Global Opioids Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

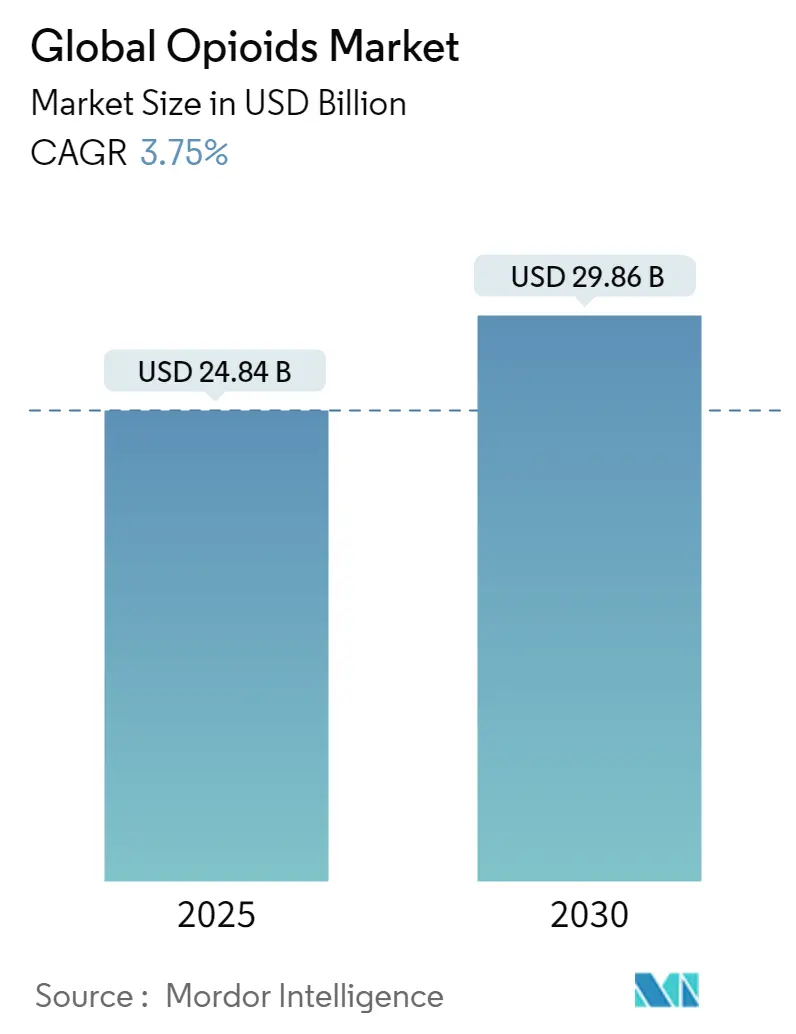

| Market Size (2025) | USD 24.84 Billion |

| Market Size (2030) | USD 29.86 Billion |

| Growth Rate (2025 - 2030) | 3.75% CAGR |

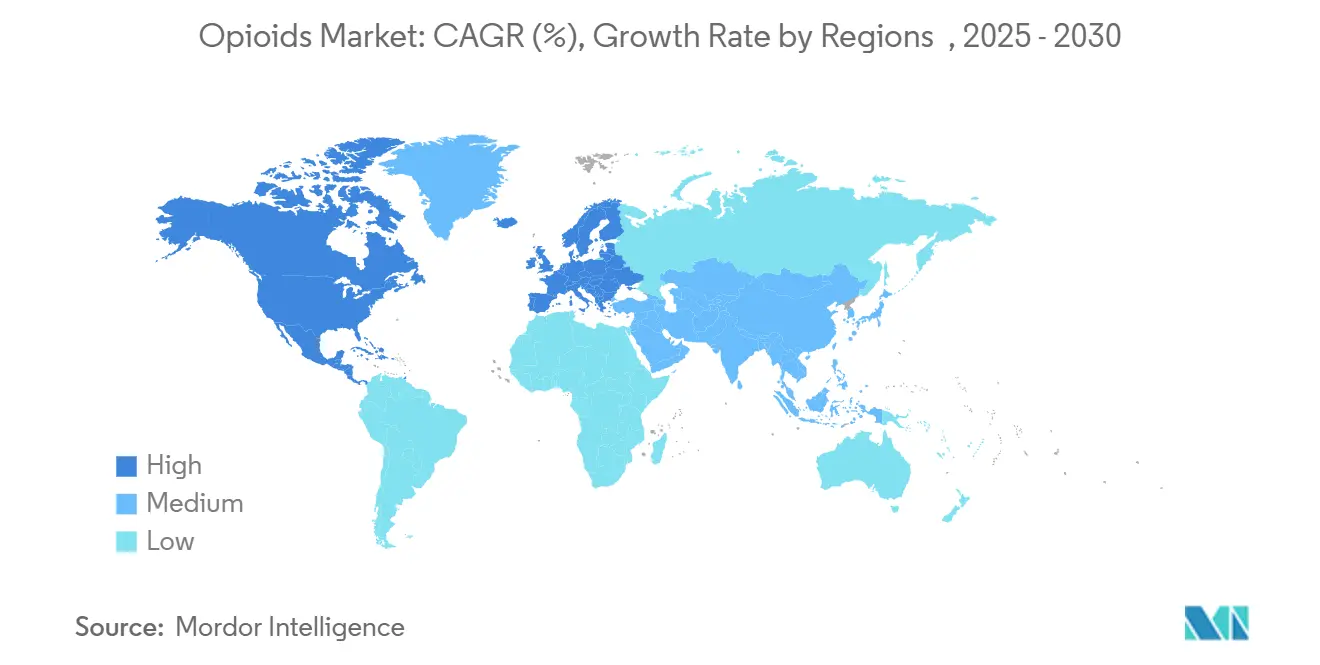

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Global Opioids Market Analysis by Mordor Intelligence

The opioids market generated USD 24.84 billion in revenue in 2025 and is forecast to reach USD 29.86 billion by 2030, advancing at a 3.75% CAGR. The steady expansion of the opioids market reflects a careful equilibrium between persistent clinical need for potent analgesics and strict global controls aimed at curbing diversion and misuse. Demand is anchored in surgical, oncology, and severe chronic pain settings, yet growth is tempered by production-quota cuts, heightened prescription monitoring, and the rising availability of substitute therapies. Hospitals worldwide continue to account for the bulk of opioid consumption, although shortages of injectable morphine, hydromorphone, and fentanyl force providers to ration supply and adopt multimodal regimens. Product innovation is pivoting toward abuse-deterrent formulations and toward first-in-class non-opioid analgesics such as suzetrigine, a NaV1.8 inhibitor that secured FDA approval in 2025, illustrating a parallel trend toward diversification of advanced pain option. Meanwhile, digital therapeutics that guide precise opioid dosing are lowering average prescription sizes and reinforcing payers’ preference for data-driven stewardship programs.

Key Report Takeaways

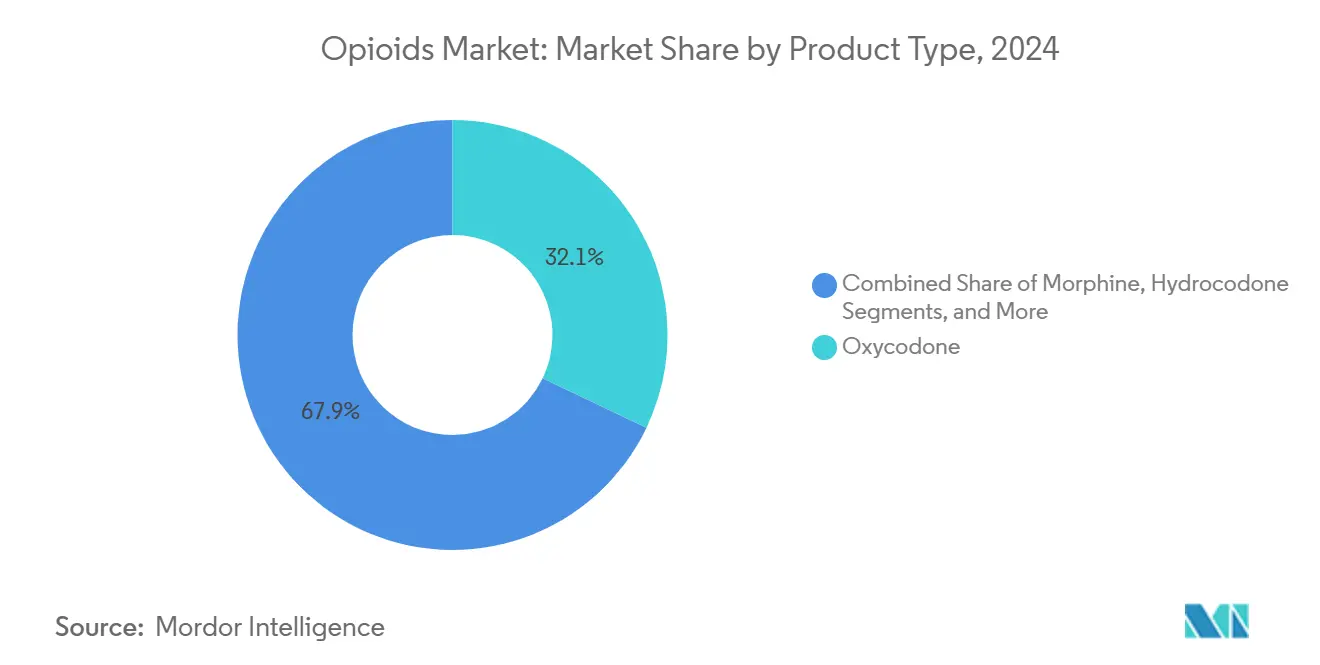

- By product type, oxycodone held 32.17% of opioids market share in 2024, while methadone is projected to post the fastest CAGR of 4.6% through 2030.

- By receptor binding, strong agonists commanded 50.71% share of the opioids market size in 2024; partial agonists are forecast to expand at a 5.1% CAGR to 2030.

- By route of administration, parenteral/IV formulations captured 54.14% of the opioids market size in 2024, outpacing all other routes; transdermal systems are the fastest growing at 4.8% CAGR.

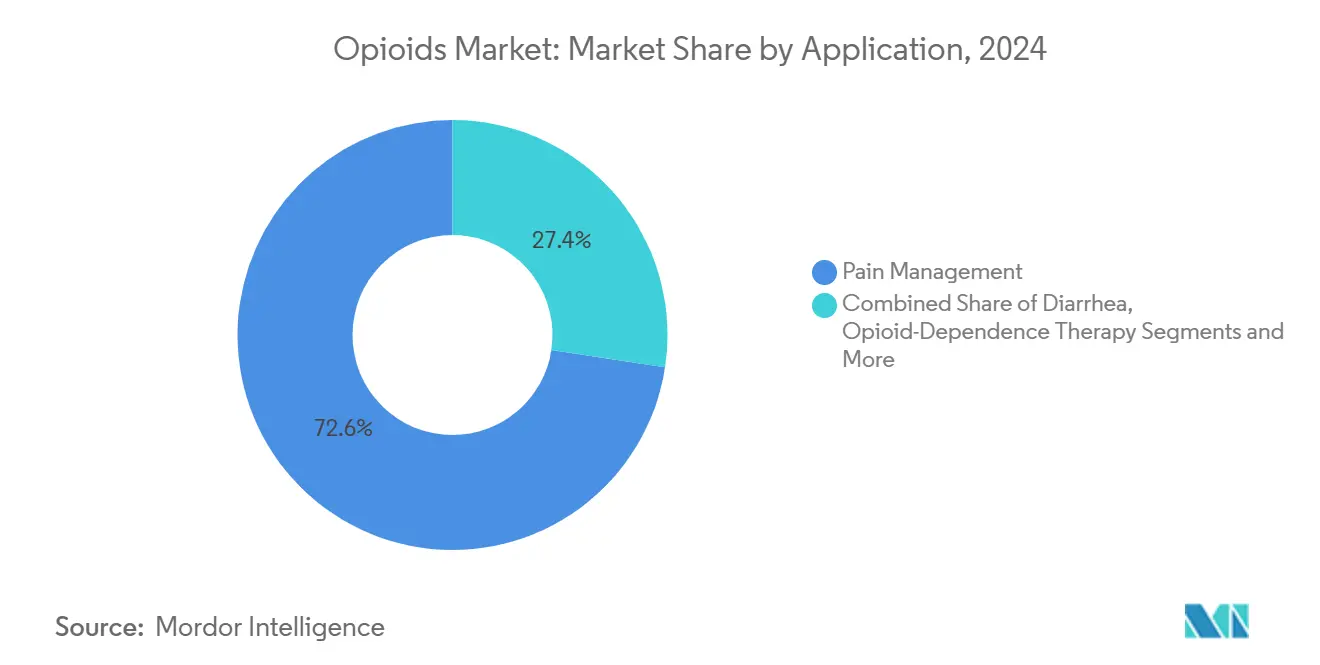

- By application, pain management accounted for a dominant 72.61% share of the opioids market size in 2024, whereas opioid-dependence therapy is expected to grow at a 5.3% CAGR through 2030.

- By distribution channel, hospitals held 55.51% revenue share in 2024; online pharmacies, although at a modest 5.12%, are advancing at a 6.2% CAGR.

By geography, North America led with 42.91% opioids market share in 2024; Asia-Pacific is projected to post the highest regional CAGR of 5.9% to 2030.

Global Opioids Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of orthopedic diseases & chronic pain | +1.2% | Global, highest in North America & Europe | Long term (≥ 4 years) |

| Inclination toward extended-release opioid formulations | +0.8% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Rising focus on abuse-deterrent formulations (ADF) | +0.6% | North America primary, EU secondary | Medium term (2-4 years) |

| Growth in surgical procedures requiring peri-operative analgesia | +0.9% | Global, led by APAC and North America | Long term (≥ 4 years) |

| Adoption of opioid-substitution therapy in emerging markets | +0.4% | APAC, Latin America, Middle East & Africa | Long term (≥ 4 years) |

| Integration of digital therapeutics for personalized dosing | +0.3% | North America & EU early, global expansion | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Orthopedic Diseases & Chronic Pain

Population aging, obesity, and sedentary lifestyles are elevating rates of osteoarthritis and back disorders, sustaining demand within the opioids market. More than 50 million U.S. adults live with chronic pain, and opioids remain critical for breakthrough pain when non-pharmacological measures fail. Sophisticated care pathways now pair opioids with adjunctive physiotherapy and cognitive support, yet formulary restrictions and step-therapy mandates prolong time to therapy initiation. Pressure to minimize adverse events is intensifying post-marketing surveillance, spurring investment in tamper-resistant packaging and analytic dashboards that flag aberrant prescribing. As a result, manufacturers that can demonstrate real-world safety benefits are securing preferential reimbursement and sustaining high formulary tier placement across the opioids market.

Inclination Toward Extended-Release Opioid Formulations

Clinicians increasingly choose once- or twice-daily extended-release tablets to stabilize plasma concentrations and reduce nocturnal breakthrough pain. The FDA’s evolving ADF pathway has accelerated approvals such as Xtampza ER, which employs microsphere technology to thwart crushing and injection abuse. Extended-release products command premium pricing, lifting unit revenues despite flat prescription volumes. Complex manufacturing processes and rigorous abuse-simulation studies, however, restrict new entrants and create elevated capital requirements, reinforcing the competitive positions of incumbents within the opioids market.

Rising Focus on Abuse-Deterrent Formulations (ADF)

Health systems seek products that withstand physical and chemical manipulation, thereby preserving clinical access while limiting diversion. Real-world analyses show a 26% drop in abuse for tamper-resistant tablets compared with legacy oral dosage forms [1]JAMA Network Editors, “Variation in Intraoperative Opioid Administration and Use,” JAMA Network Open, jamanetwork.com. Payers in the United States now tie prior-authorization criteria to ADF status, incentivizing rapid market uptake. Europe’s payers increasingly mirror this stance, and emerging APAC markets are incorporating ADF language into pharmacovigilance guidelines. As such, ADF capability is evolving from a differentiator to table stakes for new entrants in the opioids market.

Growth in Surgical Procedures Requiring Peri-Operative Analgesia

Global procedure volume continues to rise, with cardiac and orthopedic surgeries leading incremental demand for intra-operative fentanyl, sufentanil, and remifentanil. Although multimodal regimens have trimmed postoperative prescription sizes by 41.8%, opioids remain indispensable for high-acuity pain immediately after surgery [2]T Kain, “Declines in Post-Surgical Opioid Prescribing,” Annals of Surgery, journals.lww.com. Hospitals deploy decision-support algorithms that recommend weight-based titration and emphasize rapid tapering, supporting stewardship without compromising analgesia. These systems are expanding first in tertiary centers across APAC, boosting regional consumption and elevating the opioids market outlook.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advent & legalization of cannabis as an alternative | -0.9% | North America primary, EU emerging | Medium term (2-4 years) |

| Prescription-drug abuse & addiction concerns | -1.1% | Global, most pronounced in North America | Long term (≥ 4 years) |

| Stricter production quotas & regulatory curbs | -0.7% | North America primary, global spillover | Short term (≤ 2 years) |

| Late-stage non-opioid analgesics reducing demand | -0.5% | North America & EU early adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Advent & Legalization of Cannabis as an Alternative

Medical-marijuana legislation in 39 U.S. states and a growing number of European jurisdictions is producing substitution effects, cutting Schedule III opioid prescriptions among Medicaid patients by nearly 30%. Randomized trials report 39.3% reductions in morphine-milligram equivalents when cannabis is combined with opioids, especially for low-potency regimens. Nevertheless, cannabis does not fully replace high-potency opioids required for complex surgery, so its impact is more pronounced in primary care than in specialty hospitals. The trend restrains overall volume growth yet encourages manufacturers to target high-acuity niches in the opioids market.

Prescription-Drug Abuse & Addiction Concerns

The rising incidence of synthetic opioids such as nitazenes intensifies media coverage and fuels public policy debate. Mandatory-check programs and risk-evaluation mitigation strategies add administrative burden, making prescribers cautious and prompting some retail chains to stop accepting new pain patients. Despite these barriers, prescription diversion rates remain below 0.5% of total production, underscoring the difference between illicit supply and the regulated opioids market. Still, reputational risk and escalating litigation costs pressure companies to allocate larger compliance budgets and to reinforce detection technologies across distribution channels.

Segment Analysis

By Product Type: Oxycodone Maintains Leadership Under Supply Stress

Oxycodone secured 32.17% opioids market share in 2024, reflecting sustained physician preference for both immediate-release and extended-release formats that cover a wide spectrum of acute and chronic indications. Its bioavailability profile, predictable metabolism, and decades of clinical experience reinforce high formulary penetration even as DEA quota cuts and manufacturing outages periodically constrain supply. Multiple suppliers—Alvogen, Amneal, Camber—have reported shortages, prompting hospital purchasing teams to widen sourcing networks and preserve continuity of care. Methadone, with 4.16% share, remains a cornerstone of opioid-substitution treatment; long plasma half-life lowers withdrawal risk, supporting daily observed dosing within treatment programs.

Volatility persists for morphine and hydrocodone because hydrocodone production quotas have fallen 73% since 2015, and morphine shortages arise when manufacturing campaigns are delayed. Meperidine’s use continues to erode due to neurotoxic metabolite concerns, while niche agents such as oxymorphone face sustained supply gaps. The emphasis on deterrence, combined with supply-chain diligence, is reshaping competitive tiers within the opioids market.

Note: Segment shares of all individual segments available upon report purchase

By Receptor Binding: Strong Agonists Retain Core Clinical Role

Strong agonists captured 50.71% opioids market share in 2024, underpinning their role in severe postoperative oncology and trauma care. Their full μ-receptor activation delivers unmatched potency, although risk mitigation requires continuous oxygen saturation monitoring and accelerated tapering protocols. Partial agonists, notably buprenorphine at 4.51% share, continue to expand under relaxation of telemedicine rules permitting e-prescribing without prior in-person visits [3]Center for Drug Evaluation and Research, “Telemedicine Prescribing Flexibilities Final Rule,” Federal Register, federalregister.gov. This flexibility boosts treatment-program enrollment and stabilizes revenue for specialized manufacturers.

The opioids industry is channeling R&D toward peripheral-selective molecules that minimize central nervous system penetration, thereby maintaining analgesia with reduced respiratory depression. Antagonists such as naloxone remain vital adjuncts across emergency medical services, and novel dual-action molecules that combine agonism with endocytic bias are entering Phase II trials. As regulatory scrutiny tightens, receptor-binding selectivity will increasingly define differentiation strategies and value capture in the opioids market.

By Route of Administration: Parenteral Dominance Remains Yet Faces Supply Gaps

Parenteral formulations represented 54.14% of the opioids market size in 2024, cementing their status as the backbone of inpatient analgesia where rapid onset and titratable dosing are essential. Persistent shortages recorded by the American Society of Health-System Pharmacists compel surgical centers to employ conservative inventory management and to standardize opioid-sparing anesthesia protocols. Oral solids, despite a comparatively lower 4.39% share of value, account for the majority of prescription volume in ambulatory care. Technological advances are stimulating renewed interest in transdermal patches combining hydrogel layers with micro-needle arrays that improve adhesion and permit Bluetooth-enabled adherence monitoring.

Regional variations influence route preferences. European clinicians have embraced sublingual and nasal fentanyl for breakthrough cancer pain, whereas Japanese guidelines favor transdermal buprenorphine for chronic musculoskeletal conditions. These dynamics diversify the growth profile across the opioids market and protect manufacturers from isolated channel disruptions.

By Application: Pain Management Commands Resource Allocation

Pain-management indications generated 72.61% of opioids market revenue in 2024, anchored in oncology and orthopedic segments where severity and duration of pain surpass the efficacy threshold of NSAIDs and adjuvant therapies. Oncology care teams prioritize rapid titration to relieve breakthrough pain, while orthopedic surgeons leverage controlled-release tablets to ensure overnight relief during the initial 72-hour postoperative window. Robust stewardship programs have driven a 3.5% decline in postoperative prescription initiation but left peak-severity segments largely intact.

Opioid-dependence therapy, at 4.81% share, is scaling swiftly as governments expand reimbursement for medication-assisted treatment. Telehealth flexibilities, first introduced during the pandemic, became permanent in 2024, supporting program expansion into rural districts. Cold & cough and diarrhea subsegments struggle under stricter codeine restrictions, yet remain in formularies as legacy options. Overall, application diversity cushions the opioids market against single-segment policy shocks.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Hospital Dominance Faces Digital Disruption

Hospitals held 55.51% opioids market share in 2024, reflecting concentration of high-potency intravenous products in controlled environments. However, ongoing drug shortages—277 active shortages in late 2024—have forced inpatient pharmacies to deploy usage ceilings and substitute protocols, sparking collaboration across group purchasing organizations for contingency contracting. Retail pharmacies experience reputational risks and tighter DEA audits, leading select chains to refuse new opioid patients, which reroutes demand to integrated delivery networks.

Online pharmacies, representing 5.12% of sales, post the fastest growth under stringent validation programs such as NABP’s Digital Pharmacy Accreditation. DEA enforcement actions, including license revocation for non-compliant entities, maintain high compliance costs yet do not blunt consumer appetite for home delivery of maintenance opioids. Telemedicine platforms are partnering with specialty pharmacies to bundle virtual consultations with same-day shipment, accelerating share gains and broadening geographic reach within the opioids market.

Geography Analysis

North America sustained a commanding 42.91% opioids market share in 2024, anchored by advanced surgical capacity, comprehensive insurance coverage, and continued reliance on potent analgesics for high-acuity care. DEA production-quota reductions—68% for oxycodone and 73% for hydrocodone since 2015—tightened supply but did not derail demand, prompting 90% of surveyed pain patients to report access difficulties. U.S. health networks responded with prescription stewardship that cut new postoperative starts by 3.5% and trimmed tablet counts by 41.8%, yet the opioids market size for the region still rose on price-mix uplift as ADF products captured greater formulary share. Canada’s centralized monitoring system keeps diversion low, while Mexico balances domestic need with its role as a transit corridor for finished pharmaceuticals.

Europe forms the second-largest regional pool, supported by deep manufacturing capabilities and robust pain-care infrastructure. Germany, France, and the U.K. prioritize ADF procurement, while Italy and Spain increasingly rely on multimodal regimens that reserve opioids for breakthrough episodes. The European Monitoring Centre for Drugs and Drug Addiction coordinates response protocols for synthetic opioid threats such as nitazenes, informing national prescribing guidelines [4]European Monitoring Centre for Drugs and Drug Addiction, “Nitazene Alerts in Europe,” bmj.com. Brexit-linked customs checks introduced procedural frictions, yet continued mutual-recognition agreements uphold stable medicine flow across the Channel, keeping overall opioids market growth intact.

Asia-Pacific, with 5.43% opioids market share in 2024, is the fastest-advancing geography and is projected to post 5.9% CAGR through 2030. Japan’s super-aged demographic drives steady demand for transdermal and oral controlled-release formulations, while Australia refines its real-time prescription-monitoring system to curb doctor shopping. China’s reclassification of dextromethorphan to Category II Psychotropic Drugs in July 2024 underscores a broader tightening of controlled-substance rules, though severe-pain protocols remain intact for oncology and trauma centers. India’s dual role as manufacturer and consumer positions it to benefit from export expansion even as domestic authorities grapple with balancing patient access against diversion risks. Growing surgical capacity across Indonesia, Thailand, and Vietnam further elevates regional volume, collectively reinforcing long-term growth prospects for the opioids market.

Competitive Landscape

Industry concentration has intensified following a wave of liability-driven restructurings and opportunistic mergers. The USD 6.7 billion tie-up between Mallinckrodt and Endo in 2025 created scale economies in raw-material sourcing and an enlarged pipeline of abuse-deterrent tablets, positioning the combined entity as a cost leader in the opioids market. Purdue Pharma’s USD 7.4 billion settlement reshaped liabilities across the supply chain, prompting distributors to renegotiate indemnity clauses and adjust inventory turns. Payment of settlement escrows constrains R&D budgets for legacy players, opening space for mid-cap innovators.

Collegium Pharmaceutical captured share with Xtampza ER’s microsphere platform, while Hikma Pharmaceuticals leveraged flexible injectables manufacturing to cushion hospitals against fentanyl shortages. Vertex Pharmaceuticals disrupted entrenched paradigms by securing approval for NaV1.8 inhibitor suzetrigine, creating an alternative with no observed addiction profile. Early-stage firms such as Ensysce Biosciences demonstrated Phase II success for PF614-MPAR, which caps oxycodone plasma spikes even with multiple dosing, appealing to payers seeking overdose safeguards.

Competitive strategies revolve around three pillars: (1) ADF investment to secure formulary priority, (2) life-cycle management through novel delivery systems such as transdermal micro-array patches, and (3) partnership with digital-health vendors that supply analytics dashboards enabling adaptive dosing. Adoption of cloud-based pharmacovigilance is broadening, with Johnson & Johnson deploying AI engines to mine EHR data for early safety signals across its analgesic franchise. Collectively, these initiatives reinforce brand loyalty and shield revenue amid intensifying regulatory headwinds in the opioids market.

Global Opioids Industry Leaders

-

Mallinckrodt Pharmaceuticals

-

Amneal Pharmaceuticals Inc.

-

Hikma Pharmaceuticals PLC

-

Purdue Pharmaceuticals L.P.

-

Teva Pharmaceuticals Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Ensysce Biosciences reported positive Phase II data for PF614-MPAR showing significant overdose protection at the 100 mg dose, supporting plans for a pivotal Phase III launch.

- March 2023: Indivior completed its acquisition of Opiant Pharmaceuticals, broadening its addiction-treatment portfolio.

- January 2023: Teva announced that its nationwide opioid settlement gained sufficient state support to proceed.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the opioids market as global prescription-grade natural, semi-synthetic, and synthetic opioid molecules, morphine, oxycodone, hydrocodone, fentanyl, methadone, codeine, and related formulations, supplied through licensed pharmaceutical channels for analgesia, anesthesia, cough, and diarrhea management. We include finished dosage sales recorded at the manufacturer level and off-patent generics regularly captured by our paid volume trackers.

Scope Exclusion: Illicit trafficking, veterinarian opioids, and non-opioid analgesics are excluded to keep our therapeutic focus tight.

Segmentation Overview

- By Product Type

- Morphine

- Oxycodone

- Hydrocodone

- Meperidine

- Methadone

- Others

- By Receptor Binding

- Strong Agonist

- Mild-to-Moderate Agonist

- Partial Agonist

- Antagonist

- By Route of Administration

- Oral

- Parenteral / IV

- Transdermal

- Others (Sublingual, Nasal, etc.)

- By Application

- Pain Management

- Cancer Pain

- Neuropathic Pain

- Post-surgical / Traumatic Pain

- Osteoarthritis Pain

- Other Pain

- Cold & Cough

- Diarrhea

- Opioid-Dependence Therapy

- Others

- Pain Management

- By Distribution Channel

- Hospitals

- Retail Pharmacies

- Online Pharmacies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Several semi-structured calls with hospital pharmacists, pain specialists, contract manufacturers, and payors across North America, Europe, and Asia helped us validate off-invoice average selling prices, channel mix shifts, and formulary restrictions. We also ran an online pulse survey among caregivers in emerging markets to gauge post-COVID demand recovery.

Desk Research

We gathered foundational data from tier-1 public sources such as the US Centers for Disease Control, World Health Organization, United Nations Office on Drugs and Crime, US Food and Drug Administration, and the OECD health database. Supplementary insight came from trade associations (International Narcotics Control Board, European Pain Federation), peer-reviewed journals, public 10-K filings, and prescription auditing repositories. Mordor analysts accessed D&B Hoovers for company revenue splits and Dow Jones Factiva for transaction news to cross-check revenue swings. This list is illustrative; many other references informed our evidence base.

Market-Sizing & Forecasting

A single top-down model starts with national prescription volume and average sales price series, reconstructed from production and trade data, which are then value-mapped to our therapeutic segments. Supplier roll-ups and sampled ASP x volume checks play the bottom-up role to test and fine-tune totals. Key drivers, post-operative procedure counts, cancer incidence, controlled-substance policy scorecards, generic erosion rates, and abuse-deterrent formulation uptake feed a multivariate regression forecast. Scenario analysis explores opioid stewardship tightening versus status-quo reimbursement, allowing us to bound CAGR expectations.

Data Validation & Update Cycle

Outputs move through variance checks against hospital purchase dashboards, anomaly flags, and a two-step analyst review before sign-off.

Reports refresh each year, with interim revisions triggered by policy shocks or major product launches; a final pass immediately precedes client delivery.

Why Mordor's Opioids Baseline Inspires Confidence

Published estimates often diverge because firms choose different molecule baskets, price points, and refresh cadences.

Our disciplined scope alignment and yearly recalibration keep the baseline dependable for planners.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 24.84 B (2025) | Mordor Intelligence | - |

| USD 25.00 B (2024) | Global Consultancy A | Includes illicit fentanyl estimates and static 2022 exchange rates |

| USD 23.42 B (2025) | Regional Consultancy B | Omits hospital compounding volumes and adjusts prices using list, not net, ASPs |

Taken together, the comparison shows that Mordor's carefully screened inputs, mixed top-down and bottom-up testing, and annual updates yield a balanced view clients can reproduce and trust.

Key Questions Answered in the Report

How big is the Global Opioids Market?

The Global Opioids Market size is expected to reach USD 24.84 billion in 2025 and grow at a CAGR of 3.75% to reach USD 29.86 billion by 2030.

Which product leads the opioids market?

Oxycodone leads with 32.17% opioids market share thanks to its versatility in both immediate- and extended-release formats.

Who are the key players in Global Opioids Market?

Mallinckrodt Pharmaceuticals, Amneal Pharmaceuticals Inc., Hikma Pharmaceuticals PLC, Purdue Pharmaceuticals L.P. and Teva Pharmaceuticals Inc. are the major companies operating in the Global Opioids Market.

Which is the fastest growing region in Global Opioids Market?

Asia-Pacific holds 5.43% share but is forecast to expand at 5.9% CAGR to 2030, propelled by rising surgical volumes and wider adoption of pain-management protocols.

Which region has the biggest share in Global Opioids Market?

In 2025, the North America accounts for the largest market share in Global Opioids Market.

Page last updated on: