Ostomy Care Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

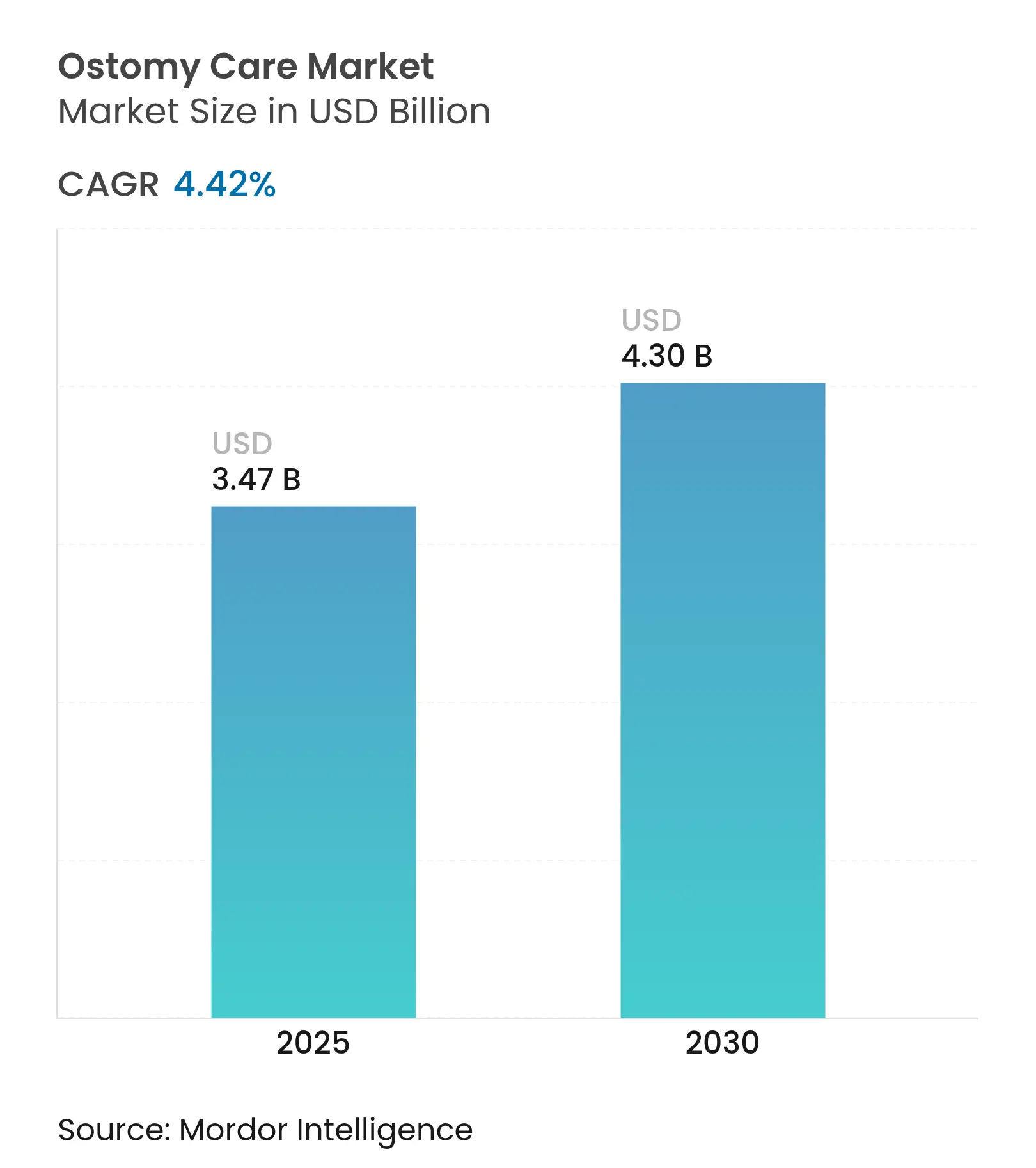

| Market Size (2025) | USD 3.47 Billion |

| Market Size (2030) | USD 4.30 Billion |

| Growth Rate (2025 - 2030) | 4.42 % CAGR |

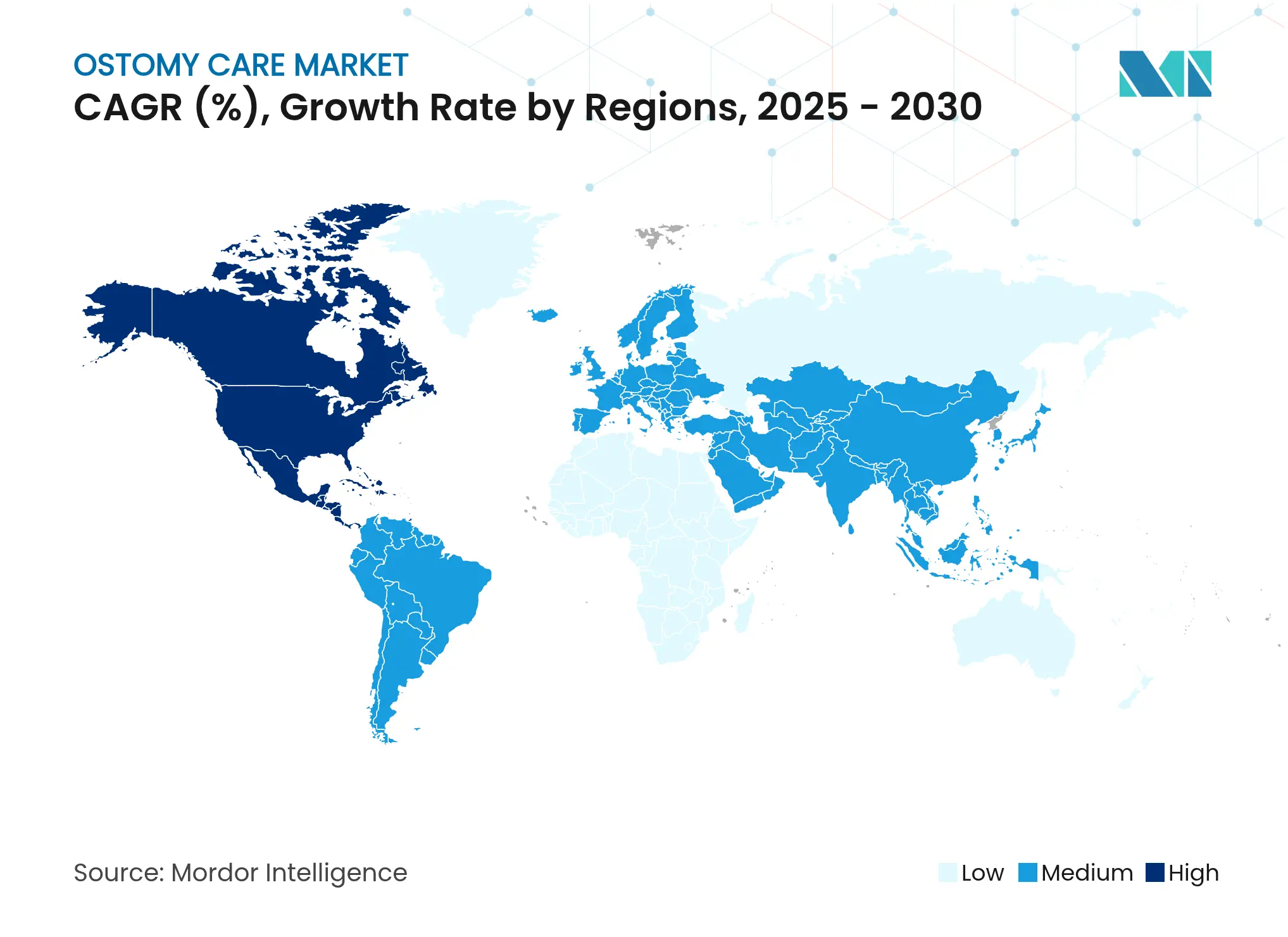

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Ostomy Care Market Analysis by Mordor Intelligence

The ostomy care market size reached USD 3.47 billion in 2025 and is on track to reach USD 4.30 billion by 2030, reflecting a steady 4.42% CAGR. Consistent demand arises from aging populations, climbing inflammatory bowel disease (IBD) prevalence, and ongoing technology upgrades that simplify self-management. Digital sensor–equipped pouches, PFAS-free barrier films, and three-dimensional (3-D) printed appliances stand out as near-term differentiators. Regional demand skews toward developed economies with broad reimbursement, yet Asia-Pacific is accelerating as surgical volumes rise and specialist care capacity expands. Competitive intensity remains moderate; three multinationals dominate core product portfolios while niche entrants exploit skin-protection technologies and remote-monitoring add-ons. Across all regions, reimbursement reforms and virtual nurse programs foster earlier hospital discharge and stronger adherence, underpinning durable growth in the ostomy care market.

Key Report Takeaways

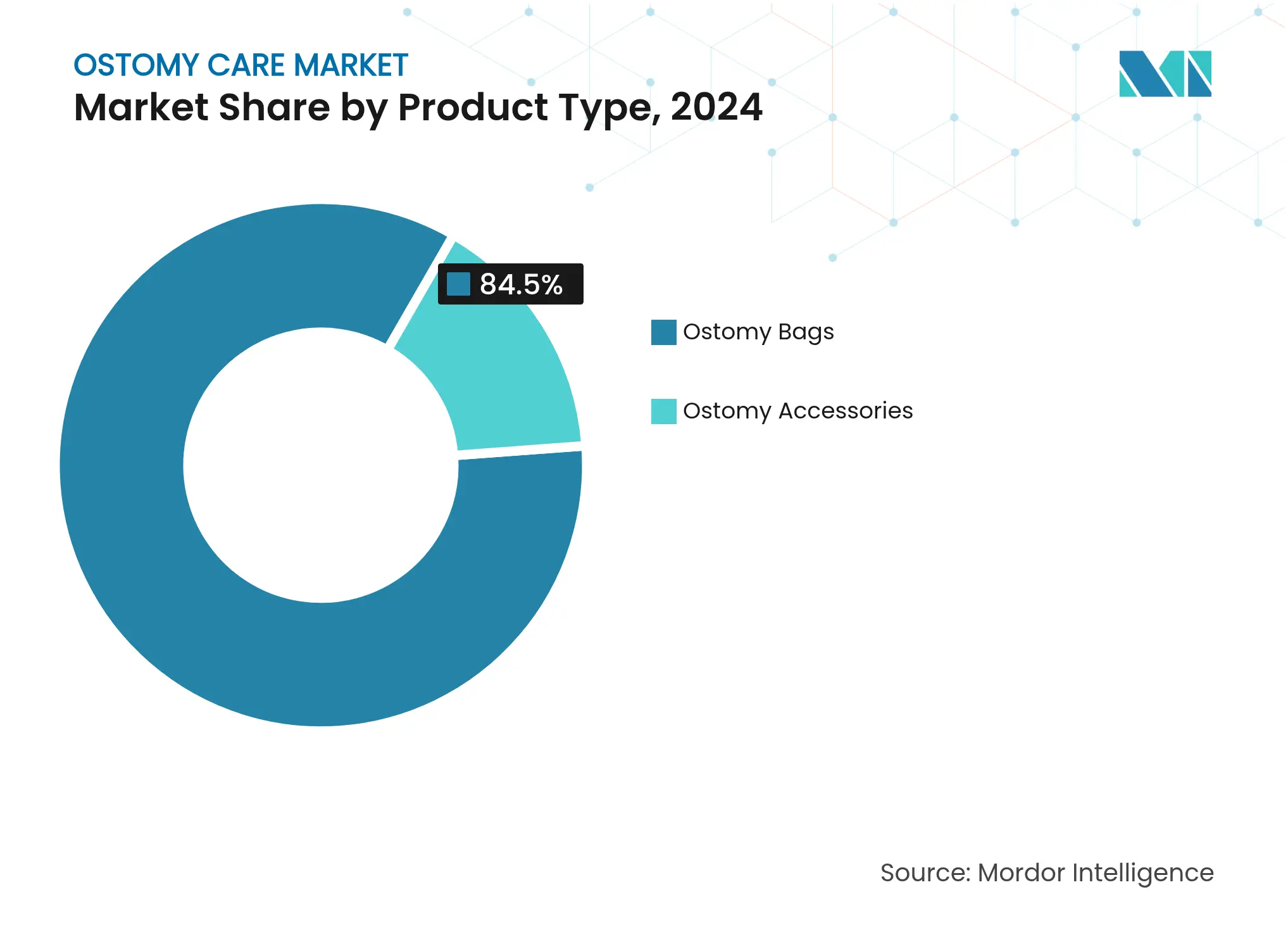

- By product category, ostomy bags led with 84.56% revenue share in 2024; accessories are projected to advance at a 5.12% CAGR to 2030.

- By surgery type, colostomy accounted for 44.34% of the ostomy care market share in 2024, while ileostomy is forecast to expand at a 5.71% CAGR through 2030.

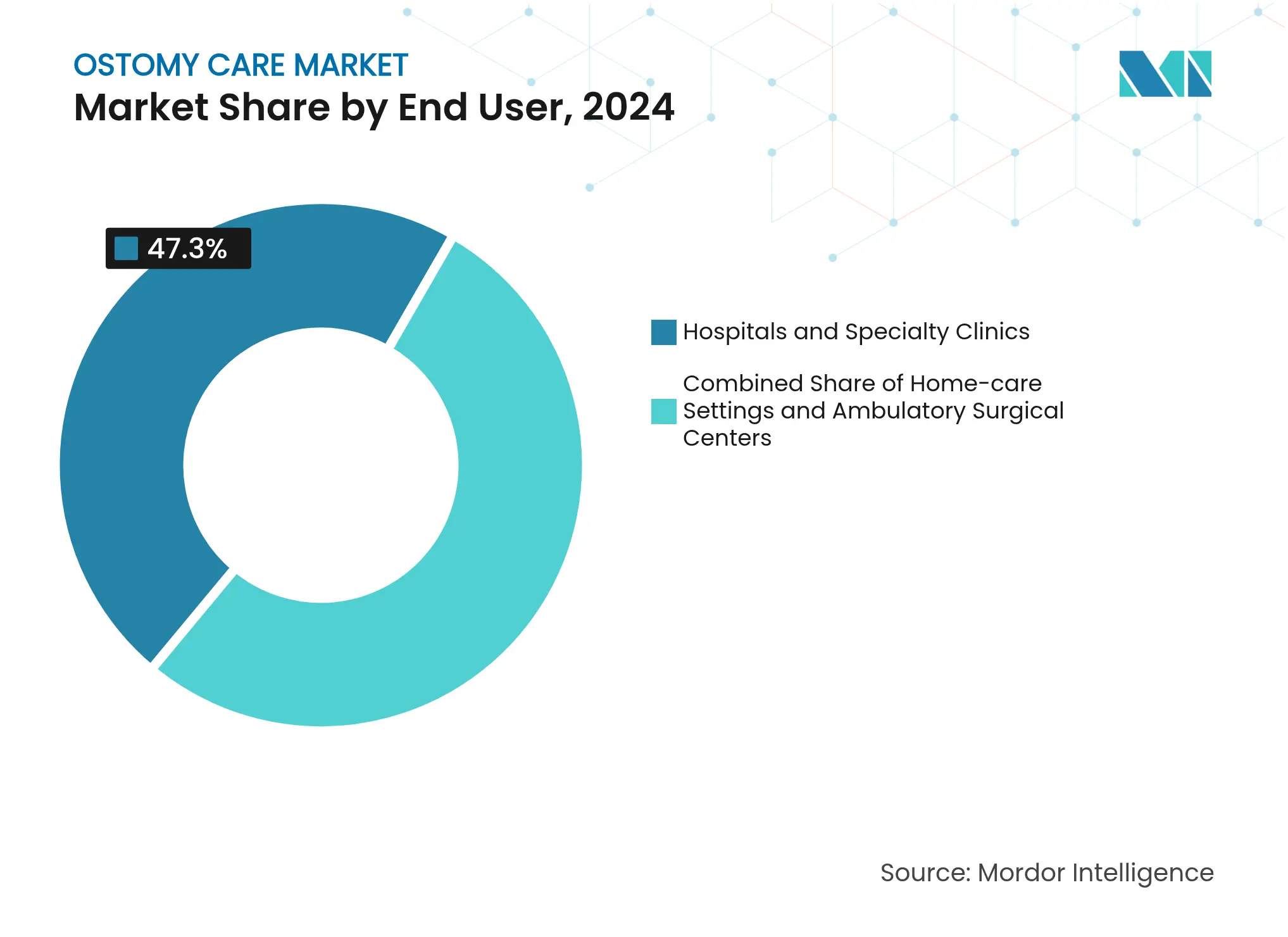

- By end user, home-care settings captured 47.32% share of the ostomy care market size in 2024 and hospitals & specialty clinics are advancing at a 5.87% CAGR through 2030.

- By geography, North America held 42.87% revenue share in 2024; Asia-Pacific is set to grow at 6.25% CAGR through 2030.

Global Ostomy Care Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising prevalence of IBD & colorectal cancer

Rising prevalence of IBD & colorectal cancer

| +1.2% | Global; highest acceleration in Asia-Pacific & LatAm | Long term (≥ 4 years) |

(~) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

Global; highest acceleration in Asia-Pacific & LatAm

|

Impact Timeline

:

Long term (≥ 4 years)

|

Rapid product & material innovation

Rapid product & material innovation

| +0.8% | North America & EU lead; spillover to emerging markets | Medium term (2-4 years) | |||

Accelerating geriatric ostomy population

Accelerating geriatric ostomy population

| +0.9% | Global; strongest in high-income economies | Long term (≥ 4 years) | |||

Expanding patient-support & awareness plans

Expanding patient-support & awareness plans

| +0.6% | North America & EU core; expanding to Asia-Pacific | Short term (≤ 2 years) | |||

3-D printed customized appliances

3-D printed customized appliances

| +0.4% | North America & EU initially; gradual global adoption | Medium term (2-4 years) | |||

Reimbursement expansion for home DME supply

Reimbursement expansion for home DME supply

| +0.5% | Primarily North America; EU & developed Asia-Pacific | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Prevalence of IBD & Colorectal Cancer

IBD now affects 2.4–3.1 million Americans and continues to spread into newly industrialized regions where lifestyle shifts mimic Western patterns [1]Centers for Disease Control and Prevention, “Inflammatory Bowel Disease Prevalence,” cdc.gov. The epidemiological transition increases ostomy surgery volumes, particularly where colorectal cancer risk compounds with long-standing inflammation. Improved survival extends lifetime device use, deepening demand for replacement pouches and accessories. Health systems in Asia-Pacific struggle with insufficient chronic-care infrastructure, creating white-space opportunities for tele-education and mobile nurse consults. As a result, the ostomy care market grows through both higher procedure incidence and longer patient lifespans.

Rapid Product & Material Innovation

Breakthroughs move beyond incremental pouch redesign. Coloplast’s digital leakage notification system embeds sensors that alert users before failures, shifting care from reactive to predictive. Ceramide-infused wafers and moldable hydrocolloids cut dermatitis rates that historically affected more than 60% of wearers. 3-D printed bases fit individual anatomy, lowering leakage and improving comfort. Simultaneously, PFAS bans in Europe and parts of North America drive R&D toward fluorine-free films that retain hydrophobicity. These innovations reinforce competitive moats and lengthen replacement cycles, propelling the ostomy care market.

Accelerating Geriatric Ostomy Population

Patients aged ≥ 70 account for a growing share of new procedures, with 59.2% receiving permanent stomas versus 41.1% in younger cohorts. Older users face dexterity limits, comorbidities, and longer hospital stays, increasing reliance on simplified closures and remote nurse coaching. Higher complication risk raises healthcare resource utilization, yet creates pull-through for leak-proof pouches and skin-friendly pastes. Demographic aging therefore amplifies baseline sales volumes across mature economies within the ostomy care market.

Expanding Patient-Support & Awareness Programs

ConvaTec’s me+ platform pairs each new patient with certified ostomy nurses, personalized lifestyle coaching, and peer networks, cutting unscheduled visits by 500%. The UOAA Virtual Ostomy Clinic extends specialist access to rural areas, while app-based self-tracking halves the time to independent self-care. Such programs underpin product loyalty and drive recurring revenue as users stay within a single brand’s ecosystem. They also lower complication rates, indirectly lifting long-term market growth.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Peristomal skin complications & infections

Peristomal skin complications & infections

| -0.7% | Global; higher where specialist access is scarce | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

-0.7%

|

Geographic Relevance

:

Global; higher where specialist access is scarce

|

Impact Timeline

:

Medium term (2-4 years)

|

High cost of advanced multi-piece systems

High cost of advanced multi-piece systems

| -0.5% | Emerging markets & uninsured cohorts worldwide | Short term (≤ 2 years) | |||

Social stigma & psychological burden

Social stigma & psychological burden

| -0.4% | Global; culturally variable | Long term (≥ 4 years) | |||

Pending PFAS restrictions on barrier films

Pending PFAS restrictions on barrier films

| -0.3% | EU & North America; global spillover possible | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Peristomal Skin Complications & Infections

Dermatitis, mechanical trauma, and Candida infections affect up to 60.3% of users, pushing average healthcare costs to USD 204,907 for affected patients versus USD 126,747 for those without issues. Risk escalates in the absence of certified wound ostomy continence nurses, widening regional outcome gaps. High complication rates drive product returns and erode confidence, dampening growth even as innovation attempts to mitigate the problem across the ostomy care market.

High Cost of Advanced Multi-Piece Systems

Premium two-piece appliances and accessory bundles remain beyond reach for many uninsured patients, and reimbursement caps in North America limit covered quantities to basic models. In emerging economies, low-cost imports often lack skin-friendly features, leading to avoidable complications that raise long-term treatment expenses. Economic barriers therefore temper near-term expansion despite recognized clinical benefits.

Segment Analysis

By Product Type: Digital Innovation Drives Accessories Growth

Ostomy bags continued to anchor demand, capturing 84.56% of 2024 revenue; however, accessories posted the fastest 5.12% CAGR outlook, signaling a pivot toward holistic care kits that elevate comfort and skin integrity [2]Yan Li et al., “Composite Hydrocolloid Skin Barriers,” Journal of Composites Science, mdpi.com. Skin barriers and seals, boosted by ceramide-infused and silicone-based recipes, are the top-selling accessory class because they slash dermatitis incidents. Stoma pastes and powders fill gaps around irregular openings, while deodorants and lubricants ease social worries. Drainable pouches dominate closed designs due to lower per-use cost and waste, yet closed pouches persist for patients with limited dexterity. Composite laminates merging gentle adhesives and moisture control layers curtail trauma during removal, supporting wider premium adoption in the ostomy care market.

Substitution battles between one-piece and two-piece systems reflect lifestyle segmentation. Active adults prefer modular two-piece sets for quick pouch swaps, whereas seniors gravitate to simple one-piece units. Digital add-ons mark the next frontier; Coloplast’s sensor platform sends integrity alerts to phones, enabling preemptive changes that prevent leaks and hospital visits. Taken together, accessories now act as revenue multipliers by raising per-patient spend and recurring use frequency, underpinning long-run profitability for manufacturers.

By Surgery Type: Ileostomy Growth Reflects Surgical Evolution

Colostomy preserved leadership with 44.34% 2024 market share; nevertheless, ileostomy is poised for 5.71% CAGR through 2030 as colorectal surgeons emphasize temporary diversions that protect anastomoses. Minimally invasive approaches reduce wound size yet often yield flush stomas that need moldable rings and convex wafers, boosting accessory uptake. Urostomy volumes stay modest, limited to bladder cancer and congenital anomalies, yet require specialized urine-resistant barriers.

The trend toward faster discharges inflates demand for intuitive products. Patients return home within three to five days, leaning heavily on virtual nurse visits and illustrated guides. Ostomy care market size for ileostomy devices is expected to widen as younger IBD patients undergoing sphincter-preserving surgery accept short-term stomas. Hospitals therefore coordinate with community suppliers to secure leak-proof pouches and tutoring kits before discharge, strengthening continuity of care.

By End User: Home Care Dominance Accelerates Digital Adoption

Home settings commanded 47.32% of 2024 revenues as patients favor autonomy and insurers push outpatient models. The ostomy care market size tied to home users benefits from bulk refill programs and subscription apps that automate monthly shipments. Tele-monitoring tools allow nurses to spot redness early, cutting readmissions. COVID-19 cemented virtual consults as a standard follow-up pathway, reducing clinic congestion.

Hospitals and specialty clinics, while smaller, are expanding at 5.87% CAGR on the back of rising elective colorectal surgeries and the complexity of geriatric cases. Dedicated ostomy centers deliver high-touch services for high-risk patients, creating referral loops that feed product selection during inpatient stays. Ambulatory surgical centers also grab a larger slice by offering cost-efficient same-day procedures, reinforcing downstream sales when patients transition home. Thus, institutional and home channels increasingly merge through connected platforms that trace pouch performance from ward to bedroom.

Geography Analysis

North America retained a 42.87% revenue lead in 2024 due to robust reimbursement and mature distribution that secures doorstep delivery within 48 hours [3]American Association for Homecare, “Ostomy Supply Delivery Statistics,” aah.org. Patient advocacy groups lobby for generous supply allowances, sustaining premium adoption across Medicare and commercial plans. Ongoing debates over Local Coverage Determinations may reshape advanced wafer reimbursement, yet near-term continuity appears stable after the March 2025 deferral.

Europe forms a mature yet innovative cluster. Universal health coverage ensures baseline access, while the European Chemicals Agency’s PFAS phase-out mandates swift reformulation of barrier films. Germany, the United Kingdom, and France anchor demand, each embedding ostomy care into broader colorectal cancer programs. Sustainability pushes manufacturers toward biodegradable pouch liners and recyclable packaging to satisfy EU waste directives.

Asia-Pacific is the fastest riser at 6.25% CAGR through 2030. China alone hosts an estimated 350,000 ostomy users, with urban hospitals installing specialized stoma clinics to meet demand. India accelerates as IBD diagnoses climb and private insurance expands to mid-income citizens. Japan’s aging society keeps baseline sales high, while local firms leverage precision molding and robotics to manufacture high-quality pouches domestically. Diverse regulatory landscapes require tailored evidence packages; some markets accept US Food and Drug Administration clearance, while others insist on local clinical data, lengthening launch timelines but widening competitive moats.

Competitive Landscape

Market Concentration

The ostomy care market features moderate consolidation. Coloplast, ConvaTec, and Hollister command dominant share, wielding global distribution, broad portfolios, and robust R&D budgets. Each emphasizes digital ecosystems. Coloplast pilots smartphone-linked leak alerts; ConvaTec integrates me+ nurse coaching; Hollister invests in tele-stoma fitting to shorten learning curves. Mid-tier players such as B. Braun, Smith & Nephew, and Welland Medical exploit niche adjacencies like silicone adhesives and pediatric pouches.

Emerging innovators carve out specialized corners. OstomyCure advances a titanium implant designed to substitute external pouches for select colostomy patients, now in late-stage trials. Start-ups explore machine-learning algorithms that predict skin breakdown from image uploads, offering subscription-based prevention services.

Strategic moves reflect a dual focus on emerging markets and connected care. ConvaTec posted 4.9% organic growth in ostomy during H1 2024, powered by China and Brazil expansion. Partnerships with home-delivery providers proliferate to secure last-mile convenience. Patent filings concentrate on hydrocolloid blends, convex baseplates, and embedded electronics, underscoring a race to lock in next-generation comfort and monitoring benefits.

Ostomy Care Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: ConvaTec welcomed the postponement of Local Coverage Determinations on skin substitutes in the United States, retaining market access for advanced barrier products used in ostomy care.

- January 2023: OstomyCure completed patient recruitment for its clinical trial evaluating the titanium TIES implant designed to eliminate external stoma bags.

- January 2022: Owens & Minor Inc. and Apria Inc. entered into a definitive agreement pursuant to which Owens & Minor would acquire Apria. The acquisition is anticipated to broaden the company's ostomy portfolio.

Table of Contents for Ostomy Care Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising prevalence of IBD & colorectal cancer

- 4.2.2Rapid product & material innovation

- 4.2.3Accelerating geriatric ostomy population

- 4.2.4Expanding patient-support & awareness programs

- 4.2.53-D printed customized stoma appliances

- 4.2.6Reimbursement expansion for home-delivered DME supplies

- 4.3Market Restraints

- 4.3.1Peristomal skin complications & infections

- 4.3.2High cost of advanced multi-piece systems

- 4.3.3Social stigma & psychological burden

- 4.3.4Pending PFAS restrictions on barrier films

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Product Type

- 5.1.1Ostomy Bags

- 5.1.1.1One-piece System

- 5.1.1.2Two-piece System

- 5.1.1.2.1Drainable

- 5.1.1.2.2Closed

- 5.1.2Ostomy Accessories

- 5.1.2.1Skin Barriers / Seals

- 5.1.2.2Stoma Pastes & Powders

- 5.1.2.3Deodorants & Lubricants

- 5.1.2.4Support Belts & Others

- 5.2By Surgery Type

- 5.2.1Colostomy

- 5.2.2Ileostomy

- 5.2.3Urostomy

- 5.3By End User

- 5.3.1Hospitals & Specialty Clinics

- 5.3.2Home-care Settings

- 5.3.3Ambulatory Surgical Centers

- 5.4By Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4Australia

- 5.4.3.5South Korea

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4Middle East & Africa

- 5.4.4.1GCC

- 5.4.4.2South Africa

- 5.4.4.3Rest of Middle East & Africa

- 5.4.5South America

- 5.4.5.1Brazil

- 5.4.5.2Argentina

- 5.4.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Coloplast A/S

- 6.3.2ConvaTec Group plc

- 6.3.3Hollister Inc.

- 6.3.4B. Braun Melsungen AG

- 6.3.5Welland Medical Ltd

- 6.3.6Salts Healthcare

- 6.3.7ALCARE Co., Ltd.

- 6.3.8Cymed MicroSkin

- 6.3.9Marlen Manufacturing

- 6.3.10Nu-Hope Laboratories

- 6.3.11Perma-Type Co.

- 6.3.12Torbot Group Inc.

- 6.3.133M Health Care Division

- 6.3.14Smith & Nephew plc

- 6.3.15Trio Ostomy Care

- 6.3.16Pelican Healthcare

- 6.3.17Genii™ Ostomy

- 6.3.18Fittleworth Medical

- 6.3.19Safe n’ Simple

- 6.3.20Eakin Healthcare

- 6.3.21Dansac (Hollister Brand)

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Segmentation Overview

- By Product Type

- Ostomy Bags

- One-piece System

- Two-piece System

- Drainable

- Closed

- Drainable

- One-piece System

- Ostomy Accessories

- Skin Barriers / Seals

- Stoma Pastes & Powders

- Deodorants & Lubricants

- Support Belts & Others

- Skin Barriers / Seals

- Ostomy Bags

- By Surgery Type

- Colostomy

- Ileostomy

- Urostomy

- Colostomy

- By End User

- Hospitals & Specialty Clinics

- Home-care Settings

- Ambulatory Surgical Centers

- Hospitals & Specialty Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- United States

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Germany

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- China

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- GCC

- South America

- Brazil

- Argentina

- Rest of South America

- Brazil

- North America

Detailed Research Methodology and Data Validation

Primary Research

Desk Research

Market-Sizing & Forecasting

Data Validation & Update Cycle

Why Our Ostomy Care Baseline Inspires Confidence

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 3.47 B (2025) | Mordor Intelligence | Anonymized source:Mordor Intelligence | Primary gap driver: | |

USD 3.87 B (2024) | Global Consultancy A | Bundles accessories and certain incontinence disposables, relies on top-line revenue extrapolation | ||

USD 4.14 B (2024) | Industry Data Firm B | Applies list-price inflation and broad retail channels, refresh cadence not disclosed |