Ophthalmic Ultrasound Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

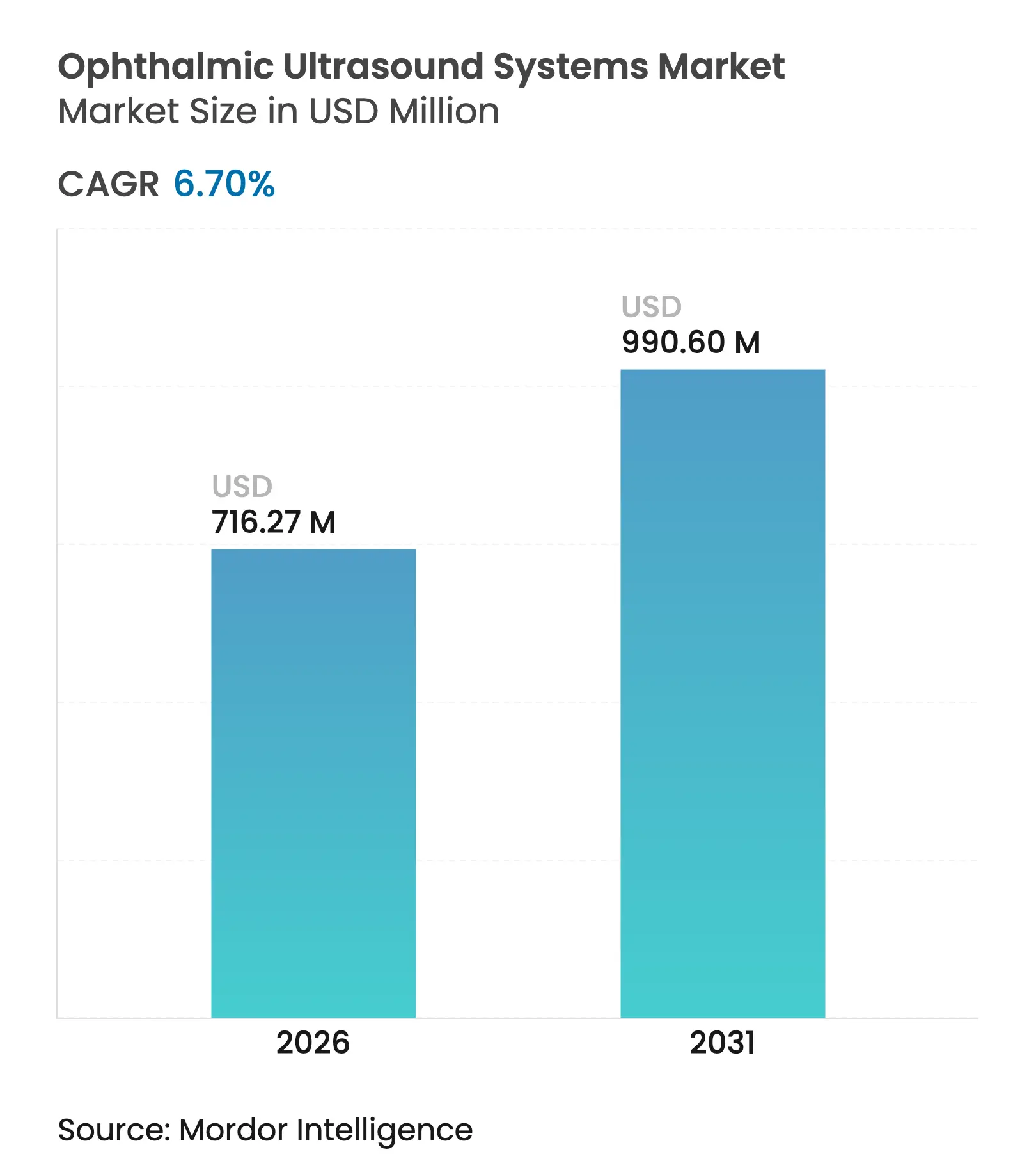

| Market Size (2026) | USD 716.27 Million |

| Market Size (2031) | USD 990.6 Million |

| Growth Rate (2026 - 2031) | 6.70 % CAGR |

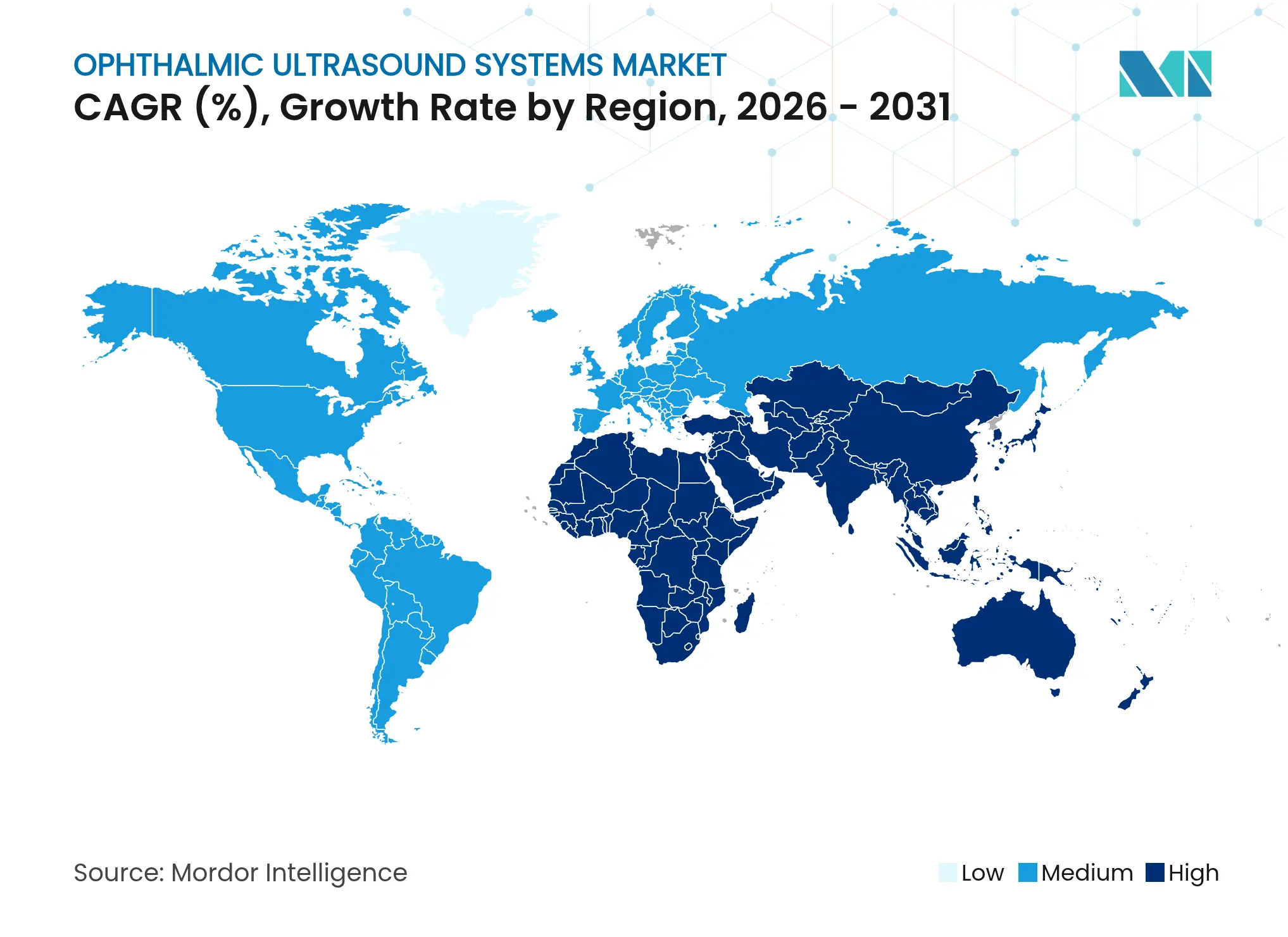

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

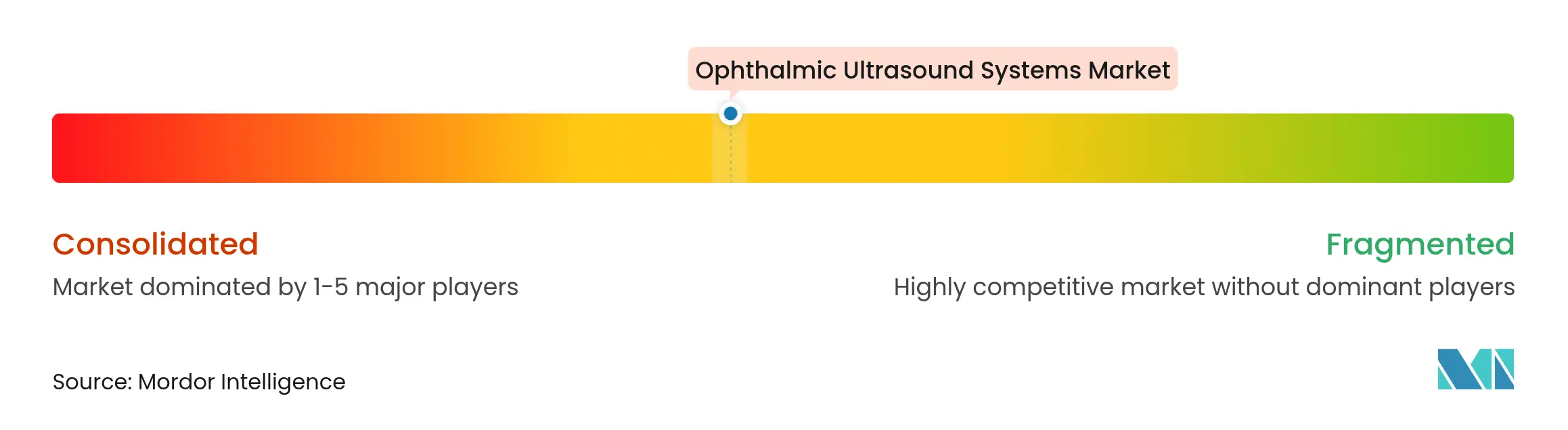

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Ophthalmic Ultrasound Systems Market Analysis by Mordor Intelligence

Robust demand stems from the growing integration of artificial intelligence with ultrasound platforms, the strategic pivot toward portable formats, and rising procedural volumes linked to cataract and glaucoma care. AI-enhanced systems now achieve diagnostic precision on par with expert clinicians, shortening workflows and improving triage in high-volume eye clinics. Demand is further stimulated by demographic aging that is expanding the pool of patients with cataracts, diabetic retinopathy, and angle-closure glaucoma. Vendors are responding with compact probes, multi-modal displays, and cloud connectivity that support point-of-care diagnostics across hospitals, ambulatory centers, and outreach programs. The competitive environment is moderately fragmented; platform differentiation increasingly depends on algorithm performance rather than purely on hardware specifications.

Key Report Takeways

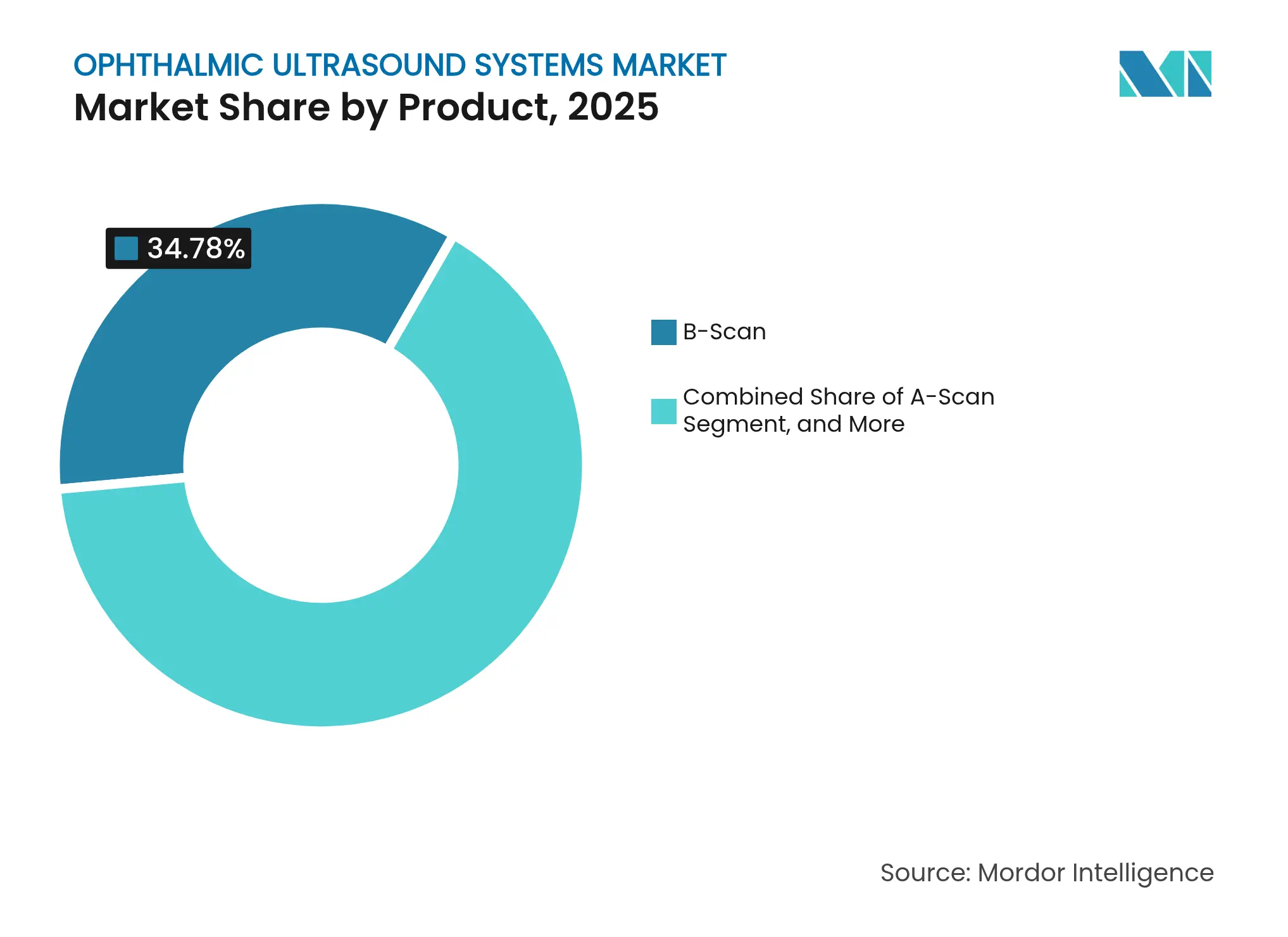

- By product category, B-scan devices led with 34.78% revenue share in 2025; ultrasound biomicroscopy is projected to expand at a 7.55% CAGR through 2031.

- By modality, stand-alone systems accounted for 59.60% of the ophthalmic ultrasound devices market share in 2025, while portable units are forecast to post the fastest CAGR at 8.55% to 2031.

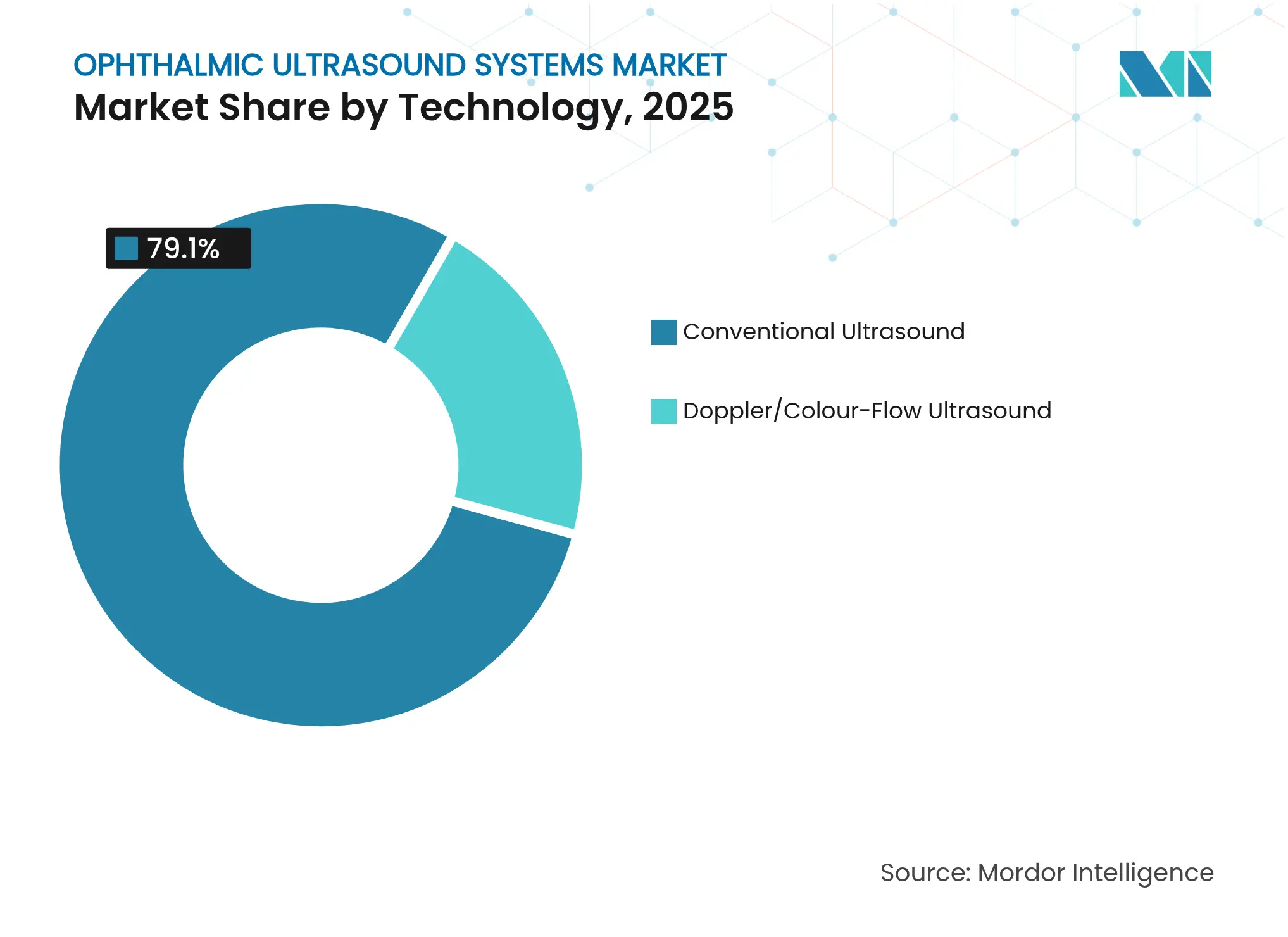

- By technology, conventional ultrasound commanded 79.10% of the ophthalmic ultrasound devices market size in 2025 and doppler/color-flow is advancing at 7.85% CAGR in the outlook period.

- By application, cataract assessment captured 40.20% share of the ophthalmic ultrasound devices market size in 2025; glaucoma management records the highest projected CAGR at 9.05% between 2026-2031.

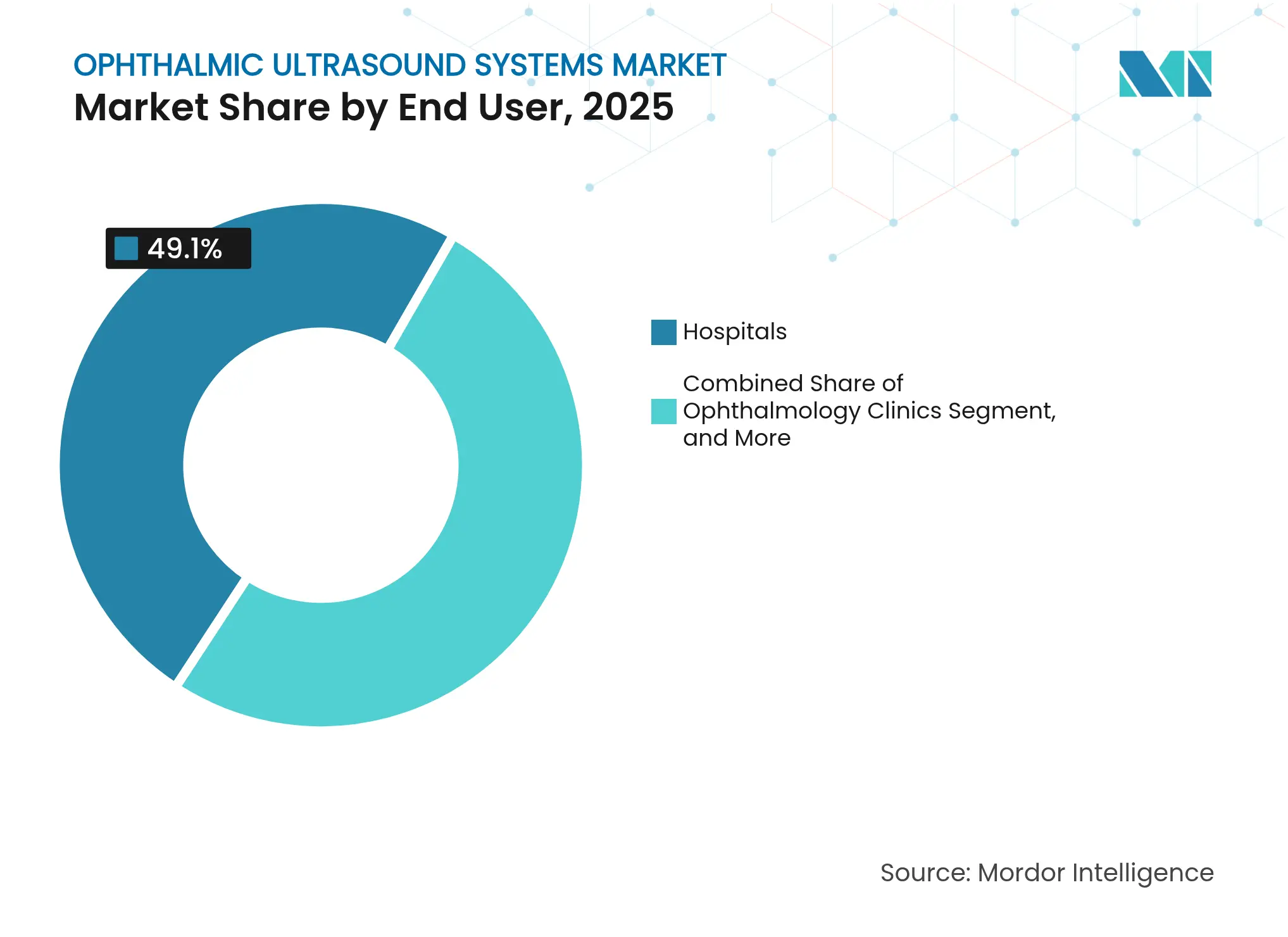

- By end user, hospitals held 49.10% revenue share in 2025, whereas ophthalmology clinics are growing at 7.75% CAGR through 2031.

- By geography, North America contributed 34.50% revenue in 2025; Asia-Pacific is set to register a 9.35% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ophthalmic Ultrasound Systems Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Increasing

Prevalence of Eye Diseases

Increasing

Prevalence of Eye Diseases

| +2.1% | Global; highest in North America, Europe, East Asia | Long term (≥ 4 years) |

(~) %

Impact on CAGR Forecast

:

+2.1%

|

Geographic

Relevance

:

Global;

highest in North America, Europe, East Asia

|

Impact

Timeline

:

Long term (≥

4 years)

|

Advent of

Novel Ophthalmic Technologies

Advent of

Novel Ophthalmic Technologies

| +1.8% | Global; early uptake in North America and Europe | Medium term (2–4 years) | |||

Growing

Adoption of Point-of-Care Portable Ultrasound

Growing

Adoption of Point-of-Care Portable Ultrasound

| +1.5% | Global; pronounced in emerging markets | Medium term (2–4 years) | |||

Integration

of AI-enhanced Image Analysis with Ultrasound Data

Integration

of AI-enhanced Image Analysis with Ultrasound Data

| +1.2% | North America, Europe, developed Asia-Pacific | Short term (≤ 2 years) | |||

Rising

Cataract Surgical Volumes

Rising

Cataract Surgical Volumes

| +1.9% | Global; strongest in Asia-Pacific | Long term (≥ 4 years) | |||

Expansion of

Ambulatory Surgical Centers & Ophthalmic Clinics

Expansion of

Ambulatory Surgical Centers & Ophthalmic Clinics

| +1.0% | North America, Western Europe, parts of Asia-Pacific | Medium term (2–4 years) | |||

| Source: Mordor Intelligence | ||||||

Increasing Prevalence of Eye Diseases

Population aging is accelerating demand across the Ophthalmic Ultrasound Devices market as larger cohorts enter the 65-plus age group that carries the highest cataract and glaucoma risk. Procedures using ultrasound are growing at 3.4% CAGR through 2030 because dense media opacities often preclude optical imaging. Cataract already affects half of adults by 75 years, and ultrasound remains indispensable for axial length measurement when corneal clarity is compromised. The prevalence of diabetic retinopathy is adding further workload because B-Scan can visualize the retina behind vitreous hemorrhage. Overall, the escalation of chronic ocular disorders is translating into sustained capital investment in ultrasound workstations across both tertiary centers and high-street clinics.

Advent of Novel Ophthalmic Technologies

Deep-learning algorithms embedded in new consoles interpret echo patterns more quickly and with higher repeatability than manual review, achieving diagnostic accuracy comparable to that of seasoned ophthalmologists.[1]Anang Soni, “Handheld Ultrasound Devices: A Comparative Study,” The Ultrasound Journal, springeropen.com Automated caliper placement and real-time angle-closure risk alerts shorten acquisition time and support less-experienced sonographers. These innovations enable manufacturers to offer value-added software subscriptions that complement equipment revenue, thereby encouraging faster replacement cycles.

Growing Adoption of Point-of-Care Portable Ultrasound

The shift toward compact devices is reshaping the Ophthalmic Ultrasound Devices market structure. Handheld probes combined with smartphone-class processors now deliver frame rates and penetration depths that rival trolley systems. A 2024 comparative study of six pocket scanners confirmed comparable image quality in posterior-segment applications, positioning portable formats for emergency-department triage and rural screening. Clinics appreciate lower capital requirements, battery operation, and simplified disinfection, while public-health teams use backpacks that include ultrasound, autorefractors, and fundus cameras for community outreach.

Integration of AI-Enhanced Image Analysis with Ultrasound Data

Emerging imaging technologies are enhancing the ability to visualize microvascular structures and assess malignancy risk in ocular lesions, supporting point-of-care differentiation between choroidal melanoma and benign nevi.[2]Kofi Adusei, “Quantitative High-Definition Microvessel Imaging of Choroidal Tumors,” Cancers, mdpi.com AI-driven heat-maps guide probe repositioning, reducing operator variability. The fusion of cloud analytics enables remote review by sub-specialists, thereby widening access in regions where ocular oncology expertise is scarce, and reinforcing the role of ultrasound even as other imaging modalities advance.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Increasing

Adoption of Alternate Imaging Modalities

Increasing

Adoption of Alternate Imaging Modalities

| −1.3% | Developed markets | Medium term (2–4 years) |

(~) %

Impact on CAGR Forecast

:

−1.3%

|

Geographic

Relevance

:

Developed

markets

|

Impact

Timeline

:

Medium term

(2–4 years)

|

High Capital

Outlay for High-Frequency Ultrasound Platforms

High Capital

Outlay for High-Frequency Ultrasound Platforms

| −1.6% | Emerging economies in Asia-Pacific, Africa, Latin America | Long term (≥ 4 years) | |||

Shortage of

Trained Ophthalmic Sonographers in Low-income Regions

Shortage of

Trained Ophthalmic Sonographers in Low-income Regions

| −1.2% | Africa, South Asia, parts of Latin America and Southeast Asia | Long term (≥ 4 years) | |||

Limited

Awareness & Adoption in Underserved Regions

Limited

Awareness & Adoption in Underserved Regions

| −1.0% | Rural areas worldwide, especially low- and lower-middle-income countries | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Increasing Adoption of Alternate Imaging Modalities

Optical coherence tomography provides superior axial resolution for retinal layers and dominates diabetic macular edema management, reducing ultrasound utilization in well-equipped centers. In vivo confocal microscopy is also preferred for corneal nerve-fiber assessment because of its non-contact design.[3]Meiqi Xiao, “Anterior-Segment Imaging Modalities: A Comparative Evaluation,” BMC Ophthalmology, biomedcentral.com Nonetheless, ultrasound retains advantages when the ocular media are opaque or when extraocular extension must be ruled out, highlighting a complementary rather than purely competitive relationship.

High Capital Outlay for High-Frequency Ultrasound Platforms

State-of-the-art Ultrasound Biomicroscopy units employ frequencies up to 100 MHz and incorporate advanced transducer cooling, driving equipment prices beyond many district hospitals’ budgets. Total cost of ownership increases further when annual calibration and specialist training are included. Financial barriers are most evident in sub-Saharan Africa and parts of Southeast Asia, where cataract incidence is high yet ophthalmic infrastructure remains underdeveloped. Progressive price erosion and refurbished equipment programs are emerging counter-measures but adoption gaps persist.

Segment Analysis

By Product: UBM Drives Precision in Anterior-Segment Care

Ultrasound Biomicroscopy posted the fastest 7.55% CAGR during 2026-2031 as ophthalmologists seek micro-level visualization of the ciliary body and iridocorneal angle. UBM contributes to early detection of plateau iris and zonular weakness, issues that are invisible on routine slit-lamp examination. B-Scan retained leadership with 34.78% of the Ophthalmic Ultrasound Devices market share in 2025 thanks to its versatility in vitreous hemorrhage and retinal detachment cases. Combined A/B platforms appeal to mid-sized hospitals that require a single cart for both biometry and posterior-segment imaging, supporting efficient capital deployment. Pachymeters maintain relevance for glaucoma risk stratification and refractive-surgery planning, while compact A-Scan modules remain the biometric cornerstone of the high-volume cataract service line.

The Ophthalmic Ultrasound Devices market size attached to UBM is reflecting sustained adoption in glaucoma specialty clinics. Conversely, B-Scan revenue growth will moderate yet remain significant as new software layers extend lifespan and reduce replacement urgency. Niche players focus on dedicated tumor-assessment probes that integrate elastography to broaden the clinical envelope.

Note: Segment shares of all individual segments available upon report purchase

By Modality: Portables Transform Workflow

Stand-alone accounted for 59.60% of the ophthalmic ultrasound systems market in 2025. Portable scanners are growing at 8.55% CAGR, triple the pace of console replacements. Portables integrate lithium-ion power packs and wi-fi modules that synchronize studies to electronic medical records before patients leave the examination room. High-resolution touchscreens enable pinch-to-zoom review that mimics smartphone use. Stand-alone systems continue to dominate surgical theaters where foot-pedal control, pedal-mapped presets, and dual-monitor output support complex cases. These units are also favored for teaching because large displays aid trainee supervision.

Manufacturers leverage interchangeable pods that allow a single handle to accept linear, convex, and annular probes. Subscription models bundle cloud analytics, firmware updates, and damage insurance, lowering the entry threshold for solo practitioners and optical retail chains expanding into diagnostic services. The flexibility of portables also supports novel care models such as drive-through cataract camps, where pre-operative biometry is performed in mobile vans.

By Technology: Doppler Adds Functional Insight

Conventional grey-scale ultrasound remains the workhorse because of its broad FDA clearance and ease of use and it held 79.10% of the ophthalmic ultrasound systems market in 2025. However, Doppler/Color-Flow technology is attracting attention for vascular-rich pathologies such as optic-nerve drusen and ocular ischemic syndrome. The segment will reach an 7.85% CAGR through 2031. Software improvements allow simultaneous B-mode and color overlay without frame-rate compromise, offering lesion morphology and perfusion insight in one clip.

Quantitative microvessel analysis, once limited to research settings, is migrating to routine practice, enhancing follow-up of choroidal tumor therapy. Conventional platforms evolve in parallel: better beam-forming algorithms improve near-field resolution, and plastic-free transducer housings reduce infection-control costs.

Note: Segment shares of all individual segments available upon report purchase

By Application: Glaucoma Outpaces Other Segments

Glaucoma and ocular hypertension use cases are projected to rise at 9.05% CAGR on the back of early-detection initiatives and laser-surgery adoption that demands precise angle imaging. UBM parameters such as trabecular-iris angle and ciliary-body thickness guide individualized management strategies.

Cataract assessment held a 40.20% of the ophthalmic ultrasound systems market in 2025 nonetheless holds sway because every phacoemulsification case requires axial-length confirmation, especially in dense lenses where optical biometers fail. Retinal disorder diagnostics, ocular trauma, and tumor assessment form complementary demand pillars that cushion vendors against cyclical shifts in any single specialty.

By End User: Clinics Gain Momentum

Hospitals accounted 49.10% market share of all shipments in 2025 since they host high-acuity retinal surgery and ocular oncology services. Yet ambulatory clinics demonstrate stronger growth because physician-owned centers benefit from quicker capital-expenditure approvals and shorter payback periods.

Clinics also dominate vision-correction counseling, where same-sit axial-length and pachymetry measurement improve patient conversion with a CAGR of 7.75% between 2026 and 2031. Academic institutes, though smaller in absolute share, drive protocol innovation; many pilot AI-assisted acquisition that later diffuses across the broader Ophthalmic Ultrasound Devices market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America led with 34.50% share in 2025 driven by early uptake of AI-enabled platforms, ample reimbursement, and a dense network of glaucoma and retina specialists. The FDA streamlined quality-management-system rules in February 2024, reducing documentation overlap and accelerating product launches. Portable scanners see brisk adoption in US ambulatory surgery centers because they eliminate the need for separate biometry suites.

Asia-Pacific is the fastest-growing region at 9.35% CAGR. Investments under India’s Ayushman Bharat program and China’s Healthy China 2030 blueprint expand cataract and diabetic-retinopathy screening. Domestic firms supply cost-optimized consoles, while global brands partner with provincial hospitals to install tele-expertise hubs. Portable ultrasound units facilitate eye camps in rural county fairs, boosting awareness and creating latent replacement demand.

Europe maintains steady performance, supported by well-funded national health services and stringent device-safety regulations that favor established brands. Carl Zeiss Meditec reported ophthalmology revenue of EUR 1,589.2 million (USD 1,776.4 million) in fiscal 2023/24, underscoring resilient capital investment despite macro headwinds. Integrated suites that link ultrasound, OCT, and fundus photography into a common software shell resonate with European workflow preferences.

Competitive Landscape

Market Concentration

The Ophthalmic Ultrasound Devices market hosts a blend of multinational corporations and specialist innovators. Zeiss expanded its capabilities through the EUR 99.9 million (USD 116.03 million) acquisition of the Dutch Ophthalmic Research Center, bringing vitreoretinal tools that complement its ultrasound portfolio. NIDEK emphasizes high-frequency biometry with swept-source modules while maintaining entry-level B-Scan lines for emerging markets. Quantel leverages its laser heritage to cross-sell ultrasound to retina surgeons.

Start-ups focus on handheld form factors and AI software layers. Clarius Mobile Health has added enterprise fleet management and CPT-code mapping to streamline US billing, illustrating the shift from hardware to workflow solutions. ArcScan gained Chinese NMPA approval for the Insight 100, broadening the technology’s addressable base. Competitive intensity is expected to rise around algorithm libraries that help less-experienced staff acquire diagnostic-grade clips, enabling differentiation beyond transducer specifications alone.

Ophthalmic Ultrasound Systems Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Clarius Mobile Health has unveiled new ultrasound innovations, including enterprise software for managing fleets of Clarius handheld scanners, enhanced AI-powered capabilities, and integrated CPT medical codes to streamline billing and reimbursement in the U.S. These advancements reinforce Clarius’ position as a prominent player in high-definition handheld ultrasound technology, offering improved workflow efficiency and support for clinical and administrative needs.

- September 2024: Clarius signed an agreement with EyeProGPO, highlighting its commitment to advancing ultrasound technology in ophthalmology and expanding its presence in the ophthalmic market.

- September 2024: ZEISS Medical Technology has announced the broad U.S. distribution of the ZEISS MICOR 700, a groundbreaking, ultrasound-free, hand-held device for lens extraction. Designed to enhance intraocular space while minimizing invasiveness, the MICOR 700 introduces a new standard in cataract surgery with its patented crystalline lens removal technology, rounded blunt-tip design, and single-use "plug & play" system. Offering a sustainable, low-cost solution with a minimal O.R. footprint, the device aims to deliver a gentler patient experience. ZEISS showcased the MICOR 700 at the American Academy of Ophthalmology (AAO) conference in October 2024 in Chicago.

- May 2024: ArcScan, Inc. has announced that its ArcScan Insight 100 has received approval from China’s National Medical Products Administration (NMPA), marking a significant milestone in the company's global expansion. The ultra-high frequency ultrasound device offers superior imaging of the anterior segment, surpassing the limitations of optical coherence tomography (OCT). This technology aims to support eyecare surgeons in addressing China’s growing myopia epidemic by enhancing diagnostic accuracy and improving post-surgical outcomes.

Table of Contents for Ophthalmic Ultrasound Systems Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Increasing Prevalence of Eye Diseases

- 4.2.2Advent of Novel Ophthalmic Technologies

- 4.2.3Growing Adoption of Point-of-Care Portable Ultrasound

- 4.2.4Rising Cataract Surgical Volumes

- 4.2.5Integration of AI-enhanced Image Analysis with Ultrasound Data

- 4.2.6Expansion of Ambulatory Surgical Centers & Ophthalmic Clinics

- 4.3Market Restraints

- 4.3.1Increasing Adoption of Alternate Imaging Modalities

- 4.3.2High Capital Outlay for High-Frequency Ultrasound Platforms

- 4.3.3Shortage of Trained Ophthalmic Sonographers in Low-income Regions

- 4.3.4Limited Awareness & Adoption in Underserved Regions

- 4.4Regulatory Landscape

- 4.5Technological Outlook

- 4.6Porter’s Five Forces Analysis

- 4.6.1Bargaining Power of Suppliers

- 4.6.2Bargaining Power of Buyers

- 4.6.3Threat of New Entrants

- 4.6.4Threat of Substitute Products

- 4.6.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value in USD)

- 5.1By Product

- 5.1.1A-Scan

- 5.1.2B-Scan

- 5.1.3Combined Scan

- 5.1.4Pachymeter

- 5.1.5Ultrasound Biomicroscopy (UBM)

- 5.2By Modality

- 5.2.1Portable

- 5.2.2Standalone

- 5.3By Technology

- 5.3.1Conventional Ultrasound

- 5.3.2Doppler / Colour-Flow Ultrasound

- 5.4By Application

- 5.4.1Cataract Assessment

- 5.4.2Glaucoma & Ocular Hypertension

- 5.4.3Retinal Disorders

- 5.4.4Ocular Trauma & Tumours

- 5.4.5Others

- 5.5By End User

- 5.5.1Hospitals

- 5.5.2Ophthalmology Clinics

- 5.5.3Ambulatory Surgical Centres

- 5.5.4Academic & Research Institutes

- 5.6By Geography

- 5.6.1North America

- 5.6.1.1United States

- 5.6.1.2Canada

- 5.6.1.3Mexico

- 5.6.2Europe

- 5.6.2.1Germany

- 5.6.2.2United Kingdom

- 5.6.2.3France

- 5.6.2.4Italy

- 5.6.2.5Spain

- 5.6.2.6Rest of Europe

- 5.6.3Asia-Pacific

- 5.6.3.1China

- 5.6.3.2Japan

- 5.6.3.3India

- 5.6.3.4Australia

- 5.6.3.5South Korea

- 5.6.3.6Rest of Asia-Pacific

- 5.6.4Middle East & Africa

- 5.6.4.1GCC

- 5.6.4.2South Africa

- 5.6.4.3Rest of Middle East & Africa

- 5.6.5South America

- 5.6.5.1Brazil

- 5.6.5.2Argentina

- 5.6.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1AMETEK (Reichert)

- 6.3.2Appasamy Associates

- 6.3.3Carl Zeiss Meditec AG

- 6.3.4Clarion Medical Technologies

- 6.3.5DGH Technology Inc.

- 6.3.6Lumibird Medical

- 6.3.7MEDA Co. Ltd.

- 6.3.8Micro Medical Devices

- 6.3.9NIDEK Co. Ltd.

- 6.3.10Sonomed Escalon

- 6.3.11Sonostar Technologies

- 6.3.12Nikon Corporation (Optos Plc)

- 6.3.13Tomey Corporation

- 6.3.14Lumibird Medical

- 6.3.15HiUltrasound.com

- 6.3.16Mecanmedical

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global Ophthalmic Ultrasound Systems Market Report Scope

Per the report's scope, ocular ultrasound, also known as ocular echography, "echo," or a B-scan, is a quick, non-invasive test routinely used in clinical practice to assess the structural integrity and pathology of the eye. The Ophthalmic Ultrasound Systems Market is segmented by product (A- Scan, B- Scan, Combined Scan, Pachymeter, and Ultrasound Bio-microscopy (UBM)), modality (Portable and Standalone), end user (Hospitals, Ophthalmology, Clinics, and Others) and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (USD million) for the above segments.