Organ Care Systems (OCS) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

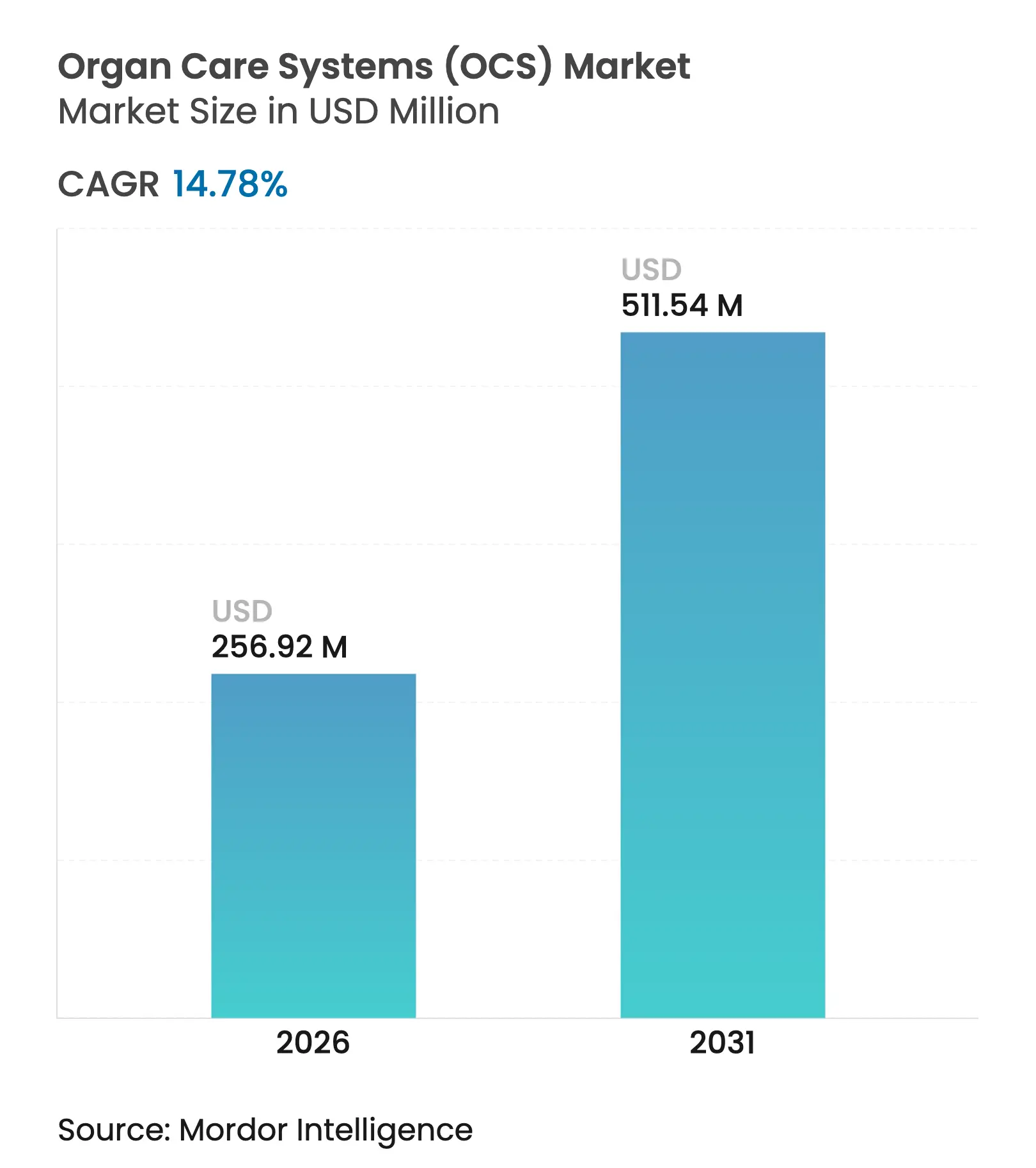

| Market Size (2026) | USD 256.92 Million |

| Market Size (2031) | USD 511.54 Million |

| Growth Rate (2026 - 2031) | 14.78 % CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Organ Care Systems (OCS) Market Analysis by Mordor Intelligence

The organ care systems market size is expected to grow from USD 223.86 million in 2025 to USD 256.92 million in 2026 and is forecast to reach USD 511.54 million by 2031 at 14.78% CAGR over 2026-2031. Sustained demand follows the clinical shift toward normothermic perfusion, which supports longer preservation windows, reduces primary graft dysfunction and broadens acceptance of marginal donor organs. Government-backed xenotransplantation studies, the PRINT bioprinting initiative and THEA whole-eye transplantation program reinforce R&D momentum, while venture capital injections above USD 200 million in 2024-2025 finance startup innovation across portable, AI-enabled devices.

Key Report Takeaways

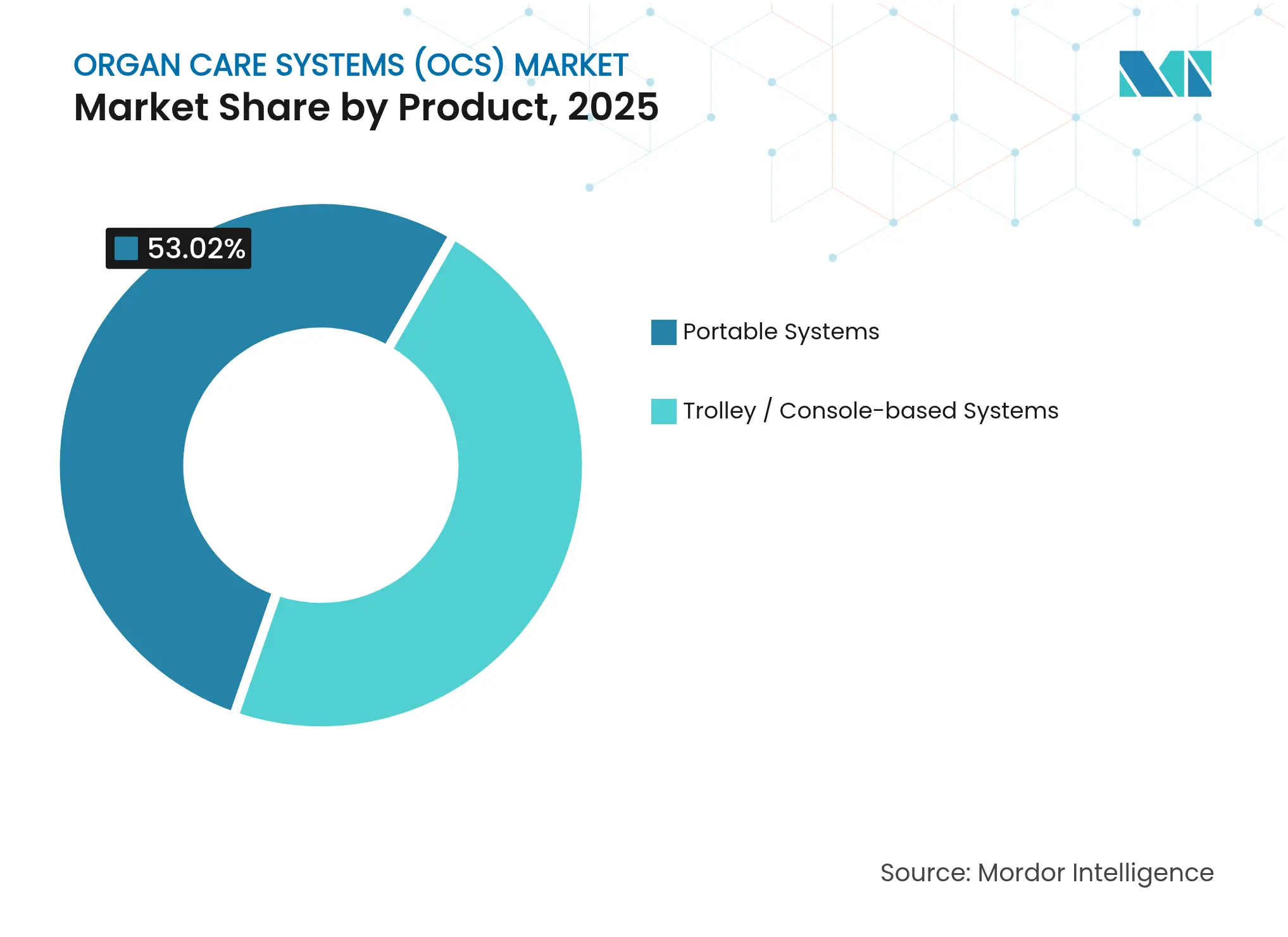

- By product type, portable systems led with 53.02% of organ care systems market share in 2025, and that segment is expanding at a 15.92% CAGR to 2031.

- By technology, normothermic perfusion commanded 58.05% revenue share of the organ care systems market size in 2025 and shows a 15.78% CAGR through 2031.

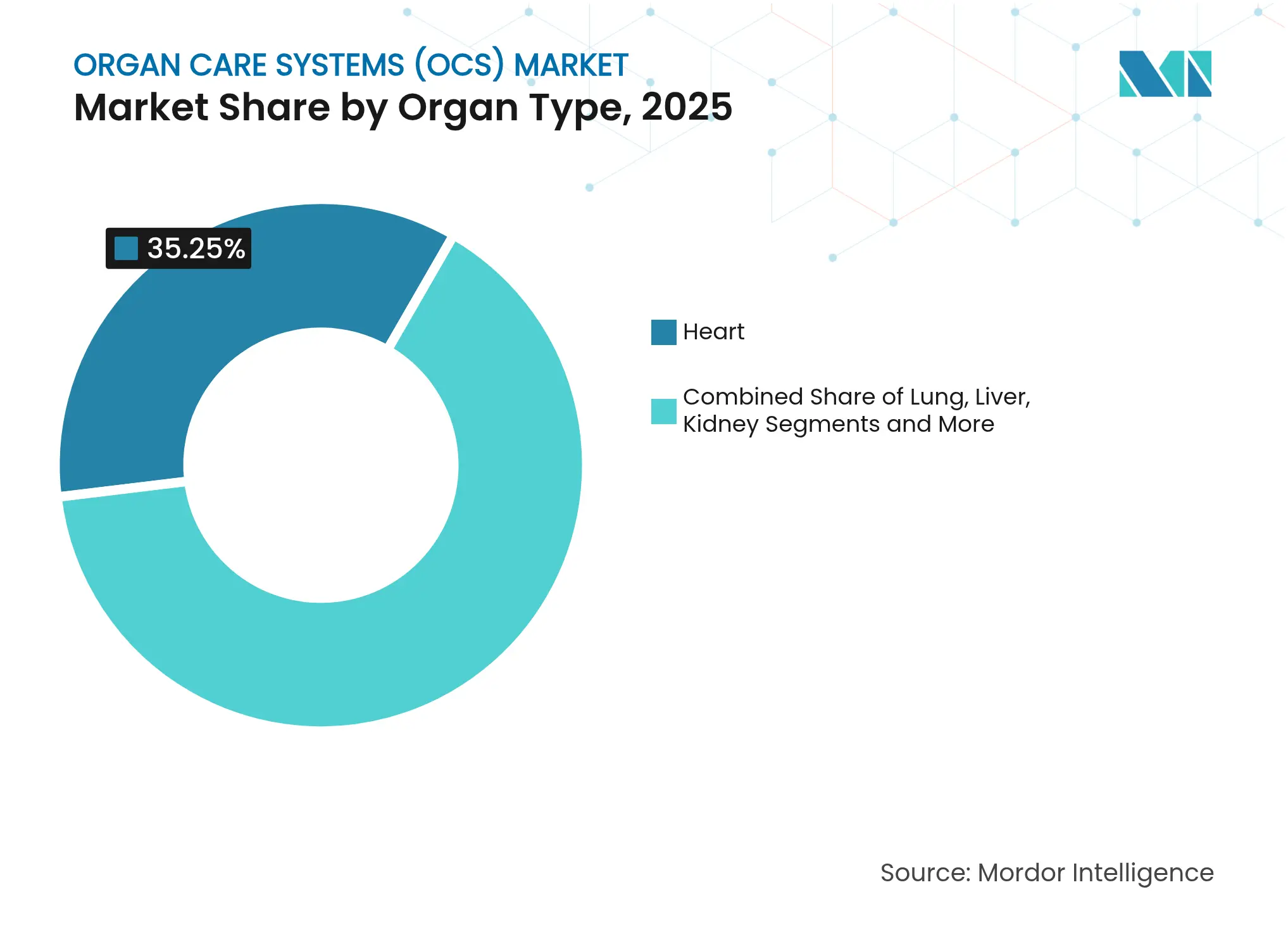

- By organ type, heart preservation contributed 35.25% to 2025 revenues, whereas lung preservation is projected to rise at 17.05% CAGR to 2031 within the organ care systems market.

- By end-user, transplant centers held 45.20% of organ care systems market share in 2025; organ procurement organizations are advancing at a 16.85% CAGR toward 2031.

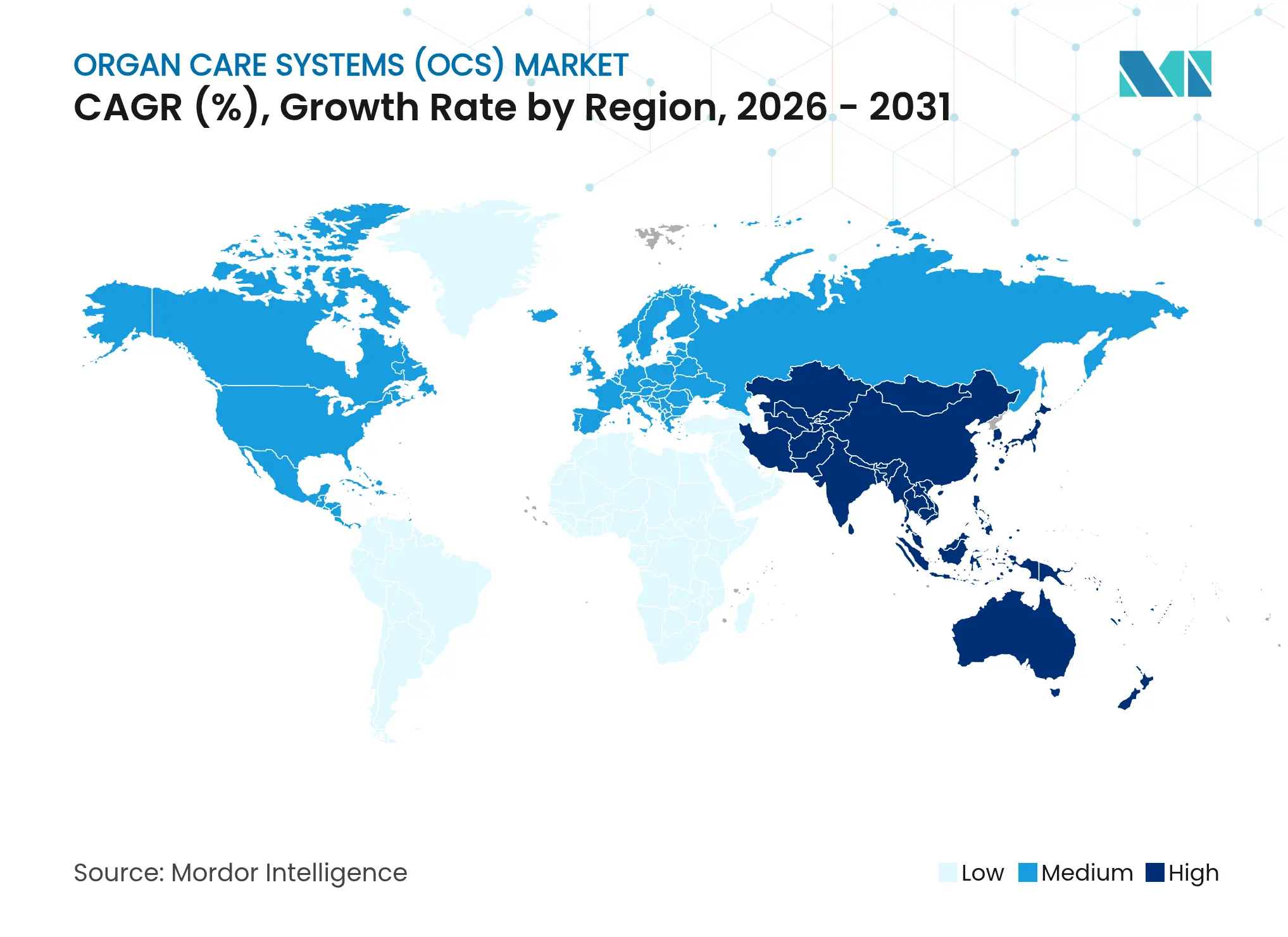

- By geography, North America captured 38.30% of 2025 revenues, while Asia-Pacific records the highest growth at 15.95% CAGR to 2031 in the organ care systems market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Organ Care Systems (OCS) Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Growing Incidence Of Organ Failure & Transplant Demand

Growing Incidence Of Organ Failure & Transplant Demand

| 4.2% | Global | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

4.2%

| Geographic Relevance:

Global

| Impact Timeline:

Long term (≥ 4 years)

|

Rising Adoption Of Normothermic Perfusion Platforms

Rising Adoption Of Normothermic Perfusion Platforms

| 3.8% | North America & EU | Medium term (2-4 years) | |||

Scaling Xenotransplant Clinical Trials

Scaling Xenotransplant Clinical Trials

| 2.9% | Global, with early gains in US, UK | Medium term (2-4 years) | |||

Government-Funded Organ-Preservation R&D Programs

Government-Funded Organ-Preservation R&D Programs

| 2.4% | APAC core, spill-over to MEA | Long term (≥ 4 years) | |||

Venture Capital Inflow Into Perfusion-Tech Start-Ups

Venture Capital Inflow Into Perfusion-Tech Start-Ups

| 1.6% | North America & EU | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Growing Incidence Of Organ Failure & Transplant Demand

Chronic kidney disease affects 850 million individuals, and heart failure cases exceed 64 million worldwide, creating structural demand for solutions that raise transplant utilization. The WHO notes that only 1% of transplants occur in low-income nations, underlining growth headroom as health infrastructure evolves[1]Advanced Research Projects Agency for Health, “ARPA-H FY 2025,” arpa-h.gov Source: World Health Organization, “HPS/OOD,” who.int. Modern organ care systems market devices prolong transport time, directly addressing shortages that leave 120,000 Americans on waiting lists. Population aging, diabetes prevalence and better critical-care survival rates expand transplant eligibility, broadening the install base for organ care systems.

Rising Adoption Of Normothermic Perfusion Platforms

Prospective studies show normothermic perfusion cuts graft dysfunction to 11% from 28% under static cold storage, prompting protocol updates at major transplant centers. American Society of Transplant Surgeons guidelines issued in 2024 accelerate procurement-organization uptake. Continuous, warm-blood perfusion also enables functional testing, salvaging marginal organs that would otherwise be discarded. Economic modeling shows postoperative complication savings offset higher device costs, reinforcing purchasing decisions within value-based care systems.

Scaling Xenotransplant Clinical Trials

The FDA cleared the first genetically modified pig-kidney trial in March 2025, moving xenotransplantation from compassionate use to organized clinical study[2]Nature, “World-first pig kidney trials mark turning point for xenotransplantation,” nature.com. United Therapeutics’ UKidney program may enroll 50 renal-failure patients and relies on advanced preservation to safeguard modified organs during transport. Proven viability standards are set higher for xenografts, driving demand for specialized perfusion circuits capable of controlling coagulation and complement activation.

Government-Funded Organ-Preservation R&D Programs

ARPA-H allocated USD 1.5 billion for PRINT and THEA programs in FY 2025 to push boundaries in organ bioprinting and ocular transplantation. An NIH xenotransplantation cooperative earmarked USD 6.4 million for research into graft immune tolerance and innovative preservation. The U.S. DoD invested USD 41 million in trauma-care preservation devices suitable for battlefield deployment, accelerating dual-use technology pathways.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High CAPEX & OPEX Of Perfusion Devices

High CAPEX & OPEX Of Perfusion Devices

| -2.8% | Global | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

-2.8%

| Geographic Relevance:

Global

| Impact Timeline:

Medium term (2-4 years)

|

Stringent Multi-Region Regulatory Approvals

Stringent Multi-Region Regulatory Approvals

| -2.1% | Global, with early gains in US, EU | Long term (≥ 4 years) | |||

Limited Logistics Capacities In Low-Income Nations

Limited Logistics Capacities In Low-Income Nations

| -1.4% | MEA, parts of APAC and South America | Long term (≥ 4 years) | |||

Persistent Shortage Of Trained Perfusionists

Persistent Shortage Of Trained Perfusionists

| -1.2% | Global | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High CAPEX & OPEX Of Perfusion Devices

Procurement expenses exceed USD 36,000 per organ for heart and kidney retrieval, and advanced devices add capital outlays that strain hospital budgets. Consumable circuits, proprietary perfusate solutions and 24/7 monitoring elevate operating expenses beyond static storage, challenging adoption in cost-sensitive environments.

Stringent Multi-Region Regulatory Approvals

The EU Medical Device Regulation and the FDA review periods—averaging 2,275 days for liver devices—extend commercialization cycles and require multiple clinical trials per geography. Japan’s devices-lag hampers patient access, highlighting persistent approval fragmentation.

Segment Analysis

By Product: Portable Systems Lead Infrastructure-Independent Adoption

Portable platforms captured 53.02% of 2025 revenue in the organ care systems market, propelled by deployment flexibilities in ambulances, aircraft and donor-hospital operating rooms. Paragonix SherpaPak cut 4-year mortality by 54% relative to ice storage, underscoring clinical gains that buttress a 15.92% CAGR outlook through 2031. Users prioritize devices that operate without external oxygen or temperature control infrastructures, meeting requirements of resource-constrained settings and long-distance retrieval missions. The organ care systems market size for portable units is projected to expand rapidly as defense and humanitarian organizations adopt backpack-scale perfusion units for austere environments. Console-based platforms, while ceding share, remain indispensable at high-volume transplant centers requiring continuous perfusion longer than 24 hours. Manufacturers now bundle portable cages with centralized analytics dashboards, allowing cloud-based performance monitoring across distributed fleets, aligning with value-based procurement contracts.

Console systems continue to service complex liver and lung cases needing advanced metabolic readouts and integrated imaging. However, improved battery life, miniaturized sensors and disposable sterile chambers narrow the performance gap, enabling portable devices to handle increasingly complex organs. Supply-chain simplification—fewer reusable parts and standardized consumables—lowers operating outlays, lifting adoption among mid-tier hospitals. Competitive differentiation centers on ease of priming, automated flow control and AI-assisted endpoint predictions that reduce technician workload. Device rental models also democratize access by shifting CAPEX to operating budgets, mitigating earlier cost barriers. As a result, the organ care systems market will likely witness portable systems accounting for more than half of all shipments well before the forecast horizon ends.

Note: Segment shares of all individual segments available upon report purchase

By Technology: Normothermic Perfusion Dominates Clinical Adoption

Normothermic solutions held 58.05% revenue share in 2025 within the organ care systems market, buoyed by peer-reviewed data showing 11% graft dysfunction versus 28% for cold storage. That advantage underpins a 15.78% CAGR, the highest among technologies. Warm-blood perfusion preserves cellular metabolism, enabling longer out-of-body times and post-retrieval diagnostics that inform acceptance decisions. The organ care systems market size for normothermic units is expanding further as payers recognize reduced ICU stays and fewer readmissions. Hypothermic machine perfusion retains relevance for kidneys, offering cost-effective outcomes when cold ischemia time is under eight hours. Static storage enhancers persist as backup, especially in low-resource geographies.

Clinicians increasingly tailor protocol selection to organ type and donor profile. Liver programs employ hybrid approaches—cold transport followed by normothermic reconditioning—blunting ischemia-reperfusion injuries. AI-assisted flow algorithms now personalize perfusate composition in real time, adjusting electrolytes and oxygen tension to donor-specific metabolic status. Software upgrades enable remote oversight by transplant surgeons during ground or air transport, supporting centralized decision making. Technology suppliers differentiate via disposable cartridge pricing and subscription analytics bundles, shifting value capture from hardware to data services. The organ care systems market, therefore, is migrating toward integrated hardware-software ecosystems that monetize continual device telemetry.

By Organ Type: Lung Preservation Achieves Fastest Growth Trajectory

Heart preservation represented 35.25% of 2025 sales in the organ care systems market, reflecting the critical mortality risk and reimbursement priority of cardiac transplants. Lung systems post the swiftest growth at 17.05% CAGR, propelled by HOPE techniques that extend viable preservation to 20 hours—double earlier benchmarks. Liver devices enjoy growing uptake thanks to OrganOx metra, which surpassed 5,000 clinical uses, demonstrating mature evidence of reduced early allograft dysfunction.

Kidney preservation remains a volume mainstay, benefiting from broad acceptance of hypothermic perfusion and emerging dual-temperature cycles that refresh mitochondrial respiration. Pancreas systems remain nascent but gained momentum after FDA clearance of Paragonix PancreasPak in 2024, signaling regulatory confidence in niche organ-specific devices. Forward adoption patterns indicate xenotransplant livers and kidneys will generate incremental demand for higher-capacity circuits and xenograft-compatible synthetic perfusates. Consequently, the organ care systems market size for lung and liver modalities will expand more quickly than heart as new indications emerge.

Note: Segment shares of all individual segments available upon report purchase

By End-User: Organ Procurement Organizations Drive Fastest Expansion

Transplant centers controlled 45.20% of 2025 revenues in the organ care systems market, leveraging in-house devices to widen donor criteria and cut cold ischemia times. Organ procurement organizations (OPOs) post a 16.85% CAGR as their field teams integrate portable perfusion into standard retrieval workflows. Federal policy allowing OPOs to bill separately for perfusion capital has also accelerated deployment. The organ care systems market share for OPOs therefore continues to rise as centralized recovery stations adopt fleet management software that matches device availability to real-time donor alerts.

Hospitals without transplant programs but with trauma units deploy basic hypothermic equipment for organ stabilization before regional transfer, yet budgetary priorities keep growth moderate. Meanwhile, military medical facilities evaluate ruggedized platforms designed to fit forward operating bases, potentially opening a specialized sub-segment. Education institutions partner with device makers to create simulation curricula that alleviate the shortage of perfusionists. By 2031, OPOs are forecast to manage more than half of portable perfusion logistics, reshaping procurement patterns and influencing vendor R&D directions.

Geography Analysis

North America accounted for 38.30% of 2025 organ care systems market revenues, supported by the FDA’s clearance of TransMedics OCS Heart and continuous reimbursement of device disposables. Europe maintains significant presence, propelled by harmonized procurement frameworks and broad acceptance of normothermic platforms. The organ care systems market size in Asia-Pacific is accelerating at 15.95% CAGR as China and India invest heavily in transplant infrastructure and adopt portable devices for long-distance retrievals.

Japan confronts sociocultural donor shortages, yet technology adoption is aided by a focus on quality and device reliability, positioning it as an early adopter of AI-assisted perfusion software. Middle East and Africa see growing interest, particularly in Gulf Cooperation Council states that import donor organs from abroad and thus value longer preservation times. South America registers moderate expansion, with Brazil piloting lung perfusion hubs that could seed regional growth. Cross-border collaborations—such as Australasian retrieval networks linking Indonesia, Singapore and Australia—underscore the role of logistics integration in lifting adoption across geographies.

Competitive Landscape

Market Concentration

Moderate market concentration characterizes the organ care systems market, with strategic acquisitions reshaping portfolios. Getinge’s USD 477 million purchase of Paragonix in 2024 expanded its presence beyond cardiopulmonary bypass into portable preservation. Bridge to Life bolstered its hypothermic offering by acquiring VitaSmart kidney perfusion technology. Vendors compete by publishing registry outcomes; Paragonix reported 27% fewer liver complications using LIVERguard versus ice, reinforcing evidence-based marketing.

Artificial-intelligence modules capable of predicting graft viability at the point of recovery have become key differentiators, prompting alliances between device firms and analytics startups. Manufacturers also pursue region-specific regulatory strategies that synchronize FDA, EMA and PMDA submissions, reducing time-to-launch. Venture capital supports challengers like X-Therma, whose USD 22.4 million Series B funds cryoprotectant development for multi-day preservation. Logistical partnerships—exemplified by DHL’s 2025 acquisition of CRYOPDP—extend cold-chain expertise into organ transport, broadening ecosystem boundaries.

Company strategies increasingly revolve around integrated service models bundling hardware, disposables, telemetry analytics and on-site training into multiyear contracts. Such offerings foster customer lock-in and elevate switching costs. As registry datasets mature, outcome-based pricing models that link consumable payments to graft-survival milestones are under pilot at several U.S. transplant centers. Competitive intensity will likely rise as xenotransplant-specific systems enter clinical phases, encouraging further consolidation as diversified med-tech firms seek to cover all organ categories under single solution suites.

Organ Care Systems (OCS) Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Paragonix Technologies reported that LIVERguard reduced post-transplant complications by 27%, including marked declines in acute kidney injury and early allograft dysfunction.

- December 2024: The UK completed its first double-lung transplant using an ex-vivo lung perfusion XPS system, validating six-hour revival and assessment capabilities.

Table of Contents for Organ Care Systems (OCS) Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Growing Incidence Of Organ Failure & Transplant Demand

- 4.2.2Rising Adoption Of Normothermic Perfusion Platforms

- 4.2.3Scaling Xenotransplant Clinical Trials

- 4.2.4Government-Funded Organ-Preservation R&D Programs

- 4.2.5Venture Capital Inflow Into Perfusion-Tech Start-Ups

- 4.3Market Restraints

- 4.3.1High CAPEX & OPEX Of Perfusion Devices

- 4.3.2Stringent Multi-Region Regulatory Approvals

- 4.3.3Limited Logistics Capacities In Low-Income Nations

- 4.3.4Persistent Shortage Of Trained Perfusionists

- 4.4Porter's Five Forces

- 4.4.1Threat of New Entrants

- 4.4.2Bargaining Power of Buyers

- 4.4.3Bargaining Power of Suppliers

- 4.4.4Threat of Substitute Products

- 4.4.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Product

- 5.1.1Portable Systems

- 5.1.2Trolley / Console-based Systems

- 5.2By Technology

- 5.2.1Normothermic Perfusion

- 5.2.2Hypothermic Machine Perfusion

- 5.2.3Static Cold Storage Enhancers

- 5.3By Organ Type

- 5.3.1Heart

- 5.3.2Lung

- 5.3.3Liver

- 5.3.4Kidney

- 5.3.5Others

- 5.4By End-user

- 5.4.1Transplant Centers

- 5.4.2Hospitals

- 5.4.3Organ Procurement Organisations

- 5.5Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4South Korea

- 5.5.3.5Australia

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1TransMedics

- 6.3.2XVIVO Perfusion AB

- 6.3.3Bridge to Life Ltd

- 6.3.4Paragonix Technologies Inc.

- 6.3.5OrganOx Ltd

- 6.3.6Organ Recovery Systems Inc.

- 6.3.7Preservation Solutions Inc.

- 6.3.8Waters Medical Systems LLC

- 6.3.9Organ Assist BV (NED)

- 6.3.10EBERS Medical

- 6.3.11Lung Bio-engineering Inc.

- 6.3.12Precardix Medical

- 6.3.13Bridge Organ Technologies

- 6.3.14Bridge to Life

- 6.3.15Shenzhen Trautec Medical

- 6.3.16Genext Medical

- 6.3.17BridgeLink Medical

- 6.3.18Korea Organ Bank

- 6.3.19Bridge Organ Support AB

- 6.3.20Transonic Systems

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Organ Care Systems market as all normothermic or hypothermic devices that actively perfuse and monitor donor hearts, lungs, livers, or kidneys outside the body, whether configured as trolley units used inside the hospital or portable consoles designed for road or air retrieval missions. Mordor Intelligence measures only new hardware and its disposable perfusion sets, valued in USD.

Scope exclusion: cold-storage solution bags and static ice boxes fall outside this boundary.

Segmentation Overview

- By Product

- Portable Systems

- Trolley / Console-based Systems

- Portable Systems

- By Technology

- Normothermic Perfusion

- Hypothermic Machine Perfusion

- Static Cold Storage Enhancers

- Normothermic Perfusion

- By Organ Type

- Heart

- Lung

- Liver

- Kidney

- Others

- Heart

- By End-user

- Transplant Centers

- Hospitals

- Organ Procurement Organisations

- Transplant Centers

- Geography

- North America

- United States

- Canada

- Mexico

- United States

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Germany

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- China

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- GCC

- South America

- Brazil

- Argentina

- Rest of South America

- Brazil

- North America

Detailed Research Methodology and Data Validation

Primary Research

Telephone interviews and online surveys with transplant surgeons, procurement coordinators, biomedical engineers, and hospital buyers across North America, Europe, and high-growth Asia-Pacific nations helped us validate average selling prices, utilization hours per device, and the pace at which centers shift from ice to warm perfusion. These discussions filled data gaps and refined model assumptions flagged during desk work.

Desk Research

We began with authoritative public datasets such as the WHO Global Observatory on Donation and Transplantation, United Network for Organ Sharing, Eurotransplant annual statistics, and the US FDA 510(k) database, which reveal procedure volumes, donor trends, and recent device clearances. Trade association releases, peer-reviewed papers in Transplantation and The Journal of Heart and Lung Transplantation, plus transplant center registries add evidence on organ viability windows and adoption of perfusion technology. Company filings, investor decks, and news feeds drawn from D&B Hoovers and Dow Jones Factiva round out cost, pricing, and installed-base clues. The secondary sources cited here are illustrative; many other public and paid references were reviewed for context and cross-checks.

Market-Sizing & Forecasting

A top-down build starts with annual deceased-donor organ retrieval counts by organ and region, which are multiplied by validated perfusion penetration rates to derive potential procedures. Results are corroborated through selective bottom-up roll-ups that blend sampled ASPs with installed base growth reported by suppliers, allowing modest adjustments where signals diverge. Key variables in the model include heart and lung transplant volumes, average perfusion kit consumption per case, capital replacement cycles, reimbursement policy shifts, and regulatory approvals of next-generation consoles. Multivariate regression, informed by three macro indicators (ICU bed additions, donor registration rates, and per capita healthcare spend), shapes the 2025-2030 forecast path. Gaps in bottom-up data are bridged by weighted regional proxies anchored to confirmed procurement costs.

Data Validation & Update Cycle

Outputs pass an analyst peer review that hunts for outliers versus historical transplant ratios, customs shipment values, and share of organ totals. Anomalies trigger re-checks with interview respondents before sign-off. The dataset refreshes every year, and mid-cycle updates are issued when material events, such as new FDA approvals or reimbursement code changes, alter demand expectations.

Why Mordor's Organ Care Systems Baseline Earns Decision-Makers' Trust

Benchmark comparison

Published market values often differ because each firm selects its own device mix, geography slate, and forecast cadence. Our disciplined scope, refreshed assumptions, and dual-track modeling keep the baseline anchored to transplant realities, not broad preservation accessories.

Key gap drivers include competitors excluding trolley platforms, omitting emerging Asian donor programs, applying flat ASP curves, or rolling forward 2023 procedure counts without verifying 2024 recovery growth. Our annual refresh and penetration rate audits help Mordor Intelligence stay current while others may lag.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 223.86 mn (2025) | Mordor Intelligence | Anonymized source:Mordor Intelligence | Primary gap driver: | |

USD 165.95 mn (2024) | Global Consultancy A | Narrow product basket and limited hospital sample set | ||

USD 168.26 mn (2024) | Trade Journal B | Combines transplant boxes yet excludes normothermic consoles | ||

USD 201.78 mn (2025) | Industry Tracker C | Covers only 15 countries and applies uniform ASP erosion |