growth is moderating from the post-pandemic construction spike yet remains firmly positive as modular housing, carbon-credit policies, and grade-driven performance standards lift baseline consumption. North America still anchors the Oriented Strand Board market with 60.12% of 2025 volume, but Asia-Pacific’s 6.28% forecast CAGR signals a decisive geographic pivot as India’s affordable-housing push and Southeast Asia’s expressway programs offset China’s property contraction. OSB/3 grade leads at 46.89% share because its dual load-bearing and moisture-resistant rating aligns with stricter codes in hurricane- and typhoon-prone regions. Construction end use, which consumed 69.51% of the 2025 volume, benefits from factory-built housing that specifies thicker OSB panels to withstand highway transport stresses. On the supply side, strategic mill curtailments—such as West Fraser’s 2026 shutdown in Alberta—have replaced pure expansion plays, stabilizing panel prices after the 2021-2022 volatility.

Key Report Takeaways

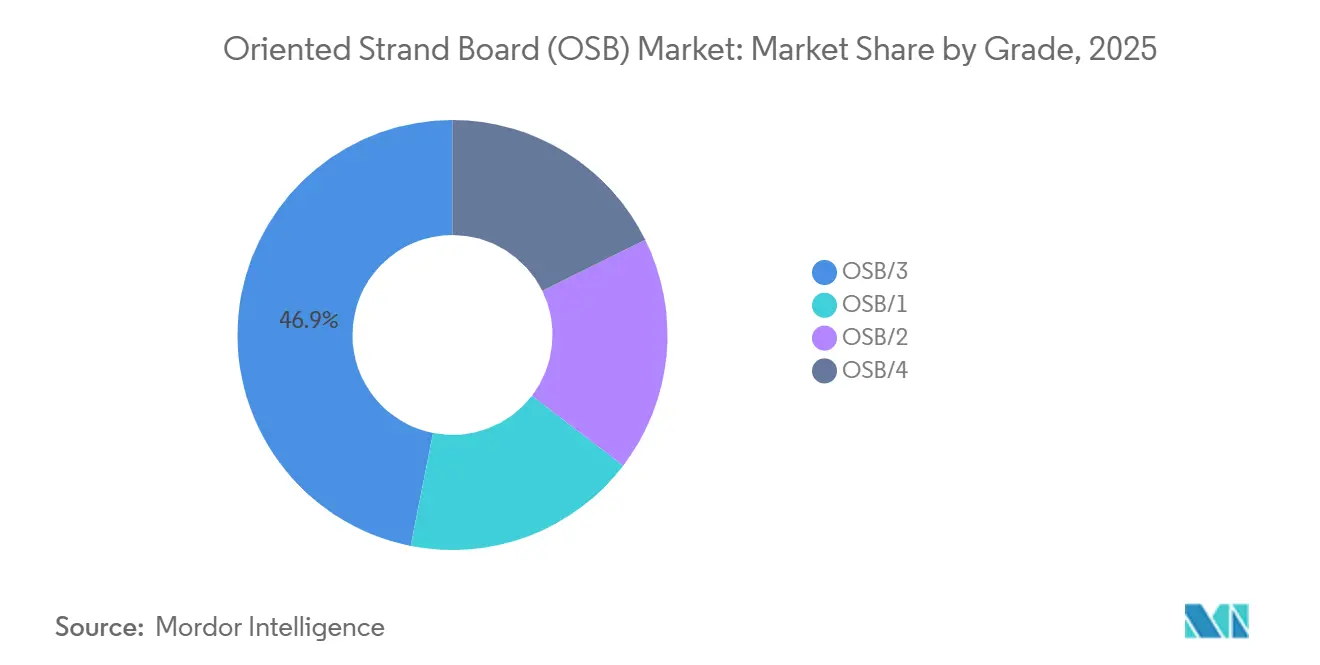

- By grade, OSB/3 captured 46.89% of the oriented strand board market share in 2025 while recording the fastest 4.61% CAGR through 2031.

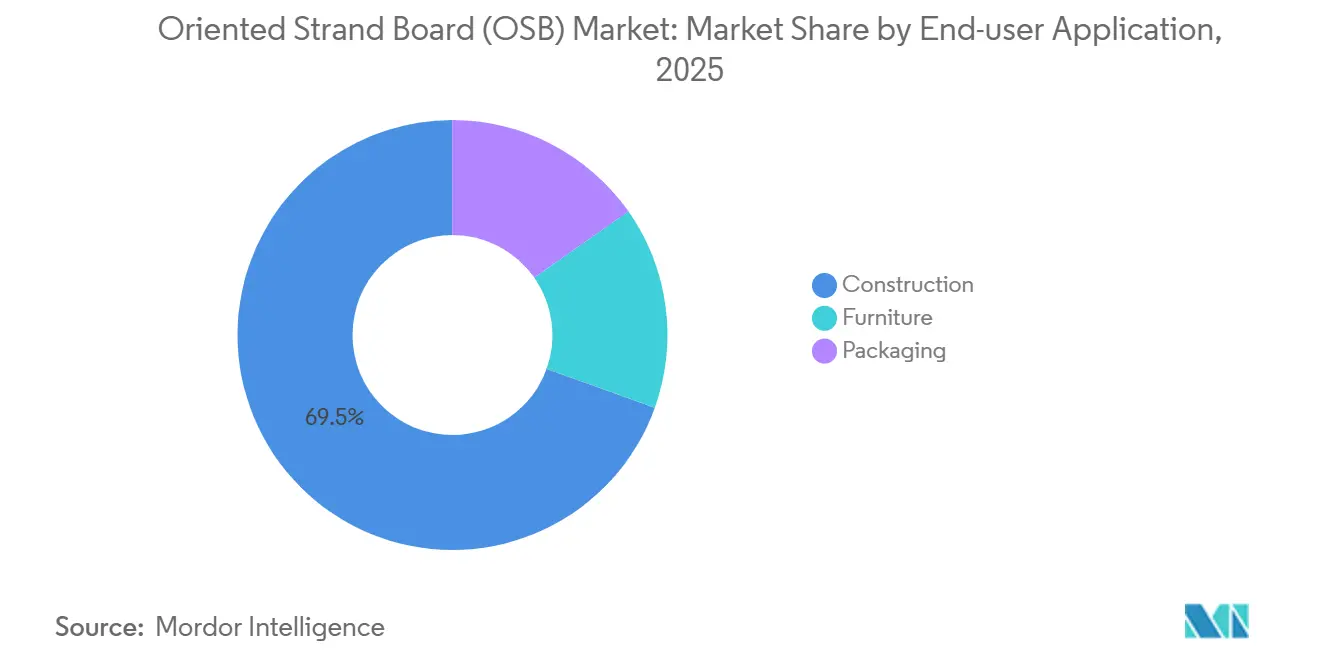

- By end-user application, the construction segment held 69.51% share of the oriented strand board market size in 2025 and is projected to expand at a 4.35% CAGR between 2026-2031.

- By geography, North America commanded 60.12% revenue share in 2025; Asia-Pacific is advancing at a 6.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Oriented Strand Board (OSB) Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-effective substitution for plywood | +0.9% | Global, with strongest uptake in North America and emerging Asia-Pacific markets | Medium term (2-4 years) |

| Expansion of global construction activity | +0.8% | North America, Europe, Asia-Pacific (India, Southeast Asia) | Long term (≥ 4 years) |

| Sustainability-driven demand for engineered wood | +0.7% | Europe, North America, with spillover to APAC urban centers | Long term (≥ 4 years) |

| Modular and prefab housing boom | +0.6% | North America, Europe, Japan, Australia | Medium term (2-4 years) |

| Carbon-credit incentives for wood-based materials | +0.4% | North America, EU, with pilot programs in Brazil and New Zealand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost-Effective Substitution for Plywood

OSB enjoys a consistent price discount compared to plywood. This price advantage is driving a steady shift in specifications for single-family homes and light-commercial projects. Builders in the U.S. Southeast and Canadian Prairies are increasingly opting for OSB in roof decking and wall bracing. OSB's uniform strand orientation provides reliable shear resistance. Additionally, OSB's pre-cut trim packages reduce on-site scrap, translating to significant labor savings, especially in areas where minimum wages are high. While plywood still holds a niche for exterior uses demanding superior edge sealing, this limits OSB's practical share of the structural sheathing demand. However, with veneer-quality logs becoming scarcer and plywood mills grappling with rising raw-wood costs, the momentum favoring OSB is expected to continue in the medium term.

Expansion of Global Construction Activity

In 2025, overall construction output saw a modest growth. However, segments like residential and infrastructure, which have a heavy reliance on Oriented Strand Board (OSB), showcased stronger performance. Thanks to India's housing initiatives, which rolled out engineered wood-specified dwellings, residential construction surged. Meanwhile, as Vietnam expanded its expressways and Indonesia embarked on its new capital project, both undertakings leaned heavily on temporary formwork. Contractors, in these instances, showed a clear preference for reusable OSB panels over traditional plywood. Although China's property market slump led to a dip in annual OSB demand, the impact was somewhat mitigated. This was largely due to the redirection of North American and European OSB exports towards India and ASEAN markets. Thus, the trajectory of the OSB market is increasingly tied to the construction activities in emerging Asia, rather than being dominated by any single nation.

Sustainability-Driven Demand for Engineered Wood

Regulatory carbon-credit mechanisms are transforming OSB panels into measurable carbon sinks. These credits finance resin upgrades and kiln electrification. In the EU, public projects must source net-negative embodied-carbon materials from 2028, a requirement OSB meets when timber is FSC- or PEFC-certified[1]European Commission, “Renewable Energy Directive III,” ec.europa.eu. Many North American mills already carry chain-of-custody certification, giving the region a head start in monetizing green premiums. These policies collectively underpin a long-run structural driver for the Oriented Strand Board market.

Modular and Prefab Housing Boom

In 2025, U.S. residential starts for factory-built housing rose as developers aimed for cycle time reductions[2]Modular Building Institute, “Modular Construction Market Analysis,” modular.org. To endure over-the-road transport, modular designs often necessitate thicker OSB, typically around 15.9 mm, increasing the panel usage per unit. Following the introduction of provincial incentives, Canada’s modular receipts surged. In Japan, a relaxation of timber-height limits led to a spike in OSB imports. The top ten modular builders in North America, now accounting for a significant share of total OSB purchases, are consolidating. This consolidation results in predictable off-take but also tightens mill margins due to bulk negotiations. Yet, despite this margin compression, the steady demand positions prefab as a robust growth avenue for the Oriented Strand Board market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Formaldehyde and VOC regulations tightening | -0.5% | Global, most stringent in California, EU, Japan, with spillover to export-oriented manufacturers | Short term (≤ 2 years) |

| Wood-fiber price volatility | -0.4% | North America, Europe, with spillover to import-dependent Asia-Pacific markets | Medium term (2-4 years) |

| CLT adoption stealing structural share | -0.3% | North America, Europe, urban centers in Asia-Pacific where mid-rise timber construction gains regulatory approval | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Formaldehyde and VOC Regulations Tightening

California's CARB Phase 2 limits are steering OSB mills towards ultra-low-emitting resins. This shift comes despite current rules exempting panels, as major retailers demand consistent compliance across all products. Transitioning from phenol-formaldehyde to MDI increases resin costs, a squeeze that smaller mills find hard to absorb. The EU's E1 ceiling, mandated since January 2025, has compelled numerous Turkish and Russian exporters to either retrofit or exit, leading to a reduction in external supply. Japan's stringent indoor-air standards further curtail the use of unsealed OSB. While major producers with their own resin plants navigate these changes with ease, the evolving regulations are hastening consolidation and, in the short term, stunting the growth of the Oriented Strand Board market.

Wood-Fiber Price Volatility

In 2025, the cost of strand fiber, which constitutes half of the OSB manufacturing expense, experienced a peak-to-trough surge. This spike was driven by sawmill curtailments that reduced the supply of residual chips, coupled with heightened energy demand for biomass, which in turn tightened pulpwood markets. Stumpage prices for southern yellow pine in the U.S. Southeast increased year-on-year. Concurrently, aspen log prices in the Lake States and Prairies rose, fueled by competition from CLT plants for similar grades. Mills situated more than 150 km from timber stands faced additional delivered costs due to diesel surcharges. While only a small percentage of producers utilize fiber-hedging instruments, leaving the majority vulnerable to quarterly price fluctuations, this sustained volatility could dissuade new green-field projects and moderate the long-term CAGR for the Oriented Strand Board market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: OSB/3 Anchors Load-Bearing Demand

OSB/3 held 46.89% of 2025 volume and is forecast to lead the Oriented Strand Board market at a 4.61% CAGR through 2031. With a load-bearing, moisture-resistant certification, OSB/3 caters to a significant portion of North American and European sheathing demands. This capability negates the need for separate dry- and humid-grade inventories. While OSB/4, tailored for high-moisture structural applications, captures a smaller market share, it is witnessing growth driven by code requirements in coastal regions prone to hurricanes and typhoons. OSB/1 and OSB/2, holding a notable market share, are lagging behind, indicating a potential phase-out as builders gravitate towards higher-performing grades.

Even with a cost increase, the rising use of MDI resins in OSB/3 and OSB/4 not only secures LEED and BREEAM credits but also boosts average selling prices. In contrast, smaller mills without resin integration are leaning towards OSB/1 and OSB/2. This trend underscores a two-tier dynamic in the Oriented Strand Board market, where grade leadership increasingly aligns with environmental compliance.

By End-User Application: Construction Dominates Volume

Construction absorbed 69.51% of 2025 consumption and will advance at a 4.35% CAGR, preserving its role as the central demand pillar for the Oriented Strand Board market. Wall and roof sheathing, making up a significant portion of construction usage, benefit from OSB's dimensional stability, which minimizes fastener pop and drywall cracking in engineered frames. Meanwhile, concrete formwork, despite its smaller volume, is witnessing the fastest growth, as contractors increasingly favor panels that can be reused for up to a dozen pours.

Furniture, driven by the appeal of visible strands in budget-friendly residential décor, accounts for a notable share of the volume and is growing steadily. Packaging holds a considerable share; lighter OSB pallets not only reduce export freight costs but are also starting to replace solid-wood alternatives in the supply chains of electronics and automotive parts. While other end uses diversify the market, construction remains the dominant force shaping the future of the Oriented Strand Board market.

Geography Analysis

North America controlled 60.12% of the 2025 volume, buoyed by the operations of numerous mills and a robustly integrated timber supply chain. However, its growth trails behind global averages. This sluggish growth is attributed to rising mortgage rates in the U.S., which dampen single-family permits, and increasing stumpage fees in Canada. Consequently, while the market size for Oriented Strand Board (OSB) in North America stabilizes, it continues to enjoy high margins, thanks to its geographical advantages.

Asia-Pacific, holding a significant market share, is on a growth trajectory with a 6.28% growth rate through 2031. The momentum in India can be largely credited to the Pradhan Mantri Awas Yojana, which has significantly boosted OSB consumption. Meanwhile, both Vietnam and Indonesia are channeling substantial infrastructure investments into expressways and new cities, emphasizing formwork-heavy constructions. Even amidst a property correction in China, infrastructure projects in the western provinces are sustaining a baseline demand. However, with South and Southeast Asia's reliance on imports, there's a notable landed-cost premium. This scenario presents a lucrative opportunity for local investors considering green-field capacities.

Europe, with a steady market share, is witnessing consistent growth. The push for near-zero-energy buildings is driving a surge in timber-frame constructions. Yet, challenges loom with stringent resin regulations and a tight pulpwood supply, both of which are pressuring profit margins. South America, capturing a modest market share, is on a growth path. Brazil, in particular, is capitalizing on its plantation eucalyptus, turning it into a lucrative export for OSB. In the Middle East and Africa, holding a modest share, there's a heavy reliance on imports, especially for large-scale formwork in ambitious giga-projects. While high freight costs pose challenges, the buoyancy from sustained oil revenues promises a robust pipeline for long-term construction endeavors.

Regulatory Landscape

OSB producers work within a tightening emissions and product-compliance framework that increasingly ties market access to verified low-emitting resins and third-party certification. In the United States, TSCA Title VI (Formaldehyde Standards for Composite Wood Products Act) sets national formaldehyde emission limits for composite wood products, including OSB, influencing resin selection and documentation practices for both domestic and imported panels.

Air emissions rules are also evolving for composite wood manufacturing. In July 2026, the US Environmental Protection Agency finalized updates to the National Emission Standards for Hazardous Air Pollutants (NESHAP) for plywood and composite wood products, reinforcing compliance requirements for panel plants and their control technologies. Export-facing producers also monitor formaldehyde classes and marking schemes used in key importing regions, including EU E1-related expectations and PS 2 performance standard alignment, since procurement policies and retailer specifications often demand uniform compliance across product lines rather than market-by-market formulations.

Value Chain Analysis

The OSB value chain begins with wood fiber procurement (pulpwood and small-diameter logs, plus residuals where available) and extends through resin and additive supply (primarily phenol-formaldehyde and MDI binders, plus waxes), panel manufacturing, distribution, and downstream fabrication across construction, furniture, and packaging. Production economics depend heavily on proximity to timber baskets and stable delivered-fiber costs, which is why mills are typically sited in timber-rich regions to limit haul distance and exposure to diesel-driven freight swings.

Core manufacturing steps include log conditioning and debarking, strand/wafer production, drying and screening, resin and wax blending, multi-layer mat formation, hot pressing, and finishing or cutting. Standards and compliance requirements, such as PS 2 in the United States and EN 300/EN 13986 alignment in Europe and the United Kingdom, shape quality systems, labeling, and testing cadence. As formaldehyde and VOC constraints tighten, mills generally shift to lower-emitting resin systems, notably MDI, alongside tighter process control. Distribution is typically routed through building-products dealers and large retail channels for sheathing and underlayment, with project-driven demand from modular builders and formwork users increasing the value of consistent thickness tolerances, reliable logistics, and certified chain-of-custody material flows.

Competitive Landscape

The oriented strand board market is moderately consolidated. Instead of capacity races, producers now focus on disciplined curtailments and resin-technology upgrades. West Fraser’s 2026 indefinite closure of its High Level mill, a calculated pullback that steadied benchmark prices. IKEA plans backward integration at its Romanian complex, signaling how large downstream users may enter production to control costs and ESG compliance. Hybrid OSB-CLT panels under patented development by Huber Engineered Woods aim to cut mid-rise structural costs while preserving fire ratings, a sign that composite solutions could blur traditional panel boundaries.

Oriented Strand Board (OSB) Industry Leaders

West Fraser

Louisiana-Pacific Corporation

Kronoplus Limited

Weyerhaeuser Company

EGGER

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clearer gap is opening between commodity sheathing and higher-performance, compliance-forward OSB solutions that reduce onsite labor and simplify code or program conformance. Integrated functional layers, such as airtight or vapour control components, and fire-retardant treated OSB target energy-efficient construction and stricter fire-safety specifications, while also helping producers move away from pure cycle-driven commodity dynamics. In 2026, this product activity is visible, including MEDITE SMARTPLY commercializing an OSB/3 panel with an integrated vapour control layer for airtight construction and LP Building Solutions advancing fire-retardant treated OSB offerings.

On the supply side, the most actionable opportunities concentrate in brownfield modernization and conversion projects that lift yield, reduce energy intensity, and align with emissions compliance, rather than focusing only on greenfield mill builds. In North America, reinvestments and expansions announced for existing sites include RoyOMartin-backed capacity expansion financing in Texas and a modernization program at Georgia-Pacific's Englehart OSB facility in Ontario, which includes new thermal energy systems and a stated capacity uplift. In Europe, conversion-based capacity and mix optimization is also in view, such as Swiss Krono's move to convert a particleboard line in France to OSB. At the same time, resin and binder innovation, including lignin-based binders, supports a pathway to meet tightening indoor-air requirements and embodied-carbon procurement rules without relying only on MDI cost pass-through.

Recent Industry Developments

- July 2026: Swiss Krono initiated a conversion of its particleboard line at the Sully-sur-Loire plant in France to OSB production, aiming to reconfigure its product mix after disruption at the site. The move adds a sizable potential OSB supply lever in Europe and signals continued interest in lower-risk conversions versus greenfield projects.

- December 2025: West Fraser decided to halt operations at its High Level, Alberta OSB mill, with a shutdown planned for spring 2026 following a wind-down and use of existing log supply. The action removed 860 million square feet (3/8-inch basis) of capacity, reinforcing the industry shift toward curtailments to stabilize pricing after earlier volatility.

- December 2024: Kronospan inaugurated a EUR 200 million OSB mill in Rivne, Ukraine, adding 700,000 cubic meters of annual capacity. This investment expanded Eastern European OSB output potential and introduced an additional regional source for construction and industrial panel demand.

Research Methodology Framework and Report Scope

Market Definition and Coverage

In this methodology, the market covers oriented strand board (OSB) production and consumption measured as finished panel volume, expressed in cubic meters, across major regions and key countries. It focuses on demand tied to construction activity, furniture manufacturing, and packaging needs.

Scope exclusions: We exclude downstream installation labor, fasteners, coatings, and broader engineered wood panels that are not OSB.

Segmentation Overview

- By Grade

- OSB/1

- OSB/2

- OSB/3

- OSB/4

- By End-user Application

- Construction

- Floor and Roof

- Wall

- Door

- Column and Beam (Shuttering)

- Staircase

- Other Constructions

- Furniture

- Residential

- Commercial

- Packaging

- Food and Beverage

- Industrial

- Pharmaceutical

- Cosmetics

- Other Packaging

- Construction

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Thailand

- Indonesia

- Vietnam

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- NORDIC Countries

- Turkey

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- Qatar

- United Arab Emirates

- Nigeria

- Egypt

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean fact base on OSB supply, trade, and end use signals so the later math has a stable foundation. We lean on public sources such as FAO forestry databases, UN Comtrade customs statistics, US Census Bureau construction spending releases, Eurostat construction indicators, and government housing starts and building permits series in major countries.

To make the inputs usable, the data is standardized into comparable units, aligned by time period, and checked against manufacturer annual reports, investor presentations, and industry association publications on wood panels and structural panels. Where coverage is uneven, we also use patent databases and a paid subscription for company financials and intelligence to understand capacity additions, product mix changes, and regional exposure. These examples are not exhaustive, and other public sources were used for data collection, validation, and clarification as well.

Primary Interviews and Surveys

Primary work is used to pressure test assumptions on OSB grade mix, typical application shares, and how pricing moves with resin inputs, log costs, and construction demand. We speak with a mix of manufacturers, distributors, builders, and procurement teams across APAC, EMEA, and the Americas so regional demand patterns and trade flows can be reconciled with the desk dataset.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 13% | APAC: 40% |

| Mid tier: 52% | Functional/Unit leaders: 33% | EMEA: 36% |

| Smaller Players: 17% | Managers: 54% | Americas: 24% |

Market-Sizing & Forecasting

Sizing is built with a top-down approach where construction and housing indicators are translated into a demand pool for structural panels, and then narrowed to OSB using validated share assumptions. The total is then corroborated through selective bottom-up approximations like sampled mill capacities, capacity utilization ranges, and channel checks on OSB shipment direction, which helps us adjust for gaps where public production or trade series lag.

Key model inputs include housing starts and building permits, repair and remodeling activity, OSB imports and exports by major corridors, grade-level mix (OSB/1 to OSB/4), and average thickness and application intensity in construction. Price movement is handled as a supporting lens, mainly to explain volume switching versus plywood and regional substitution trends, rather than to force a value-only story.

For forecasting, we use scenario analysis supported by short-series time techniques such as exponential smoothing on demand indicators, and then align the outlook with what practitioners expect on near-term construction cycles and capacity ramp ups. Where bottom-up supply checks are incomplete for a country, we bridge using trade balances and regional consumption proxies, and then revalidate the implied per-capita usage with interview feedback.

Data Validation & Update Cycle

Outputs are cross-checked against independent signals such as net import trends, construction activity direction, and visible capacity announcements, and then variances are investigated before sign-off. When a gap is found, assumptions are revisited, the math is rerun, and follow-up calls are triggered if the movement is material.

Every dataset and calculation step goes through multi-stage analyst review so unit conversions, time alignment, and share assumptions stay consistent across regions. Reports are refreshed annually, and interim updates are made when major events occur, such as sharp construction slowdowns, new capacity start-ups, or trade policy shifts. Right before delivery, a fresh review pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's Oriented Strand Board Osb Market Estimate Compared With Other Published Estimates

It is normal to see different published market sizes for OSB because teams choose different units, coverage boundaries, and timing for the inputs they use. Some estimates are built as revenue markets, while others stay closer to physical board demand, which can quickly change the apparent size.

By tracking housing starts, trade flows in cubic meters, and grade mix, Mordor Intelligence keeps the sizing anchored to panel volume, while some sources lean on value-only reporting and broader application buckets that can fold in adjacent wood panel categories. Differences also come from how prices are converted across currencies, whether wholesale or end-user pricing is assumed, and whether a report is updated after a major swing in construction cycles or panel pricing.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 40.77 M (2025) | |

| Global Publisher A | USD 26.20 B (2024) | Uses revenue-based sizing with broad application groupings, which can reflect price assumptions and may not align to cubic meter demand tracking by grade and end use. |

| Industry Publisher B | USD 24.20 B (2025) | Reports market value with thickness and grade framing, but the conversion from volume to value depends heavily on assumed average selling prices and the chosen pricing point in the chain. |

The spread in the table is mainly explained by unit choice and scope handling, since a volume market in million cubic meters will not reconcile directly with a revenue market in USD without a clear and consistent price bridge. A practical way to interpret the results is to first align on whether the decision needs physical demand (capacity and trade planning) or value demand (pricing and revenue planning), and then compare estimates that are built on the same unit and boundary.

Key Questions Answered in the Report

How large will global demand for Oriented Strand Board be by 2031?

Consumption is forecast to reach 50.50 million cubic meters by 2031, growing at a 3.63% CAGR, from 42.25 million cubic meters in 2026.

Which grade leads global sales?

OSB/3 holds 46.89% of 2025 volume and is projected to remain dominant due to its load-bearing and moisture-resistant rating.

What drives Asia-Pacific’s rapid growth?

India’s affordable-housing programs and Southeast Asia’s infrastructure projects underpin a 6.28% CAGR for the region through 2031.

What is the competitive outlook for producers?

Capacity discipline, vertical timber integration, and proprietary resin coatings are key levers that help the firms retain a moderate consolidation.

Page last updated on: