Ophthalmic Loupes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

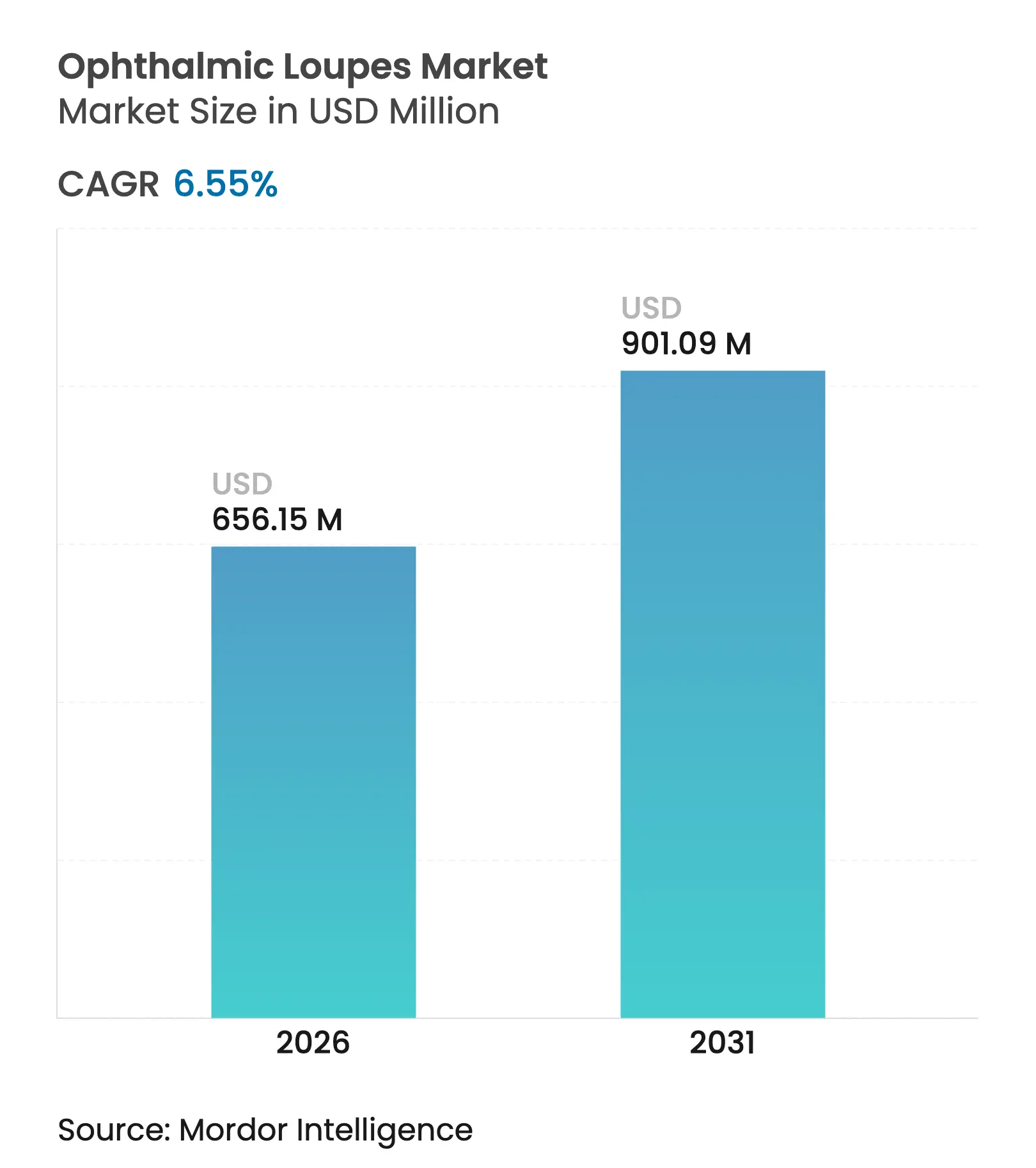

| Market Size (2026) | USD 656.15 Million |

| Market Size (2031) | USD 901.09 Million |

| Growth Rate (2026 - 2031) | 6.55 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Ophthalmic Loupes Market Analysis by Mordor Intelligence

Ophthalmic loupes market size in 2026 is estimated at USD 656.15 million, growing from 2025 value of USD 615.81 million with 2031 projections showing USD 901.09 million, growing at 6.55% CAGR over 2026-2031. Surgeons moving routine procedures into ambulatory settings favor compact magnification systems that fit easily inside smaller theaters. Galilean optics still dominate entry-level purchases, yet prismatic and Keplerian solutions gain ground as buyers seek higher visual acuity and lower musculoskeletal strain. Wider coverage for day-care eye surgery across major payors reduces the financial barrier to premium loupes, while e-commerce platforms that capture facial metrics online shorten the custom-fit sales cycle. Ergonomically optimized frames lower the risk of work-related neck pain, an increasingly important factor for aging surgeons.

Key Report Takeaways

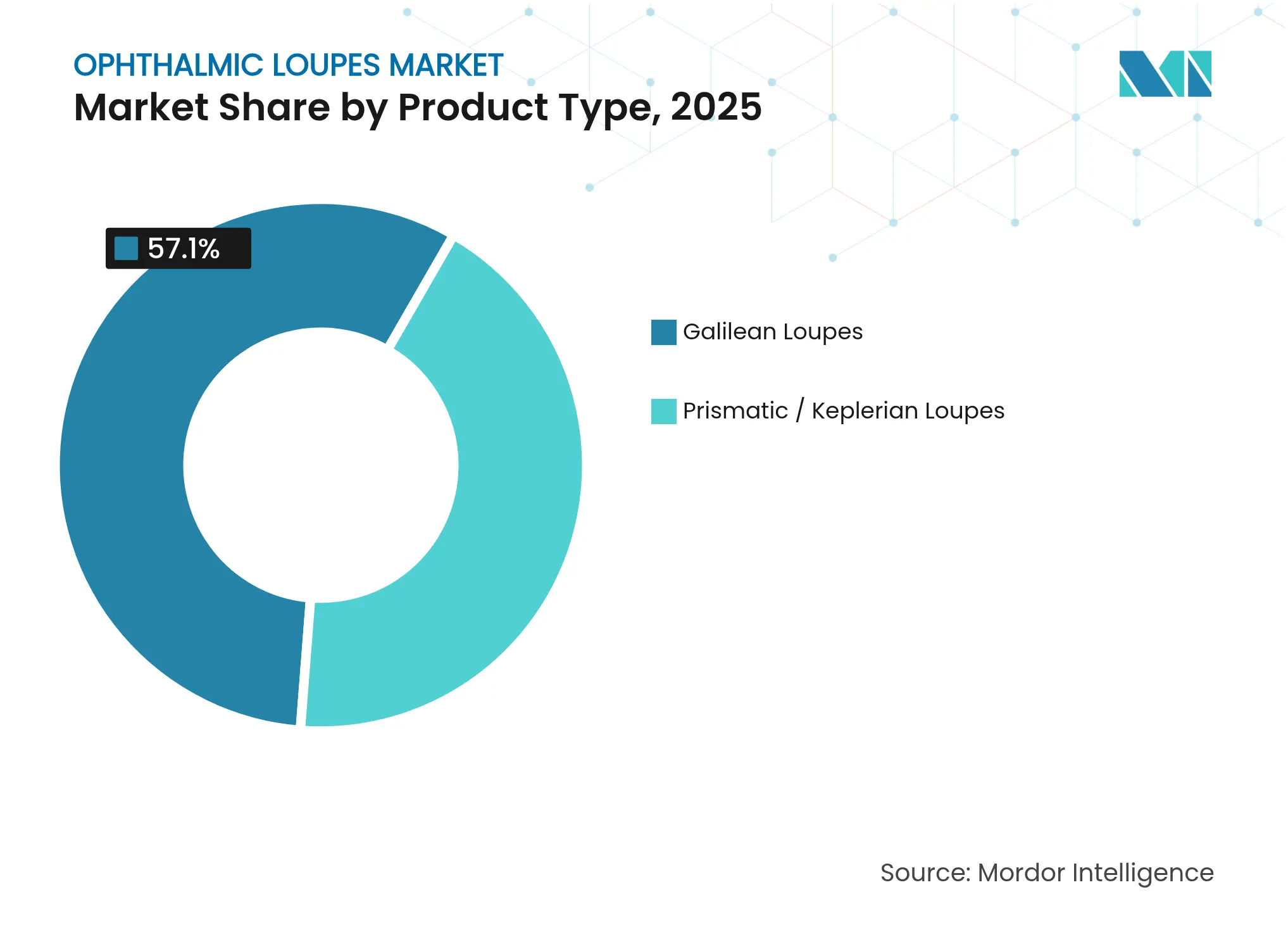

- By product type, Galilean loupes held 57.10% of the ophthalmic loupes market share in 2025, whereas prismatic systems are poised for the quickest expansion at a 7.28% CAGR to 2031.

- By design, through-the-lens (TTL) models accounted for 63.90% revenue share in 2025; flip-up units record the highest projected CAGR of 7.05% through 2031.

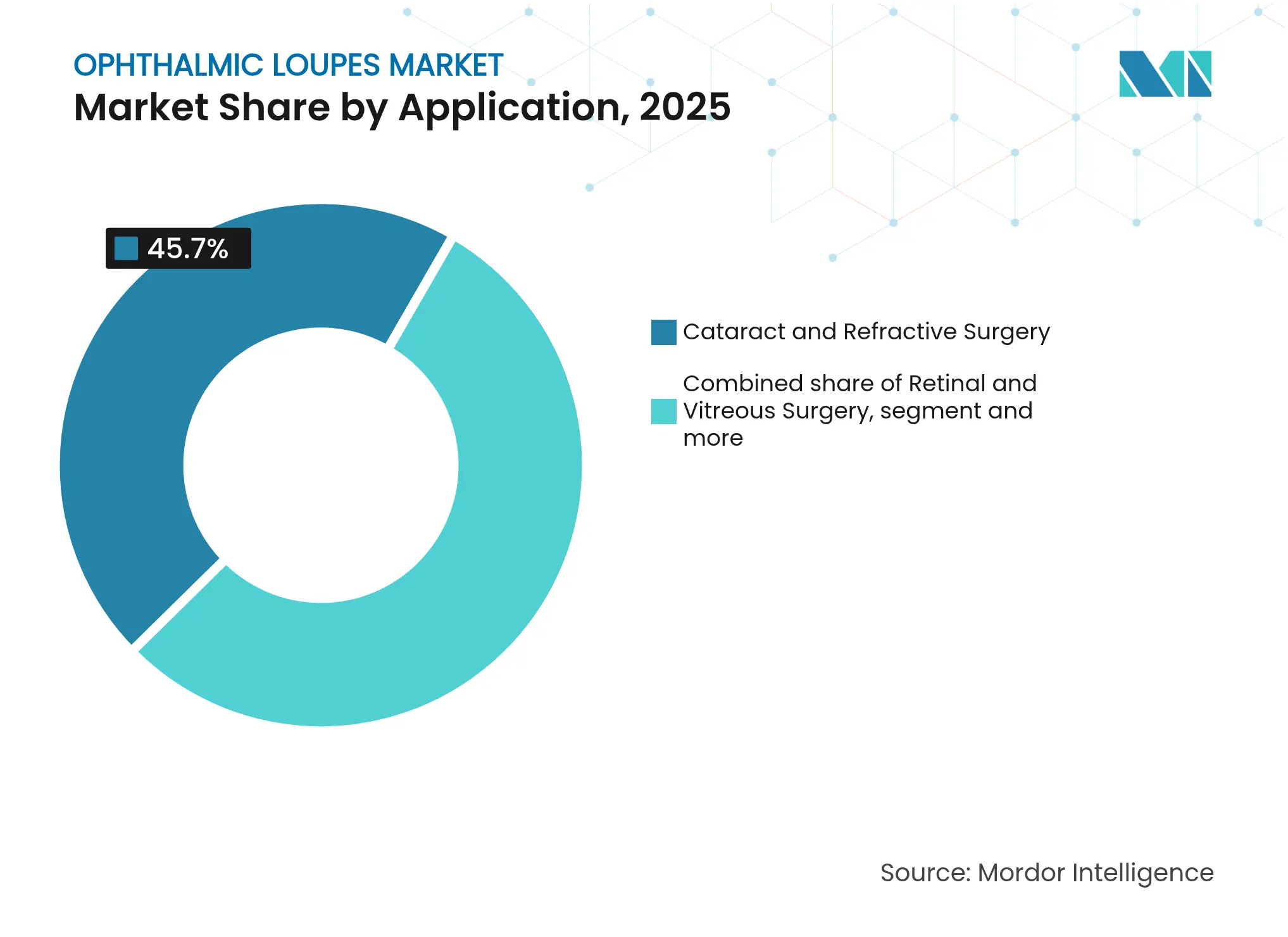

- By application, cataract and refractive surgery captured 45.70% of the ophthalmic loupes market size in 2025; retinal and vitreous surgery is projected to grow at a 7.46% CAGR to 2031.

- By end user, ambulatory surgical centers led growth with an 7.79% CAGR forecast through 2031, while hospitals retained 45.60% share of current revenue.

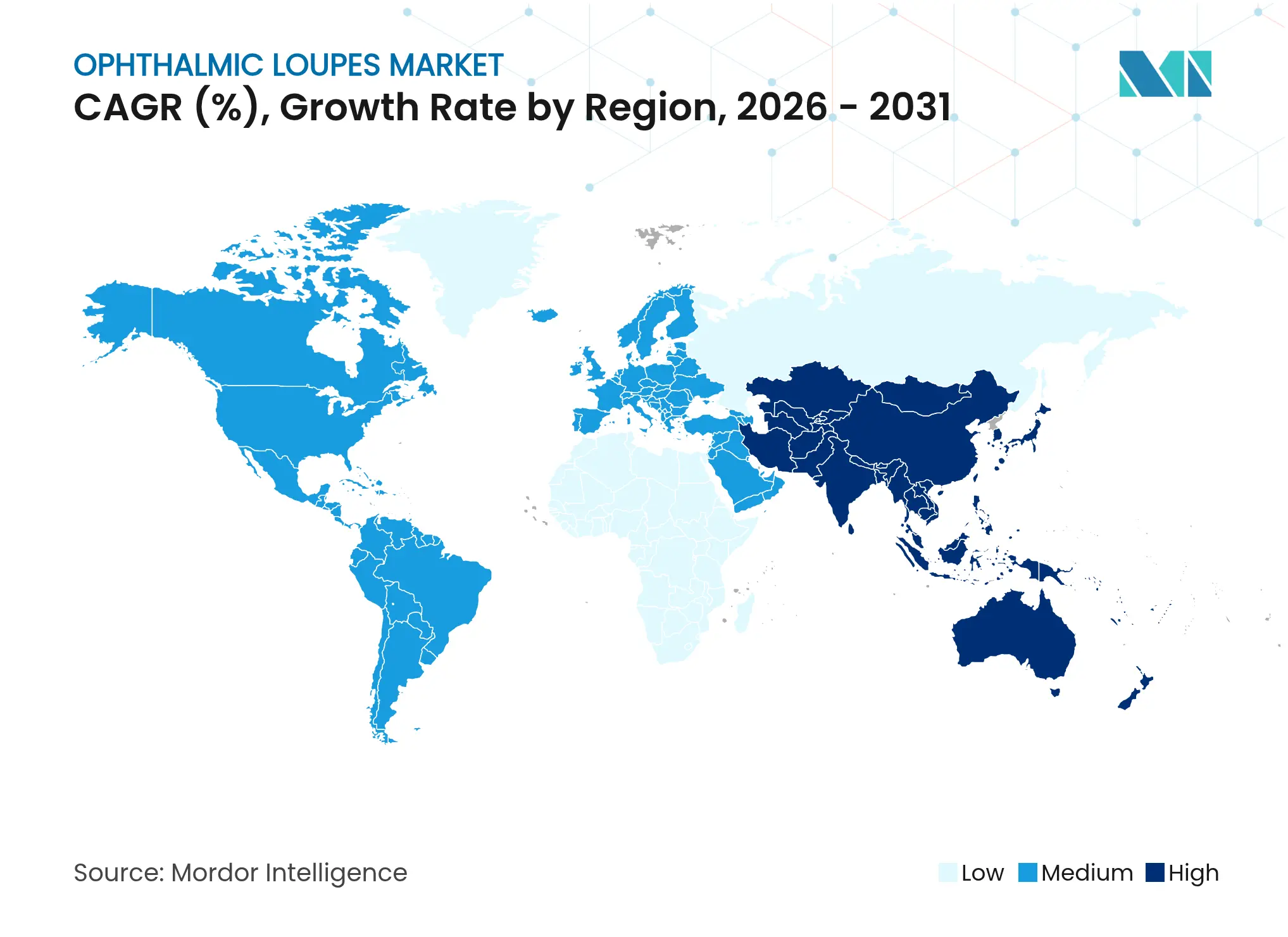

- By geography, North America represented 41.00% of 2025 sales; Asia-Pacific stands out as the fastest-growing region at an 8.22% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ophthalmic Loupes Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising prevalence of ocular diseases & surgical volumes Rising prevalence of ocular diseases & surgical volumes | +1.2% | Global, with concentration in aging populations of North America and Europe | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:+1.2% | Geographic Relevance:Global, with concentration in aging populations of North America and Europe | Impact Timeline:Long term (≥ 4 years) |

Rapid optical & ergonomic technology advances in loupes Rapid optical & ergonomic technology advances in loupes | +0.8% | Global, led by innovation centers in Germany, USA, and Japan | Medium term (2-4 years) | |||

Wider insurance coverage for day-care ophthalmic surgeries Wider insurance coverage for day-care ophthalmic surgeries | +0.6% | North America and Europe, with emerging coverage in Asia-Pacific | Medium term (2-4 years) | |||

Expansion of ophthalmic training programs globally Expansion of ophthalmic training programs globally | +0.4% | Global, with accelerated growth in Asia-Pacific and Latin America | Long term (≥ 4 years) | |||

Surgeons' demand for ergonomic devices to cut MSD risk Surgeons' demand for ergonomic devices to cut MSD risk | +0.3% | Global, particularly in developed markets with aging surgeon populations | Short term (≤ 2 years) | |||

E-commerce custom-fit loupe platforms shortening sales cycles E-commerce custom-fit loupe platforms shortening sales cycles | +0.2% | Global, with fastest adoption in North America and Europe | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Rising prevalence of ocular diseases & surgical volumes

Age-linked cataract, diabetic retinopathy, and glaucoma continue to swell procedure counts worldwide. Cataract operations already dominate outpatient ophthalmology, representing 86% of day-care eye surgeries. Medicare coverage of micro-invasive glaucoma surgery further enlarges the pool of procedures that benefit from portable magnification. A projected 30% shortfall in trained ophthalmologists by 2035 magnifies productivity pressures, making loupes indispensable in sustaining throughput without compromising accuracy.

Rapid optical & ergonomic technology advances in loupes

Prismatic systems cut head flexion and neck muscle activity compared with Galilean optics, improving surgeon comfort during long cases.[1]Frontiers in Public Health, “Ergonomic Assessment of Prismatic Loupes,” frontiersin.org High-index glass, anti-reflection coatings, and angled-optic designs now deliver 4.5× magnification with minimal chromatic aberration. Precise verification of prism alignment under ANSI Z80.1 has become routine to prevent eye strain and ensure image fidelity, compelling manufacturers to strengthen quality controls.

Wider insurance coverage for day-care ophthalmic surgeries

Reimbursement shifts speed adoption of office-based surgical suites that rely on lightweight loupes instead of bulky microscopes. UnitedHealthcare Medicare Advantage now recognizes a wider array of postoperative vision services, reinforcing demand for precision magnification in lower-cost settings. Comparative studies show office suites deliver safety outcomes on par with hospital theaters while cutting overhead, encouraging practices to invest in premium optics.

Expansion of ophthalmic training programs globally

Diversity-focused initiatives such as the Rabb-Venable program increase residency placements, enlarging the trainee base that requires affordable starter loupes. In parallel, expanded procedural scope for optometrists, including YAG capsulotomy, drives sales of mid-range systems to non-surgical specialists who now perform laser treatments.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High cost of premium prismatic systems High cost of premium prismatic systems | -0.9% | Global, with particular impact in price-sensitive emerging markets | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-0.9% | Geographic Relevance:Global, with particular impact in price-sensitive emerging markets | Impact Timeline:Medium term (2-4 years) |

Preference for surgical microscopes in tertiary centers Preference for surgical microscopes in tertiary centers | -0.7% | Global, concentrated in academic medical centers and large hospitals | Long term (≥ 4 years) | |||

Lack of declination-angle training causing adoption hesitancy Lack of declination-angle training causing adoption hesitancy | -0.5% | Global, with higher impact in regions with limited continuing education | Short term (≤ 2 years) | |||

Supply-chain concentration in precision optics drives lead times Supply-chain concentration in precision optics drives lead times | -0.4% | Global, with particular vulnerability in supply-chain dependent regions | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High cost of premium prismatic systems

Keplerian optics can cost two to three times more than Galilean units, slowing uptake in price-sensitive clinics. Although the ergonomic payoff is clear for high-volume surgeons, smaller practices hesitate to commit capital until insurers raise procedural fees. Zeiss noted softer demand in China in FY 2024/25 as financing costs rose, illustrating how macro-economic headwinds constrain big-ticket optical purchases.

Preference for surgical microscopes in tertiary centers

Large teaching hospitals increasingly adopt 3D digital microscopes such as the ARTEVO 850, which integrate image capture, heads-up display, and intra-operative OCT in one platform.[2]Cleveland Clinic, “Comparative Study of Digital Microscopes,” clevelandclinic.org These systems deliver broader functionality than loupes and can displace them in complex retinal or corneal work, capping potential volumes in the top end of the surgical market.

Segment Analysis

By Product Type: Prismatic Systems Drive Innovation

Galilean optics retained a 57.10% revenue lead in 2025, underscoring their cost-efficiency for routine cataract work. The ophthalmic loupes market, however, increasingly pivots toward prismatic designs growing at 7.28% CAGR. Early adopters praise Keplerian clarity during micro-incision vitrectomy, where 4.5× imaging delivers crisp depth cues. Clinical trials logged a measurable 15° reduction in head tilt for prismatic users, lowering chronic neck strain. Second-generation interchangeable barrels now let surgeons toggle magnifications mid-case, boosting throughput in multi-stage procedures.

The premium segment rewards manufacturers that certify optical fidelity down to 0.25 diopter variance, exceeding ANSI tolerances. Emerging 3D-printed titanium frames lighten overall weight by 18%, enabling longer wear times without pressure points. Although sticker shock limits entry in low-resource clinics, e-commerce platforms that bundle financing and virtual try-on narrow the gap. With surgeons valuing every saved minute, prismatic tooling is expected to outpace basic optics even where initial budgets are tight.

Note: Segment shares of all individual segments available upon report purchase

By Design: TTL Dominance Faces Flip-Up Challenge

Through-the-lens configurations captured 63.90% of 2025 revenue thanks to fixed-axis stability that virtually eliminates parallax errors. Each optical pod is laser-aligned to the wearer’s pupillary distance, enhancing focus while reducing eye fatigue. Hospitals still outfit residents with TTL starter kits to build habit strength early. Nonetheless, flip-up adoption is climbing 7.05% annually as multispecialty practices switch between microscopic and gross visualization inside one session.

Modern hinge architecture now endures 20,000 up-down cycles without drift, extending service life beyond five years. Detachable LED modules snap onto flip-ups, freeing surgeons from ceiling-mounted light booms. Augmented-reality developers favor pivoting frames because displays never block the unaided field when raised. The ophthalmic loupes market shows early signs of convergence, with hybrid TTL frames offering partial vertical travel to marry rigidity with occasional declination.

By Application: Retinal Surgery Drives Growth

Cataract and refractive work contributed 45.70% of the ophthalmic loupes market share in 2025, reflecting sheer case volume. Outpatient suites where 86% of cataract procedures occur lean on portable loupes for quick room turnover. Yet retinal and vitreous interventions expand fastest at a 7.46% CAGR, buoyed by rising diabetic retinopathy prevalence. Micro-incision plasmablade repairs demand 4× or greater magnification, steering surgeons toward prismatic optics with larger ocular ports.

Combined cataract-glaucoma packages reimbursed by Medicare spur dual-procedure days, pushing buyers toward lightweight gear that avoids resetting table-mounted microscopes. Training labs likewise order higher-mag systems so residents can practice ILM peeling on simulated eyes. As reimbursement widens to cover more posterior-segment therapeutics, premium loupe sales in vitreoretinal clusters will exceed historical trends.

Note: Segment shares of all individual segments available upon report purchase

By End User: ASCs Accelerate Adoption

Hospitals still generated 45.60% of revenue in 2025, buoyed by capital budgets and teaching rotations. They often pair TTL optics with overhead microscopes, deploying loupes mainly for peri-operative steps. Ambulatory surgical centers, however, are the clear growth engine, advancing 7.79% per year. Bundled payments push case efficiency, and loupes slash room setup by eliminating microscope draping.

Specialty clinics exploit this edge to migrate high-margin lens exchanges out of hospitals. Medicare’s site-neutral payment trials further encourage community-based facilities to invest in premium optical aids. Artificial-intelligence video analytics embedded within ASC workflow platforms already synchronize loupe LEDs with phase-of-surgery cues, shaving seconds off each pass. Consequently, administrators view ergonomic optics as operational assets rather than discretionary tools.

Geography Analysis

North America accounted for 41.00% of global revenue in 2025. Uptake is bolstered by Medicare rules that reimburse micro-invasive glaucoma add-ons, making precision optics essential for combo surgeries. The United States faces a 30% ophthalmologist shortfall by 2035, so practices adopt high-magnification loupes to maintain productivity without hiring additional staff. Zeiss’s new Missouri plant adds domestic capacity and shortens service turnaround, giving the firm a home-field advantage.

Asia-Pacific leads in growth at an 8.22% CAGR as middle-class demand for vision correction rises. Japan’s super-aged society keeps cataract corridors busy, whereas India’s public-private hospital build-outs invite cost-effective entry-level optics. Temporary softness in China due to macro headwinds saw premium prices trimmed, yet long-term fundamentals remain intact as provincial insurers gradually extend day-surgery coverage. Manufacturers that offer 3D-printed lightweight frames at sub-USD 1,000 price points find ready buyers in Southeast Asia.

Europe shows steady but slower expansion under stringent MDR rules that favor clinically proven models. German and French insurers cover loupe purchases for accredited surgeries, driving steady TTL refresh cycles every five years. The Middle East invests heavily in ophthalmology hubs within medical-tourism corridors, offering tax incentives for equipment imports. Latin America lags due to currency volatility, but Chile and Colombia post double-digit unit growth where private insurers subsidize day-care cataract bundles.

Competitive Landscape

Market Concentration

The ophthalmic loupes market remains moderately fragmented. Five leading vendors collectively control 55% of revenue, leaving ample space for niche entrants. Zeiss consolidates optical know-how and surgical instrumentation after acquiring D.O.R.C., positioning itself as a one-stop supplier for retina suites. Orascoptic and Designs for Vision diversify with custom 3D facial scanning apps that cut fitting time to under seven minutes, differentiating on user experience.

Regulatory overhead is low; the FDA classifies most surgical loupes as Class I devices exempt from 510(k), accelerating launch cycles. This openness attracts tech start-ups such as Ocutrx, whose DigiLoupe overlays fluorescence imaging onto the surgical field, merging AR with traditional optics.[3]Ocutrx Technologies, “DigiLoupe AR Product Brief,” ocutrxtech.com Established brands respond by embedding wireless battery packs and Bluetooth-driven adjustment motors that let users tweak inter-pupillary distance mid-case.

Supply-chain stress in precision glass grinding persists, with two German foundries providing the bulk of high-index blanks. Vendors mitigate risk through dual-sourcing and by machining polymer hybrids that match glass clarity at half the weight. The race to prove ergonomic claims fuels academic partnerships; peer-reviewed papers validating postural benefits often translate into hospital purchasing criteria. In this environment, manufacturers that back data with independent trials win long-term tenders.

Ophthalmic Loupes Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: FDA finalized Quality System Regulation amendments, harmonizing device GMP with ISO 13485 standards and raising documentation expectations for loupe manufacturers.

- October 2024: Carl Zeiss Meditec opened a research and production site in Chesterfield, Missouri, expanding U.S. capacity for high-precision surgical instruments.

- September 2024: Zeiss debuted the ARTEVO 850 3D digital visualization platform and single-use RESIGHT lenses at EURETINA 2024, extending digital workflow compatibility.

- January 2024: Ocutrx released the DigiLoupe AR headset, blending augmented reality overlays with standard optical magnification to enhance vitreoretinal procedures.

Table of Contents for Ophthalmic Loupes Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising prevalence of ocular diseases & surgical volumes

- 4.2.2Rapid optical & ergonomic technology advances in loupes

- 4.2.3Wider insurance coverage for day-care ophthalmic surgeries

- 4.2.4Expansion of ophthalmic training programs globally

- 4.2.5Surgeons’ demand for ergonomic devices to cut MSD risk

- 4.2.6E-commerce custom-fit loupe platforms shortening sales cycles

- 4.3Market Restraints

- 4.3.1High cost of premium prismatic systems

- 4.3.2Preference for surgical microscopes in tertiary centers

- 4.3.3Lack of declination-angle training causing adoption hesitancy

- 4.3.4Supply-chain concentration in precision optics drives lead times

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitute Products

- 4.7.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Product Type

- 5.1.1Galilean Loupes

- 5.1.2Prismatic / Keplerian Loupes

- 5.2By Design

- 5.2.1Through-The-Lens (TTL)

- 5.2.2Flip-Up

- 5.3By Application

- 5.3.1Cataract and Refractive Surgery

- 5.3.2Retinal and Vitreous Surgery

- 5.3.3Glaucoma and Corneal Surgery

- 5.3.4Others

- 5.4By End User

- 5.4.1Hospitals

- 5.4.2Specialty Ophthalmology Clinics

- 5.4.3Ambulatory Surgical Centers

- 5.4.4Others

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Carl Zeiss Meditec AG

- 6.3.2Orascoptic (KaVo Kerr)

- 6.3.3SurgiTel (General Scientific Corporation)

- 6.3.4Designs for Vision, Inc.

- 6.3.5Univet S.r.l.

- 6.3.6Keeler Ltd (Halma plc)

- 6.3.7SheerVision Inc.

- 6.3.8Rudolph Riester GmbH

- 6.3.9Neitz Instruments Co., Ltd.

- 6.3.10Rose Micro Solutions

- 6.3.11LumaDent Inc.

- 6.3.12HEINE Optotechnik GmbH & Co. KG

- 6.3.13Den-Mat Holdings, LLC

- 6.3.14Zumax Medical Co., Ltd.

- 6.3.15Novocam Medical Innovations Oy

- 6.3.16Ergonoptix

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Ophthalmic Loupes Market Report Scope

Ophthalmic loupes are simple optical devices that are used to view the object. Loupes are essential in ophthalmic surgery as they enhance and magnify the object.

The ophthalmic loupes market is segmented by type of loupe, application, end user, and geography. The type of loupe segment is further divided into Galilean loupes and prismatic loupes. The application segment is further divided into surgical procedures, dental applications, and others. Other applications include research applications and academic applications. By end user, the market is further divided into hospitals, specialty clinics, and ambulatory surgical centers. The geography segment is further divided into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report offers the value (USD) for all the above segments.