Rheology Modification Coating Additives Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

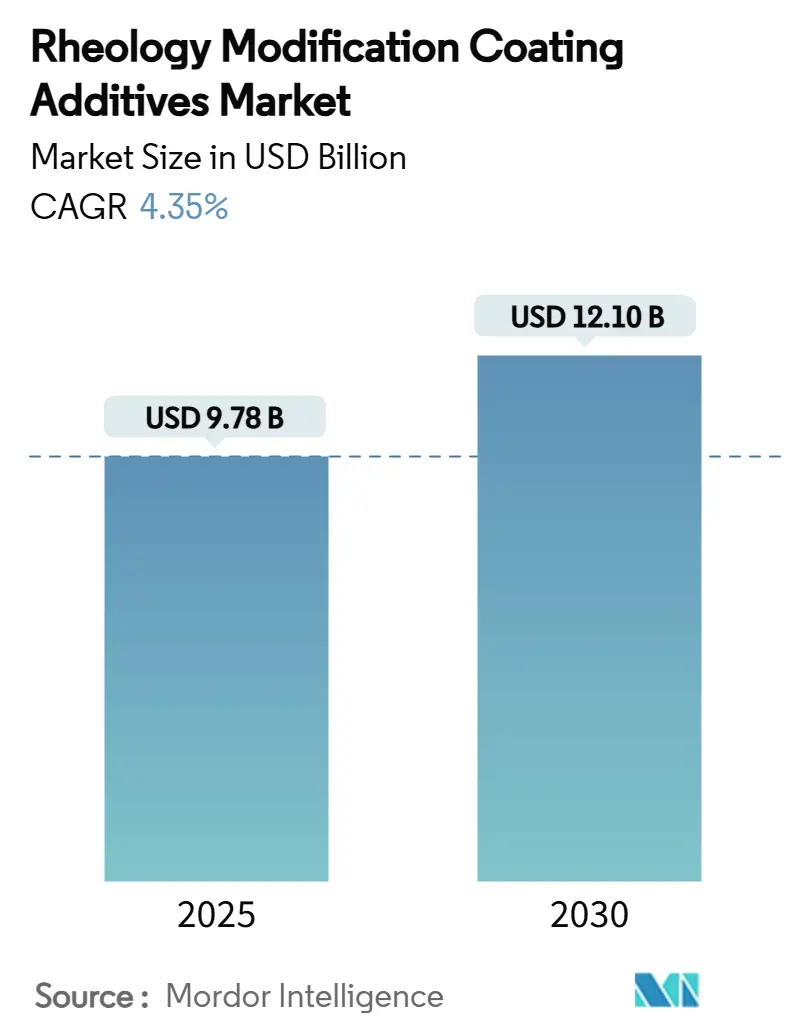

| Market Size (2025) | USD 9.78 Billion |

| Market Size (2030) | USD 12.10 Billion |

| Growth Rate (2025 - 2030) | 4.35% CAGR |

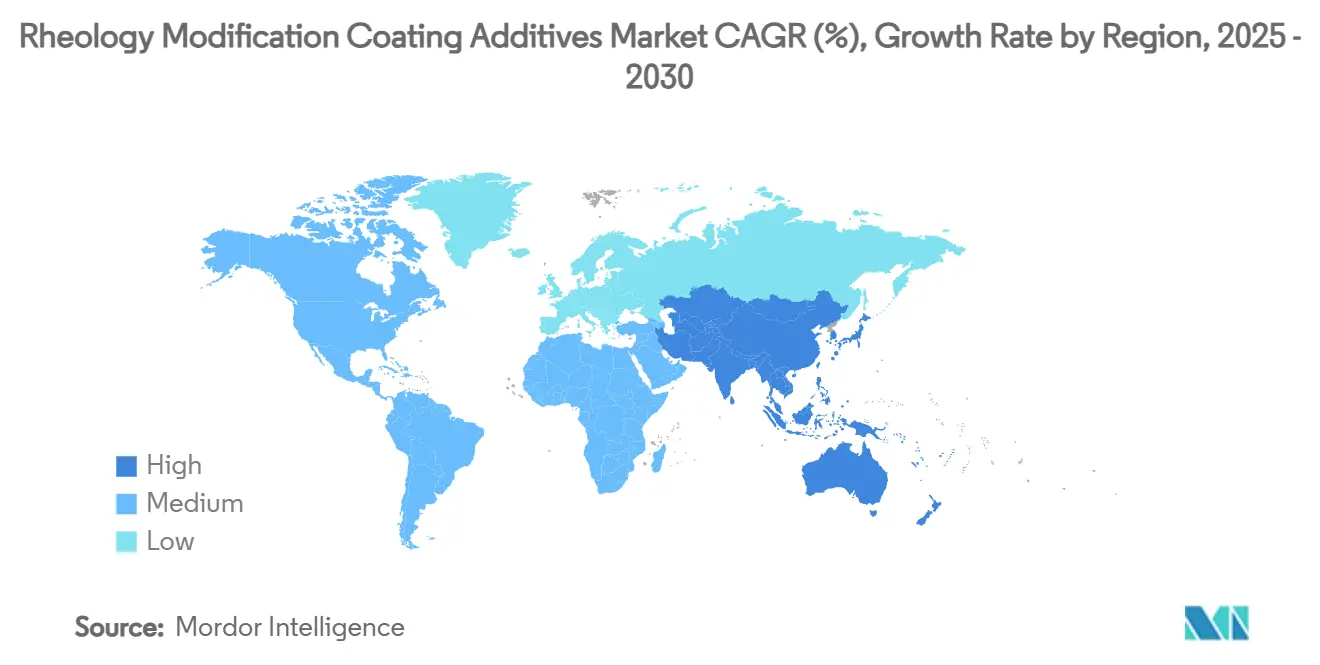

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rheology Modification Coating Additives Market Analysis by Mordor Intelligence

The Rheology Modification Coating Additives Market size is estimated at USD 9.78 Billion in 2025, and is expected to reach USD 12.10 Billion by 2030, at a CAGR of 4.35% during the forecast period (2025-2030). Rising deployment of water-borne, solvent-borne, and UV-curable coatings across construction, automotive, and marine value chains anchors this steady growth. Greater focus on low-VOC (Volatile Organic Compound) compliance, rapid industrial automation, and offshore wind projects is sustaining demand for additives that deliver precise viscosity profiles. Suppliers able to balance low-shear storage stability with high-shear spray application properties are expanding premium product lines, while bio-based chemistries and digital formulation tools open new revenue pockets. Ongoing feedstock price swings and microplastics regulation present headwinds, yet are spurring accelerated innovation in sustainable thickener platforms.

Key Report Takeaways

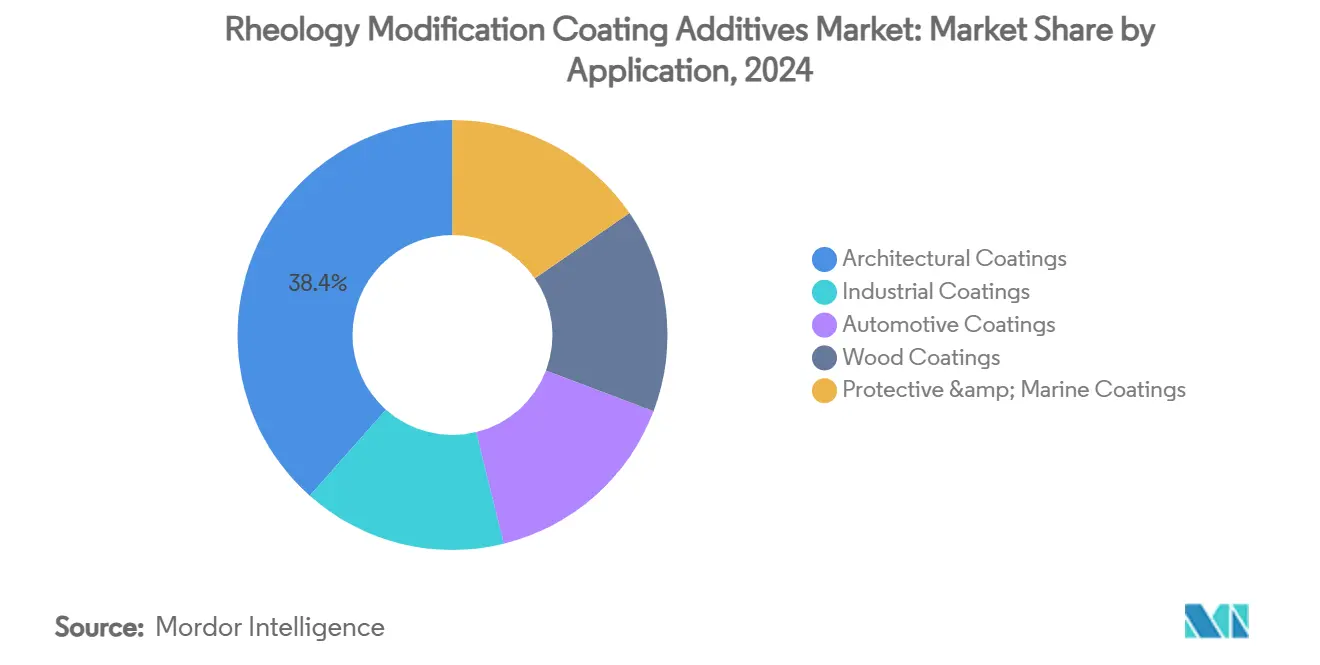

- By application, architectural coatings led with a 38.45% revenue share in 2024, whereas protective and marine coatings are projected to rise at a 5.45% CAGR through 2030.

- By type, polymeric thickeners captured 42.66% of the Rheology Modification Coating Additives market share in 2024, while natural and bio-based thickeners are expected to post the highest 5.35% CAGR over 2025-2030.

- By end-use industry, construction accounted for 41.56% of the Rheology Modification Coating Additives market size in 2024 and furniture & woodcare is forecast to expand at a 4.89% CAGR through 2030.

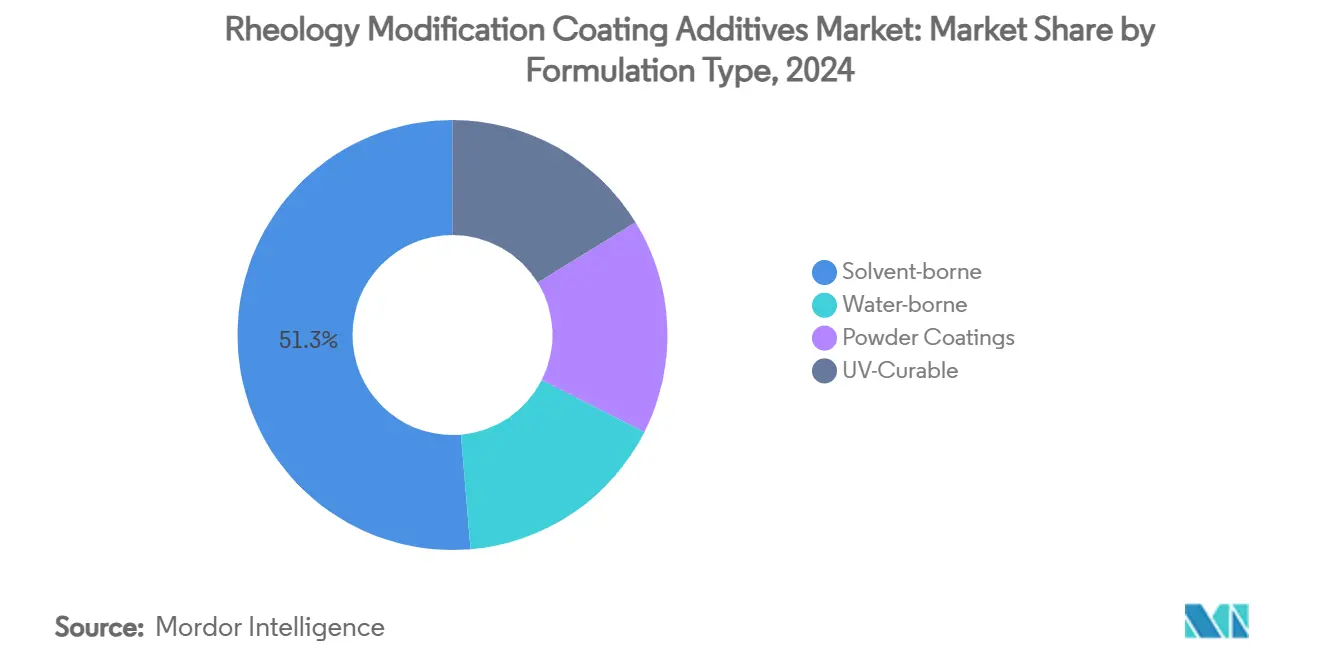

- By formulation type, solvent-borne systems retained 51.34% share of the Rheology Modification Coating Additives market size in 2024, yet UV-curable systems are set to advance at a 5.34% CAGR between 2025-2030.

- By geography, Asia-Pacific accounted for the largest revenue share of 35.77% in 2024, and is also expected to grow with the fastest CAGR of 5.35% over 2025-2030.

Global Rheology Modification Coating Additives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift Toward Low-VOC Water-borne Systems | +1.2% | North America and EU strongest | Medium term (2-4 years) |

| Rapid Urbanization and Infrastructure Spend in APAC | +0.8% | APAC core, MEA spill-over | Long term (≥ 4 years) |

| Automotive OEM Demand for Texture Consistency in Advanced Finishes | +0.5% | Global automotive hubs | Medium term (2-4 years) |

| Stringent Emission Norms Pushing High-solids Coatings | +0.6% | North America, EU, expanding APAC | Short term (≤ 2 years) |

| AI-driven Formulation Platforms Enabling Hyper-custom Rheology | +0.4% | Early adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Low-VOC Water-borne Systems

Increasingly strict VOC ceilings force formulators to abandon traditional solvent-borne architectures in favor of water-borne coatings that rely on associative thickeners such as HEUR (Hydrophobically modified Ethoxylated Urethane) and HASE (Hydrophobically modified Alkali Swellable Emulsion) for equivalent film build. The chemistry challenge lies in preserving flow and leveling at high shear while preventing sag under low shear, a balance that commands premium pricing. BASF has introduced bio-based ethyl acrylate grades that meet these dual requirements, reinforcing the competitive edge of suppliers with multifunctional additive portfolios[1]BASF Press Office, “BASF Adds Bio-based Ethyl Acrylate Grades,” BASF, basf.com.

Rapid Urbanization and Infrastructure Spend in APAC

Smart city rollouts across China, India, and key ASEAN members are accelerating demand for weather-resistant architectural finishes, each requiring optimized rheological packages to deliver uniform film thickness under tropical humidity and monsoon cycles. Extended public investments in rail, ports, and renewable energy platforms promise multi-year visibility for additive volumes as local producers switch to water-based systems.

Automotive OEM Demand for Texture Consistency in Advanced Finishes

Vehicle manufacturers are tightening appearance tolerances on increasingly complex body geometries. Next-generation electric models undergo broader thermal cycling, raising the bar for rheology modifiers that must maintain edge-cover on sharp creases and avoid orange-peel defects during robotic spraying. Suppliers delivering application-specific thickener packages that stabilize metallic pigments and tune viscoelasticity are gaining specification wins with tier-one paint shops.

Stringent Emission Norms Pushing High-solids Coatings

Legislation that caps VOC grams per liter is accelerating the industrial switch to high-solids formulations. Reduced solvent content diminishes flow distance, driving demand for additives that maintain workable viscosity without sacrificing sag resistance. Performance-critical tank linings and heavy-duty machinery coatings rely on novel associative polymer networks to fulfill these stricter thresholds.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Prices of Key Feedstock | -0.7% | Global, import-dependent regions acute | Short term (≤ 2 years) |

| Environmental Regulations on Microplastics Limiting Synthetic Associative Thickeners | -0.5% | EU, North America expanding | Medium term (2-4 years) |

| Competition From Multifunctional Nano-Additives Reducing Need for Separate Rheology Modifiers | -0.3% | Global, high-tech niches | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in prices of key feedstock

Raw material price instability, particularly for titanium dioxide and specialty monomers used in rheology modifier production, constrains market growth as manufacturers struggle to maintain consistent pricing and profit margins. Titanium dioxide market dynamics show signs of stabilization following recent volatility, but rising costs of sulfuric acid and production cuts in China continue to create supply uncertainty. The situation is compounded by trade tensions and tariff implementations that disrupt established supply chains for critical coating raw materials, forcing manufacturers to seek alternative sourcing strategies that may increase costs. Specialty chemical suppliers face particular challenges as they must balance raw material cost fluctuations with customer demands for stable pricing, often absorbing short-term volatility to maintain long-term relationships.

Environmental Regulations on Microplastics Limiting Synthetic Associative Thickeners

EU Regulation 2023/2055 restricting synthetic polymer microparticles is forcing fundamental changes in rheology modifier chemistry as traditional associative thickeners face potential market restrictions. The regulation's broad definition of synthetic polymer microparticles creates uncertainty around widely used HASE (Hydrophobically Modified Alkali Swellable Emulsions) and ASE (Alkali Swellable Emulsions) thickeners, prompting suppliers to develop alternative chemistries or demonstrate permanent modification of restricted materials, European Commission. The regulatory impact extends beyond Europe as other regions consider similar restrictions, creating global market uncertainty for synthetic thickener suppliers. This regulatory pressure is accelerating the development of bio-based alternatives, but these systems often require reformulation to achieve equivalent performance, creating short-term market disruption while long-term opportunities emerge for sustainable solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application – Protective & Marine Coatings Gain Premium Momentum

Protective and marine coatings recorded the highest 5.45% CAGR over 2025-2030, well above the overall rheology modification coating additives market, as offshore wind monopiles and Floating Production Storage and Offloading (FPSO) refurbishments require sag-free high-build layers in exposed saline environments. Uniform film build at 250 µm dry film thickness mandates bespoke thickener systems that stabilize heavy zinc and aluminum pigments. Architectural coatings, still holding 38.45% share in 2024, rely on water-borne acrylic binders where HEUR packages safeguard open time and roller spatter performance. Industrial maintenance programs and automotive refinish lines contribute incremental demand through enhanced robotics that call for tighter viscosity windows.

The marine sector’s willingness to fund premium additives rests on the multi-million-dollar cost of corrosion-related downtime. Suppliers offering high solids, low VOC rheology packages win specifications on liquefied natural gas (LNG) carriers and cruise vessels. Simultaneously, wood coatings benefit from plantation timber legalization and consumer appetite for natural wood grain aesthetics, stimulating the need for shear-stable bio-thickeners that withstand outdoor UV while limiting fiber raise.

By Type – Bio-based Alternatives Gather Pace

Polymeric thickeners maintained a 42.66% share in 2024, driven by their compatibility with water-borne systems and ability to embed additional surfactant-like functionality that levels flow and enhances color acceptance. Natural and bio-based grades, however, are forecast to expand at 5.35% CAGR, the fastest within the rheology modification coating additives market, as cellulose nanofibrils and modified guar derivatives approach synthetic performance. Inorganic clays continue serving acid-stable or high-temperature environments, offering thixotropy that prevents settling in epoxy primers.

Suppliers are scaling enzymatic functionalization processes that impart hydrophobically modified side chains onto renewable backbones, meeting both biodegradability and performance criteria. Evonik’s pivot to specialty additive lines underscores the mainstreaming of bio-based solutions that match shear build profiles once exclusive to synthetic ASE (Alkali Swellable Emulsions) networks.

By End-Use Industry – Construction Rules, Furniture Surges

Construction commanded 41.56% of the 2024 value as global megaprojects and retrofit insulation programs drove huge volumes of architectural paints, all of which lean on associative thickeners for viscosity build. Furniture and woodcare applications are projected to clock a 4.89% CAGR thanks to rapid growth in flat-pack exports and demand for VOC-free interior finishes. Automotive original equipment manufacturer (OEM) shops preserve steady pull-through due to heightened surface quality standards in luxury EV (electric vehicle) launches, whereas rail and aviation remain niche yet specification-heavy, favoring high-purity, low-ionic thickeners for uncompromised appearance.

The construction sector’s reliance on spray-applied elastomeric coatings for cool-roof systems introduces shear gradient extremes, reinforcing the value proposition of multi-mode rheology packages that resist sag while maximizing coverage. Furniture market expansion rests on higher-solids UV-curable lacquers, demanding photostable thickeners that avoid yellowing during prolonged sun exposure.

By Formulation Type – UV-curable Systems Accelerate

Solvent-borne coatings still held a 51.34% share in 2024 due to their unmatched robustness in heavy-duty applications, yet UV-curable technologies are set to register a 5.34% CAGR through 2030 as manufacturers prioritize shorter cure cycles and energy savings. These systems rely on rheology modifiers that resist premature UV crosslinking while delivering in-can stability. Water-borne platforms continue replacing solvent lines in decorative paints, propelled by eco-label certifications and municipal procurement policies. Powder coatings, although smaller in volume, necessitate specialized melt-phase rheology aids that ensure edge coverage and prevent orange peel during baking.

Formulators increasingly choose hybrid systems that blend UV and high-solids chemistries, requiring additives with dual cure resistance. This push elevates demand for monomer-free associative polymers that do not interfere with photo-initiated polymerization yet provide low-shear storage viscosity.

Geography Analysis

Asia Pacific accounted for 35.77% of global demand in 2024 and is projected to post a 5.35% CAGR, the quickest among regions, supported by megacity housing schemes and port infrastructure that consume protective and architectural coatings in large volumes. Regional regulators tighten VOC targets, accelerating substitution toward water-borne acrylics and bolstering additive uptake. Local formulators partner with multinational suppliers to co-create climate-specific rheology packages, illustrated by Evonik’s specialty amine expansion in Nanjing that ensures regional self-sufficiency[2]Evonik Investor Relations, “Specialty Amine Plant Expansion Nanjing,” Evonik, corporate.evonik.com.

North America remains a technology-rich and regulation-intensive arena where low-VOC and high-solids compliance drives preference for multifunctional additive packages. Domestic producers such as Lubrizol invested USD 20 Million in acrylic emulsion capacity in North Carolina during 2025 to cushion supply chain disruptions and maintain short lead times for regional paint majors. Federal infrastructure stimulus packages sustain a steady baseline demand for bridge, highway, and industrial maintenance coatings.

Europe continues to influence global chemistry through its sustainability legislation. European Union (EU) Regulation 2023/2055 is reshaping formulation choices, directing R&D toward bio-degradable rheology systems and spurring cross-border collaboration on circular raw materials. Although construction growth is moderate, refurbishment projects and heritage preservation keep volumes stable while quality requirements escalate. South America and Middle East & Africa, though smaller, reveal accelerating uptake of UV-curable wood and metal coatings as regional furniture and appliance clusters gain export traction.

Competitive Landscape

The Rheology Modification Coating Additives market is moderately consolidated. Leading multinationals such as BASF, Dow, and Arkema leverage integrated production and global technical centers to hold core positions, while mid-tier specialists compete on niche performance claims. Digital customer interfaces, exemplified by Dow’s Paint Vision, shorten lab-to-line timelines and deepen client loyalty through predictive formulation support. Smaller innovators tap venture capital to commercialize nanocellulose and silica aerogel rheology systems, courting automotive and aerospace formulators that prize lightweighting and multifunctionality. Feedstock volatility is prompting larger players to forward-integrate into biomass supply chains, ensuring long-term security of bio-based inputs while capturing sustainability premiums.

Rheology Modification Coating Additives Industry Leaders

BASF

Dow

Arkema

ALTANA

Ashland

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: At the European Coatings Show in Nuremberg, Germany, Nouryon unveiled Bermocoll EHM MAX. This hydrophobically modified cellulose ether is a rheology modifier for use in interior and exterior architectural paints.

- March 2024: Elementis PLC unveiled its latest offerings, RHEOLATE 125 P and RHEOLATE 185 P. These are rheological additives that aim to enhance coating applications, guaranteeing improved viscosity control, seamless application, and enhanced water retention.

Global Rheology Modification Coating Additives Market Report Scope

| Architectural Coatings |

| Industrial Coatings |

| Automotive Coatings |

| Wood Coatings |

| Protective & Marine Coatings |

| Polymeric Thickeners (HEUR, HASE, ASE) |

| Inorganic Thickeners (clays, silica) |

| Synthetic Cellulosics |

| Natural/Bio-Based Thickeners |

| Construction |

| Automotive & Transportation |

| Furniture and Woodcare |

| Other End-users (Packaging and Printing Inks) |

| Water-borne |

| Solvent-borne |

| Powder Coatings |

| UV-Curable |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Malaysia | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Application | Architectural Coatings | |

| Industrial Coatings | ||

| Automotive Coatings | ||

| Wood Coatings | ||

| Protective & Marine Coatings | ||

| By Type | Polymeric Thickeners (HEUR, HASE, ASE) | |

| Inorganic Thickeners (clays, silica) | ||

| Synthetic Cellulosics | ||

| Natural/Bio-Based Thickeners | ||

| By End-Use Industry | Construction | |

| Automotive & Transportation | ||

| Furniture and Woodcare | ||

| Other End-users (Packaging and Printing Inks) | ||

| By Formulation Type | Water-borne | |

| Solvent-borne | ||

| Powder Coatings | ||

| UV-Curable | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current global value of Rheology Modification Coating Additives?

The Rheology Modification Coating Additives market is valued at USD 9.78 billion in 2025.

How fast is demand for marine coatings additives expanding?

Protective and marine applications are projected to grow at 5.45% CAGR from 2025 to 2030.

Which additive type is gaining momentum for sustainability reasons?

Natural and bio-based thickeners are expected to record the highest 5.35% CAGR over the forecast period.

Why are UV-curable coatings important for manufacturers?

They shorten production cycles and cut energy use, driving a 5.34% CAGR in additive demand.

What major regulation is shaping additive chemistry in Europe?

EU Regulation 2023/2055 restricts synthetic polymer microparticles, encouraging bio-based thickener development.

Page last updated on: