Ophthalmic Viscosurgical Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

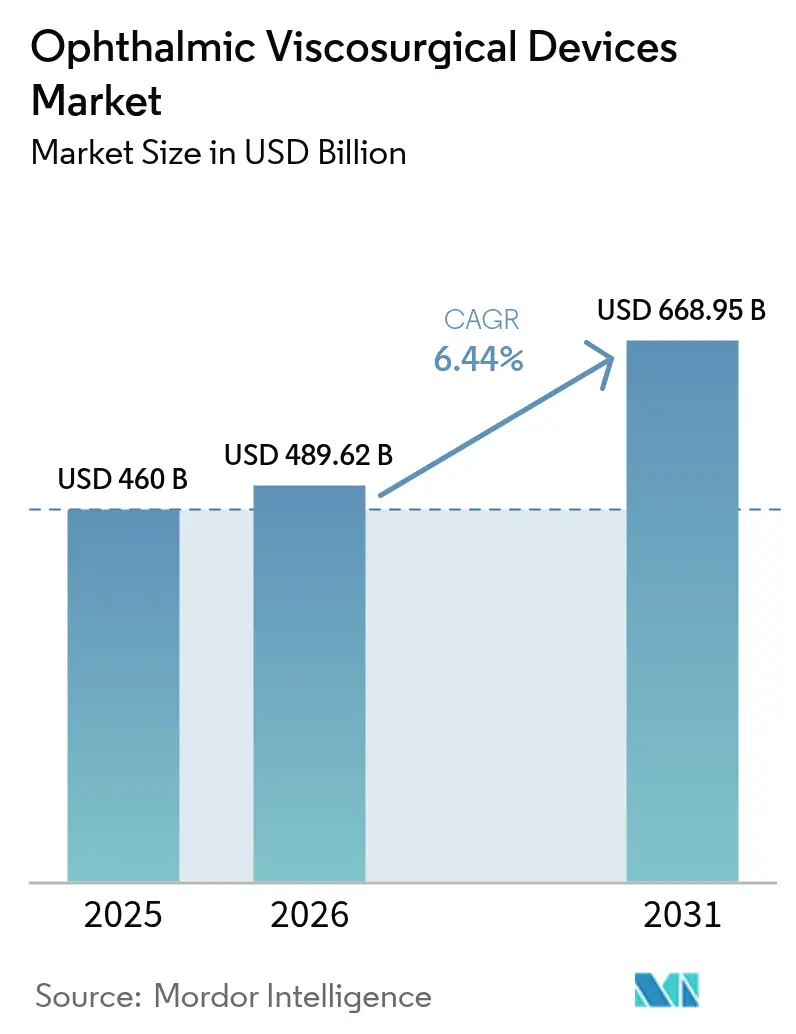

| Market Size (2026) | USD 489.62 Billion |

| Market Size (2031) | USD 668.95 Billion |

| Growth Rate (2026 - 2031) | 6.44% CAGR |

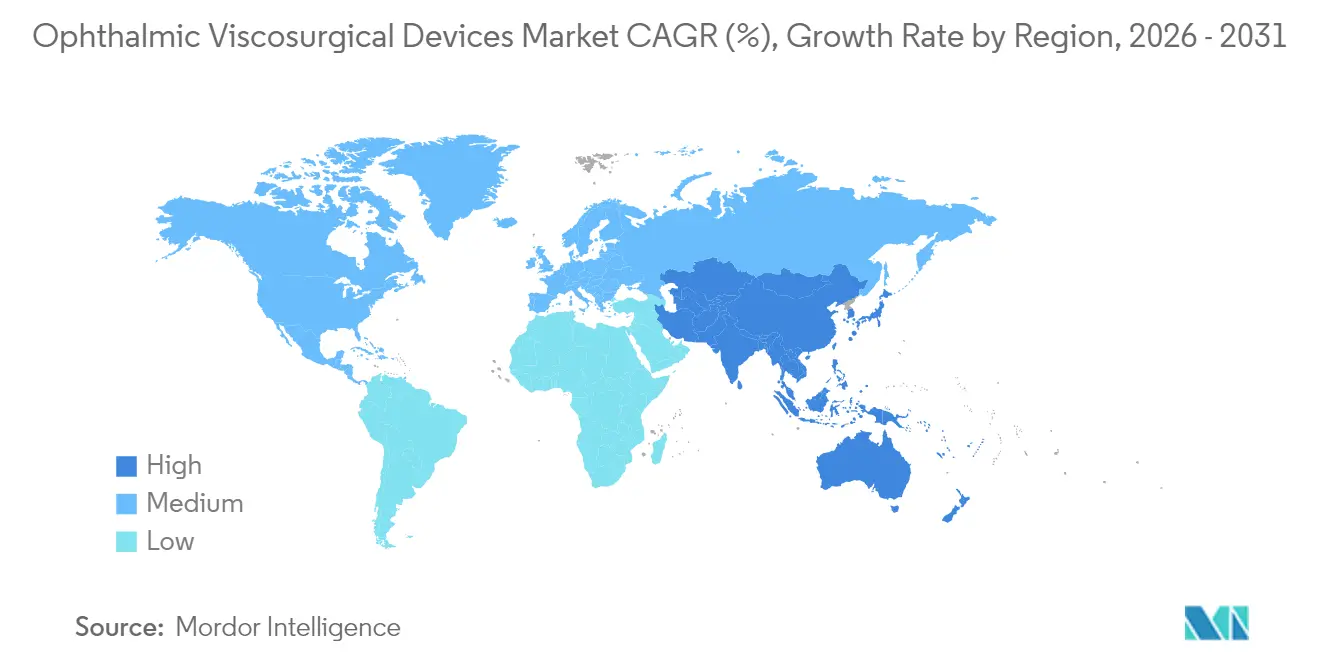

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

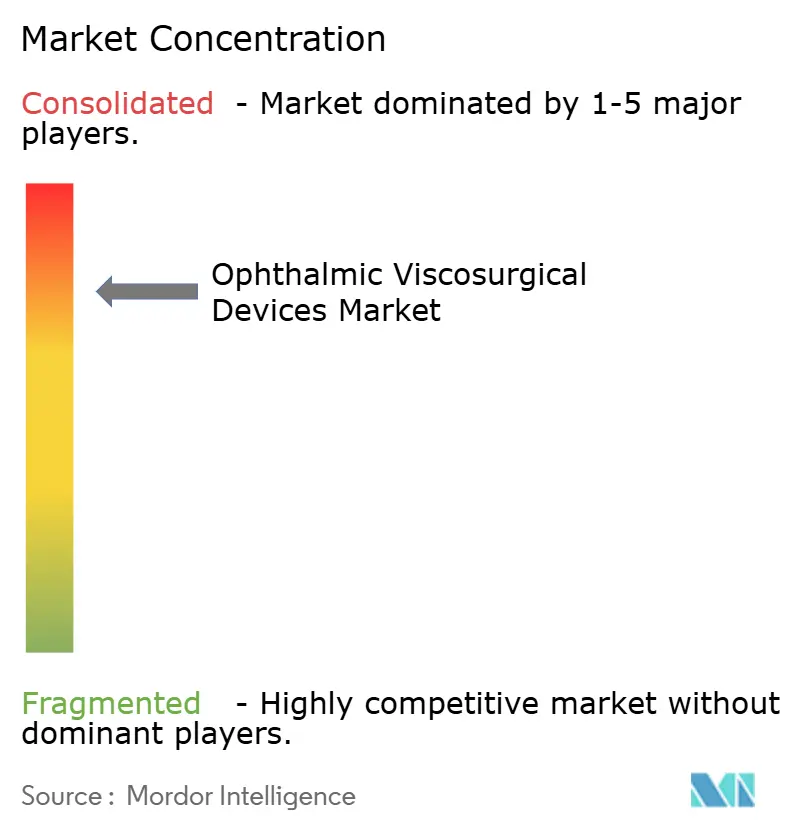

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ophthalmic Viscosurgical Devices Market Analysis by Mordor Intelligence

The ophthalmic viscosurgical devices market size is expected to grow from USD 460 million in 2025 to USD 489.62 million in 2026 and is forecast to reach USD 668.95 million by 2031 at 6.44% CAGR over 2026-2031. Rising global cataract procedure counts, broader adoption of minimally invasive glaucoma surgery, and steady upgrades to premium anterior-segment platforms combine to lift both unit volumes and average selling prices. Hospitals in mature health systems keep lengthening theatre schedules to accommodate cataract backlogs, while ambulatory surgical centers (ASCs) drive throughput gains that favor single-use viscoelastic packs. Surgeons are consolidating purchases around multi-property formulations that toggle between dispersive and cohesive behavior, strengthening the role of full-procedure kits. Environmental criteria are starting to sway tenders, prompting manufacturers to publish life-cycle analyses and revamp packaging as a competitive lever.

Key Report Takeaways

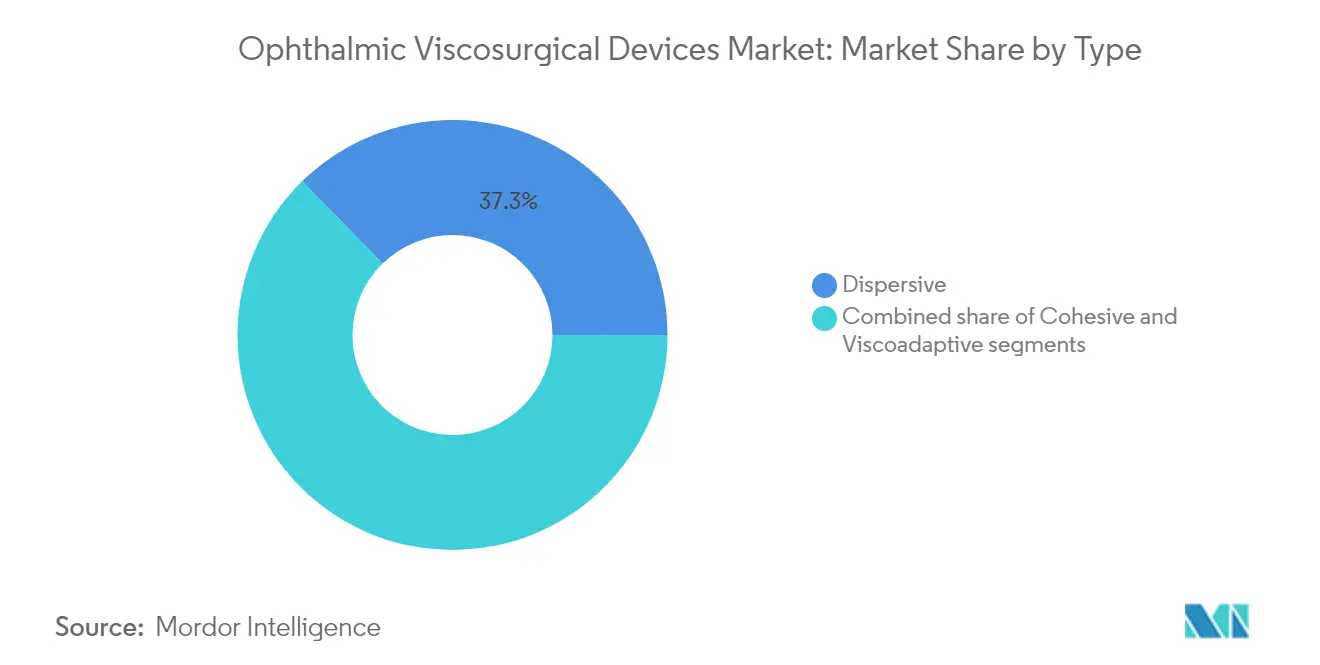

- By product type, dispersive agents led with 37.33% of ophthalmic viscosurgical devices market share in 2025, whereas viscoadaptive agents are forecast to post the fastest 7.59%CAGR through 2031.

- By source, bacteria-derived hyaluronic acid captured 39.02% share of the ophthalmic viscosurgical devices market size in 2025; semi-synthetic/fermentation grades are set to expand at an 8.74%CAGR to 2031.

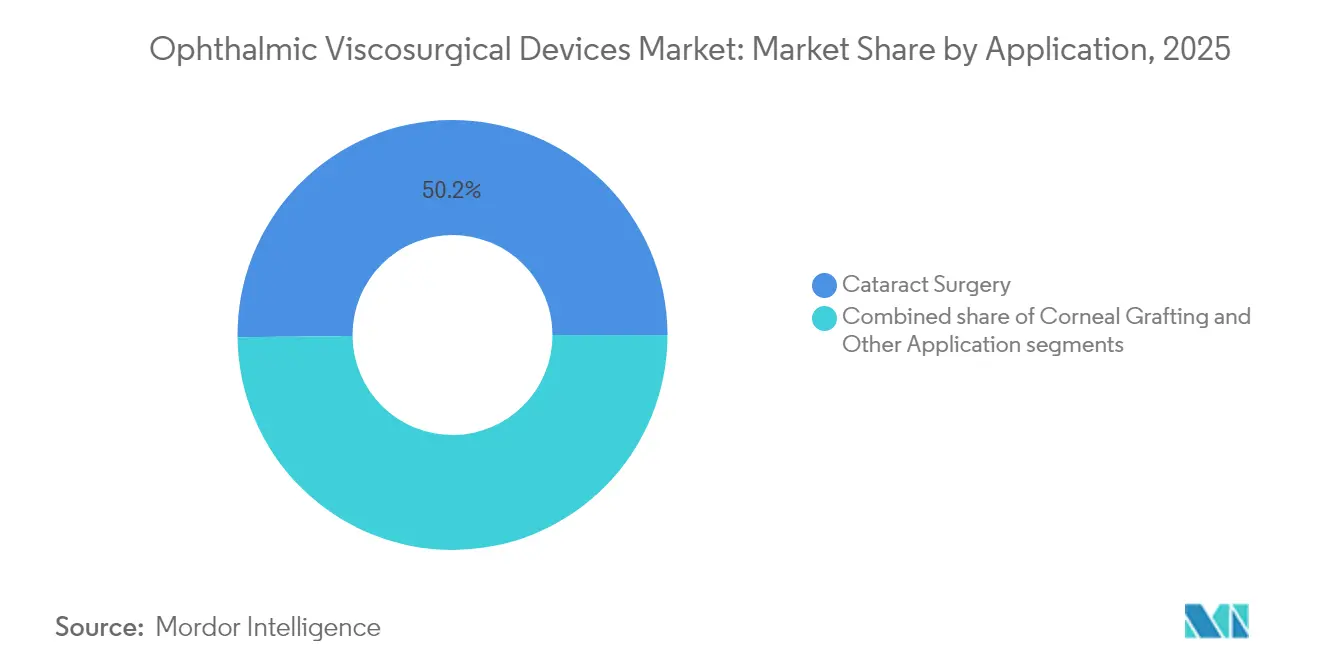

- By application, cataract surgery accounted for 50.17% of the ophthalmic viscosurgical devices market size in 2025, while glaucoma procedures exhibit the highest 6.47%CAGR through 2031.

- By end user, hospitals held 59.74% revenue share in 2025; ASCs represent the fastest-growing channel with an 8.06%CAGR through 2031.

- By geography, North America held 37.58% revenue share in 2025; Asia-Pacific represent the fastest-growing region with an 7.68%CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ophthalmic Viscosurgical Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging cataract-prone population | +1.3% | Global (high in North America & Europe) | Long term (≥ 4 years) |

| Diabetes-linked ocular complications | +1.0% | North America & Asia-Pacific | Medium term (2-4 years) |

| Phaco, femto & MIGS tech evolution | +0.9% | Tri-region (NA, EU, APAC) | Short term (≤ 2 years) |

| ASC growth & blindness-prevention programs | +0.8% | United States & Asia | Short term (≤ 2 years) |

| Rising healthcare spend & cataract reimbursement | +0.7% | OECD markets & large emerging economies | Medium term (2-4 years) |

| Precision-fermentation of high-MW HA | +0.6% | Europe, North America, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Demographic Expansion of the Cataract-Prone Elderly Cohort

Disability-adjusted life years lost to cataract rose from 6.68 million in 2019 to 7.1 million in 2021 and could exceed 7.5 million by 2025 if incidence trends hold[1]Thomas R. et al., “Global Burden of Disease Cataract Update,” nature.com. A 2024 meta-analysis logged 17 million people blind and 83.5 million experiencing moderate-to-severe visual impairment from cataract in 2020. Hospitals in high-income countries now face six-week median waitlists for extraction slots, directly inflating baseline use of viscoelastic syringes. Every additional year of life expectancy raises the surgical funnel, ensuring that the ophthalmic viscosurgical devices market keeps outpacing the broader ophthalmology consumables sector. Forward bookings released in early 2025 underscore unmet demand, implying stronger device pull-through even when per-procedure dosing remains constant.

Escalating Incidence of Diabetes-Linked Ocular Complications

Adults with diabetes develop cataract earlier and more aggressively than non-diabetic peers, pulling forward first-surgery age and lengthening lifetime exposure to viscoelastics. Routine early screening raises intervention rates that spill over into glaucoma and vitrectomy indications. Manufacturers now emphasize formulas that temper postoperative intraocular pressure spikes, positioning such attributes as clinical differentiators. Surgeons treating younger diabetic cohorts favor viscoadaptives that preserve endothelial integrity, reinforcing premium-tier demand. The ophthalmic viscosurgical devices market therefore benefits from a double-lift of larger patient cohorts and higher-value product mix.

Technological Evolution in Phaco, Femto and MIGS Platforms

Femtosecond laser-assisted cataract surgery produces micro-bubble turbulence that threatens corneal endothelium without high-molecular-weight buffering. As micro-incision tips enter mainstream use, surgeons demand viscoadaptive blends that hold chamber depth yet evacuate debris swiftly. Rapid growth in MIGS procedures intensifies calls for ultra-clear, low-particulate viscoelastics that do not obscure gonioscopic views. These platform advances raise performance expectations and solidify the ophthalmic viscosurgical devices market as a growth outlier among single-use surgical supplies.

Growing Surgical Capacity via ASCs and National Blindness-Prevention Programs

ASCs now conduct nearly one in five Medicare-funded cataract operations in the United States. Lower overhead speeds payback on premium gear, encouraging uptake of high-performance ophthalmic viscosurgical agents that shorten chair time. Across Asia, government-backed cataract campaigns equip outreach units with compact kits that bundle pre-filled viscoelastic syringes, generating bulk orders during high-volume surgical days. This temporal clustering of demand helps manufacturers plan production runs and smooth inventory cycles for the ophthalmic viscosurgical devices market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price sensitivity & reimbursement caps | –0.7% | United States & Europe | Short term (≤ 2 years) |

| Low-OVD or OVD-free surgical techniques | –0.5% | High-volume global centers | Medium term (2-4 years) |

| Stringent regulatory scrutiny | –0.4% | Global (notably EU & US) | Long term (≥ 4 years) |

| Environmental waste-management costs | –0.3% | Europe & North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Sensitivity and Reimbursement Caps on Premium OVD Grades

ASC payments are tethered to the hospital outpatient schedule, bundling viscoelastic costs into wider cataract reimbursement packages. When payment ceilings squeeze margins, procurement teams pivot toward mid-tier formulations or negotiate bulk discounts. European hospitals operating under value-based budgets demand peer-reviewed endothelial cell-loss data before approving costlier upgrades, favoring companies that fund robust clinical-support programs. This reimbursement compression moderates premium-mix expansion within the ophthalmic viscosurgical devices market without derailing overall volume growth.

Availability of Low-OVD or OVD-Free Surgical Techniques

New fluidics systems stabilize the anterior chamber with balanced salt solution, reducing viscoelastic volume per case. Pilot audits show tangible cutbacks, yet surgeons still rely on OVDs for capsulorhexis and lens implantation phases. Immediate sequential bilateral cataract surgery promises per-patient efficiencies but usually mandates separate single-use packs for risk control, partially offsetting consumption declines. The net effect is a gradual, not precipitous, tempering of demand within the ophthalmic viscosurgical devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Dispersive Agents Dominate, Viscoadaptives Accelerate

Dispersive agents accounted for the largest 37.33% share of the ophthalmic viscosurgical devices market size in 2025, benefiting from their ability to coat delicate tissue during nucleus disassembly. Surgeons manage complex cataract presentations—pseudoexfoliation, shallow chambers, post-LASIK cases—by alternating dispersive and cohesive OVDs within a single procedure, lifting per-case volume. Innovators now embed anti-oxidant additives into dispersive formulations, defending price points even in cost-sensitive tenders.

Viscoadaptive blends are expanding fastest at a 7.59%CAGR to 2031, propelled by premium intraocular lens (IOL) cases that demand superior endothelial protection. These agents behave cohesively under low shear and disperse under high flow, maintaining chamber stability during phacoemulsification or femtosecond fragmentation. Manufacturers tie viscoadaptive syringes to injector systems, locking in surgeon loyalty and deepening penetration of the ophthalmic viscosurgical devices market.

By Source: Biological Hyaluronic Acid Leads, Fermentation Grades Gain Ground

Bacteria-derived hyaluronic acid secured a 39.02% slice of the ophthalmic viscosurgical devices market share in 2025, prized for consistent chain length and low immunogenicity. Hospitals align these products with sustainability scorecards that favor animal-free sourcing. Supply reliability further cements the segment’s leadership.

Semi-synthetic/fermentation grades are slated for an 8.74%CAGR through 2031. Fermentation allows rapid scale-up and precise molecular-weight control, enabling custom blends for combined cataract–glaucoma cases. Procurement teams appreciate insulation from livestock disease shocks, increasing the strategic appeal of fermentation routes within the ophthalmic viscosurgical devices market. Animal-derived sources retain a foothold on price but are ceding ground as regulators endorse animal-protein reduction.

By Application: Cataract Still the Workhorse, Glaucoma Emerging

Cataract surgery generated 50.17% of the ophthalmic viscosurgical devices market size in 2025. Procedure volumes in the United States top 4 million annually and are heading toward 6 million by 2030. Every cataract case consumes at least one syringe, anchoring baseline demand. Hospitals now schedule extended evening lists to cut waiting times, an operational change that further lifts syringe uptake.

Glaucoma procedures contribute a smaller absolute share but show the strongest 6.47%CAGR through 2031. Micro-invasive glaucoma surgery relies on precise viscoelastic delivery to protect angle structures, spurring formulary committees to stock specialized rheologies. Diagnostic screening programs detect disease earlier, expanding the addressable pool and nudging the ophthalmic viscosurgical devices market toward higher procedural diversity.

By End User: Hospitals Anchor Demand, ASCs Accelerate

Hospitals held 59.74% of ophthalmic viscosurgical devices market share in 2025 as they manage complex cases and pioneer premium viscoadaptive adoption. Central purchasing across multi-state networks safeguards supply continuity, reinforcing incumbent brands. Teaching hospitals also run comparative trials that shape regional formularies, indirectly steering market preferences.

ASCs record the fastest 8.06%CAGR to 2031, buoyed by a 15.41% year-on-year jump in Medicare payments in 2023. Their efficiency focus tilts product selection toward single-use packs that cut turnover time. Specialty clinics maintain a steady presence by serving premium or complex cohorts, and nascent office-based suites could spawn a micro-tier of compact viscoelastic syringes, adding nuance to the ophthalmic viscosurgical devices market.

Geography Analysis

North America represented 37.58% of the global ophthalmic viscosurgical devices market size in 2025, underpinned by robust reimbursement and dense ophthalmologist distribution. Medicare confirms cataract extraction as the top surgical episode in ASCs at roughly 19% of volume. Nearly 27.8% of U.S. adults aged 71+ report visual impairment, reinforcing surgical load. Bundled purchase agreements that link viscoelastic with phaco tips and IOL injectors are gaining traction, cementing supplier lock-in.

Asia-Pacific posts the highest 7.68%CAGR to 2031. Expanding health insurance in China and India drives cataract penetration, while provincial facilities transition to femtosecond platforms needing advanced viscoelastics. Surveys from Southwest China reveal a rising share of cataract patients with prior refractive surgery or high myopia. As reimbursement begins to acknowledge premium IOLs, dual-action viscoadaptives capture surgeon preference, lifting regional mix and directing incremental revenue into the ophthalmic viscosurgical devices market.

Europe sustains a sizable base yet faces tighter value-based procurement. Hospitals demand head-to-head endothelial cell-loss data before approving premium upgrades, favoring firms with strong clinical-evidence budgets. Regional societies advocate electronic instructions for use, aiming to cut intraocular lens packaging emissions by 67%. Early compliance with eco-qualified packaging may enhance tender scores and preserve share in the ophthalmic viscosurgical devices market.

Competitive Landscape

Roughly 65.0% of the ophthalmic viscosurgical devices market share resides with the five largest producers, led by Alcon, Johnson & Johnson, and Bausch + Lomb. Alcon’s 2025 capital-markets update pledged continued investment in next-generation viscoadaptives integrated into its micro-incision surgical packs. Bundled solutions raise switching costs for hospitals already using Alcon consoles.

Johnson & Johnson deepened its cataract ecosystem by launching TECNIS Odyssey IOLs in 2024, paired with clinical protocols that highlight reduced endothelial cell loss when implanted with company-branded viscoadaptives. Surgeon-support programs and real-world evidence solidify pull-through demand, reinforcing Johnson’s foothold in the ophthalmic viscosurgical devices market.

Bausch + Lomb sharpened differentiation by introducing ClearVisc and Totalvisc dual-action systems that blend hyaluronic acid with antioxidant sorbitol. SEC filings confirm a strategic shift toward ocular surface and surgical franchises. Niche players such as Seikagaku exploit proprietary hyaluronic-acid chains to preserve lubricity under high shear, retaining loyalty in Japan and selected export territories.

Ophthalmic Viscosurgical Devices Industry Leaders

Carl Zeiss Meditec AG

Bausch & Lomb Incorporated

Rayner Intraocular Lenses Limited

Alcon AG

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Alcon held a Capital Markets Day outlining fresh investment in next-generation viscoelastic formulations and digital surgery platforms. Two pipeline products were highlighted for late-2026 launch, indicating a bid to defend viscoadaptive share.

- September 2024: Johnson & Johnson expanded its TECNIS Odyssey presbyopia-correcting IOL portfolio in the United States, pairing the roll-out with guidance to use company-branded viscoadaptive OVDs.

- April 2023: Bausch + Lomb introduced the Totalvisc dual-action viscoelastic system, with early feedback citing smoother removal at the close of phaco procedures.

- May 2023: Bausch + Lomb launched the Totalvisc viscoelastic system, an ophthalmic viscosurgical device designed to enhance safety during cataract surgery by combining properties of both fluid and elastic viscoelastics and including sorbitol to combat oxidative damage in eye tissue.

Global Ophthalmic Viscosurgical Devices Market Report Scope

As per the scope of the report, ophthalmic viscosurgical devices are used in several ocular surgeries to guard the delicate ocular structure and to maintain space in the anterior chamber of an eye, leading to faster and safer surgery. These devices are composed of sodium hyaluronate, chondroitin sulfate, and hydroxypropyl methylcellulose. The market is segmented by type (cohesive, dispersive, and viscoadaptive), source (biological, animal, and semi-synthetic), application (glaucoma surgery, cataract surgery, corneal grafting, and other applications), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Cohesive |

| Dispersive |

| Viscoadaptive |

| Biological (Bacteria-Derived HA) |

| Animal (Rooster Comb, Porcine, Bovine) |

| Semi-Synthetic / Fermentation-Based |

| Cataract Surgery |

| Corneal Grafting / Keratoplasty |

| Other Applications |

| Hospitals |

| Specialty Ophthalmic Clinics |

| Ambulatory Surgery Centers (ASCs) |

| Other End-users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Cohesive | |

| Dispersive | ||

| Viscoadaptive | ||

| By Source | Biological (Bacteria-Derived HA) | |

| Animal (Rooster Comb, Porcine, Bovine) | ||

| Semi-Synthetic / Fermentation-Based | ||

| By Application | Cataract Surgery | |

| Corneal Grafting / Keratoplasty | ||

| Other Applications | ||

| By End User | Hospitals | |

| Specialty Ophthalmic Clinics | ||

| Ambulatory Surgery Centers (ASCs) | ||

| Other End-users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the ophthalmic viscosurgical devices market?

The ophthalmic viscosurgical devices market size stands at USD 489.62 million in 2026 and is projected to reach USD 668.95 million by 2031, reflecting a 6.44%CAGR.

Which product type holds the largest share in 2025?

Dispersive agents led the market with a 37.33% revenue share in 2025.

Which application area is growing fastest?

ASCs focus on high throughput; their preference for single-use, efficiency-oriented viscoelastic packs is driving an 8.06%CAGR in this channel.

How concentrated is the competitive landscape?

Approximately 65.0% of revenue is held by the top five players, yielding a market concentration score of 8 on a 10-point scale.

What regional market is expanding most rapidly?

Asia-Pacific is forecast to advance at a 7.68%CAGR, powered by expanding insurance coverage and rapid adoption of premium cataract platforms.

Page last updated on: