Market Overview

| Study Period | 2020 - 2031 |

|---|---|

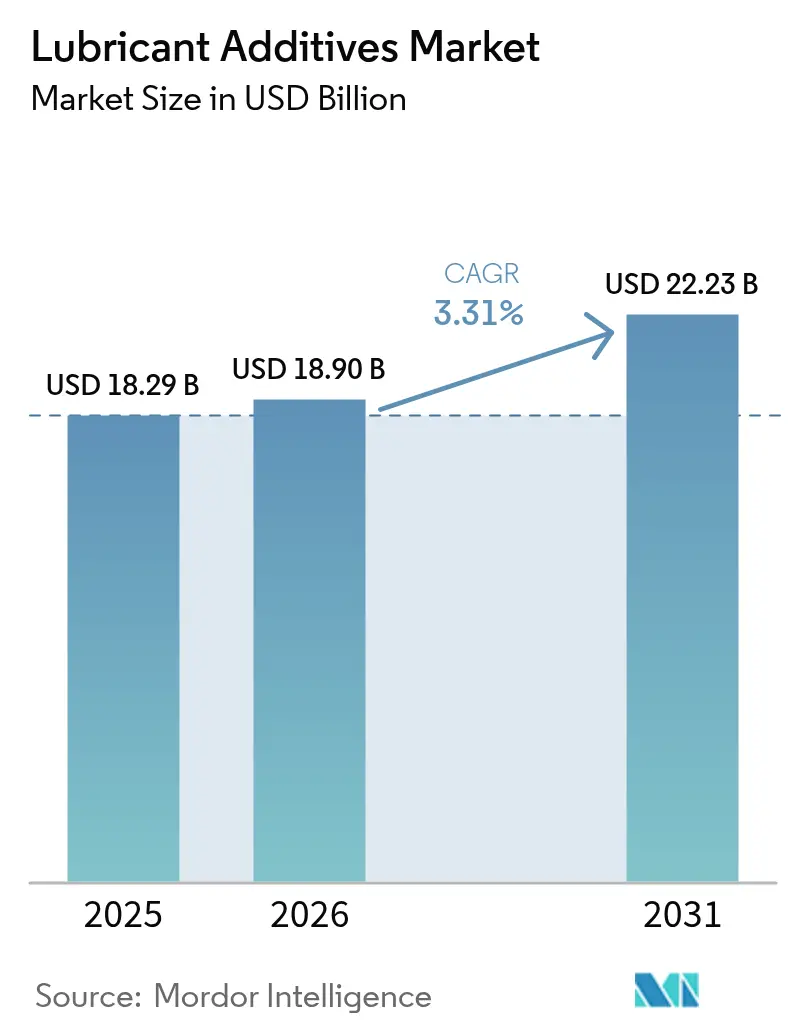

| Market Size (2026) | USD 18.90 Billion |

| Market Size (2031) | USD 22.23 Billion |

| Growth Rate (2026 - 2031) | 3.31% CAGR |

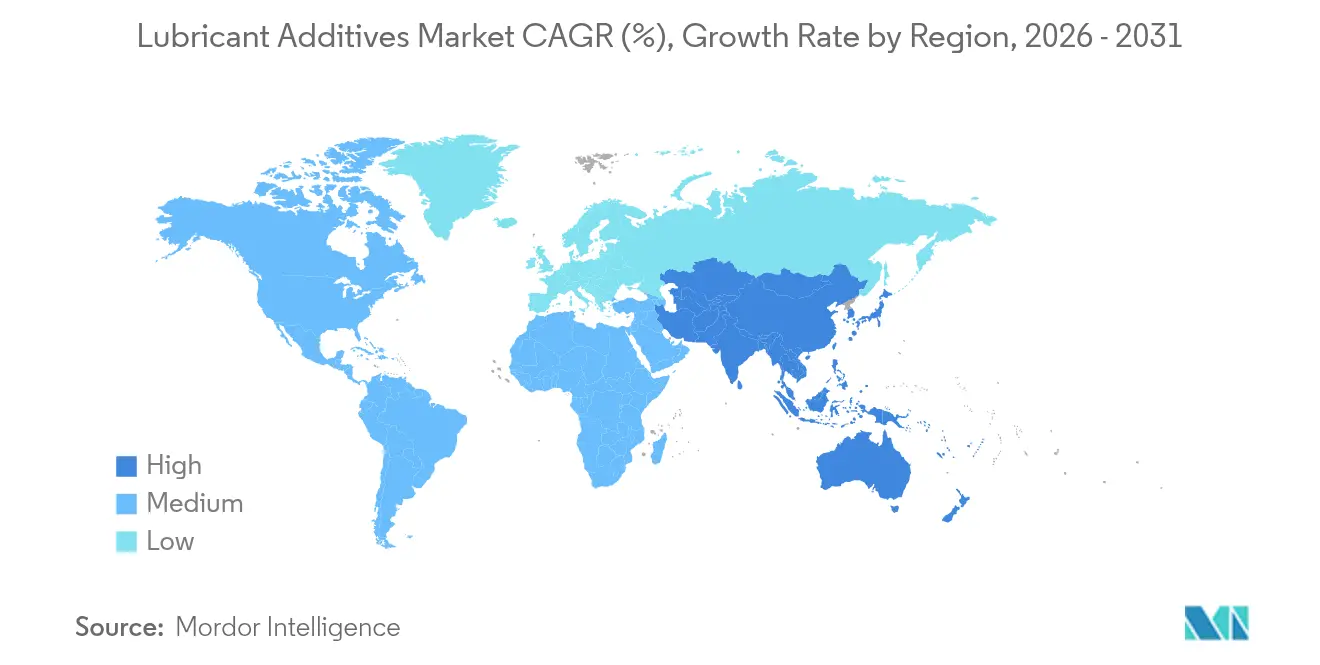

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lubricant Additives Market Analysis by Mordor Intelligence

Lubricant Additives Market size in 2026 is estimated at USD 18.9 billion, growing from 2025 value of USD 18.29 billion with 2031 projections showing USD 22.23 billion, growing at 3.31% CAGR over 2026-2031. This measured expansion reflects the industry’s shift from volume-driven growth toward value-focused innovation, where premium additive chemistries offset moderating lubricant demand. Rising regulatory stringency, led by the March 2025 introduction of ILSAC GF-7, has accelerated the uptake of sophisticated multi-functional packages that support tighter emission limits and lower viscosities. Asia-Pacific commands both the largest regional presence and the highest growth momentum because manufacturing expansion in China and India underpins robust automotive and industrial lubricant consumption. Competitive dynamics emphasize technology differentiation rather than price, exemplified by Lubrizol’s launch of Solsperse W60 Hyperdispersant in February 2025, a product positioned for next-generation low-SAPs engine oils. Extended drain intervals and electrification temper absolute additive volumes, yet nano-scale innovations and stricter emission standards sustain demand for high-value solutions.

Key Report Takeaways

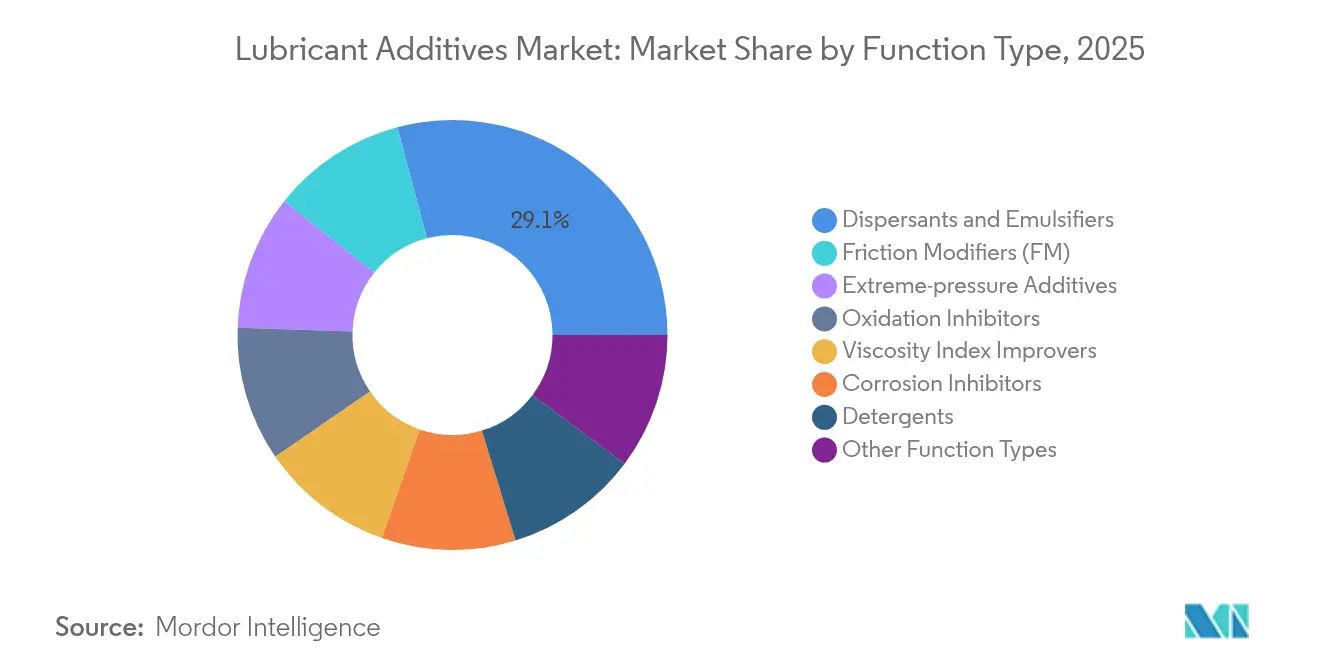

- By function type, dispersants and emulsifiers led with 29.13% revenue share in 2025 and are projected to expand at a 4.32% CAGR through 2031.

- By lubricant type, engine oils accounted for 54.42% share of the lubricant additives market size in 2025 and are forecast to grow at a 3.52% CAGR through 2031.

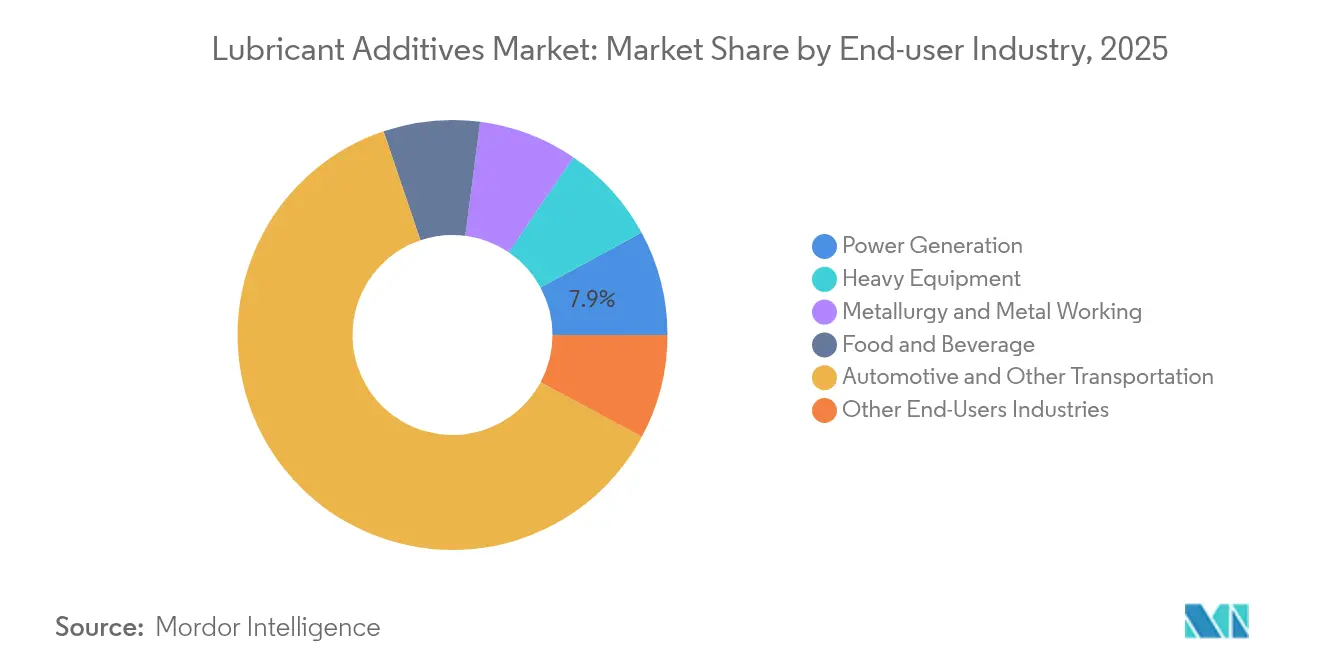

- By end-user industry, automotive and other transportation held 61.95% of the lubricant additives market share in 2025; power generation is advancing at a 4.02% CAGR to 2031.

- By geography, Asia-Pacific captured 45.05% regional share in 2025, and the geography is poised to grow at a 3.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Lubricant Additives Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent environmental regulations on emissions | +1.2% | Global, early adoption in North America and EU | Medium term (2–4 years) |

| Industrial capacity build-up in MEA | +0.8% | Middle East and Africa, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Surging automotive lubricant demand in Asia-Pacific | +0.7% | Asia-Pacific core, secondary impact in MEA | Short term (≤ 2 years) |

| Rising OEM shift to high-performance engine oils | +0.5% | Global, led by North America and Europe | Medium term (2–4 years) |

| Emergence of nano-additive packages | +0.3% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Environmental Regulations on Emissions

ILSAC GF-7 took effect in March 2025 and compels additive suppliers to mitigate low-speed pre-ignition while safeguarding timing chains under tighter phosphorus and sulfur caps. New ACEA 2023 C7 categories in Europe target SAE 0W-16 oils, spurring demand for friction modifiers and viscosity index improvers that deliver at least 0.3% fuel-economy gains versus reference oils. As OEMs push toward 0W-8 grades, additive formulations must reconcile fuel efficiency with wear protection and oxidative stability. This balancing act elevates the value of high-purity detergent chemistries and advanced antiwear boosters. Regulatory convergence across regions accelerates global harmonization of performance standards, incentivizing multinational suppliers to invest in versatile additive platforms rather than region-specific blends. Suppliers that demonstrate rapid certification capabilities secure stronger bargaining power with both blenders and OEMs.

Industrial Capacity Build-up in MEA

Downstream diversification programs under Saudi Arabia’s Vision 2030 have triggered joint ventures that localize additive production close to abundant feedstocks. Projects such as the prospective Aramco-Castrol facility and Richful Group’s partnership with Farabi Petrochemicals illustrate regional momentum toward self-reliance in the lubricant additives market. Integrated complexes lower logistics costs for import-dependent African manufacturers and shorten lead times for customers across the Red Sea corridor. Over the long term, these investments create an export platform serving Asia-Pacific demand spikes while insulating local blenders from global freight volatility. Regional governments also incentivize specialty chemical clusters through tax holidays and preferential land leases, amplifying the financial viability of greenfield facilities. As installed capacity rises, additive suppliers can tailor formulations to climatic extremes and fuel qualities characteristic of MEA markets.

Surging Automotive Lubricant Demand in Asia-Pacific

China added more than 1 million barrels per day of refining capacity during 2024, enabling competitive base-oil output and captive additive integration for domestic consumption. India’s production-linked incentive scheme supports specialty chemical investment, positioning local producers as regional suppliers to ASEAN assemblers. Vehicle parc growth, coupled with the shift toward higher-performance lubricants meeting Bharat Stage VI and China VI standards, lifts per-unit additive value even as oil volumes stabilize. OEM service contracts are increasingly bundled with factory-fill fluids specified to ACEA or API protocols, reinforcing premiumization. Multinationals collaborate with domestic blenders to co-develop formulations adapted to high-sulfur fuel pockets and monsoon humidity. Short-term demand spikes are evident in after-sales service as fleet operators accelerate oil changes before warranty expirations.

Rising OEM Shift to High-Performance Engine Oils

Light-duty vehicle platforms slated for the 2027 model year already specify SAE 0W-16 or 0W-12 oils that demand shear-stable polymer modifiers and ash-optimized detergent systems[1]American Petroleum Institute, “Oil Categories,” api.org . Ford’s adoption of 10W-30 oils for next-generation diesel engines under API FA-4 classification illustrates the trend in the lubricant additives market. OEMs align lubricant recommendations with warranty cost reduction goals, driving additive treat rates that support 15,000-mile drain intervals. The push for lifetime transmission fluids and fill-for-life hybrid e-axle oils further boosts the importance of oxidative inhibitors with elevated seal compatibility. Specification complexity raises entry barriers because passing a single OEM test sequence can cost suppliers more than USD 1 million in bench and fleet trials. Vendors with modular additive platforms and in-house engine testing benches secure preferred-supplier status during new API category rollouts.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extended drain intervals in vehicles and machinery | -0.6% | Global, most pronounced in developed markets | Short term (≤ 2 years) |

| Electrification curbing engine-oil volumes | -0.4% | Global, led by Europe and China | Medium term (2–4 years) |

| Volatile supply of PIB and other key chemistries | -0.3% | Global, acute in regions dependent on imports | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Extended Drain Intervals in Vehicles and Machinery

Passenger-car oil-change intervals in the United States have doubled from 5,000 miles to 10,000 miles, while wind-turbine gearboxes now target 36-month lubricant life cycles. Condition-monitoring sensors embedded in filters enable data-driven maintenance that defers service until oil oxidation or particle levels trigger alarms. Although each oil fill contains a higher additive loading, the aggregate annual additive volume contracts in the lubricant additives market. Blenders therefore shift marketing toward premium long-life brands, squeezing suppliers focused on commodity chemistries. Independent workshops lose service revenue, reinforcing consumer adoption of extended intervals. To compensate, additive manufacturers promote supplemental products such as flush fluids and filter-conditioner tablets, but uptake remains limited.

Electrification Curbing Engine-Oil Volumes

Battery electric vehicles eliminate crankcase lubrication entirely, and hybrid powertrains slash internal-combustion engine runtime per mile traveled. Global BEV stock surpassed 40 million in 2025, displacing roughly 1.5 billion liters of engine oil annually[2]STLE, “Feature,” stle.org . Nevertheless, e-motor cooling and e-axle reduction gears require fluids with tight dielectric and thermal-conductivity windows. These niche fluids depend on synthetic esters blended with copper-friendly additive systems, offering higher margins but lower volumes than traditional engine oils. Suppliers must retool test protocols to cover electrical breakdown voltage and coil-insulation compatibility. Europe and China lead the transition, making them early adopters of specialized e-fluids, while North America follows a hybrid-heavy trajectory that moderates demand erosion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function Type: Dispersants Anchor Modern Multi-Additive Formulations

Dispersants and emulsifiers accounted for 29.13% of 2025 revenues, reflecting their critical role in keeping soot and oxidation by-products suspended to prevent varnish formation. The segment is forecast to grow at a 4.32% CAGR through 2031, outpacing the lubricant additives market as OEMs migrate to gasoline direct-injection engines with elevated particulate loading. The lubricant additives market size attributed to dispersants is projected to expand steadily because regulatory caps on sulfated ash and phosphorus intensify the need for highly efficient polyisobutylene succinimide chemistries that operate at lower treat rates.

Polymeric viscosity index improvers hold the second-largest share, benefiting from the pivot toward low-viscosity grades such as 0W-8 that require robust film strength at high operating temperatures. Detergents and corrosion inhibitors enjoy stable demand as extended drain intervals magnify the importance of base-number retention. Friction modifiers gain relevance in passenger-car and heavy-duty oils targeting a 1% fuel-economy improvement, while extreme-pressure additives remain core to industrial gear oils and metalworking fluids. Suppliers consolidate these chemistries into multi-functional packages to optimize treat levels within stringent ash budgets, a trend that enables formulators to meet global engine-test matrices with fewer SKUs.

By Lubricant Type: Engine Oils Retain Scale but Face Transition Pressures

Engine oils represented 54.42% of 2025 value, demonstrating the centrality of passenger-car and heavy-duty vehicles to the lubricant additives market. Despite electrification headwinds, the segment is expected to post a 3.52% CAGR because remaining combustion engines demand higher-value packages to comply with GF-7 and Euro VII limits. The lubricant additives market share for engine oils will gradually erode as e-mobility scales, yet per-unit additive intensity rises through advanced detergents, antioxidants, and friction modifiers.

Transmission and hydraulic fluids should see a 3.76% CAGR, driven by industrial automation and renewable-energy hydraulics. Metalworking-fluid consumption tracks manufacturing activity in Asia-Pacific, while general industrial oils serve compressors and turbines across power and process industries. Gear-oil demand benefits from offshore wind deployments that necessitate synthetic PAO-based lubricants with high micropitting resistance. Grease sales rise modestly with bearing and chassis applications, though automotive segments face a shift to sealed-for-life components. Process oils remain a niche portfolio for rubber and polymer manufacturing, favoring suppliers with boutique technical support.

By End-User Industry: Power Generation Emerges as the Fastest-Growing Consumer

Automotive and other transportation applications maintained a 61.95% share in 2025 owing to continued internal-combustion dominance in commercial fleets and off-highway machinery. Even as BEV adoption accelerates, diesel trucks, marine vessels, and aviation engines preserve sizable additive demand. The lubricant additives market size in power generation is, however, projected to expand faster at a 4.02% CAGR through 2031, propelled by wind and solar assets that rely on specialty synthetic lubricants requiring high-performance antioxidant and antiwear chemistries.

Heavy equipment segments experience incremental growth from infrastructure spending in emerging economies, necessitating high-load gear oils and hydraulic fluids. Metallurgy and metalworking remain tied to manufacturing output, particularly in East Asia, and count on water-soluble additives to manage thermal loads. Food and beverage end-users adopt NSF-approved white-oil-based lubricants with benign additive systems to minimize contamination risk, a small but premium segment with stringent audit requirements. Across industries, the trend toward predictive maintenance and longer service intervals means each lubricant fill carries a higher concentration of high-performance additives, reinforcing the value proposition for suppliers with advanced formulation capability.

Geography Analysis

Asia-Pacific dominated the global landscape with 45.05% share in 2025 and is anticipated to register a 3.98% CAGR through 2031. China’s vertically integrated petrochemical complexes generate competitively priced Group II and Group III base oils that feed additive blend plants, supporting local and export demand. India leverages production-linked incentives to attract investment in specialty chemicals, transforming the country into a sourcing hub for ASEAN assemblers. Japan and South Korea contribute proprietary polymer modifiers and high-purity dispersants, while Thailand and Vietnam offer cost-efficient blending services for regional OEM service-fill programs.

North America retains significant influence through its role in setting global performance specifications. API and ILSAC committees headquartered in the United States drive new category introductions, supporting the US lubricant additives market and compelling worldwide adoption of accompanying additive test protocols. While vehicle electrification and extended drain intervals temper volume growth, fleet owners in the region demand superior oxidative stability and fuel-efficiency credentials, sustaining high per-unit additive value. Mexico’s expanding automotive assembly capacity further underpins regional demand as OEMs localize supply chains to meet trade-agreement content rules.

Europe combines a mature car parc with some of the world’s strictest environmental regulations. ACEA 2023 standards and Euro VII proposals mandate particulate filter compatibility and ultra-low-viscosity grades, forcing formulators to balance ash limits against turbocharger cleanliness in the lubricant additives market. German chemical majors supply advanced antioxidants and friction modifiers, while the United Kingdom maintains notable additive research and development hubs. Russia’s geopolitical situation restricts technology transfer, yet domestic blenders continue to consume traditional additive packages for industrial oils.

South America experiences moderate expansion led by Brazil, where agricultural mechanization boosts heavy-duty diesel lubricant consumption. Energy reforms in Argentina encourage shale development, translating into gear-oil and hydraulic-fluid demand for drilling equipment. Saudi Arabia’s Vision 2030 downstream projects and United Arab Emirates’ push to become a regional maritime services center stimulate demand for marine and industrial lubricants.

Competitive Landscape

The lubricant additives market exhibits moderate fragmentation. Companies such as Lubrizol, BASF, Afton Chemical, Infineum, and Chevron Oronite are among the leading lubricant additives manufacturers, leveraging broad chemistry portfolios and global engine-test centers to meet complex OEM specifications. Strategic partnerships deepen competitive moats. ExxonMobil’s collaboration with turbine OEMs to co-develop gear-box fluids that withstand micropitting extends product lifecycles and locks in exclusive supply agreements. Innovation pipelines highlight nano-additive research and synthetic ester base-fluid advancements. Start-ups targeting tribology-grade graphene secure venture funding by demonstrating 20% energy-consumption reductions in test rigs. Established suppliers hedge defensively by filing broad patent families covering composite eco-friendly additive systems to forestall disruptive entry.

Lubricant Additives Industry Leaders

The Lubrizol Corporation

AFTON CHEMICAL

BASF

Chevron Corporation

INFINEUM INTERNATIONAL LIMITED

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Lubrizol appointed IMCD Group as its channel partner for lubricant and additive distribution in Vietnam, enabling faster local delivery of specialty packages.

- September 2024: Lubrizol completed a dispersant capacity expansion at its Deer Park, Texas facility to meet rising demand for ILSAC GF-7-compliant additive components.

Global Lubricant Additives Market Report Scope

Lubricant additives are organic or inorganic compounds dissolved or suspended as solids in oil. Specifically, they are added to provide one or more functions in the fluid, when used at a specific treatment rate. The lubricant additives market is segmented by product type, lubricant type, end-user industry, and geography. By product type, the market is segmented by dispersants and emulsifiers, viscosity index improvers, detergents, corrosion inhibitors, oxidation inhibitors, extreme-pressure additives, friction modifiers, and other functions. By lubricant type, the market is segmented by the engine oil, transmission and hydraulic fluids, metal working fluids, general industrial oil, gear oil, grease, process oil, and other lubricant types. By end-user industry, the market is segmented by automotive and other transportation, power generation, heavy equipment, metallurgy, and metal working, food and beverage, other end-user industries. The report also covers the market size and forecasts for the lubricant additives market in 16 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD million).

By Function Type

| Dispersants and Emulsifiers |

| Viscosity Index Improvers |

| Detergents |

| Corrosion Inhibitors |

| Oxidation Inhibitors |

| Extreme-pressure Additives |

| Friction Modifiers (FM) |

| Other Function Types |

By Lubricant Type

| Engine Oil |

| Transmission and Hydraulic Fluid |

| Metalworking Fluid |

| General Industrial Oil |

| Gear Oil |

| Grease |

| Process Oil |

| Other Lubricant Types |

By End-user Industry

| Automotive and Other Transportation |

| Power Generation |

| Heavy Equipment |

| Metallurgy and Metal Working |

| Food and Beverage |

| Other End-Users Industries |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| North America | United States |

| Mexico | |

| Canada | |

| Europe | Germany |

| United Kingdom | |

| Russia | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Function Type | Dispersants and Emulsifiers | |

| Viscosity Index Improvers | ||

| Detergents | ||

| Corrosion Inhibitors | ||

| Oxidation Inhibitors | ||

| Extreme-pressure Additives | ||

| Friction Modifiers (FM) | ||

| Other Function Types | ||

| By Lubricant Type | Engine Oil | |

| Transmission and Hydraulic Fluid | ||

| Metalworking Fluid | ||

| General Industrial Oil | ||

| Gear Oil | ||

| Grease | ||

| Process Oil | ||

| Other Lubricant Types | ||

| By End-user Industry | Automotive and Other Transportation | |

| Power Generation | ||

| Heavy Equipment | ||

| Metallurgy and Metal Working | ||

| Food and Beverage | ||

| Other End-Users Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Mexico | ||

| Canada | ||

| Europe | Germany | |

| United Kingdom | ||

| Russia | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the lubricant additives market in 2026?

It reached USD 18.9 billion in 2026 and is projected to grow at a 3.31% CAGR to USD 22.23 billion by 2031.

Which region drives the most demand for lubricant additives?

Asia-Pacific leads with 45.05% share in 2025 and is expanding at a 3.98% CAGR thanks to manufacturing and automotive growth.

What segment represents the largest share of lubricant additives consumption?

Engine oils accounted for 54.42% of 2025 value, reflecting continued reliance on internal-combustion vehicles.

Why are dispersants critical in modern formulations?

They suspend soot and oxidation by-products, preventing deposits in direct-injection and turbocharged engines where contamination risk is high.

How does electrification affect additive demand?

Battery electric vehicles remove engine-oil demand, but specialized e-axle and cooling fluids create smaller yet higher-value opportunities.

Which drivers support long-term growth despite volume headwinds?

Stricter emission regulations, OEM migration to ultra-low-viscosity oils, and nano-additive innovation sustain premium additive demand.

Page last updated on: