Organoids And Spheroids Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.29 Billion |

| Market Size (2031) | USD 2.55 Billion |

| Growth Rate (2026 - 2031) | 14.57% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

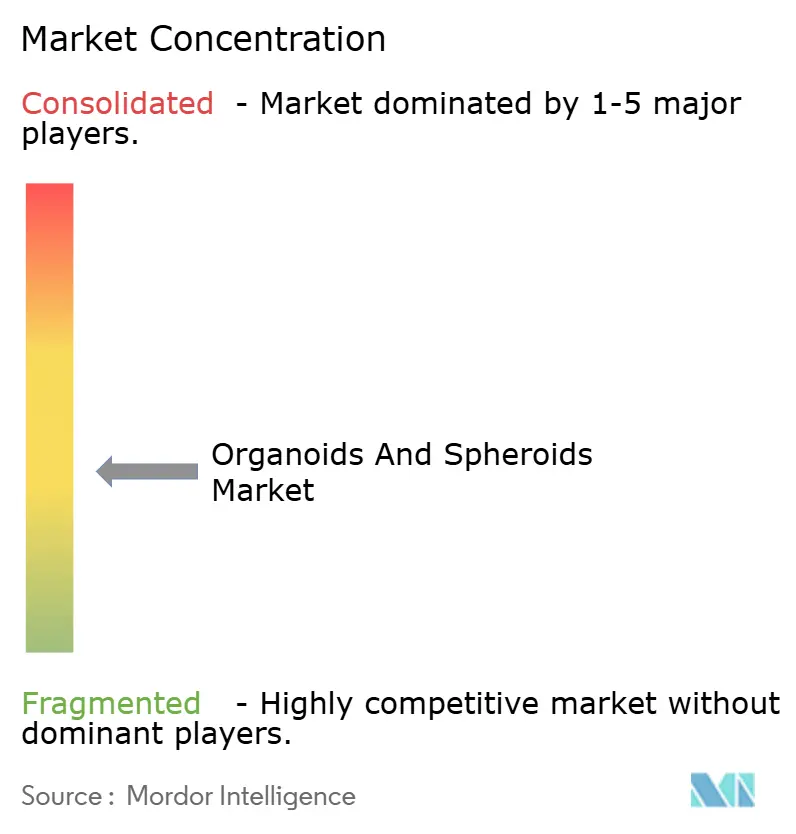

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Organoids And Spheroids Market Analysis by Mordor Intelligence

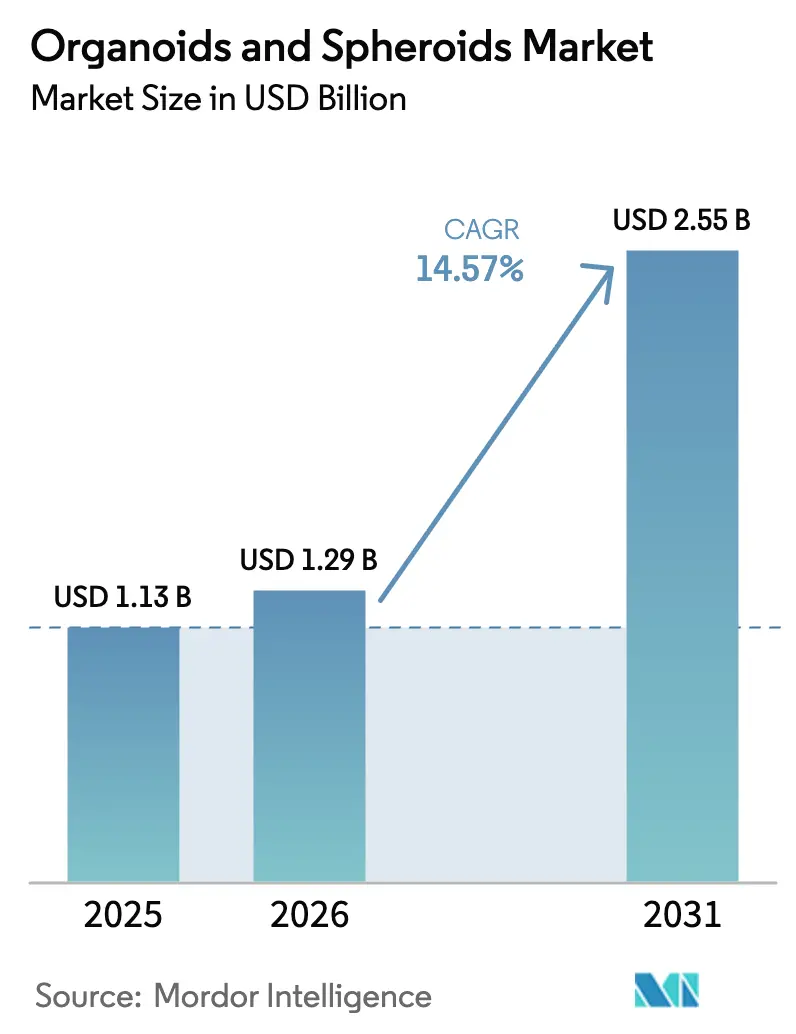

The organoids and spheroids market size in 2026 is estimated at USD 1.29 billion, growing from 2025 value of USD 1.13 billion with 2031 projections showing USD 2.55 billion, growing at 14.57% CAGR over 2026-2031. This robust trajectory reflects the pharmaceutical sector’s pivot toward human-relevant pre-clinical models, a shift accelerated by the FDA’s April 2025 decision to phase out mandatory animal testing for monoclonal antibodies. Organoids show 83.3% sensitivity and 92.9% specificity in forecasting patient treatment responses, highlighting their clinical predictability advantage over 2D cultures. Heightened public-sector funding—from ARPA-H’s USD 40 million PRINT program to NIH’s USD 2 million annual grants for auditory organoids—strengthens the technology base and shortens commercialization timelines. The organoids and spheroids market continues to benefit from automation advances such as the CellXpress.ai system, which enables high-throughput screening with lower labor input.

Key Report Takeaways

- By type, organoids led with 57.18% revenue share in 2025; spheroids recorded the fastest CAGR at 16.21% through 2031.

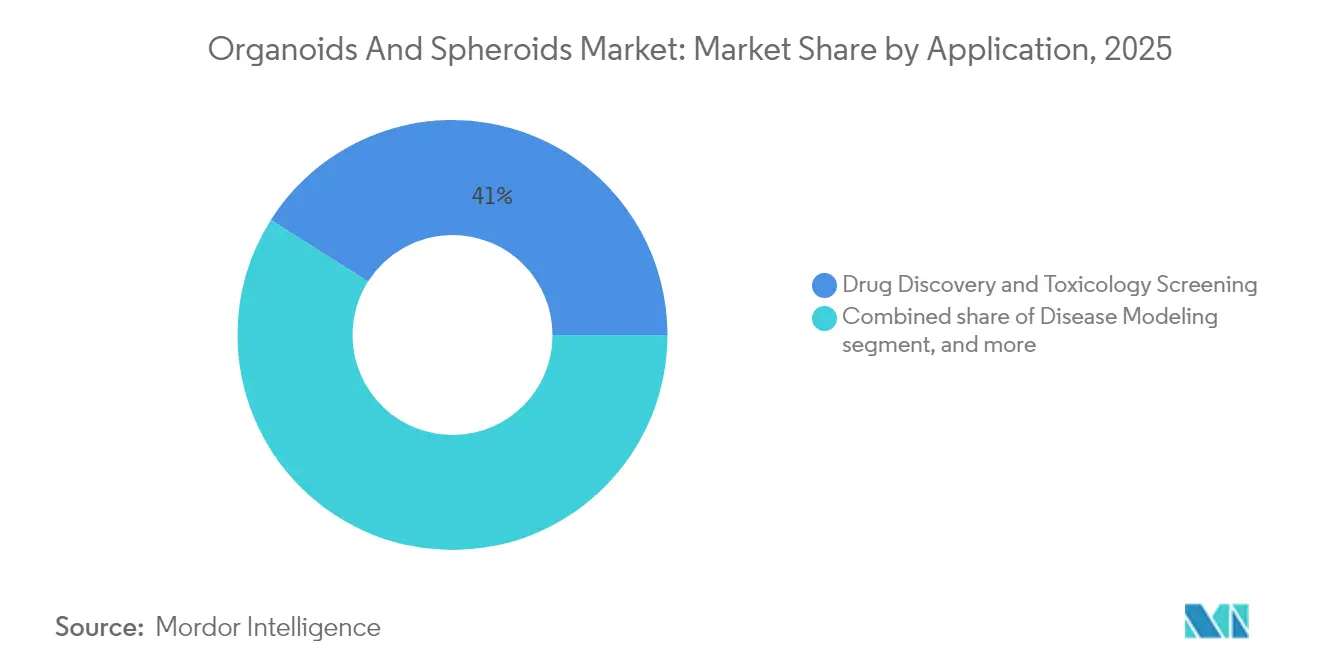

- By application, drug discovery and toxicology screening accounted for 41.02% of the organoids and spheroids market share in 2025, while personalized medicine is advancing at a 16.95% CAGR through 2031.

- By end user, pharmaceutical and biotechnology companies held 45.93% of the organoids and spheroids market size in 2025, whereas contract research organizations are projected to expand at 16.88% CAGR to 2031.

- By geography, North America contributed 39.98% of 2025 revenue; Asia-Pacific is forecast to register the highest regional CAGR of 15.21% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Organoids And Spheroids Market Trends and Insights

Driver Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of 3D cell culture in drug discovery | +3.2% | North America & EU lead; expanding adoption in Asia-Pacific | Medium term (2-4 years) |

| Rising demand for personalized medicine and precision oncology | +2.8% | Strongest in North America; rapid uptake in Asia-Pacific and Europe | Long term (≥ 4 years) |

| Increasing investment in regenerative medicine research | +2.1% | North America & EU core; spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Shift toward reducing animal testing in pre-clinical studies | +3.5% | Regulatory-driven in US & EU; global momentum | Short term (≤ 2 years) |

| Expanding government and private funding for organoid biobanks | +1.8% | North America & EU; emerging programs in Asia-Pacific | Medium term (2-4 years) |

| Emergence of automated high-throughput organoid platforms | +1.4% | Technology hubs in North America, EU, and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of 3D Cell Culture in Drug Discovery

Pharmaceutical developers report that legacy 2D assays misclassify up to 30% of compounds that later fail in Phase II trials, driving intense interest in 3D alternatives. The FDA Modernization Act 2.0 created a clear regulatory lane for organoid-based evaluations, slicing typical pre-clinical timelines by 18–24 months. CellXpress.ai automates organoid expansion and compound addition, cutting manual handling errors by 70%. Large firms now earmark as much as 12% of R&D budgets to human-relevant assays, reflecting risk-mitigation objectives. High-throughput organoid screens can process thousands of candidates concurrently, recapturing costs through lower late-stage attrition.

Rising Demand for Personalized Medicine and Precision Oncology

Patient-derived organoids (PDOs) enable oncologists to test drug panels on a patient’s tumor proxy before therapy begins; success rates of 91% have been reported for advanced pancreatic cancer[1]Gastroenterology Society, “Organoids in Pancreatic Cancer Precision Therapy,” gastroenterology.org. CRISPR-edited PDOs mirror individual tumor mutations, creating “patient avatars” that guide therapy matching. Expanding PDO biobanks maintain genetic diversity and accelerate cohort-wide drug sensitivity analysis. Health-system payers note that organoid-guided drug choice prevents ineffective treatments, reducing expenditure on non-responders. As clinical evidence mounts, leading cancer centers are embedding PDO workflows into routine molecular tumor boards.

Increasing Investment in Regenerative Medicine Research

The USD 40 million PRINT initiative funds kidney, liver and heart bioprinting for transplant studies[2]ARPA-H, “PRINT Program Overview,” arpa-h.gov. Private capital follows: Vivodyne closed a USD 40 million Series A to industrialize AI-driven human tissue testing. Stanford’s vascularized heart and liver organoids overcome diffusion limits and mature to organ-like size, marking a step toward transplantable constructs. Governments emphasize organoid research as a hedge against organ shortages, with 17 transplant candidates dying daily in the US alone. This multilateral funding environment reduces technology-validation risks and speeds the path from lab prototype to therapeutic use.

Shift Toward Reducing Animal Testing in Pre-Clinical Studies

In April 2025 the FDA signaled the end of compulsory animal testing for monoclonal antibodies, explicitly endorsing organoid and AI models. The European Medicines Agency is drafting parallel guidance, and industry adoption of organ-on-chip systems has doubled since 2021. Emulate reports a surge in inquiries as sponsors race to upgrade safety packages. Early adopters gain differentiation by embedding validated human-relevant assays before guidance becomes mandatory. Financial models show that avoiding long and controversial animal studies saves up to USD 5 million per investigational drug.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced 3D cell culture systems | -2.4% | Global; greatest barrier for small and mid-size biotechs | Short term (≤ 2 years) |

| Lack of standardized protocols and quality control | -1.8% | Global; regulatory uncertainty sharper in emerging markets | Medium term (2-4 years) |

| Stringent regulatory and ethical oversight | -1.9% | US, EU, and markets with strict bioethics frameworks | Medium term (2-4 years) |

| Limited scalability for clinical-grade manufacturing | -2.1% | Global; impacts regions lacking advanced bioprocess infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced 3D Cell Culture Systems

Automated bioreactors price between USD 100,000 and USD 500,000 per unit, keeping entry hurdles high for small firms. Organoid media can cost 5-10 times more than conventional 2D reagents; a single experimental run often exceeds USD 1,500 with specialty matrices. Labor expenses rise because operators must hold advanced tissue-culture skillsets, inflating overhead by 40-60%. CROs occasionally surcharge clients, limiting adoption among budget-constrained programs. Scalability gains from automation have begun lowering per-sample costs, but capital outlay remains a near-term restraint on market diffusion.

Lack of Standardized Protocols and Quality Control

Success rates span 15–20% for certain organ types and up to 87.5% for others, reflecting disparate lab procedures. Regulatory agencies need uniform reference standards, yet consensus on readouts—viability, morphology and functional assays—varies widely[3]International Society for Stem Cell Research, “Quality Standards for Organoid Research,” isscr.org. CEN/CENELEC’s organ-on-chip roadmap will not finalize before 2027, extending the harmonization timeline. Pharmaceutical sponsors hesitate to bank pivotal trials on methods that differ from site to site. Multi-site studies therefore allocate extra budgets to protocol alignment, delaying data packages for regulatory submission.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Biological Complexity Drives Organoid Leadership

Organoids captured 57.18% of 2025 revenue in the organoids and spheroids market, while spheroids posted a 16.21% CAGR to 2031. Organoids maintain genetic fidelity from source tissues, enabling disease-specific applications such as cystic-fibrosis airway models that predict patient response to CFTR modulators. Conversely, spheroids appeal to high-throughput screens because their production requires less growth-factor supplementation and shorter maturation times. Corning’s dual-mode platforms allow laboratories to alternate between spheroid and organoid setups without changing hardware, reducing capital duplication.

A converging trend involves hybrid 3D models: early-stage compound triage uses spheroids for throughput, followed by organoid validation for physiological depth. Hepatic organoids gain momentum in metabolic disease pipelines, whereas neural organoids benefit from vascularization breakthroughs that support extended culture. This two-tier strategy matches time-to-data with depth-of-insight, aligning with drug-discovery milestones.

By Application: Personalized Medicine Gains Traction

Drug discovery and toxicology screening remained the largest slice at 41.02% in 2025, but personalized medicine now shows the fastest expansion at 16.95% CAGR—reflecting rising clinical validation of PDOs in therapy selection. Safety testing benefits from the growing preference for the organoids and spheroids market size metrics linked to ADME&T workflows. Precision-oncology labs increasingly rely on biobanked PDOs for multi-drug sensitivity panels, integrating genomic and functional data to formulate treatment regimens. Regenerative-medicine applications, though nascent, secured fresh capital from insurers exploring curative-therapy cost savings.

Meanwhile, disease-modeling programs spread to metabolic, neurodegenerative and infectious-disease areas. Pancreatic islet organoids, for instance, show improved engraftment over beta-cell transplants, offering a potential curative path for diabetes. CRISPR-enabled organoids elucidate genotype-phenotype links at scale, accelerating gene-therapy target discovery.

By End User: CROs Outpace Internal Pharma Adoption

Pharmaceutical and biotech firms commanded 45.93% revenue in 2025, but CRO revenues are growing 16.88% per year, reflecting outsourcing economics. Large CROs, such as Charles River Laboratories, centralize PDO production, standardize assays and offer regulatory-compliant data packages, reducing client capex. Academic centers contribute foundational innovation but often license protocols to commercial partners for scale-up. Hospital pathology units begin incorporating PDO tests for refractory cancers, signalling a clinical-diagnostics frontier.

CRO expansion aligns with the organoids and spheroids market outlook by lowering the per-study cost for smaller biotechs that cannot justify full in-house 3D capacity. This tiered ecosystem distributes capabilities efficiently: discovery groups innovate, service providers scale, and clinical sites translate findings into patient care.

Geography Analysis

North America, at 39.98% market share in 2025, benefits from the FDA’s regulatory leadership, deep grant pools and an integrated supplier base. Major players like Thermo Fisher Scientific earmark USD 500 million of a broader USD 2 billion capex plan for R&D initiatives, including organoid and spheroid applications. Government collaboration accelerates scale-up programs; ATCC and NIH jointly curate standardized organoid reference lines, smoothing inter-lab reproducibility.

Asia-Pacific is projected to post a 15.21% CAGR to 2031—the fastest among regions—lifting the organoids and spheroids market size locally from USD 0.32 billion in 2022 to USD 0.88 billion by 2031. Technology transfer partnerships, exemplified by InSphero-Chayon, localize production, while government subsidies defray equipment import costs. Lower operating expenditure and a skilled talent pool draw Western companies to establish manufacturing hubs in Singapore, South Korea and China.

Europe maintains steady growth underpinned by strong academic-industry networks and a regulatory push for standardization. Merck KGaA’s acquisition of HUB Organoids integrates Dutch PDO expertise into a global life-science supply chain. The CEN/CENELEC roadmap seeks unified organ-on-chip criteria, likely setting a global benchmark once ratified. Smaller markets in the Middle East, Africa and South America remain emergent but attract pilot projects aimed at infectious-disease modeling using regional pathogen strains.

Competitive Landscape

The organoids and spheroids market is moderately fragmented, with an accelerating consolidation wave. Merck KGaA’s December 2024 purchase of HUB Organoids demonstrates how large suppliers absorb niche innovators to secure proprietary platforms. Thermo Fisher leverages its reagent and instrument breadth to bundle end-to-end 3D solutions, challenging single-product specialists. Competitive leverage increasingly hinges on validated datasets accepted by regulators; Emulate’s FDA ISTAND milestone for a liver-injury chip provides a notable moat.

Funding continues to stream toward automation and AI integration—Vivodyne’s USD 40 million Series A funds a 23,000-square-foot robotic laboratory focused on high-throughput human tissue testing. CN Bio’s USD 21 million raise pairs its PhysioMimix platform with global CRO Pharmaron, underscoring the strategic value of geographic reach. White-space opportunities remain in cost-down reagent formulations and unified QC software, where few players currently claim dominant IP positions.

Start-ups pursuing simplified, kit-based organoid protocols address smaller labs that lack advanced bioreactors, expanding the organoids and spheroids industry adoption funnel. Strategic partnerships between instrumentation giants and microfluidic specialists illustrate a shift toward integrated hardware-software ecosystems that lower operator skill barriers.

Organoids And Spheroids Industry Leaders

Cellesce Ltd.

InSphero AG

STEMCELL Technologies Inc.

Corning Incorporated

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Stanford researchers created vascularized heart and liver organoids, enhancing maturation and size for potential therapeutic use.

- May 2025: Vivodyne secured USD 40 million Series A to expand an AI-powered human tissue testing platform.

- April 2025: FDA announced plans to phase out animal testing mandates for monoclonal antibodies, endorsing organoid toxicity assays.

- April 2025: CN Bio partnered with Pharmaron to globalize organ-on-chip R&D on the PhysioMimix platform.

- April 2025: Thermo Fisher Scientific pledged USD 2 billion investment in US manufacturing, with USD 500 million for life-science R&D.

- March 2025: ARPA-H launched the USD 40 million PRINT program to bioprint organs on demand.

Global Organoids And Spheroids Market Report Scope

Organoids are 3D mini-organs grown from stem cells that mimic organ structure and function and are used for research on development and disease. Spheroids are simpler 3D cell clusters that study cellular behaviors like growth and drug responses.

The organoids and spheroids market is segmented into type, application, end user, and geography. By type, the market is segmented into organoids (intestinal organoids, hepatic organoids, pancreatic organoids, neural organoids, and other organoids {lung, kidney, and gastric, among others}) and spheroids (multicellular tumor spheroids, neurospheres, hepatospheres, mammospheres, and other spheroids {embryoid bodies, etc.}), application (disease modeling, drug discovery and toxicology screening, regenerative medicine, stem cell research, personalized medicine, and other applications {gene editing and immuno-oncology, among others}), end user (pharmaceutical and biotechnology companies, academic and research institutes, hospitals and diagnostic centers, contract research organizations {CROs}, and other end users {biobanks, stem cell banks}). By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The report also offers the market size and forecasts for 17 countries across the region. For each segment, the market sizing and forecasts were made on the basis of value (USD).

| Organoids | Intestinal Organoids |

| Hepatic Organoids | |

| Pancreatic Organoids | |

| Neural Organoids | |

| Other Organoids | |

| Spheroids | Multicellular Tumor Spheroids |

| Neurospheres | |

| Hepatospheres | |

| Mammospheres | |

| Other Spheroids |

| Disease Modeling |

| Drug Discovery & Toxicology Screening |

| Regenerative Medicine |

| Stem-Cell Research |

| Personalized Medicine |

| Other Applications |

| Pharmaceutical & Biotechnology Companies |

| Academic & Research Institutes |

| Hospitals & Diagnostic Centers |

| Contract Research Organizations (CROs) |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Organoids | Intestinal Organoids |

| Hepatic Organoids | ||

| Pancreatic Organoids | ||

| Neural Organoids | ||

| Other Organoids | ||

| Spheroids | Multicellular Tumor Spheroids | |

| Neurospheres | ||

| Hepatospheres | ||

| Mammospheres | ||

| Other Spheroids | ||

| By Application | Disease Modeling | |

| Drug Discovery & Toxicology Screening | ||

| Regenerative Medicine | ||

| Stem-Cell Research | ||

| Personalized Medicine | ||

| Other Applications | ||

| By End User | Pharmaceutical & Biotechnology Companies | |

| Academic & Research Institutes | ||

| Hospitals & Diagnostic Centers | ||

| Contract Research Organizations (CROs) | ||

| Other End Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast will spending on 3D cell culture platforms grow through 2031?

The organoids and spheroids market is projected to post a 14.57% CAGR, taking revenue from USD 1.29 billion in 2026 to USD 2.55 billion by 2031.

Which region offers the highest growth potential for suppliers?

Asia-Pacific is forecast to expand 15.21% per year, buoyed by cost advantages and rising government biotech investment.

What share do organoids hold compared with spheroids?

Organoids commanded 57.18% revenue in 2025, reflecting their higher biological complexity, while spheroids are catching up with a 16.21% CAGR.

Why are CROs gaining ground as end users?

CROs grow 16.88% annually because they let small-to-mid-size drug developers access organoid assays without heavy capital investment.

How is regulation affecting technology adoption?

The FDAÕs 2025 guidance to phase out certain animal tests is accelerating demand for validated organoid and organ-on-chip platforms across the development pipeline.

Page last updated on: