Organic Friction Modifier Additives Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

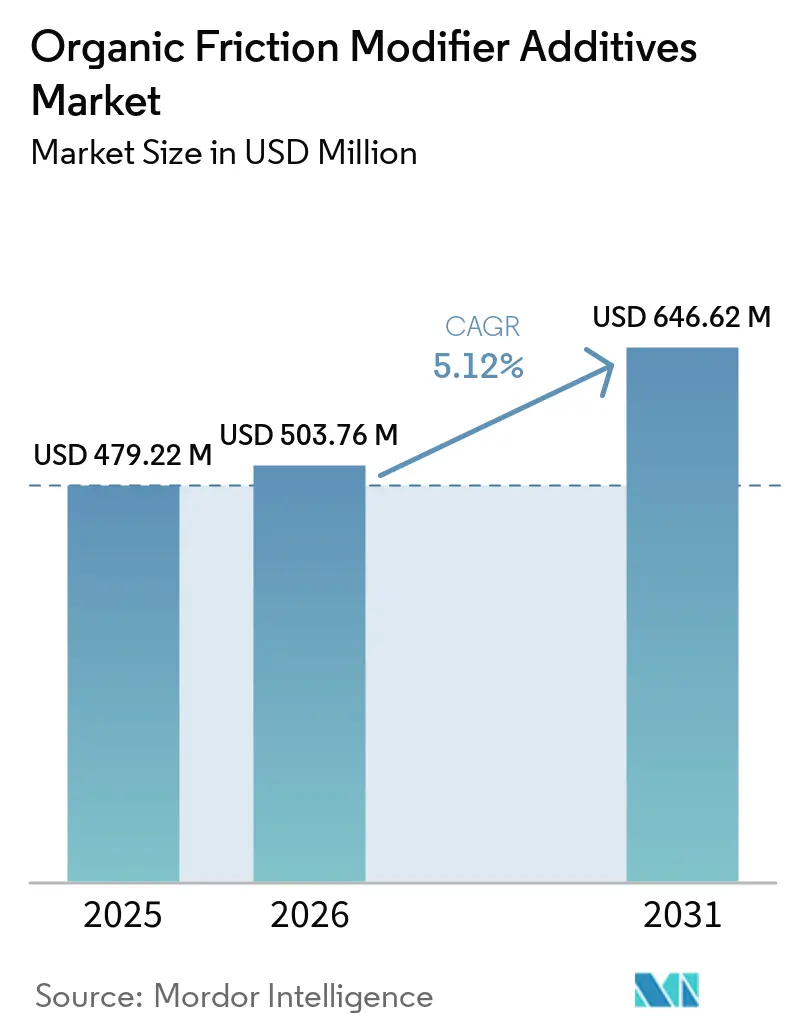

| Market Size (2026) | USD 503.76 Million |

| Market Size (2031) | USD 646.62 Million |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

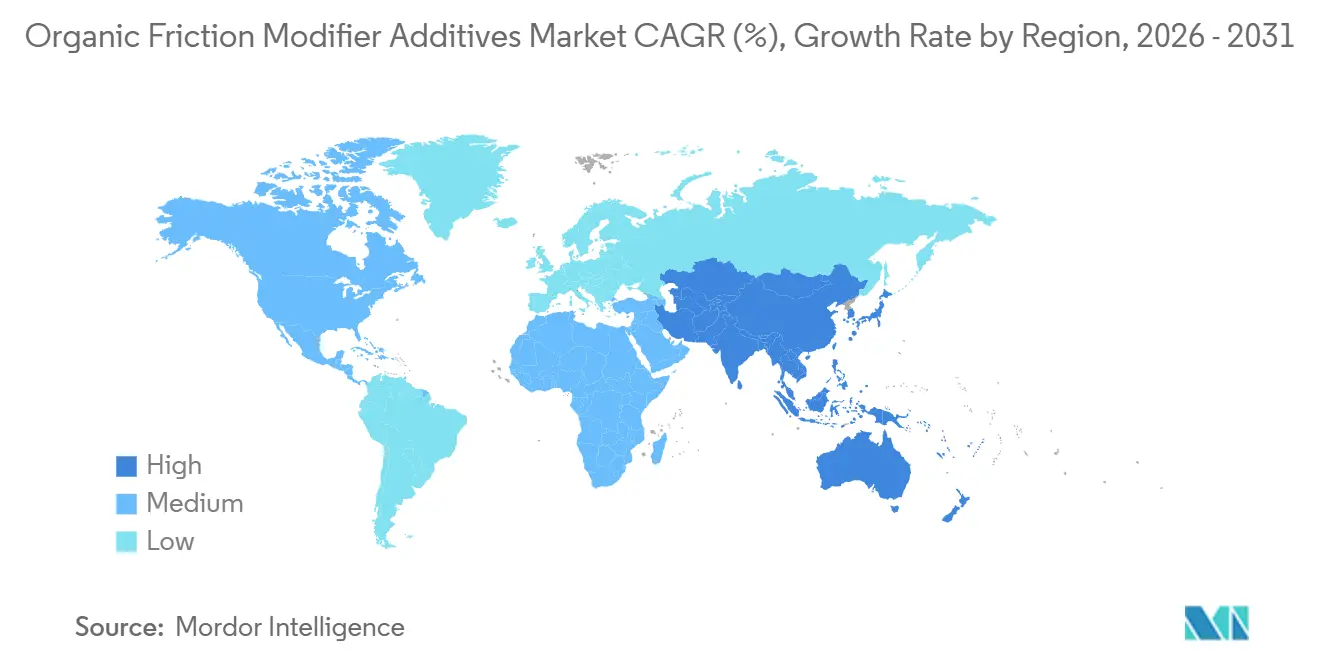

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

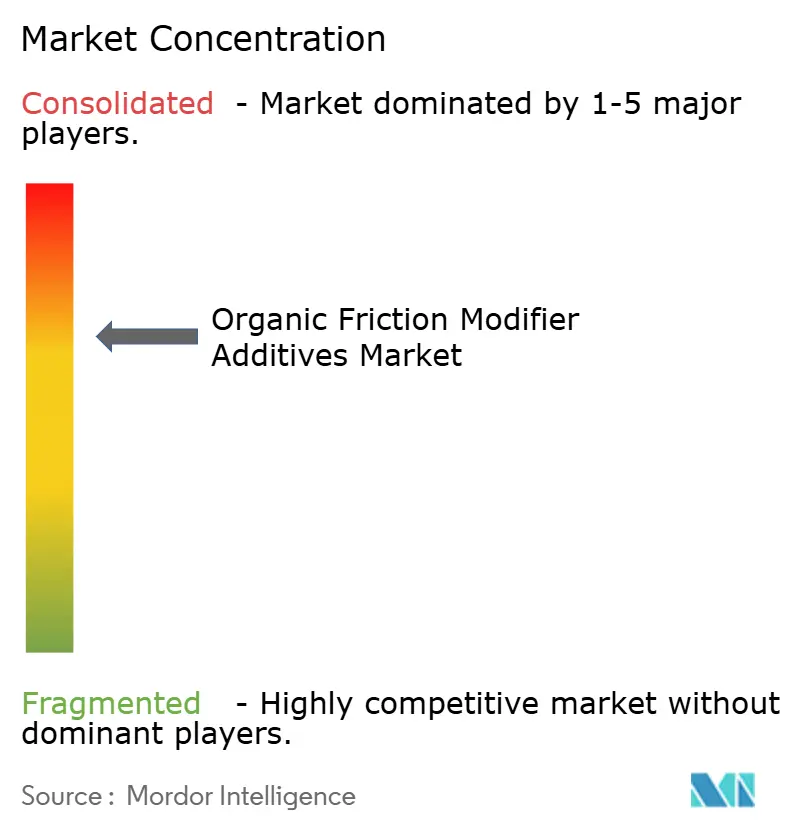

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Organic Friction Modifier Additives Market Analysis by Mordor Intelligence

The Organic Friction Modifier Additives Market size is projected to be USD 479.22 million in 2025, USD 503.76 million in 2026, and reach USD 646.62 million by 2031, growing at a CAGR of 5.12% from 2026 to 2031. Accelerating automotive electrification, stricter global emission rules that favor ash-free chemistries, and OEM moves toward 20,000-kilometer drain intervals are reshaping lubricant-additive demand. Transmission makers are specifying friction coefficients below 0.06 to curb clutch shudder, which is boosting the use of ester and amide molecules in dual-clutch and continuously variable fluids. Rapid gains in e-axle production require ultra-low-friction fluids with electrical-conductivity ceilings of 100 pS/m, pushing suppliers to introduce polyalphaolefin-soluble esters that remain stable at 150°C. At the same time, supply risks tied to palm-oil-based oleochemicals and upcoming European micro-plastics rules are steering formulators toward biodegradable feedstocks and multifunctional molecules that cut total treat rates.

Key Report Takeaways

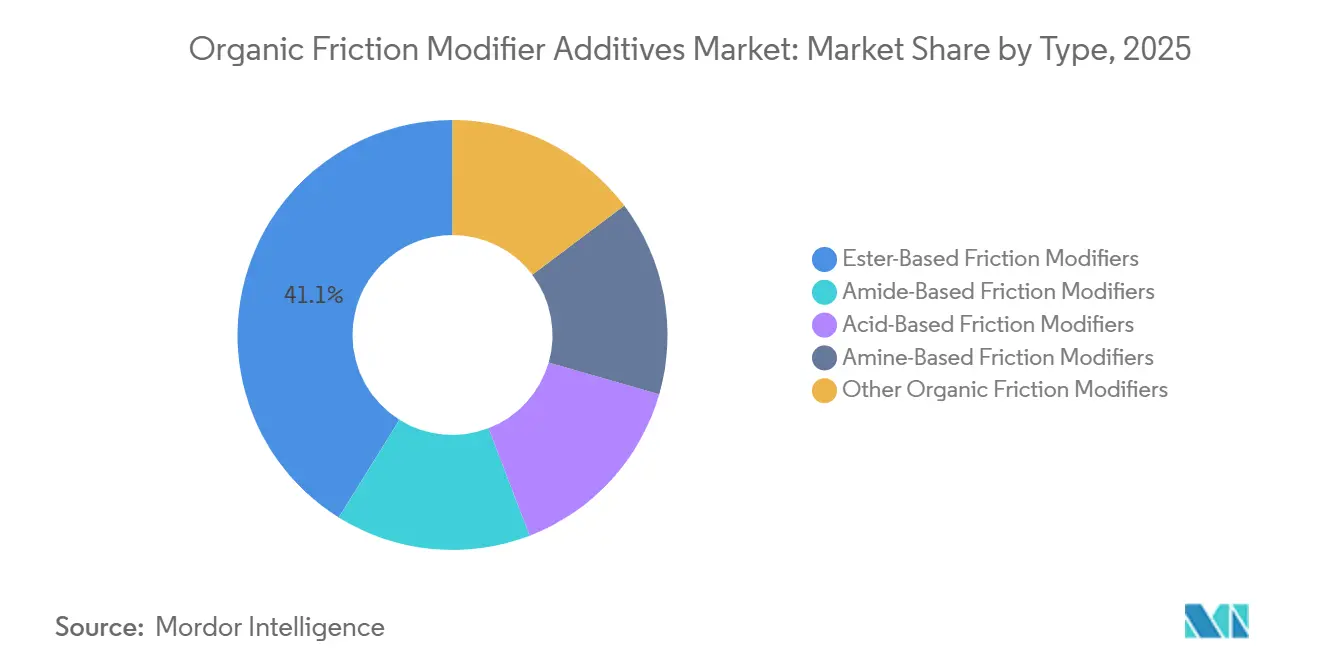

- By type, ester-based friction modifiers accounted for 41.11% of the organic friction modifier additives market share in 2025, whereas amide-based friction modifiers are poised for a 5.63% CAGR during the forecast period (2026-2031).

- By form, liquid held 83.34% of the organic friction modifier additives market in 2025, while solid (powder/dispersible) is set to expand at a 5.99% CAGR during the forecast period (2026-2031).

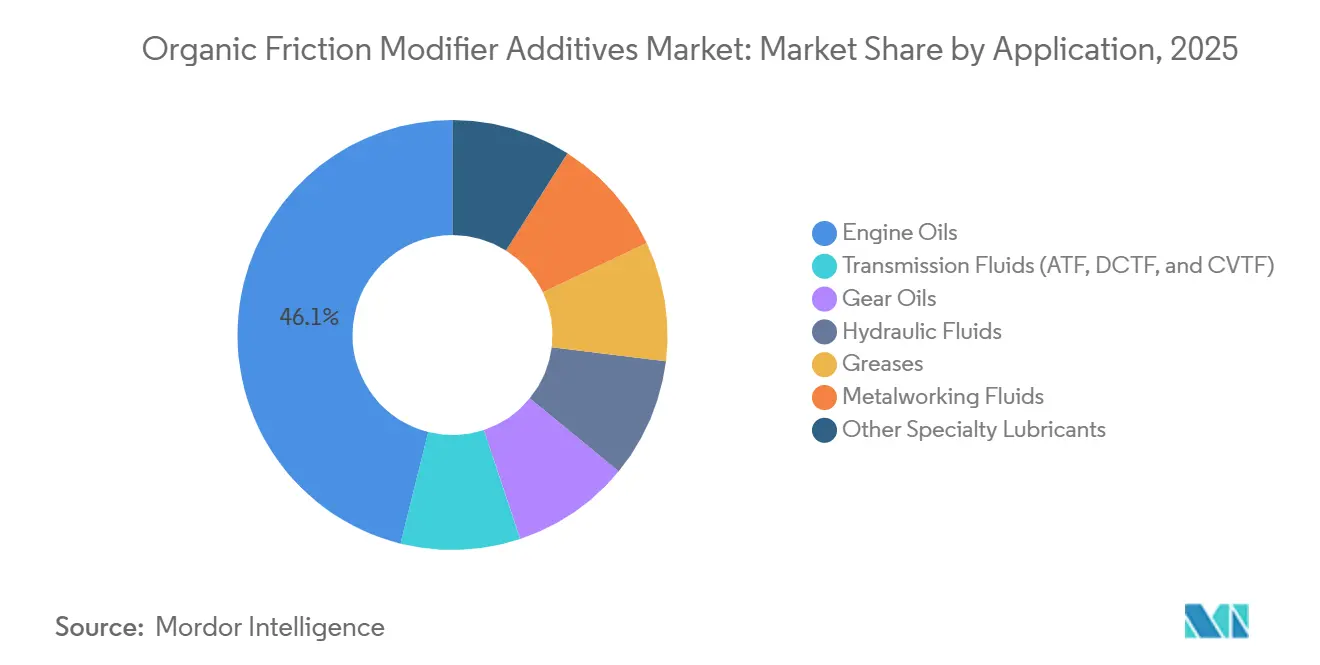

- By application, engine oils dominated with a 46.12% share of the organic friction modifier additives market size in 2025, and transmission fluids will advance at a 6.12% CAGR during the forecast period (2026-2031).

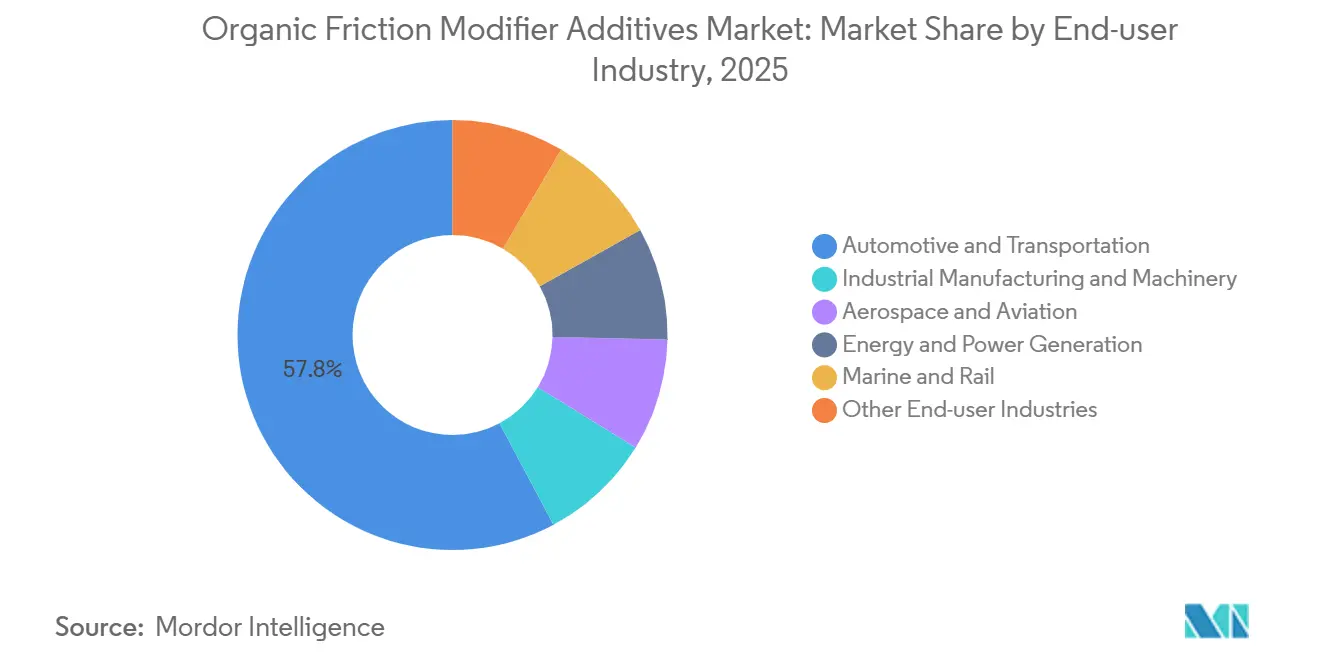

- By end-user industry, automotive and transportation controlled 57.78% of 2025 revenue, yet aerospace will post a 6.34% CAGR during the forecast period (2026-2031).

- By geography, Asia-Pacific led with 52.22% of 2025 revenue, and the region is forecast to grow at a 6.26% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Organic Friction Modifier Additives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter environmental regulations on engine-oil formulations | +1.2% | Global, with early enforcement in EU and China | Medium term (2-4 years) |

| Growing penetration of automatic and dual-clutch transmissions | +1.5% | APAC core, spill-over to North America and Europe | Short term (≤ 2 years) |

| Development of high-temperature, long-drain synthetic lubricants | +0.9% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Formulation synergies with ionic-liquid boosters in hybrid powertrains | +0.6% | North America, EU, Japan, South Korea | Medium term (2-4 years) |

| OEM warranty extensions for ultra-low-friction e-axle lubricants | +0.8% | Global, led by EU and China EV markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter Environmental Regulations on Engine-Oil Formulations

Regulatory agencies are capping phosphorus, sulfur, and sulfated ash, which forces blenders to shift from metallic to organic friction modifiers. The EU’s 2024 REACH reclassification of short-chain chlorinated paraffins created an immediate need for ashless alternatives[1]European Chemicals Agency, “Authorisation List Updates,” echa.europa.eu. The United States Environmental Protection Agency finalized Tier 4 limits in 2025 that require diesel lubricants compatible with after-treatment devices. China’s GB 11121-2024 specification restricts phosphorus to 0.06%, making glycerol mono-oleate and PIB-succinimide derivatives indispensable. These simultaneous rules are accelerating the adoption curve for ester and amide molecules that hold friction coefficients below 0.08 without poisoning catalytic hardware. Suppliers that completed field trials ahead of the 18-month OEM approval cycle now enjoy first-mover pricing power.

Growing Penetration of Automatic and Dual-Clutch Transmissions

Automatic and dual-clutch units represented 68% of 2025 passenger-car builds, up seven points from 2023, with Asia–Pacific adding most of the volume. Dual-clutch boxes rely on organic modifiers dosed at 0.3%-0.8% to keep clutch friction steady between -40°C and 150°C. Chinese output reached 5.5 million dual-clutch cars in 2025 as BYD and Geely moved to seven- and eight-speed designs to meet 4.0 L/100 km fuel targets. Continuously variable units need thermally robust amides to stabilize belt traction, while North American OEMs pushed eight- and ten-speed automatics to 42% penetration, further lifting demand. Longer 10-year warranties oblige fluids to hold oxidation stability beyond 100,000 km, which is reshaping additive treat packages.

Development of High-Temperature Long-Drain Synthetic Lubricants

Synthetic base stocks now cover 38% of global engine oil volume as OEMs stretch drains to 20 000 km. Conventional oleic-acid esters hydrolyze above 120°C, but branched esters derived from TMP and pentaerythritol withstand 200°C, enabling 30,000-km diesel drains in Europe. North American heavy-duty fleets use API CK-4 oils that must last 150,000 miles, a target met by synthetic esters paired with hindered-phenol antioxidants. Ionic-liquid candidates showed friction coefficients below 0.05 at 150°C in Oak Ridge tests, yet the cost-per-kilogram remains ten times higher than standard esters[2]Oak Ridge National Laboratory, “Ionic Liquid Tribology,” ornl.gov. BASF and Cargill are scaling production to close the gap by 2028.

Formulation Synergies with Ionic-Liquid Boosters in Hybrid Powertrains

Hybrid vehicle output hit 14.2 million units in 2025, raising focus on stop-start friction spikes. Ionic liquids lack vapor pressure and build durable boundary films that cut friction by 40% relative to ZDDP in boundary regimes. Toyota and Honda field tests showed 8% battery-life gains from 2% ionic-liquid dosages. Phosphate esters complement ionic adsorption, enabling 0W-16 viscosity grades with sub-0.06 friction at 40°C. EU PFAS proposals may still delay commercialization past 2027 for fluorinated anion variants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material supply risks (oleochemicals, esters, amines) | -0.7% | Global, concentrated in APAC sourcing | Short term (≤ 2 years) |

| Compatibility issues with certain base oils and additive packs | -0.4% | Global, particularly North America heavy-duty segment | Medium term (2-4 years) |

| Pending EU micro-plastics legislation on long-chain alkyl esters | -0.3% | EU, with potential spill-over to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Supply Risks (Oleochemicals, Esters, Amines)

Palm-oil levies in Indonesia lifted oleic-acid prices by 34% in Q1 2025 and squeezed additive margins for blenders without integrated feedstock positions. Only 40% of spot palm oil meets the less than 2 mg KOH/g acid-value spec, forcing upstream purification or premium sourcing. Propylene-oxide capacity trails downstream needs, creating a looming 1.1-million-ton shortfall by 2031, which is inflating costs for amine modifiers. Petronas Chemicals opened a 50,000-tons/year oleochemical hub in Johor in 2025 to secure a captive supply and cut volatility. Castor oil and algae pathways are still under 5% of feedstock, but pilot projects aim for 10% by 2028.

Compatibility Issues with Certain Base Oils and Additive Packs

Ester modifiers precipitate in Group I stocks with high aromatics, clogging filters and impairing heat transfer. Lubrizol tests showed 18% friction-loss when glycerol mono-oleate met sulfur above 300 ppm in Group II bases. Competitive adsorption with ZDDP can cut wear protection by 25%, which is problematic for diesel fleets still running 1,200 ppm P packages. Afton’s patent for a borated ester that blends friction and anti-wear in one molecule may resolve part of the conflict, but commercial release awaits 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Ester Dominance Amid Rising Cost-Efficient Amides

Ester-based molecules secured 41.11% of the organic friction modifier additives market share in 2025, owing to excellent thermal stability and low-viscosity compatibility demanded by GF-6B and ACEA C5 oils. Glycerol mono-oleate and sorbitan esters deliver friction coefficients near 0.07 at 0.5%-1.0% dosages, whereas di(2-ethylhexyl) adipate has become the e-axle benchmark because of low conductivity. Amide products priced 25% below esters are catching up fast, led by oleamide in transmission fluids that promise a 5.63% CAGR during the forecast period (2026-2031).

Amide durability tapers above 130°C, which limits usage in high-temperature sump environments. Mixed ester–amine hybrids under BASF’s 2025 patent aim to merge ester heat stability with amine polarity for friction below 0.06 in 0W-12 oils. Acid-based modifiers stay niche in greases and metal-forming fluids, while multifunctional polymeric dispersants are gaining share in heavy-duty diesel oils that require simplified additive slates.

By Form: Liquids Prevail as Solids Surge in Sealed Bearings

Liquid products comprised 83.34% of the organic friction modifier additives market size in 2025 because they blend easily into Group III and polyalphaolefin oils through automated dosing. Precise treat-rate control down to 0.3% lets OEMs target exact friction curves, which secures strong demand.

Solid (powder/dispersible) is set for a 5.99% CAGR to 2031, mainly through molybdenum disulfide and graphite packages used in sealed EV bearings. Nanometer-scale PTFE introduced by Shamrock in 2025 resists sedimentation for 12 months and meets servo-valve cleanliness in aerospace hydraulics. EU micro-plastics policy could, however, cap further carbon-based powder growth if particle persistence triggers new disposal rules.

By Application: Transmission Fluids Accelerate on DCT Rollout

Engine oils held 46.12% of demand in 2025, thanks to fleet size, yet transmission fluids are projected to grow at 6.12% CAGR, outpacing the broader organic friction modifier additives market. Dual-clutch boxes need stable 0.06-0.08 friction coefficients across wide temperature spans, driving 0.5%-0.9% treat levels of ester-amide blends.

Continuously variable and eight-speed automatics in China and North America underpin additive growth. Gear oils and hydraulic fluids together lean on biodegradable esters for offshore wind and forestry rigs. Greases increasingly rely on MoS₂ powders to extend EV wheel-bearing life beyond 100,000 km.

By End-user Industry: Automobiles Dominate while Aerospace Climbs Fast

Automotive and transportation consumed 57.78% of the 2025 demand of the market. Electric-vehicle penetration adds e-axle fluid demand that compounds engine-oil requirements in hybrids, thereby holding the segment’s leadership.

Aerospace lubricants are advancing at 6.34% CAGR for the forecast period (2026-2031) on the back of 1,340 aircraft deliveries in 2025 and stricter MIL-PRF-23699 standards that mandate ashless additives capable of 200°C turbine operation. Energy, marine, and off-highway machinery are moving toward biodegradable hydraulics and electrified drivetrains, which presents fresh volume for organic friction modifier additives industry suppliers.

Geography Analysis

Asia-Pacific led with 52.22% of 2025 revenue and is forecast for a 6.26% CAGR through 2031. China built 30.5 million vehicles, including 9.8 million EVs, each unit demanding low-viscosity oils that depend on organic friction modifiers for compliance with China-6b limits. India’s 5.8 million-unit output and 21.2 million two-wheelers also adopt BS-VI Phase 2 oils that cap particulates at 4.5 mg/km. ASEAN investment surged after Petronas opened a regional additive hub in Johor in 2025. Japan and South Korea continue as innovation centers for ionic-liquid hybrids.

In North America, the United States light-vehicle builds climbed to 10.8 million, while Class 8 trucks hit 320,000 units and now need API CK-4 oils containing ashless modifiers for after-treatment durability. Canadian winter grades such as 0W-16 rely on ester friction modifiers for -40°C pumpability. Afton doubled its Monterrey capacity in 2025 to serve Mexican exports. EPA Tier 4 off-road mandates and California LEV rules are prompting faster metal-free adoption.

In Europe, Germany’s 3.8 million vehicles, including 1.2 million EVs, require ultra-low-friction e-axle fluids. Pending micro-plastics limits triggered EUR 45 million in research and development for biodegradable esters by BASF and Lubrizol in 2025. Norway’s 90% EV share spurred demand for -30°C-capable e-axle lubricants. South America’s market share is led by Brazil’s 2.3 million vehicles, while the Middle East and Africa share is supported by mining and petrochemical hydraulics.

Competitive Landscape

The Organic Friction Modifier Additives market is moderately concentrated. Start-ups pursuing ionic-liquid boosters advertise less than or equal to 0.05 friction but remain hampered by USD 80/kg economics and pending REACH clearance for fluorinated anions. This niche invites partnership or acquisition by incumbents once prices fall and regulatory clouds lift. White-space opportunities persist in offshore wind hydraulic fluids, aerospace greases beyond 200°C, and biodegradable solutions for forestry machinery, where no dominant supplier has yet emerged.

Organic Friction Modifier Additives Industry Leaders

BASF

LANXESS

Afton Chemical

Lubrizol

Infineum International Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: International Lubricants, Inc. unveiled its latest product, the LUBEGARD Multi-System Friction Modifier Additive. Designed for differentials, transmissions, and transfer cases, the company highlighted its low-odor formula, making it ideal for use in confined workplace environments.

- August 2025: Ravensberger Schmierstoffvertrieb GmbH launched RAVENOL CeramiX-Pro, a ceramic-based motor oil additive designed to lower mechanical wear. The formulation combines advanced ceramic components with organic friction modifiers to improve lubrication and durability under varying operating conditions.

Global Organic Friction Modifier Additives Market Report Scope

Organic Friction Modifier Additives (OFMs) are amphiphilic, surface-active compounds, commonly fatty acids, esters, or amines, added to lubricants to reduce friction and wear under boundary lubrication (metal-to-metal contact) conditions.

The Organic Friction Modifier Additives market is segmented by type, form, application, end-user industry, and geography. By type, the market is segmented into ester-based friction modifiers, amide-based friction modifiers, acid-based friction modifiers, amine-based friction modifiers, and other organic friction modifiers. By form, the market is segmented into liquid and solid (powder/dispersible). By application, the market is segmented into engine oils, transmission fluids (ATF, DCTF, and CVTF), gear oils, hydraulic fluids, greases, metalworking fluids, and other specialty lubricants. By end-user industry, the market is segmented into automotive and transportation, industrial manufacturing and machinery, aerospace and aviation, energy and power generation, marine and rail, and other end-user industries. The report also covers the market size and forecasts for organic friction modifier additives in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Ester-Based Friction Modifiers |

| Amide-Based Friction Modifiers |

| Acid-Based Friction Modifiers |

| Amine-Based Friction Modifiers |

| Other Organic Friction Modifiers |

| Liquid |

| Solid (Powder / Dispersible) |

| Engine Oils |

| Transmission Fluids (ATF, DCTF, CVTF) |

| Gear Oils |

| Hydraulic Fluids |

| Greases |

| Metalworking Fluids |

| Other Specialty Lubricants |

| Automotive and Transportation |

| Industrial Manufacturing and Machinery |

| Aerospace and Aviation |

| Energy and Power Generation |

| Marine and Rail |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Ester-Based Friction Modifiers | |

| Amide-Based Friction Modifiers | ||

| Acid-Based Friction Modifiers | ||

| Amine-Based Friction Modifiers | ||

| Other Organic Friction Modifiers | ||

| By Form | Liquid | |

| Solid (Powder / Dispersible) | ||

| By Application | Engine Oils | |

| Transmission Fluids (ATF, DCTF, CVTF) | ||

| Gear Oils | ||

| Hydraulic Fluids | ||

| Greases | ||

| Metalworking Fluids | ||

| Other Specialty Lubricants | ||

| By End-user Industry | Automotive and Transportation | |

| Industrial Manufacturing and Machinery | ||

| Aerospace and Aviation | ||

| Energy and Power Generation | ||

| Marine and Rail | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the organic friction modifier additives market by 2031?

The Organic Friction Modifier Additives Market size is projected to be USD 479.22 million in 2025, USD 503.76 million in 2026, and reach USD 646.62 million by 2031, growing at a CAGR of 5.12% from 2026 to 2031.

Which chemistry held the largest share in 2025?

Ester-based molecules led with 41.11% of 2025 revenue of the organic friction modifier additives market.

Why are transmission fluids a fast-growing application?

Dual-clutch and continuously variable transmissions need precise friction control, driving a 6.12% CAGR during the forecast period (2026-2031) in additive demand.

Which region leads in consumption?

Asia-Pacific accounted for 52.22% of 2025 sales and is expanding at a 6.26% CAGR during the forecast period (2026-2031).

Page last updated on: