Anti-slip Additives Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 498.69 Million |

| Market Size (2031) | USD 616.28 Million |

| Growth Rate (2026 - 2031) | 4.33% CAGR |

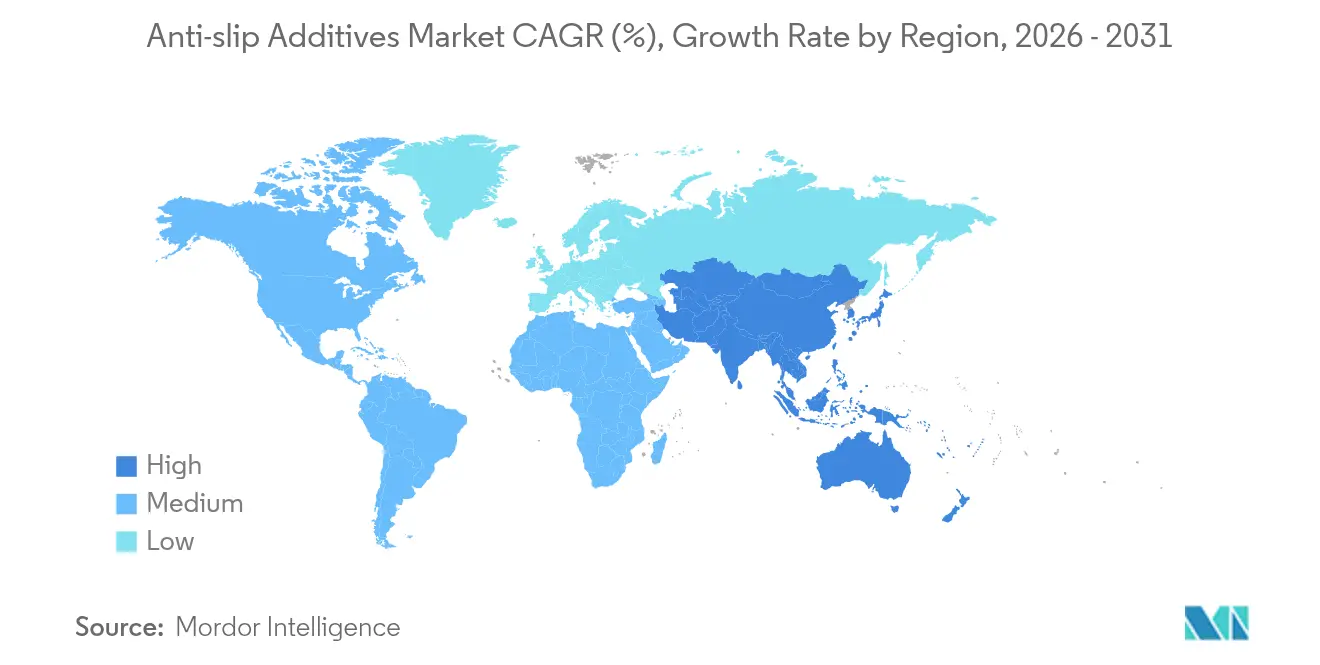

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

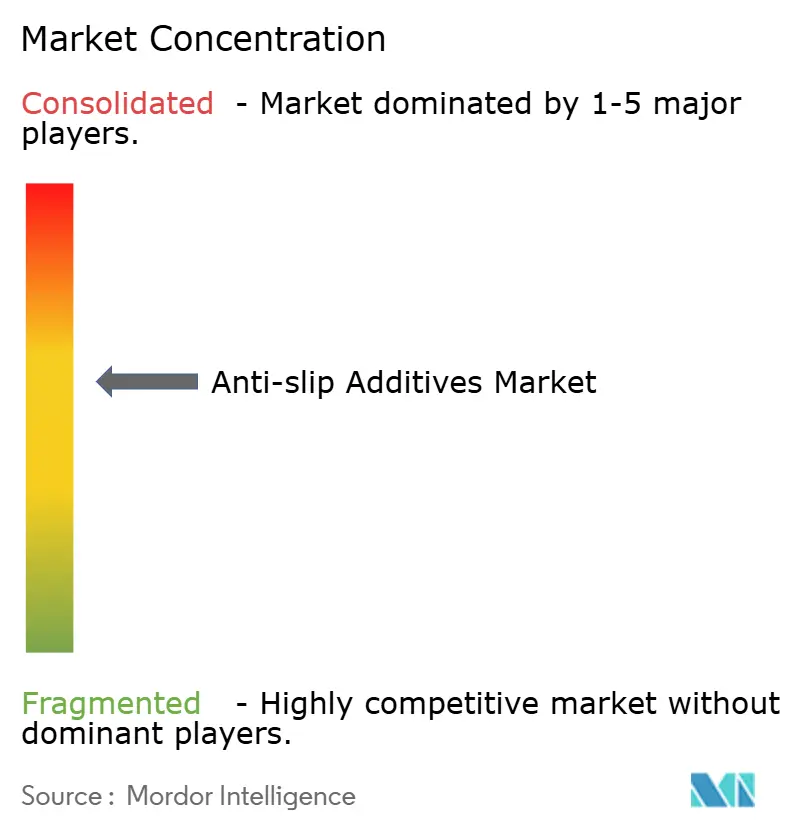

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anti-slip Additives Market Analysis by Mordor Intelligence

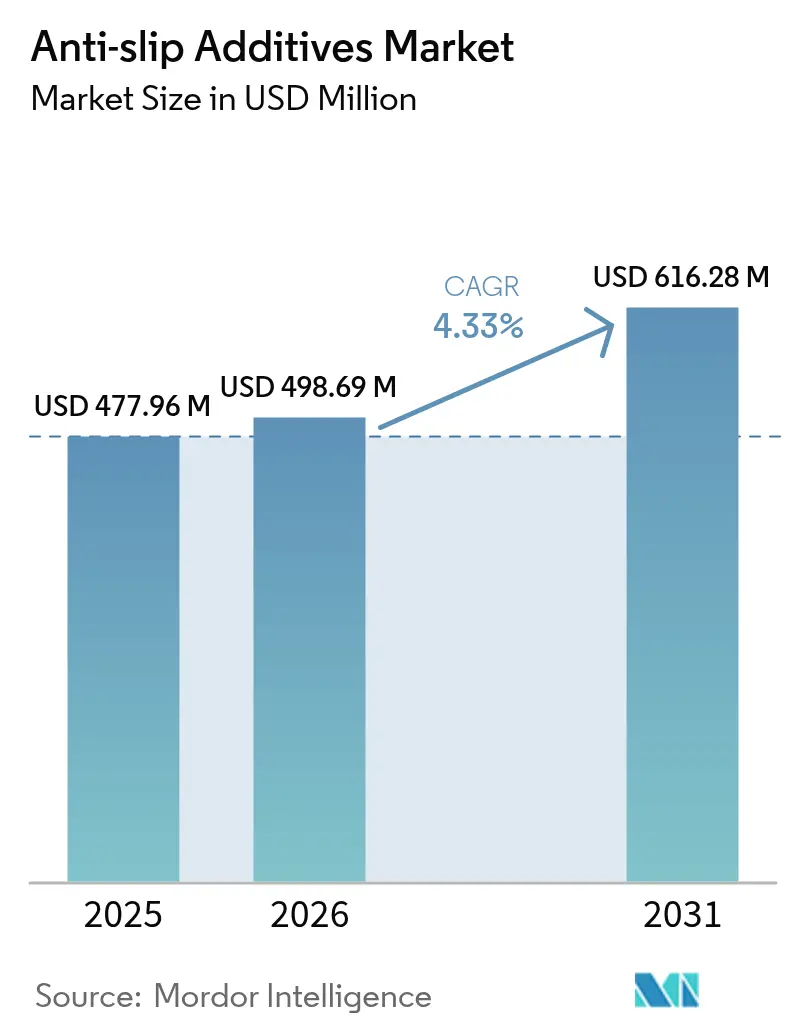

The Anti-slip Additives Market size was valued at USD 477.96 million in 2025 and estimated to grow from USD 498.69 million in 2026 to reach USD 616.28 million by 2031, at a CAGR of 4.33% during the forecast period (2026-2031). The growth outlook reflects steady adoption across manufacturing, construction, and marine sectors as employers tighten safety protocols and governments strengthen flooring standards. Heightened infrastructure spending in emerging economies, ongoing retrofits in mature regions, and the rollout of advanced low-VOC chemistries collectively anchor demand. In parallel, product innovation around nanoparticle dispersions and bio-based alternatives is widening application breadth while supporting compliance with evolving emission limits. Competitive intensity remains moderate because the leading suppliers benefit from large portfolios, global distribution, and sustained research and development pipelines even as smaller regional players vie for price-sensitive orders.

Key Report Takeaways

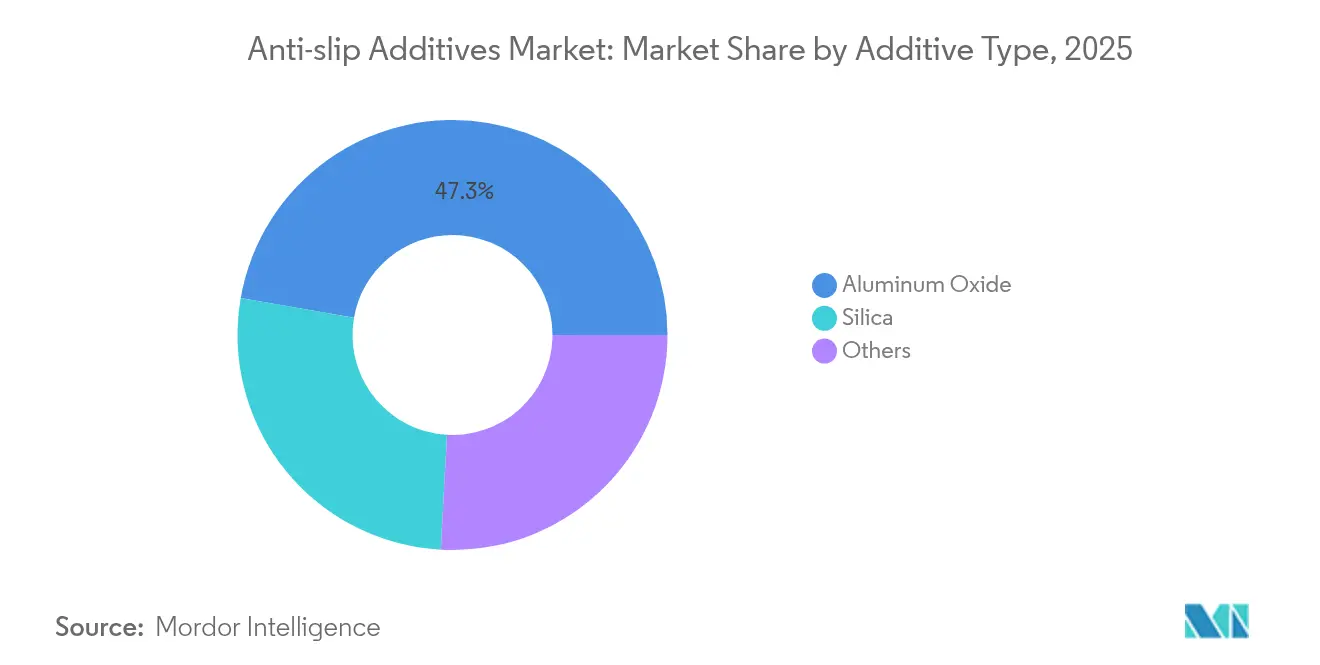

- By additive type, aluminum oxide led with 47.25% revenue share in 2025; silica is forecast to expand at a 5.05% CAGR through 2031.

- By additive nature, the powder form accounted for 50.15% of the Anti-Slip Additives market share in 2025 and are projected to grow at 4.42% CAGR to 2031.

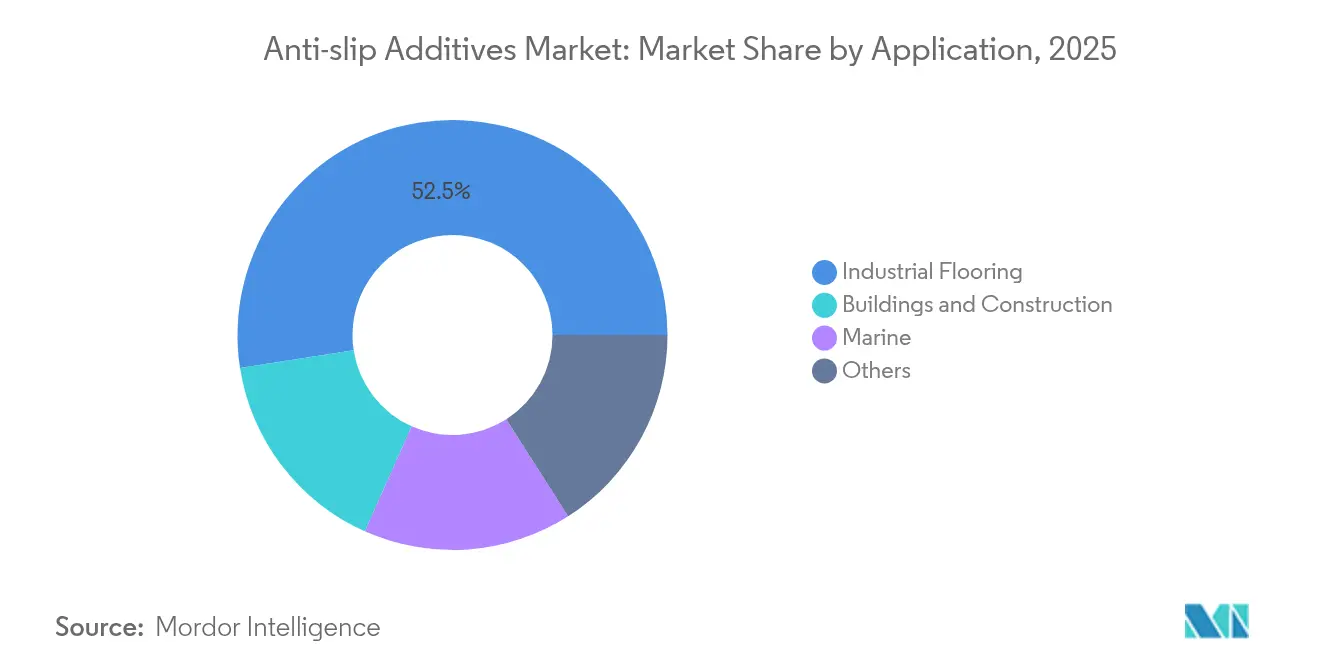

- By application, industrial flooring captured 52.45% share of the Anti-Slip Additives market size in 2025 and is advancing at a 4.51% CAGR through 2031.

- By geography, Asia-Pacific commanded 56.62% of global revenue in 2025; the region is also set to post the fastest 4.62% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Anti-slip Additives Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for industrial flooring safety | + 1.2% | Global, with concentration in North America and EU | Short term (≤ 2 years) |

| Expansion of APAC construction sector | + 0.8% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Marine-deck safety compliance | +0.6% | Global, with emphasis on maritime nations | Medium term (2-4 years) |

| Nanoparticle-enabled durability upgrades | + 0.9% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| Phase-out of PFAS drives bio-based alternatives | + 0.7% | Global, with stricter enforcement in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Industrial Flooring Safety

Slips, trips, and falls rank as the second-leading cause of workplace fatalities in general industry, prompting regulators to tighten surface-traction mandates. Rising workers’ compensation premiums further encourage manufacturers to install high-performance coatings that sustain friction over the full maintenance cycle. In response, suppliers are engineering synthetic grains that embed evenly within epoxies or polyurethane screeds to achieve a balance of coefficient of friction and esthetic finish. End users increasingly integrate such solutions at the design stage rather than reacting to incidents, reflecting a wider shift toward risk-managed operations. As a result, industrial flooring remains the largest pull-through channel for the Anti-Slip Additives market.

Expansion of APAC Construction Sector

Aggressive infrastructure spending across China, India, and the ASEAN bloc is injecting steady volume into the Anti-Slip Additives market. Public procurement guidelines now specify slip-resistant pavement and transit concourse finishes, stimulating recurring orders for broadcast quartz and silica blends. Rapid urbanization raises pedestrian density, intensifying wear on floor surfaces and accelerating refurbishment cycles. Contractors value additives that disperse quickly in cementitious toppings and self-leveling mortars because jobsite timelines are compressed. Multinational owners of logistics hubs and regional manufacturing plants also impose global safety codes, multiplying addressable demand beyond classical public works. Consequently, Asia-Pacific simultaneously hosts the largest base and the fastest growth trajectory.

Marine-Deck Safety Compliance

Military and commercial fleet operators specify coatings that satisfy ASTM F718 and NAVSEA non-skid criteria, typically employing aluminum oxide or barium sulfate grains for high-load helicopter decks. Such platforms endure salt spray, temperature shocks, and hydraulic-fluid spills, creating niche demand for premium additive packages that maintain micro-profile over long dry-dock intervals. Shipyards increasingly favor non-abrasive synthetics on auxiliary decks to limit equipment wear without sacrificing grip. These stringent requirements allow suppliers to command price premiums that offset lower volumetric throughput relative to terrestrial uses, supporting margins in the Anti-Slip Additives market.

Nanoparticle-Enabled Durability Upgrades

Silica nanoparticles around 100 nm have demonstrated friction reductions of 38.3% and wear declines of 49.4% when dispersed at 5 wt% in water-borne lubricants. These advances translate into coatings that preserve traction across extended maintenance windows, reducing life-cycle cost for high-traffic assets. Suppliers leveraging nanoparticle technology differentiate on endurance and thin-film transparency, enabling designers to maintain floor esthetics while meeting slip benchmarks. As production scale improves, nanoparticle additives are moving from pilot lines toward mainstream industrial flooring, underpinning long-term growth in the Anti-Slip Additives market.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| VOC and hazardous-substance regulations | -0.7% | Global, with stricter enforcement in North America and EU | Short term (≤ 2 years) |

| Raw-material price volatility | -0.5% | Global, with particular impact on cost-sensitive markets | Medium term (2-4 years) |

| Shift to textured polymer flooring | -0.4% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

VOC and Hazardous-Substance Regulations

The US National AIM Rule fixes a 400 g/l VOC ceiling for floor coatings, while certain state codes enforce even tighter thresholds, compelling reformulation toward water-borne or 100% solid systems. European REACH and local PFAS phase-out directives add complexity, evidenced by Micro Powders’ decision to terminate PTFE-based grades by end-2025[1]Micro Powders, “PTFE (PFAS) Replacement Additive Solutions,” micropowders.com. Compliance accelerates research and development expenditure and lengthens qualification cycles, especially for small and mid-size producers. Although regulation ultimately steers users toward cleaner chemistries, near-term uncertainty can defer capital projects, temporarily muting order flow in the Anti-Slip Additives market.

Raw-Material Price Volatility

Aluminum oxide and silica spot prices fluctuate with energy tariffs, freight rates, and capacity shifts in China’s mineral-processing belt. High-purity alumina relies on energy-intensive calcination stages affected by emissions surcharges, exposing producers to margin compression during price spikes. While tier-one suppliers hedge via long-term contracts and backward integration, regional blenders often carry limited inventory, forcing rapid price pass-through that squeezes downstream applicators. Erratic costs complicate budgeting for large infrastructure tenders, at times encouraging substitution with lower-grade aggregates, which can weigh on unit revenue growth within the Anti-Slip Additives market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Additive Type: Aluminum Oxide Dominance Faces Silica Innovation

Aluminum oxide held 47.25% revenue share in 2025, underscoring its entrenched status among plant engineers who prize hardness and abrasion resistance for fork-truck aisles and loading bays. The segment’s maturity stems from proven field data and widespread distributor availability, giving purchasing managers confidence in predictable slip performance over multi-year maintenance cycles.

Yet silica is advancing at a market-leading 5.05% CAGR as precipitated and fumed variants leverage superior oil-absorption and low specific gravity to deliver the required surface profile at lower addition rates. PPG indicates that its precipitated silica can carry more than 40 times the weight of traditional bulking agents, translating into thinner yet efficient coatings. The shift also aligns with environmental preferences because silica grades typically exhibit benign regulatory profiles compared with certain metal oxides.

By Additive Nature: Powder Form Maintains Versatility Advantage

Powder formulations occupied 50.15% of global revenue in 2025 and are projected to grow in lockstep with overall demand at 4.42% CAGR through 2031. Contractors favor powders because they broadcast easily onto wet film or disperse homogeneously when pre-mixed into epoxies. Lightweight polymeric powders such as SCOFIELD Traction Additive improve safety without altering appearance or adding application steps. Mix products that bundle additive and resin in one package reduce dosing errors yet add logistics complexity for multi-component industrial lines.

Continued investment in milling and surface-treatment technology supports powders’ versatility, enabling functionalization that counters floatation and improves adhesion to resins with disparate polarity. As a result, powders are forecast to hold their leadership position, with incremental gains derived from water-borne and UV-curable formulations where fine particle control underpins gloss retention.

By Application: Industrial Flooring Drives Safety Compliance

Industrial flooring accounted for 52.45% share in 2025, reflecting compulsory compliance programs in automotive, food processing, and pharmaceutical manufacturing. Floor coating OEMs embed additives during factory batching to guarantee coefficient-of-friction targets without relying on installer accuracy. European PVC flooring standard EN 13845:2017 mandates strict slip thresholds, reinforcing demand for additive-rich wear layers. Buildings and construction is supported by residential towers and commercial lobbies where owners want low-profile textures that uphold esthetics. The Anti-Slip Additives market size for marine decks, while modest, commands premium unit values because every flight deck or tanker hatch demands non-skid certification throughout harsh duty cycles.

Healthcare corridors, public transport platforms, and consumer goods packaging lines populate the “Others” bucket, each contributing small yet rising volumes as safety awareness filters into ancillary markets. Industrial flooring will remain the anchor vertical, but as demographic aging drives accessibility retrofits, public buildings are set to widen the usage base and cushion cyclical swings.

Geography Analysis

Asia-Pacific retained 56.62% revenue in 2025 and is forecast to expand at 4.62% CAGR, cementing its dual status as largest and fastest region. Surging investments in public infrastructure and mega-factory complexes anchor steady demand for floor coatings that integrate anti-slip powders at the batch stage.

North America and Europe each retain robust baseline demand anchored in regulatory discipline. The US National AIM Rule meshes with UL floor-slip testing to enforce low-VOC thresholds and friction certification. European directives require documented slip resistance in hospitals and rail terminals, steering specifiers toward certified coarse-texture systems. Although volume growth is slower, margin structures remain attractive because clients emphasize premium durability and environmental labels.

The Middle-East and Africa and South America deliver emerging upside. Gulf states’ airport and offshore complex expansions specify non-skid walkways to mitigate heat-related surface smoothness. In South America, resource-driven economies invest in safer mineral-processing and port facilities, sustaining additive orders despite broader economic swings. Collectively, these regions inject diversification into the Anti-Slip Additives market, buffering suppliers against demand plateaus in mature territories.

Competitive Landscape

Moderate fragmentation defines the Anti-Slip Additives market. Top players benefit from integrated raw material sourcing, multi-continent manufacturing, and direct sales teams that influence specification at the architect and engineering level. Strategic moves encompass vertical integration, regional capacity additions, and alliances with coating formulators to embed additives during factory batching. Suppliers pivot from PFAS-containing grains toward bio-based or fluorine-free synthetics, capturing early-mover advantage in low-hazard portfolios. Nanoparticle platforms unlock high-margin niches where longevity and optical clarity outweigh unit price. Smaller players compete through localized service, custom particle sizing, and agile fulfillment. However, as multinationals deploy smart factories and digital color-matching, entry barriers for high-volume channels are climbing.

Anti-slip Additives Industry Leaders

Hempel A/S

Akzo Nobel N.V.

Axalta Coating Systems, LLC

ALTANA

PPG Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2023: Ampacet unveiled PERMSLIP 1409, a solution designed to provide a non-migrating, permanent anti-slip properties for flexible packaging conversions.

- June 2023: Evonik Industries AG launched TEGO Rad 2550, an anti-slip and defoamer additive specifically designed for radiation-curing inks and coatings.

Global Anti-slip Additives Market Report Scope

The anti-slip additives market report include:

| Aluminum Oxide |

| Silica |

| Others |

| Powder |

| Aggregate |

| Mix |

| Buildings and Construction |

| Industrial Flooring |

| Marine |

| Others |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Additive Type | Aluminum Oxide | |

| Silica | ||

| Others | ||

| By Additive Nature | Powder | |

| Aggregate | ||

| Mix | ||

| By Application | Buildings and Construction | |

| Industrial Flooring | ||

| Marine | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Anti-Slip Additives market?

The Anti-Slip Additives market size reached USD 498.69 million in 2026 and is forecast to climb to USD 616.28 million by 2031.

Which additive type dominates global sales?

Aluminum oxide leads the market with 47.25% revenue share in 2025 thanks to proven hardness and abrasion resistance.

Why is Asia-Pacific growing the fastest?

Massive infrastructure investment, stringent safety codes, and expanding manufacturing footprints drive a 4.62% CAGR in the region.

How do VOC regulations influence product development?

Regulators impose strict VOC caps, forcing suppliers to reformulate toward water-borne and 100% solids systems, which raises research and development costs but spurs cleaner chemistries.

What technological trend offers the biggest upside?

Nanoparticle-enhanced additives deliver longer-lasting slip resistance and lower film thickness, opening high-margin opportunities across industrial and architectural coatings.

Page last updated on: